3D Printed Brain Model Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

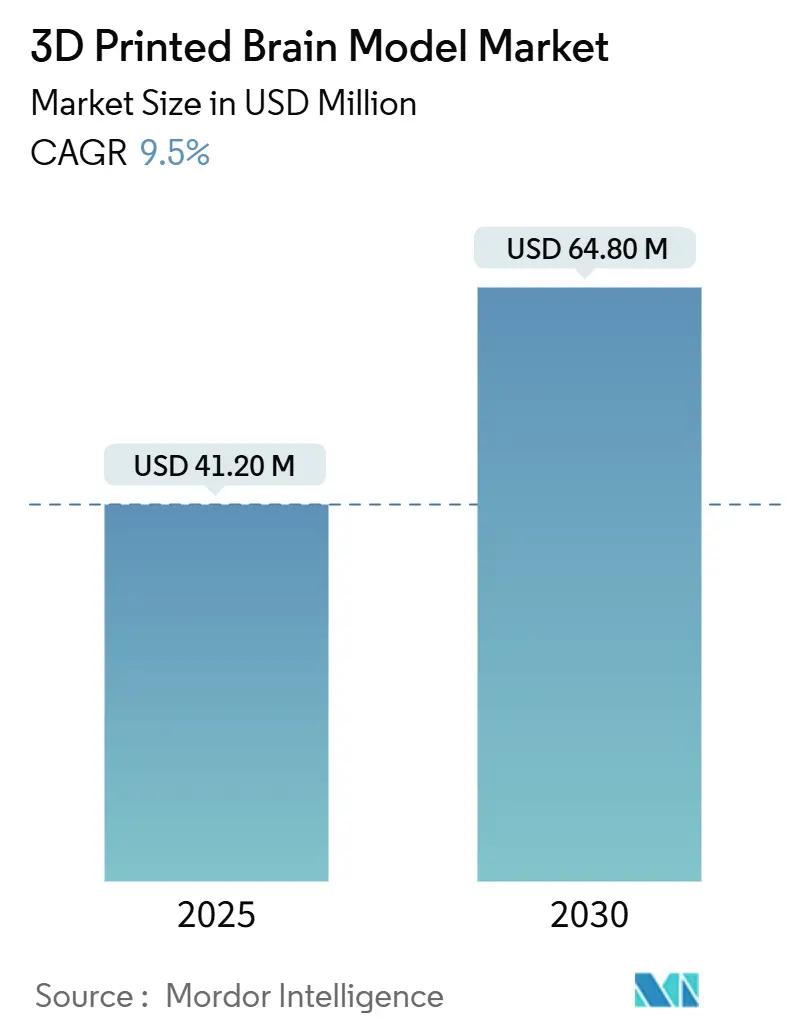

| Market Size (2025) | USD 41.20 Million |

| Market Size (2030) | USD 64.80 Million |

| Growth Rate (2025 - 2030) | 9.50% CAGR |

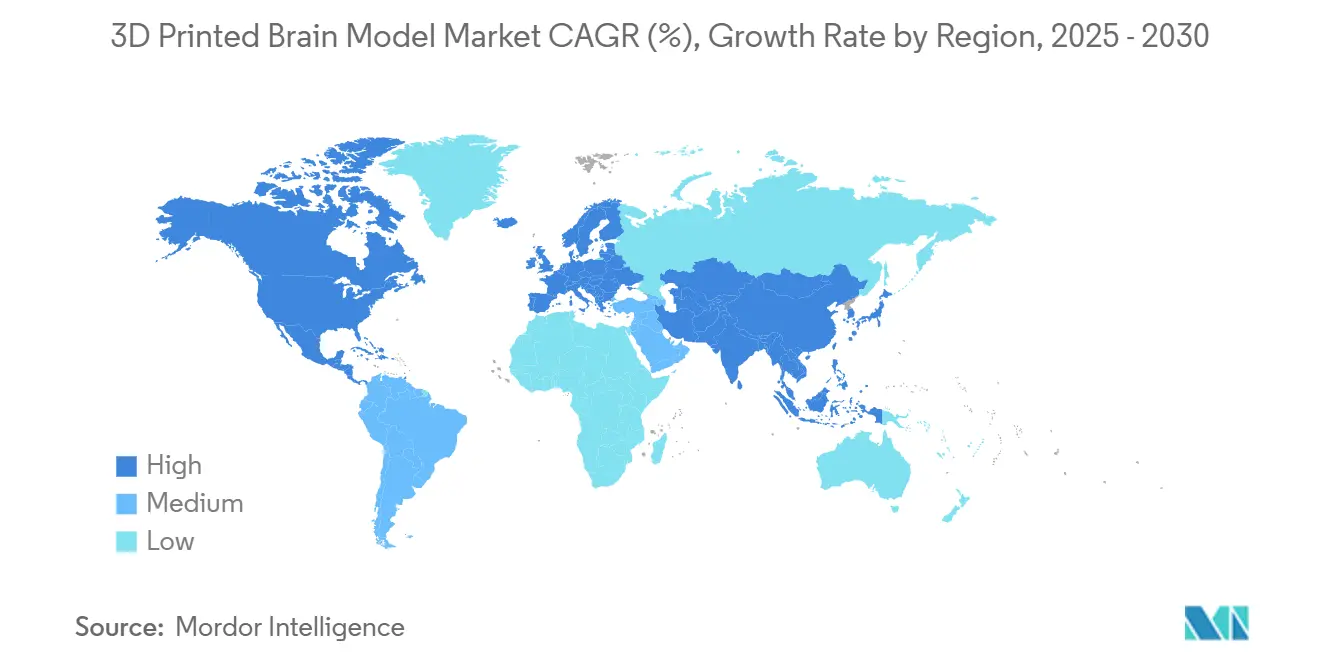

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

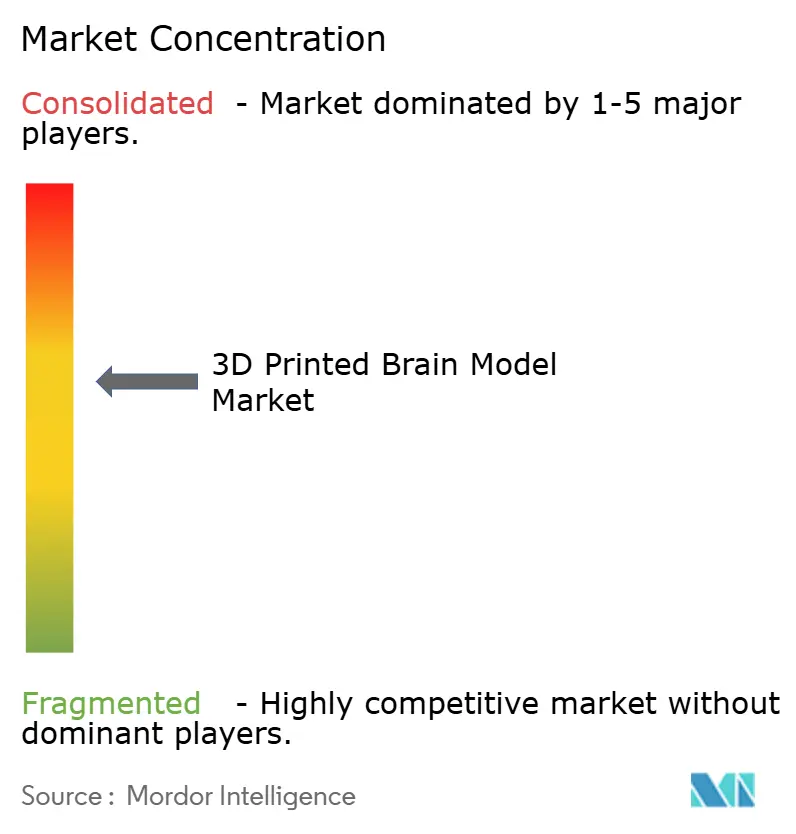

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Printed Brain Model Market Analysis by Mordor Intelligence

The 3D printed brain models market size stands at USD 41.2 million in 2025 and is projected to reach USD 64.8 million by 2030, reflecting a robust 9.5% CAGR over the forecast period. End-user demand is rising as neurosurgical residency programs adopt model-based simulation, reimbursement codes recognize patient-specific prints, and point-of-care (POC) manufacturing clears key regulatory hurdles. Hospitals now embed in-house 3D labs into surgical pathways, cutting average operative time by up to 62 minutes and saving USD 3,720 per case through reduced theater occupancy. Material advances, especially bioprinted hydrogels capable of forming functional neural networks, signal a shift from static visualization to living tissue constructs. At the same time, falling stereolithography printer prices and sub-USD 15 biocompatible resin costs expand access to mid-tier hospitals and medical colleges. Competitive strategies revolve around platform integration—combining segmentation software, printers, and validated materials under one quality umbrella—while value-chain opportunities emerge in automated DICOM segmentation, multi-material printing, and standards harmonization.

Key Report Takeaways

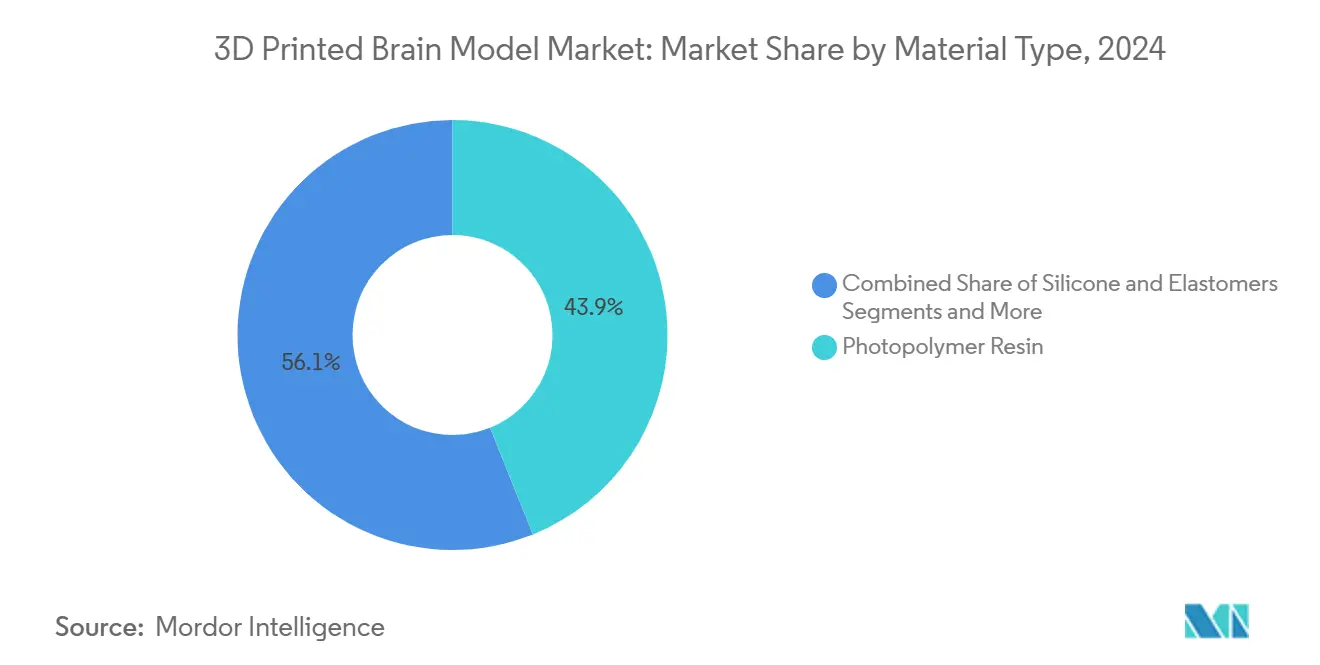

- By material, photopolymer resins led with 43.9% of 3D printed brain models market share in 2024, whereas bioprinted hydrogels are forecast to advance at a 27.5% CAGR through 2030.

- By technology, SLA/DLP platforms captured 38.6% of revenue in 2024; 3D bioprinting is projected to expand at a 29.2% CAGR to 2030.

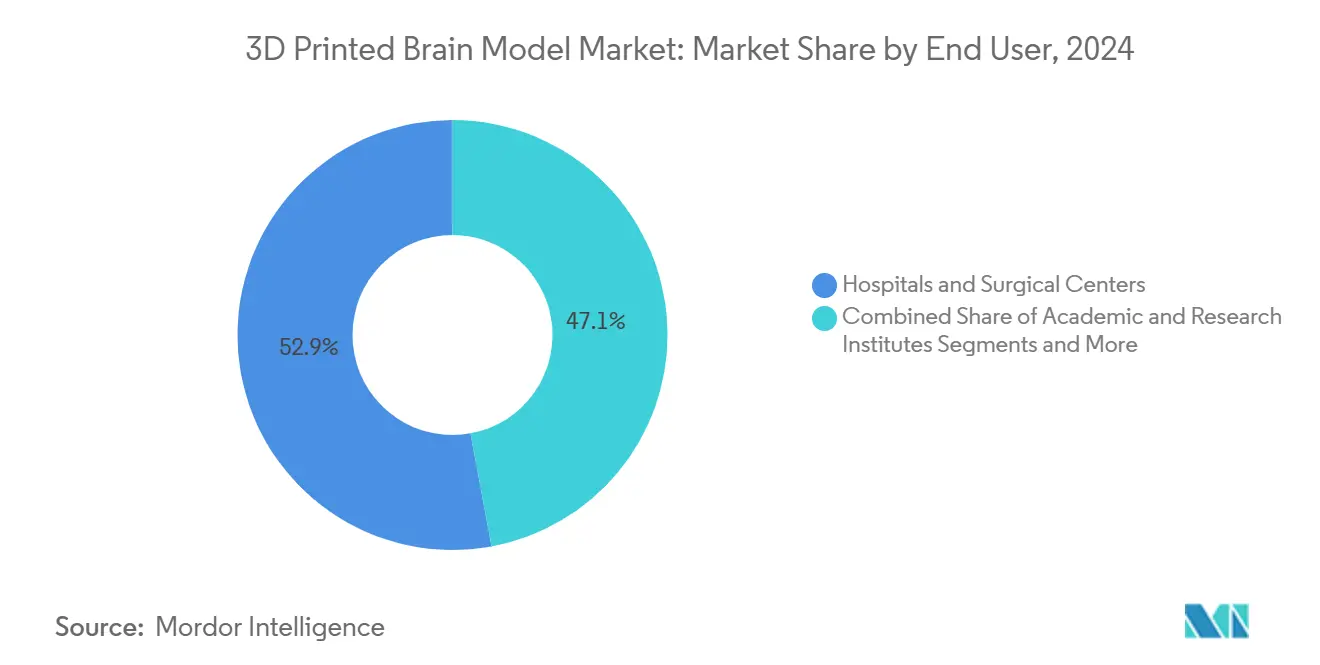

- By end user, hospitals and surgical centers held 52.9% of the 3D printed brain models market size in 2024, while medical device manufacturers register the fastest growth at 24.8% CAGR.

- By geography, North America generated 42.8% of 2024 revenue, yet Asia Pacific is anticipated to record the fastest regional growth at a 20.3% CAGR during 2025–2030.

Global 3D Printed Brain Model Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Neurosurgical Simulation Mandates | +2.10% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Growing Reimbursement Pathways For 3DP Anatomical Models | +1.80% | North America core, gradual EU adoption | Medium term (2-4 years) |

| Declining Desktop-VP Printer & Resin Costs | +1.40% | Global, with strongest impact in emerging markets | Short term (≤ 2 years) |

| Emergence Of FDA-Cleared Point-Of-Care Software/Printer Combos | +1.90% | North America, regulatory spillover to other regions | Long term (≥ 4 years) |

| Academic-Industry Consortia for Functional Brain Bioprinting | +1.20% | Global research hubs, concentrated in US, EU, Asia | Long term (≥ 4 years) |

| Philanthropic Funding for Low-Cost Neurosurgery Training in LMICS | +0.80% | Sub-Saharan Africa, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Neurosurgical Simulation Mandates

Medical boards now require residents to complete simulation hours using anatomically precise prints. The Accreditation Council for Graduate Medical Education added 3D model–based tasks to neurosurgery milestones, prompting U.S. residency programs to purchase dedicated printers.[1]Accreditation Council for Graduate Medical Education, “Milestones 2.0 Neurosurgery,” acgme.orgEuropean faculties follow suit after aneurysm-clipping rehearsals cut complication rates by double digits. Hospitals extend the concept to pre-operative rehearsals, with Yale’s in-house lab reducing average craniotomy time by one hour. These mandates lock in recurring demand because training cohorts renew annually, ensuring stable print volumes.

Growing Reimbursement Pathways for 3DP Anatomical Models

The American Medical Association introduced CPT codes 0620T-0621T for patient-specific 3D prints, converting what was once a cost center into a reimbursable service.[2]American Medical Association, “Category III Codes: 3D Printing,” ama-assn.org Early Medicare pilots demonstrated net savings through shorter OR occupancy, catalyzing private insurers to mirror the policy. In Europe, Germany’s DRG system approved case-based add-on payments for complex neurovascular models in 2025, and France is trialing a similar pathway for congenital malformation cases. Reimbursement materially improves return on investment for hospital POC labs, accelerating capital purchases of mid-range SLA printers.

Declining Desktop-VP Printer & Resin Costs

Medical-grade desktop stereolithography systems that cost USD 45,000 in 2018 now list below USD 2,000, while ISO-10993 class-l resins price under USD 15 per model. The cost drop lets community hospitals, nursing colleges, and low-resource clusters adopt 3D printed brain models market solutions once restricted to tertiary centers. Cheaper consumables also enable larger model batches for simulation boot camps, supporting evidence-based curricula without budget overruns.

FDA-Cleared Point-of-Care Software-Printer Combos

In 2025, the U.S. FDA cleared 3D Systems’ EXT 220 MED workflow—covering segmentation software, printer, and resin as a single medical device—for cranial applications. The ruling simplifies compliance for hospital-based production and shortens model lead time from two days to less than four hours. U.S. health systems are now establishing “clinical manufacturing suites” adjacent to radiology for on-demand prints during emergent hematoma evacuations, creating a new competitive frontier based on turnaround speed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Labor Hours for DICOM Segmentation & Post-Processing | -1.60% | Global, particularly acute in high-labor-cost regions | Short term (≤ 2 years) |

| Fragmented Material Biocompatibility Standards | -1.10% | Global, with regulatory complexity in multi-market operations | Medium term (2-4 years) |

| IP Uncertainty Around Patient-Specific Neuro-Models | -0.90% | North America & Europe, with spillover to APAC markets | Medium term (2-4 years) |

| Limited Autoclave-Safe Polymers for OR Use | -0.70% | Global, with highest impact in sterile surgical environments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Labor Hours for DICOM Segmentation & Post-Processing

Complex neuroanatomy often demands manual cleanup after automated AI passes. Peer-reviewed time-motion studies put average segmentation at 8–24 hours per patient. This bottleneck inflates per-case cost and limits emergency deployment. Smaller centers lacking neuroradiology staff must outsource data prep, losing the immediacy offered by POC printing. Vendors respond with deep-learning plugins, yet regulatory validation of automated contours remains a gating factor.

Fragmented Material Biocompatibility Standards

ISO 10993 supplies general guidance, but regional authorities overlay divergent sterility and extractable limits, forcing parallel test programs for each resin batch.[3]Chenyang Niu et al., “Biocompatibility Standards in 3D Printing,” Frontiers in Materials, frontiersin.org For example, the same photopolymer passes U.S. FDA cytotoxicity tests but fails EU particulate thresholds. Developers absorb duplicative validation costs that deter novel neural-specific resins or conductive hydrogels. Ongoing ISO/ASTM joint task groups aim for harmonized additive-manufacturing annexes, but market friction persists during the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Bioprinted Hydrogels Drive Innovation

Bioprinted hydrogels recorded the fastest 27.5% CAGR through 2030, propelled by breakthroughs in fibrin-based inks that supported synaptic signaling after seven days in culture. Photopolymer resins remained dominant with 43.9% share in 2024 owing to sub-100 micron accuracy essential for microvascular models. Thermoplastic filaments serve price-sensitive teaching labs, while silicone elastomers improve tactile feedback for cerebrovascular clipping practice. Composite formulations integrating radiopaque barium sulfate allow intra-operative fluoroscopy training, an emerging niche within the 3D printed brain models market.

Material selection increasingly hinges on sterilization compatibility; few resins survive 134 °C autoclave cycles required for sterile theatre use. Consequently, hospitals often print in-house reference models and outsource OR-grade guides to specialized bureaus. Nevertheless, the convergence of hydrogel bioprinting with photopolymer chassis hints at hybrid constructs that pair rigid skull scaffolds with living cortex analogs, positioning material science as a core value driver of the 3D printed brain models market.

By Printing Technology: 3D Bioprinting Transforms Applications

SLA/DLP captured 38.6% revenue in 2024 because its laser-cured layers achieve the 150–200 micron sulcus detail required by vascular surgeons. Yet 3D bioprinting shows the highest 29.2% CAGR and is redefining utility: Wisconsin researchers printed centimeter-scale neural tissue with functional connectivity, enabling drug-response assays impossible with inert plastics. Multi-jet platforms combine rigid and elastomeric droplets, offering surgeons a single-piece model that differentiates tumor mass from surrounding cortex colors. Open-source masked-SLA bioprinters documented on PubMed lower entry barriers for academic consortia, fostering global diffusion.

Point-of-care suites blur modality lines, embedding AI segmentation, resin mixing, and printer farm orchestration into one validated appliance. This plug-and-play experience helps small hospitals leapfrog steep learning curves, fueling competitive intensity inside the 3D printed brain models market.

By End User: Medical Device Manufacturers Accelerate Adoption

Hospitals and surgical centers controlled 52.9% of 2024 revenue, reflecting residency mandates and pre-operative rehearsal needs. However, device manufacturers clock a 24.8% CAGR as they iterate cranial implants and neurostim leads on patient datasets instead of cadaver averages. Medtronic used high-fidelity brain prints to refine electrode trajectories for its BrainSense adaptive DBS platform, cutting prototype cycles and securing FDA clearance in late 2025. Academic labs maintain a steady share by leveraging living tissue prints for Alzheimer’s drug screening, while dedicated simulation centers purchase large model batches for board-certification courses. Consumer tinkering remains nascent but grows as sub-USD 2,000 printers enter the home-lab ecosystem, echoing broader maker-movement trends.

Geography Analysis

North America accounted for 42.8% revenue in 2024, driven by ACGME simulation rules, CMS reimbursement pilots, and FDA precedents that collectively de-risk hospital adoption. Flagship institutions such as the Mayo Clinic publish case studies showing operative-time reductions and fewer clip misplacements in aneurysm surgery after POC model rehearsals. The United States also leads patent filings for neural-specific hydrogels, reinforcing its technology leadership within the 3D printed brain models market.

Asia-Pacific delivers the fastest 20.3% CAGR through 2030 as China quadruples neurosurgeon training seats and funds additive-manufacturing industrial parks. Japan’s aging society raises craniotomy volumes, stimulating demand for patient-specific rehearsal tools. India’s medical-tourism hubs integrate printed models to differentiate complex tumor packages, while South Korea’s government matches grants for open-platform bioprinters in university hospitals.

Europe posts moderate growth amid regulatory heterogeneity. Germany’s Fraunhofer institutes commercialize ISO-class photopolymer blends, but cross-border workflows face CE-Mark variances. France and Italy pilot reimbursement for 3DP surgical guides, yet adoption remains center-specific. Post-Brexit U.K. maintains prowess in neuro-robotic research, channeling Innovate UK funds to hybrid printing ventures. Despite fragmentation, EU universities sustain demand for cortex organoid prints used in pharma collaborations, cementing Europe as an R&D heavyweight within the global 3D printed brain models market.

Competitive Landscape

The 3D printed brain models market shows moderate concentration. Top five suppliers—3D Systems, Stratasys, Materialise, Axial3D, and Anatomage—collectively control roughly 55% of revenue, reflecting expertise in regulated healthcare workflows. Large incumbents bundle software, printers, and resins under ISO 13485 quality systems, giving hospitals a single-vendor path to compliance. Specialist firms differentiate via neuro-specific libraries and AI segmentation as-a-service, while start-up bioprinting houses chase venture funding for living-tissue constructs.

Strategic moves underscore ecosystem control. 3D Systems secured FDA clearance for its EXT 220 MED POC line, creating a template competitors must follow. Materialise acquired a minority stake in an AI segmentation specialist to automate model prep, cutting technician time by half. Brainlab’s planned USD 216 million IPO funds software-first workflow engines that integrate 3D models with OR navigation. Meanwhile, Medtronic cross-licenses print files with academic labs to co-develop implantable neurostim prototypes, exemplifying how device OEMs leverage the 3D printed brain models market for agile R&D.

The innovation frontier is functionalization—embedding perfusable channels and electro-conductive hydrogel layers. Wisconsin’s functional tissue proof-of-concept sparked OEM partnerships seeking pre-clinical screening platforms. Vendors that master hybrid printing stand to disrupt traditional service bureaus by offering turnkey constructs rather than inert plastics.

3D Printed Brain Model Industry Leaders

3D Systems Corporation

Stratasys Ltd.

Materialise NV

Axial3D Ltd.

Lazarus 3D, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Medtronic reported FY2025 revenue of USD 33.5 billion and launched BrainSense adaptive DBS, developed using patient-specific 3D models.

- May 2025: Restor3d secured USD 38 million to accelerate 3D-printed spinal and cranial implants.

- February 2024: University of Wisconsin-Madison printed functional human brain tissue with synaptic activity, published in Cell Stem Cell.

Global 3D Printed Brain Model Market Report Scope

| Thermoplastic Polymers (PLA, ABS, PETG) |

| Photopolymer Resins (SLA/DLP) |

| Silicone & Elastomers |

| Composite & Filled Materials |

| Bioprinted Hydrogels |

| FDM / FFF |

| SLA / DLP |

| SLS |

| PolyJet / Material-Jetting |

| 3D Bioprinting |

| Hospitals & Surgical Centers |

| Academic & Research Institutes |

| Simulation Training Labs |

| Medical Device Manufacturers |

| Individual Consumers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material Type | Thermoplastic Polymers (PLA, ABS, PETG) | |

| Photopolymer Resins (SLA/DLP) | ||

| Silicone & Elastomers | ||

| Composite & Filled Materials | ||

| Bioprinted Hydrogels | ||

| By Printing Technology | FDM / FFF | |

| SLA / DLP | ||

| SLS | ||

| PolyJet / Material-Jetting | ||

| 3D Bioprinting | ||

| By End User | Hospitals & Surgical Centers | |

| Academic & Research Institutes | ||

| Simulation Training Labs | ||

| Medical Device Manufacturers | ||

| Individual Consumers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the 3D printed brain models market in 2025?

The market is valued at USD 41.2 million in 2025 and is forecast to grow at a 9.5% CAGR to USD 64.8 million by 2030.

Which material type grows fastest in neurosurgical 3D printing?

Bioprinted hydrogels expand at a 27.5% CAGR because they support functional neural network formation for research and drug testing.

Why are hospitals investing in point-of-care 3D printing suites?

FDA-cleared integrated printer-software combos let hospitals produce patient-specific models within hours, trimming operative time and qualifying for reimbursement.

What limits wider adoption of these models today?

Labor-intensive DICOM segmentation and fragmented biocompatibility standards raise costs and slow throughput.

Which company innovations should executives watch?

3D Systems FDA-cleared POC platform and Medtronics BrainSense DBS, both developed on 3D printed brain models, signal market-shaping advances.

Page last updated on: