Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

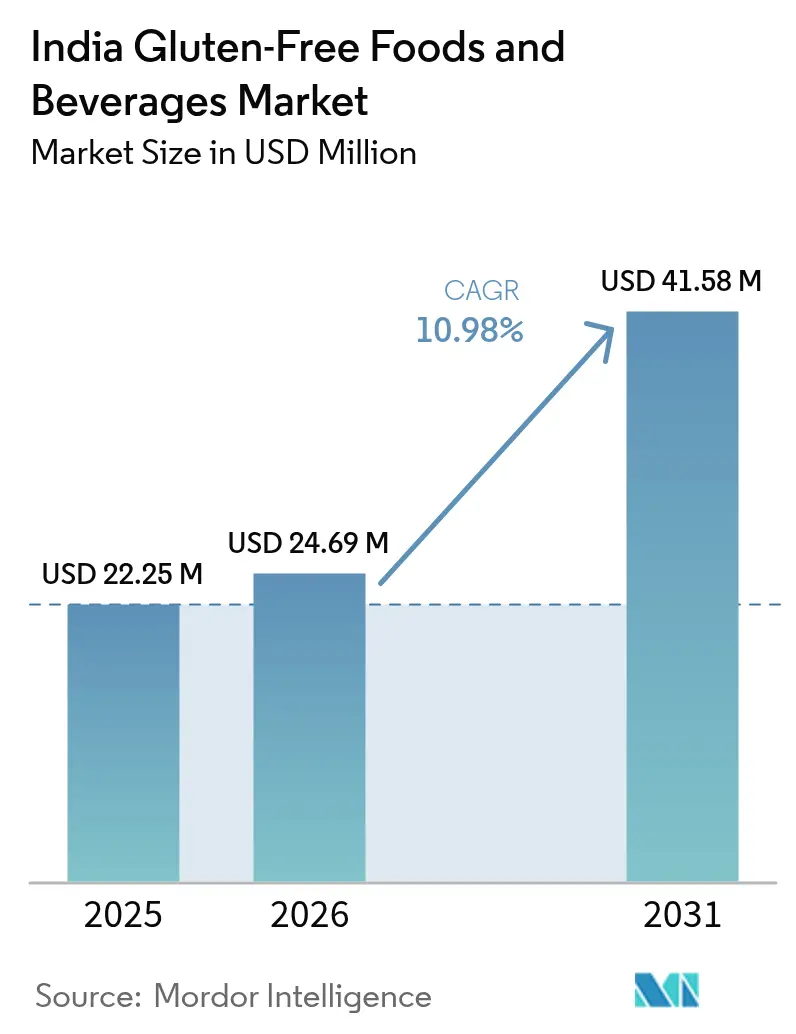

| Base Year Market Size (2025) | USD 22.25 Million |

| Market Size (2026) | USD 24.69 Million |

| Market Size (2031) | USD 41.58 Million |

| Growth Rate (2026 - 2031) | 10.98% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Gluten-Free Foods And Beverages Market Analysis by Mordor Intelligence

The India Gluten-Free Foods and Beverages market size in 2026 is estimated at USD 24.69 million, growing from 2025 value of USD 22.25 million with 2031 projections showing USD 41.58 million, growing at 10.98% CAGR over 2026-2031. Growing urban health consciousness, government incentives for millet processing, and digital-first distribution models are expanding the India Gluten-Free Foods and Beverages market well beyond its original niche. National schemes, such as the INR 800 crore Production-Linked Incentive for Millet-Based Products, are lowering entry barriers. Meanwhile, quick-commerce platforms deliver specialty SKUs within 20 minutes to more than 50 cities, sharply reducing trial friction. Parallel private-sector innovation, from multi-millet buns to probiotic pearl-millet desserts, signals a decisive shift from medical-necessity positioning to mainstream lifestyle adoption. The competitive arena now spans large FMCG incumbents and agile startups, creating a dynamic that drives both breadth of assortment and depth of penetration in the India Gluten-Free Foods and Beverages market.

Key Report Takeaways

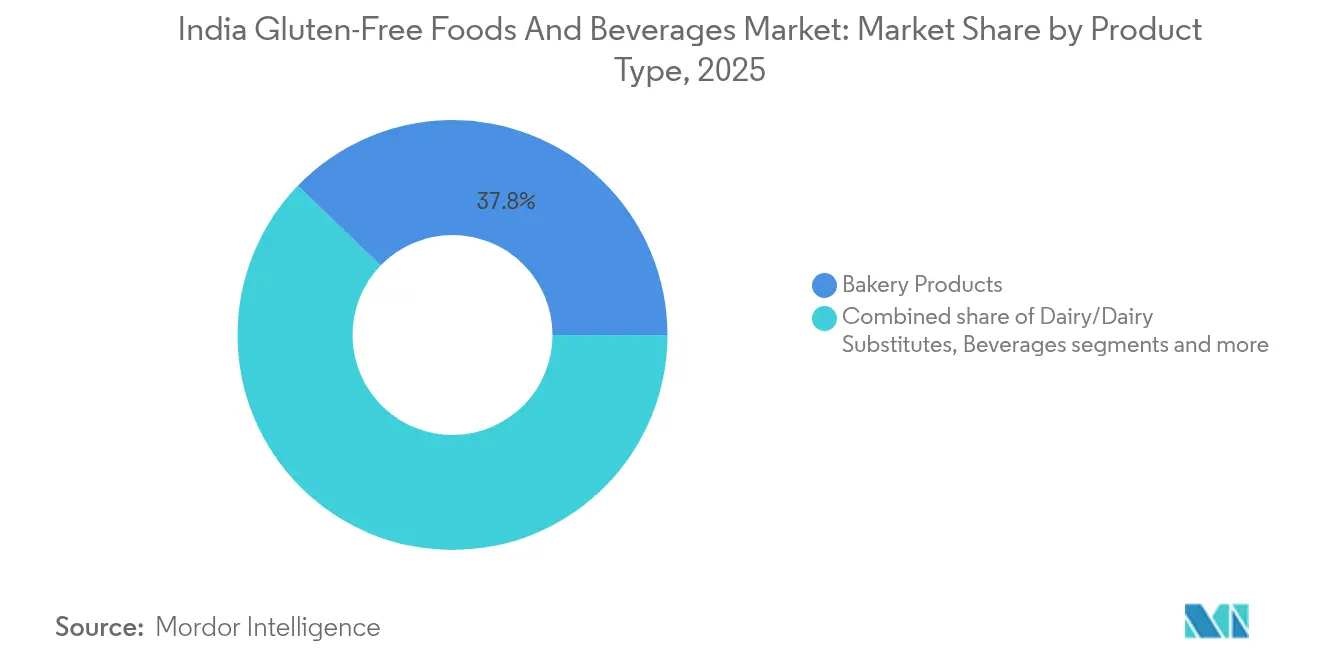

- By product type, bakery products captured 37.79% of the Indian gluten-free foods and beverages market share in 2025, while snacks and RTE products are forecast to expand at a 11.72% CAGR through 2031.

- By nature, conventional items held 82.65% share of the Indian gluten-free foods and beverages market size in 2025, whereas organic variants are advancing at a 12.31% CAGR during 2026-2031.

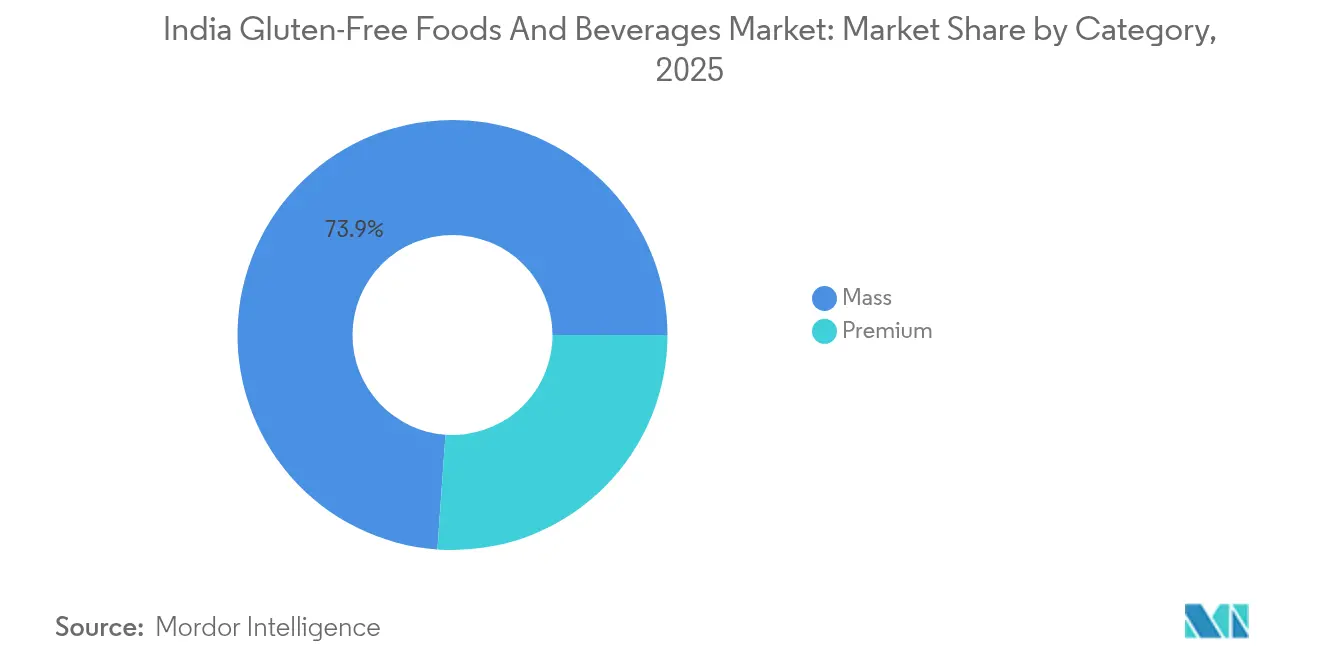

- By category, mass products accounted for 73.88% share of the Indian gluten-free foods and beverages market size in 2025; premium offerings are projected to grow at a 12.05% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets led with 45.72% share in 2025, while online retail stores are set to post a 11.9% CAGR to 2031.

- By geography, the West region commanded a 35.25% share in 2025, and the South is forecast to expand at an 11.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Gluten-Free Foods And Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Geographic Relevance |

|---|---|---|---|

| Rising prevalence of celiac disease and gluten intolerance boosts demand for specialized products | +2.0% | North India (Punjab, Haryana, Delhi-NCR), with spillover to urban metros nationwide | Medium term (2-4 years) |

| Product innovation and diversification, including local flavors and functional additions like probiotics, attracts broader adoption | +2.5% | National, with early gains in Bengaluru, Mumbai, Delhi-NCR | Short term (≤ 2 years) |

| Growth of "free-from" positioning in packaged food | +1.5% | Urban metros (Tier-1 cities), expanding to Tier-2 hubs | Medium term (2-4 years) |

| Influence of fitness influencers and wellness centers promotes dietary shifts | +1.8% | South India (Bengaluru, Chennai, Hyderabad), West India (Mumbai, Pune) | Short term (≤ 2 years) |

| Millet-based government initiatives | +2.3% | National, with concentrated impact in Karnataka, Rajasthan, Maharashtra | Long term (≥ 4 years) |

| Digital-first D2C brands widening reach | +1.5% | National, with accelerated penetration in Tier-2 and Tier-3 cities via ONDC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of celiac disease and gluten intolerance boosts demand for specialized products

The increasing prevalence of celiac disease and gluten intolerance is driving demand for specialized gluten-free products in India. North India reports a prevalence nearly 10 times higher than South India, creating a concentrated medical-necessity segment in wheat-consuming states such as Punjab and Haryana. Beyond diagnosed celiac cases, the Indian Council of Medical Research estimates a significant portion of the population experiences non-celiac gluten sensitivity (NCGS), characterized by gastrointestinal distress without autoimmune markers. This expands the market beyond clinical diagnoses, forming a dual-tier demand structure: therapeutic needs in the north and wellness-driven gluten avoidance in southern metropolitan areas, where it is viewed as a lifestyle choice. This differs from mature markets with a uniform 1% celiac prevalence, as per Celiac India and Beyond Foundation [1]Source: Celiac India and Beyond Foundation, "Prevalence", celiacindia.org.in. Latent demand is expected to grow as diagnostic infrastructure improves in tier-2 cities, supported by the Food Safety and Standards Authority of India's (FSSAI) mandatory allergen declaration rules. However, the absence of standardized gluten-free certification logos poses challenges for first-time buyers. A 2025 study in North West Rajasthan reported a 12% celiac prevalence among Type 1 diabetes patients, highlighting genetic clustering in northern wheat belts, while 2024 seroprevalence data revealed a 16.3% prevalence in nutritional anemia cases, underscoring underdiagnosis. Brands like Dr. Schär address northern therapeutic needs with certified gluten-free breads, while Nourish Organics targets NCGS consumers in the south with millet-based snacks. FSSAI's 2025 labeling initiatives aim to enhance ingredient transparency and ease consumer navigation.

Growth of “free-from” positioning in packaged food

The growth of "free-from" positioning in packaged foods is accelerating as the category, encompassing gluten-free, dairy-free, and preservative-free claims, expands at a faster pace than traditional snacks. This shift is driven by consumers seeking innovative, health-oriented options and paying closer attention to ingredient labels, aligning with the increasing demand for clean-label products. Single-serve packs from smaller brands are gaining popularity over multi-serve formats, as they reduce risk for price-sensitive shoppers exploring premium products. Data from the Household Consumption Expenditure Survey (HCES 2023–24) by MoSPI highlights food's significant share in monthly per-capita consumption expenditure, 48.4% in rural areas and 40.3% in urban areas, indicating robust demand for packaged foods [2]Source: Ministry of Statistics and Programme Implementation (MOSPI), "Household Consumption Expenditure Survey: 2023-24 Fact Sheet", mospi.gov.in. "Free-from" brands are capitalizing on this trend by reformulating existing SKUs to offer premium attributes without significant price increases, thereby capturing market share from competitors reliant on legacy recipes. Patanjali's Gluten Free Atta, priced at INR 110 per kilogram, exemplifies this approach by leveraging Ayurvedic heritage to position gluten avoidance as indigenous wisdom, resonating particularly in tier-2 cities with limited modern retail penetration. Similarly, Nestlé India's 2023 memorandum of understanding (MOU) with NUTRIHUB-IIMR for millet-based "free-from" innovations in products like CEREGROW and MAGGI demonstrates how multinational companies are evolving their portfolios to encourage trials among high-food-spend households, positioning "free-from" products as mainstream choices.

Influence of fitness influencers and wellness centers promotes dietary shifts

In metropolitan cities such as Mumbai, Delhi, Bengaluru, and Chennai, where gym penetration and fitness-conscious urban lifestyles are prominent, gluten avoidance is increasingly being positioned as a lifestyle choice rather than a medical requirement. This shift emphasizes benefits such as performance optimization, digestive comfort, and clean eating, resonating strongly with millennials and Gen Z. Influenced by social media-driven wellness narratives, these demographics view gluten-free diets as part of a broader focus on functional nutrition and holistic wellness. Reports indicate that gluten-free snacks in India, made from ingredients like millets, makhana, and rice, are gaining traction not only as alternatives for individuals with gluten sensitivity but also as everyday health-conscious options. The growing adoption of gluten-free products by fitness communities, wellness centers, and online health retailers is a key driver of this trend. Domestic brands such as True Elements and Nourish Organics, offering products like gluten-free oats, millet snacks, and energy bars, are increasingly featured in urban e-commerce platforms and fitness-oriented diet plans. This has contributed to making gluten-free consumption more accessible and mainstream, extending its appeal beyond niche dietary needs and aligning with the evolving preferences of health-conscious consumers in urban markets.

Millet-based government initiatives

Government initiatives centered on millet-based products are significantly influencing the growth of the gluten-free foods and beverages market in India. The INR 800 crore Production-Linked Incentive (PLI) Scheme for Millet-Based Products, operational from 2022 to 2027, has already disbursed INR 3.917 crore to 29 beneficiaries, as reported by the Ministry of Food Processing Industries (MoFPI) [3]Source: Ministry of Food Processing Industries (MoFPI), "Promotion of Millet Based Products", pib.gov.in . This scheme facilitates capacity expansion by reducing the risks associated with private investments in untested unit economics and complements policies integrating millets into the Public Distribution System (PDS), Integrated Child Development Services (ICDS), and Mid-Day Meal schemes, ensuring consistent demand and stabilizing millet processing infrastructure. ICRISAT-TCI's 2024 research highlights that replacing 1 kilogram of rice with millets in the PDS could save USD 1.37 billion annually, driving institutional procurement despite slower retail adoption. APEDA, through its Nutri Cereals Export Promotion Forum, has launched 16 strategic initiatives to tap into the global millet market, projected to reach USD 15.10 billion by 2030. These efforts create a cycle where export revenues support domestic development, while government procurement stabilizes prices and reduces raw material volatility, encouraging processors to expand gluten-free product portfolios. A December 2024 DD News report emphasized the scheme's user-friendly portal and weekly beneficiary meetings, which have enhanced local farmer procurement, with verified brands embedding naturally gluten-free millets into everyday consumption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher unit price versus conventional products | -1.2% | National, with acute impact in Tier-2 and Tier-3 cities | Short term (≤ 2 years) |

| Limited awareness in tier-2 and tier-3 cities hampers market penetration | -0.8% | Nationa, Tier-2 and Tier-3 cities across all regions | Medium term (2-4 years) |

| Lack of standardized regulations for gluten-free labeling creates consumer uncertainty | -0.6% | National (uniform across all states and union territories) | Medium term (2-4 years) |

| Supply volatility of specialty grains | -0.7% | National, with concentrated risk in Karnataka, Rajasthan, Maharashtra | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher unit price versus conventional products

The higher unit prices of gluten-free foods and beverages, driven by the use of specialized ingredients that are often imported or locally scarce, significantly impact market growth by escalating production costs. These costs are transferred to consumers, limiting affordability in India's price-sensitive market and restricting accessibility primarily to higher-income urban segments. This pricing dynamic discourages broader adoption and deters small and mid-sized manufacturers from entering the market due to cost pressures, thereby reducing product variety and competition. Although health awareness is increasing and gluten-free products are becoming more available through supermarkets and e-commerce platforms, high prices remain a key barrier to mainstream consumption. Many gluten-free products, such as snacks and bakery items, are priced noticeably higher than conventional alternatives. For example, brands like Bake&Co. (Agrimax Foods) and GobbleRight (a Mumbai-based startup) offer gluten-free millet-based cookies and vegan snacks at premium prices, catering to niche wellness-focused consumers. Recent reports from 2024 indicate that, despite government efforts to reduce costs, gluten-free products are still perceived as premium and nutritionally imbalanced compared to traditional foods, further limiting market penetration. Addressing this price sensitivity requires ongoing innovation in product formulation and supply chain efficiencies to enhance affordability and expand access for India's growing health-conscious consumer base.

Limited awareness in tier-2 and tier-3 cities hampers market penetration

The limited awareness in tier-2 and tier-3 cities poses a significant challenge to the penetration of the gluten-free market, as consumers in these regions are less exposed to wellness narratives and product education commonly provided by urban influencers and specialty retailers. This lack of awareness discourages product trials, with shoppers in smaller towns often favoring familiar staples and perceiving gluten-free options as niche or expensive rather than practical alternatives. As a result, distribution remains uneven, with brands and modern retail chains prioritizing metropolitan areas, leading to weaker point-of-sale visibility and limited sampling programs in smaller cities. Urban-focused retailers and direct-to-consumer (D2C) platforms offering gluten-free products, such as Urban Platter, find it easier to cater to metro markets than to smaller towns. Even brands selling naturally gluten-free staples like millets, such as 24 Mantra, face challenges in positioning their products, as consumers may recognize the ingredient but not its branding or convenient formats. Market commentary for 2024–25 highlights that while the gluten-free market is expanding and organized retail is beginning to extend beyond metros, this growth depends on consumer education. Without targeted on-ground marketing, clear labeling, and local influencer outreach, price sensitivity and habit-driven purchasing in tier-2 and tier-3 cities will continue to limit adoption. Addressing these challenges through local sampling initiatives, transparent labeling, and health-education partnerships will be critical for brands aiming to unlock the next phase of demand growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bakery Drives Volume, Snacks Capture Velocity

Bakery products are expected to hold a significant share of 37.79% in the gluten-free category mix in 2025. Consumers continue to favor familiar, ready-to-eat bakery formats, even as health and convenience trends evolve. This strong foundation allows manufacturers to introduce gluten-free variants that align with existing distribution channels and consumption occasions. The snacks and ready-to-eat (RTE) segment is projected to grow at a 11.72% CAGR through 2031, driven by the shift toward convenience formats. This growth bridges indulgent bakery products with millet- and legume-based snacks carrying gluten-free claims. Platforms like Urban Platter are already catering to urban consumers with millet pancake mixes, almond and quinoa flours, and other wheat-free bakery alternatives, showcasing the convergence of bakery and snacks innovation with gluten-free positioning. Additionally, the adoption of plant-based proteins in metropolitan areas expands formulation possibilities, enabling the development of gluten-free meat substitutes and fortified RTE products. However, the meats and meat substitutes category remains nascent due to India’s predominantly vegetarian population.

Sauces, dressings, and seasonings provide additional revenue opportunities by allowing brands to extend trusted gluten-free claims across various meal components. For instance, a consumer purchasing gluten-free pancake mix is likely to opt for a gluten-free labeled sauce if available. Beverages, however, remain a less explored category. Millet-based drinks and alternative gluten-free beer formats are just beginning to emerge in India, presenting opportunities for premium positioning and functional claims. Examples of brands leveraging these trends include 24 Mantra, which focuses on millets and packaged millet staples, and GoodDot, a plant-based startup showcasing how pea and chickpea proteins can be incorporated into mainstream, meat-alternative products. These brands are accessible through Indian retail and e-commerce channels, highlighting the diverse entry points for gluten-free innovation in the market.

By Nature: Conventional Dominates, Organic Premiumizes

Conventional gluten-free products hold a significant share of the Indian market, representing approximately 82.65% in 2025. Consumer price sensitivity continues to drive preference for lower-cost, familiar product formats, even as manufacturers introduce wheat-free alternatives that replicate conventional SKUs. This dynamic provides a broad base for gluten-free product adoption but presents challenges for premium organic lines, which must navigate entrenched value expectations. The market's scale and potential explain why established food companies and major retail channels prioritize conventional gluten-free bakery and snack products that align with existing distribution frameworks.

Organic gluten-free products, growing at a compound annual growth rate (CAGR) of 12.31% through 2031, are emerging as a premium segment, particularly among urban millennials willing to pay a premium for pesticide-free claims. This trend is reflected in product innovation and trade flows, such as the reported growth in Indian organic millet exports in 2024. Brands that effectively combine affordability with organic or naturally gluten-free offerings, such as millet and makhana snacks, are capturing health-conscious urban consumers while addressing cost-sensitive shoppers through scaled SKUs. Examples include Slurrp Farm’s millet-based cereals and pastas, Sattviko’s gluten-free makhana snacks, and Tata-owned Soulfull’s millet breakfast products, showcasing the use of millet and other naturally wheat-free ingredients across diverse price points and distribution channels in India.

By Category: Mass Anchors Volume, Premium Signals Aspiration

Mass products captured a 73.88% market share in 2025, driving significant volume through brands like Tata Soulfull. These brands derive substantial revenue from non-metro towns, where price sensitivity limits the adoption of premium products. By offering affordable staples aligned with mass-market consumption patterns, they ensure broad accessibility. This strong mass-market presence is expected to support the growth of premium variants, which are projected to achieve a CAGR of 12.05% through 2031. Urban consumers are increasingly drawn to artisanal products that transform gluten-free offerings from a necessity to a luxury, combining the scale of mass-market products with the margin potential of premium purchases. Tata Soulfull's 2024 Ragi Bites expansion into tier-2 towns via general trade exemplifies mass-market penetration, while the anticipated e-commerce growth in 2025 underscores the urban demand for premium products.

Premium variants, with their projected 12.05% CAGR, address the preferences of urban consumers who prioritize artisanal quality and clean-label attributes over affordability. These offerings complement the 73.88% mass-market base by targeting high-value segments willing to invest in superior formulations, such as specialty flours or flavored ready-to-eat (RTE) products. This segmentation strategy sustains overall market growth, with mass products driving penetration in price-sensitive non-metro areas and premium offerings fostering loyalty among health-conscious urban consumers. For instance, The Whole Truth's offering of gluten-free chocolate spreads, positioned for urban premium markets, reflects this trend, alongside Tata Soulfull's established presence in the mass segment.

By Distribution Channel: Supermarkets Anchor, Online Accelerates

Supermarkets and hypermarkets held a 45.72% share in 2025, leveraging the expansion of organized retail, which continues to gain traction in urban and peri-urban areas despite the broader market remaining largely unorganized. These outlets provide extensive assortments, ensuring easy access to gluten-free staples and packaged goods, supported by growing shelf space for health and wellness products. This channel caters to both mass-market and premium consumers, promoting awareness through in-store promotions and sampling. For example, Reliance Fresh expanded its gluten-free aisles in 2024, targeting metro cities and emerging urban centers.

Online retail is projected to grow at a CAGR of 11.9% through 2031, driven by quick-commerce platforms like Zepto, Blinkit, and Instamart, which enhance convenience by offering delivery within 10-20 minutes. This channel supports direct-to-consumer engagement and premium branding, enabling consumers to discover niche gluten-free options such as millet-based snacks from brands like Nourish Organics and True Elements, which have gained significant traction since 2024. Specialty stores and health-food chains serve as curated discovery points for premium buyers but face scalability challenges due to geographic constraints. Alternative channels, including subscription boxes and brand websites, facilitate new product launches and foster customer loyalty by reducing dependence on traditional retail outlets.

Geography Analysis

The West region held a 35.25% market share in 2025, driven by the presence of fitness-conscious millennials in cities like Mumbai and Pune. These consumers benefit from advanced retail infrastructure, enabling easy access to premium gluten-free products. Maharashtra, contributing nearly one-third of India's FMCG sales, provides economies of scale, allowing brands to adapt existing distribution networks for gluten-free SKUs with minimal additional costs. This dynamic supports market penetration and positions the region as a hub for innovation. For instance, Foods & Inns Ltd. introduced gluten-free bakery products in Mumbai hypermarkets to meet millennial demand. The West's retail maturity also complements the South's growth, offering a model for nationwide expansion.

The South region is projected to grow at a CAGR of 11.35% through 2031, driven by increasing health awareness in cities like Bengaluru and Chennai. These urban centers exhibit higher gym penetration, with fitness influencers encouraging dietary shifts toward gluten-free products. Karnataka's millet production, supported by government initiatives, provides a supply chain advantage, reducing logistics costs by 10-15% compared to pan-India sourcing, as reported by the Ministry of Agriculture. This cost efficiency enhances affordability and freshness, fostering product innovation. For example, Slurrp Farm launched millet-based gluten-free snacks for children in Bengaluru, leveraging local sourcing and influencer collaborations. The South's growth trajectory contrasts with the North's medically driven demand, diversifying the market's geographic drivers.

The North region, encompassing Punjab, Haryana, and Delhi-NCR, has the highest prevalence of celiac disease, creating a medical-necessity segment that prioritizes product efficacy over sensory appeal. This demand ensures steady adoption of certified gluten-free products despite the region's wheat-dominant diets. In contrast, the East and North-East regions face limited market penetration due to lower incomes and sparse retail infrastructure. However, indigenous grains like buckwheat in Sikkim and finger millet in Jharkhand present opportunities for localized product development. Research on green gram and rice-based cookies in Northeast India demonstrated strong consumer acceptance, while KRBL Ltd.'s 2024 trials of gluten-free basmati rice snacks in Delhi-NCR highlight the North's focus on efficacy, with potential for expansion into emerging markets in the East.

Competitive Landscape

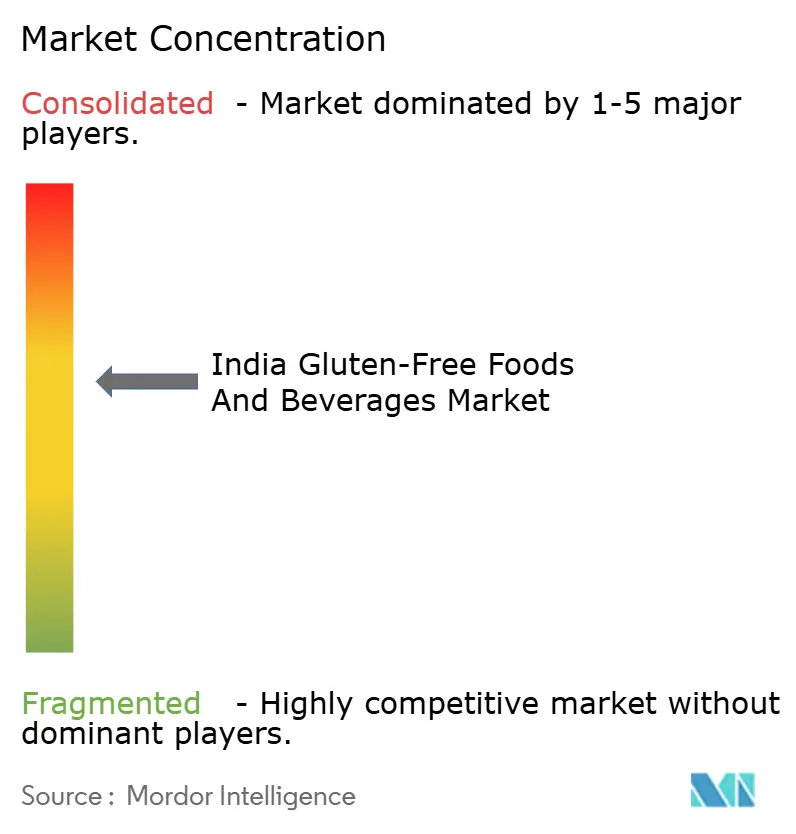

The competitive landscape of the gluten-free market in India reflects a balance between established FMCG players with significant scale and emerging, digitally native challengers, resulting in a moderately consolidated market. Prominent players, such as KRBL with its Tilda rice range, and multinational food companies emphasizing allergen labeling and extensive distribution networks, leverage their brand equity, established sales channels, and trade relationships to introduce gluten-free staples into mainstream retail and foodservice outlets. This strategy reduces barriers to entry for consumers across various distribution points. Consequently, national supermarket chains and general-trade distributors often prioritize listing gluten-free SKUs from these established brands, facilitating consumer access to familiar, branded alternatives to wheat-based staples.

Conversely, agile direct-to-consumer (D2C) brands and specialty retailers capitalize on market trends by swiftly launching niche SKUs and utilizing influencer marketing and e-commerce platforms to target urban health-conscious consumers. Recent developments highlight these players' expanding product assortments and leveraging celebrity endorsements to enhance visibility. For example, a notable brand collaboration announced in 2024 significantly increased the reach of a D2C gluten-free breakfast brand. These players excel in speed, targeted marketing, and leveraging direct consumer data, enabling them to test premium or functional gluten-free innovations and iterate rapidly without the burden of legacy costs. Additionally, these brands contribute to raising category awareness, which larger incumbents can later scale.

The result is a bifurcated yet complementary ecosystem. Established players (offering scale, distribution, and consumer trust) ensure widespread availability across India's retail infrastructure, while D2C and specialty brands (focused on innovation, digital reach, and niche positioning) drive category expansion and premiumization. Recent examples from 2024-25, such as KRBL/Tilda enhancing its gluten-free narrative in India and online platforms like Urban Platter broadening their gluten-free product ranges, illustrate how incumbents and digital retailers coexist and occasionally collaborate to grow the overall market rather than competing for a limited share. For brands and investors, the strategic approach is clear: utilize digital channels to validate concepts and build premium demand, then partner with larger players or retail networks to scale distribution across mass-market channels.

India Gluten-Free Foods And Beverages Industry Leaders

-

Dr. Schär AG

-

General Mills Inc.

-

ITC Limited

-

KRBL Limited

-

Amy’s Kitchen, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Dowbox introduced India's safest gluten-free subscription box, offering 100% certified gluten-free staples, snacks, flours, mixes, and spices. The curated monthly box featured lab-tested, certified gluten-free food products developed by individuals living with celiac disease to address their dietary needs. It included everyday flours such as Gluten-Free Roti Flour, Gluten-Free All-Purpose Flour, and Jowar, Ragi, Rajgira, Varai Bhagar, Yellow Moong Dal, and Upwas Bhajani Flours; easy mixes like Gluten-Free Split Green Moong Dosa Mix, Dhokla Mix, and Bajra Khichda Mix; and snacks and cookies, including Oreo-style Gluten-Free Chocolick White Cookies, Butter, Coconut, Elaichi, and Chocochip Cookies, as well as Gluten-Free Namkeens such as Masala Sev, Mathri, Papdi, and Namakpare.

- May 2025: Kameda LT Foods, a joint venture between LT Foods, an Indian-origin global FMCG company in the consumer food segment, and Kameda Seika, a prominent rice cracker and rice innovation company from Japan, expanded its roasted gluten-free snack portfolio under the brand Kari Kari with the introduction of a new product, 'Krispy Hopu,' featuring the 'Sweet and Salty' flavor.

- June 2024: Mumbai-based startup Gobbleright introduced a range of products designed for health-conscious consumers seeking nutritious and flavorful alternatives. The product line addressed various dietary preferences, including gluten-free and vegan options. Offerings such as savory chickpea wraps, wholesome pizza crusts, and protein-rich Crunchies were developed to provide a satisfying culinary experience while supporting digestive health.

India Gluten-Free Foods And Beverages Market Report Scope

A gluten-free food & beverage excludes foods containing gluten. Gluten is a protein in wheat, barley, rye, and triticale.

India's gluten-free foods and beverages market is segmented by product type, nature, category, distribution channel, and region. Based on product type, the market is segmented into bakery products, meats/meat substitutes, dairy/dairy substitutes, sauces, dressings, and seasonings, snacks and RTE products, beverages, and other product types. Based on nature, the market is segmented into conventional and organic. Based on category, the market is segmented into mass and premium. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. By region, the market is segmented into North, West, South, and East and North-East. Market Forecasts are in Value (USD).

By Product Type

| Bakery Products |

| Meats/Meat Substitutes |

| Dairy/Dairy Substitutes |

| Sauces, Dressings, and Seasonings |

| Snacks and RTE Products |

| Beverages |

| Other Product Types |

By Nature

| Conventional |

| Organic |

By Category

| Mass |

| Premium |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Region

| North |

| West |

| South |

| East and North-East |

| By Product Type | Bakery Products |

| Meats/Meat Substitutes | |

| Dairy/Dairy Substitutes | |

| Sauces, Dressings, and Seasonings | |

| Snacks and RTE Products | |

| Beverages | |

| Other Product Types | |

| By Nature | Conventional |

| Organic | |

| By Category | Mass |

| Premium | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Region | North |

| West | |

| South | |

| East and North-East |

Key Questions Answered in the Report

What is the current value of the India Gluten-Free Foods and Beverages market?

The India Gluten-Free Foods and Beverages market size stands at USD 24.69 million in 2026 and is forecast to reach USD 41.58 million by 2031.

Which product category is growing fastest in India’s gluten-free segment?

Snacks and ready-to-eat products are projected to register the fastest growth at a 11.72% CAGR through 2031.

Which distribution channel is set to gain share most rapidly?

Online Retail Stores, especially quick-commerce platforms, are expected to post a 11.9% CAGR to 2031.

Which Indian region leads gluten-free consumption today?

The West region, anchored by Maharashtra and Gujarat, held 35.25% market share in 2025.

Page last updated on: