Surgical Gloves Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

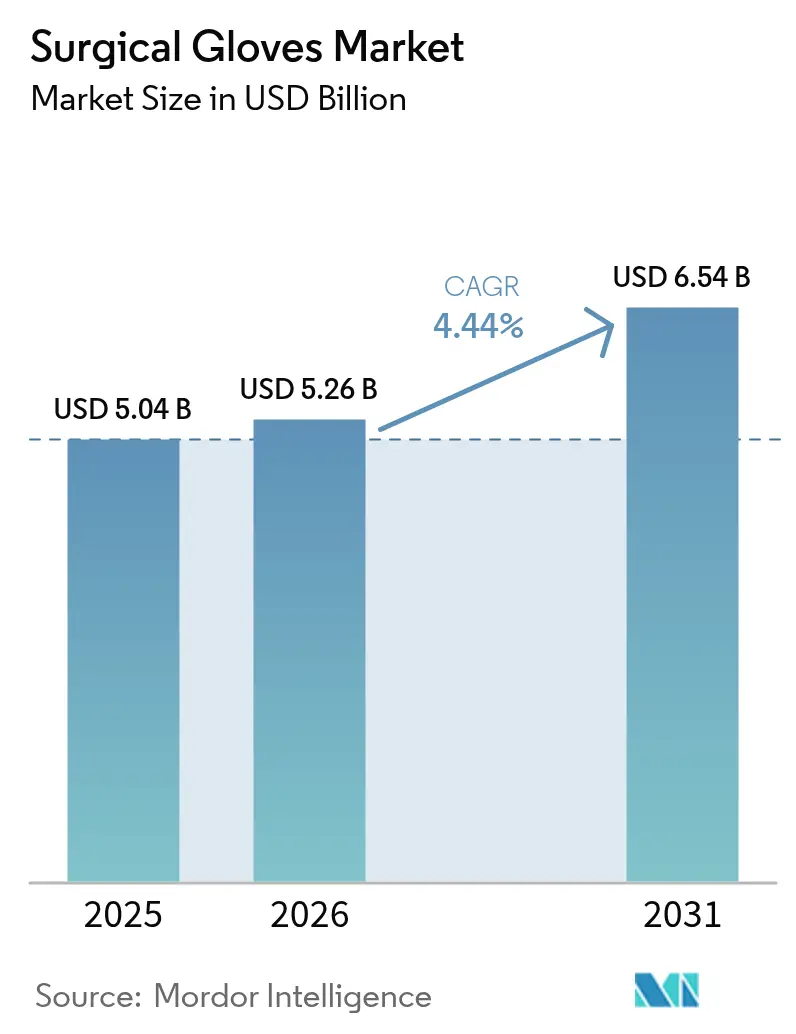

| Market Size (2026) | USD 5.26 Billion |

| Market Size (2031) | USD 6.54 Billion |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Gloves Market Analysis by Mordor Intelligence

The surgical gloves market size was valued at USD 5.04 billion in 2025 and estimated to grow from USD 5.26 billion in 2026 to reach USD 6.54 billion by 2031, at a CAGR of 4.44% during the forecast period (2026-2031). Stable growth rests on an aging world population that undergoes a rising volume of elective and trauma surgeries, an enduring post-pandemic focus on infection control, and continued product innovation that balances safety and tactile performance. North America remains the revenue anchor, but Asia-Pacific sets the growth pace on the back of rapid healthcare investment, wider insurance coverage, and expanding surgical volumes. Material trends pivot toward low-allergy polyisoprene, while form factors skew heavily to powder-free variants following global regulatory bans on powdered gloves. Hospitals will keep their purchasing clout, yet ambulatory surgical centers (ASCs) are creating new logistics and pricing pressures that favor suppliers with digital ordering portals and just-in-time delivery.

Key Report Takeaways

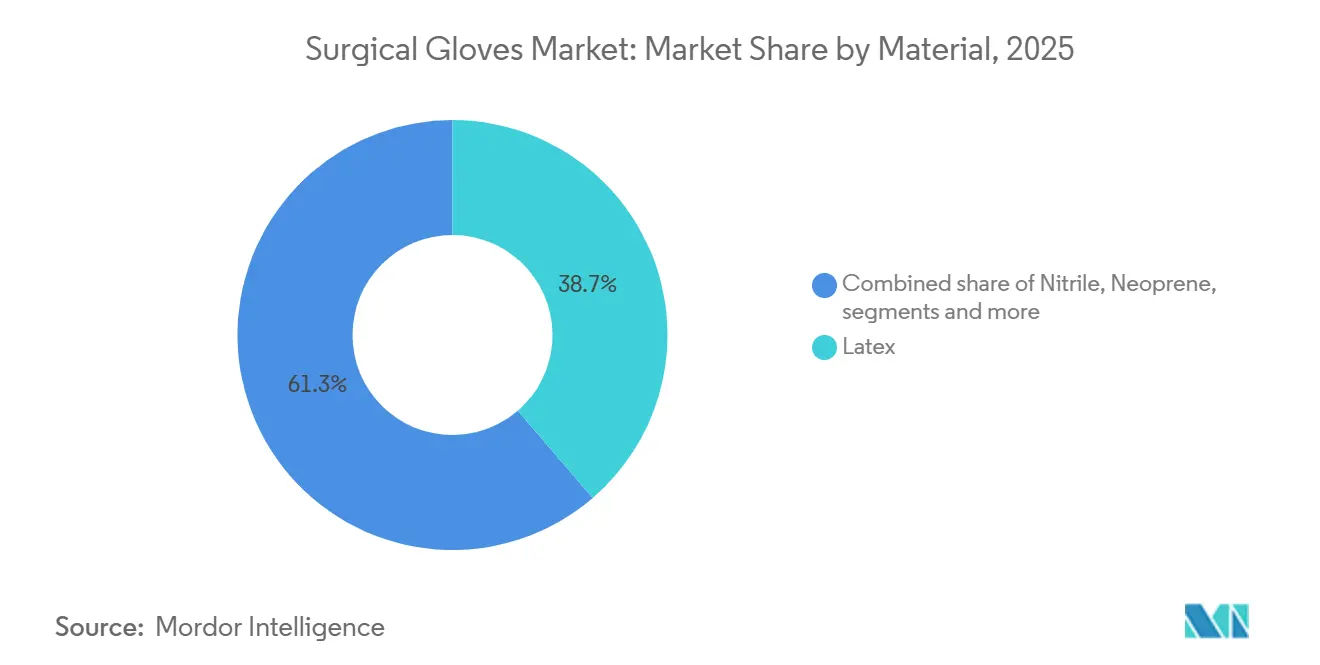

- By material - latex held 38.70% of surgical gloves market share in 2025; polyisoprene is projected to post the fastest 4.96% CAGR to 2031.

- By form - powder-free variants commanded 87.65% share of the surgical gloves market size in 2025 and are expanding at a 5.92% CAGR through 2031.

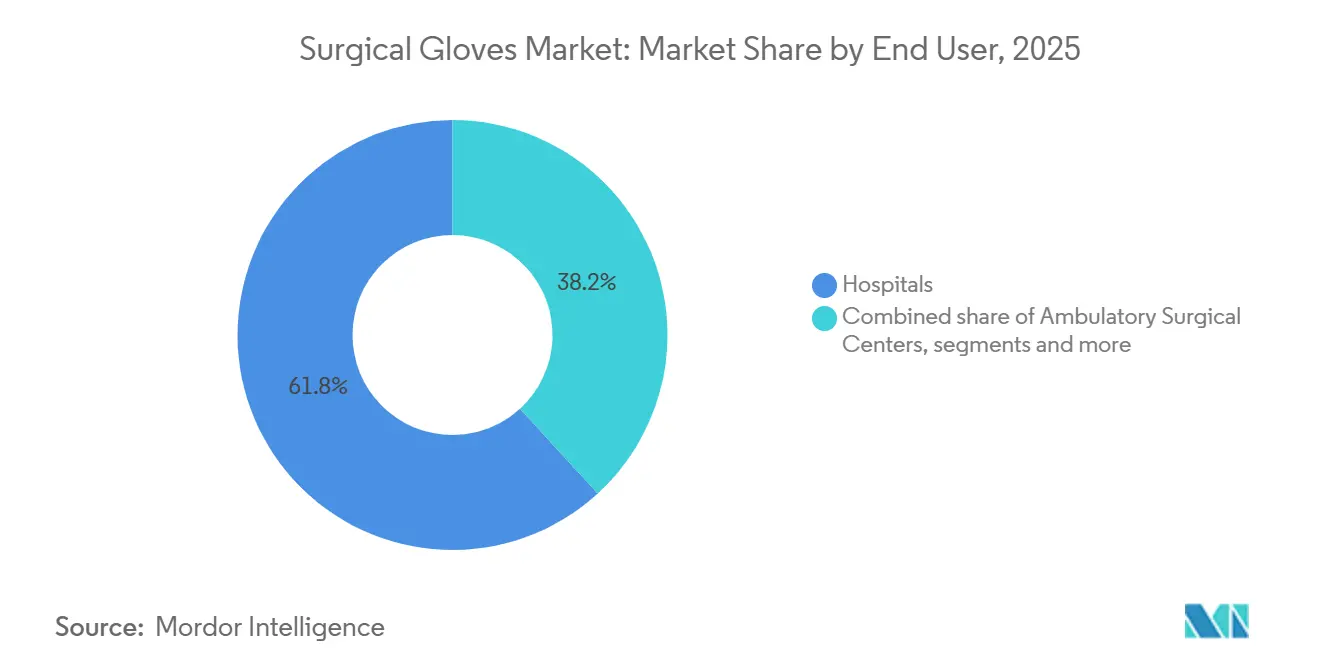

- By end user - hospitals accounted for 61.80% of the surgical gloves market size in 2025, while ASCs are advancing at a 5.41% CAGR to 2031.

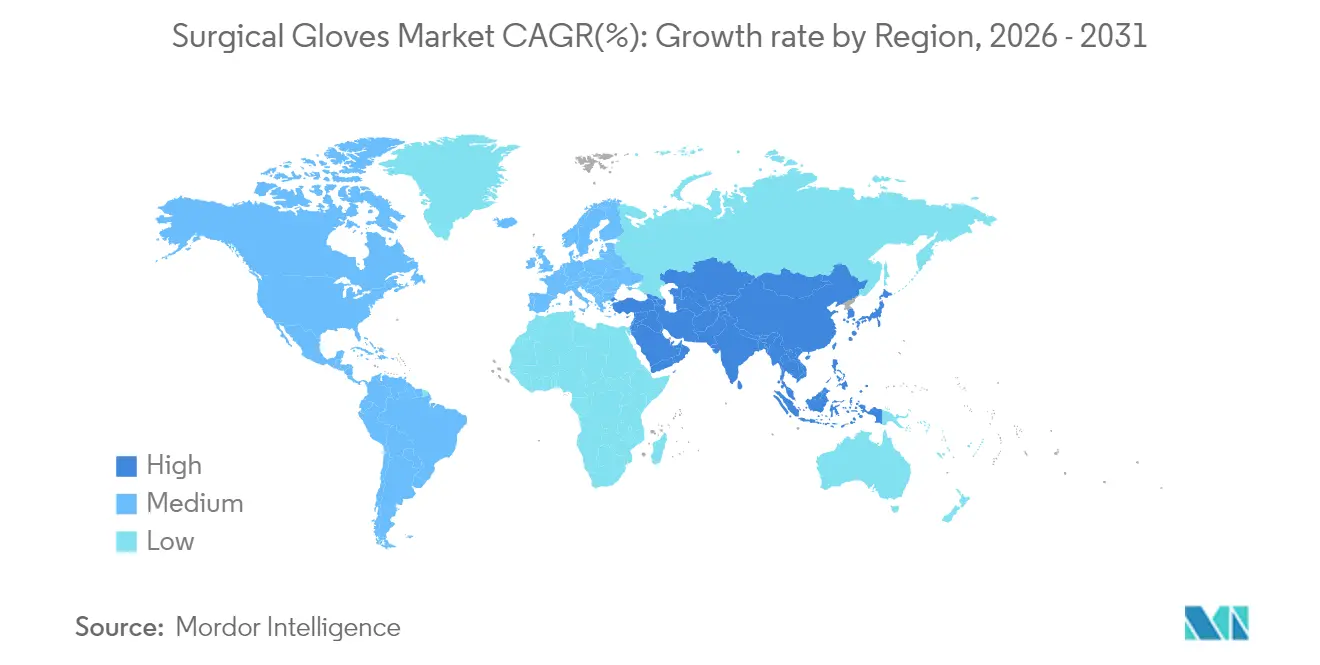

- By geography - North America led with 34.10% revenue share in 2025; Asia-Pacific is forecast to expand at a 5.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Gloves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in global surgical procedures | +1.2% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Stringent workplace safety mandates in emerging markets | +0.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Shift toward powder-free & accelerator-free chemistries | +0.6% | Global | Short term (≤ 2 years) |

| Adoption of e-commerce procurement by hospitals & ASCs | +0.4% | North America & EU | Medium term (2-4 years) |

| Blockchain-enabled provenance tracking for latex sourcing | +0.2% | Global, early adoption in North America | Long term (≥ 4 years) |

| Robotic surgery expansion driving demand for high-tactility gloves | +0.3% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Global Surgical Procedures

Elective, trauma, and outpatient surgeries continue to climb as life expectancy rises and minimally invasive techniques shorten recovery time. Sg2 projects that ASC procedure volume will expand 21% to hit 44 million cases by 2034, more than offsetting lower glove consumption per case than inpatient settings [1]Sg2, “Impact of Change Forecast 2024,” ascfocus.org. Orthopedic and spine operations dominate this wave, demanding gloves with high puncture resistance and tactile feedback. Despite tight global supplies, the Malaysian Rubber Glove Manufacturers Association (MARGMA) forecasts a shortfall of 80 billion pieces in 2024. Demand is set to reach 500 billion pieces, but installed capacity is only at 420 billion. This gap not only sustains pricing power but also encourages measured capacity additions, steering clear of speculative oversupply. Hospitals keep complex cases, preserving premium glove demand, while cost-sensitive ASCs lean toward bulk purchasing contracts that bundle high-usage items. Overall, the surgical gloves market benefits from volume growth even as unit cost pressure intensifies.

Stringent Workplace Safety Mandates in Emerging Markets

Governments from India to Indonesia are tightening personal protective equipment (PPE) rules that parallel European norms, making certified surgical gloves mandatory in operating theaters and high-risk industrial zones. The World Intellectual Property Organization (WIPO) records a 26.4% CAGR in occupational-health tech patents between 2018 and 2023, underscoring regulatory momentum. Enforcement is shifting from paper audits to digital monitoring, creating steady rather than sporadic glove demand. Domestic-content stipulations encourage local manufacturing, yet quality variances across plants necessitate strict supplier audits by global buyers.

Shift Toward Powder-Free & Accelerator-Free Chemistries

Polyisoprene and advanced nitrile formulations now mimic latex elasticity without protein allergens, but production complexity lifts factory conversion costs by up to 20%. A systematic review shows that double-gloving reduces inner-glove perforation rates by 80%, prompting hospitals to standardize thin, high-performance variants. The change accelerates innovation cycles and fattens demand for premium chemistries that command higher average selling prices.

Adoption of E-Commerce Procurement by Hospitals & ASCs

Supply chain shocks have pushed healthcare providers to cloud-based purchasing portals that support demand forecasting, automatic replenishment, and real-time pricing. Cardinal Health’s USD 340 million robotics-enabled distribution center in Fort Worth cuts order-to-ship time by 40–60% and illustrates the infrastructure underpinning e-commerce uptake. ASCs, operating with lean staff and limited storage, favor vendors that can guarantee small, frequent shipments. Suppliers that integrate inventory data with hospital ERP systems gain stickiness, reinforcing digital platform investment across the surgical gloves market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (NRL, nitrile) | -0.9% | Global, acute impact in APAC manufacturing hubs | Short term (≤ 2 years) |

| Latex allergy concerns & regulatory bans on powdered gloves | -0.5% | Global, concentrated in developed markets | Medium term (2-4 years) |

| ESG scrutiny on Southeast-Asian glove factories | -0.4% | APAC manufacturing hubs, global supply impact | Medium term (2-4 years) |

| Supply-chain concentration risk in Malaysia & Thailand | -0.3% | Global, originating from APAC manufacturing base | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Natural rubber latex (NRL) surged to a 13-year price high in October 2024 after heavy rains hammered Thai and Chinese plantations, squeezing margins for glove makers reliant on Southeast Asian supply. Simultaneous shortages of nitrile butadiene rubber in the United States prompted federal waivers for foreign sourcing until at least late 2025. Producers pass some costs to buyers, yet long-term contracts cap price flexibility, pressuring EBITDA margins. Diversifying into guayule or Scorzonera tau-saghyz remains at pilot scale, leaving the surgical gloves market exposed to commodity swings.

Latex Allergy Concerns & Regulatory Bans

Healthcare worker sensitization rates of 8–12% keep pressure on hospitals to minimize latex exposure. Clinical evidence shows latex-free gloves incur 4.24-times higher perforation risk, creating a procurement trade-off between allergy avoidance and barrier integrity. The rupture risk drives demand for premium polyisoprene, priced 15–20% above conventional latex. Manufacturers must run parallel production lines to serve diverging customer preferences, adding capital overhead and operational complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Polyisoprene Innovation Drives Premium Segment

The surgical gloves market have latex occupying 38.70% of surgical gloves market share on the strength of low cost and proven performance. Yet hospitals are migrating toward latex-free operating rooms, propelling polyisoprene to a 4.96% CAGR through 2031. Molecular-dynamics studies peg polyisoprene’s glass-transition temperature at 204.2 K, balancing flexibility and tear resistance—traits valued in microsurgery. Manufacturers add antioxidant packages to curb discoloration, and accelerator-free curing lowers Type IV allergy risk. Nitrile keeps traction in examination settings, while neoprene fills chemical-resistant niches such as oncology compounding. Sustainable sourcing is gaining ground; Top Glove’s BioGreen nitrile gloves biodegrade under anaerobic landfill conditions, aligning with hospital waste-reduction mandates .

In procurement bids, buyers now score materials on a weighted matrix of allergenicity, tactile response, environmental footprint, and price. This shift favors vertically integrated suppliers that control latex tapping, compounding, and finished-goods molding because they can adjust formulations quickly. Regional contract awards in India and Indonesia increasingly require localized raw-rubber content, nudging multinationals to joint ventures or toll-manufacturing deals. The resulting tactical alliances will shape capacity additions over the next cycle in the surgical gloves market.

By Form: Powder-Free Dominance Accelerates

Powder-free variants captured 87.65% share of the surgical gloves market size in 2025 after powder ban mandates swept across major economies. Surface-coating chemistries such as polyurethanes or chlorination now give gloves a silky feel that speeds donning without cornstarch, while micro-texturing boosts grip in wet fields. Capital expenditure to retrofit production lines can reach USD 20 million per plant, erecting barriers that have quickened consolidation as smaller Asian manufacturers exit. Buyers benefit from reduced granuloma risk and lower intra-operative particle counts, which translate into shorter surgical times and fewer post-operative infections.

Conversely, remaining powdered glove users cluster in small industrial segments where surgical-grade sterility is unnecessary, but even these markets face imminent restrictions as occupational-safety regulations tighten. Automation technologies, such as Ansell’s DERMASHIELD spray-on polymers, accelerate throughput and shrink defect rates, improving plant OEE to the mid-80% range. Such efficiency gains blunt the cost penalty historically associated with powder-free processing, allowing suppliers to defend margins amid rising energy and labor expenses.

By End User: ASCs Drive Structural Market Shift

Hospitals consumed 61.80% of surgical gloves market size in 2025, but the compound effect of payer incentives and physician ownership structures is redirecting simpler procedures to ASCs, which are growing at a 5.41% CAGR. ASCs standardize trays and pursue vendor consolidation, favoring suppliers that can bundle gloves with drapes, gowns, and antiseptics under a single-source contract. They also require digital dashboards that reconcile case costing with supply usage in near-real time, pushing glove makers to integrate EDI and bar-code serialization.

The hospital channel still dominates revenue thanks to longer procedure times and higher glove changes, especially in transplant and cardiothoracic specialties. Teaching facilities increasingly adopt double-gloving for resident training, lifting per-procedure utilization. Over in primary-care clinics, demand holds steady, but margin pressure remains acute as reimbursement cuts persist. Dental and veterinary offices offer modest niche growth driven by infection-control accreditation requirements. Collectively, these patterns underscore the need for segmented sales strategies within the larger surgical gloves market.

Geography Analysis

North America generated 34.10% of global revenue in 2025 and remains the procurement standard-setter due to a mature hospital network, robust infection-control guidelines, and group-purchasing organizations that mandate ASTM compliance. U.S. federal agencies alone ordered 55.5 million boxes of nitrile gloves in 2025 as part of domestic-stockpile programs. Tariff pressures and geopolitical risk from China have revived interest in near-shoring to Mexico and Puerto Rico. To fortify resilience, Cardinal Health invested USD 340 million in an automation-heavy distribution hub that supports one-day delivery to 80% of U.S. surgical sites.

Asia-Pacific is advancing at a 5.26% CAGR through 2031, reflecting rising surgical infrastructure and the region’s dual identity as both supply base and demand center. Malaysia and Thailand produce roughly two-thirds of the world’s surgical gloves, yet Thai research flags persistent labor shortages and climate-change exposure that could disrupt latex tapping seasons . China’s elective-surgery rebound post-zero-COVID adds a substantial incremental volume, while India’s Ayushman Bharat insurance scheme continues to unlock latent demand in tier-2 cities. Local content rules in Indonesia and Vietnam encourage foreign brands to build or partner in-country, altering the competitive map of the surgical gloves market.

Europe maintains stable mid-single-digit growth, driven by sustainability regulations and a push for circular-economy compliance. Mölnlycke’s EUR 50 million Malaysian plant includes biomass boilers and solar rooftops to satisfy EU carbon-footprint reduction targets. The bloc’s EcoDesign directive will likely require material passports, amplifying interest in blockchain traceability. South America and the Middle East & Africa trail but offer long-run potential once macroeconomic volatility settles; Brazil’s new PPP program for hospital upgrades and Saudi Arabia’s Vision 2030 private-hospital wave represent catalysts, albeit from a low base. Logistics bottlenecks and currency swings remain obstacles that suppliers must price into long-term contracts.

Competitive Landscape

The competitive landscape is moderately concentrated, featuring several dominant manufacturers. In Q1 FY2025, Top Glove experienced a significant revenue increase, swinging its net profit back to positive territory. This rebound, fueled by normalized demand and enhanced utilization rates, is reshaping share positions in the surgical gloves market.

Technology is emerging as a pivotal differentiator. Meanwhile, experimental haptic-feedback gloves for VR surgical training suggest potential new revenue avenues. In a nod to food-traceability initiatives, Mayo Clinic and a consortium of Midwest suppliers are piloting blockchain projects to verify the origins of latex. Proponents of these systems anticipate lower recall costs and improved ESG ratings.

As demand stabilizes, capacity rationalization is in full swing. Kossan Rubber's investment in robotics for stripping lines has reduced labor requirements by 1,000 gloves per shift. Meanwhile, smaller, less automated plants in Malaysia and Thailand have either shut down or shifted focus to domestic industrial-glove production. Leveraging their financial strength, larger manufacturers are securing long-term contracts for butadiene and latex, shielding themselves from raw material price fluctuations. In Europe and North America, sustainability credentials, whether through EcoVadis ratings or commitments to science-based targets, are increasingly crucial in tender awards.

Surgical Gloves Industry Leaders

Ansell Limited

Top Glove Corporation Bhd

Hartalega Holdings Berhad

Kossan Rubber Industries Bhd

Cardinal Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: U.S. Medical Glove Company (USMGC), the sole American manufacturer of machinery, chemicals, and materials for nitrile and polyisoprene gloves, announced the execution of a master lease for a 638,000 square-foot manufacturing facility in Ohio, managed by CAI Investments LLC. This strategic development represents the final phase of USMGC's initiative to establish a fully American-made supply chain for medical and surgical gloves, eliminating reliance on China or other foreign suppliers.

- May 2025: Ansell entered a national group purchasing agreement in the Surgeons' Gloves category with Premier, Inc. This agreement empowers Premier members to opt for exclusive pricing and terms, pre-negotiated by Premier, on Ansell’s Surgeons' Gloves portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the surgical gloves market as all sterile, single-use gloves specifically certified for invasive surgical procedures, regardless of material (latex, nitrile, neoprene, polyisoprene, or blends) and distributed through institutional or retail channels to hospitals, ambulatory surgery centers, and specialty clinics.

Scope Exclusion: Examination, clean-room, and industrial gloves fall outside this scope, as do reusable textile or polymer sleeves.

Segmentation Overview

- By Material

- Latex

- Nitrile

- Neoprene

- Polyisoprene

- Others (Vinyl and Synthetic blends, among others)

- By Form

- Powdered

- Powder-free

- By End-user

- Hospitals

- Ambulatory Surgical Centers

- Clinics & Physician Offices

- Dental & Veterinary Facilities

- Others (Emergency Centers, among others)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed material scientists, theater nursing supervisors, infection-control officers, and procurement heads across North America, Europe, and Asia Pacific. These conversations validated powder-free penetration rates, typical price premiums by polymer, and post-COVID inventory norms, filling gaps left by secondary data.

Desk Research

Our analysts first mapped the demand pool using open datasets such as WHO Surgical Procedures Volumes, UN Comtrade sterile glove trade codes, U.S. FDA 510(k) device listings, and EU EUDAMED recall notices. Complementary signals were gathered from sources such as the American Hospital Association annual survey, NHS England theater activity statistics, and peer-reviewed papers in the Journal of Hospital Infection. To cross-check company positioning, we drew selectively on D&B Hoovers and Dow Jones Factiva, while import volumes were benchmarked with Volza shipment data. The sources cited illustrate our evidence base; many other public records and specialist databases were consulted to complete fact-finding and sanity checks.

Market-Sizing & Forecasting

A top-down model scales global surgical procedure counts by average glove pairs per surgery and post-operative change rates, then applies country-level adoption and wastage multipliers before conversion with regional average selling prices. Bottom-up supplier shipment samples and channel checks are used to test and tune totals. Key model drivers include elective surgery backlog clearance, regulatory powder bans, raw latex index prices, and material-mix shifts toward nitrile. Forecasts through 2030 rely on multivariate regression blending procedure growth, healthcare spending elasticity, and polymer cost trends; expert consensus guides scenario bounds. Where bottom-up evidence is thin, conservative buffers are introduced and highlighted for review.

Data Validation & Update Cycle

Outputs pass a two-step anomaly screen versus historical ratios and trade flows, followed by senior analyst review. Models refresh each year, with interim edits triggered by price shocks, major recalls, or guideline changes; a final pre-publication sweep ensures clients receive the most current view.

Why Mordor's Surgical Gloves Baseline Earns Buyer Confidence

Published estimates often diverge because firms vary in product scope, procedure multipliers, price assumptions, and refresh timing.

Key gap drivers include whether double-gloving is counted, the treatment of powdered legacy stock, and if post-pandemic demand normalization is fully recognized, which are then reconciled transparently in Mordor Intelligence's framework.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.04 B | Mordor Intelligence | - |

| USD 1.0 B | Regional Consultancy A | Excludes double-gloving and uses 2024 ASPs without inflation adjustment |

| USD 3.73 B | Industry Association B | Omits ambulatory centers and applies flat polymer pricing across regions |

The comparison shows that when surgical setting breadth, current ASP tracking, and procedure-pair factors are consistently applied, Mordor's balanced baseline emerges as the most dependable reference for strategic planning.

Key Questions Answered in the Report

What is the current size of the surgical gloves market?

The Surgical Gloves Market size is expected to reach USD 5.26 billion in 2026 and grow at a CAGR of 4.44% to reach USD 6.54 billion by 2031.

Which material segment is growing fastest?

Polyisoprene gloves are growing quickest at a 4.96% CAGR because they match latex feel without protein allergens.

Why are powder-free gloves dominant now?

Regulatory bans on powdered gloves and hospital infection-control protocols have pushed powder-free variants to 87.65% market share in 2025.

How are ambulatory surgical centers affecting demand?

ASCs shift routine surgeries out of hospitals, expanding glove volume while emphasizing cost-efficient digital procurement and standardized products.

What risks threaten surgical glove supply?

Price spikes in natural rubber latex and nitrile feedstocks, plus geographic concentration of plantations in Southeast Asia, create ongoing supply-chain vulnerability.

Page last updated on: