Proteinase K Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.56 Billion |

| Market Size (2031) | USD 8.06 Billion |

| Growth Rate (2026 - 2031) | 7.68% CAGR |

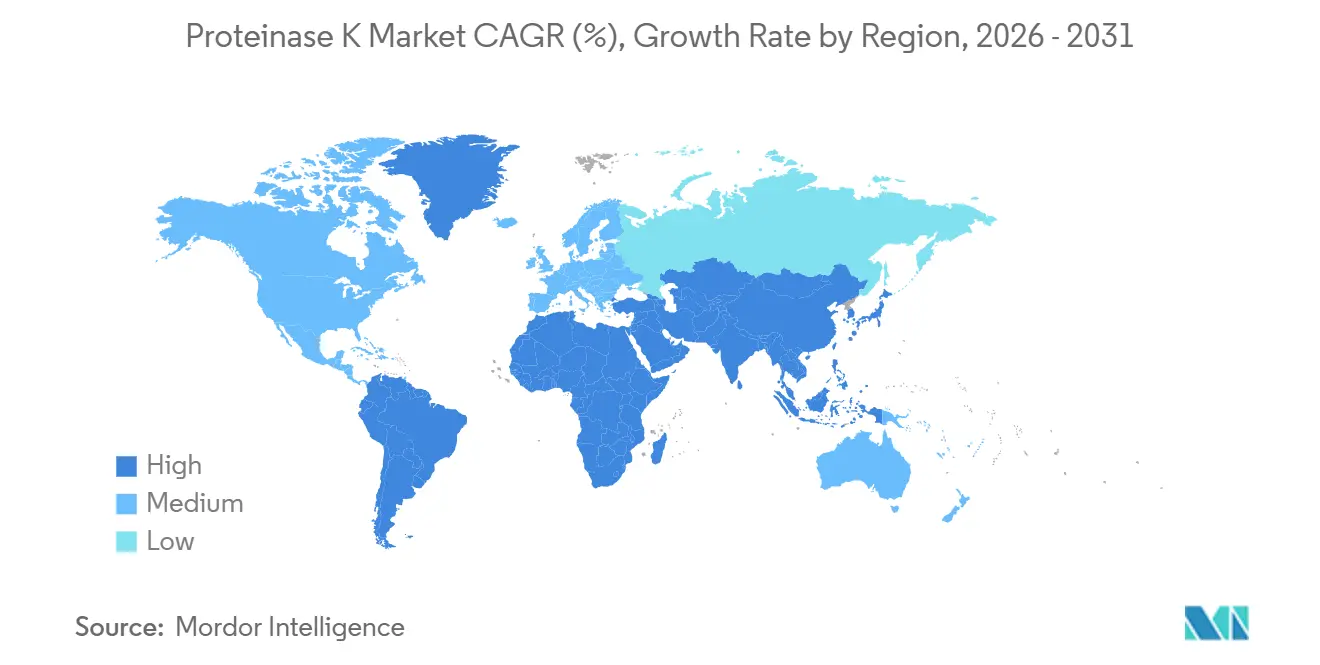

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

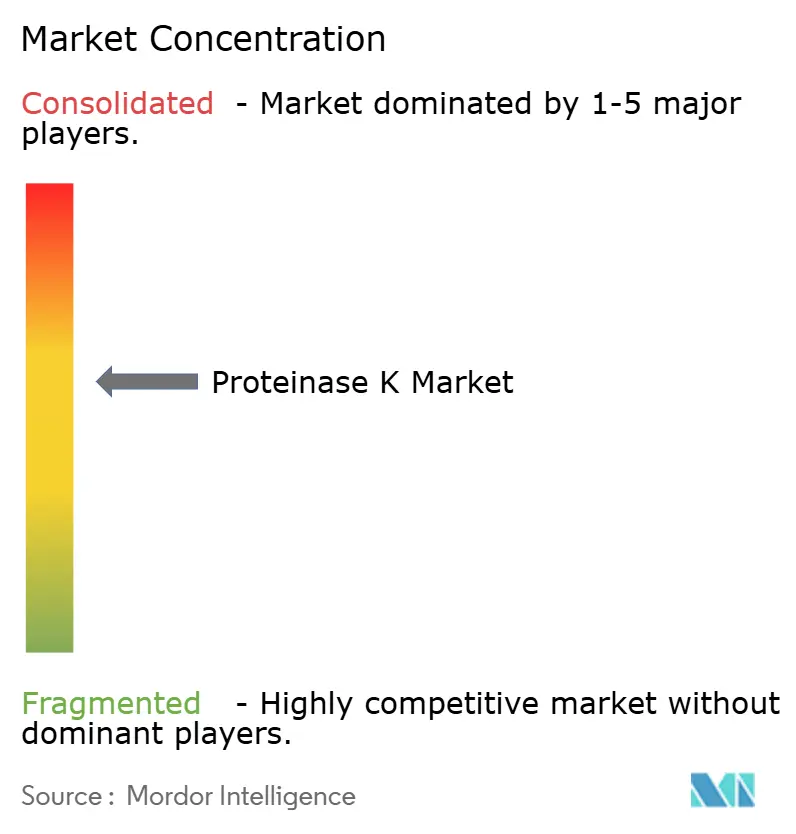

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Proteinase K Market Analysis by Mordor Intelligence

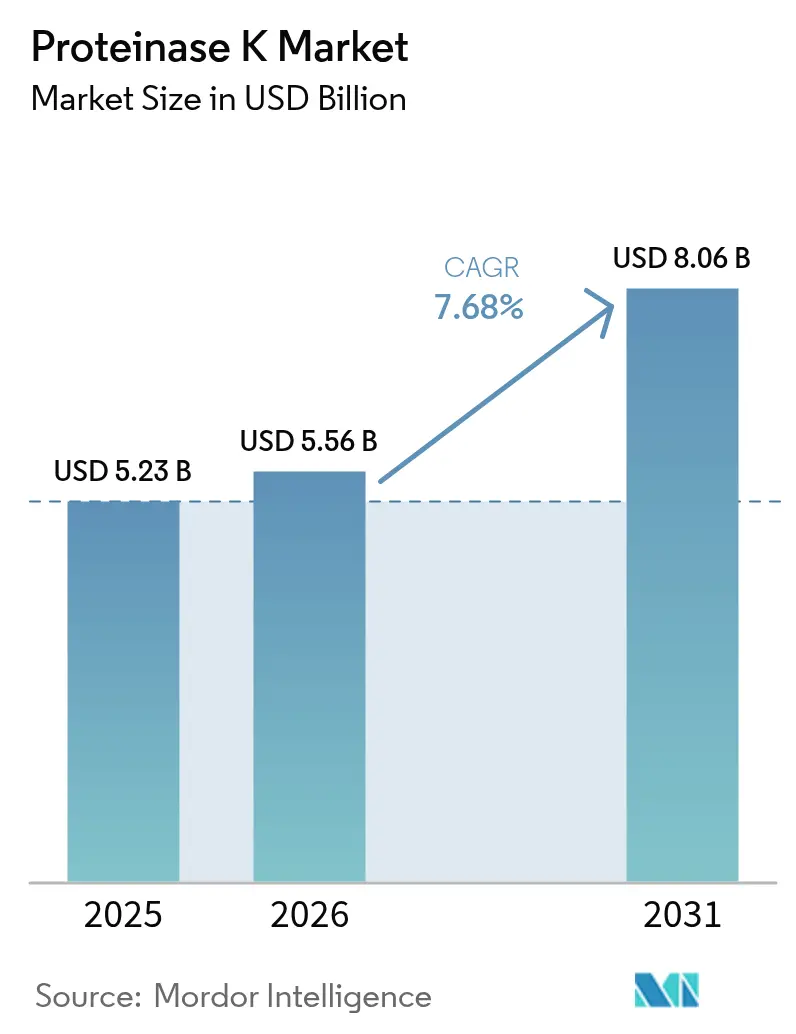

The Proteinase K Market size is projected to be USD 5.23 billion in 2025, USD 5.56 billion in 2026, and reach USD 8.06 billion by 2031, growing at a CAGR of 7.68% from 2026 to 2031.

Demand is tilting toward recombinant expression in Pichia pastoris and E. coli, which removes mycotoxin risk and ensures lot-to-lot consistency that is essential for GMP-grade diagnostics and biomanufacturing.[1]Promega Corporation, “Recombinant Trypsin in Pichia,” promega.com Automation is reshaping procurement patterns, as high-throughput instruments such as QIAsymphony Connect require ready-to-use liquid reagents that can trim turnaround time by 30% over manual reconstitution.[2]QIAGEN NV, “Tracer and Foresight Partnerships,” qiagen.com Lyophilized formats still dominate because they tolerate ambient shipping and storage, but room-temperature-stable liquids are closing the gap despite a 15–20% price premium. North America remains the highest-value region, yet the Asia-Pacific Proteinase K market is expanding fastest on the back of more than USD 3 billion in CDMO investments announced during H1 2025.

Key Report Takeaways

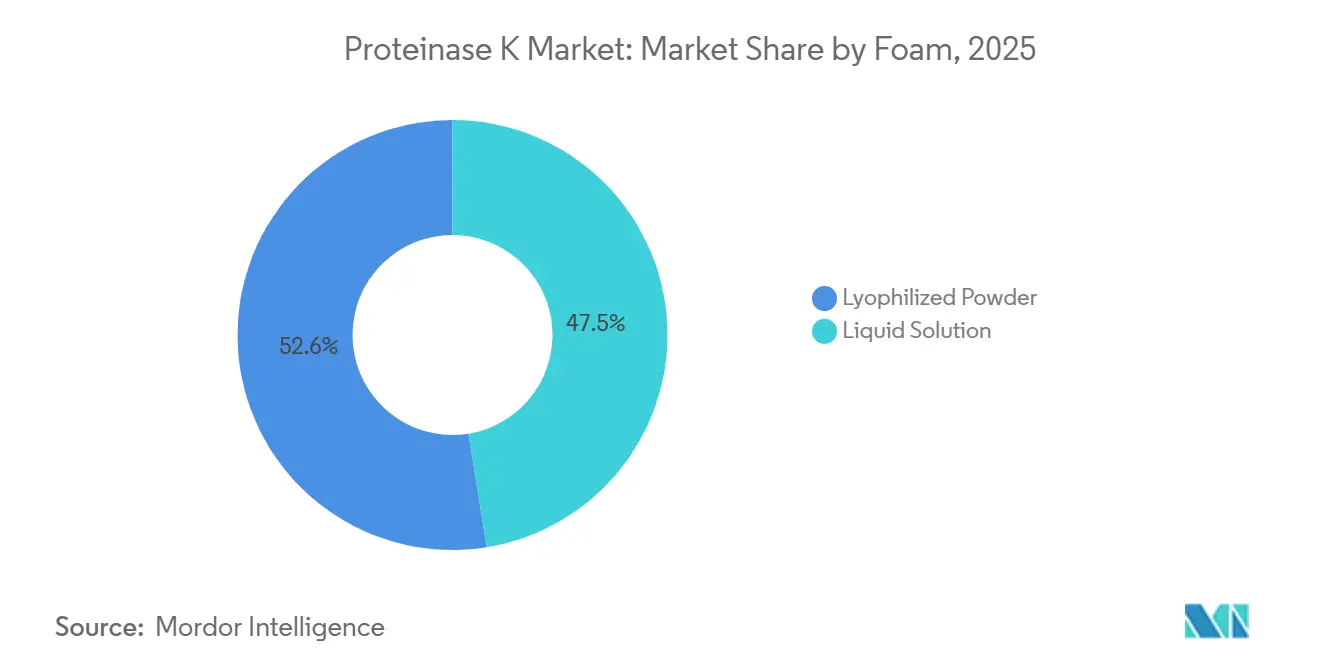

- By form, lyophilized powder led with 52.55% of Proteinase K market share in 2025, while liquid solutions are projected to record the highest 9.56% CAGR through 2031.

- By purity grade, standard research-grade enzyme accounted for 61.42% share of 2025 revenue, whereas GMP and clinical-grade variants are forecast to expand at a 10.78% CAGR to 2031.

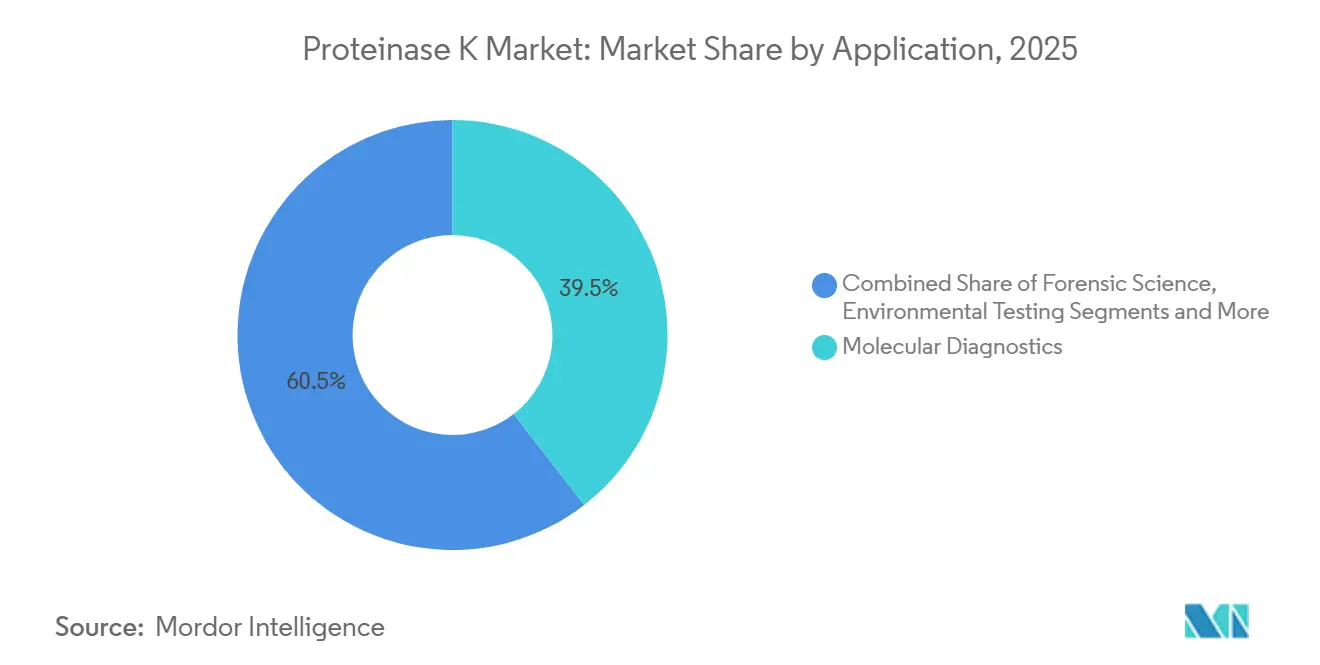

- By application, molecular diagnostics commanded 39.55% revenue share in 2025, and environmental testing is expected to rise fastest at an 11.83% CAGR during 2026–2031.

- By source type, fungal-derived native enzyme held 53.78% share in 2025, but recombinant variants are set to grow at a 9.77% CAGR through 2031.

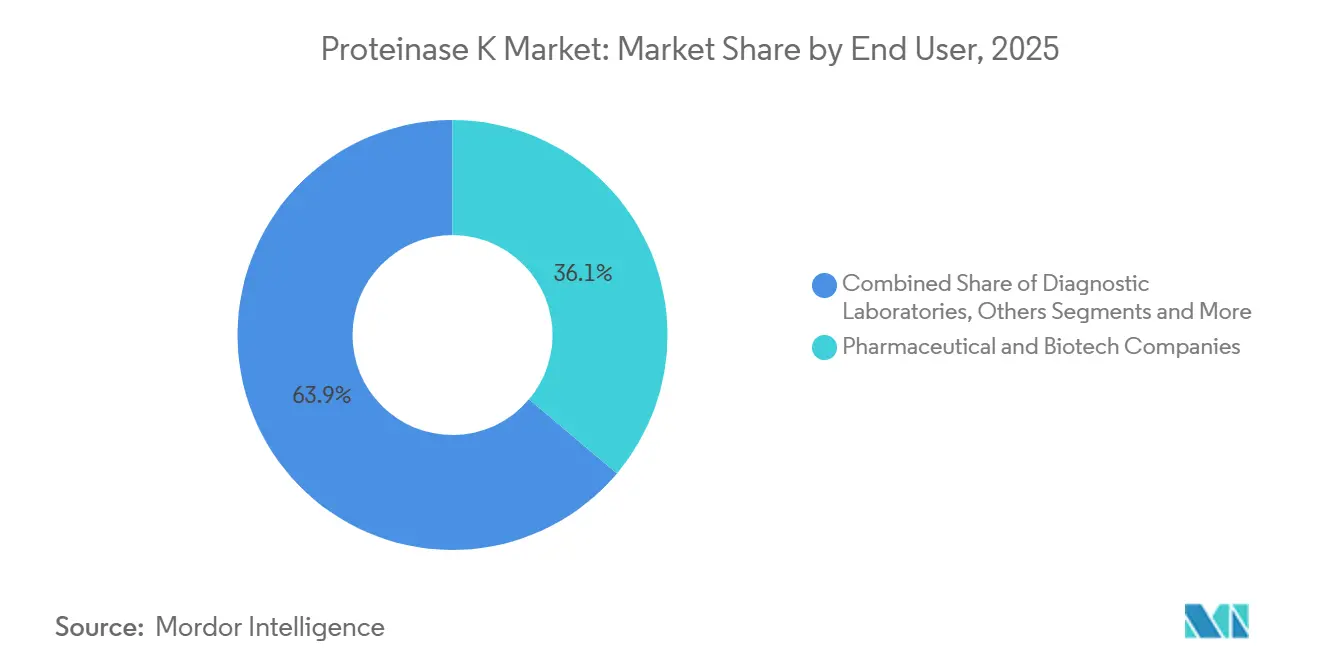

- By end user, pharmaceutical and biotechnology companies represented 36.13% of demand in 2025, whereas contract research organizations are anticipated to post a 10.81% CAGR to 2031.

- By geography, North America dominated with a 39.55% share in 2025, while Asia-Pacific is projected to register the fastest 9.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Proteinase K Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-quality DNA/RNA extraction in diagnostics | +1.8% | North America and Europe clinical labs, Asia-Pacific infectious disease programs | Medium term (2–4 years) |

| Biopharmaceutical production expansion | +1.5% | North America and Europe biologics plants, Asia-Pacific CDMO hubs | Long term (≥4 years) |

| Growth in forensic and food safety testing | +0.9% | North America and Europe forensic labs, global food-pathogen screening | Medium term (2–4 years) |

| Automation and high-throughput adoption | +1.2% | Early adoption in North America and Europe, roll-out in Asia-Pacific research institutes | Short term (≤2 years) |

| Environmental microbiome sample processing | +1.1% | North America and Europe soil-water studies, Asia-Pacific biodiversity monitoring | Medium term (2–4 years) |

| Integration into cell-free expression | +0.7% | North America and Europe synthetic biology centers, emerging Asia-Pacific academic labs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High-Quality DNA/RNA Extraction in Molecular Diagnostics

Clinical labs are standardizing on Proteinase K for extraction-free SARS-CoV-2 assays and for FFPE tissue processing because the enzyme works across pH 7.5–12 and tolerates ionic detergents, enabling single-tube lysis without organic solvents. QIAGEN’s September 2025 deals with Tracer Biotechnologies and Foresight Diagnostics highlight rising demand for nuclease-free enzyme with ≥30 U/mg activity to protect RNA during 56 °C overnight digestions. FDA emergency-use guidance issued in January 2025 now requires stability data across three lots and evidence of activity retention after six freeze-thaw cycles, pushing suppliers toward higher-specification batches. New England Biolabs launched EM-seq v2 in January 2025, cutting minimum DNA input from 10 ng to 100 pg and opening liquid-biopsy markets.[3]New England Biolabs, “EM-seq v2 Launch,” neb.com Diagnostic manufacturers also seek ISO 13485-certified production and compliance with 21 CFR 864.4400 when sourcing reagents.

Biopharmaceutical Production Requiring Enzymatic Digestion

Biologics manufacturers depend on Proteinase K to strip host-cell proteins during mAb purification and to generate peptide maps under denaturing conditions such as 8 M urea and 0.5% SDS. Amgen’s USD 1 billion North Carolina drug-substance plant, announced in December 2024, typifies the capital wave that will enlarge demand for GMP-grade proteases. Promega’s recombinant trypsin produced in Pichia pastoris shows the shift toward animal-origin-free reagents that minimize BSE risk and ease regulatory filings. Codexis’s ECO Synthesis milestone reached more than 98% coupling efficiency in enzymatic siRNA manufacture, demonstrating how engineered proteases can displace chemical catalysts. EMA GMP guidelines demand full fermentation records and quality-control test data, which shapes vendor qualification.

Increasing Demand in Forensic and Food Safety Testing

Forensic labs value Proteinase K because it digests histones and boosts DNA yield by 40% versus Chelex protocols in low-template samples. Promega’s engineered variant launched in September 2024 reduces stutter artifacts in STR amplification, improving mixture interpretation in sexual-assault evidence. Food-safety labs employ the enzyme to remove inhibitors ahead of CRISPR-based pathogen assays that rely on Cas13a cleavage. The SCOPE system published in April 2024 detects monkeypox at 0.5 copies/µL in 15 minutes after Proteinase-K lysis. ISO 17025 accreditation and FSMA rules reinforce validated protocols that define concentration, incubation, and heat inactivation.

Automation and High-Throughput Sample Preparation Adoption

Laboratories are integrating Proteinase K into robots such as Opentrons OT-2 and Thermo Fisher KingFisher Apex, achieving ≤5% coefficient of variation in 96-well plates while freeing staff for interpretive tasks. QIAGEN’s April 2025 roadmap unveiled instruments that run 192 samples per batch, relying on pre-aliquoted liquids that slash hands-on time by one-third. Sansure’s iPonatic POCT system completes extraction and detection in 30 minutes at USD 0.50 per cartridge by using lyophilized Proteinase K in a microfluidic chip. Promega markets a thermolabile version that auto-deactivates at 95 °C, avoiding column cleanup. Instrument makers must meet IEC 61010 and CLSI AUTO15 requirements, which specify safety and performance benchmarks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Alternative proteases and recombinant enzymes | −0.8% | Cost-sensitive research in Asia-Pacific and Latin America | Medium term (2–4 years) |

| High cost of GMP-grade Proteinase K | −1.1% | Emerging markets in India, Southeast Asia, Latin America, Africa | Long term (≥4 years) |

| Cold-chain dependency for liquid formulations | −0.9% | Regions with unreliable refrigeration infrastructure | Medium term (2–4 years) |

| Regulatory uncertainties for enzyme diagnostic kits | −0.6% | Europe under IVDR, United States during LDT transition | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Availability of Alternative Proteases and Recombinant Enzymes

Recombinant trypsin, pepsin, and LysC variants are substituting Proteinase K in peptide mapping, proteomics, and budget-constrained DNA extraction. Codexis out-licensed a genomics enzyme suite to Alphazyme and Maravai in October 2024, demonstrating how engineered polymerases compete on speed and inhibitor tolerance. Academic benchmarks show Achromobacter lyticus protease outperforming classic LysC in cleavage specificity, tempting laboratories to swap when ultra-broad digestion is not required. Cell-free screening platforms enable rapid design of niche enzymes that displace Proteinase K in targeted assays. Lower unit costs, often 20–30% below Proteinase K, attract universities in Asia-Pacific and Latin America.

High Cost of High-Purity GMP-Grade Proteinase K

GMP batches cost three- to five-fold more than research grade due to ICH Q7 compliance, full traceability, and endotoxin testing ≤10 EU/mg. Diagnostic labs in India and sub-Saharan Africa often resort to detergent boil protocols that cut sensitivity but avoid enzyme expense. The U.S. LDT phaseout demands full validation by 2028, adding compliance costs that smaller kit makers struggle to fund. Import duties such as India’s GST and China’s VAT add 10–18% to final prices. CRO budgets also stretch to cover biosimilar pipelines that already consume USD 50–75 million per candidate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Automation Tilts the Balance Toward Liquids

Lyophilized powder captured 52.55% of Proteinase K market share in 2025, mainly because it ships and stores at ambient temperature up to 24 months. Liquid solutions are forecast to record a 9.56% CAGR through 2031 as labs embrace walk-away automation on platforms such as QIAsymphony Connect that process 192 samples per run with pre-mixed reagents. The Proteinase K market size for liquids is poised to expand fastest where hospitals adopt laboratory-information-system integration and manpower costs are high. Powder remains vital for outbreak deployments, illustrated by ProtonDx Dragonfly kits that delivered 100% mpox detection in Sierra Leone in 2025. Liquid formats still face −20 °C cold-chain constraints outside OECD regions, but room-temperature-stable variants from Thermo Fisher are closing that gap.

Automation-ready liquids win when reconstitution variability threatens qPCR reproducibility and when reagent barcoding enables error-proof inventory. Yet, lyophilized powder enjoys lower freight costs that can trim landed price by up to 12% in air-cargo lanes. Vendors are also offering dual-pack SKUs so purchasers can align formulation to workflow mix. Regulatory files must include stability data on rehydrated powder and on ready-to-use liquids, with FDA 21 CFR 211 guidance framing batch release.

By Purity Grade: Clinical Compliance Drives Margin Growth

Research-grade enzyme generated 61.42% of 2025 revenue because academic and early-stage industrial labs emphasize volume over documentation. The Proteinase K market size for GMP and clinical grade is expanding at 10.78% CAGR through 2031 as diagnostics transition from EUA to full PMA filings that require COA, endotoxin data, and master-cell-bank traceability. PCR-grade products occupy a middle tier that answers nuclease-free needs without full ICH Q7 paperwork, providing a grooming lane for future conversion to GMP grade.

Growth in GMP demand is strongest in North America and the EU, where IVDR and FDA reforms tighten oversight. Emerging Asia-Pacific bio-foundries increasingly order GMP lots to serve multinational sponsors that embed ISO 13485 clauses into supply contracts. Research grade retains dominance in environmental genomics and educational labs, whose budgets seldom accommodate a 3–5× price uplift. Vendors differentiate with mycoplasma-tested labels and e-COAs that integrate with eQMS platforms, meeting 21 CFR 820 records requirements.

By Application: Diagnostics Still Rule, Environment Gains Momentum

Molecular diagnostics generated 39.55% of 2025 revenue thanks to ubiquitous DNA/RNA extraction for PCR, NGS, and FFPE processing. Environmental testing is forecast to register an 11.83% CAGR to 2031, reflecting a surge in soil, water, and air metagenomics that standardizes on Proteinase K for low-biomass protocols. The Proteinase K market size in environmental labs will benefit from climate-funded surveillance projects tracking antimicrobial-resistant genes in rivers.

Biopharmaceutical workflows such as host-cell-protein removal and peptide mapping keep demand steady, anchored by the USD 1 billion Amgen facility and similar plants in the CMO pipeline. Forensic science adoption of an engineered enzyme that minimizes STR stutter improves evidentiary clarity and nudges legal systems toward enzyme-validated kits. Food-safety testing leverages Proteinase K in CRISPR diagnostics to clear inhibitors before Cas13a readout. Cell-free systems and synthetic biology represent emerging but growing avenues, especially where rapid prototyping trims drug-candidate screening timelines by weeks.

By Source Type: Recombinant Expression Accelerates

Native fungal Proteinase K from Tritirachium album still held 53.78% of 2025 volume, offering broad specificity at 20–30% lower cost than recombinant equivalents. Recombinant platforms in Pichia pastoris and E. coli are growing at a 9.77% CAGR through 2031, favored for batch consistency, endotoxin control, and mycotoxin-free status that streamline regulatory dossiers. Engineered or synthetic variants, though niche, showcase performance gains such as thermostability and inhibitor tolerance delivered by machine-learning-guided design engines screening 10^14 protease constructs.

Clinical diagnostics and biomanufacturing lean toward recombinant sources because they remove animal-origin concerns tied to BSE. Research labs continue to purchase native enzyme when budget trumps pedigree. Regulators apply 21 CFR 610 and EMA GMP certificates to fermentation-derived reagents, so suppliers document seed-lot systems, fermentation parameters, and downstream purification steps. The Proteinase K market share for engineered variants will likely rise as cell-free synthesis scales to gram quantities, opening catalytic roles beyond nucleic-acid cleanup.

By End User: Outsourcing Wave Lifts CRO Demand

Pharma and biotech companies consumed 36.13% of Proteinase K market demand in 2025, tied to monoclonal-antibody purification and LC-MS peptide mapping. CROs are advancing at a 10.81% CAGR through 2031 as outsourcing penetration in Phase II–III oncology trials climbs toward 80%. The Proteinase K market size among CROs expands when sponsors centralize assay development and validation, preferring vendors that can drop-ship enzyme to multiple trial sites.

Academic institutes still order bulk packs for metagenomics and synthetic biology research, leaning on grant budgets. Diagnostic laboratories source GMP or PCR-grade lots with COA and nuclease-free certification to comply with IVDR and LDT policies. Food-testing agencies and environmental watchdogs follow ISO 17025 standards and select formulations that specify inactivation protocols matching field capacity. Suppliers cultivate service models offering lot reservation, e-COA portals, and method-transfer support that align with CRO just-in-time logistics.

Geography Analysis

North America accounted for 39.82% of global revenue in 2025, supported by more than USD 300 billion in announced pharma-capacity expansions and the FDA PreCheck program that cuts plant build timelines by up to 12 month. Tariff uncertainties have accelerated onshoring of API production, increasing domestic demand for fermentation enzymes. U.S. diagnostic makers face the LDT sunset, so they are locking in long-term supply of nuclease-free Proteinase K with detailed stability files. Canada follows closely, with provinces funding genomic surveillance against antimicrobial resistance, maintaining consumption of research-grade packs.

Europe benefits from IVDR-driven compliance spending; however, lengthy notified-body queues delay some kit launches, temporarily dampening volume growth. Germany and Switzerland host several global enzyme production sites that export GMP lots worldwide. The region also pursues room-temperature-stable liquids to meet green-logistics targets under Fit-for-55.

Asia-Pacific is forecast to register a 9.63% CAGR through 2031, propelled by >USD 3 billion CDMO investments in H1 2025, including Lotte Biologics’ antibody-drug conjugate megaplant and WuXi Biologics’ 120,000-L Singapore campus. India’s PLI scheme earmarked USD 3 billion to grow domestic biopharma, spurring local fermentation of recombinant proteases. ASEAN’s eCTD harmonization accelerates diagnostic reagent approvals across six member states. Japan and South Korea lead regional automation with OT-2 and KingFisher roll-outs, while China’s gene-therapy boom fuels GMP enzyme imports despite geopolitical scrutiny.

Middle East and Africa, along with South America, maintain single-digit shares but offer powder-format upside because lyophilized Proteinase K tolerates ambient shipping where cold-chain reliability remains poor. WHO-funded surveillance projects in sub-Saharan Africa adopt sponge-swab pathogen kits that include shelf-stable enzyme. Brazil’s public-health labs, upgrading genomic sequencing for dengue monitoring, are piloting room-temperature liquids under refrigerated locker distribution.

Competitive Landscape

Six incumbents include Thermo Fisher Scientific, QIAGEN, Merck KGaA, Roche, Promega, and New England Biolabs giving the space moderate concentration. Machine-learning enzyme designers such as Codexis, Arzeda, and Exozymes capture niche workflows like cell-free bioproduction by reducing variant discovery from months to weeks. Incumbents counter with portfolio refreshes: QIAGEN’s three automated prep systems announced April 2025, Promega’s forensic-grade enzyme launched September 2024, and New England Biolabs’ EM-seq v2 unveiled January 2025.

Strategic moves include Thermo Fisher’s September 2025 acquisition of Sanofi’s Ridgefield fill-finish site, bolstering contract manufacturing reach. QIAGEN struck collaborations with Tracer Biotechnologies and Foresight Diagnostics for MRD assays in September 2025, embedding proprietary Proteinase K formulations into bundled kits. Start-ups exploit white space in point-of-care where ProtonDx Dragonfly kits, validated during the 2025 mpox outbreak, delivered 100% sensitivity in under 40 minutes using lyophilized enzyme.

Quality credentials are differentiators as buyers demand ISO 13485 certificates, 21 CFR 820-compliant documentation, and digital COAs auto-uploaded to eQMS. Suppliers also tailor pack sizes and barcoded vials that integrate with robotics. Pricing remains stable for powder but competitive dynamics in liquids are pressuring margins by 2–3 percentage points annually as more vendors launch RT-stable SKUs.

Proteinase K Industry Leaders

Merck KGaA

Thermo Fisher Scientific

QIAGEN

Promega Corporation

F. Hoffmann-La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Canvax introduced a robust Proteinase K powder targeting demanding nucleic-acid workflows, providing high activity retention under chaotropic conditions.

- December 2025: Hyasen Biotech published “Proteinase K: The Golden Partner for Nucleic Acid Purification,” highlighting broad-spectrum utility across DNA/RNA extraction and proteomics research

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the proteinase K market as all standalone liquid, powder, or immobilized grades of the serine protease sold through catalog, OEM, or bulk channels for academic, diagnostic, and industrial workflows, irrespective of host expression or purity class.

Scope exclusion: Multienzyme extraction kits or sample-prep bundles that combine proteinase K with buffers, detergents, or other proteases are not sized here.

Segmentation Overview

- By Form

- Lyophilized Powder

- Liquid Solution

- By Purity Grade

- Standard Research Grade

- PCR / Molecular-Biology Grade

- GMP / Clinical Grade

- By Application

- Molecular Diagnostics

- Biopharmaceutical Manufacturing

- Forensic Science

- Food & Feed Testing

- Environmental Testing

- Other Applications

- By Source Type

- Fungal-Derived Native Enzyme

- Recombinant (Pichia pastoris, E. coli)

- Engineered / Synthetic Variants

- By End User

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

- Diagnostic Laboratories

- Contract Research Organizations

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with biobank managers, forensic DNA technicians, reagent distributors, and enzyme-production engineers across North America, Europe, and Asia validated average selling prices, purity-related discounts, and inventory turns. Targeted surveys of contract research organizations tested our preliminary demand pools and highlighted regional demand swings.

Desk Research

Mordor analysts began with public biomedical repositories such as PubChem, NCBI Protein, and the European Nucleotide Archive, which reveal usage intensity through citation volumes. Trade statistics from UN Comtrade (HS 3507), Eurostat, and the U.S. International Trade Commission traced cross-border enzyme flows, while regulatory dossiers from the FDA and the ECDC mapped approved diagnostic products containing proteinase K. Company 10-Ks, investor decks, and scientific society cost surveys enriched price and margin assumptions. Subscription platforms like D&B Hoovers and Dow Jones Factiva supplied revenue splits for niche suppliers. The sources named are illustrative; many additional references supported data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction converts global production and trade tonnage for HS 3507 into 2025 revenue using weighted ASPs, which are then stress-tested through sampled supplier roll-ups and academic purchase logs. Key variables like genomic sequencing run counts, forensic case backlogs, biopharma R&D spend, extraction-kit throughput, and currency-adjusted ASP arcs drive the model, and a multivariate regression with scenario analysis projects 2026-2030 growth. Gaps in bottom-up inputs are filled by triangulating peer price lists and distributor mark-ups before final sign-off.

Data Validation & Update Cycle

Outputs pass variance scans versus quarterly shipment alerts, reagent price indices, and FX movements. Senior reviewers interrogate anomalies, re-contact sources whenever a ±7% swing emerges, and refresh every study annually, with interim mini-updates for material events to keep clients current.

Why Our Proteinase K Baseline Deserves Trust

Published figures often diverge because firms pick different scopes, pricing ladders, and refresh cadences.

We report purified enzyme only, whereas some studies fold in full extraction kits or downstream diagnostic margins, thereby inflating totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 82.86 million | Mordor Intelligence | - |

| USD 5.22 billion | Global Consultancy A | Counts all protease reagents and bundled kit accessories |

| USD 4.82 billion (2024) | Trade Journal B | Uses 2024 FX rates and includes downstream diagnostic revenues |

The competitor values are taken from industry pages published in 2025 and 2024 respectively. These contrasts show how Mordor's disciplined scope, transparent variables, and yearly refresh deliver a balanced, repeatable baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current global value of the Proteinase K market?

The Proteinase K market was valued at USD 5.56 billion in 2026 and is projected to reach USD 8.06 billion by 2031.

Which form is growing fastest within Proteinase K workflows?

Ready-to-use liquid solutions are expanding at a 9.56% CAGR through 2031 as automation in high-throughput labs accelerates.

Why are recombinant Proteinase K variants gaining share?

Recombinant expression in Pichia pastoris and E. coli removes mycotoxin risk, improves batch consistency, and meets GMP documentation needs.

Which region shows the fastest demand growth?

Asia-Pacific is forecast to grow at 9.63% CAGR, fueled by more than USD 3 billion in CDMO investments announced in H1 2025.

How will upcoming regulations affect Proteinase K purchasing?

The EU IVDR and the U.S. LDT phaseout require fully validated reagents, pushing labs toward GMP-grade Proteinase K with detailed stability data.

Page last updated on: