Glycomics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

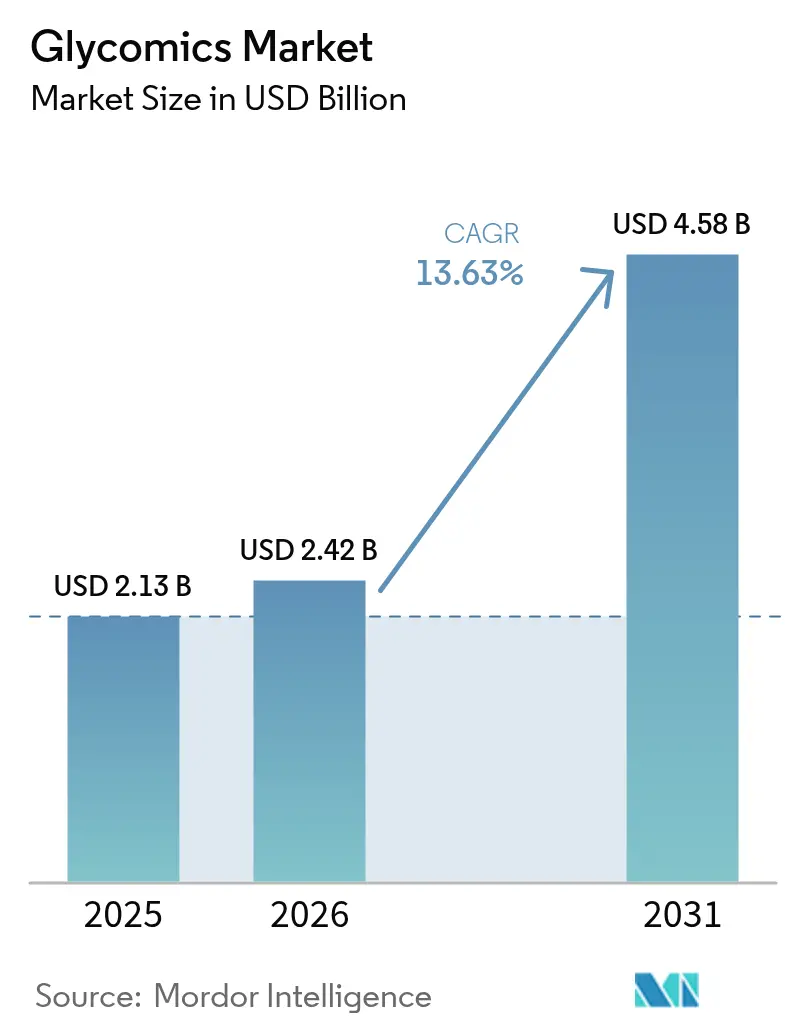

| Market Size (2026) | USD 2.42 Billion |

| Market Size (2031) | USD 4.58 Billion |

| Growth Rate (2026 - 2031) | 13.63% CAGR |

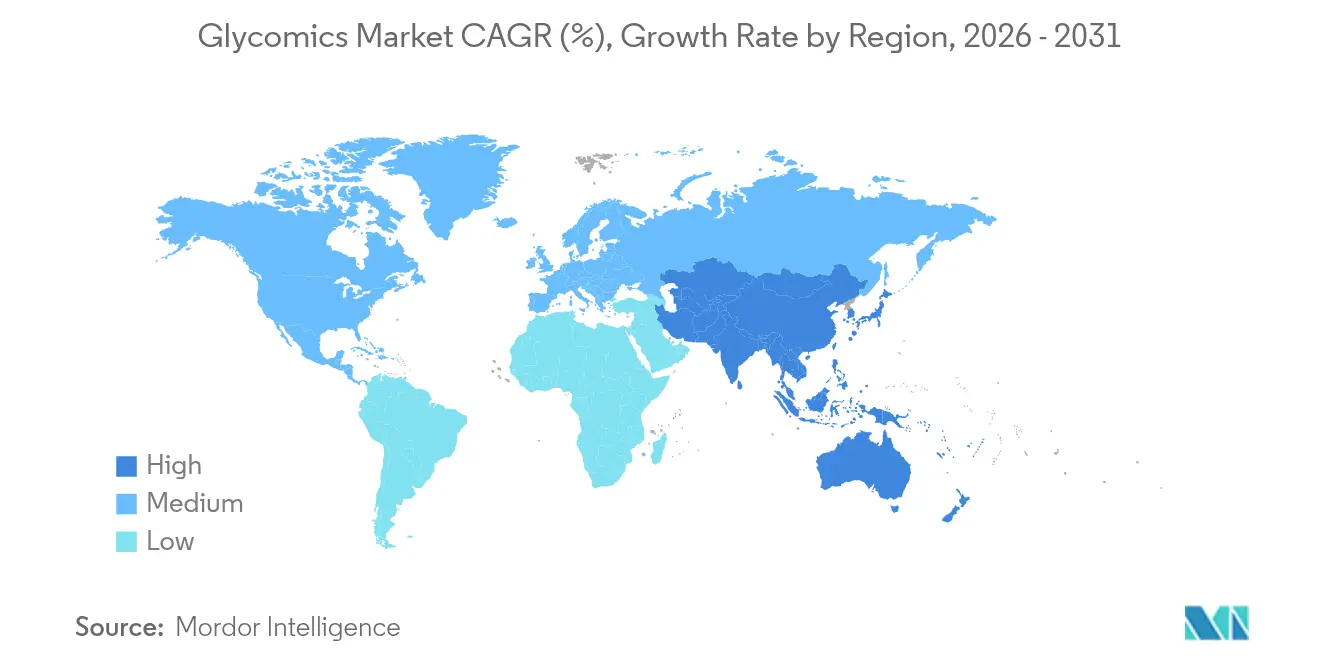

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glycomics Market Analysis by Mordor Intelligence

The glycomics market size was valued at USD 2.13 billion in 2025 and estimated to grow from USD 2.42 billion in 2026 to reach USD 4.58 billion by 2031, at a CAGR of 13.63% during the forecast period (2026-2031). Momentum comes from the convergence of advanced mass-spectrometry, AI-driven informatics, and the demand for novel biomarkers that improve early disease detection. Pharmaceutical pipelines are shifting toward glyco-engineered biologics, and analytical platform vendors are responding with integrated hardware–software systems that simplify complex workflows. Chronic disease prevalence continues to rise, driving healthcare providers to adopt glycoproteomic diagnostics, while government funding programs reduce the entry barriers for academic laboratories. Market competition remains moderate as large life-science tool vendors contend with focused reagent suppliers and cloud-based data-analytics start-ups. Supply constraints for rare glycan reagents and a shortage of trained glycobiologists temper short-term expansion, yet regulatory reforms and strategic partnerships are steadily easing these challenges.

Key Report Takeaways

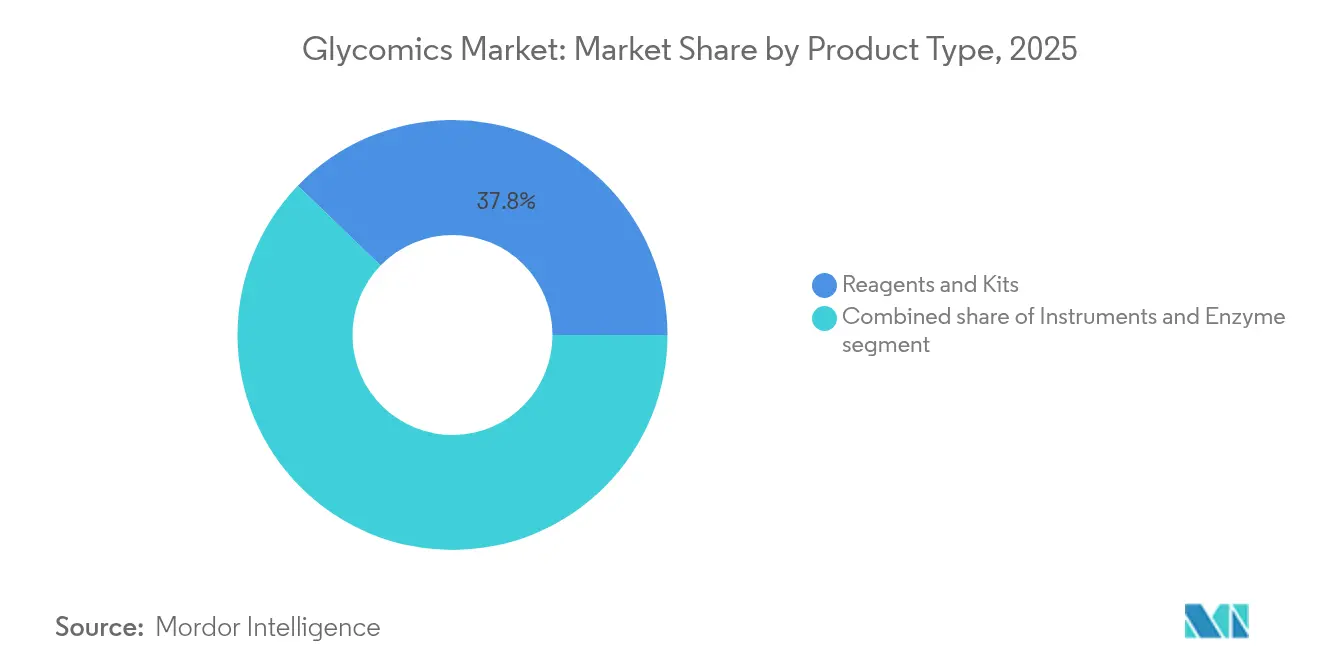

- By product type, reagents and kits held 37.78% of glycomics market share in 2025, while enzymes are on track for a 15.18% CAGR through 2031.

- By technology, mass spectrometry captured 40.92% revenue share in 2025; microarray and chip-based platforms are projected to grow at 14.32% CAGR to 2031.

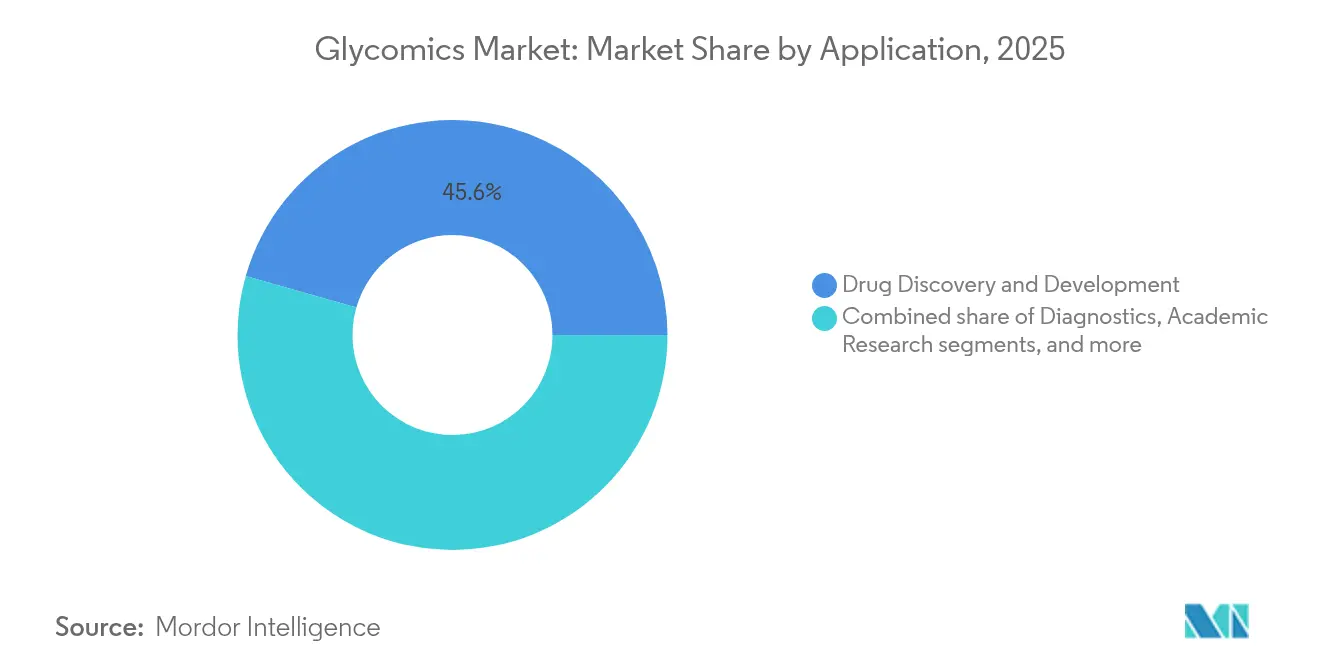

- By application, drug discovery and development commanded 45.57% of the glycomics market size in 2025, whereas vaccine development is set to advance at 14.21% CAGR.

- By end user, pharmaceutical and biotechnology companies accounted for 48.62% of overall demand in 2025, yet hospitals and clinical laboratories will post the fastest 14.98% CAGR through 2031.

- By geography, North America led with 38.10% share of the glycomics market in 2025, and Asia-Pacific is forecast to expand at 14.09% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glycomics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Pharmaceutical Investments in Glycobiology | +2.8% | North America, Europe | Medium term (2–4 years) |

| Growing Adoption of Mass Spectrometry Platforms | +2.1% | Global | Short term (≤2 years) |

| Expansion of Biopharmaceutical Production Capacities | +1.9% | North America, Europe, spill-over to Asia-Pacific | Long term (≥4 years) |

| Rising Prevalence of Chronic Diseases Driving Biomarker Demand | +2.4% | Global | Medium term (2–4 years) |

| Emergence of Glyco-Engineered Cell and Gene Therapies | +1.6% | North America, Europe | Long term (≥4 years) |

| Integration of AI-Enabled Glycan Informatics Solutions | +1.3% | Global, early gains in North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Accelerating Pharmaceutical Investments in Glycobiology

R&D portfolios inside large drug makers now assign priority budgets to glycobiology because glycan changes can foreshadow disease up to ten years before symptoms appear. Glycomine’s USD 115 million Series C raise in 2025 demonstrates investor confidence and channels capital into specialized reagent demand. Alliance formation between academic centers and industry has intensified; Harvard Medical School’s Center for Glycoscience works with multiple sponsors to push lab insights toward clinical trials. Controlled glyco-engineering improves monoclonal antibody potency and reduces immunogenicity, fuelling orders for advanced mass-spectrometry systems and recombinant glycosyltransferases. The trend lifts mid-cap tool suppliers that provide turnkey glycoprotein workflows, making the glycomics market attractive for venture investors searching for platform scale.

Growing Adoption of Mass Spectrometry Platforms

Mass spectrometry has become the analytical backbone for structural glycomics because it now delivers single-molecule clarity. Bruker’s glyco-PASEF method, launched in 2024, reads complex glycopeptides in minutes and lowers sample volumes, shortening project timelines for CROs. Hybrid analyzers paired with rapid ion-mobility separation provide linkage-specific detail without labor-intensive derivatization. AI tools such as CandyCrunch raise identification accuracy toward 90% for unknown structures, reducing the learning curve for new entrants. Taken together, these advances broaden the customer base from elite core facilities to regional hospitals, thereby widening the glycomics market.

Expansion of Biopharmaceutical Production Capacities

Biomanufacturers are scaling cell-culture suites to meet antibody demand, and each production run must replicate the originator’s glycan fingerprint. Process-analytical-technology guidelines now highlight real-time glycan monitoring, so contract manufacturers are acquiring high-throughput LC-MS systems while licensing recombinant enzymes that steer glycoforms toward targeted profiles. Continuous downstream processing relies on rapid analytics, locking in multi-year procurement deals for consumables. Europe’s network of midsize CDMOs and North America’s mega plants share similar needs, which lifts recurring revenue streams for reagent vendors and boosts overall glycomics market growth.

Rising Prevalence of Chronic Diseases Driving Biomarker Demand

Health systems confront growing volumes of diabetes, oncology, and neurodegenerative disorders, and decision makers prize biomarkers that flag disease earlier than current assays. IgG N-glycan panels now stratify insulin resistance and foresee type 2 diabetes onset years ahead. Cancer researchers profile tumor-associated carbohydrate antigens in liquid biopsies to match immunotherapy responders with more precision. As laboratory guidelines adopt glycoproteomic markers, clinical labs purchase automated sample-prep kits and partner with cloud analytics providers, reinforcing the upward trajectory of the glycomics market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost and Technical Complexity of Glycomics Workflows | -1.8% | Global | Short term (≤2 years) |

| Limited Availability of Skilled Glycobiology Professionals | -1.4% | Global, acute in emerging markets | Medium term (2–4 years) |

| Regulatory Uncertainty for Glycan-Based Diagnostics | -1.2% | Global | Medium term (2–4 years) |

| Constrained Supply of Rare Glycan Reagents | -1.1% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Cost and Technical Complexity of Glycomics Workflows

State-of-the-art LC-MS platforms suitable for intact glycoprotein analysis can top USD 500,000, and specialized consumables remain several multiples costlier than proteomics reagents. Method development often requires six to twelve months before routine operation, which stretches project budgets. Each sample may undergo enzymatic release, fluorescent labeling, and multidimensional separation, so consumable usage is high. For many small laboratories, outsourcing remains cheaper, slowing internal adoption and constraining early glycomics market penetration in cost-sensitive regions.

Limited Availability of Skilled Glycobiology Professionals

Fewer than fifty universities offer dedicated glycobiology tracks, and that leaves a talent gap as firms scramble for interdisciplinary experts who can synthesize chemistry, analytical science, and bioinformatics. Senior specialists command salary premiums of 20% to 30%, raising operational costs for new entrants. While NIH Common Fund programs sponsor curriculum development, a full pipeline of qualified graduates is five or more years away[1]NIH Common Fund, “Glycoscience program funds training and technology,” commonfund.nih.gov. The shortfall is most severe in emerging markets where recruiting incentives cannot match multinational budgets, delaying technology transfer and slowing the glycomics market rollout.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reagents Drive Market Foundation

Reagents and kits generated the largest revenue in 2025, capturing a 37.78% share as each analytical cycle necessitates multiple specialized enzymes, lectins, and derivatization chemicals. The glycomics market size for reagents is set to expand steadily in line with sample throughput growth in both R&D and quality-control labs. Enzymes lead volume escalation, advancing at a 15.18% CAGR through 2031, supported by recombinant production routes that offer higher purity and regulatory acceptance for pharmaceutical workflows. Suppliers emphasize lot-to-lot consistency because minute impurities can skew glycan fingerprints and trigger costly batch failures. Instrument sales trail reagents in absolute value yet remain critical for long-term market stickiness. Vendors bundle service contracts and cloud analytics subscriptions, turning one-time hardware purchases into annuity streams. As new users enter the glycomics market, starter kits that combine sample-prep consumables with SOPs lower adoption hurdles.

The instruments category relies heavily on mass spectrometry upgrades, but inline capillary electrophoresis and emerging nanopore sequencers add diversity. Each technology class spurs distinct reagent demand, including fluorescent dyes for HPLC and capture probes for microarrays. Laboratories optimize workflows across platforms, creating cross-selling opportunities. Over the forecast window, reagents will remain the foundation of the glycomics market because every sample analyzed drives recurring consumable spend, and expanded clinical testing will magnify that multiplier effect.

By Technology: Mass Spectrometry Leads Innovation

Mass spectrometry held 40.92% of overall revenue in 2025 and will stay dominant because it delivers definitive linkage and site information. Users embrace time-of-flight and Orbitrap hybrids that pair speed with ultra-high mass accuracy, shortening identification cycles. As infrastructure builds out, the glycomics market size for microarray and chip-based platforms rises fastest, climbing at 14.32% CAGR through 2031. Miniaturized arrays enable high-throughput screening, which appeals to vaccine developers who need thousands of antigen variants screened under budget constraints. Regulatory validation of lectin microarrays for monoclonal antibody lot release widened commercial acceptance.

HPLC and UHPLC remain staples because they integrate seamlessly into existing QC labs. Capillary electrophoresis retains niche status for charge-variant resolution of acidic glycans. The technology landscape is shifting toward integrated multi-modal systems that fuse front-end separations with MS detection and AI-based structure calling. Software platforms that automate data reduction are now decisive in purchase decisions because they relieve staff shortages and enable smaller labs to enter the glycomics market. Over time, instrument makers that combine hardware, reagents, and bioinformatics will secure a broader installed base and raise switching costs.

By Application: Drug Discovery Dominates

Drug discovery and development generated 45.57% of total demand in 2025, underlining the pharmaceutical sector’s dependence on precise glycan analytics for biologic potency and safety. Detailed glycoform mapping is mandatory for regulatory filings of monoclonal antibodies and fusion proteins. The application also benefits from pipeline diversification into antibody-drug conjugates and next-generation cell therapies whose efficacy depends on surface glycan engineering. Vaccine development is the quickest riser with a 14.21% CAGR, catalyzed by pandemic-era lessons that viral glycosylation can mask or reveal neutralizing epitopes. Future mRNA and protein-subunit vaccines will incorporate glycan optimization earlier in design cycles, pulling in additional analytical spend.

Diagnostics is shifting from research to clinical utility as glycoproteomic panels deliver earlier and more specific detection of cancers and metabolic disorders. Hospitals pilot kits that measure IgG-N glycans to stratify disease risk, a move that will spur routine testing once reimbursement codes expand. Academic research continues to contribute baseline method innovation by leveraging grant programs that subsidize instrument access, cushioning the glycomics market against macroeconomic volatility.

By End User: Pharma Companies Lead Adoption

Pharmaceutical and biotechnology firms contributed 48.62% of 2025 revenue, reflecting their need for in-house control of critical quality attributes during biologic development. These companies fund dedicated glycomics core labs and subscribe to enterprise informatics suites that centralize data across global sites. Contract research organizations deepen service menus with glycan mapping to win outsourcing projects, importing instrumentation in bulk and boosting reagent purchases.

Hospitals and clinical laboratories will grow fastest at 14.98% CAGR as regulatory bodies approve diagnostic assays that use glycan signatures to predict therapy response. Early adopters demonstrate shorter patient stratification timelines, encouraging peer institutions to follow. Academic and government institutes remain essential end users because they pioneer new assay formats and validate clinical relevance, feeding discoveries back to industry. Collectively, heterogeneous end-user demand insulates the glycomics market from single-sector downturns.

Geography Analysis

North America retained 38.10% share of the glycomics market in 2025 thanks to sustained NIH funding and an advanced biopharma manufacturing base. The FDA’s validated protocols for glycan profiling now streamline lot-release testing, prompting tool vendors to locate demo centers near Boston, San Diego, and Toronto. Universities such as the University of Georgia received an USD 18 million NSF award to democratize glycoscience infrastructure, creating regional training hubs that seed future adoption.

Europe ranks second in revenue, anchored by Germany’s instrumentation expertise, the United Kingdom’s biologics accelerators, and France’s vaccine institutes. Pan-European regulatory alignment promotes shared validation studies, lowering compliance costs and fostering cross-border collaborations. Contract research organizations in Ireland and the Netherlands provide specialized glycan analysis for U.S. and Asian sponsors, linking continents within a global supply chain.

Asia-Pacific is the fastest climber with a 14.09% CAGR to 2031. China’s shift toward high-value biologics drives demand for glycan monitoring as plants aim for FDA and EMA licensure. Japanese instrument makers ship high-end MS systems to local universities, while South Korean CDMOs bundle glyco-engineering services for Western clients. Southeast Asian nations benefit from China’s capacity diversification strategy, receiving technology transfers and joint ventures that broaden the regional customer base. India’s biosimilar manufacturers pursue U.S. market approvals, further boosting the glycomics market. Australia leverages national research grants to study glycan roles in neurodegeneration, anchoring Oceania’s contribution. Together these dynamics expand the addressable installed base and strengthen long-term revenue visibility.

Regulatory Landscape

Regulatory requirements for glycan characterization continue to tighten for biologics and biosimilars, where glycosylation is treated as a critical quality attribute for comparability and change control. In September 2025, the US FDA published biosimilar guidance that explicitly reinforces the need for detailed characterization of posttranslational modifications, including glycosylation, which increases demand for validated glycan profiling workflows across development and lot-release testing. FDA regulatory-science work has also highlighted rapid glycan-profiling approaches (including lectin microarray-based methods) to support characterization of therapeutic monoclonal antibodies.

Standardization efforts are advancing alongside regulator scrutiny, and they help reduce cross-lab variability that limits clinical translation. MIRAGE reporting guidelines for mass spectrometry-based glycomics and glycoproteomics, along with reference-material work and interlaboratory benchmarking activities from bodies such as NIST, are increasingly used as quality anchors for method validation. In parallel, global data harmonization initiatives such as the Global Glyco-Data Standard (GGDS) and proposed minimum-information frameworks are being developed to align discovery outputs with CMC-grade documentation needs, which supports broader adoption of regulated, repeatable glycomics workflows.

Competitive Landscape

The glycomics market is moderately fragmented. No single vendor exceeds a one-third share, and the top five suppliers collectively hold roughly half of global revenue, leaving room for emerging specialists. Thermo Fisher Scientific, Agilent Technologies, Waters Corporation, and Bruker command strong brand recognition and extensive service networks. They bundle MS hardware, chromatography columns, and software, which appeals to pharmaceutical clients seeking validated end-to-end solutions. New England Biolabs focuses on high-purity recombinantly expressed enzymes, carving a niche among quality-conscious users.

Strategic transactions shape competition. Astellas Pharma agreed to pay up to USD 784 million to Go Therapeutics for glycoproteomic cancer programs, signaling big-pharma appetite for external innovation. Pentixapharm acquired Glycotope’s discovery unit to enrich radiopharmaceutical targeting. Instrument makers partner with cloud AI firms to integrate automated structure elucidation, reducing customer reliance on scarce expert staff. Vendors that offer subscription analytics lock in multiyear revenue and increase switching costs.

Price competition remains limited because performance differentiation is high and reagent quality directly affects regulatory outcomes. Yet as clinical labs scale up, demand for mid-range instruments may invite lower-cost entrants from Asia, intensifying rivalry over time. Overall, suppliers that combine hardware, reagents, and data analytics stand to gain share as customers favor single-vendor accountability.

Glycomics Industry Leaders

Thermo Fisher Scientific Inc.

Agilent Technologies Inc.

Merck KGaA (Sigma-Aldrich)

Bruker Corporation

Danaher (SCIEX)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace for the market is the shift from expert-only, manual interpretation of glycomics toward routine, automated analytics that fit biopharma QC and clinical laboratory constraints. Agilent's May 2026 launch of a Multi-Attribute Method (MAM) solution for LC/HRMS in regulated biopharma testing points to a concrete route for high-resolution mass spectrometry to move into standardized QC use, where glycan-related attributes are tracked as part of release and stability programs. Tool vendors that pair instruments with validated workflows and software automation are positioned to capture spend linked to process-analytical-technology adoption and biosimilar comparability requirements.

Another opportunity centers on shared data infrastructure and networked service access that reduces barriers for hospitals, regional laboratories, and smaller biotechs that cannot staff dedicated glycobiology teams. Programs and consortia such as the Human Glycome Atlas (building the TOHSA knowledge base), GlycoNet Integrated Services (GIS), and Japan's J-GlycoNet provide aggregation, standardization, and access models that support cross-site studies and method transfer. Informatics platforms emerging from the research community, including the March 2026 StrucGAP release for structural and site-specific N-linked glycoproteomics data mining, reinforce the move toward modular pipelines that shorten the path from spectra to interpretable glycan features for drug discovery, vaccine design, and diagnostic biomarker development.

Recent Industry Developments

- June 2026: Bruker announced automated glycoproteomics workflow capabilities on its timsOmni platform, including dissociation methods designed to improve glycan characterization in complex samples. The update supports higher-throughput, more standardized glycoproteomics that aligns with pharma and CRO demand for repeatable glycan analytics across projects.

- May 2026: Agilent launched a Multi-Attribute Method (MAM) solution aimed at enabling LC/HRMS for routine, regulated biopharma quality control. By packaging a QC-oriented workflow, Agilent addressed an adoption hurdle for bringing high-resolution MS into lot release and stability testing where glycosylation-related attributes are monitored.

- August 2024: Pentixapharm acquired Glycotope's target-discovery business, adding preclinical antibody assets directed at tumor-associated carbohydrate structures. The acquisition broadened the downstream pull for glycan-focused discovery and characterization tools used in oncology target validation and early development.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the glycomics market covers revenues generated from tools and consumables used to identify, profile, and quantify glycans and glycan patterns, along with supporting workflows used in research and clinical-research settings.

Scope exclusions: Pure bioinformatics-only services and generic lab hardware not configured for glycan-specific analysis are excluded to avoid overstating spend.

Segmentation Overview

- By Product Type

- Instruments

- Reagents & Kits

- Enzymes

- By Technology

- Mass Spectrometry

- HPLC & UHPLC

- Capillary Electrophoresis

- Microarray & Chip-Based Platforms

- Lectin-Affinity Assays

- Other Techniques

- By Application

- Drug Discovery & Development

- Diagnostics

- Academic Research

- Biopharmaceutical Production

- Vaccine Development

- By End User

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Contract Research Organizations

- Hospitals & Clinical Laboratories

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with building a clear demand pool for glycomics activity and then linking it to measurable spending. Public sources such as the National Institutes of Health (NIH) funding databases, World Health Organization disease burden indicators, US FDA biologics and diagnostics guidance pages, and patent databases were reviewed to understand research intensity and where glycan analytics is being applied.

We also used peer reviewed journals for glycan biomarker and biotherapeutic characterization trends, customs trade statistics where relevant for lab equipment flows, and association and conference materials that signal adoption of specific analytical approaches. Company filings, investor presentations, and reputable press were used to sense-check product mix changes and pricing movement for instruments versus consumables, supported by a paid subscription for company financials and a separate paid subscription for shipment-level import and export checks. These examples are illustrative, and many other sources were also used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on validating what portion of glycan analytics spending is truly glycomics-specific, and how demand shifts between research, drug development support, and diagnostics-oriented workflows. We spoke with a balanced set of respondents, including lab directors, product and application specialists, and procurement-facing managers, and the coverage spanned major regions so assumptions on usage intensity, replacement cycles, and pricing could be checked with real-world feedback.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | APAC: 42% |

| Mid tier: 46% | Functional/Unit leaders: 35% | EMEA: 31% |

| Smaller Players: 18% | Managers: 53% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up logic where R&D and clinical-research activity indicators were translated into an addressable glycomics spend pool, and then allocated by typical workflow cost. Inputs used in the model included public funding direction for glycoscience, biologics pipeline intensity (where glycosylation characterization becomes mandatory), adoption of mass spectrometry and HPLC/UHPLC workflows for glycan analysis, consumables-to-instrument spending mix, and replacement and utilization patterns reported by labs.

To keep totals realistic, selective bottom-up approximations were used as cross-checks, such as sampled average selling prices multiplied by estimated unit demand for key consumables, plus channel checks on instrument placements. Where bottom-up visibility was uneven by country, gaps were handled through proxy indicators like research spend per active lab site and adjusted with primary feedback before aggregation.

Forecasting relied mainly on scenario analysis, since adoption can swing based on funding cycles, biopharma pipeline priorities, and regulatory emphasis on characterization. Growth rates were set by combining historical trend signals with expert views on how quickly labs expand glycan testing into routine development and diagnostics pathways.

Data Validation & Update Cycle

Model outputs were checked against independent signals, including funding and publication momentum, biologics development activity, and the expected split between instruments and recurring consumables. If a country or region showed a sudden jump that could not be explained by these signals, the assumptions were re-checked and, when needed, respondents were re-contacted to confirm what changed.

Before sign-off, the work goes through multiple analyst reviews that focus on scope consistency, year-on-year variance checks, and whether assumptions match what users report in practice. Reports are refreshed annually, and interim updates are triggered when material events occur, after which a final pre-delivery pass is done so clients receive the latest updated view.

Mordor Intelligence's Glycomics Market Size Measured Against Other Published Estimates

Published market sizes for glycomics often vary because the spend scope is not identical across sources, and the starting year and pricing logic can also differ. Even small differences in what is treated as a glycomics instrument versus a general life science tool can create a noticeable spread.

The benchmark table shows a tight cluster around the mid USD 2 billion range for nearby years, but the wider estimate is usually linked to broader category roll-ups and longer-range projections that pull faster adoption into the early years. In Mordor Intelligence's model, only dedicated glycomics instruments, kits, enzymes, and reagents tied to glycan characterization workflows are counted, with pure bioinformatics-only services excluded.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.42 B (2026) | |

| Global Consultancy A | USD 2.41 B (2025) | Uses a different base year and may blend glycomics with broader glycobiology activity, which can shift instrument and service edges and alter early-year totals. |

| Industry Publisher B | USD 2.35 B (2024) | Starts from an earlier base year and often applies a broad product and application frame, which can pull in adjacent carbohydrate research tools beyond dedicated glycan characterization workflows. |

Overall, the spread is mainly explained by scope edges, base-year selection, and how pricing and adoption are carried forward across instruments and recurring consumables. By tying the sizing steps to visible demand signals and then checking them with interviews, the outputs stay easier to trace and repeat when buyers need to update assumptions.

Key Questions Answered in the Report

What is the current size of the glycomics market?

The glycomics market stands at USD 2.42 billion in 2026.

How fast is the glycomics market growing?

It is projected to grow at a 13.63% CAGR, reaching USD 4.58 billion by 2031.

Which technology holds the largest share within the glycomics market?

Mass spectrometry leads with 40.92% revenue share in 2025.

Which application area is expanding the fastest?

Vaccine development is the fastest-growing application with a 14.21% CAGR through 2031.

Why is Asia-Pacific considered the fastest-growing region?

Regional growth is driven by China’s push into biologics manufacturing and increased healthcare investment across emerging markets.

What restraints could slow near-term growth?

High workflow costs and a shortage of skilled glycobiologists currently limit broader adoption, especially in emerging economies.

Page last updated on: