Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

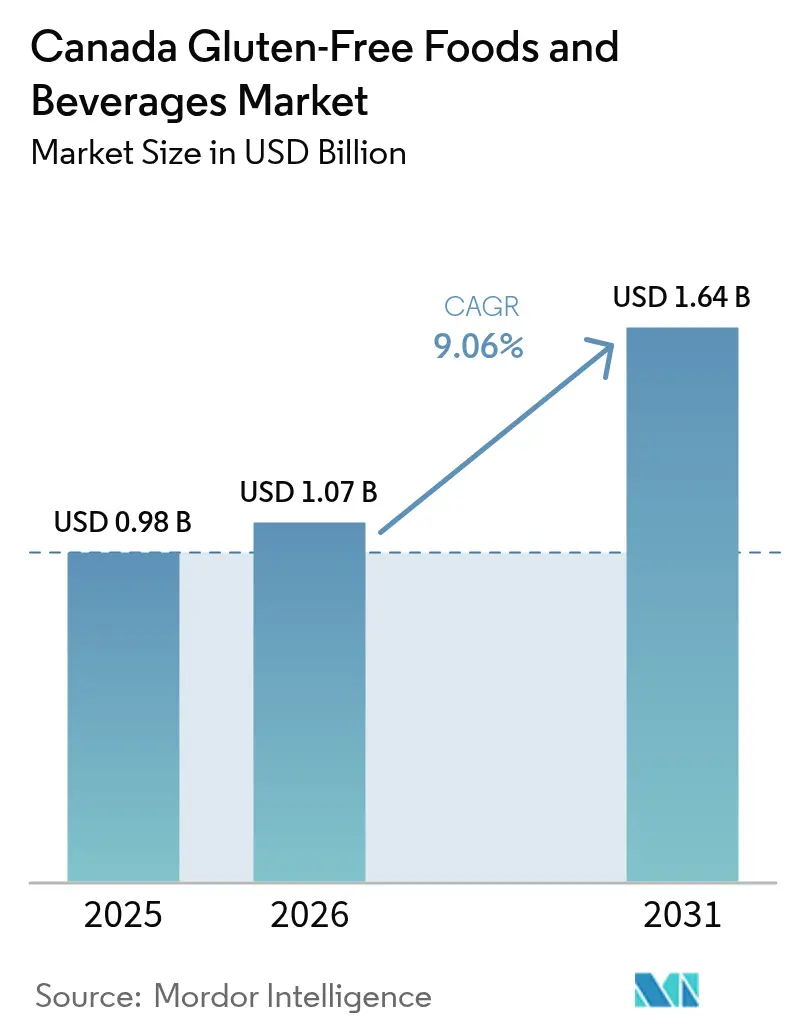

| Base Year Market Size (2025) | USD 0.977 Billion |

| Market Size (2026) | USD 1.07 Billion |

| Market Size (2031) | USD 1.64 Billion |

| Growth Rate (2026 - 2031) | 9.06% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Gluten-Free Foods & Beverages Market Analysis by Mordor Intelligence

The Canada gluten-free foods and beverages market size in 2026 is estimated at USD 1.07 billion, growing from 2025 value of USD 0.977 billion with 2031 projections showing USD 1.64 billion, growing at 9.06% CAGR over 2026-2031. Momentum comes from the 400,000 clinically diagnosed celiac consumers, an expanding group of self-diagnosed gluten-sensitive shoppers, and Health Canada’s <20 ppm rule that anchors trust in certified labels.[1]Canadian Food Inspection Agency, “Undeclared allergens and gluten in ground spices/herbs,” inspection.gc.ca Major grocery chains have enlarged private-label assortments, while e-commerce subscriptions simplify replenishment for households that cannot risk out-of-stock events. Ingredient innovation led by pulse-based flours is improving texture and protein density, encouraging repeat purchases even among lifestyle adopters. At the same time, sustained price premiums and cross-contamination concerns continue to check total category uptake, especially among lower-income families.

Key Report Takeaways

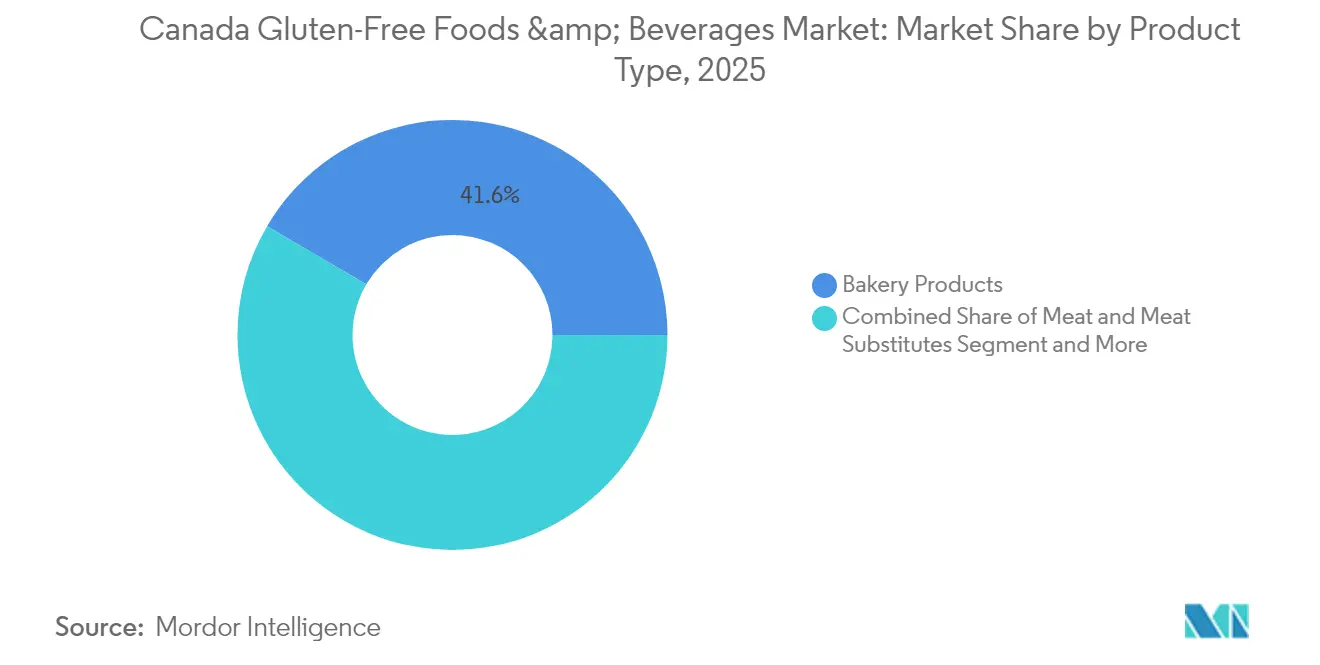

- Bakery products accounted for 41.55% of the market share in 2025, where as meat and meat substitutes recorded the fastest 10.35% CAGR within the Canada gluten-free foods and beverages market size through 2031.

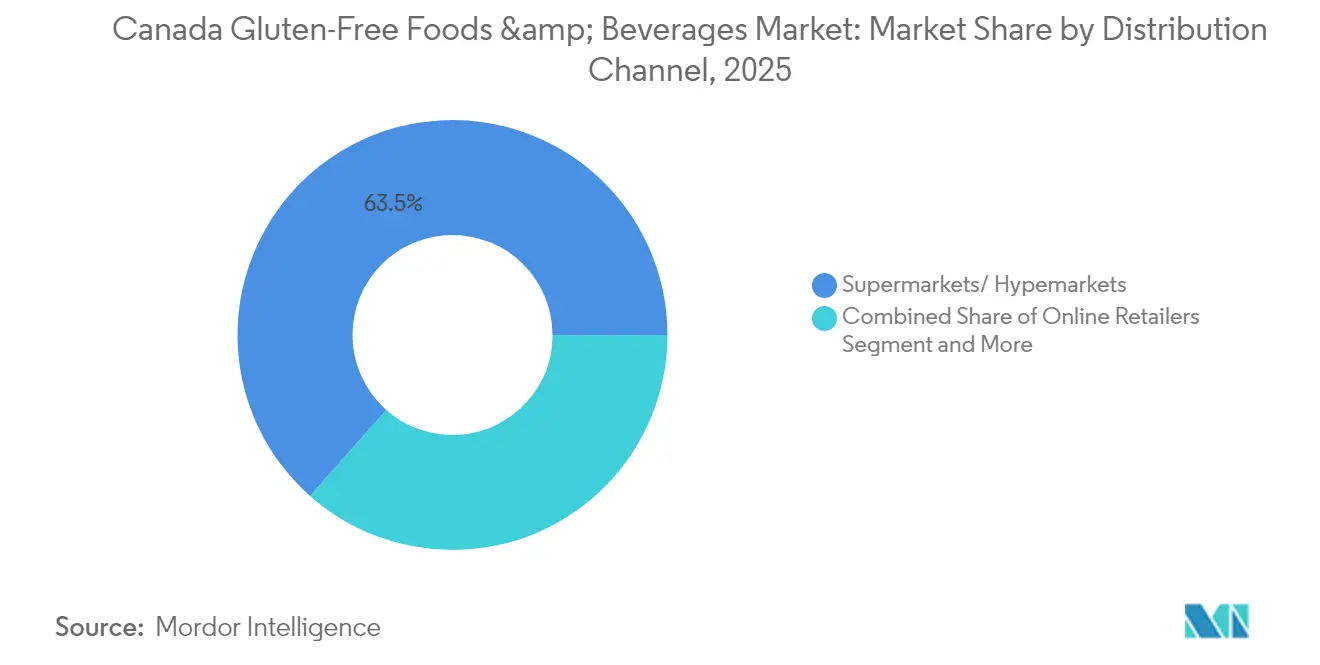

- Supermarkets and hypermarkets held 63.47% of the market share in 2025, and online retailers are expanding at a 13.05% CAGR in the Canada gluten-free foods and beverages market through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Gluten-Free Foods & Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of celiac disease & non-celiac gluten sensitivity | +1.8% | Urban centers nationwide | Long term (≥ 4 years) |

| Mainstream grocery chains adding private-label lines | +1.5% | Ontario and Quebec first | Medium term (2-4 years) |

| Digestive-wellness and weight-management perception | +1.2% | BC and large metros | Medium term (2-4 years) |

| Third-party “Certified GF” logos | +0.9% | Major metro markets | Short term (≤ 2 years) |

| Pulse-based flour reformulation | +0.7% | Prairie supply clusters | Medium term (2-4 years) |

| Allergen-free snack demand in schools post-2025 | +0.6% | Ontario, BC, Alberta | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of celiac disease and non-celiac gluten sensitivity

Medical diagnosis rates are accelerating beyond historical patterns, with celiac disease incidence rising year on year. This clinical momentum extends beyond diagnosed cases, as Health Canada's regulatory framework acknowledges the broader population affected by gluten sensitivity through its comprehensive labeling requirements for wheat, rye, and barley-containing products. The diagnostic expansion is particularly pronounced in urban centers where access to specialized gastroenterology services enables earlier detection and formal confirmation of gluten-related disorders. Consumer awareness campaigns by organizations like the Canadian Celiac Association are driving testing rates higher, with British Columbia alone listing multiple specialized gluten-free producers and vendors across categories from craft beer to bakery products[2]Canadian Celiac Association British Columbia. "Celiac in the News." January 1, 2024. https://bcceliac.ca/celiac-in-the-news.html. This medical foundation creates sustained demand that transcends lifestyle trends, establishing a baseline market floor that supports long-term industry investment and innovation.

Mainstream grocery chains expanding private-label gluten-free lines

Retail consolidation is accelerating private-label development as major chains recognize the category's premium pricing potential and customer loyalty benefits. President's Choice achieved Gluten-Free Certification Program (GFCP) certification for its bakery products in January 2025, while Sobeys expanded its Compliments Gluten-Free line in March 2025, demonstrating the strategic priority retailers place on controlled-brand differentiation. Metro's refresh of its Irresistibles brand and Walmart's launch of Great Value Organics reflect broader industry recognition that gluten-free private labels can command higher margins while building customer retention through perceived value and quality assurance. The GFCP certification process, managed by Milton, Ontario-based Allergen Control Group Inc., provides retailers with third-party validation that reduces liability concerns while enabling premium positioning. This trend fundamentally alters competitive dynamics by giving major retailers direct control over product development, pricing, and shelf placement in the category's most valuable real estate.

Growing perception of gluten-free diets as key to weight management & digestive wellness

Consumer behavior research reveals that gut health concerns are driving adoption beyond medical necessity, with Danone/Activia reporting that 57% of Canadians want to improve gut health but lack knowledge about effective approaches[3]Taste Tomorrow. "Food trends following the gut health boom." July 12, 2024. https://www.tastetomorrow.com/inspiration/Food-trends-following-the-gut-health-boom. This knowledge gap creates opportunities for gluten-free products positioned with digestive wellness claims, particularly when combined with prebiotic-enriched formulations or sprouted grain technologies like those used by Canadian Silver Hills Bakery. The intersection of weight management and digestive health perceptions is reinforced by the premium pricing structure of gluten-free products, which can exceed regular equivalents by 150-500%, creating a psychological association between higher cost and superior health benefits. However, this trend also generates consumer skepticism toward ultra-processed gluten-free substitutes, as health-conscious buyers increasingly scrutinize ingredient lists and processing methods. The challenge for manufacturers lies in balancing convenience with clean-label positioning while maintaining the functional properties that consumers expect from gluten-free alternatives.

Proliferation of third-party "Certified-GF" logos boosting shopper trust

Certification programs are becoming essential market differentiators as consumers seek assurance beyond basic labeling claims, with the Gluten-Free Certification Program (GFCP) emerging as a key trust signal for Canadian products. The GFCP, operated by Allergen Control Group Inc. and endorsed by the Canadian Celiac Association, provides manufacturers with recognizable trademark symbols that simplify purchasing decisions for both medical and lifestyle consumers. This certification trend extends beyond individual products to facility-level validation, as demonstrated by companies like Yourbarfactory, which maintains nut-free, peanut-free, and gluten-free facility certifications with annual third-party audits Yourbarfactory. The proliferation of certification logos addresses a critical market failure where consumers struggle to distinguish between products that meet medical-grade standards and those making general gluten-free claims. Regulatory compliance factors include adherence to Health Canada's <20 ppm threshold and CFIA's Safe Food for Canadians Regulations, which require valid SFC licenses for importing manufactured foods including many gluten-free ingredients and finished products.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price premium versus conventional counterparts | -2.1% | National, with acute impact on lower-income demographics | Long term (≥ 4 years) |

| Cross-contamination risk in co-manufacturing facilities | -1.3% | National, concentrated in provinces with shared manufacturing | Medium term (2-4 years) |

| Supply shortage of certified gluten-free oats | -0.8% | National, with supply chain impacts from Prairie provinces | Short term (≤ 2 years) |

| Consumer scepticism toward ultra-processed GF substitutes | -0.7% | National, stronger in health-conscious urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price premium versus conventional counterparts

The economic burden of gluten-free products creates significant market friction, with Canadian research documenting cost premiums ranging from 150% to 500% compared to conventional alternatives, translating to over CAD 1,000 in additional annual food costs per person. This pricing structure forces many consumers to make difficult trade-offs between medical necessity and household budgets, with Celiac Canada surveys reporting increased food bank usage among people with celiac disease and perceived post-pandemic price increases creating additional financial hardship. The premium pricing paradox is particularly acute for families with multiple affected members, where the cumulative cost impact can represent a substantial portion of discretionary income. While some policy discussions focus on grocery rebates as potential relief mechanisms, economists warn that such interventions could inadvertently drive prices higher by increasing demand without addressing underlying supply constraints. The more sustainable solution involves increasing competition and supply capacity, drawing parallels to the plant-based category where expanded production scale and competitive entry have gradually reduced price premiums over time.

Cross-contamination risk in co-manufacturing facilities

Manufacturing infrastructure limitations create persistent quality and liability concerns that constrain market expansion, as evidenced by CFIA surveillance data showing 26% of ground spice and herb samples containing undeclared allergens including gluten at levels ranging from 5.7 to 550 ppm. These contamination risks are particularly problematic for co-manufacturing arrangements where shared equipment and facilities process both gluten-containing and gluten-free products, requiring extensive cleaning protocols and testing procedures that increase operational costs and complexity. The challenge is compounded by the medical necessity of maintaining <20 ppm gluten levels for celiac consumers, where even trace contamination can trigger adverse health reactions and potential legal liability. Companies like Fun Foods Canada and Yourbarfactory are addressing this constraint by maintaining dedicated gluten-free facilities with comprehensive allergen control systems, but such infrastructure investments require significant capital commitments that limit market entry for smaller players. The regulatory environment under CFIA's Safe Food for Canadians Regulations adds additional compliance complexity for manufacturers and importers, requiring valid SFC licenses and comprehensive preventive control plans that address contamination risks throughout the supply chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Bakery Products Lead Traditional Demand

Bakery products represented 41.55% of the market share in 2025, underscoring their role as everyday staples for newly diagnosed consumers. The segment’s dominance rests on the technical challenge of replicating wheat structure; brands that master texture secure strong repeat rates. General Mills and Grupo Bimbo leverage scale to maintain competitive shelf pricing and nationwide distribution. However, consciousness around sugar and refined starch is prompting reformulation toward pulse-flour blends rich in protein.

Meat and meat substitutes posted a 10.35% CAGR, the fastest within the Canada gluten-free foods and beverages market. Protein-rich positioning appeals to consumers who lose traditional wheat-based protein sources. Plant-based innovators exploit the overlap of allergen-free, vegan, and environmental narratives. The Good Flour Corp’s PureMelt Cheeeze™ entered 200 Panago Pizza outlets in April 2025, showing foodservice pull for multi-attribute SKU's. Pulse concentrates deliver amino-acid completeness without gluten binders, allowing cleaner decks than soy-textured options.

By Distribution Channel: Supermarkets Maintain Retail Dominance

Supermarkets and hypermarkets claimed 63.47%, share during 2025. Diagnosed shoppers gravitate toward one-stop basket fulfillment where certified breads, snacks, and frozen meals sit in unified sections. Retailers reward premium margins by granting top-shelf sets and running periodic “Allergen-friendly” endcaps. Loyalty programs mine purchase data to personalize coupons, enhancing stickiness for high-value households who average larger ticket sizes. Private-label penetration accelerates as chains harness direct sourcing to narrow price gaps with conventional staples, thereby softening the restraint of cost premiums.

The online channel is expanding at 13.05% CAGR, the swiftest in the Canada gluten-free foods and beverages market. E-commerce solves discovery pain points through filter tools that isolate “Certified GF” SKUs and cross-reference other allergens. Subscription boxes stabilize replenishment for pantry staples, shielding consumers from brick-and-mortar stockouts. Higher average selling prices absorb delivery fees with less resistance than conventional groceries. Digital-native brands capitalize on direct customer feedback loops to iterate flavors and textures faster than shelf-planogram cycles allow.

Geography Analysis

Ontario and Quebec lead Canada's gluten-free food and beverage market due to high population density and retailer concentration. In 2026, Ontario's market size surpassed USD 0.38 billion, followed by Quebec at just over USD 0.24 billion, driven by prevalence rates and extensive private-label assortments. Urban consumers frequently purchase fresh gluten-free baked goods, while policies like PPM 150 increase demand for certified snacks in school lunches. Western provinces, particularly British Columbia and Alberta, show strong growth. BC's wellness culture drives higher per-capita spending, and its e-commerce channel is expanding as Metro Vancouver consumers opt for home delivery of niche products. Alberta's medically driven market base also contributes significantly to the region's performance.

Prairie provinces, led by Saskatchewan and Manitoba, play a key role in ingredient supply, with pulse processors supporting national formulations and provincial governments funding extrusion-technology pilots for gluten-free snacks. Atlantic Canada faces challenges due to dispersed populations and limited facilities, leading to higher reliance on online orders and inflated prices from freight costs. However, targeted tourism campaigns promoting celiac-safe menus in PEI and Newfoundland highlight potential growth opportunities if supply chains improve.

Competitive Landscape

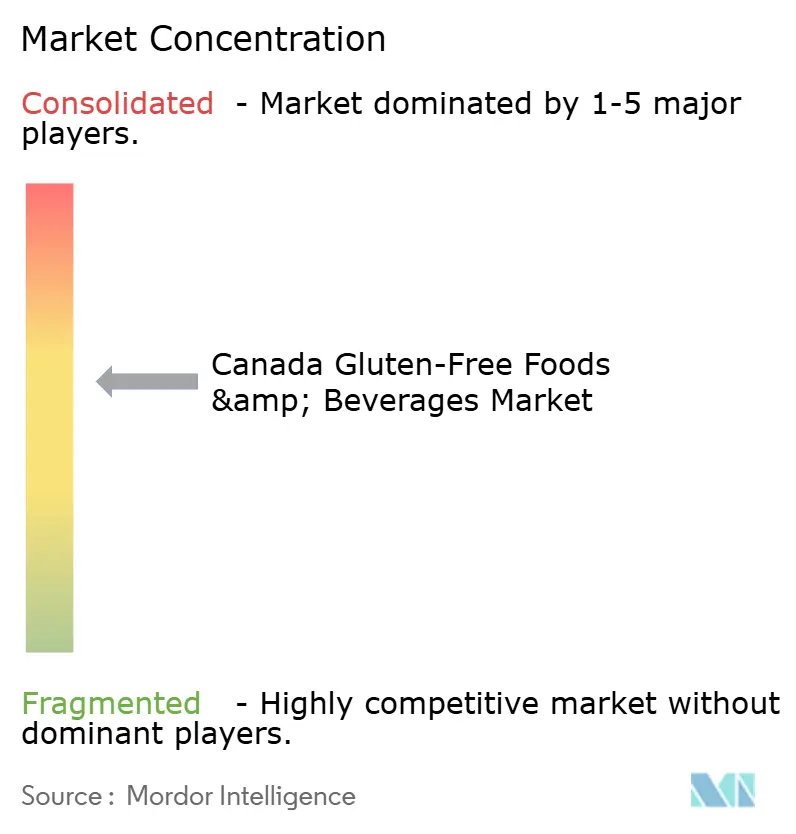

Canada's gluten-free food and beverage market demonstrates moderate concentration, scoring a 6 on a 10-point intensity scale. General Mills leads with a market share through brands like Cheerios, Betty Crocker, and Cascadian Farm, supported by strong logistics. Grupo Bimbo follows, driven by Dempster’s Gluten-Zero and Little Northern Bakehouse, while Nestlé focus on prepared meals and snacks. Specialist firms like Nature’s Path Foods and Kinnikinnick Foods also play key roles, with the latter set for 40% capacity growth by 2026 after its acquisition by English Bay Blending in April 2025.

Vertical integration and technological advancements are shaping the competitive landscape. Yourbarfactory produces 400 million bars annually near Montreal, targeting school-snack contracts with nut-free, peanut-free, and gluten-free claims. The Good Flour Corp diversifies into foodservice with allergen-free pizza toppings. Investments in optical sorting, rapid-gluten PCR, and blockchain traceability aim to reduce recall risks and enhance marketing credibility. As private-label offerings expand and pulse-protein capacity grows, competition is expected to intensify, enabling second-tier grocers to introduce house brands more easily.

Canada Gluten-Free Foods & Beverages Industry Leaders

-

Grupo Bimbo

-

General Mills Inc.

-

Nestlé S.A.

-

Nature’s Path Foods

-

Kinnikinnick Foods Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Natura, based in Montreal, introduced a range of plant-based oat beverages made from 100% organic Canadian and gluten-free oats. The oat beverages are available in three flavors, Original, Vanilla, and Chocolate, and are claimed to be the only gluten-free oat drinks holding a Canadian Coeliac stamp, ensuring safety for consumers concerned about gluten.

- February 2023: NEX-XOS introduced OBAR by OMEALS, a versatile daily bar that can serve as a meal replacement or nutrition bar. NEX-XOS specializes in producing shelf-stable foods and providing contract packaging, assembly, and distribution services. The OBAR daily bars offered by NEX-XOS are nutrient-dense, plant-based, allergen-free, gluten-free, and non-GMO.

Canada Gluten-Free Foods & Beverages Market Report Scope

Gluten-free food and beverages are products, either in whole or processed form, which are free from gluten, a mixture of proteins found in wheat and related grains.

The Canadian gluten-free foods and beverages market is segmented by type and distribution channel. Based on type, the market is segmented into beverages, bakery products, savory snacks, dairy and dairy-free food, meat and meat substitutes, and other types. By distribution channel, the market is segmented into supermarkets/hypermarkets, online retail channels, convenience/grocery stores, and other distribution channels.

The market sizing has been done in value (USD) for all the abovementioned segments.

By Type

| Beverages |

| Bakery Products |

| Savory Snacks |

| Dairy and Dairy-free Food |

| Meats and Meat Substitutes |

| Other Types |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Online Retail Channels |

| Convenience / Grocery Stores |

| Other Channels |

| By Type | Beverages |

| Bakery Products | |

| Savory Snacks | |

| Dairy and Dairy-free Food | |

| Meats and Meat Substitutes | |

| Other Types | |

| By Distribution Channel | Supermarkets / Hypermarkets |

| Online Retail Channels | |

| Convenience / Grocery Stores | |

| Other Channels |

Key Questions Answered in the Report

What is the 2026 value of Canada’s gluten-free foods and beverages sector?

The category is valued at USD 1.07 billion in 2026.

How fast is the segment for meat and meat substitutes expanding?

It is projected to advance at a 10.35% CAGR to 2031.

Which retail channel holds the largest share?

Supermarkets and hypermarkets commanded 63.47% of 2025 sales.

Why are certification logos important to Canadian shoppers?

GFCP and similar seals provide medical-grade assurance that products meet Health Canada’s <20 ppm threshold.

What main factor restrains broader adoption?

A 150-500% price premium over conventional products limits uptake among budget-sensitive households.

Page last updated on: