Bread Mixes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 20.92 Billion |

| Market Size (2031) | USD 27.24 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bread Mixes Market Analysis by Mordor Intelligence

Bread mixes market size in 2026 is estimated at USD 20.92 billion, growing from 2025 value of USD 19.85 billion with 2031 projections showing USD 27.24 billion, growing at 5.41% CAGR over 2026-2031. This growth is largely driven by consumers' heightened emphasis on health, clean-label ingredients, and convenient meal solutions. In response, product developers are rolling out gluten-free, organic, and protein-enriched variants. These not only mimic artisanal textures but also reduce preparation times. With clearer regulations on gluten-free labeling and organic certifications, there's a surge in investments towards specialized production lines. Meanwhile, social media's influence has bolstered the home-baking trend, expanding the market's consumer base. Digitalization in supply chains, coupled with cutting-edge mixing technologies, has enhanced consistency. This advancement aids producers in maintaining their margins, even amidst fluctuations in raw material prices. The market's competitive landscape is bustling, with regional specialists, direct-to-consumer newcomers, and established food giants all vying for a slice of the bread mixes pie.

Key Report Takeaways

- By nature, conventional products led with 69.82% of the bread mixes market share in 2025, whereas organic variants are projected to expand at a 6.98% CAGR through 2031.

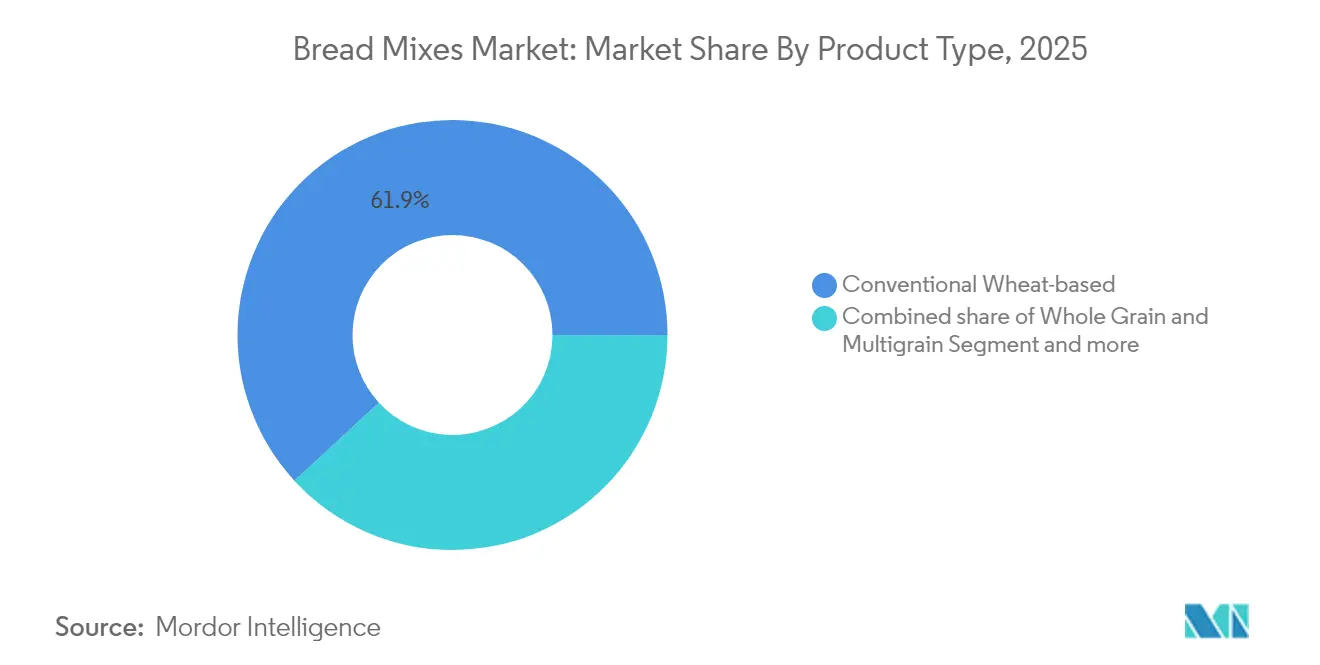

- By product type, conventional wheat-based mixes captured 61.85% share of the bread mixes market size in 2025; gluten-free alternatives are forecast to climb at a 7.29% CAGR to 2031.

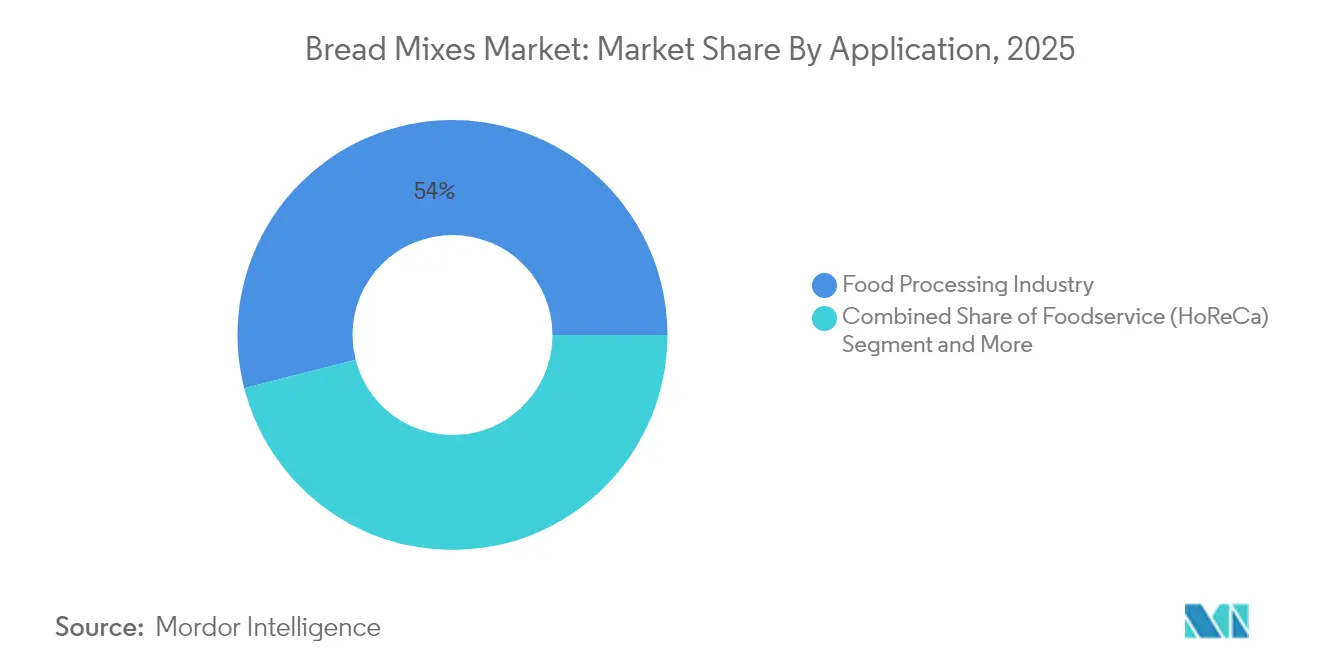

- By application, the food processing industry held 53.98% revenue share in 2025, while the retail/household segment is set to grow at a 6.32% CAGR through 2031.

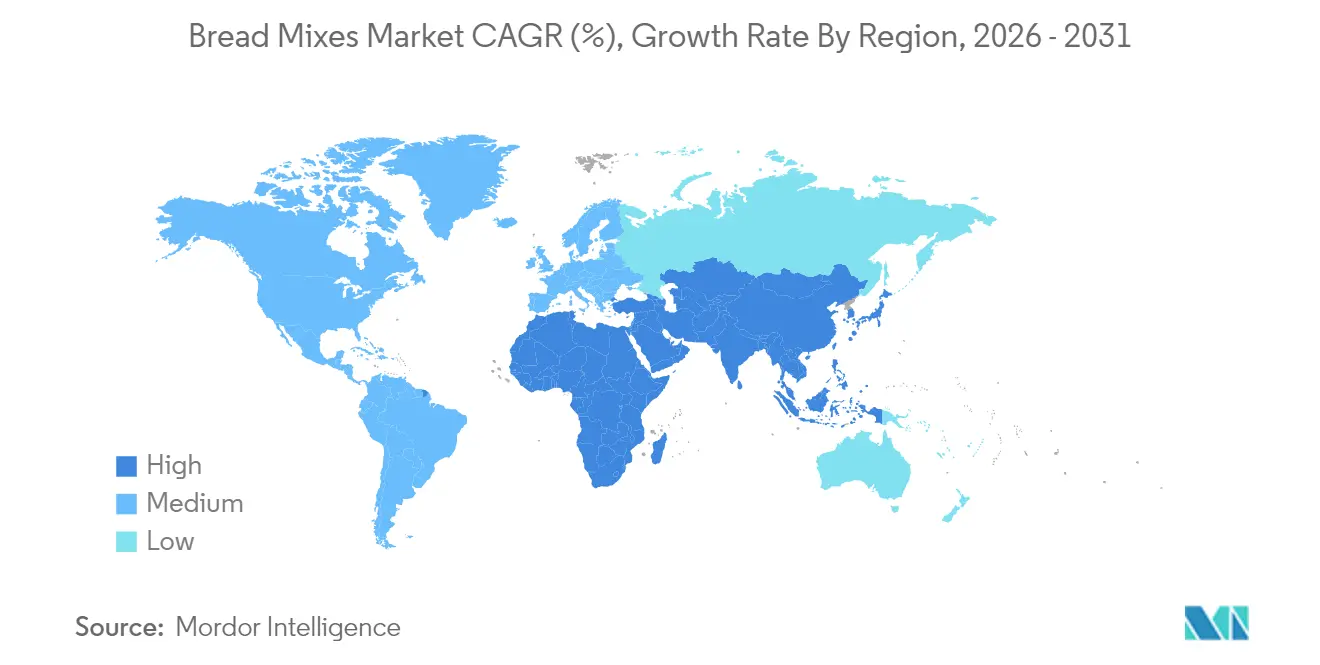

- By geography, Europe accounted for 31.20% of total revenue in 2025; Asia-Pacific represents the fastest regional CAGR at 6.14% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bread Mixes Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing popularity of home baking | +1.2% | Global, with peak intensity in North America & Europe | Medium term (2-4 years) |

| Increasing demand for convenient baking solutions | +0.9% | Global, strongest in urban centers across all regions | Short term (≤ 2 years) |

| Rising demand for gluten-free and clean-label bread mixes | +1.1% | North America & Europe core, expanding to APAC | Long term (≥ 4 years) |

| Growth of foodservice and artisan bakery sectors | +0.8% | Global, with APAC showing accelerated adoption | Medium term (2-4 years) |

| Technological advancements in bread mix formulations | +0.6% | Developed markets initially, scaling to emerging economies | Long term (≥ 4 years) |

| Widening adoption of plant-based and vegan bread mixes | +0.7% | North America & Europe, selective APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing popularity of home baking

Home baking's resurgence has reshaped consumer buying habits, elevating bread mixes from mere conveniences to essential pantry staples. This shift, which took off during the pandemic, now resonates with evolving lifestyle choices that prioritize experiential cooking and family bonding. Data from the National Agricultural Statistics Service underscores this trend, showing a notable uptick in wheat flour consumption at retail outlets, a testament to the home baking boom in American homes. The U.S. Department of Agriculture reports that per capita wheat flour consumption in the U.S. hit over 130.5 pounds in 2023, a rise from 129.4 pounds in 2020, signaling a growing appetite[1]US Department of Agriculture, "Per capita consumption of wheat flour in the United States from 2000 to 2024", www.usda.gov. Today's consumers, moving beyond mere convenience, are on the lookout for products that not only hone their baking skills but also guarantee top-notch results. Social media has played a pivotal role in this baking renaissance, cultivating lively communities that celebrate home baking milestones. These platforms have heightened the demand for visually appealing, Instagram-ready bread types, a demand that traditional bread mixes are adeptly meeting with their innovative formulations.

Increasing demand for convenient baking solutions

Time-pressed consumers are increasingly seeking products that deliver artisanal-quality results without requiring extensive expertise or lengthy preparation. This trend has prompted manufacturers to focus on innovations in packaging formats, simplified mixing instructions, and ingredient pre-treatment methods. Dual-income households and urban professionals, in particular, find these solutions appealing as they aspire to enjoy the experience of homemade bread but often lack the time or traditional baking skills. According to Statistics South Korea, in 2023, approximately 48.2% of households in South Korea were dual-earner families, reflecting a slight increase from 46.1% in 2022[2]Statistics Korea, "Share of dual-income households in South Korea from 2011 to 2023", www.kostat.go.kr. To meet these evolving consumer needs, manufacturers are adopting advanced processing technologies. For instance, high-pressure hydration systems enhance the hydration process by increasing the surface area of dry ingredients, enabling faster and more uniform mixing. By integrating such innovations, the industry is successfully bridging the gap between convenience and quality, addressing the shifting preferences of modern consumers and reinforcing its commitment to delivering value through technological advancements.

Rising demand for gluten-free and clean-label bread mixes

Regulatory clarity on gluten-free labeling has significantly contributed to market expansion while strengthening consumer trust in product claims. The FDA's enforcement of a 20 parts per million gluten threshold has provided manufacturers with well-defined compliance standards. This regulatory certainty has encouraged investments in specialized production facilities and the procurement of high-quality, gluten-free ingredients. Additionally, the growing consumer preference for clean-label products extends beyond gluten-free offerings, emphasizing the importance of ingredient transparency. The current regulatory framework benefits companies capable of navigating complex ingredient labeling requirements while meeting stringent safety standards and consumer expectations for naturalness. In 2024, the FDA introduced updated guidance that further clarified labeling requirements for specialty dietary products. These updates have simplified compliance processes, creating clearer pathways for product innovation, development, and market entry, thereby fostering growth opportunities for businesses in this segment.

Growth of foodservice and artisan bakery sectors

The recovery trajectory of the foodservice industry is driving sustained demand for bread mixes, which play a crucial role in ensuring consistent quality across multiple preparation sites while simultaneously reducing labor requirements. In 2024, U.S. baked goods exports amounted to an impressive USD 4.35 billion, with Canada, Mexico, and Japan emerging as key markets. This highlights the robust international demand for American baking products and ingredients[3]U.S. Department of Agriculture, "U.S. Baked Goods Exports in 2024 ", www.fas.usda.gov. Artisan bakeries are increasingly leveraging premium bread mixes as foundational formulations. These mixes allow operators to incorporate signature ingredients, enabling smaller players to differentiate their offerings and compete on uniqueness rather than relying solely on traditional baking expertise. This shift reflects a broader trend in the foodservice sector, where operational efficiency is prioritized without sacrificing product differentiation. Bread mixes, in this context, serve as versatile platforms for culinary innovation, empowering bakers to balance creativity with efficiency.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternative carbohydrate foods | -0.8% | Global, particularly in health-conscious developed markets | Medium term (2-4 years) |

| Price competition and low profit margins | -0.6% | Global, intensified in price-sensitive emerging markets | Short term (≤ 2 years) |

| Competition from local bakeries and ready-to-eat bread products | -0.5% | Regional variations, strongest in Europe and established markets | Medium term (2-4 years) |

| Fluctuating raw material costs | -0.7% | Global, with regional variations based on agricultural conditions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from alternative carbohydrate foods

The growing popularity of low-carbohydrate and ketogenic diets has significantly impacted traditional bread consumption patterns. Consumers are increasingly opting for alternatives such as cauliflower-based products, almond flour, and other low-carbohydrate options. This trend reflects a broader shift toward health-conscious eating, where traditional wheat-based products are perceived as less desirable, even when they offer convenience. USDA dietary intake data highlights a persistent gap between actual consumption and federal dietary recommendations, particularly in whole grain intake. This suggests that even bread mixes marketed as health-focused face challenges due to these fundamental changes in dietary habits. Furthermore, the shift goes beyond direct substitution; it reflects evolving meal composition preferences. Consumers are increasingly favoring protein-rich or vegetable-forward meals, leading to a noticeable decline in overall bread consumption.

Fluctuating raw material costs

Fluctuations in raw material costs continue to pressure profit margins, intensifying price competition across all market segments. Data from the U.S. Bureau of Labor Statistics indicates that wheat prices for December 2024 dropped to USD 5.49 per bushel, a 19.15% year-over-year decline. Despite this decrease in commodity prices, consumer prices remain insulated due to rising costs in processing, packaging, and distribution. For example, the Producer Price Index for wheat flour rose from 246.432 in April 2024 to 258.178 in May 2024, underscoring persistent inflation in processing costs. On the supply side, U.S. wheat production for the 2024/25 marketing year reached 1.971 billion bushels, marking a 9% increase from the previous year and the highest production level since the 2016/17 season. This production growth is expected to improve raw material availability, potentially alleviating supply-side pressures and supporting market stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialty Formulations Challenge Wheat-Based Leadership

In 2025, conventional wheat-based formulations command a dominant 61.85% market share, capitalizing on established taste preferences, cost efficiency, and reliable baking performance across various applications. This segment's stronghold is a testament to decades of product development and a deep-rooted consumer familiarity with wheat-based bread. According to USDA wheat outlook data, U.S. wheat production is poised to hit an 8-year high, bolstering the availability and cost competitiveness of raw materials for these conventional formulations. Moreover, ongoing technological advancements in wheat processing and milling are not only elevating product quality but also ensuring cost efficiency, allowing conventional wheat products to stand their ground against specialty alternatives.

Meanwhile, gluten-free alternatives are on a rapid ascent, boasting a 7.29% CAGR growth rate projected through 2031. This surge is buoyed by clearer regulatory guidelines on gluten-free labeling and a growing public awareness of celiac disease and gluten sensitivities. The swift rise of the gluten-free segment underscores its dual appeal: a medical imperative for those with celiac disease and a lifestyle choice for many others. The FDA's enforcement of a 20 parts per million gluten threshold offers manufacturers a clear compliance benchmark, simultaneously bolstering consumer trust in product claims. Furthermore, innovations in processing—like advanced ingredient treatments and specialized mixing techniques—are enabling gluten-free products to closely mimic the taste and texture of their traditional wheat counterparts.

By Nature: Organic Growth Accelerates Despite Conventional Dominance

In 2025, conventional bread mixes command a dominant 69.82% market share, underscoring entrenched consumer preferences and a keen price sensitivity across various economic strata. This enduring supremacy of the conventional segment underscores a fundamental market truth: for many, price sensitivity is the primary driver of purchase decisions. Projections from the USDA's agricultural baseline suggest a stable wheat supply, bolstering conventional product manufacturing. Furthermore, heightened price competitiveness of U.S. wheat exports paints a promising picture for domestic producers. The conventional segment enjoys the advantages of well-established supply chains, tried-and-true manufacturing processes, and a broad retail distribution network, ensuring accessibility for all economic demographics and regions.

Organic bread variants are on a robust growth trajectory, expanding at a 6.98% CAGR through 2031. This surge is fueled by consumers increasingly willing to pay a premium for certified organic ingredients and production methods. The organic segment's ascent is further bolstered by clearer regulatory standards for organic certification and a widening retail distribution network, making these products more accessible to the average consumer. Moreover, as clean-label preferences increasingly align with organic demands, manufacturers that can seamlessly integrate both attributes stand to gain significantly. Additionally, FDA's guidance on labeling for plant-based alternatives lends indirect support to the organic sector, clarifying regulatory frameworks and enhancing consumer education for premium positioning.

By Application: Retail Segment Gains Momentum Against Industrial Leadership

In 2025, the food processing industry captures a commanding 53.98% market share, underscoring its scale advantages and steady demand from commercial baking. This leading position is largely due to the industry's reliance on dependable, standardized ingredients, essential for achieving uniform results in large-scale production. Highlighting the industry's significance, the Bureau of Labor Statistics notes that food manufacturing employs over 1.7 million workers, contributing significantly to the economy. Furthermore, the food processing sector leverages economies of scale in purchasing, nurtures established supplier relationships, and boasts technical expertise, allowing for tailored bread mix formulations that meet specific production and product standards.

Retail and household usage is on an upswing, projected to grow at a 6.32% CAGR through 2031. This surge is fueled by a persistent interest in home baking and enhanced product formulations that yield professional-quality results at home. Such growth signals a deeper shift in consumer behavior, moving past pandemic-induced baking trends to a broader embrace of experiential cooking and family-centric activities. Data from the American Time Use Survey by the Bureau of Labor Statistics highlights the significance of home cooking across diverse American demographics. Moreover, advancements in packaging technologies and clearer instructions empower retail products to achieve consistent results, irrespective of the user's expertise, thus making artisanal baking accessible to all.

Geography Analysis

In 2025, Europe commands a 31.20% share of the market, underscoring its rich baking traditions and a discerning consumer base that prioritizes quality and authenticity over mere price. By 2030, Europe's growth is bolstered by regulatory frameworks championing premium positioning, especially in organic certification and clean-label mandates, resonating with consumers' demand for ingredient transparency. European consumers are willing to pay a premium for specialized formulations, paving the way for innovations in gluten-free, organic, and artisanal products. Furthermore, Europe's well-established retail infrastructure and distribution channels offer a competitive edge to both domestic and international manufacturers targeting affluent consumers.

Asia-Pacific is on track to be the fastest-growing region, boasting a 6.14% CAGR through 2031, driven by economic and cultural shifts leaning towards convenience foods and Western dietary habits. With rapid urbanization, there's a burgeoning demand for products that simplify home baking, especially among younger consumers who cherish experiential cooking and social media moments. Rising disposable incomes in markets like China, India, and Southeast Asia are fueling the adoption of premium products, further supported by an expanding retail infrastructure. Given the region's currently low penetration rates, there's a vast potential for growth as consumer awareness and distribution networks evolve.

North America stands as a mature market, characterized by established consumption patterns and a competitive landscape that prioritizes innovation and brand differentiation. The foodservice sector remains robust, highlighted by General Mills' 8% growth in foodservice net sales in Q2 of fiscal 2025, underscoring a steady demand for dependable baking solutions. As consumers increasingly gravitate towards clean-label and organic products, regulatory clarity on labeling and broader retail distribution channels bolster this trend. Moreover, North America's prowess in food processing innovation not only benefits domestic manufacturers but also opens doors for exports, especially with USDA data showcasing enhanced wheat price competitiveness.

Competitive Landscape

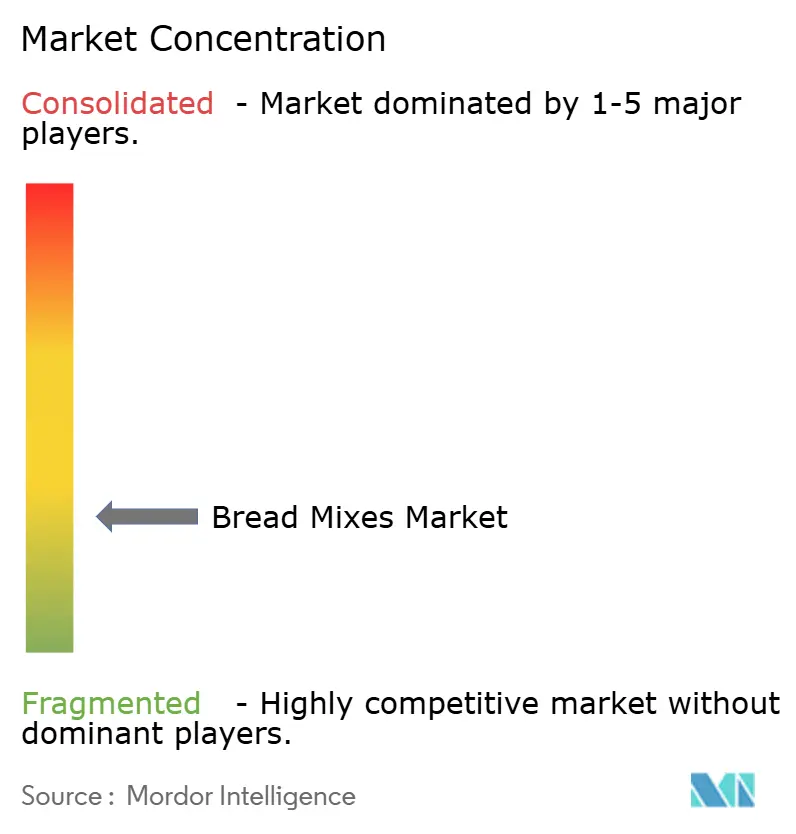

The global bread mixes market is highly fragmented, with numerous regional and international players competing on factors such as product variety, pricing strategies, and distribution networks. Prominent players in the market include General Mills, Inc., Archer Daniels Midland Company, Cargill, Incorporated, Puratos Group, and Associated British Foods Plc. Smaller brands are focusing on niche segments, such as gluten-free and high-protein blends, while larger companies leverage their economies of scale to supply conventional mixes across extensive retail and foodservice channels. This competitive environment fosters continuous innovation, particularly in clean-label and fortified formulations, to meet evolving consumer demands.

Vertical integration has emerged as a key strategic approach, with companies like General Mills and ADM utilizing their positions across the agricultural supply chain to mitigate raw material cost volatility and maintain consistent product quality. Patent activity in the market underscores significant investments in processing innovations, including high-protein formulations and advanced baking techniques, which align with changing consumer preferences for healthier and more nutritious options.

Technology adoption remains a critical differentiator in the bread mixes market. Companies are investing in advanced mixing systems, ingredient pre-treatment technologies, and innovative packaging solutions to enhance product performance and extend shelf life. For instance, the Rapidojet high-pressure hydration system exemplifies how technological advancements can improve ingredient integration while simplifying preparation processes for end users. Additionally, emerging disruptors are reshaping the market by focusing on direct-to-consumer channels and subscription-based models. These approaches bypass traditional retail distribution, enabling brands to build loyalty through personalized product offerings and educational content that enhances consumer baking experiences and success rates.

Bread Mixes Industry Leaders

-

General Mills, Inc

-

Archer Daniels Midland Company

-

Cargill, Incorporated

-

Puratos Group

-

Associated British Foods Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Arabian Mills launched a premium brand for both commercial and consumer use, ‘Master Mills’, as part of a strategic growth initiative. According to the brand, the new range will initially include specialty flours, bread mixes, and baking solutions designed to meet the increasing demand for convenience, quality, and consistency in the bakery and food service sectors.

- March 2025: Birch Benders has introduced its first organic bread and muffin mixes, featuring Organic Blueberry and Organic Chocolate Chip flavors. These mixes combine real, organic ingredients with the convenience of quick preparation—just add eggs, milk, and oil to achieve bakery-quality results. According to the brand, these mixes are the first widely available organic options of their kind, catering to busy consumers who want wholesome, healthier baked goods without sacrificing taste or quality.

- June 2024: At Bakery China 2024, Angel Yeast and BakeMark launched over 40 products under the BakeMark By Angel brand, with a major focus on bakery mixes and icings that include bread mixes for bagels and sourdough, cake mixes, cookie and donut mixes, and a variety of decorative icings. According to the company, these bakery mixes and icings are designed to meet the growing demand for clean-label, nutritious, and convenient baking solutions, supporting healthier eating and catering to both professional and home bakers.

- March 2024: King Arthur Baking Company has launched Savory Bread Mix Kits, a new line of premium mixes featuring Pull-Apart Garlic Bread, Soft & Chewy Pretzel Bites, Crisp & Airy Focaccia, and Perfectly Tender Flatbread. According to the company, each kit includes all necessary dry ingredients, yeast, mix-ins, and toppings, catering to the growing demand for easy, approachable homemade bread options and bridging a gap in the market for convenient savory baking.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the bread mixes market as all dry or liquid formulations containing a balanced blend of flour, leavening agents, conditioners, improvers, and flavor inclusions that enable commercial bakeries, food-service kitchens, and households to produce finished bread with minimal extra ingredients or skill. We include mixes sold in retail packs as well as bulk premixes supplied to industrial plants across every major region during 2020-2030.

Scope Exclusion: Ready-to-bake frozen dough, sweet cake mixes, and pure flour commodities are outside the frame.

Segmentation Overview

-

By Product Type

- Conventional Wheat-based

- Whole Grain and Multigrain

- Gluten Free

- Functional and High Protein

-

By Nature

- Organic

- Conventional

-

By Application

- Food Processing Industry

- Foodservice (HoReCa)

- Retail/Household Use

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with bakery technologists, procurement heads at quick-service chains, regional food distributors, and e-commerce category managers across North America, Europe, Asia-Pacific, South America, and the Middle East. These interviews clarified ingredient cost pass-through, wastage norms, and upcoming gluten-free launches, allowing us to fine-tune elasticities and regional mix preferences.

Desk Research

Our analysts first mapped the demand pool through public datasets such as FAO grain balances, UN Comtrade premix trade codes, USDA bakery product outlooks, and Eurostat bread consumption trends, and then enriched it with insights from bakery trade associations, patent filings on enzyme blends, and 10-K disclosures of leading ingredient suppliers. Subscription tools like D&B Hoovers and Dow Jones Factiva helped us screen company revenues while Questel aided in tracking novel clean-label mix formulations.

The macro inputs were supplemented by price trackers, quarterly wheat futures, and national consumer expenditure surveys that signal home-baking intensity. This desk effort builds the foundational volumes and average selling prices, yet it is not exhaustive; many other reputable open sources were also reviewed for validation.

Market-Sizing & Forecasting

A blended top-down approach starts with flour utilization and premix penetration rates by channel, which are then cross-checked through selective bottom-up roll-ups of supplier sales and sampled ASP x volume calculations. Key variables feeding the model include wheat price spreads, retail private-label share, count of artisan bakeries, per-capita packaged bread intake, and regulatory sodium limits that shift formulation demand. Forecasts rely on multivariate regression layered over ARIMA baselines, with scenario analysis capturing shifts in commodity cycles. Gaps in supplier data are bridged using regional consumption proxies and validated through our expert panel before lock-in.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer analyst checks, and final sector lead sign-off. We refresh every twelve months and trigger interim updates when material events, such as crop shocks or major capacity additions, arise. A pre-publication sweep ensures clients receive the latest reconciled view.

Why Mordor's Bread Mixes Baseline Commands Reliability

Published estimates often diverge because firms pick different product mixes, geographies, and pricing ladders. Our disciplined scoping, consistent currency conversion, and annual refresh mean decision-makers start from a steadier platform.

Key gap drivers include narrower retail-only coverage by some publishers, exclusion of bulk food-service mixes, static ASP assumptions, and less frequent data updates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.85 B (2025) | Mordor Intelligence | - |

| USD 5.00 B (2022) | Global Consultancy A | Retail focus and limited Asian data |

| USD 4.10 B (2025) | Industry Publisher B | Omits industrial premix and food-service channels |

| USD 5.10 B (2024) | Regional Research Firm C | Uses single ASP and biennial refresh cycle |

These contrasts show that Mordor's wider channel capture, live commodity tracking, and yearly recalibration deliver a balanced, transparent baseline that planners can replicate, debate, and trust.

Key Questions Answered in the Report

What is the current value of the bread mixes market?

The bread mixes market is valued at USD 20.92 billion in 2026 and is expected to reach USD 27.24 billion by 2031.

Which product type generates the largest sales?

Conventional wheat-based mixes account for 61.85% of sales, maintaining the lead due to familiarity and cost efficiency.

Which segment is growing the fastest?

Gluten-free bread mixes post the highest forecast CAGR at 7.29% through 2031, supported by regulatory clarity and health-driven demand.

Which region shows the strongest growth momentum?

Asia-Pacific records the fastest regional CAGR at 6.14% as urbanization and Western culinary influence expand the consumer base.

Page last updated on: