Fecal Incontinence Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

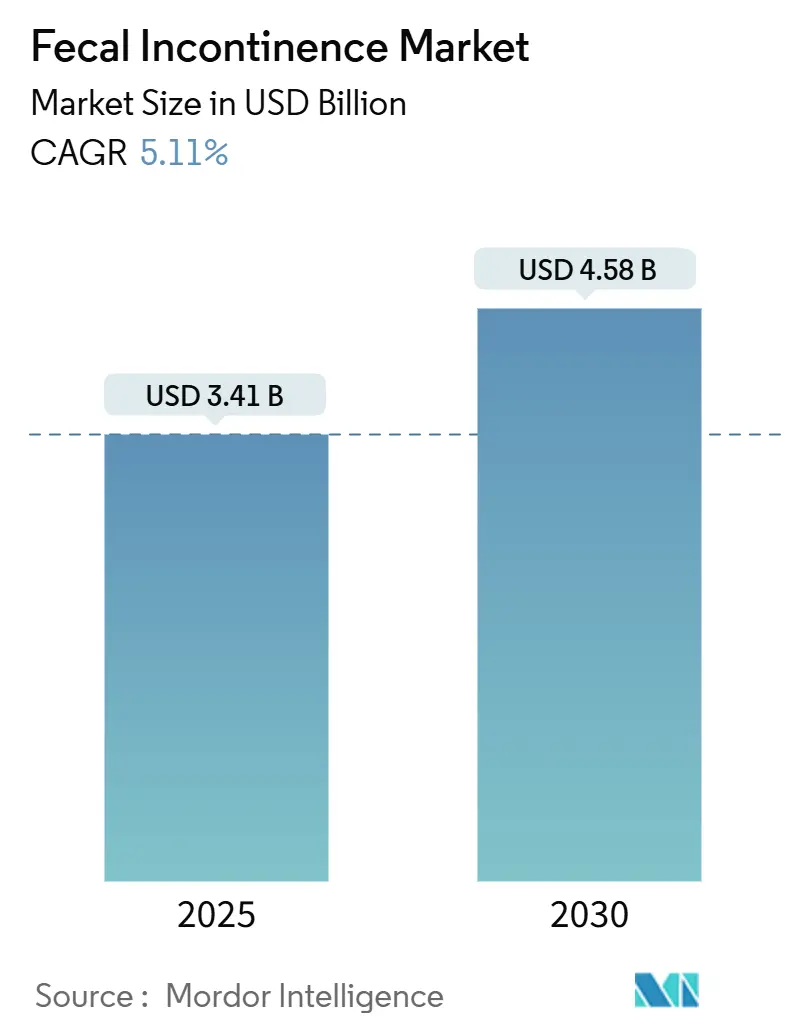

| Market Size (2025) | USD 3.41 Billion |

| Market Size (2030) | USD 4.58 Billion |

| Growth Rate (2025 - 2030) | 5.11% CAGR |

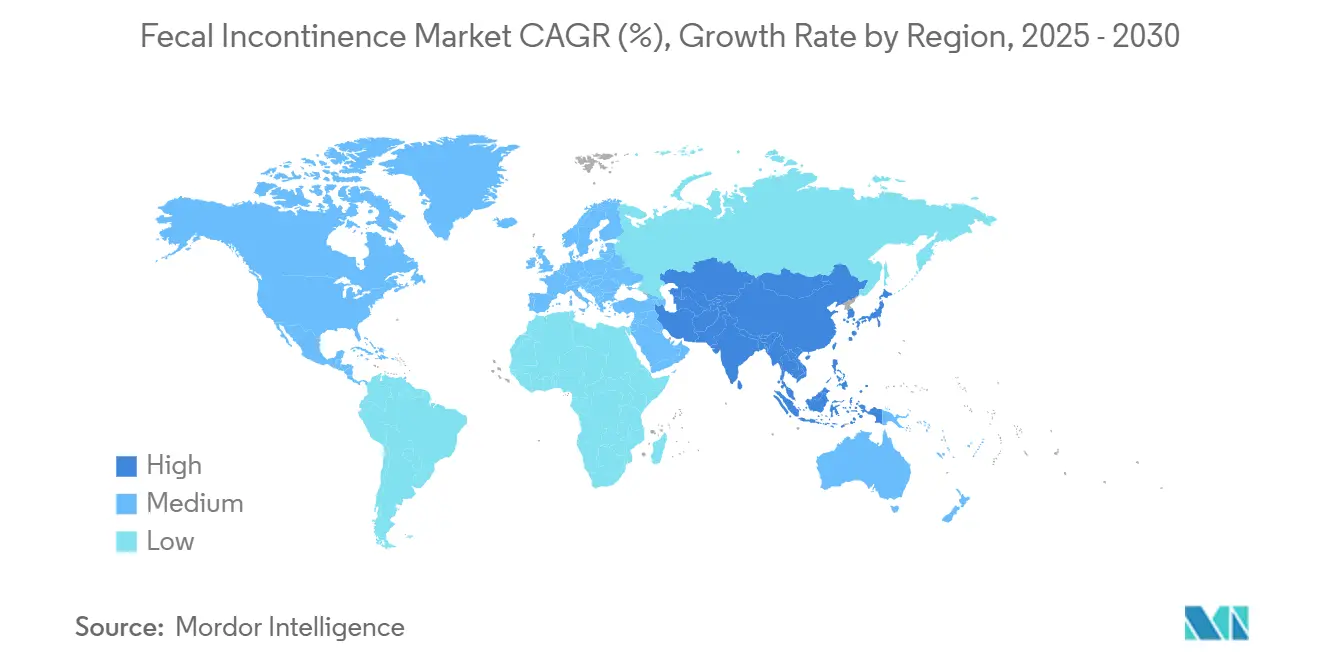

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fecal Incontinence Market Analysis by Mordor Intelligence

The fecal incontinence market size stands at USD 3.41 billion in 2025 and is projected to reach USD 4.38 billion by 2030, registering a 5.11% CAGR over the forecast period. Demographic aging, rising prevalence of chronic gastrointestinal conditions, and growing acceptance of minimally-invasive neuromodulation systems underpin this steady expansion. Manufacturers are consolidating to secure technology leadership, as illustrated by Boston Scientific’s USD 3.7 billion purchase of Axonics, which reinforces the attractiveness of sacral neuromodulation assets. Regional momentum differs markedly: North America retains dominance due to favorable reimbursement pathways, while Asia-Pacific is gaining traction from rapid healthcare infrastructure upgrades and targeted awareness campaigns. Social stigma and the high upfront cost of advanced implants continue to impede patient access, yet digital health solutions that enable discreet home-based therapy are beginning to lower those barriers. Intensifying intellectual-property litigation signals a competitive shift toward differentiated platforms and bundled digital services that enhance clinical outcomes.

Key Report Takeaways

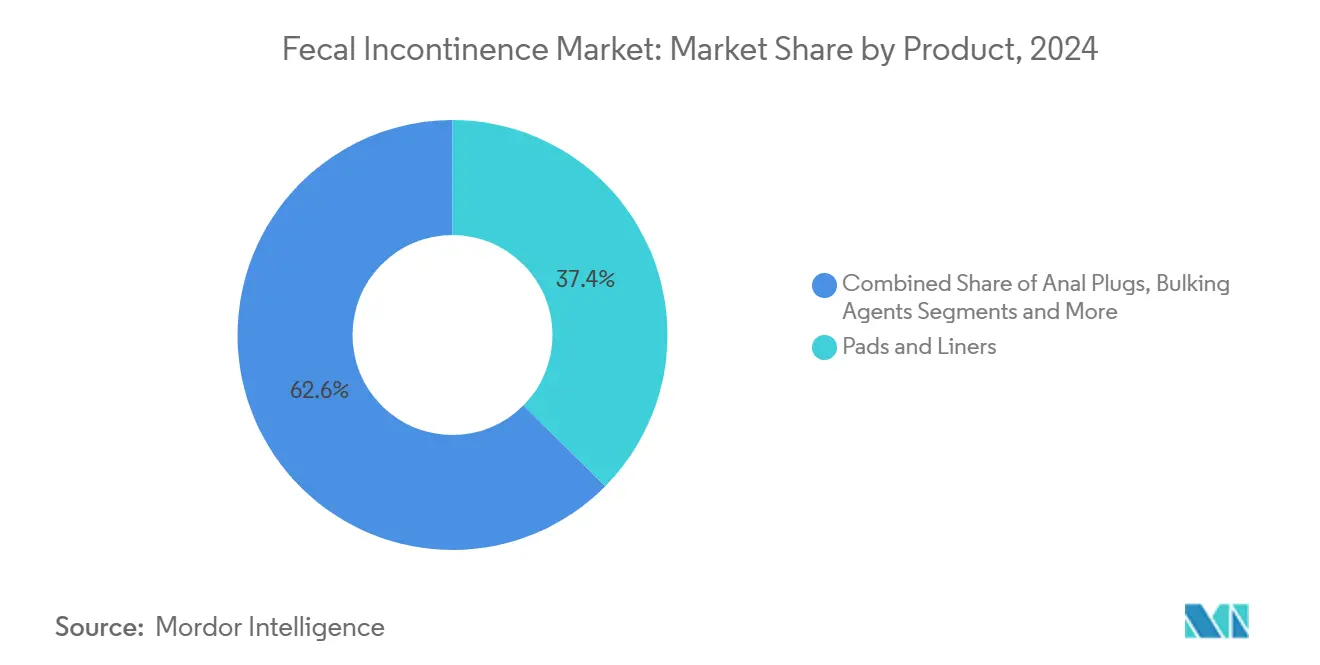

- By product category, pads and liners led with a 37.42% share of the fecal incontinence market in 2024, while sacral nerve stimulation implants are forecast to expand at a 9.31% CAGR through 2030.

- By patient type, adult patients held 84.65% of the fecal incontinence market share in 2024; the pediatric cohort is projected to record the fastest 8.35% CAGR to 2030.

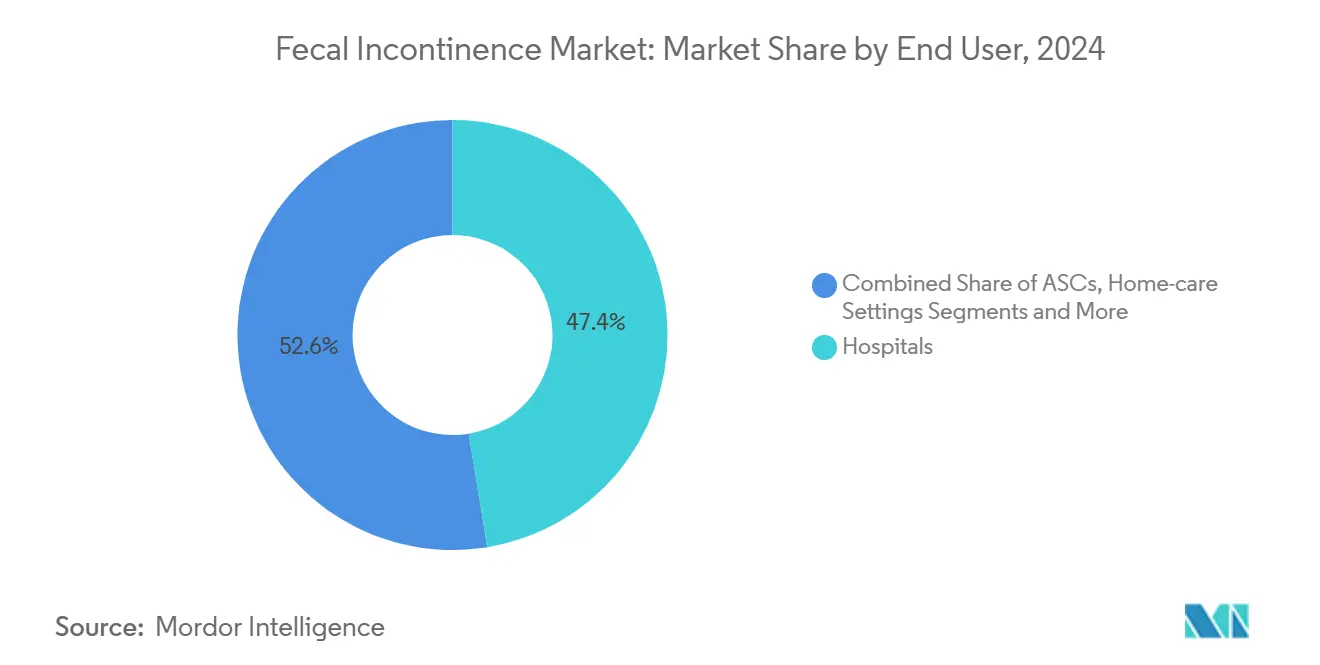

- By end user, hospitals accounted for 47.41% of the fecal incontinence market size in 2024, whereas home-care settings are advancing at a 7.54% CAGR through 2030.

- By geography, North America commanded 41.23% of the fecal incontinence market in 2024, whereas Asia-Pacific represents the quickest-growing region at 7.63% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fecal Incontinence Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly Aging Global Population | +1.8% | Global, with concentration in North America, Europe, and Japan | Long term (≥ 4 years) |

| Rising Prevalence Of Chronic GI Disorders | +1.2% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Growing Adoption Of Minimally-Invasive Bowel Management Devices | +0.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Favourable Reimbursement For Sacral Neuromodulation | +0.7% | North America, select EU markets | Short term (≤ 2 years) |

| AI-Enabled Biofeedback Therapy Platforms | +0.4% | North America, EU, with APAC adoption | Medium term (2-4 years) |

| Expansion Of Pelvic-Floor Neuromodulation Clinics In Emerging Markets | +0.3% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapidly aging global population

Adults aged 65 and older exhibit a 15% fecal-incontinence prevalence compared with 8% among all adults, expanding the addressable base as longevity rises.[1]Mayo Clinic, “Examining the Prevalence of FI and Its Relationship With Age, Sex and Geographic Location in Adults,” Mayo Clinic, mayoclinic.org Annual economic burden per patient averages USD 4,110, split between direct care costs and productivity losses, escalating pressure on payers.[2]Anne-Marie Leroi et al., “Outcome and Cost Analysis of Sacral Nerve Modulation for Treating Urinary and/or Fecal Incontinence,” Annals of Surgery, lww.com Nursing-home prevalence of 50–70% drives institutional demand for advanced bowel-management systems. Age-related comorbidities such as diabetes and neurological disorders further elevate risk. Long-term care providers increasingly view advanced containment and neuromodulation solutions as cost-effective given the staffing efficiencies they create. Consequently, the fecal incontinence market is tightly coupled to aging trends in high-income economies.

Rising prevalence of chronic GI disorders

Inflammatory bowel disease patients report 54% fecal-incontinence incidence, far exceeding population baselines and underscoring unmet therapeutic needs. Irritable bowel syndrome carries a 52% lifetime incidence, amplifying demand for structured management pathways. Psychological distress linked to uncontrolled symptoms accelerates help-seeking behavior, with 56% of respondents in recent surveys prioritizing fatigue and continence control. Post-surgical complications, especially after rectal-cancer resections, introduce additional patient pools that require devices such as transanal irrigation kits and neuromodulation implants. Together these factors sustain double-digit growth pockets within the broader fecal incontinence market.

Growing adoption of minimally-invasive bowel-management devices

MRI-compatible sacral neuromodulation systems now deliver 93.2% patient-reported symptom improvement while removing imaging restrictions that once limited eligibility.[3]Katuwal B. et al., “Outcomes and Efficacy of MRI-Compatible Sacral Nerve Stimulator,” World Journal of Radiology, wjgnet.com High-intensity focused electromagnetic therapy achieves 95% quality-of-life gains in only five sessions, attracting time-constrained patients. AI-driven biofeedback platforms administered at home have demonstrated statistically significant reductions in incontinence episodes. As convenience converges with efficacy, patients and clinicians migrate toward less invasive options, propelling unit sales of advanced implants and digital therapeutics throughout the fecal incontinence market.

Favorable reimbursement for sacral neuromodulation

Medicare, UnitedHealthcare, and other major payers now reimburse sacral-neuromodulation procedures once conservative treatments fail and a ≥50% symptom reduction is documented during trial stimulation. Economic modeling reveals favorable cost-effectiveness ratios over 24 months, strengthening coverage justifications. New CPT and HCPCS codes simplify billing, accelerating provider adoption. Coverage is incrementally widening to include posterior tibial nerve stimulation and modular bowel-management systems, lowering financial barriers for qualified patients and enlarging the fecal incontinence market size.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social Stigma & Under-Reporting Of The Condition | -1.4% | Global, with cultural variations | Long term (≥ 4 years) |

| High Cost Of Advanced Implants & Procedures | -0.8% | Emerging markets, uninsured populations | Medium term (2-4 years) |

| Fragmented Regulatory Pathways For Bio-Absorbable Bulking Agents | -0.5% | Global, with regional variations | Short term (≤ 2 years) |

| Shortage Of Colorectal Specialists Trained In Latest Therapies | -0.6% | Global, acute in rural and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Social stigma and under-reporting

Only 23% of patients accurately disclose fecal-incontinence episodes during clinical encounters, highlighting a substantial recognition gap. Cultural norms frame the condition as an inevitable result of aging or childbirth, discouraging proactive care seeking. Clinicians seldom initiate dialogue, missing early intervention windows. Advocacy groups and peer-support platforms have begun public-awareness campaigns, yet behavior change remains gradual. Digital therapeutics that allow discreet home treatment lessen embarrassment, but stigma continues to constrain the fecal incontinence market.

High cost of advanced implants and procedures

Sacral-neuromodulation implantation can exceed USD 10,000 in out-of-pocket costs for uninsured patients, limiting uptake in lower-income segments. Battery replacements and revision surgeries add lifetime expenses that deter adoption, particularly in emerging economies with constrained reimbursement. Hospitals in cost-sensitive markets prioritize absorbent products over capital-intensive devices, dampening market penetration. Manufacturers are responding with value-based pricing and modular platforms, but economic hurdles still weigh on the global fecal incontinence market size.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Neuromodulation Accelerates Growth

Pads and liners generated the largest revenue slice, holding 37.42% of the fecal incontinence market in 2024. Device familiarity, wide retail distribution, and immediate symptom containment sustain their prominence. In contrast, sacral-nerve-stimulation implants are the fastest-growing category, advancing at a 9.31% CAGR as payers widen coverage and clinical data consolidate their superiority in durable continence restoration. The fecal incontinence market size for neuromodulation products is set to widen further as manufacturers introduce MRI-safe generators and longer-lasting batteries. Emerging bowel-management systems that integrate sensors with closed drainage have cut nursing time by 59%, improving hospital efficiency. Biofeedback equipment is enjoying a digital renaissance, with cloud-linked platforms enabling remote coaching and adherence tracking. Bulking agents remain confined by regulatory complexity, whereas anal plugs serve niche postoperative applications.

Demand for advanced products is being catalyzed by the Boston Scientific–Axonics merger, which consolidates IP portfolios, enhances distribution reach, and funds pipeline expansions. Competitive differentiation now revolves around device miniaturization, battery longevity, and software ecosystems that capture real-world evidence. Taken together, these dynamics reinforce neuromodulation as the innovation engine within the fecal incontinence market.

By Patient Type: Pediatric Opportunity Emerges

Adult patients accounted for 84.65% of the fecal incontinence market in 2024, reflecting higher age-related prevalence and established reimbursement pathways. However, pediatric adoption is accelerating at an 8.35% CAGR as awareness of childhood bowel dysfunction rises and purpose-built devices such as the Indepenema enable self-administration of enemas. The fecal incontinence market share of pediatric solutions is expected to climb steadily as clinical trials validate sacral-neuromodulation efficacy in adolescents and non-invasive pelvic-floor magnetic stimulation demonstrates favorable safety profiles. Family-centered care models, digital education resources, and school-based screening programs further support volume growth.

Pediatric treatment regimes increasingly combine anorectal manometry diagnostics with personalized therapy algorithms, improving response prediction and caregiver confidence. Manufacturers are tailoring catheter sizes, user interfaces, and training materials to pediatric needs, underscoring this segment’s strategic relevance to the fecal incontinence industry.

By End User: Home-Care Transformation

Hospitals generated 47.41% of the fecal incontinence market size in 2024 by serving as the primary diagnostic and intervention hubs for complex cases. Yet home-care settings exhibit the strongest 7.54% CAGR as patients seek privacy and convenience. FDA-cleared home biofeedback devices now guide pelvic-floor exercise regimens with remote clinician oversight, bridging the gap between outpatient follow-up and daily-life adherence. Smart diaper sensors such as the MONIT platform cut dermatitis incidence by facilitating timely changes, validating technology’s role in domiciliary settings.

Ambulatory surgical centers are capturing sacral-neuromodulation implantation volume thanks to streamlined workflows and lower overhead. Long-term care facilities, where fecal-incontinence prevalence reaches 70%, are adopting comprehensive bowel-management programs that integrate advanced containment systems and staff training. Collectively, these shifts toward decentralized care models expand therapeutic touchpoints and drive sustained momentum within the fecal incontinence market.

Geography Analysis

North America retained a 41.23% fecal incontinence market share in 2024, supported by mature reimbursement systems, high procedure volumes, and ongoing NIH-funded neuromodulation research. Payer pilots such as Mass General Brigham Health Plan’s pelvic-health initiative bundle sensor-enabled products with virtual coaching, enhancing patient engagement and reducing downstream costs.

Europe represents a mature and highly structured landscape. Germany, the United Kingdom, and France spearhead adoption through specialized pelvic-floor rehabilitation centers and coordinated care networks. Harmonized EU regulatory pathways expedite device approvals, although pricing pressures encourage adoption of cost-effectiveness frameworks. Multicenter clinical trials evaluating transanal irrigation for low anterior resection syndrome continue to fine-tune patient-selection criteria, supporting sustainable growth across the region.

Asia-Pacific is the fastest-growing territory, expanding at 7.63% CAGR on the back of rising health-care expenditure and improved awareness campaigns. Cross-sectional surveys in China reveal elevated pelvic-floor dysfunction prevalence coupled with limited public literacy, highlighting education as a key growth lever. Thailand’s urogynecology associations are scaling professional-training programs that integrate Western and traditional modalities, enlarging the physician talent pool. Japan’s super-aged demographic and robust insurance coverage underpin early adoption of premium devices, while emerging economies leverage medical tourism to access advanced treatments. These developments collectively diversify revenue streams and amplify the global fecal incontinence market.

Competitive Landscape

The fecal incontinence market is moderately consolidated around neuromodulation platforms, with Boston Scientific’s acquisition of Axonics in 2024 marking the sector’s largest deal and signaling a strategic pivot toward integrated implant–software ecosystems. Medtronic defends a significant installed base exceeding 375,000 patients through continuous innovation and aggressive patent enforcement.

Coloplast differentiates via digital health integration, launching the first leakage-notification system for stoma users in 2024 to enhance patient quality of life and support remote monitoring. Emerging entrants like Minnesota Medical Technologies are targeting niche indications with user-friendly silicone inserts, broadening therapeutic choice sets. Venture funding gravitates toward AI-enabled biofeedback startups that promise data-driven personalization and lower barriers to adoption.

Strategic priorities across leading firms now emphasize battery longevity, MRI compatibility, and cloud-connected analytics. Intellectual-property disputes intensify as incumbents seek to protect key differentiators. Partnerships with academic centers accelerate evidence generation, while regional distributors extend reach into high-growth markets. These dynamics ensure that technological innovation remains central to competitive positioning within the fecal incontinence market.

Fecal Incontinence Industry Leaders

Medtronic plc

Coloplast A/S

Boston Scientific Corporation

Axonics Inc.

Hollister Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Minnesota Medical Technologies obtained FDA 510(k) clearance for its StaySure disposable silicone insert designed for day-long comfort in managing fecal incontinence.

- October 2024: UCI Health initiated a phase 3 trial of stem-cell-derived therapy iltamiocel targeting obstetric injury–related bowel incontinence.

- July 2024: Coloplast unveiled one of the world’s first digital leakage-notification systems for stoma patients, integrating real-time alerts to reduce complications.

Global Fecal Incontinence Market Report Scope

| Pads & Liners |

| Bowel Management Systems |

| Anal Plugs |

| Bulking Agents |

| Sacral Nerve Stimulation Implants |

| Biofeedback Equipment |

| Adult |

| Paediatric |

| Hospitals |

| Ambulatory Surgical Centres |

| Home-care Settings |

| Long-term Care Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Pads & Liners | |

| Bowel Management Systems | ||

| Anal Plugs | ||

| Bulking Agents | ||

| Sacral Nerve Stimulation Implants | ||

| Biofeedback Equipment | ||

| By Patient Type | Adult | |

| Paediatric | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Home-care Settings | ||

| Long-term Care Facilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the fecal incontinence market by 2030?

The fecal incontinence market is forecast to reach USD 4.38 billion by 2030.

Which product segment is growing the fastest?

Sacral-nerve-stimulation implants are expanding at a 9.31% CAGR through 2030.

Which region is showing the quickest growth?

Asia-Pacific is advancing at a 7.63% CAGR through 2030 due to healthcare-infrastructure upgrades and rising awareness.

How large is the adult patient share?

Adult patients represent 84.65% of current market revenue.

What drives the shift toward home-care settings?

Discreet digital therapeutics and FDA-cleared home biofeedback devices are enabling 7.54% CAGR growth in home-care adoption.

What is the main barrier to treatment adoption?

Social stigma leads to under-reporting, with only 23% of patients accurately disclosing symptoms to clinicians.

Page last updated on: