Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 22.55 Billion |

| Market Size (2031) | USD 30.08 Billion |

| Growth Rate (2026 - 2031) | 5.93% CAGR |

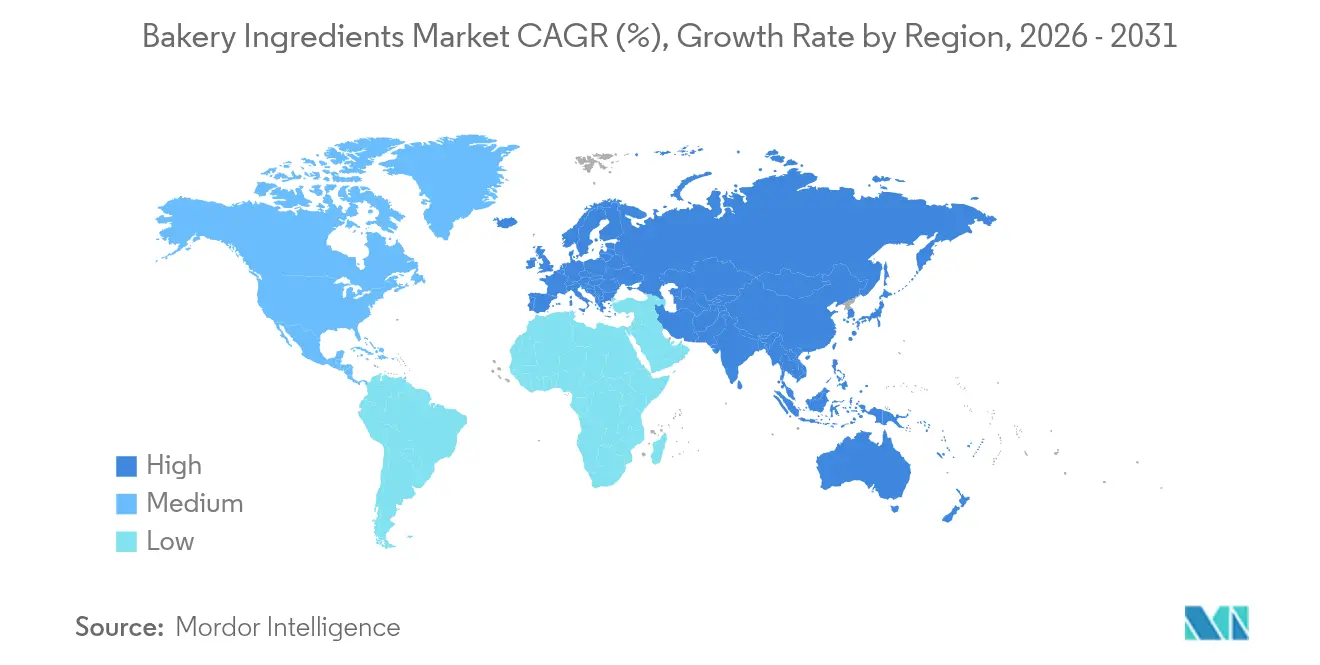

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

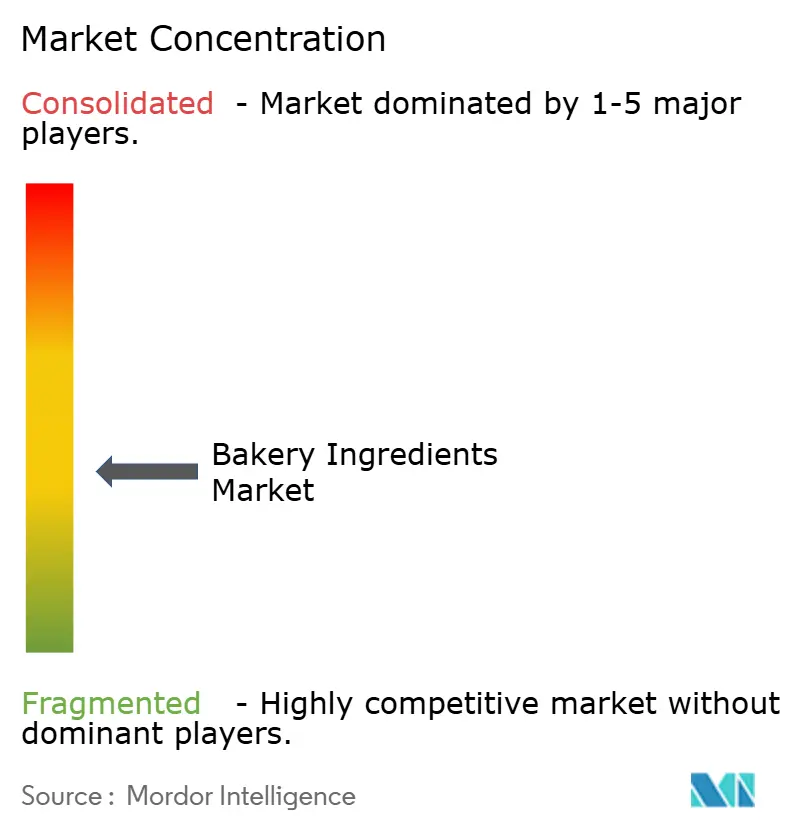

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bakery Ingredients Market Analysis by Mordor Intelligence

The bakery ingredients market is expected to grow from USD 21.29 billion in 2025 to USD 22.55 billion in 2026 and is forecast to reach USD 30.08 billion by 2031 at 5.93% CAGR over 2026-2031. The market growth is primarily attributed to increasing consumer health consciousness, which has resulted in heightened demand for bakery products incorporating natural, clean-label ingredients, whole grains, and low-sugar alternatives. The escalating preference for convenience and ready-to-eat foods in urban regions has substantially increased the consumption of packaged bakery goods. Significant product innovation in the market, particularly in gluten-free, vegan, and functional bakery items, continues to address diverse dietary requirements. The market demonstrates a notable shift toward premium bakery products, characterized by high-quality and artisanal offerings, thereby intensifying the demand for specialized ingredients. Furthermore, the expansion of distribution networks through foodservice, retail, and e-commerce platforms has enhanced market accessibility, positioning the global bakery ingredients market for sustained growth in the forecast period.

Key Report Takeaways

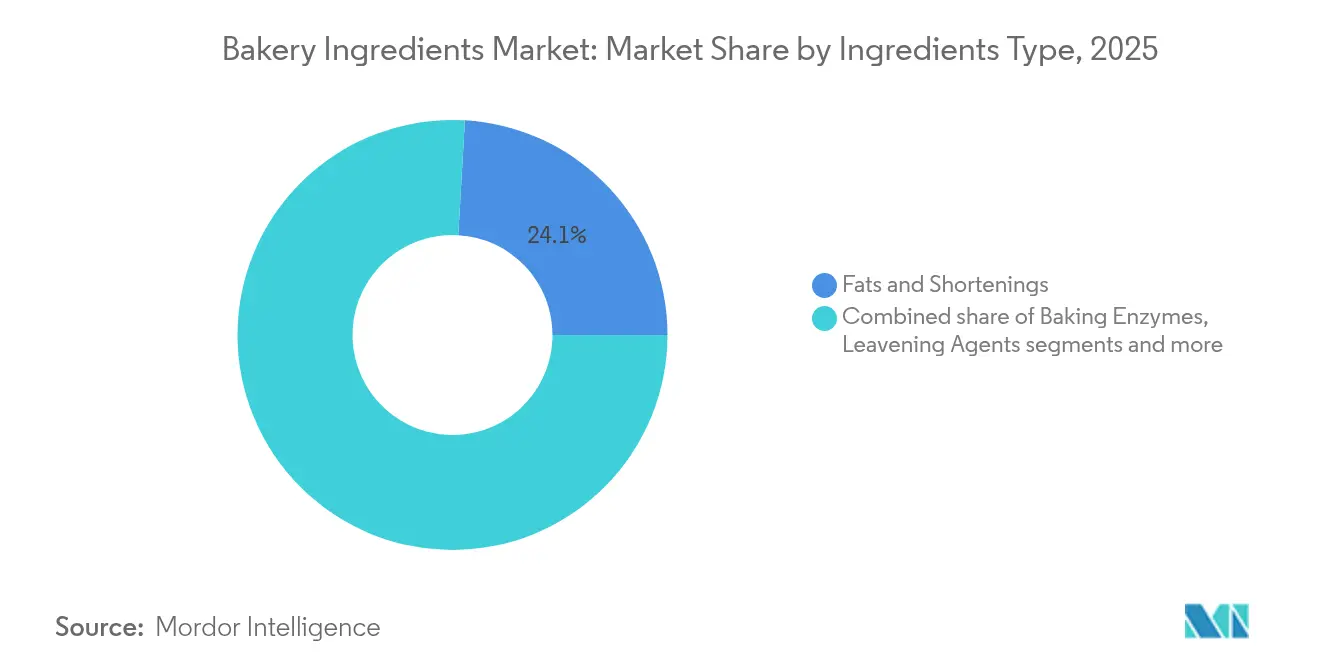

- By ingredients type, fats and shortenings led with 24.08% of bakery ingredients market share in 2025, while baking enzymes are projected to expand at an 8.02% CAGR through 2031.

- By application, bread captured 45.92% share of the bakery ingredients market size in 2025, whereas cakes and pastries recorded the fastest 6.86% CAGR to 2031.

- By form, dry formats accounted for 63.05% revenue share in 2025, while liquid formats are growing at a 7.18% CAGR.

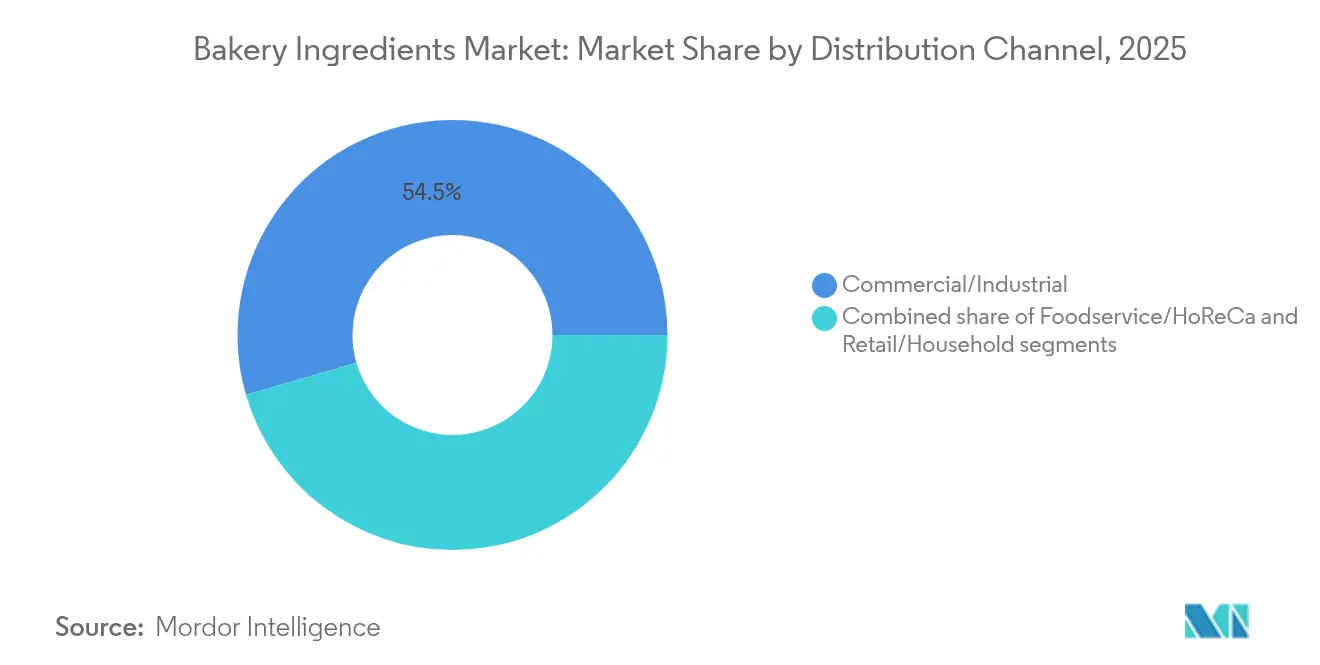

- By distribution channel, commercial/industrial bakeries captured a 54.48% share in 2025, while foodservice/HoReCa logged the highest 6.72% CAGR.

- By geography, Europe dominated with a 33.95% share in 2025; Asia-Pacific is the fastest-growing region at 7.41% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bakery Ingredients Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for clean-label and natural ingredients | +1.2% | Global, with strongest adoption in North America and Europe | Medium term (2-4 years) |

| Rising demand for premium artisanal and specialty bread | +0.8% | Europe and North America core, expanding to Asia-Pacific urban centers | Long term (≥ 4 years) |

| Increased adoption of functional and fortified bakery ingredients | +0.9% | Global, with early gains in developed markets | Medium term (2-4 years) |

| Growing consumer preference for vegan bakery products drives alternative emulsifier usage | +0.6% | North America and Europe, with emerging adoption in Asia-Pacific | Short term (≤ 2 years) |

| Growing urbanization and changing lifestyles | +1.1% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Long term (≥ 4 years) |

| Rising demand for gluten-free products | +0.7% | North America and Europe primary, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Preference for Clean-Label and Natural Ingredients

The global bakery ingredients market is undergoing substantial transformation, attributed to increasing consumer preference for clean-label and natural ingredients. This fundamental shift influences product development strategies, branding initiatives, and supply chain operations throughout the industry. The transformation is primarily driven by elevated health consciousness, enhanced awareness of food sourcing practices, and increased concerns regarding synthetic additives and allergens. Contemporary consumers conduct thorough examinations of ingredient lists and require comprehensive transparency in their food purchases. According to the International Food Information Council (IFIC), in 2023, approximately 40% of consumers in the United States regularly purchased food and beverages labeled as natural, while 29% preferred products labeled with clean ingredients [1]Source: International Food Information Council (IFIC), "2023 Food and Health Survey", foodinsight.org. In response to these market dynamics, bakery manufacturers are implementing product reformulations by eliminating artificial colors, preservatives, and high-fructose corn syrup, while incorporating plant-based or minimally processed alternatives such as natural emulsifiers, enzymes, and whole grain flours.

Rising Demand for Premium Artisanal and Specialty Bread

The specialty bread segment is experiencing significant growth, driven by consumer demand for authentic, craft-baked products with distinct flavors and health benefits. Health consciousness among consumers has increased the demand for nutritious bread options, particularly those offering specific benefits such as low-carbohydrate content, high fiber, or gluten-free formulations. The market expansion is further supported by growing interest in global cuisines and ethnic foods, which has increased demand for specialty breads from various cultures. Consumers seeking authentic culinary experiences and diverse flavors are increasingly choosing breads that represent different cultural traditions and characteristics. The growth of premium artisanal and specialty bread production is supported by increased wheat production. According to the USDA Foreign Agricultural Service, global wheat production stood at 799.91 million metric tons in 2024/2025, up from 791.95 million metric tons in 2023/2024 [2]Source: United States Department of Agriculture (USDA), "World Agricultural Production", usda.gov. This increased wheat availability enables bakers to meet the rising demand for specialty breads. Additionally, the emphasis on quality in artisanal and specialty breads has encouraged farmers to cultivate premium wheat varieties.

Increased Adoption of Functional and Fortified Bakery Ingredients

The incorporation of functional ingredients into bakery products represents a significant market driver, aligning with consumer preferences for both health benefits and indulgence. The increasing prevalence of food allergies and intolerances, particularly gluten sensitivity and dairy intolerance, drives substantial growth in the bakery ingredients market. Manufacturers are strategically responding to this demand by offering gluten-free and dairy-free products that utilize specialized ingredients, including alternative flours, plant-based milks, stabilizers, and emulsifiers. These ingredients enable the production of appealing bakery products that accommodate specific dietary requirements while maintaining product quality. This market evolution is evidenced by Revyve, a food technology company, which opened a facility in the Netherlands in September 2024 to manufacture its gluten-free ingredients derived from baker's yeast. The continuous development of functional and fortified bakery ingredients indicates a sustained market trajectory driven by consumer health consciousness and dietary requirements.

Growing Consumer Preference for Vegan Bakery Products Drives Alternative Emulsifier Usage

The increasing consumer preference for vegan bakery products significantly influences the demand for plant-based emulsifiers in the global bakery ingredients market. This transformation is driven by heightened health consciousness among consumers seeking nutritional benefits, growing environmental sustainability concerns regarding food production, and increased awareness of animal welfare considerations. The market demonstrates a substantial shift toward bakery ingredients that exclude animal-derived components while adhering to clean-label and non-GMO requirements. This trend is evidenced by InnovoPro's February 2024 introduction of clean-label emulsification solutions for bakery applications, utilizing chickpea protein technology. The company's innovation represents a strategic response to evolving consumer preferences, providing natural alternatives to conventional synthetic and chemically derived emulsifiers. This development underscores the industry's commitment to sustainable, plant-based solutions and indicates a continued trajectory toward alternative emulsifier adoption in bakery applications.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety and labeling regulations | -0.8% | Global, with strictest enforcement in North America and Europe | Short term (≤ 2 years) |

| Consumer concerns regarding artificial additives | -0.5% | Developed markets primarily, spreading to emerging economies | Medium term (2-4 years) |

| Short shelf life of natural ingredients | -0.6% | Global, with acute impact in hot climates and long supply chains | Short term (≤ 2 years) |

| Fluctuating raw material prices hamper market growth | -0.9% | Global, with highest volatility in commodity-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Food Safety and Labeling Regulations

Food safety and labeling regulations significantly constrain the global bakery ingredients market by affecting innovation, ingredient sourcing, and product formulation. Government authorities worldwide have implemented stricter controls on food additives, labeling requirements, and traceability standards, limiting the use of synthetic, functional, and novel ingredients in bakery products. Regional variations in these regulations create operational challenges for global manufacturers, who must ensure compliance while managing costs related to reformulation, label modifications, and market-specific production. The European Food Safety Authority (EFSA) has conducted rigorous re-evaluations of additives, resulting in restrictions such as the ban on titanium dioxide (E171) in food products, including baked goods. In 2023, California enacted legislation prohibiting four chemicals: brominated vegetable oil, potassium bromate, propylparaben, and Red No. 3 dye in food products sold within the state, with enforcement beginning January 1, 2027. These regulatory constraints continue to shape the industry landscape, requiring manufacturers to adapt their formulations and processes while potentially limiting market growth opportunities.

Consumer Concerns Regarding Artificial Additives

The intensifying consumer scrutiny of artificial additives emerges as a critical restraint impeding the growth trajectory of the bakery ingredients market. According to Proveg International, in 2023, 62% of consumers demonstrated heightened vigilance toward ingredient lists, signifying a profound transformation in purchasing patterns. This evolving consumer behavior has necessitated bakery manufacturers to implement extensive product reformulations, mandating the incorporation of natural alternatives to replace synthetic preservatives, colors, and flavors. The inherent technical complexities in sustaining product quality and shelf stability without conventional additives pose substantial operational challenges for manufacturers. While ingredient suppliers continue to advance clean-label solutions, the Food and Drug Administration (FDA)'s rigorous review of color additives in food products, encompassing comprehensive safety assessments of synthetic colors, introduces additional regulatory constraints. These combined factors significantly restrict market expansion and catalyze an accelerated industry-wide transition toward natural alternatives in bakery products, fundamentally reshaping the market landscape.

Segment Analysis

By Ingredients Type: Enzymes Drive Clean-Label Innovation

Fats and shortenings currently hold the largest market share at 24.08% in 2025, owing to their multifunctional role in texture development, mouthfeel enhancement, and shelf-life extension across bakery applications. The segment's dominance persists due to the technical challenges in replacing these ingredients, despite increasing consumer health concerns. Baking enzymes represent the fastest-growing segment with a projected CAGR of 8.02% (2026-2031). This growth stems from their ability to meet clean-label requirements while improving dough handling and product quality. Microbial enzymes, including amylases, proteases, and lipases, play an essential role in enhancing the quality, flavor, and texture of bakery products.

The leavening agents segment demonstrates consistent growth, supported by advancements in encapsulation technology that enhance stability and controlled release during baking. Emulsifiers continue to evolve as plant-based alternatives gain market presence, while colors and flavors shift toward natural sources to align with clean-label requirements. The preservatives segment undergoes significant transformation as manufacturers develop fermentation-derived alternatives to replace synthetic options. The Food and Drug Administration (FDA)'s recent guidance on food additives permitted for direct addition to food for human consumption establishes an updated regulatory framework for these ingredients, shaping innovation in the bakery sector.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Bread Maintains Dominance Amid Diversification

The bread segment commands 45.92% of the global bakery ingredients market share in 2025, maintaining its position as a fundamental dietary component across regions. This dominance results from its affordability, nutritional value, and continuous product innovation in artisanal and functional varieties. Manufacturers are incorporating specialized ingredients to develop bread products with enhanced nutritional profiles and distinct flavor characteristics to retain their market position. The integration of alternative flours, functional additives, and bioactive compounds reflects the industry's response to increasing consumer demand for healthier options.

The cakes and pastries segment exhibits the highest growth rate at 6.86% CAGR (2026-2031), driven by premium ingredient offerings, functional components, and increased snack consumption patterns. The segment's growth benefits from the extensive availability of freezer storage in retail establishments for frozen processed foods. Other segments demonstrate specific growth trajectories, with cookies and biscuits expanding through portion-controlled formulations and healthier ingredient alternatives, rolls and pies advancing through artisanal production methods and premium ingredient selection, and donuts and muffins developing through innovative ingredient combinations and hybrid product formulations.

By Distribution Channel: HoReCa Segment Accelerates Post-Pandemic

The commercial/industrial channel accounts for 54.48% of the global bakery ingredients market in 2025. This dominance is attributed to the extensive production requirements, sophisticated manufacturing processes, and complex ingredient specifications in large-scale bakery operations. Industrial bakeries maintain strategic supplier partnerships and implement customized formulation systems to ensure consistent product quality across their high-volume production lines. The commercial segment's market position is further strengthened by industry consolidation trends, where larger bakeries optimize operational efficiency through streamlined ingredient procurement, advanced processing technologies, and integrated supply chain management systems.

The foodservice/HoReCa segment is projected to grow at a CAGR of 6.72% from 2026 to 2031. This growth is driven by increasing demand for convenience foods, expansion of quick-service restaurants, and growing consumer preference for artisanal and specialty baked goods in the hospitality sector. The retail/household segment demonstrates consistent growth, driven by continued home baking activities and increasing consumer preference for premium, health-oriented, and clean-label ingredients. This trend is reflected in the United States retail and food services sales, which reached USD 715.4 billion in May 2025, according to the United States Census Bureau . The total sales for March through May 2025 increased by 4.5%, indicating sustained consumer participation in both home and out-of-home bakery consumption.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Liquid Segments Gain Processing Advantages

In the global bakery ingredients market, dry ingredients maintain market leadership, accounting for 63.05% of the total market value in 2025. This market dominance is attributed to fundamental operational advantages: prolonged shelf stability, optimized storage and transportation logistics, superior cost efficiency, and compatibility with industrial production infrastructure. Dry ingredients demonstrate enhanced stability characteristics, minimal perishability factors, and robust temperature tolerance, positioning them as optimal components for large-scale industrial bakery operations and medium-scale commercial facilities. The established global supply chain network for dry ingredient procurement, distribution, and storage further reinforces their market position across international markets, particularly in regions with diverse logistics capabilities.

The liquid bakery ingredients segment demonstrates significant market momentum, projecting a compound annual growth rate (CAGR) of 7.18% through 2031. This segment's expansion is driven by enhanced operational safety through reduced particulate exposure and superior dosing accuracy in industrial-scale manufacturing operations. Advanced processing technologies increasingly favor liquid formulations, specifically in enzyme and emulsifier applications where homogeneous distribution is crucial for product standardization. Liquid enzyme formulations demonstrate superior stability, retention, and enhanced activation parameters compared to dry alternatives, supporting the segment's market expansion trajectory.

Geography Analysis

Europe dominates the global bakery ingredients market with a 33.95% share in 2025, underpinned by established bakery manufacturing capabilities and advanced ingredient formulation technologies. Germany stands as the region's primary market, with its food processing industry generating USD 247 billion turnover in 2023, according to the United States Department of Agriculture (USDA). The region's market leadership is attributed to its established commercial and artisanal bakery operations, premium ingredient specifications, and comprehensive regulatory frameworks that promote innovation while maintaining stringent food safety standards. European bakery manufacturers demonstrate consistent demand for premium-grade ingredients, particularly in organic and sustainable ingredient categories.

The Asia-Pacific bakery ingredients market projects the highest growth rate at 7.41% CAGR (2026-2031), driven by industrial bakery expansion, increasing consumer purchasing power, and widespread adoption of Western bakery products. China and India's substantial manufacturing base and population demographics accelerate market development. The region's industrial bakery sector demonstrates increasing demand for specialized ingredients, prompting manufacturers to enhance production capabilities and implement advanced processing technologies. This market evolution creates significant opportunities for bakery ingredient manufacturers across key categories, including emulsifiers, enzymes, baking powders, oils, and fats.

Moreover, North America maintains a significant market share through continuous innovation in health-oriented bakery ingredients and clean-label formulations. The Middle East and Africa present expanding opportunities, particularly in industrial bakery operations within urban centers. Latin America's bakery ingredients market advances through industrial modernization and urbanization, despite economic factors affecting premium ingredient procurement.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The bakery ingredients market shows moderate fragmentation, with global players maintaining strong positions through vertical integration and geographic expansion. The market concentration varied across ingredient categories. The enzyme and specialty additive segments showed higher consolidation due to technical barriers and research and development requirements. In contrast, commodity ingredients, such as flours and basic sweeteners, maintained a fragmented market structure. Key companies, including Cargill Incorporated, Archer Daniels Midland Company, Associated British Foods plc, and Kerry Group plc, utilize their scale advantages in procurement and distribution networks while investing in innovation to differentiate products.

The competitive dynamics in the global market are shaped by strategic initiatives focused on developing clean-label solutions, functional ingredients, and implementing sustainable sourcing practices in response to evolving international consumer preferences and regulatory frameworks. The strategic acquisition of CP Kelco by Tate & Lyle for USD 1.8 billion in November 2024 exemplifies the ongoing market trends aimed at strengthening specialty food and beverage capabilities across global markets.

Market competitiveness is further intensified by technological advancement, with major companies investing significantly in advanced fermentation capabilities, enzyme engineering, and digital platforms to develop next-generation ingredients for international markets. While emerging opportunities exist in global plant-based alternatives, functional fortification, and sustainable packaging solutions, specialized suppliers maintain market presence in niche segments through advanced technical expertise and strong international customer relationships.

Bakery Ingredients Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Associated British Foods plc

-

Kerry Group plc

-

DSM-Firmenich AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: ACI Group has launched bakery ingredients that improved operational efficiency and minimized waste in bakery production. The product line comprised TIP-TOP Low-Dust Dusting Flour, DUBOR Release Agents, and GECKO Ultra Seed Adhesive.

- April 2025: AWL Agri Business Limited, a major food company in India, entered the bakery ingredient market through the launch of Fortune Cake Premix. The product served the HoReCa and B2B segments by providing professional bakers and commercial kitchens with standardized solutions for high-volume cake production.

- June 2024: Angel Yeast established a partnership with BakeMark to introduce multiple product lines under the name BakeMark By Angel at Bakery China 2024. The partnership aimed to deliver bakery ingredients and services that supported healthier food options for consumers.

- March 2024: Kerry Group introduced Biobake Fresh Rich, an enzyme system for sweet baked products that maintained softness, freshness, and moisture throughout their shelf life while reducing food waste. The starch-acting enzyme helped sweet goods with sugar content above 20% maintain freshness for longer periods.

Global Bakery Ingredients Market Report Scope

Bakery ingredients such as enzymes, emulsifiers, baking powders, and yeast are commonly used in the production of bakery products, including bread, cakes, pastries, tarts, pies, and others. These ingredients help maintain freshness and softness and improve the shelf life of products.

The Bakery Ingredients Market is segmented by ingredient type, application, form, distribution channel, and geography. By ingredients type, the market is segmented into baking enzymes, leavening agents, emulsifiers, fats & shortenings, sweeteners, colors & flavors, preservatives, and others. By application, the market is segmented into bread, cakes & pastries, cookies & biscuits, rolls & pies, donuts & muffins, and others. By form, the market is segmented into dry and liquid. By distribution channel, the market is segmented into commercial/industrial, retail/household, and foodservice/ horeca. The geographical segmentation of the market is also included, with a detailed analysis of North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Ingredients Type

| Baking Enzymes |

| Leavening Agents |

| Emulsifiers |

| Fats and Shortenings |

| Sweeteners |

| Colors and Flavors |

| Preservatives |

| Others |

By Application

| Bread |

| Cakes and Pastries |

| Cookies and Biscuits |

| Rolls and Pies |

| Donuts and Muffins |

| Others |

By Form

| Dry |

| Liquid |

By Distribution Channel

| Commercial/Industrial |

| Retail/Household |

| Foodservice/HoReCa |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Ingredients Type | Baking Enzymes | |

| Leavening Agents | ||

| Emulsifiers | ||

| Fats and Shortenings | ||

| Sweeteners | ||

| Colors and Flavors | ||

| Preservatives | ||

| Others | ||

| By Application | Bread | |

| Cakes and Pastries | ||

| Cookies and Biscuits | ||

| Rolls and Pies | ||

| Donuts and Muffins | ||

| Others | ||

| By Form | Dry | |

| Liquid | ||

| By Distribution Channel | Commercial/Industrial | |

| Retail/Household | ||

| Foodservice/HoReCa | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the bakery ingredients market?

The bakery ingredients market stands at USD 22.55 billion in 2026 and is projected to reach USD 30.08 billion by 2031.

Which region leads the bakery ingredients market?

Europe leads with a 33.95% revenue share in 2025 due to strong artisanal traditions and high per-capita bread consumption.

Which ingredient segment is growing fastest?

Baking enzymes show the strongest momentum, advancing at an 8.02% CAGR on the back of clean-label and functional performance demands.

Why are liquid ingredients gaining popularity?

Liquid formats improve dosing precision, shorten mix times, and disperse uniformly in automated plants, giving them a 7.18% CAGR through 2031.