Gluten-Free Bakery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

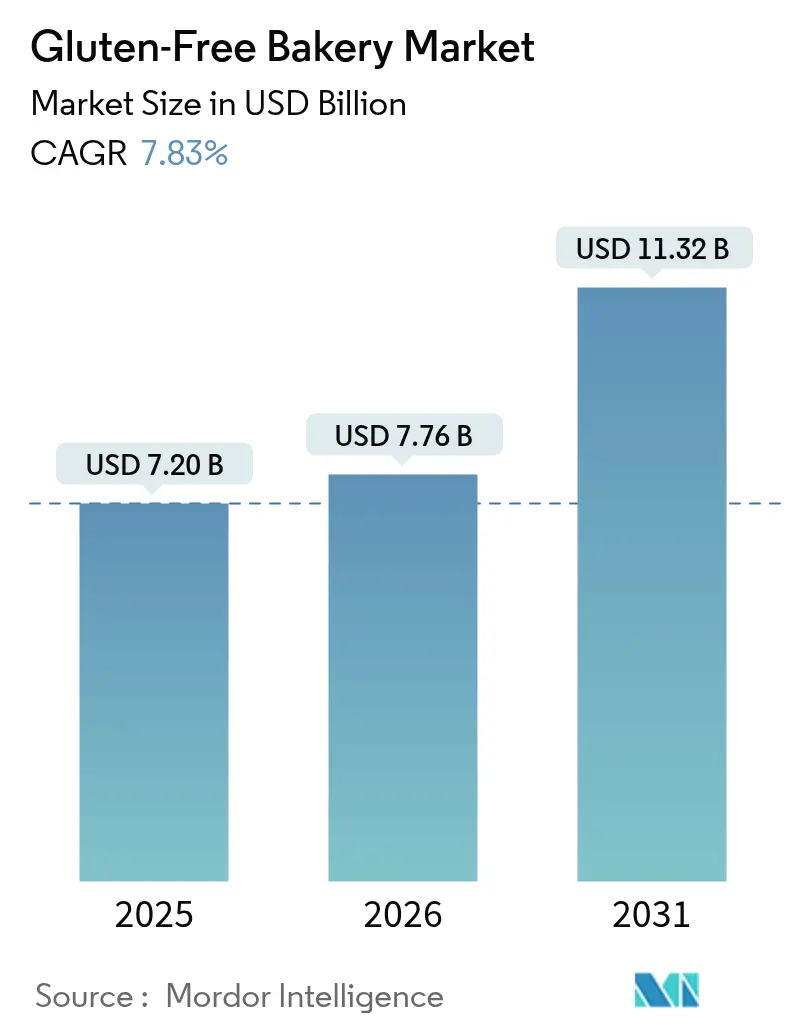

| Market Size (2026) | USD 7.76 Billion |

| Market Size (2031) | USD 11.32 Billion |

| Growth Rate (2026 - 2031) | 7.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gluten-Free Bakery Market Analysis by Mordor Intelligence

The gluten-free bakery market is expected to grow from USD 7.20 billion in 2025 to USD 7.76 billion in 2026 and is forecast to reach USD 11.32 billion by 2031 at 7.83% CAGR over 2026-2031. The market expansion is attributed to the increasing prevalence of celiac disease, which affects approximately 1% of the global population, and consumers who adopt gluten-free diets as a health-conscious decision, according to the National Institutes of Health. Besides, regulatory clarity also supports demand; the US FDA requires any product labeled “gluten-free” to contain less than 20 ppm gluten, giving shoppers confidence in safety and label accuracy. On the supply side, large bakeries continue to scale dedicated production lines, while smaller brands exploit online channels and direct-to-consumer (D2C) subscriptions to reach niche audiences. Persistent price premiums, cross-contamination risks, and climate-related grain shortages remain the key friction points, yet they have not slowed new-product velocity or capital investment.

Key Report Takeaways

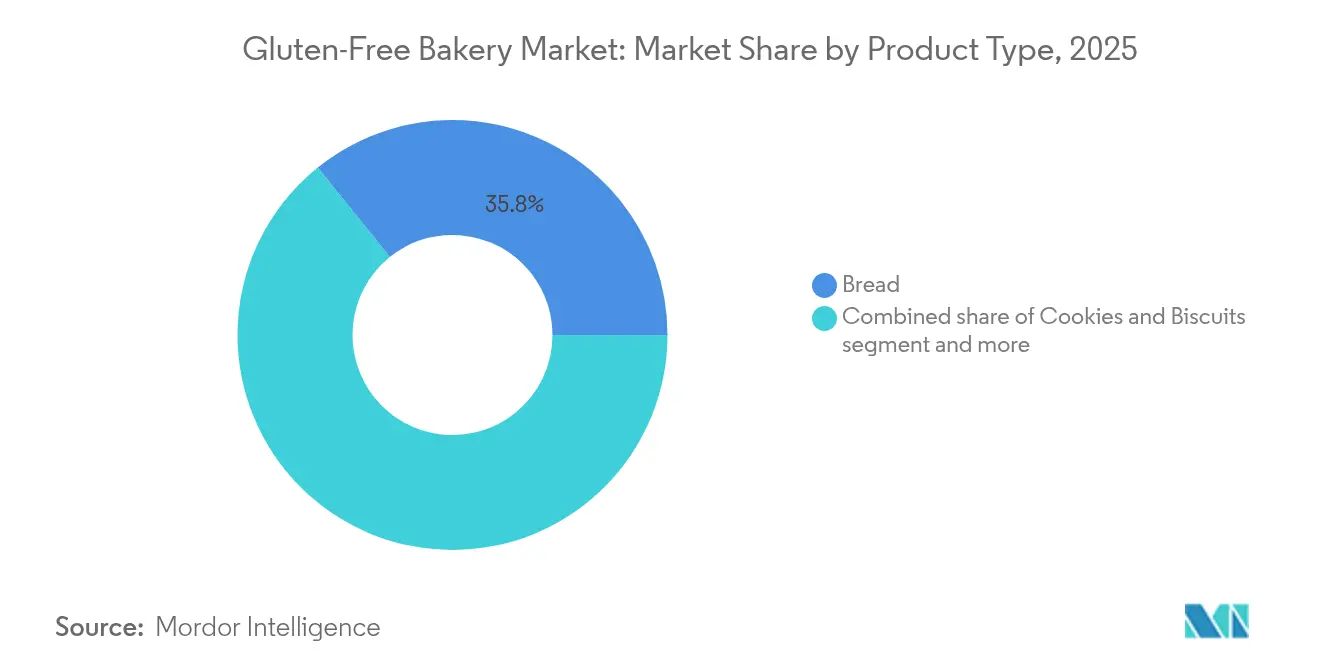

- By product type, bread led with 35.78% of the gluten-free bakery market share in 2025; cakes and muffins are forecast to post a 11.66% CAGR from 2026-2031.

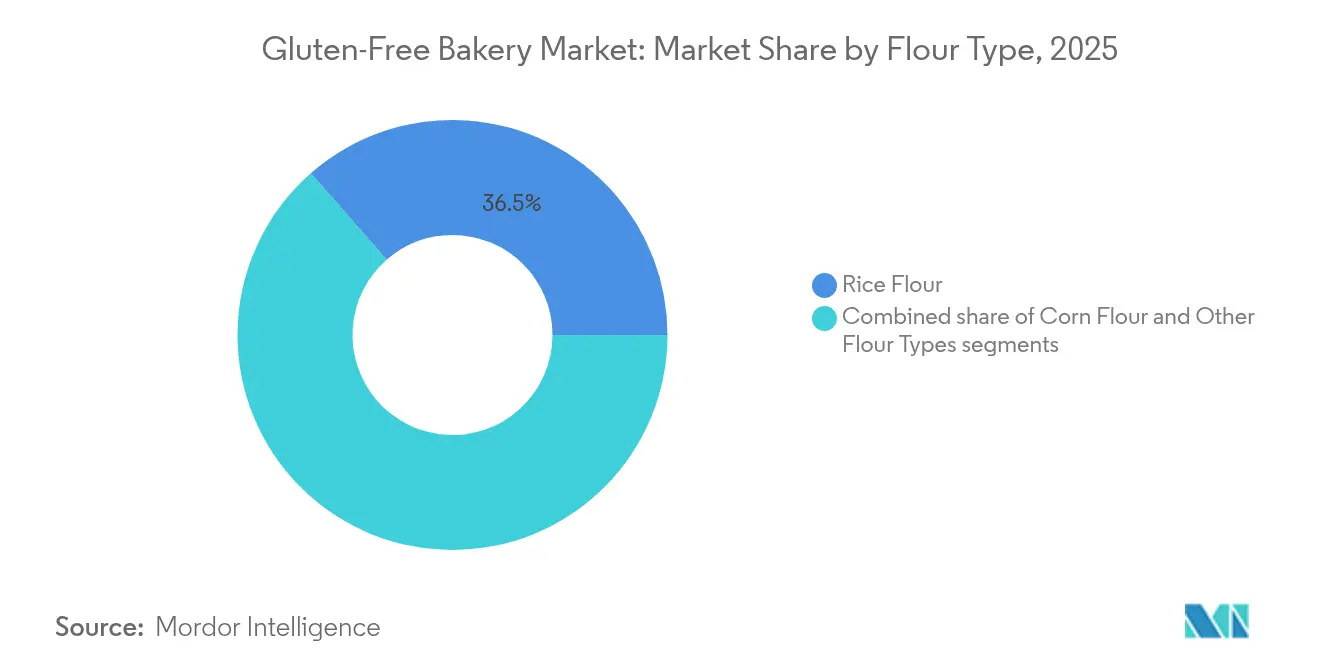

- By flour type, rice flour captured 36.45% share of the gluten-free bakery market in 2025; corn flour is anticipated to grow at a 7.55% CAGR through 2031.

- By distribution channel, supermarkets/hypermarkets held 33.86% of the gluten-free bakery market share in 2025, while online retail is projected to expand at a 14.21% CAGR to 2031.

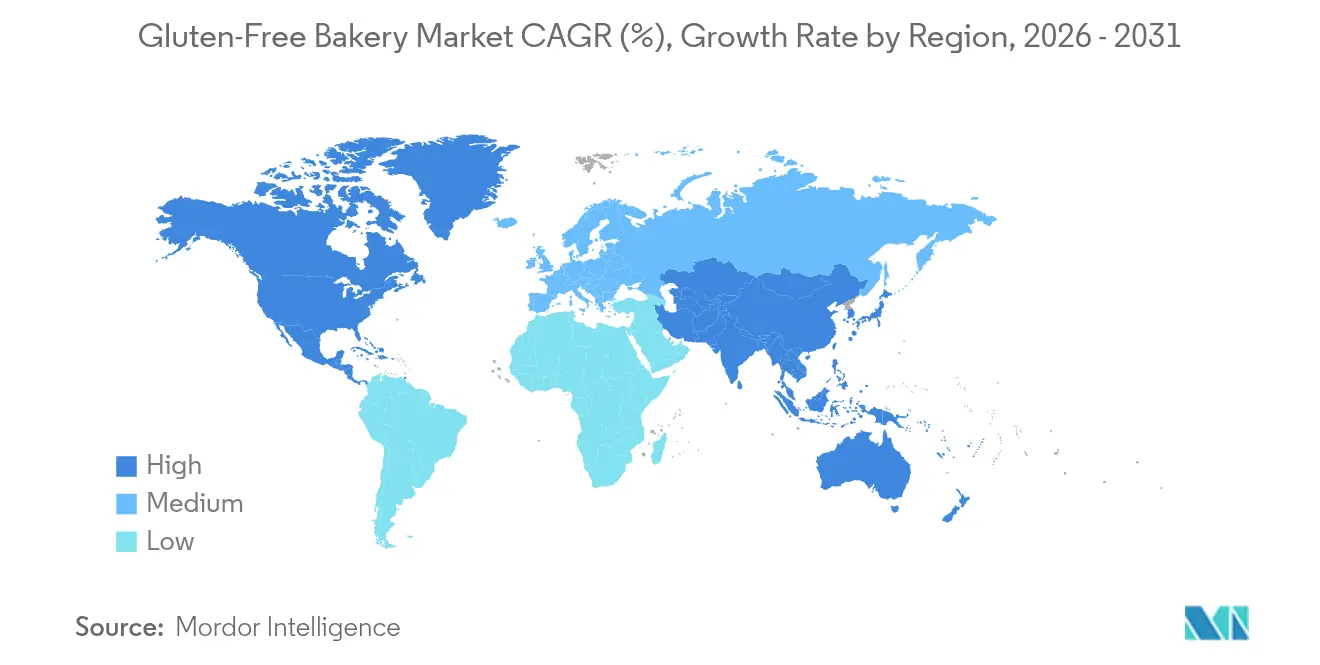

- By geography, North America commanded 33.42% of the gluten-free bakery market share in 2025, whereas Asia-Pacific is expected to advance at a 11.72% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gluten-Free Bakery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of celiac disease and gluten sensitivity | +1.8% | Global; higher rates in North America and Europe | Long term (≥ 4 years) |

| Clean-label “free-from” positioning by premium bakery brands | +1.2% | North America and Europe; widening to Asia-Pacific | Medium term (2-4 years) |

| Labeling laws and certifications build consumer trust | +0.9% | Global; led by North America | Medium term (2-4 years) |

| D2C subscription models boosting niche brand reach | +0.7% | North America and Europe; emerging in urban Asia-Pacific | Short term (≤ 2 years) |

| Increasing innovation and variety | +1.1% | Global; concentrated in developed markets | Medium term (2-4 years) |

| Influence of celebrity endorsements | +0.5% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of celiac disease and gluten sensitivity

The increasing prevalence of celiac disease, with 1 in 70 Australians affected according to the Australian Broadcasting Corporation's 2024 data and 1% prevalence in the US as reported by the Agency for Healthcare Research and Quality, generates market demand for gluten-free food options [1]Source: Australian Broadcasting Corporation, "Coeliac disease affects one in 70 Australians and it's on the rise, but diagnoses often fly under the radar", abc.net.au . The gluten-free bakery segment addresses the requirements of both medically diagnosed gluten-intolerant consumers and health-focused customers who select gluten-free products. Enhanced diagnostic capabilities and ongoing research into enzyme therapies and immune modulation are projected to increase consumer awareness of gluten sensitivity, strengthening the demand for gluten-free alternatives. Manufacturers are implementing product development strategies using alternative flours such as almond, rice, and quinoa to produce gluten-free baked goods that maintain quality standards comparable to conventional products. Companies implementing certified gluten-free labeling, supply chain transparency, and product quality optimization are positioned to capitalize on this expanding market. The gluten-free bakery segment, comprising artisan breads, muffins, and pastries, offers market opportunities for both large-scale manufacturers and specialized bakeries.

Clean-label “free-from” positioning by premium bakery brands

The gluten-free bakery market has evolved from serving medical needs to becoming a lifestyle choice through premium positioning and clean-label messaging. This shift allows manufacturers to increase profit margins and reach broader consumer segments. In 2024, Ardent Mills expanded its portfolio by introducing Ancient Grains Plus Baking Flour Blend and Egg Replace products across its network of over 40 gluten-free facilities, focusing on plant-based and sustainable solutions. Companies like Renewal Mill are addressing both ingredient transparency and environmental concerns by developing upcycled heirloom corn flour with gluten content below 5 ppm. However, manufacturers face the challenge of maintaining product functionality while meeting clean-label demands, as traditional gluten-free formulations depend on hydrocolloids and emulsifiers to achieve desired texture and shelf life.

Labeling laws and certifications build consumer trust

Regulatory standardization has driven the growth of the gluten-free bakery market by establishing measurable safety parameters. The FDA's definition of gluten-free, which sets a threshold at 20 parts per million (ppm), functions as a global standard, with countries like Canada implementing similar requirements through the Canadian Food Inspection Agency [2]Source: U.S. Food & Drug Administration (FDA), “'Gluten-Free' Means What It Says”, fda.gov . This standardization ensures that gluten-free labeled products meet safety specifications for individuals with celiac disease or gluten sensitivities. Third-party certifications from organizations like the Gluten-Free Certification Organization (GFCO) supplement government standards through enhanced requirements and systematic audits. These certifications minimize brand risk from mislabeling and potential recalls while increasing consumer confidence. In response, bakery manufacturers have allocated resources to dedicated gluten-free production facilities, implemented ingredient verification protocols, and developed standardized labeling practices to meet regulatory and certification requirements. The established regulatory and certification frameworks enable both established companies and specialized producers to develop compliant products that meet the requirements of consumers with medical conditions and lifestyle preferences.

D2C subscription models boosting niche brand reach

Subscription commerce breaks down traditional retail barriers, offering personalized nutrition and convenience that appeal to health-conscious consumers. This model thrives by addressing the discovery and availability issues gluten-free consumers face in conventional retail settings. Digital platforms not only facilitate data collection for tailored recommendations but also foster direct customer relationships, sidestepping the need for retailer negotiations. Additionally, subscription commerce provides consumers with the convenience of regular deliveries, ensuring consistent access to products that meet their dietary needs. Yet, challenges like subscription fatigue and high customer acquisition costs loom large. To sustain its growth trajectory, the model must continually innovate, diversifying its product range and differentiating its services to cater to evolving consumer preferences and expectations.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecasts | Geographic relevance | Impact Timeline |

|---|---|---|---|

| Premium price versus conventional bakery items | -1.4% | Global, most pronounced in price-sensitive emerging markets | Long term (≥ 4 years) |

| Cross-contamination risks in shared facilities of emerging markets | -0.8% | Asia-Pacific and Latin America, limited impact in mature markets | Medium term (2-4 years) |

| Shorter shelf-life of clean-label gluten-free bread | -0.6% | Global, particularly affecting distribution efficiency | Medium term (2-4 years) |

| Climatic volatility affecting specialty flour supply | -0.7% | Global, concentrated in agricultural regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium price versus conventional bakery items

The elevated pricing of gluten-free bakery products results from the high cost of ingredient alternatives to wheat flour, including rice, tapioca, sorghum, and almond flour. These alternative ingredients do not provide the binding and elastic properties of gluten, requiring manufacturers to implement more complex formulations for baked goods. Operational costs increase due to the necessity for dedicated gluten-free manufacturing facilities or separate production lines to prevent cross-contamination, combined with reduced production volumes. The manufacturing process requires increased labor allocation and rigorous quality control protocols due to the technical challenges of gluten-free doughs, which demonstrate reduced stability and increased adhesion compared to conventional doughs. In North American and European markets, the current competitive landscape enables manufacturers to maintain premium pricing while implementing product certifications and safety protocols. This pricing structure may shift as production capacity increases, manufacturing processes automate, and market entrants introduce cost-effective alternatives. In emerging markets, the premium pricing of gluten-free bakery products continues to impede market penetration, despite increasing consumer awareness of gluten sensitivities and health considerations among populations with constrained purchasing power.

Cross-contamination risks in shared facilities of emerging markets

Manufacturing safety concerns create significant barriers in markets lacking robust regulatory oversight and dedicated production infrastructure. Studies in China reveal gluten contamination in labeled gluten-free products often exceeds safe limits, highlighting enforcement gaps in emerging markets. Cross-contamination risks extend beyond manufacturing to include shared transportation, storage, and retail environments where gluten-containing products dominate supply chains. The challenge intensifies in markets where gluten-free awareness remains limited among food service workers and supply chain partners. Enzymatic cleaning methods show promise for gluten removal from surfaces and equipment, but implementation requires training and investment that many smaller manufacturers cannot afford.

Segment Analysis

By Product Type: Bread Dominance Faces Indulgent Category Surge

Bread maintains a commanding 35.78% market share in 2025, reflecting its status as a dietary staple that consumers prioritize when transitioning to gluten-free diets. However, the cakes, muffins, and brownies segment accelerates at 11.66% CAGR through 2031, indicating evolving consumer expectations beyond basic nutrition toward indulgent experiences. Lancaster Colony launched its first gluten-free frozen bread line under the New York Bakery brand in September 2024, featuring patent-pending formulation technology that enhances texture and flavor while maintaining certification standards. Cookies and biscuits occupy the middle ground, benefiting from portion control appeal and longer shelf life advantages that facilitate distribution and inventory management.

In January 2024, Nothing Bundt Cakes introduced new gluten-free products, aligning with the market trend of mainstream bakery chains expanding their gluten-free portfolios to address increasing consumer demand. This expansion demonstrates the segment's commercial potential beyond niche markets. The bakery products segment has diversified through the incorporation of protein-enriched and functional ingredients, meeting consumer requirements for baked goods with enhanced nutritional benefits beyond gluten-free attributes.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Acceleration Reshapes Retail Landscape

Supermarkets/hypermarkets command a 33.86% share in 2025 through dedicated gluten-free sections and improved product placement, yet online retail surges at a 14.21% CAGR as consumers seek convenience and product variety unavailable in physical stores. Digital platforms solve discovery challenges inherent in gluten-free shopping, enabling detailed ingredient analysis and customer reviews that build purchase confidence. Convenience stores capture impulse purchases and emergency needs, while specialist stores maintain premium positioning through expert curation and customer education. The "other distribution channels" category encompasses food service, direct sales, and emerging formats like automated retail and subscription boxes.

Moreover, e-commerce growth accelerates through subscription models that guarantee product availability and enable personalized nutrition approaches. Wildgrain's success with over 80,000 subscribers demonstrates consumer willingness to pay premiums for convenience and quality assurance. However, cold chain requirements and shipping costs create profitability challenges that favor shelf-stable products over fresh alternatives. Traditional retailers respond through click-and-collect services and expanded online catalogs that leverage existing distribution infrastructure while meeting digital expectations.

By Flour Type: Rice Flour Leadership Challenged by Corn Innovation

In 2025, rice flour commands a dominant 36.45% share of the market, owing to its neutral flavor, fine texture, and well-established supply chains, especially from Asian agricultural hubs. Rice flour's versatility in various culinary applications further solidifies its position as a staple in the market. Meanwhile, corn flour is on an upward trajectory, boasting a 7.55% CAGR growth rate projected through 2031. This surge is largely attributed to its sustainable positioning and functional enhancements that rectify traditional taste and texture shortcomings.

Moreover, the growing consumer preference for gluten-free diets is increasing the use of corn flour, a naturally gluten-free ingredient in bakery and snack products. Alternative flours, including quinoa, sorghum, chickpea, and lentil varieties, are experiencing increased market adoption. These alternatives offer higher nutritional value through increased protein, fiber, and micronutrient content while meeting consumer demands for sustainable food options. Consumers seeking healthier options are selecting these flours for their minimal processing and health benefits. In response, manufacturers are developing new bakery products using these alternative flours to address both nutritional requirements and environmental considerations.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America holds 33.42% market share in 2025, supported by high consumer awareness, well-established regulatory frameworks, and premium positioning strategies that drive per capita revenue. The region's market leadership stems from sophisticated distribution networks, strong retail partnerships, and continuous product innovation. Consumer preferences in North America increasingly favor premium gluten-free options, particularly in snacks and bakery segments. The market demonstrates sustained growth potential through expanding product categories and enhanced nutritional profiles.

Asia-Pacific demonstrates the highest growth rate at 11.72% CAGR through 2031, fueled by increasing disposable incomes, urbanization trends, and growing health consciousness among middle-class consumers. The IFIA/HFE 2024 exhibition in Japan highlighted gluten-free bakery product innovations, including specialized madeleines, demonstrating manufacturers' growing focus on Asian markets. Regional market development is supported by improving retail infrastructure and digital commerce platforms. India's FSSAI extended foreign food manufacturing facility registration deadlines to September 2024, creating market entry opportunities for international brands, as reported by the United States Department of Agriculture.

Europe shows increasing demand for gluten-free bakery products, particularly in the bakery segment, with strong growth in countries like Germany, France, and the United Kingdom. Market participants are developing new gluten-free bakery options in response to rising health consciousness and awareness among consumers, focusing on taste improvement and texture enhancement. For instance, IfD Allensbach reported that 2.16 million consumers in Germany purchased gluten-free products within 14 days in 2024 . Moreover, in June 2025, gluten-free food manufacturer Juvela introduced a new bakery brand, Oaf, offering bread and related products, exemplifying the market's innovation trajectory. The region's growth is further supported by stringent food labeling regulations, increased celiac disease diagnosis rates, and expanding retail distribution channels.

Competitive Landscape

The gluten-free bakery market demonstrates moderate consolidation, with both established manufacturers and new entrants competing across product categories and distribution channels. Key market players include Dr. Schar AG/SpA, General Mills, Inc., Hain Celestial Group, and Grupo Bimbo SAB de CV. These companies are expanding their distribution through e-commerce platforms and specialty stores, while local bakeries serve regional markets with fresh, premium products. The market continues to grow as consumer awareness of gluten intolerance increases and demand for health-focused products rises.

To cater to health-conscious consumers, companies are rolling out premium product lines featuring clean-label, organic, and functional gluten-free bakery items. These firms bolster their market presence via retail collaborations, securing independent certifications, and committing to continuous product development. By focusing on these strategies, companies aim to address the growing demand for healthier alternatives while differentiating themselves in a competitive market.

Data analytics technology is now pivotal for fine-tuning distribution and managing inventory. It enables companies to predict demand patterns, reduce waste, and ensure product availability, thereby enhancing operational efficiency. As leading food corporations expand their gluten-free offerings, the market trends towards consolidation. Yet, specialized producers boasting direct-to-consumer channels can uphold their independence, thanks to premium positioning and robust customer loyalty initiatives. These producers leverage their niche expertise and personalized customer engagement to maintain a competitive edge.

Gluten-Free Bakery Industry Leaders

-

General Mills, Inc.

-

Hain Celestial Group

-

Grupo Bimbo SAB de CV

-

Hero Group AG

-

Dr. Schar AG/SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tim Tam, the Australian chocolate biscuit brand, introduced its gluten-free products in the United States through Albertsons stores nationwide. The expansion addressed the increasing consumer demand for gluten-free alternatives while maintaining the brand's signature indulgent taste.

- March 2025: Doughlicious expanded its product portfolio by introducing a range of vegan and gluten-free gourmet cookies in Double Chocolate Chip, Salted Caramel, Chocolate Chip, and Banana Good Granola variants. The company established distribution channels through Hunt's Food Group and Amazon to serve independent convenience retailers.

- December 2024: Dr. Schär expanded its product range through the introduction of Artisan Baker White Bread and Deli Style bread in all Publix retail stores, which increased product accessibility for consumers. The Artisan Baker White Bread featured a soft texture and rich flavor, which made it suitable for sandwiches and toast.

- August 2024: Lancaster Colony Corp. developed a gluten-free frozen bread line under the New York Bakery brand, which included Garlic Texas Toast and Five Cheese Texas Toast varieties. The company formulated these products using a patent-pending process that established a foundation for future product development.

Global Gluten-Free Bakery Market Report Scope

Gluten-free bakery refers to bakery products that do not contain gluten - a protein found in many cereal grains such as wheat, barley, etc.

The global gluten-free bakery market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into bread, cookies & biscuits, cakes & muffins, and other gluten-free products. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialist stores, online channels, and others. By geography, the global gluten-free bakery market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

For each segment, the market sizing and forecasting have been done in value terms (USD million).

| Bread |

| Cookies and Biscuits |

| Cakes, and Muffins (includes cupcakes) |

| Other Gluten-Free Bakery Products (brownies) |

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Specialist Stores |

| Online Retail |

| Other Distribution Channels |

| Corn Flour |

| Rice Flour |

| Other Flour Types |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Bread | |

| Cookies and Biscuits | ||

| Cakes, and Muffins (includes cupcakes) | ||

| Other Gluten-Free Bakery Products (brownies) | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Specialist Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Flour type | Corn Flour | |

| Rice Flour | ||

| Other Flour Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the gluten free bakery products market?

The gluten free bakery products market is valued at USD 7.76 billion in 2026 and is projected to reach USD 11.32 billion by 2031, growing at a 7.83% CAGR.

Which product segment leads the market?

Bread remains the largest segment, holding 35.78% revenue share in 2025, though cakes and muffins are the fastest-growing at a 11.66% CAGR through 2031.

Which region is expected to grow fastest?

Asia-Pacific is forecast to expand at a 11.72% CAGR to 2031 due to rising diagnoses, regulatory harmonization and digital retail adoption.

What factors most influence market growth?

Key drivers include higher celiac disease prevalence, clean-label consumer preferences, stringent labeling laws and the rise of D2C subscription services.