3D Printed Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

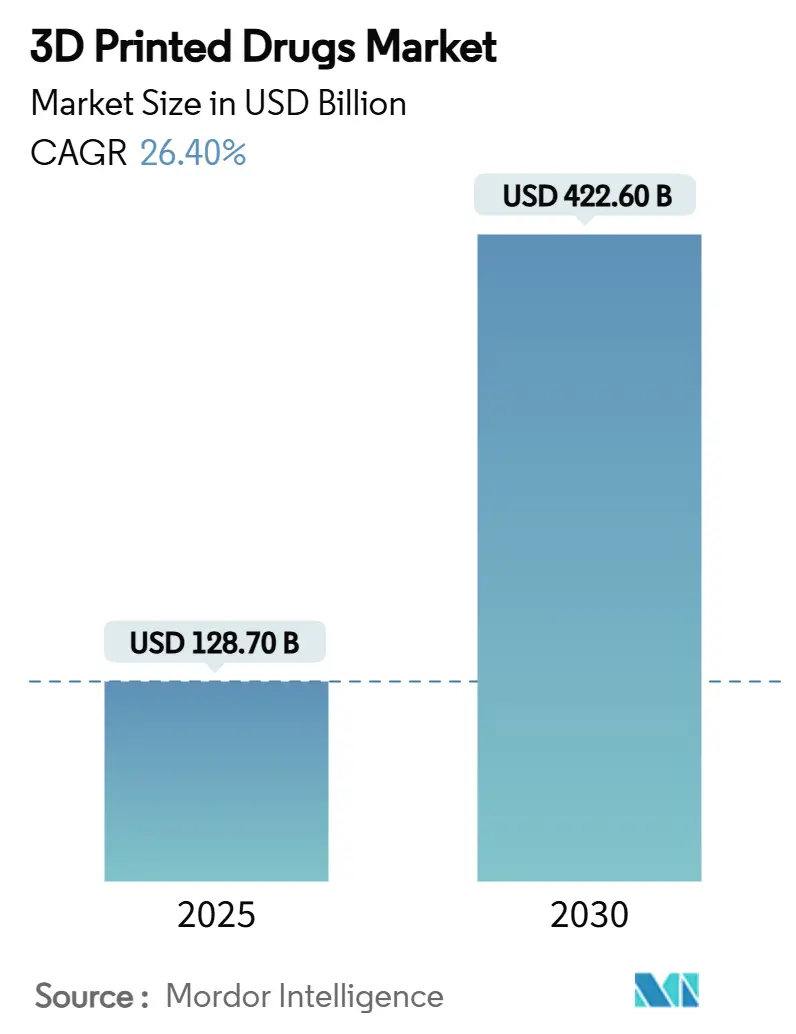

| Market Size (2025) | USD 128.70 Billion |

| Market Size (2030) | USD 422.60 Billion |

| Growth Rate (2025 - 2030) | 26.40% CAGR |

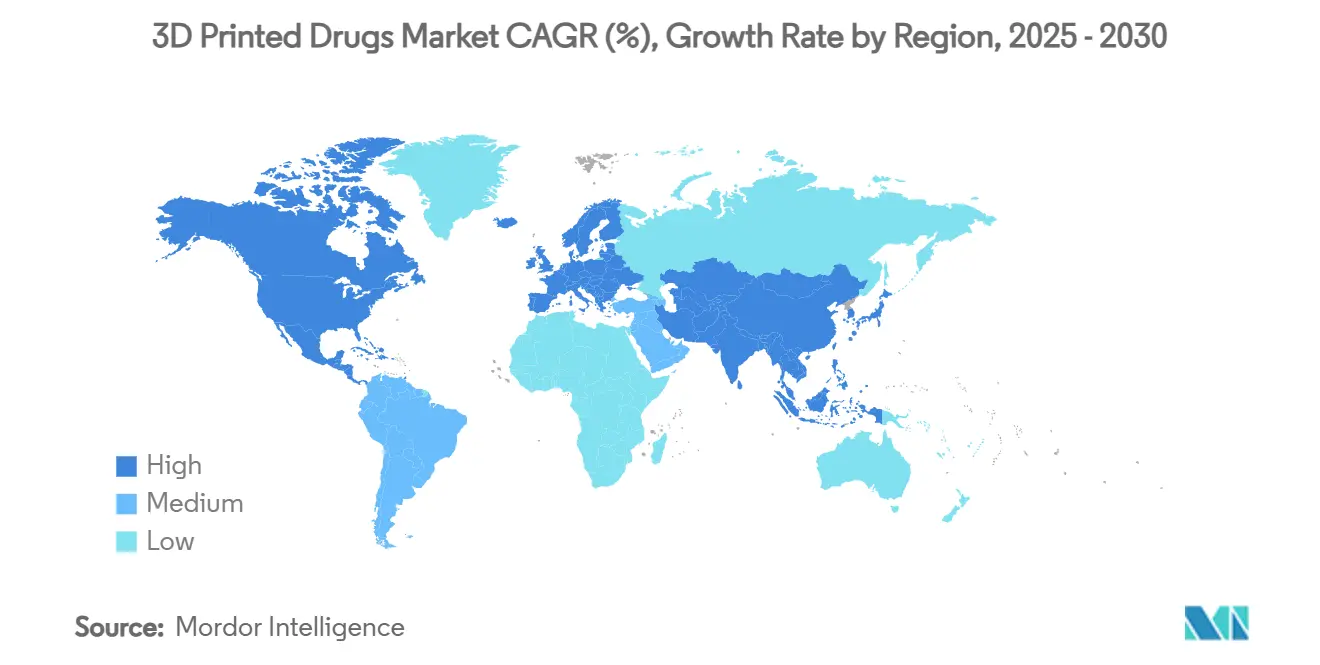

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Printed Drugs Market Analysis by Mordor Intelligence

The 3D printed drugs market size stands at USD 128.7 million in 2025 and is forecast to reach USD 422.6 million by 2030, registering a 26.40% CAGR. This rapid growth reflects the transition from batch-based manufacturing toward patient-specific production and underlines the sector’s emerging commercial viability. Regulatory milestones, notably the FDA’s 2015 approval of Spritam and the 2025 launch of the Advanced Manufacturing Technology designation program, have normalized additive techniques in drug fabrication. Hospitals are piloting on-demand printing to avoid inventory waste, while pharmaceutical companies invest in GMP-compliant platforms that shorten formulation cycles. Ageing populations, dysphagia prevalence, and increasing polypharmacy cases create consistent demand for customized dosage forms. Meanwhile, binder-jet and semisolid extrusion improvements are lowering unit costs, and newly validated excipients are expanding formulation options, signaling a sustained expansion phase for the 3D printed drugs market.

Key Report Takeaways

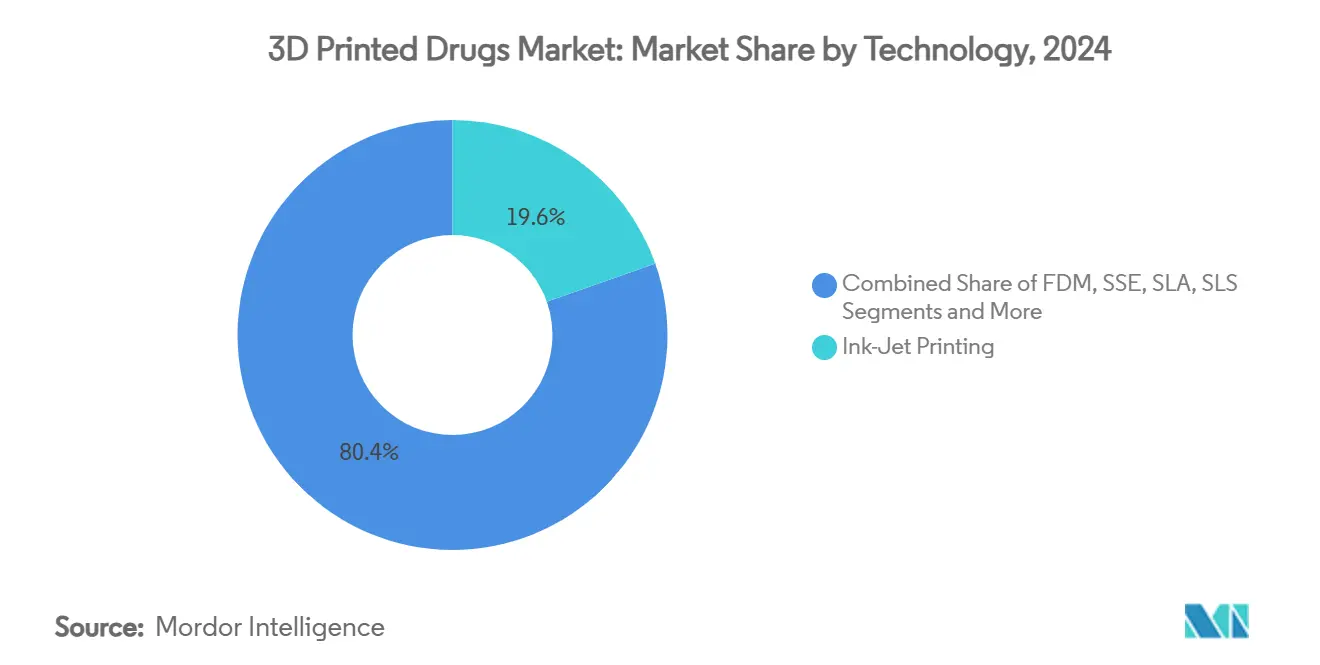

- By technology, ink-jet printing led with 19.6% revenue share in 2024, whereas direct powder extrusion is advancing at a 22.5% CAGR through 2030.

- By drug form, tablets accounted for a 20.4% slice of the 3D printed drugs market share in 2024, while microneedle patches are set to grow at 24.0% CAGR to 2030.

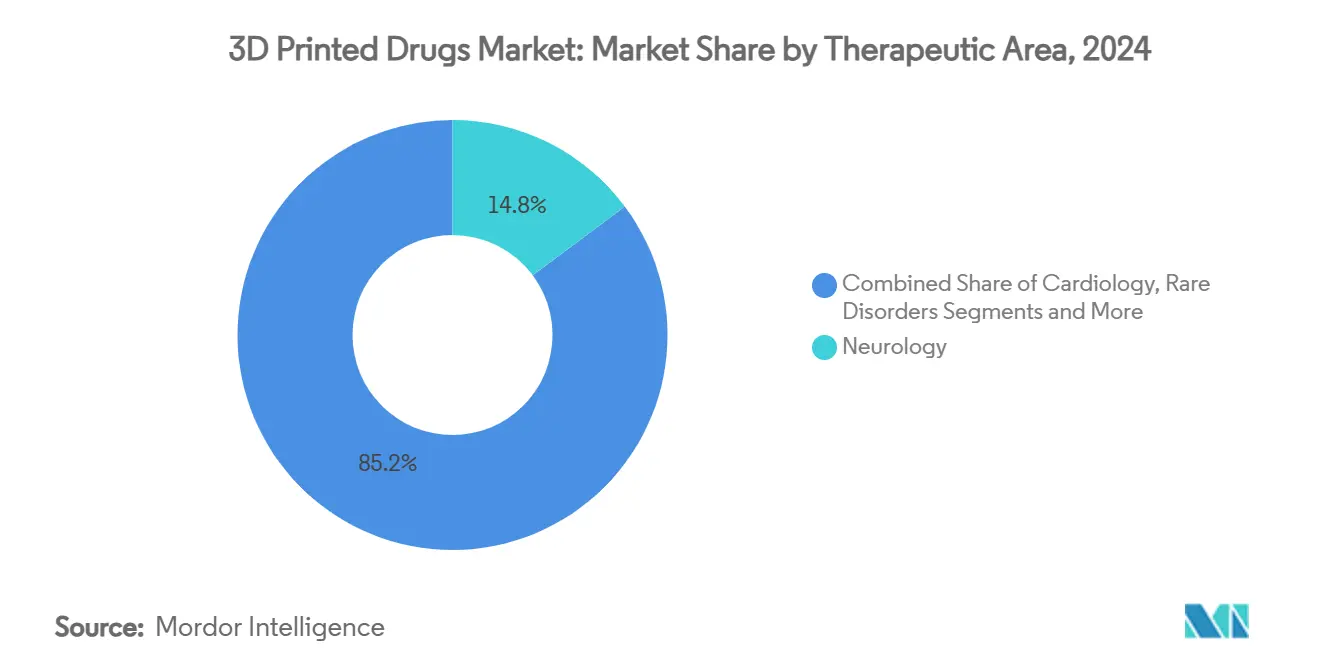

- By therapeutic area, neurology captured 14.8% of the 3D printed drugs market size in 2024, and oncology records the highest projected CAGR at 18.2% to 2030.

- By end-user, hospital pharmacies held a 20.6% share in 2024; compounding pharmacies post the fastest CAGR at 17.5% through 2030.

- By geography, North America dominated with a 30.8% share in 2024; Asia-Pacific posts a 19.8% CAGR through 2030.

Market Trends and Insights

Drivers Impact Analysis of 3D Printed Drugs Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising geriatric & dysphagic population | +4.20% | North America & Europe | Long term (≥ 4 years) |

| FDA approval of Spritam accelerating acceptance | +5.80% | North America, spillover to APAC | Medium term (2-4 years) |

| Surge in demand for personalised medicines | +6.10% | North America & European Union | Long term (≥ 4 years) |

| Advances in binder-jet & SSE lowering unit cost | +3.90% | North America & Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Hospital-based on-demand manufacturing pilots | +2.80% | North America & European Union | Short term (≤ 2 years) |

| Emergence of pharma-ink licensing revenue model | +1.70% | North America & European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Geriatric & Dysphagic Population

Growing life expectancy increases polypharmacy, yet older adults often struggle with large tablets. 3D printing enables single polypills that combine multiple APIs and dissolve quickly, curbing non-adherence that historically reached 50% in this cohort.[1]University of Nottingham, “Multi-Material InkJet 3D Printing for Pharmaceuticals,” nottingham.ac.uk Orodispersible films designed for dysphagic patients disintegrate in seconds and deliver better bioavailability. These solutions improve patient outcomes and lower systemic costs tied to medication errors. National health services, therefore, champion additive techniques that tailor dosage strength, geometry, and release profiles.

FDA Approval of Spritam Accelerating Regulatory Acceptance

Spritam provided a precedent that reassured regulators across major markets. In 2025, the FDA created an Advanced Manufacturing Technology designation that shortens review cycles for 3D-printed submissions, shrinking commercial lead times.[2]U.S. Food & Drug Administration, “Quality Management System Regulation (QMSR) Final Rule,” fda.gov DARPA’s EQUIP-A-Pharma framework offers real-time data exchange to regulators, establishing the digital backbone for distributed, secure manufacturing. This alignment between defence and health agencies signals enduring institutional support, encouraging pharmaceutical firms to scale additive lines.

Surge in Demand for Personalized / Precision Medicines

Pharmacogenomics underscores the inadequacy of one-size-fits-all dosing. 3D printing links genomic data to on-demand tablets that match metabolic profiles, enhancing efficacy while mitigating toxicity. Pfizer’s Pharma 5.0 program embeds robotics around additive platforms to deliver genotype-driven formulations. Hospital devices such as UMC Utrecht’s NANOSPRESSO fabricate nano-scale medicines at the bedside, addressing ultra-rare disorders hitherto ignored by traditional supply chains. Oncology stands to gain as clinicians adjust micro-doses based on tumor response metrics.

Advances in Binder-Jet & SSE Lowering Unit Cost

Binder-jet upgrades now print at higher speeds with validated microcrystalline cellulose and lactose, cutting per-unit cost gaps with conventional tableting. Merck and EOS/AMCM demonstrated GMP-grade powder bed fusion tablets with release profiles exceeding 80% API liberation in 5 minutes. Continuous granulation paired with selective laser sintering compresses production footprints, letting mid-volume batches become profitable. These improvements unlock broader portfolios beyond orphan drugs.

Restraints Impact Analysis of 3D Printed Drugs Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolving FDA-EMA quality-by-design requirements | -3.20% | North America & European Union | Medium term (2-4 years) |

| Limited GMP-grade printable excipient portfolio | -2.80% | North America & European Union | Long term (≥ 4 years) |

| Cyber-security & IP leakage of digital files | -1.90% | Global distributed networks | Short term (≤ 2 years) |

| Scarcity of large-batch validated printers | -2.10% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Evolving FDA-EMA Quality-by-Design Requirements

The FDA’s Quality Management System Regulation, effective February 2026, adopts ISO 13485:2016 but introduces additive-specific controls. Firms must validate layer thickness, laser power, and print orientation to guarantee bioequivalence. Microneedle patch trials showed 10 µm layers and 65 mW/cm² exposure optimal for integrity, yet added months to verification tasks.[3]MDPI, “Optimization of 3D-Printed Microneedles,” mdpi.com Similar guidance from the European Medicines Agency raises compliance spend, favouring incumbents with deep regulatory teams.

Limited GMP-Grade Printable Excipient Portfolio

Only a handful of excipients—polyvinyl alcohol, microcrystalline cellulose, lactose—hold full GMP validation for additive routes. New chemistries such as thiol-ene resins promise better strength yet require multi-year toxicology dossiers before clearance. This bottleneck slows complex formulations needing specialised release matrices. Material suppliers and academia have therefore intensified joint screening programs, though commercial roll-out remains distant.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

3D Printed Drugs Market Segment Analysis

By Technology:

Ink-Jet Printing Maintains Lead While Powder Extrusion AcceleratesInk-jet printing retained 19.6% of the 3D printed drugs market in 2024, benefiting from precise droplet placement and seamless integration with existing clean-room facilities. Direct powder extrusion posts a 22.5% CAGR as its solvent-free process and faster throughput resonate with cost-sensitive manufacturers. Binder-jetting also gains traction through Merck–EOS collaborations that deliver GMP-grade powder bed fusion tablets. Semisolid extrusion caters to orodispersible films that dissolve in under 30 seconds, while selective laser sintering unlocks novel geometries that realize 80% drug release within 5 minutes. Equipment vendors have responded with modular printers featuring in-line Raman spectroscopy for closed-loop quality control. Over the forecast window, powder extrusion’s productivity upside should narrow the revenue gap, yet ink-jet’s entrenched user base and deeper validation history cement its relevance.

A wave of public-private test beds, especially across U.S. Veterans Affairs hospitals, will prove pivotal. These pilots gather stability data that translates into regulatory submissions, compressing time-to-market for follow-on formulations. Chinese CDMOs replicate the model, bundling direct powder extrusion lines with formulation services aimed at regional generics firms. As a result, the 3D printed drugs market is expected to witness diversified technology portfolios rather than winner-takes-all outcomes.

By Drug Form:

Tablets Dominate but Microneedles Disrupt AdministrationTablets captured 20.4% of the 3D printed drugs market share in 2024 after Spritam’s success validated fast-disintegrating, high-load designs. Complex geometries now accommodate multi-API layering, lessening pill burden in epilepsy, Parkinson’s, and hypertension protocols. Microneedle patches, registering a 24.0% CAGR, answer needle-phobia and avoid hepatic first-pass metabolism. Hospitals trial tailored insulin patch arrays that allow overnight basal delivery with improved glycaemic control. Capsules and multilayer polypills serve geriatric cohorts by embedding morning and evening doses in one unit, improving adherence.

Oral fast-dissolving films are rising as paediatric oncologists seek noninvasive routes for cytotoxics. Micro-implants printed from bioresorbable polymers provide sustained analgesic release for postoperative pain. Across forms, additive manufacturing’s ability to modulate geometry and porosity drives adoption in indications where conventional methods cannot balance release kinetics with patient comfort.

By Therapeutic Area:

Neurology Leads, Oncology Gains MomentumNeurology constituted 14.8% of the 3D printed drugs market size in 2024, as epilepsy treatments require rapid disintegration and precise milligram-level dosing. Parkinson’s regimens similarly benefit from polypills that align L-dopa with COMT inhibitors to smooth motor response. Oncology’s 18.2% CAGR reflects its dependence on patient-specific dosing windows; additive platforms enable 5-FU and capecitabine tablets calibrated to genomic markers. Digital twin simulations refine solid-tumour dosing by mapping drug diffusion across heterogeneous tissue, guiding printer G-code to encode release gradients.

Cardiology trials explore polypills integrating beta-blockers, statins, and antiplatelets, targeting the 50% medication non-compliance in post-infarct patients. Rare paediatric disorders, historically hindered by minuscule batch sizes, tap 3D printing for personalized siRNA implants. Pain management leverages matrix tablets that deliver multi-day opioid release while embedding naloxone fail-safes. Together, these applications expand the 3D printed drugs market beyond orphans into high-volume chronic diseases.

By End-User:

Hospital Pharmacies Anchor Growth, Compounding Pharmacies AccelerateHospital pharmacies owned 20.6% of revenue in 2024 by integrating on-site printers that cut drug-stock obsolescence and improve formulary agility. The NANOSPRESSO benchtop unit prints nano-scale chemotherapeutics within 30 minutes, enabling same-day administration for paediatric oncology wards. Compounding pharmacies record the fastest 17.5% CAGR as they retrofit clean-rooms with desktop extrusion printers, transforming the long-tail of personalized hormone and veterinary drugs.

Specialty clinics explore chair-side fabrication for dermatology biologics wrapped in microneedle arrays. Contract development and manufacturing organizations (CDMOs) expand pilot lines, luring biotech’s that lack capital for in-house GMP facilities. Ambulatory surgical centres adopt dissolving implants that obviate nurse-driven dose titrations, shortening discharge times. Collectively, these trends embed additive capabilities across diverse care settings, reinforcing demand resilience for the 3D printed drugs market.

By Material:

Excipients, Landscape Faces, Controlled ExpansionPolyvinyl alcohol (PVA) and microcrystalline cellulose remain the backbone polymers because of their documented biocompatibility and sintering characteristics. Lactose leads soluble filler applications owing to its established regulatory record. Experimental thiol-ene resins enable ultraviolet cross-linking for ink-jet photopolymer tablets, although toxicology dossiers remain under FDA review. Hydroxypropyl methylcellulose matrices, when combined with pore-formers, create zero-order release curves that are advantageous in oncology. Collaboration between material suppliers and pharmaceutical labs aims to certify additional polymer–API combinations, yet stringent GMP demands curb the cadence of approvals.

Continued shortages of GMP-qualified excipients could restrain the 3D-printed drugs market unless rapid material-screening consortia scale up. The U.S. Pharmacopeia is working on a public standard additive manufacturing chapter that will streamline risk-assessment documentation, potentially unlocking a broader palette of polymers and fillers.

By Licensing Model:

Pharma-Ink Monetization EmergesPlatform owners have started licensing proprietary “pharma-inks” containing co-processed excipient blends and surfactants, shifting revenue from hardware sales to consumables. Aprecia drafted multi-year contracts supplying ZipDose powder cartridges tied to minimum volume commitments. FabRx offers paediatric-grade filament spools embedded with sweeteners compliant with EMA taste-masking guidelines. Such models echo razor-and-blade economics and promise recurring income streams, stimulating printer fleet expansion among hospital and compounding partners. Nonetheless, healthcare providers negotiate for open-source consumables to avert vendor lock-in, signalling a gradual convergence toward hybrid ecosystems.

Geography Analysis

North America 3D Printed Drugs Market

North America retained 30.8% of the 3D printed drugs market in 2024, propelled by FDA programs that streamline additive submissions and by DARPA’s EQUIP-A-Pharma data pipeline that underpins regulatory confidence. Aprecia’s Ohio manufacturing hub and Johnson & Johnson’s USD 55 billion capital plan illustrate pharmaceutical incumbents’ investment in advanced production. Academic-industry consortia in Boston and Raleigh conduct stability trials across temperature and humidity ranges, feeding datasets into common review dossiers that shorten market-entry timelines.

APAC 3D Printed Drugs Market

Asia-Pacific posts the fastest 19.8% CAGR through 2030 as Japan, China, and India adopt Pharmaceutical Inspection Co-operation Scheme GMP frameworks that harmonize cross-border approvals. Singapore’s National Additive Manufacturing Innovation Cluster funds lab-to-clinic pathways, while South Korean CDMOs integrate direct powder extrusion lines into biologics campuses. Chinese public hospitals pioneer point-of-care printing for paediatric leukaemia polypills, reducing reliance on imported age-appropriate formulations.

Europe 3D Printed Drugs Market

Europe maintains moderate yet stable progress. The European Medicines Agency’s additive-specific guidance elevates compliance thresholds, but projects such as Merck’s EOS powder-bed tablet facility in Darmstadt validate continental leadership in process industrialization. University-hospital networks across the Netherlands print personalized vancomycin capsules to counter antimicrobial stewardship challenges. Sustainability mandates encourage zero-inventory approaches that dovetail with distributed additive production. Collectively, regional policy support and manufacturing investments sustain broad geographic diversification for the 3D printed drugs market.

Competitive Landscape

Competitive intensity remains moderate, as high technical barriers restrict new entrants yet do not create monopoly conditions. Aprecia capitalises on first-mover FDA approval and markets ZipDose licenses to neurology firms seeking rapid reformulation paths. Triastek partnered with BioNTech in a potential USD 1.2 billion venture to produce oral RNA therapeutics, signaling additive applicability beyond small-molecule drugs. FabRx targets paediatrics with the Printlets platform, which delivers chewable tablets printed in under 10 seconds per dose.

Large pharmaceutical companies adopt dual approaches: internal pilot lines for high-value indications and external CDMO partnerships for lower-volume niche products. Johnson & Johnson’s North Carolina biologics site embeds additive tablet cell lines adjacent to fill-finish suites, creating a continuum from biologic substance to personalised oral dosage. GlaxoSmithKline trials binder-jet equipment inside R&D campuses to reduce formulation cycle times by one-third, positioning additive as a catalyst for pipeline acceleration.

Start-ups differentiate through novel hardware, such as stereolithography micro-needle printers and AI-driven slicing software that predicts mechanical integrity from powder rheology. Material suppliers file patents covering excipient blends with pigment markers that verify authenticity under near-infrared scans, deterring counterfeiters in decentralised production models. Overall, strategic emphasis on platform diversification, GMP validation, and intellectual property management shapes competition within the 3D printed drugs market.

3D Printed Drugs Industry Leaders

Aprecia Pharmaceuticals

Triastek Inc.

FabRx Ltd.

GlaxoSmithKline plc

Merck KGaA

- *Disclaimer: Major Players sorted in no particular order

3D Printed Drugs Market Companies Covered in this Report

- Aprecia Pharmaceuticals

- Triastek Inc.

- FabRx Ltd.

- GlaxoSmithKline

- Merck

- AstraZeneca

- Pfizer

- Johnson & Johnson

- Novartis

- Eli Lilly and Company

- Sanofi

- Bristol-Myers Squibb

- Bayer

- Boehringer Ingelheim

- Takeda Pharmaceuticals

- Teva Pharmaceutical Industries

- Thermo Fisher Scientific (Pharma Services)

- Stratasys

- Triastek Inc.

- Laxxon Medical

Recent Industry Developments in 3D Printed Drugs Market

- July 2025: Triastek entered a potential USD 1.2 billion collaboration with BioNTech to develop oral RNA therapeutics via additive manufacturing.

- March 2025: Johnson & Johnson announced a USD 55 billion investment in U.S. manufacturing facilities over four years, including a 500,000 sq ft biologics site in North Carolina featuring additive capabilities.

- January 2025: The FDA released draft cGMP guidance that explicitly supports 3D printing. The comment period will end in April 2025.

- September 2024: Adare Pharma Solutions and Laxxon Medical partnered to co-develop 3D-printed pharmaceuticals targeting enhanced bioavailability.

Global 3D Printed Drugs Market Report Scope

Segmentation Overview

| Binder Jetting (Powder-Bed) |

| Fused Deposition Modelling (FDM) |

| Semisolid / Paste Extrusion (SSE) |

| Stereolithography (SLA) |

| Selective Laser Sintering (SLS) |

| Direct Powder Extrusion |

| Other / Hybrid Techniques |

| Tablets |

| Capsules |

| Multi-layer Polypills |

| Oral Fast-Dissolving Films |

| Micro-implants & Depots |

| Microneedle Patches |

| Others |

| Immediate-Release |

| Sustained / Modified Release |

| Orally Disintegrating |

| Multi-compartmental / Polypill |

| Neurology |

| Oncology |

| Cardiology |

| Rare / Paediatric Disorders |

| Pain Management & Others |

| Hospital Pharmacies |

| Specialty Clinics & Centres |

| Compounding & Academic Pharmacies |

| Ambulatory Surgical Centres |

| Contract Manufacturing Organisations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Binder Jetting (Powder-Bed) | |

| Fused Deposition Modelling (FDM) | ||

| Semisolid / Paste Extrusion (SSE) | ||

| Stereolithography (SLA) | ||

| Selective Laser Sintering (SLS) | ||

| Direct Powder Extrusion | ||

| Other / Hybrid Techniques | ||

| By Drug Form | Tablets | |

| Capsules | ||

| Multi-layer Polypills | ||

| Oral Fast-Dissolving Films | ||

| Micro-implants & Depots | ||

| Microneedle Patches | ||

| Others | ||

| By Drug-Release Profile | Immediate-Release | |

| Sustained / Modified Release | ||

| Orally Disintegrating | ||

| Multi-compartmental / Polypill | ||

| By Therapeutic Area | Neurology | |

| Oncology | ||

| Cardiology | ||

| Rare / Paediatric Disorders | ||

| Pain Management & Others | ||

| By End-User | Hospital Pharmacies | |

| Specialty Clinics & Centres | ||

| Compounding & Academic Pharmacies | ||

| Ambulatory Surgical Centres | ||

| Contract Manufacturing Organisations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the 3D-printed drugs market growing?

The 3D printed drugs market is expanding at a 26.40% CAGR between 2025 and 2030, rising from USD 128.7 million to USD 422.6 million.

Which region leads the 3D printed drugs market?

North America leads with 30.8% revenue share in 2024 due to supportive FDA frameworks and hospital pilot programs.

What technology holds the largest share?

Ink-jet printing dominates with 19.6% share in 2024, favoured for precision drug deposition and established regulatory acceptance.

Why are microneedle patches gaining popularity?

Microneedles grow at 24.0% CAGR because they offer painless transdermal delivery, bypass first-pass metabolism, and boost patient compliance.

What is the biggest hurdle for commercial scale-up?

The limited range of GMP-grade excipients and evolving quality-by-design requirements pose the primary obstacles, extending validation timelines and raising costs.

Which therapeutic area is growing quickest?

Oncology is the fastest-growing segment, projected at an 18.2% CAGR through 2030, as personalised dosing is critical for complex cancer regimens.

Page last updated on: