Protein Engineering Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

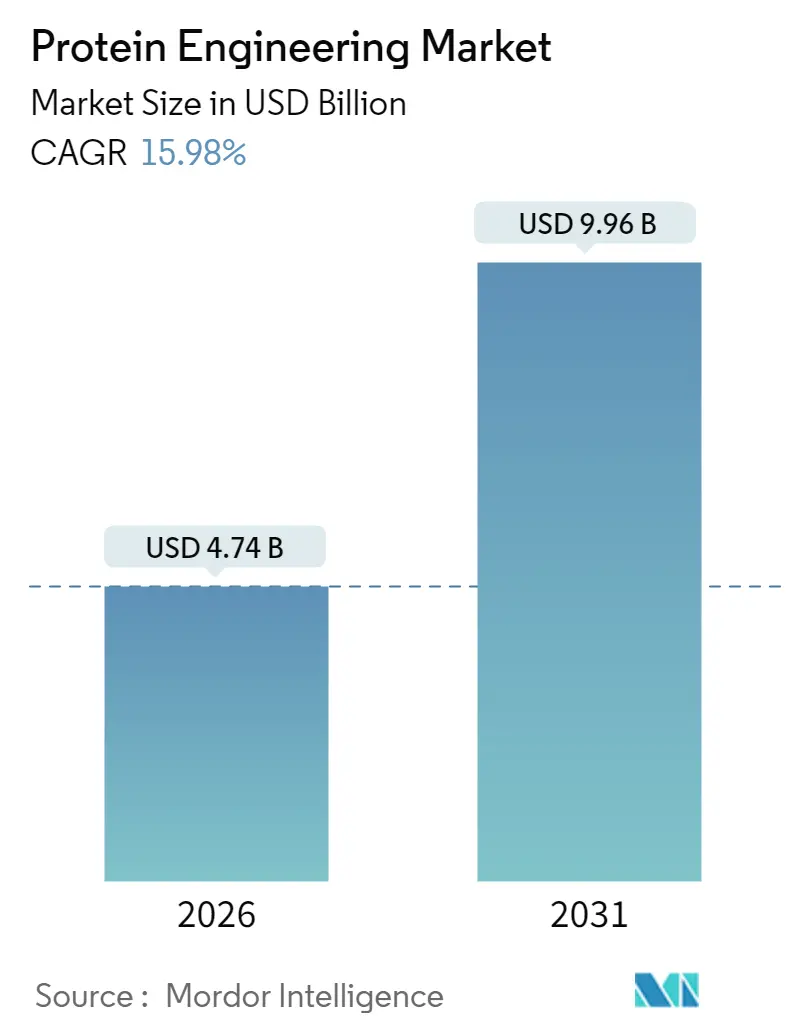

| Market Size (2026) | USD 4.74 Billion |

| Market Size (2031) | USD 9.96 Billion |

| Growth Rate (2026 - 2031) | 15.98% CAGR |

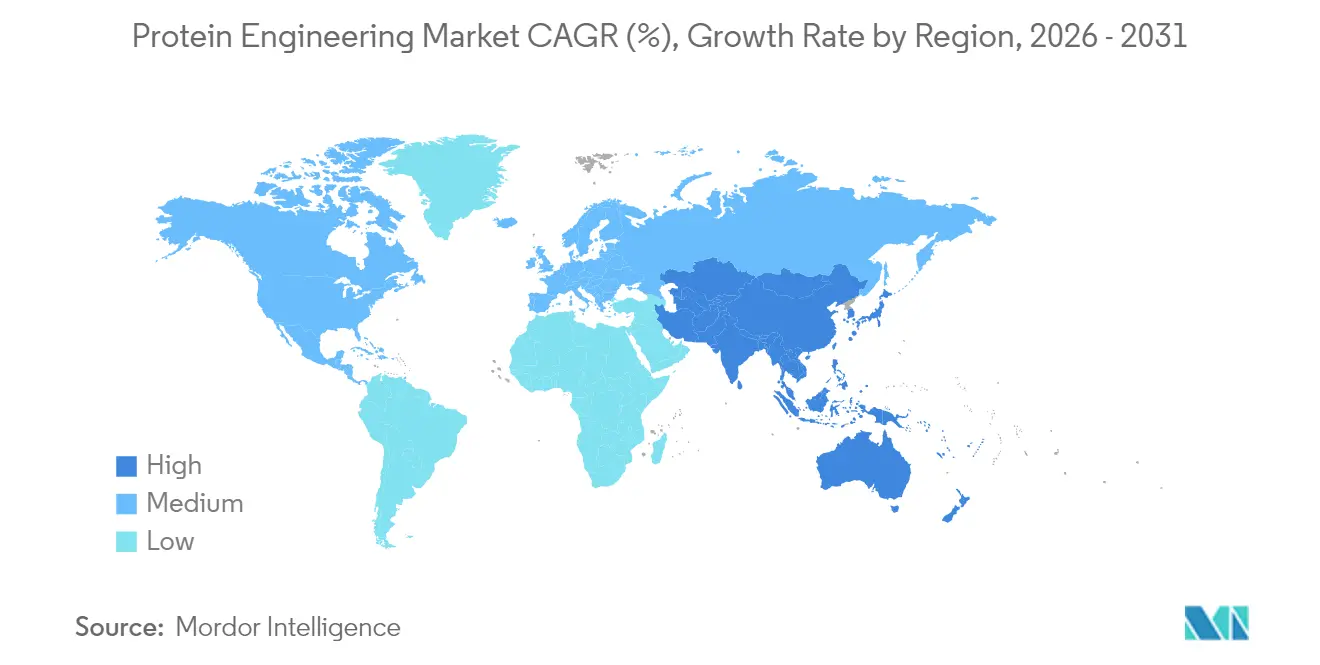

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Protein Engineering Market Analysis by Mordor Intelligence

The global protein engineering market size in 2026 is estimated at USD 4.74 billion, growing from 2025 value of USD 4.09 billion with 2031 projections showing USD 9.96 billion, growing at 15.98% CAGR over 2026-2031. This strong expansion reflects a decisive move away from traditional trial-and-error methods toward AI-enabled design platforms, faster regulatory pathways for biologics, and sustained public-sector funding. Rapid advances in in-silico modeling, exemplified by Google DeepMind’s AlphaProteo system that delivers binding affinities up to 300-fold better than earlier techniques, are compressing development cycles and widening the addressable opportunity for therapeutics. Demand also benefits from chronic-disease prevalence, the success of mRNA technology in prophylactic and therapeutic vaccines, and growing outsourcing to contract research organizations that can provide specialized expertise without heavy capital requirements. Competitive dynamics are shifting as incumbent instrument suppliers strengthen digital capabilities while AI-native startups enter with significant venture funding and billion-dollar collaborations, signalling an ecosystem in flux yet rich in partnership opportunities.

Key Report Takeaways

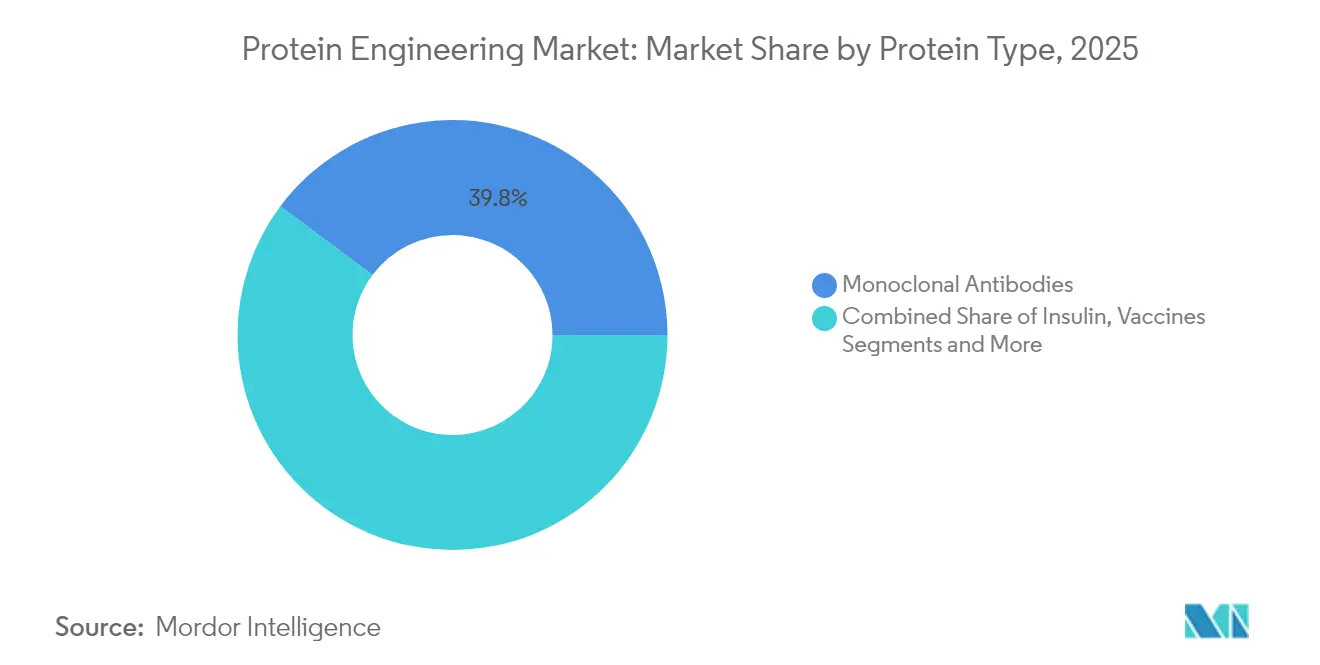

- By protein type, monoclonal antibodies held 39.78% of the protein engineering market share in 2025, while vaccines are projected to advance at an 18.07% CAGR to 2031.

- By product & service, consumables led with 51.92% revenue share in 2025; software and services are set to grow the fastest at a 19.55% CAGR through 2031.

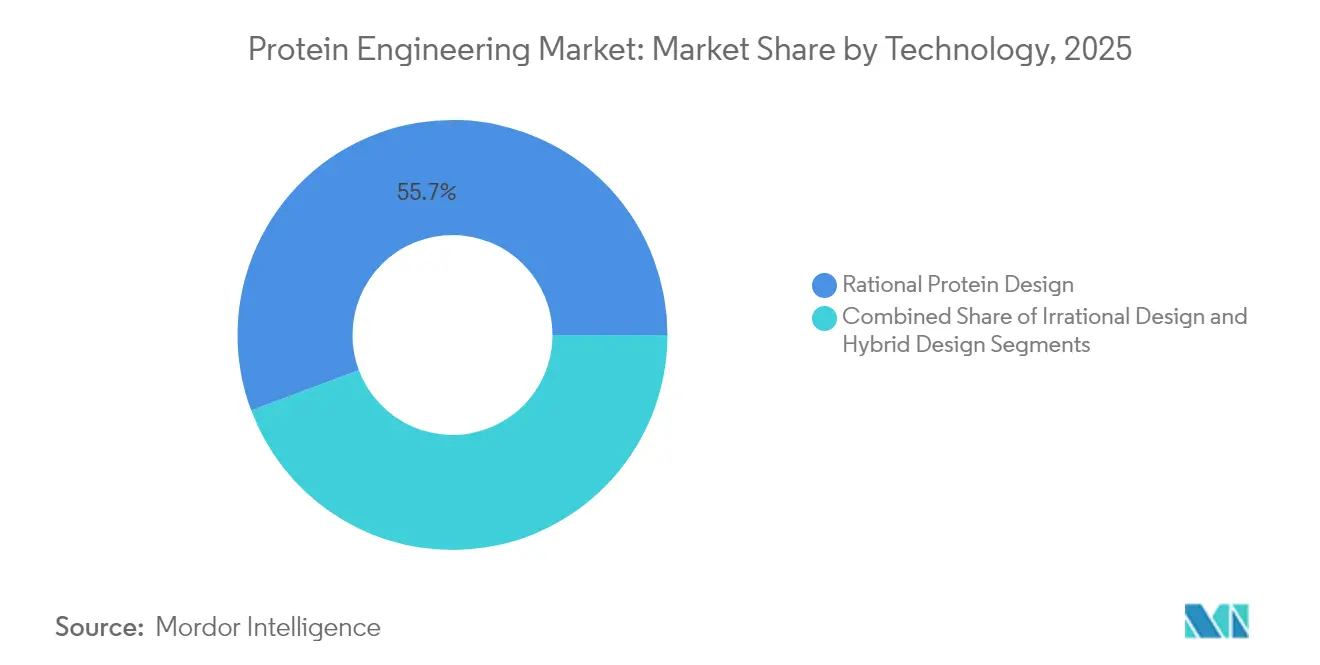

- By technology, rational design dominated with 55.72% share of the protein engineering market size in 2025, yet hybrid semi-rational approaches will post the quickest pace at 18.19% CAGR over the same horizon.

- By end user, pharmaceutical and biotechnology companies accounted for 48.42% of 2025 revenue, whereas contract research organizations are forecast to expand at an 18.39% CAGR to 2031.

- By geography, North America commanded 44.32% of 2025 revenue; Asia-Pacific is projected to grow at a 19.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Protein Engineering Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Monoclonal Antibody (Mab) Commercialization | +4.2% | Global, with North America & Europe leading | Medium term (2-4 years) |

| AI-Driven In-Silico Protein Design Platforms | +3.8% | Global, concentrated in US, UK, China | Short term (≤ 2 years) |

| Growing Chronic-Disease Burden Demanding Biologics | +3.1% | Global, accelerated in aging populations | Long term (≥ 4 years) |

| Government & VC Funding For Synthetic-Biology Start-Ups | +2.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Cell-Free Protein Synthesis Enabling Rapid Prototyping | +2.4% | Global, early adoption in biotech hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Monoclonal Antibody Commercialization

Monoclonal antibodies continue to headline late-stage pipelines, with forecasts pointing to USD 315 billion in annual sales by 2025, propelled by accelerated FDA approvals and expanded indications beyond oncology. Bispecific formats now comprise a notable share of new filings, and recent clearances such as Merck’s clesrovimab for RSV prevention underscore the therapeutic breadth. Manufacturing innovation is lowering cost-of-goods, exemplified by Sutro Biopharma’s commercial-scale cell-free expression of an antibody–drug conjugate. These gains improve patient access and reinforce the revenue base for the protein engineering market.

AI-Driven In-Silico Protein Design Platforms

Artificial intelligence is compressing discovery timelines from years to months. AlphaProteo has shown 300-fold affinity improvements over legacy techniques[1]Artificial Intelligence News, “AlphaProteo: Google DeepMind Unveils Protein Design System,” artificialintelligence-news.com. Generate:Biomedicines’ Chroma validated 310 experimentally tested proteins with favorable properties, underpinning a USD 1 billion multi-target deal with Novartis. Technical University of Munich researchers extended AlphaFold2 to 1,000-amino-acid designs, bridging a gap between prediction and custom sequence generation. Collective advances position AI as a primary engine of growth for the protein engineering market.

Growing Chronic-Disease Burden Demanding Biologics

An aging world population is escalating demand for disease-modifying biologics. The FDA now expects 10–20 cell- and gene-therapy approvals annually by 2025. Expanded indications such as Elevidys for Duchenne muscular dystrophy illustrate how novel proteins can address rare yet serious conditions[2]Food and Drug Administration, “A Novel Method for Rapid Glycan Profiling of Therapeutic Monoclonal Antibodies,” fda.gov. Fusion protein formats in diabetes therapy exploit Fc fragments and albumin to extend half-life, boosting patient adherence. The shift toward biologics sustains a demand tailwind that supports expansion of the protein engineering market.

Government and VC Funding for Synthetic-Biology Start-Ups

Public and private capital inflows are enlarging the innovation base. The U.S. National Science Foundation committed USD 40 million to a new protein design acceleration program[3]National Science Foundation, “New $40M Funding Opportunity Accelerates the Translation of Novel Approaches to Protein Design,” nsf.gov. The United Kingdom pledged GBP 100 million (USD 125 million) toward engineering-biology infrastructure. East-Asian biotech ventures raised USD 471 million in 2024 despite broader funding softness, showing resilience in the region. Abundant financing accelerates tech transfer, enriches deal flow and broadens participation in the protein engineering market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Instruments & Specialty Reagents | -2.1% | Global, acute in emerging markets | Medium term (2-4 years) |

| Complex IP & Freedom-To-Operate Hurdles | -1.8% | Global, concentrated in US & Europe | Long term (≥ 4 years) |

| Sustainability & Regulatory Scrutiny Of Bioprocess Waste | -1.3% | Global, stringent in EU & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Instruments and Specialty Reagents

Sophisticated equipment, single-cell proteomics workflows and proprietary reagents keep capital intensity high. Single-cell protein analysis can range from under USD 2 to more than USD 50 per cell depending on throughput. Industry estimates point to multibillion-dollar investment needs to bring novel proteins to scale, a burden that smaller firms often mitigate by outsourcing or sharing facilities. Robotics-enabled, low-cost enzyme discovery pipelines are beginning to narrow cost gaps by automating tedious tasks. While these innovations ease pressure, high upfront spending remains a moderating force on the protein engineering market.

Complex IP and Freedom-to-Operate Hurdles

A dense patent landscape can impede speed to market and add litigation risk. The CRISPR patent dispute between the University of California and Broad Institute shows how ownership uncertainties can linger for a decade. Patent‐challenge victories such as the PTAB’s invalidation of Moderna vaccine claims illustrate vulnerability even for leaders. Policy moves like the proposed BIOSECURE Act could restrict cross-border collaboration and inject additional complexity into global supply chains. As design-around strategies consume time and resources, IP friction weighs on new entrants to the protein engineering market.

Segment Analysis

By Protein Type: Monoclonal Antibodies Sustain Leadership

Monoclonal antibodies retained 39.78% of 2025 revenue, securing the largest slice of the protein engineering market. Sustained regulatory approvals, broadening indications and manufacturing advances such as cell-free expression keep entry barriers high while cementing commercial predictability. Vaccines are set to register an 18.07% CAGR through 2031, leveraging mRNA versatility to deliver rapid antigen design and robust immunogenicity. Continued investment in bispecifics and antibody-drug conjugates further fortifies the segment’s pipeline resilience.

The vaccine opportunity gains momentum from pandemic preparedness spending, with AI-directed antigen design accelerating candidate selection. Insulin and coagulation factors remain mature but evolve through long-acting formulations and gene-therapy alternatives. Growth factors and fusion proteins address regenerative medicine and metabolic disease niches, supported by regulatory initiatives such as the FDA’s rapid glycan-profiling method that improves quality oversight. Collectively, these developments reinforce the expansion trajectory of the protein engineering market.

Note: Segment shares of all individual segments available upon report purchase

By Product & Service: Digital Platforms Accelerate Spending

Consumables generated 51.92% of 2025 revenue, underscoring the recurring demand for reagents and kits across laboratory workflows. Yet software and services are projected to scale fastest at a 19.55% CAGR, signifying an industry pivot toward AI-enabled modeling and cloud-based collaboration. The protein engineering market size for software and services is expected to outpace hardware budgets as algorithms replace brute-force screening.

Compute-rich approaches lower the barrier for smaller entities to participate. Generate:Biomedicines’ billion-dollar alliance with Novartis and Cradle’s USD 73 million Series B reflect confidence that algorithmic design can shorten discovery timelines. Instruments still see steady upgrades, highlighted by Thermo Fisher’s USD 3.1 billion Olink acquisition that deepens next-generation proteomics. As hardware integrates with digital platforms, synergy will drive the next efficiency leap within the protein engineering market.

By Technology: Hybrid Semi-Rational Methods Gain Ground

Rational design held 55.72% of 2025 revenue, benefiting from reliable structure-guided mutagenesis and an extensive knowledge base. However, hybrid semi-rational workflows that blend directed evolution with AI-supported prediction are forecast to expand at an 18.19% CAGR to 2031. The protein engineering market size for hybrid approaches is set to grow as labs adopt iterative design-build-test-learn cycles that accelerate optimization.

Advances such as gradient-descent sequence refinement coupled with AlphaFold2 predictions demonstrate high-complexity proteins can now be drafted in silico before empirical screening. Deep-learning language models like ESM-2 and ProtGPT2 generate de novo sequences that self-assemble into functional folds. With high-throughput cell-free assays bringing confirmation in hours, hybrid strategies will capture an increasing share of the protein engineering market.

Note: Segment shares of all individual segments available upon report purchase

By End User: CROs Capture Outsourcing Wave

Pharmaceutical and biotechnology firms accounted for 48.42% of 2025 sales, tapping internal platforms for strategic assets. Contract research organizations, projected to grow at an 18.39% CAGR, are emerging as critical partners that deliver specialty expertise without capital outlay. Lonza’s acquisition of Roche’s 330,000-liter Vacaville plant and its GS Xceed gene-expression platform underscore the scale of resources now available on a fee-for-service basis. The protein engineering market continues to decentralize as startups and mid-cap developers rely on CRO programs that promise 11 months from DNA to IND for monoclonal antibodies.

Academic centers and government labs remain essential innovation nodes, while small biotechnology enterprises leverage shared facilities to conserve cash. Animal-health applications provide an incremental opportunity, showcased by Absci’s partnership with Invetx to adapt generative AI for veterinary antibodies. Together these users diversify demand across the protein engineering market.

Geography Analysis

North America led the protein engineering market with a 44.32% revenue contribution in 2025, anchored by the United States’ mature venture ecosystem, premier academic research and FDA policies that reward innovation. Federal programs such as DARPA’s Switch initiative and the NSF’s USD 40 million protein-design grant pool amplify the regional advantage. Biopharma manufacturers are reinforcing supply chains through large domestic builds; Eli Lilly and Novo Nordisk together earmarked USD 6.1 billion for new facilities in North Carolina that will support GLP-1 production. The protein engineering market benefits from proximity between discovery labs, regulators and scalable production capacity.

Asia-Pacific is forecast to grow at 19.41% CAGR, the fastest regional clip through 2031. China’s commitment to biotech self-sufficiency yielded USD 471 million in 2024 start-up funding despite capital-market headwinds. South Korea is pairing fermentation expertise with agricultural innovation, while Australia’s CSIRO projects a USD 30 billion synthetic-biology industry by 2040 supported by USD 44.5 million in recent grants. Japan’s ecosystem lags due to pricing pressures, yet domestic champions such as Chugai delivered record 2024 revenue on the strength of proprietary antibody technologies. These developments collectively sharpen Asia-Pacific’s stake in the protein engineering market.

Europe remains an influential node, supported by coordinated policy and a strong academic network. The EU’s 2024 “Building the Future with Nature” blueprint promotes biotechnology sovereignty and sustainability. The United Kingdom’s GBP 100 million (USD 125 million) engineering-biology program accelerates pandemic readiness, while Nuclera’s GBP 1.14 million (USD 1.4 million) Innovate UK grant exemplifies seed-stage support for rapid protein expression tools. The Netherlands’ EUR 60 million (USD 65 million) cellular-agriculture fund extends biotech principles into food systems. These initiatives maintain Europe’s competitiveness and diversify the global footprint of the protein engineering market.

Competitive Landscape

Competition is intensifying as incumbent instrument suppliers meet a cohort of AI-first entrants. Thermo Fisher Scientific deepened its analytics stack by purchasing Olink for USD 3.1 billion and plans up to USD 50 billion in future M&A. Simultaneously, the firm is allocating USD 2 billion to U.S. manufacturing expansion, positioning itself for end-to-end customer engagement. Generate:Biomedicines, BigHat, Absci and AI Proteins have attracted nine-figure deals from Novartis, Bristol Myers Squibb and other pharmaceutical majors, signaling a validation shift toward generative design capabilities biospace.com.

Emerging white-space segments include single-molecule protein sequencing, projected as a USD 75 billion longer-term opportunity. Cell-free and plant-based expression systems are gaining traction for both therapeutics and food applications, demonstrated by Taiyo Nippon Sanso’s commercial cytokine launch at >95% purity. Asimov and others are promoting low-footprint bioprocessing that avoids steel-tank fermentation, broadening manufacturing optionality.

Regulatory levers remain strategic. The FDA’s determination of additional patent-extension time for POMBILITI shows that exclusivity remains a policy tool able to tilt commercial outcomes. As IP rights and fast-track reviews interlace, companies that can secure both algorithmic advantage and regulatory know-how are poised to shape the evolution of the protein engineering market.

Protein Engineering Industry Leaders

Amgen Inc.

Bio-Rad Laboratories Inc.

Agilent Technologies Inc.

Eli Lilly and Company

Bruker Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Taiyo Nippon Sanso commercialized >95%-purity Human IL-1β and Human Oncostatin M via cell-free synthesis, demonstrating scalable reagent production.

- February 2025: Harbour BioMed partnered with Insilico Medicine to merge Harbour Mice antibody platforms with AI-driven discovery for immunology, oncology and neuroscience targets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global protein engineering market as all revenue that manufacturers and service providers earn from instruments, reagents, kits, software, and related services enabling rational, directed evolution, or hybrid redesign of therapeutic, diagnostic, and industrial proteins, including monoclonal antibodies, insulin, vaccines, coagulation factors, and growth factors, across every end-user group worldwide.

Scope exclusion: bulk functional food proteins and commodity home-care enzymes are not counted.

Segmentation Overview

- By Protein Type

- Monoclonal Antibodies

- Insulin

- Coagulation Factors

- Vaccines

- Growth Factors

- Other Protein Types

- By Product & Service

- Instruments

- Consumables (Reagents & Kits)

- Software & Services

- By Technology

- Rational Protein Design

- Irrational / Directed-Evolution Design

- Hybrid / Semi-Rational Design

- By End User

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutions

- Contract Research Organizations

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured calls and short surveys with bioprocess engineers, CRO managers, reagent distributors, and academic group heads across North America, Europe, and Asia-Pacific. These discussions clarified capacity utilization, average selling prices, and upcoming regulatory milestones, closing gaps left by desk work.

Desk Research

We began by mining publicly available biotech datasets, FDA Biologics License files, EMA product lists, WHO INN registries, and OECD biotechnology outlooks, which framed the approved base and late-stage pipeline. Extra texture came from BIO statistics, UN Comtrade customs lines, Questel patent counts, and company 10-Ks housed in D&B Hoovers, letting us sketch price corridors and regional adoption curves. The sources named are illustrative; many additional records informed verification.

Market-Sizing & Forecasting

We apply a top-down reconstruction that starts with approved and late-stage pipeline proteins, multiplies them by typical production scale and price bands, and then adjusts for regional penetration, trade flows, and outsourcing ratios. Supplier roll-ups and sampled ASP times volume checks give bottom-up counterpoints that fine-tune totals. Variables fed into our multivariate regression include biologics R&D spend, GMP cell-culture capacity, granted rational-design patents, and CRO outsourcing share; scenario analysis projects results from 2025 to 2030 while midpoint interpolation resolves price opacity.

Data Validation & Update Cycle

Outputs clear automated variance scans and a two-layer peer review before sign-off. Material events trigger interim refreshes, and full datasets rebuild each year so clients receive the latest view.

Why Mordor's Protein Engineering Baseline Commands Confidence

Published estimates often diverge because firms select different product bundles, price files, and refresh cadences, and protein revenue can swing sharply when a single biologic launches or a reagent list price moves.

Key gap drivers we observe are omission of software and services, inclusion of peripheral synthetic biology tools, and narrow regional sampling.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.09 B (2025) | Mordor Intelligence | - |

| USD 3.09 B (2024) | Global Consultancy A | Excludes software and services; older pricing |

| USD 4.35 B (2024) | Trade Journal B | Adds adjacent synthetic biology tooling |

| USD 3.02 B (2024) | Regional Consultancy C | Limited geographic coverage |

These contrasts show that our disciplined scope selection, dual-path validation, and annual refresh cycle give decision-makers a transparent baseline that is easy to reproduce with clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current size of the protein engineering market?

The protein engineering market is valued at USD 4.74 billion in 2026 and is projected to reach USD 9.96 billion by 2031.

Which protein type holds the largest share in the protein engineering market?

Monoclonal antibodies lead with 39.78% share in 2025 on the back of broad therapeutic adoption.

Which region is growing the fastest?

Asia-Pacific is forecast to expand at a 19.41% CAGR through 2031 owing to government incentives and strong private investment.

Why are AI platforms important for the protein engineering industry?

AI-driven design platforms dramatically shorten discovery timelines and improve binding affinity, thereby lowering risk and cost.

What segment is the fastest-growing by product & service?

Software and services, including cloud-based modeling and analytics, are expected to grow at a 19.55% CAGR.

How does outsourcing influence market growth?

The rapid rise of contract research organizations enables small and mid-size firms to access high-end capabilities, fueling an 18.39% CAGR in the CRO end-user segment.