Neurotechnology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

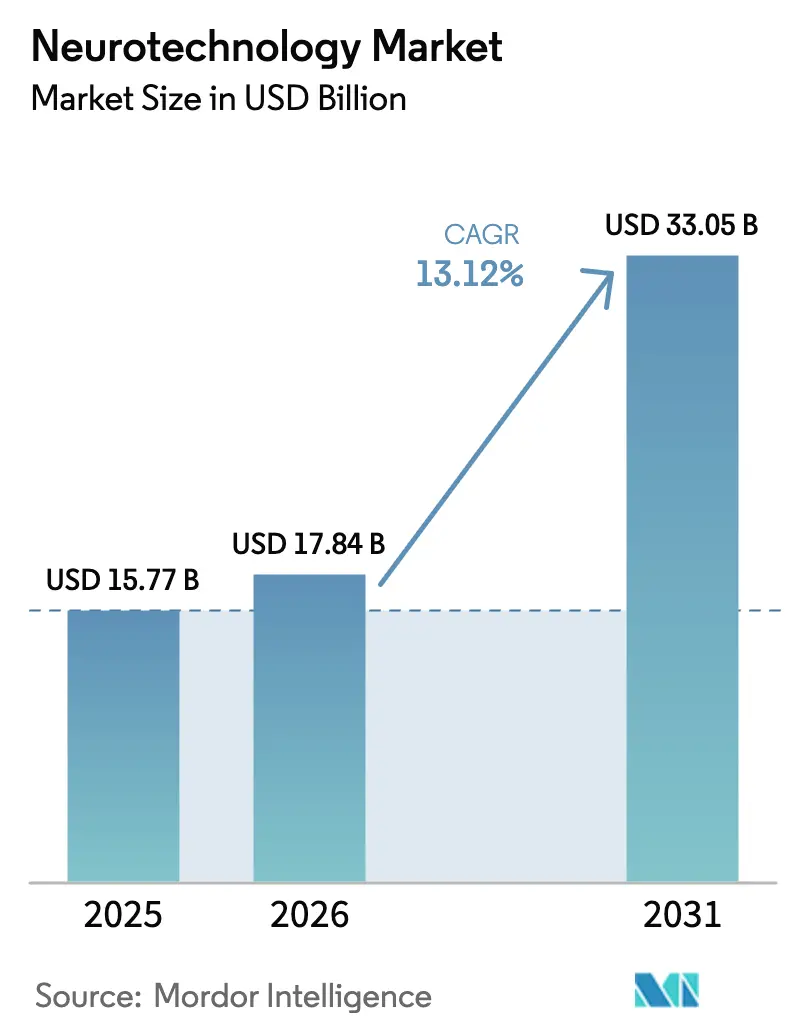

| Market Size (2026) | USD 17.84 Billion |

| Market Size (2031) | USD 33.05 Billion |

| Growth Rate (2026 - 2031) | 13.12% CAGR |

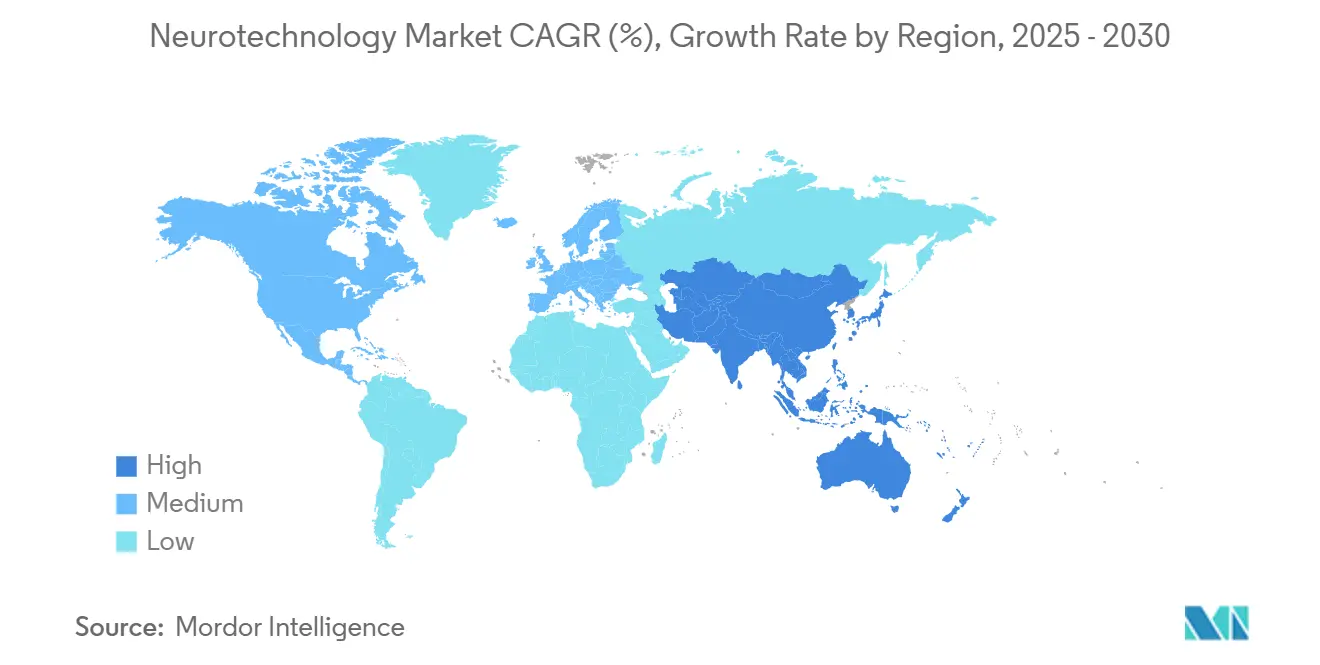

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

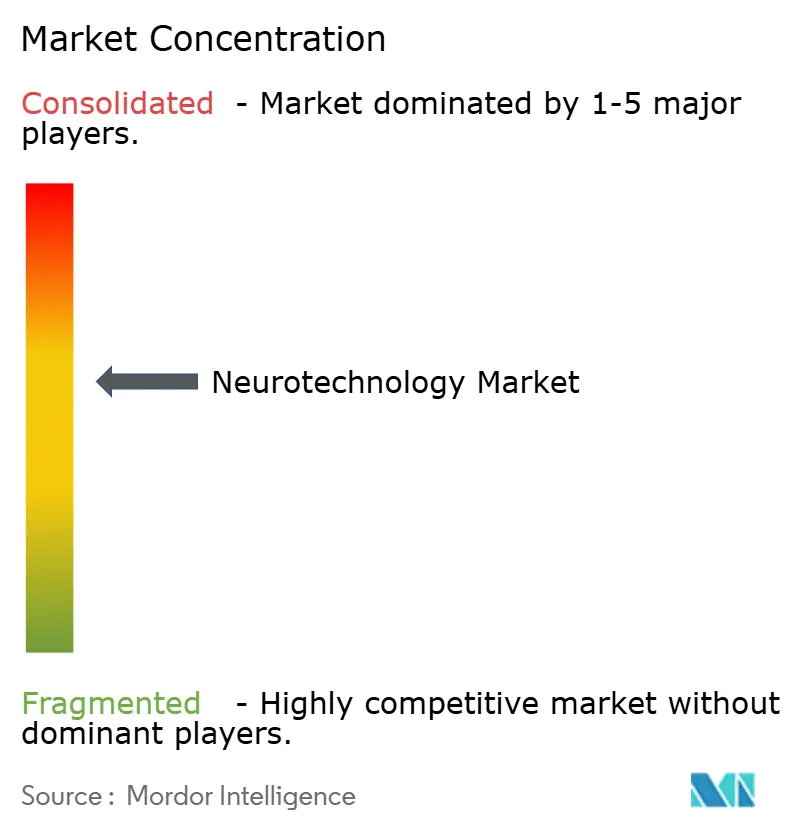

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurotechnology Market Analysis by Mordor Intelligence

The neurotechnology market size is expected to grow from USD 15.77 billion in 2025 to USD 17.84 billion in 2026 and is forecast to reach USD 33.05 billion by 2031 at 13.12% CAGR over 2026-2031. Growth is being propelled by rapid advances in brain-computer interfaces, expanding clinical validation for adaptive neuro-stimulation, and rising prevalence of neurological disorders in aging societies. Asia-Pacific adoption is climbing rapidly on the back of government-backed research initiatives, while North American reimbursement reforms are removing long-standing commercial hurdles. Competition is intensifying as technology multinationals collaborate with neural-interface start-ups to accelerate product iterations and access proprietary data streams. At the same time, regulatory bodies are refining approval pathways for novel neurotechnology categories, creating both opportunities for fast-track designation and challenges around post-market surveillance.

Key Report Takeaways

- By product type, neuro-stimulation devices commanded 45.21% of the neurotechnology market share in 2025, while brain-computer interfaces are projected to expand at a 15.98% CAGR to 2031.

- By application, chronic pain management accounted for 40.05% of the neurotechnology market size in 2025; depression and other neuro-psychiatric disorders record the highest projected CAGR at 15.07% through 2031.

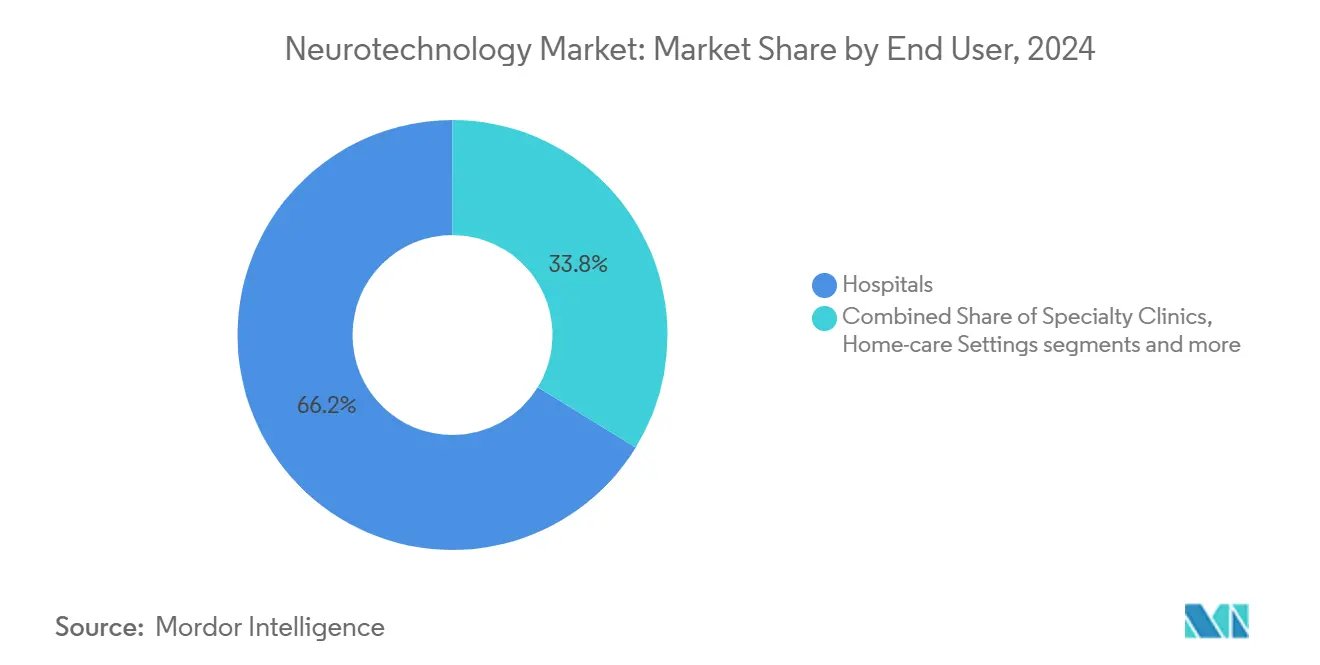

- By end user, hospitals held 65.79% of the neurotechnology market share in 2025, whereas home-care settings are expected to advance at a 14.02% CAGR between 2026 and 2031.

- By geography, North America generated 39.10% revenue in 2025; Asia-Pacific is forecast to be the fastest-growing region with a 14.94% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neurotechnology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of neurological disorders | +3.2% | Global | Long term (≥ 4 years) |

| Advancements in neuroscience and AI-enabled interfaces | +2.8% | North America, Europe, East Asia | Medium term (2-4 years) |

| Growing demand for improved treatment options | +2.4% | Global | Medium term (2-4 years) |

| Increasing public & private funding | +1.9% | Asia-Pacific, Europe, North America | Short term (≤ 2 years) |

| Shift toward minimally and non-invasive neuro-interventions | +1.6% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Emergence of consumer neurotechnology | +1.2% | North America, Europe, East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Neurological Disorders

The global burden of neurodegenerative diseases has surpassed 50 million cases and continues to climb in tandem with aging populations.[1]World Health Organization, “Neurological disorders: public health challenges,” who.int In the United States alone, Parkinson’s disease affects 5%–10% of the geriatric population each year, with roughly 500,000 new diagnoses annually.[2]National Institutes of Health, “Parkinson’s disease statistics,” nih.gov Health-system planners are moving capital toward early-intervention devices that can slow functional decline and lessen long-term care costs. This demographic reality underpins aggressive investment in early-stage brain-monitoring platforms positioned for future preventive protocols.

Surging Advancements in Neuroscience and Technology

Breakthroughs in microscale electrode arrays now allow sensors to sit between hair follicles while maintaining 96.4% signal-detection accuracy over prolonged use.[3]Georgia Institute of Technology, “Researchers unveil nearly invisible BCI,” techxplore.com Parallel gains in large-language-model-powered decoding have yielded prototypes capable of translating cortical signals into coherent speech. These innovations are widening the neurotechnology market by creating hybrid product classes that straddle consumer wearables and regulated medical devices.

Growing Demand for Improved Treatment Options

Pharmacological limitations in Parkinson’s and chronic pain are steering clinicians toward adaptive deep-brain and spinal-cord stimulation. Closed-loop spinal-cord stimulators that adjust therapy 50 times per second were cleared by the FDA in 2024, enabling 84% of patients to achieve ≥ 50% pain reduction at 12 months. Similar adaptive systems for movement disorders earned approval in 2025, underscoring how data-guided personalization is becoming the standard of care.

Rising Public & Private Funding for Neurotechnology R&D and Commercialization

Government agencies have elevated brain-computer interface (BCI) programs to national priority status. China’s 2025–2030 action plan lists BCI among its strategic industries, backed by dedicated grant lines and commercialization incentives. Venture financing remains robust, with multi-million-dollar rounds flowing into mid-stage neural-interface developers as early regulatory successes de-risk new business models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front device and procedure costs | -2.1% | Emerging economies | Medium term (2-4 years) |

| Complex multiregional regulatory approvals | -1.8% | Global | Long term (≥ 4 years) |

| Reimbursement gaps and limited skilled workforce | -1.6% | Asia-Pacific, Latin America, Africa | Medium term (2-4 years) |

| Limited clinical evidence and long-term data | -1.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-front Device & Procedure Costs Limiting Adoption Beyond Tier-1 Hospitals

Advanced neuromodulation platforms may cost more than USD 100,000, with implantable components adding USD 20,000–50,000 per patient. This expenditure confines deployments to academic centers and limits penetration in community settings. Insurance coverage is uneven, amplifying out-of-pocket burdens and dampening uptake in resource-constrained markets. Manufacturers are piloting risk-sharing and outcomes-based contracts, but these frameworks remain in formative stages.

Complex, Multiregional Regulatory Approvals Delaying Market Entry

Neurotechnology innovators must navigate divergent safety standards across the FDA, European CE Mark, and China’s National Medical Products Administration. Precision Neuroscience secured a 30-day clearance for its wireless cortical interface in 2025, yet requires additional trials for long-term implants. Such phased pathways extend time-to-market and absorb scarce capital. Smaller firms often lack dedicated regulatory teams, increasing the likelihood of staggered or region-specific launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Neuro-stimulation devices held 45.21% of the neurotechnology market in 2025, validating decades of clinical experience and established reimbursement. Adoption continues to rise as adaptive algorithms refine stimulation parameters in real time, reducing habituation and side-effects. Medtronic’s Inceptiv system senses bodily responses 50 times per second to maintain therapeutic thresholds. This convergence of sensing and stimulation is nudging the neurotechnology market size associated with implantable systems toward steady mid-teens expansion.

Brain-computer interfaces (BCIs) are scaling faster, supported by advances in minimally invasive electrode design and cloud-based decoding. The segment’s 15.98% projected CAGR makes it the neurotechnology market’s fastest mover, attracting partnerships between medical device firms and consumer electronics leaders. Integration with mixed-reality headsets signals potential spill-over into mainstream health monitoring, providing fresh revenue channels beyond clinical neurology. Co-development frameworks are emerging in which hardware, firmware, and data-analytics IP are shared to accelerate iteration cycles.

Chronic pain management commands the largest slice of the neurotechnology market size, accounting for 40.05% of 2025 revenue. Closed-loop spinal-cord systems extend pain relief durability and have allowed many patients to return to work without opioid reliance. Payers view the reduced downstream costs—lower addiction rates and fewer hospitalizations—as justification for coverage, safeguarding the segment’s revenue base.

Depression and broader neuro-psychiatric indications are growing at 15.07% through 2031, catalyzed by non-invasive neuro-stimulation modalities that can be administered in outpatient settings. Prefrontal-cerebellar transcranial pulsed-current stimulation improved social functioning in children with autism spectrum disorder during randomized trials. Regulatory momentum is building for psychiatric devices, and ongoing studies aim to formalize dosing protocols, further broadening the addressable population.

Hospitals retained 65.79% of 2025 revenue owing to their expertise in device implantation, programming, and acute monitoring. Leading academic centers leverage integrated care teams that combine neurology, psychiatry, and rehabilitation to optimize outcomes. However, cost pressures and staffing constraints are motivating providers to shift appropriate follow-up to outpatient settings.

Home-care environments exhibit a 14.02% CAGR as compact, connected neurotechnology devices enable clinician oversight without requiring in-person visits. Elderly patients show a rising willingness to adopt remote monitoring when family caregivers are present. Telerehabilitation platforms that pair BCIs with functional electrical stimulation have demonstrated recruitment rates above 80% and retention rates near 88% in stroke populations. These results underscore a growing evidence base supporting decentralized neurological care models.

Segment Analysis

Segment 1

North America generated 39.10% of global revenue in 2025 on the strength of a mature clinical infrastructure, active venture capital, and an accelerating FDA Breakthrough Devices program. Approvals such as the world’s first adaptive deep-brain stimulation system for Parkinson’s patients illustrate regulators’ willingness to fast-track transformative solutions. Strategic alliances linking hospital systems with technology firms are proliferating, enabling rapid validation of neural-data-driven digital therapeutics.

Asia-Pacific is the neurotechnology market’s fastest-growing region at a 14.94% CAGR through 2031. China’s national BCI strategy has catalyzed cross-sector consortia that pair academic labs with semiconductor manufacturers, resulting in real-time decoding of Chinese speech at sub-100-millisecond latency. Government funding, manufacturing agility, and large domestic patient pools are shortening product-development cycles. Parallel innovation in Japan and South Korea, leveraging sensor miniaturization expertise, is producing export-ready non-invasive neuro-monitoring devices.

Europe maintains stringent regulatory oversight, but its emphasis on long-term safety data has fostered pioneering neuromodulation protocols for movement disorders. The United Kingdom’s National Health Service is trialing an ultrasound-enabled BCI for mood modulation under an USD 8 million value-based framework. National reimbursement agencies are actively evaluating cost-effectiveness models that could unlock broader adoption once outcome thresholds are met.

Competitive Landscape

The neurotechnology market features moderate concentration: with Medtronic, Abbott, and Boston Scientific leading through diversified device portfolios and worldwide service networks. Each is investing in software-centric enhancements that transform static implants into data-rich platforms capable of learning from patient-specific neural signatures.

Emerging competitors specialize in thin-film electrodes, wireless power, and cloud-based analytic engines. Technology conglomerates are increasingly active: Meta’s acquisition of CTRL-Labs and Apple-compatible BCIs developed by Synchron underscore the convergence between consumer wearables and regulated neuro-therapeutics.

Competitive differentiation now revolves around data stewardship, privacy safeguards, and algorithmic transparency. Firms that can securely harness longitudinal neural datasets are positioned to offer adaptive therapeutics and subscription-style software upgrades. Regulatory frameworks such as 21 CFR Part 882 mandate strict performance and biocompatibility standards, but evolving guidance on AI/ML platforms will shape future product classifications.

Neurotechnology Industry Leaders

Abbott

Boston Scientific

Medtronic

Cochlear Ltd.

LivaNova PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: University of Chicago scientists advanced neuroprosthetics by providing tactile feedback through targeted brain stimulation.

- March 2025: Cognixion launched a clinical trial to evaluate its Axon-R headset, a non-invasive brain-computer interface designed to assist late-stage ALS patients in communication without requiring eye movement.

- February 2025: Researchers at Tsinghua University and Tianjin University unveiled a two-way adaptive BCI leveraging memristor-based neuromorphic decoding that boosts efficiency 100-fold.

- August 2024: The FDA approved the Altius Direct Electrical Nerve Stimulation System for alleviating chronic phantom limb and residual limb pain in adult amputees.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the neurotechnology market as the global revenue generated from equipment and integrated software that record, stimulate, or translate neural activity, including neuro-stimulation systems, brain-computer interfaces, neuro-prosthetics, and dedicated neuro-imaging platforms, sold to healthcare providers, research institutes, and home-care settings. The definition deliberately centers on hardware-driven value because device purchases and associated software licenses are the clearest, auditable flows of spending that an analyst can track.

Pure pharmaceutical sales, generic radiology consumables, and consultancy-only services lie outside this study's boundaries.

Segmentation Overview

- By Product

- Neuro-stimulation Devices

- Deep Brain Stimulation (DBS)

- Spinal Cord Stimulation (SCS)

- Vagus Nerve Stimulation (VNS)

- Sacral Nerve Stimulation (SNS)

- Transcranial Magnetic Stimulation (TMS)

- Others

- Brain-Computer Interfaces

- Invasive BCI

- Semi-invasive BCI

- Non-invasive BCI

- Neuro-prosthetics

- Output Neural Prosthetics

- Input Neural Prosthetics

- Other Products

- Neuro-stimulation Devices

- By Application

- Parkinson’s Disease

- Epilepsy

- Alzheimer’s and Dementia

- Chronic Pain Management

- Stroke and Motor Rehabilitation

- Depression and Other Neuro-psychiatric Disorders

- By End User

- Hospitals

- Specialty Clinics

- Home-care Settings

- Research and Academic Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed neurosurgeons, hospital procurement heads, neuro-device start-ups, and reimbursement analysts across North America, Europe, and Asia Pacific. These conversations clarified real-world implant rates, average selling prices, and likely adoption curves, allowing us to refine assumptions flagged during desk work.

Desk Research

Our analysts begin with tier-1 public sources such as the World Health Organization's neurological burden statistics, US FDA 510(k) device approvals, OECD health-expenditure tables, and population projections from the United Nations. Trade bodies such as the Neurotech Network and IEEE Brain Initiative provide installation counts and standards updates, while peer-reviewed journals in Nature Neuroscience help us map emerging clinical indications. For commercial color, we extract company financials through D&B Hoovers and screen shipment records on Volza. All other paywalled and open datasets consulted are too numerous to list here and support only foundational cross-checks.

Market-Sizing & Forecasting

The model starts with a top-down reconstruction of installed bases and annual procedure volumes, which are then multiplied by replacement cycles and average selling prices. Selective bottom-up checks, supplier shipment tallies and channel audits, validate totals before adjustments. Key variables include aging population growth, Parkinson's and epilepsy prevalence, reimbursement expansion milestones, average device ASP movement, and annual FDA/CE approvals. Multivariate regression, supplemented by scenario analysis where policy shifts loom, drives the 2025-2030 forecast. Gaps in shipment data are bridged with regional penetration proxies benchmarked in primary calls.

Data Validation & Update Cycle

Outputs pass variance tests against external sales disclosures, patent-filing spikes, and hospital capital-budget trends. A second analyst reviews anomalies, and we refresh every twelve months, with interim updates triggered by material device approvals or regulatory changes.

Why Mordor's Neurotechnology Baseline Earns Trust

Published estimates often differ because each publisher selects its own scope, pricing basis, and refresh cadence.

We make those choices explicit so readers can trace every figure back to auditable inputs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.77 B (2025) | Mordor Intelligence | - |

| USD 17.32 B (2025) | Global Consultancy A | Includes neuro-rehabilitation services and imaging consumables outside our hardware focus |

| USD 15.35 B (2024) | Industry Association B | One-year older base and relies mainly on self-reported vendor revenue without hospital spend validation |

| USD 15.38 B (2024) | Trade Journal C | Broad scope and limited primary interviews, leading to higher uncertainty in device ASPs |

The comparison shows that scope creep, timing, and limited field checks drive most disparities. By anchoring numbers to clearly defined hardware revenue streams, refreshing annually, and verifying assumptions with front-line experts, Mordor Intelligence delivers a balanced baseline decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the present market size and growth rate of the neurotechnology market over 2026-2031?

The neurotechnology market is valued at USD 17.84 billion in 2026 and is expected to grow at rate of 13.12% CAGR over the 2026-2031.

Which product area is attracting the most venture-capital interest in neurotechnology?

Early-stage brain-computer interface platforms—especially thin-film cortical arrays and wireless decoders—are drawing the largest share of private funding because they promise new communication and mobility solutions for severe paralysis.

How are consumer electronics firms influencing competition in neurotechnology?

Technology giants are partnering with or acquiring neuro-interface startups, adding cloud analytics and user-experience design skills that speed product iterations and blur the line between medical devices and everyday wearables.

What regulatory developments could streamline neurotechnology commercialization?

Efforts by major agencies to create specific guidance for neural interfaces, along with expanding breakthrough-device programs, are expected to shorten review cycles and reduce redundant safety tests across multiple regions.

Why is Asia-Pacific emerging as a hotspot for neurotechnology R&D?

National brain-science initiatives, generous public grants and growing domestic manufacturing capacity are enabling rapid prototyping and clinical trials, positioning regional firms at the forefront of neural-signal decoding breakthroughs

How is home-based neurotechnology reshaping care delivery models?

Wearable neurofeedback and non-invasive stimulation devices allow long-term monitoring and therapy outside hospital walls, reducing travel burdens for patients and freeing up specialist resources for complex implant procedures.

Page last updated on: