Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

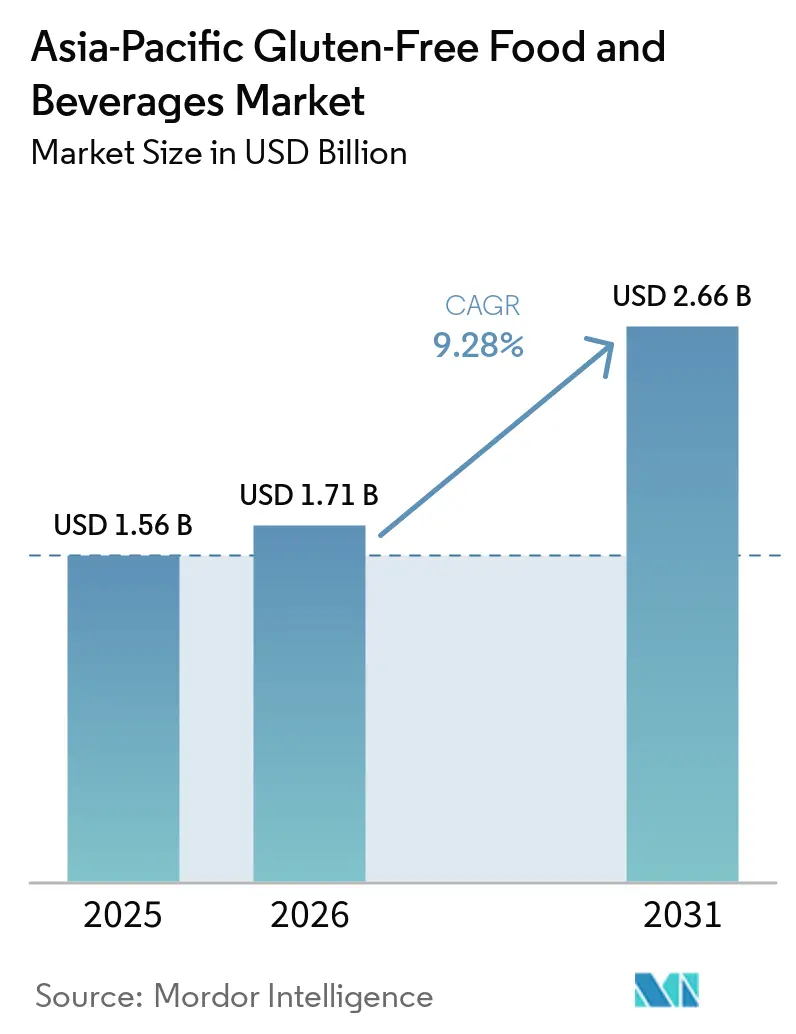

| Base Year Market Size (2025) | USD 1.56 Billion |

| Market Size (2026) | USD 1.71 Billion |

| Market Size (2031) | USD 2.66 Billion |

| Growth Rate (2026 - 2031) | 9.28% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Gluten-Free Food and Beverages Market Analysis by Mordor Intelligence

The Asia-Pacific gluten-free food and beverages market is expected to grow from USD 1.56 billion in 2025 to USD 1.71 billion in 2026 and is forecast to reach USD 2.66 billion by 2031 at 9.28% CAGR over 2026-2031. This growth trajectory not only underscores the market's expanding footprint but also highlights its momentum, which currently eclipses that of the broader regional packaged-food sector. A surge in clinical diagnoses related to gluten disorders, paired with a growing consumer inclination towards preventive nutrition, has propelled once-niche medical diet products into the realm of everyday pantry staples. Structural assurances, bolstered by national labeling reforms such as Singapore’s 2025 Food (Amendment) Regulations and China’s stringent allergen declarations, have not only fueled premium pricing but also paved the way for multinational companies to introduce new products[1]Source: Singapore Statutes Online, "Food Regulations", sso.agc.gov.sg. The market's growth is further amplified by a wave of innovation, spearheaded by technology hubs in Japan and Korea. These hubs are adeptly translating their expertise in milling, extrusion, and fermentation into products that closely mimic traditional tastes and textures. However, challenges persist. Traditional steamed buns and noodles still struggle with taste-texture discrepancies, and certain regions in Southeast Asia face underdeveloped raw material supply chains, both of which hinder rural adoption rates.

Key Report Takeaways

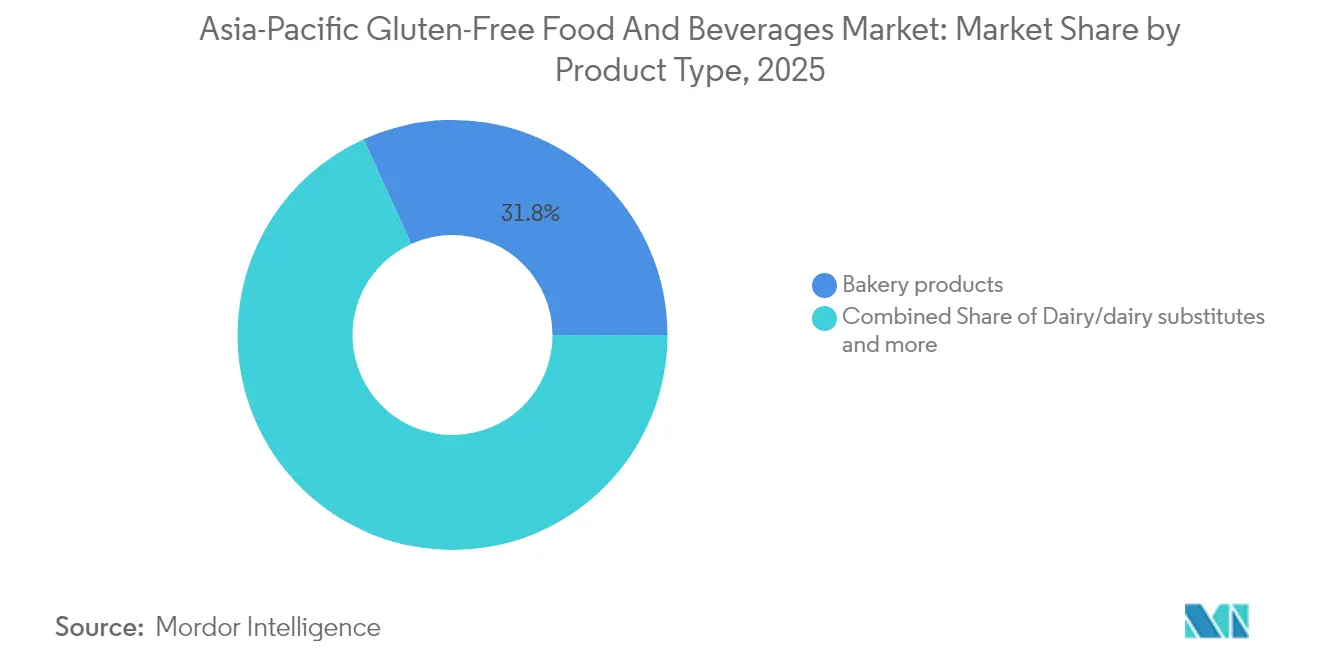

- By product type, bakery products led with 31.78% revenue share in 2025, while dairy and dairy substitutes are forecast to expand at a 10.52% CAGR through 2031.

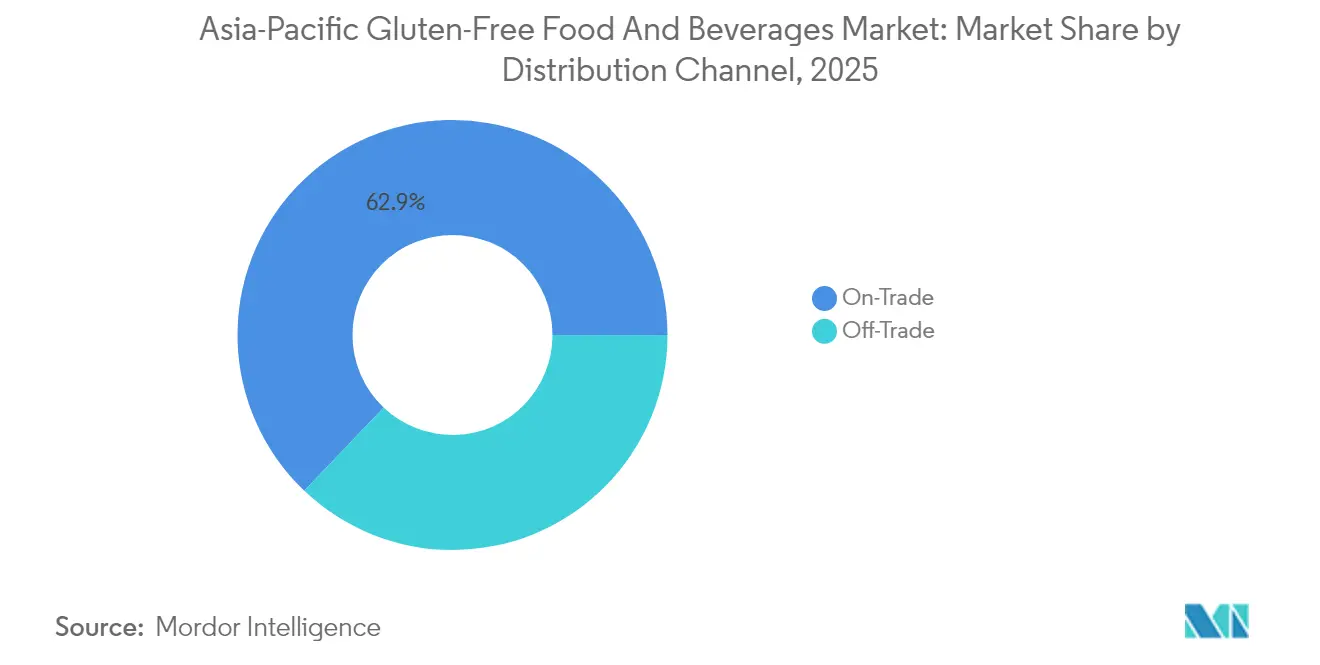

- By distribution channel, the off-trade accounted for a 37.10% share of the Asia-Pacific gluten-free food and beverages market size in 2025, whereas the on-trade is set to grow at a 11.25% CAGR through 2031.

- By geography, China dominated the Asia-Pacific gluten-free food and beverages market with a 31.90% share in 2025; however, India is projected to record the highest CAGR of 10.95% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Gluten-Free Food and Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in gluten-related disorder diagnoses | +2.1% | Global, with the highest impact in Australia, Japan, and South Korea | Medium term (2-4 years) |

| Increased health and wellness focus | +1.8% | China, India, and Singapore are leading; spillover to Southeast Asia | Long term (≥ 4 years) |

| Innovation in product development | +1.5% | Japan, South Korea, innovation hubs; China, manufacturing scale | Short term (≤ 2 years) |

| Government-backed awareness and initiatives | +1.2% | Singapore, Australia policy leadership, and China regulatory support | Medium term (2-4 years) |

| Positive social media and influencer marketing | +0.9% | China, India, Southeast Asia digital-first markets | Short term (≤ 2 years) |

| Fusion of traditional and modern cuisine | +0.7% | Japan, Korea, culinary innovation, regional adaptation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Gluten-Related Disorder Diagnoses

In developed Asia-Pacific markets, heightened clinical recognition of celiac disease and non-celiac gluten sensitivity is fueling a surge in demand. Australia stands at the forefront, with celiac disease, with Coeliac Australia Ltd reporting that while about 1 in 70 Australians is affected by celiac disease, a mere 20% have received a diagnosis[2]Source: Coeliac Australia Ltd, "Coeliac disease",.coeliac.org.au. Meanwhile, Japan and South Korea are ramping up awareness initiatives, led by healthcare professionals. The rise of specialized gastroenterology clinics in major urban hubs, focusing on gluten-related disorders, highlights a consumer base that prioritizes product efficacy over cost. This medical endorsement sets the Asia-Pacific market apart from its Western peers, where lifestyle choices often sway adoption. In Australia, the healthcare system's integration of gluten-free product subsidies for diagnosed patients lays a robust foundation for demand, resilient to economic fluctuations.

Increased Health and Wellness Focus

In China and India, urbanization is closely linked to evolving dietary preferences. Here, the rise in gluten-free consumption is more a reflection of health consciousness than a response to medical needs. As of 2024, China's middle class has expanded to 400 million households, as reported by the Ministry of Foreign Affairs of the People’s Republic of China[3]Source: Ministry of Foreign Affairs of the People’s Republic of China, "China's Economy Rebounds with Sound Momentum on The Hill Times", mfa.gov.cn. This burgeoning middle class wields significant purchasing power, turning its attention towards premium food categories, including gluten-free alternatives. Moreover, the melding of traditional Chinese medicine with contemporary nutritional science rebrands gluten-free foods. They're now seen as solutions for digestive wellness, rather than mere dietary restrictions. In Singapore, the government's commitment to promoting healthier food alternatives, including gluten-free options, is evident. The Singapore Food Agency's Healthier Ingredient Development Scheme has earmarked a substantial SGD 20 million for food innovation. This strategic positioning in the wellness arena not only justifies premium pricing but also propels market value growth, outpacing mere volume increases.

Innovation in Product Development

Japanese food technology leaders are spearheading regional innovations in gluten-free formulations, especially in matching the textures of wheat-based products. By harnessing advanced milling techniques like cryogenic grinding and air classification, companies are enhancing the functionality of rice flour for traditional dishes such as ramen and udon noodles. Furthermore, the creation of gluten-free instant noodle prototypes from cassava not only caters to dietary needs but also champions environmental sustainability, given cassava's reduced fertilizer demands compared to wheat. Meanwhile, Korean food producers are excelling in fermentation-driven gluten-free offerings, skillfully modifying traditional kimchi and gochujang methods to craft gluten-free seasonings and condiments. Such innovations bolster intellectual property advantages, enhancing the region's export competitiveness.

Government-Backed Awareness and Initiatives

Across ASEAN markets, regulatory harmonization has led to standardized gluten-free labeling requirements, streamlining compliance for regional manufacturers. Malaysia has set gluten-free claim standards, capping allowable gluten at under 20 parts per million, a move that aligns with global best practices and eases cross-border trade. In 2025, Singapore tightened its gluten-free labeling rules, mandating allergen declarations, a step that bolsters consumer trust and enhances market positioning. In Thailand, government nutrition programs are weaving gluten-free awareness into broader dietary guidance, elevating these products from niche medical uses to mainstream acceptance. The synchronized efforts across these markets not only create compliance economies of scale for established players but also heighten entry barriers for newcomers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Taste and texture challenges | -1.4% | Universal across regions, most acute in traditional cuisine markets | Medium term (2-4 years) |

| Competition from traditional and naturally gluten-free alternatives | -1.1% | China, India, and Southeast Asia with strong rice-based cuisines | Long term (≥ 4 years) |

| Immature supply chains for raw materials | -0.8% | Indonesia, Philippines, Thailand, emerging markets | Short term (≤ 2 years) |

| Limited product availability in rural areas | -0.6% | India, China, and Indonesia rural populations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Taste and Texture Challenges

In the Asia-Pacific region, formulation challenges in gluten-free products lead to consumer dissatisfaction, which in turn hinders repeat purchases. Bread alternatives made from rice flour often fall short of delivering the elasticity and mouthfeel that Asian consumers associate with high-quality baked goods, particularly in steamed buns and dinner rolls. Many gluten-free flours have a higher glycemic index, which raises concerns for health-conscious consumers regarding blood sugar management. This poses a challenge for adoption among diabetes-aware populations, a significant market segment in developed countries of the Asia-Pacific region. Smaller regional players struggle to compete with well-funded multinational corporations due to the substantial research and development investments required for advanced binding agents and texture modifiers. Furthermore, there's a lack of consumer education on realistic texture expectations, leading to trial disappointments and negative word-of-mouth, especially in price-sensitive segments.

Competition from Traditional and Naturally Gluten-Free Alternatives

In China, India, and Southeast Asia, rice-centric cuisines naturally provide gluten-free meal bases, thereby reducing the demand for specialized gluten-free products. In Vietnam and Thailand, traditional rice noodle production delivers authentic textures and flavors, a benchmark that manufactured gluten-free pasta alternatives, especially in price-sensitive markets, often fail to achieve. With an abundance of naturally gluten-free ingredients, such as rice, corn, and root vegetables, consumers often view specialized gluten-free products as premium add-ons rather than dietary necessities. Furthermore, regional culinary traditions prioritize fresh preparations over processed options, fostering skepticism towards packaged gluten-free products that prioritize convenience over authenticity. This competitive landscape constrains market growth, limiting it primarily to diagnosed celiac individuals, while broader health-conscious segments, which fuel volume growth in Western markets, remain largely untapped.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bakery Products Lead Despite Dairy Innovation

In 2025, bakery products command a dominant 31.78% market share, underscoring consumers' preference for bread and baked goods as their primary choices in the gluten-free category. Yet, it's the dairy and its substitutes that are poised for the most significant growth, projected at a robust 10.52% CAGR through 2031. This trend signals a shift in consumer behavior, moving from merely substituting wheat to seeking holistic dietary solutions. While the bakery segment enjoys the advantage of consumer familiarity with gluten-free bread alternatives, it faces rising competition from artisanal rice-based products, which are gaining traction due to traditional Asian baking methods. Meanwhile, meat and its substitutes hold a moderate market share, yet they're witnessing steady growth. This uptick is largely attributed to the convergence of plant-based protein trends with gluten-free positioning, especially among health-conscious urban dwellers in China and Singapore.

There's a burgeoning opportunity in sauces, dressings, and seasonings. Traditional Asian condiments are evolving with gluten-free formulations, and leading the charge are Korean firms, innovating with fermented gluten-free seasonings that preserve authentic flavors. While frozen desserts and beverages occupy a smaller slice of the market, they're on a consistent growth trajectory, buoyed by premium positioning and seasonal demand. Addressing both dietary needs and environmental sustainability, the development of gluten-free instant noodles using cassava-based formulations stands out. Cassava, requiring notably less fertilizer than traditional wheat, presents an eco-friendlier alternative. Other product categories, such as snacks and ready-to-eat meals, are finding their footing through e-commerce platforms, which facilitate niche product discovery and direct-to-consumer sales.

By Distribution Channel: Off-Trade Dominance Faces On-Trade Acceleration

In 2025, off-trade channels capture a 37.10% market share, leveraging established retail infrastructures and consumer shopping habits for packaged food products. Among off-trade segments, supermarkets and hypermarkets account for the largest distribution volumes. In contrast, specialty and health food stores carve out a niche, offering premium products with higher margins. Urban Asian markets are seeing convenience stores thrive, as frequent shopping trips fuel impulse buys of gluten-free snacks and beverages. Meanwhile, online retail stores are on a rapid ascent, especially in China and India. Here, robust e-commerce infrastructures breach rural markets, a feat that traditional retail struggles to achieve economically.

On-trade channels are projected to grow at an impressive 11.25% CAGR through 2031. This surge mirrors the foodservice industry's pivot towards health-conscious dining and accommodating dietary restrictions. As restaurants weave gluten-free options into their menus, they fuel a consistent demand for bulk ingredients and specialized preparation tools. This trend not only bolsters the B2B market but also extends beyond mere consumer retail. The "Find Me Gluten Free" mobile app is making waves in major Asia-Pacific cities, streamlining restaurant discovery. This bolsters demand-side infrastructure, nudging foodservice entities towards adoption and enticing consumers to try. Hotels and institutional foodservices are increasingly embracing gluten-free offerings, driven by the expectations of international guests and the mandates of corporate wellness programs. Such diversification in channels not only lessens the market's reliance on retail distribution but also paves the way for premium pricing strategies through higher-value commercial applications.

Geography Analysis

In 2025, China commanded a dominant 31.90% share of the regional revenue, solidifying its position as the foremost demand hub for gluten-free food and beverages in the Asia-Pacific. In March 2025, China's updated GB 7718-2024 allergen standards required clear labeling of gluten. This move has bolstered confidence among young urban consumers, who increasingly associate certified products with contemporary wellness. WeChat mini-apps now seamlessly integrate barcode scanning with instant ingredient translations, bridging the information divide for bilingual shoppers. However, competition from naturally gluten-free rice dishes has moderated the adoption of these products in rural areas. This has resulted in a bifurcated market, with coastal Tier-1 cities experiencing robust value growth, while hinterland provinces lag. Domestic processors are investing in specialized milling equipment to tap into export channels. Yet, they grapple with the challenge of legacy wheat-based supply chains, which complicates their segregation protocols.

India is set to lead the region with the fastest projected CAGR of 10.95% through 2031. positioning the India gluten free foods and beverages market as one of the fastest-growing in Asia-Pacific. This growth is fueled by rising urban disposable incomes and heightened awareness of autoimmune disorders. The Food Safety and Standards Authority of India has introduced front-of-pack allergen icons, streamlining consumer choices at retail outlets. Major local bakery chains are experimenting with millet-based bread loaves, aligning with government campaigns promoting indigenous grains. While distribution challenges persist beyond metropolitan areas, direct-to-consumer models tied to domestic e-commerce platforms are bridging the gap in Tier-2 cities. To truly capitalize on the Asia-Pacific gluten-free food and beverages market, players must adeptly navigate the preference for smaller pack sizes in rural areas, aligning with household budgets.

Japan and South Korea showcase mature consumption patterns, emphasizing ingredient sophistication and culinary authenticity. In Tokyo's ramen districts, cryogenic rice-flour ramen is achieving sensory parity with its wheat counterparts, commanding a 30% price premium. Drawing from Korea's rich fermentation heritage, the market is expanding into condiments, with gluten-free soy-bean paste (doenjang) becoming a favorite among flexitarians. In Australia, a robust demand is bolstered by healthcare reimbursement schemes that subsidize gluten-free bread for celiac patients. Meanwhile, ASEAN nations, Singapore, Malaysia, Thailand, Indonesia, and the Philippines, are reaping benefits from standardized labeling protocols, streamlining cross-border product movements. The Singaporean government is facilitating pilot-scale research and development and expediting commercialization processes, positioning the city as a strategic launchpad for the broader Asia-Pacific gluten-free food and beverages market.

Competitive Landscape

In the Asia-Pacific gluten-free food and beverage market, fragmentation prevails, with no single player capturing more than a modest double-digit share. While global giants like General Mills and Nestlé invest heavily in manufacturing and tap into worldwide ingredient networks, they often find themselves at odds with regional specialists who understand the nuances of local flavors. For instance, Japanese innovators have patented techniques that enhance the elasticity of rice-flour dough, while Korean companies focus on fermentation, adding depth to their clean-label products. Meanwhile, Australian bakeries, by sourcing domestic sorghum and buckwheat, cater to a clientele that is sustainability-conscious.

Technological advancements play a pivotal role, from binding agents to high-shear mixing and extrusion. Companies that pioneered enzyme-activated starch matrices have achieved superior bread crumb structures, earning them loyalty in upscale urban markets. Those investing in blockchain traceability, especially when exporting to provenance-sensitive markets like China, are reaping regulatory benefits and countering counterfeit concerns. Furthermore, by partnering with regional e-commerce giants, microbrands are sidestepping traditional shelf-space challenges, thereby amplifying direct-to-consumer competition.

Capital investments are on the rise: In January 2023, Arnott’s committed over USD 30 million to establish a gluten-free production hub, driven by surging B2B demand from foodservice operators. Concurrently, Japanese contract manufacturers are extending private-label services to foreign entrants, aiding them in navigating local compliance. Yet, merely scaling in volume won't suffice; the next growth phase in the Asia-Pacific gluten-free market will hinge on mastering flavor localization and ensuring dependable rural distribution.

Asia-Pacific Gluten-Free Food and Beverages Industry Leaders

-

Conagra Brands Inc.

-

General Mills Inc

-

Nestlé SA

-

Danone SA

-

Hain Celestial Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Central Food Technological Research Institute (CSIR-CFTRI), a public-sector research organization, launched three new gluten-free products for the Indian retail market under its Refrigerated Processed Foods of Extended Durability (REPFED) technology. These products aimed to make safe, healthy, and convenient food accessible to a wider audience, including those with dietary restrictions.

- December 2024: China's Healy Group, a fast-growing local player in the food industry, launched gluten-free dumpling wrappers. This product innovation catered to the rising demand for gluten-free versions of traditional Asian cuisine, converting classic dishes into specialized, allergen-friendly options for the mainstream market.

- July 2024: India's Wholsum Foods introduced a line of millet-based snacks. The company is known for its strategy of adapting traditional grains into modern, gluten-free formulations. This launch capitalized on the increasing consumer interest in traditional grains and healthier, millet-based snacking alternatives.

- April 2024: Australian biscuit giant Arnott's introduced gluten-free versions of two popular savory crackers, Jatz and Barbecue Shapes. The crackers were asserted to be made with a gluten-free flour blend and have been endorsed by Coeliac Australia and New Zealand, ensuring the same taste and quality as the original products.

Asia-Pacific Gluten-Free Food and Beverages Market Report Scope

Gluten is a group of proteins often found in foods like wheat, barley, rye, and other cereals. It is responsible for the soft, chewy texture characteristic of most gluten-containing cereal-based products. For the purpose of this study, the Asia-Pacific gluten-free food and beverages market is segmented by product type, distribution type, and country. The product type-based is segmented into bakery, meat/meat substitute, dairy/dairy substitute, sauces, dressings and seasonings, frozen desserts, beverages, and other product types. By distribution type, it is segmented into supermarkets/hypermarkets, specialty stores, convenience stores, online retail stores, and other distribution channels. By geography, the report is segmented into India, China, Japan, Australia, and Rest of Asia-pacific. The report offers market size and forecast in value terms in USD million for all the above segments.

By Product Type

| Bakery products |

| Meat/meat substitutes |

| Dairy/dairy substitutes |

| Sauces, dressings, and seasonings |

| Frozen desserts |

| Beverages |

| Other product types |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty/Health Food Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

By Geography

| China |

| Japan |

| India |

| Malaysia |

| Philippines |

| Thailand |

| Singapore |

| Indonesia |

| South Korea |

| Australia |

| Rest of Asia Pacific |

| By Product Type | Bakery products | |

| Meat/meat substitutes | ||

| Dairy/dairy substitutes | ||

| Sauces, dressings, and seasonings | ||

| Frozen desserts | ||

| Beverages | ||

| Other product types | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty/Health Food Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | China | |

| Japan | ||

| India | ||

| Malaysia | ||

| Philippines | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

Key Questions Answered in the Report

How big is the Asia-Pacific gluten-free food and beverages market in 2026?

It stands at USD 1.71 billion and is projected to reach USD 2.66 billion by 2031, growing at a 9.28% CAGR.

Which product category leads sales?

Bakery products hold the top position with 31.78% revenue share as of 2025.

Which distribution channel is expanding fastest?

On-trade foodservice is forecast to grow at a 11.25% CAGR through 2031 due to restaurant menu integration.

Which country offers the highest growth momentum?

India shows the steepest trajectory with an 10.95% CAGR expected between 2026 and 2031.

What is the main barrier to wider adoption?

Taste and texture limitations in gluten-free substitutes remain the largest consumer disappointment, restraining repeat purchases.

How are regulations shaping the market?

Unified ASEAN labeling and national allergen standards in China and Singapore are creating consistent regional compliance frameworks that favor certified products.

Page last updated on: