Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.83 Billion |

| Market Size (2026) | USD 0.87 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

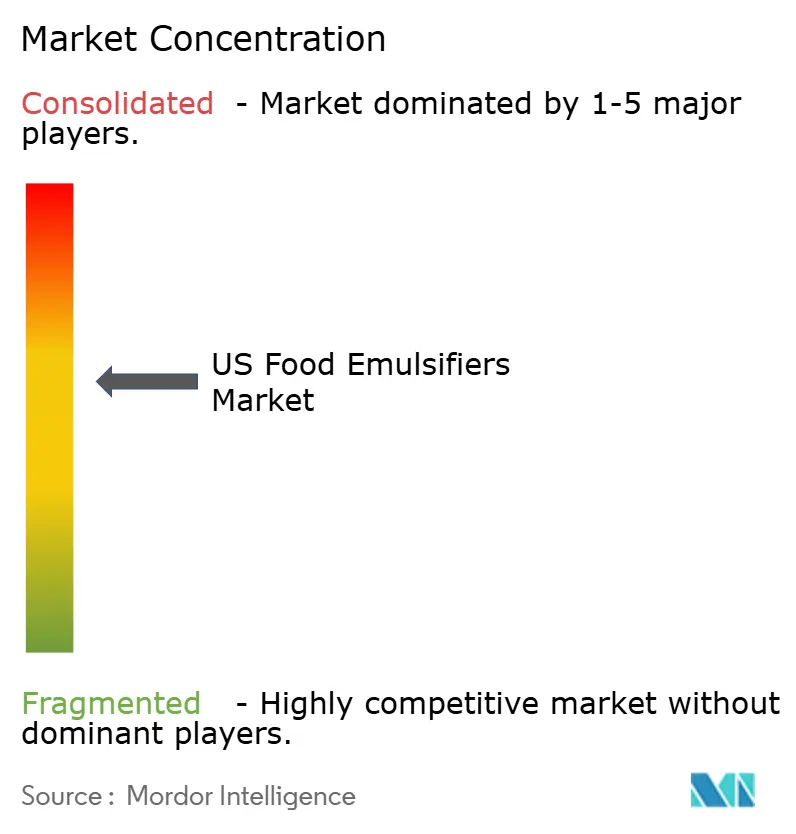

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Food Emulsifiers Market Analysis by Mordor Intelligence

The United States Food Emulsifiers Market size is expected to grow from USD 0.83 billion in 2025 to USD 0.87 billion in 2026 and is forecast to reach USD 1.09 billion by 2031 at 4.72% CAGR over 2026-2031. Consistent demand for texture-enhanced processed foods, a steady shift toward plant-based ingredients, and the Food and Drug Administration’s (FDA) tightened Generally Recognized as Safe (GRAS) notification process are steering growth while reshaping competitive rules Momentum also comes from premium dairy, fortified snacks, and functional beverages where sophisticated emulsifiers stabilize sensitive bioactives and deliver indulgent textures. Key players leverage vertical integration to navigate raw material cost volatility, with rising cocoa prices driving demand for specialized emulsifiers that optimize formulations and reduce input costs. This trend extends beyond confectionery, as food processors increasingly adopt emulsifiers to manage cost pressures and enhance product performance. Segmentation analysis highlights opportunities across product types and forms, with innovative plant-based alternatives and liquid formulations gaining traction. Manufacturers are prioritizing efficiency and clean-label solutions to align with market demands and regulatory expectations. On the flip side, allergen worries around soy lecithin and consumer calls for “emulsifier-free” foods temper near-term gains, prompting investment in sunflower, pea, and cellulose-based systems.

Key Report Takeaways

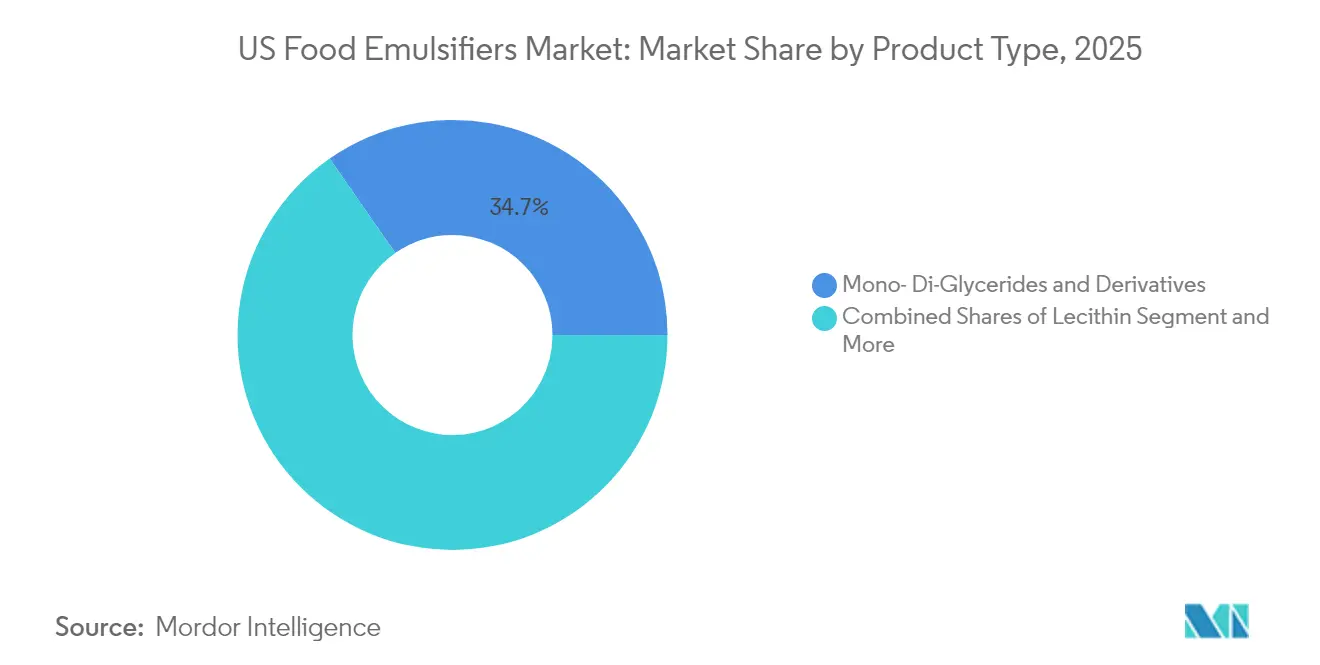

- By product type, mono- and di-glycerides led with 34.68% of the U.S. food emulsifiers market share in 2025; the “Others” cluster of plant and specialty variants is slated for the fastest 5.88% CAGR through 2031.

- By form, powder products held 66.35% of the U.S. food emulsifiers market size in 2025, whereas liquid formats are pacing ahead at a 5.42% CAGR.

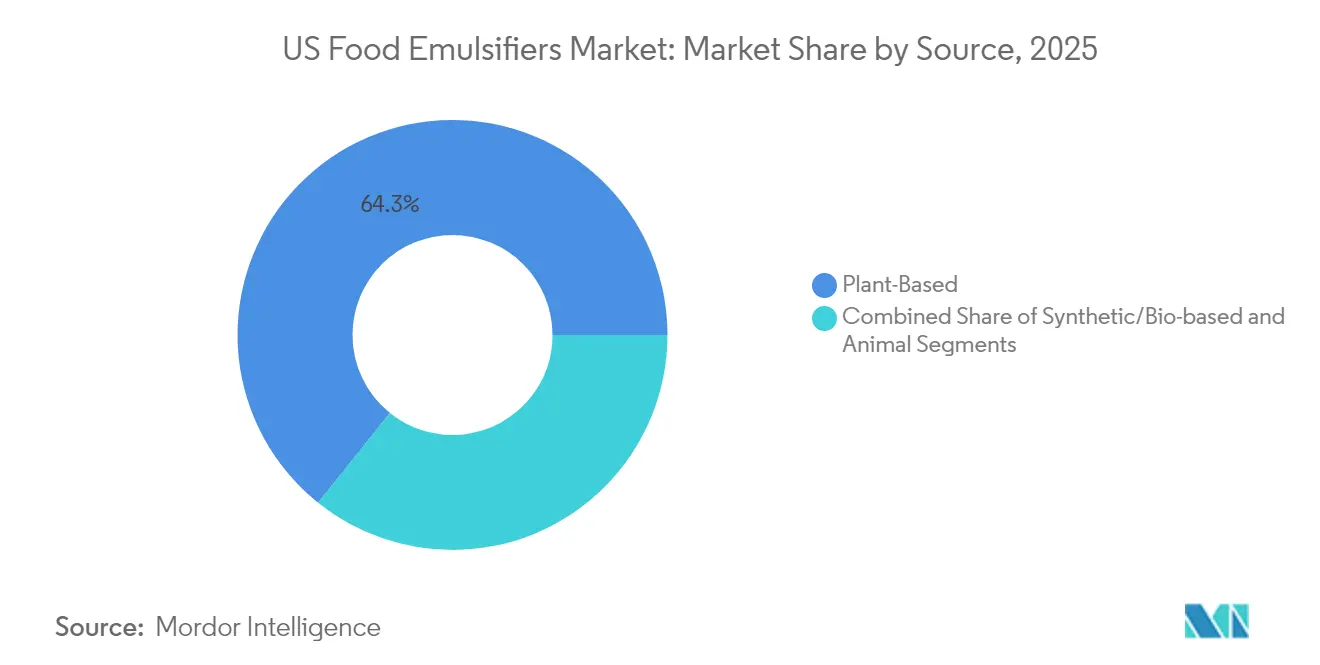

- By source, plant-based offerings captured 64.25% share of the U.S. food emulsifiers market size in 2025 and are growing at 6.31% CAGR.

- By application, bakery and confectionery retained 33.52% share of the U.S. food emulsifiers market size in 2025; dairy and desserts represent the quickest 6.02% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Food Emulsifiers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for texture-enhanced processed foods in the U.S. | +1.2% | National, concentrated in major food manufacturing hubs | Medium term (2-4 years) |

| Growing health consciousness fueling demand for low-fat and fat-replacer ingredients | +0.9% | National, with premium segments in coastal regions | Long term (≥ 4 years) |

| Innovation in functional foods and nutraceutical snacks | +0.8% | National, early adoption in California, New York, Texas | Medium term (2-4 years) |

| Boom in premium and artisanal ice cream and dessert market | +0.6% | National, concentrated in urban and affluent suburban areas | Short term (≤ 2 years) |

| Widespread use in fat-soluble vitamin fortified food | +0.4% | National, with regulatory support from FDA initiatives | Long term (≥ 4 years) |

| Emulsifier role in enhancing freeze-thaw stability in frozen foods | +0.3% | National, driven by cold chain infrastructure improvements | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for texture-enhanced processed foods in the U.S.

Consumer demand for premium textures in processed foods is driving advanced applications of emulsifiers beyond their traditional stabilization functions. According to the Institute of Food Technologists, texture is a critical factor influencing purchasing decisions. In response, manufacturers are leveraging hydrocolloids and specialized emulsifiers to develop sensory profiles that replicate artisanal preparation methods[1]Source: Institute of Food Technologists, “Texture Tops Consumers’ Purchase Drivers,” ift.org. Ultra-shear technology, funded by USDA NIFA research grants, enables food processors to produce stable emulsions without synthetic additives, addressing both texture enhancement and clean label requirements. This technology’s capability to process liquid foods with minimal thermal exposure delivers unique sensory attributes while extending shelf life. This is particularly beneficial for plant-based protein beverages, where achieving consistent texture remains a formulation challenge. The integration of texture science and processing innovation positions emulsifiers as strategic tools for premium product differentiation rather than basic functional ingredients.

Growing health consciousness fueling demand for low-fat and fat-replacer ingredients

Health-conscious consumers are influencing emulsifier demand by prioritizing reduced-fat formulations that retain premium sensory attributes. Soy protein isolate has positioned itself as a multifunctional ingredient, delivering both emulsification and fat replacement benefits, particularly in applications like ice cream. Its foaming and gelling properties enable manufacturers to lower fat content while maintaining texture integrity. The FDA's updated "healthy" claim definition, effective February 2025, introduces specific criteria for food group equivalents and nutrient thresholds, driving manufacturers to innovate with fat-replacing emulsifiers[2]Source: U.S. Food and Drug Administration, “Food Labeling; Nutrient Content Claims; Definition of Term ‘Healthy’,” federalregister.gov. This regulatory shift presents a significant opportunity for plant-based emulsifiers, which address fat reduction, align with clean label trends, and enhance nutritional profiles. The competitive advantage lies in emulsifiers' ability to sustain product performance while supporting health claims, enabling premium pricing in a crowded market.

Innovation in functional foods and nutraceutical snacks

Innovation in functional foods is driving the need for advanced emulsifiers that stabilize bioactive compounds while ensuring product appeal and shelf life. Emulsification technologies are essential for incorporating lipophilic functional ingredients, such as omega-3 fatty acids and fat-soluble vitamins, into food systems. Recent developments in encapsulation materials and stabilization techniques have significantly improved bioavailability during processing and digestion. The emergence of Pickering emulsions, which utilize solid particles instead of traditional surfactants, marks a shift toward sustainable emulsification systems. These systems reduce reliance on synthetic additives while delivering superior stability for hydrophobic compounds. Additionally, the technology's capability to encapsulate bioactive compounds for controlled release aligns with the growing demand from nutraceutical manufacturers for targeted delivery solutions. Companies investing in these advanced emulsification platforms are well-positioned to capitalize on premium pricing opportunities in the expanding functional foods market, where consumers are increasingly willing to pay for scientifically validated health benefits.

Boom in premium and artisanal ice cream and dessert market

The expansion of the premium ice cream segment is driving sophisticated demand for emulsifiers, shifting their role from traditional stabilization to enabling texture customization and supporting clean label claims. Studies indicate that fat content plays a critical role in shaping the sensory attributes of ice cream, with emulsifiers being essential for texture development and maintaining stability during freeze-thaw cycles. Functional ice cream formulations, incorporating ingredients such as microparticulated whey proteins, inulin, and omega-3 fatty acids, utilize specialized emulsifiers like locust bean gum to ensure product consistency while delivering added nutritional value. The premium positioning of these products enables manufacturers to offset higher emulsifier costs and achieve margins that justify investments in advanced formulation technologies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Allergen concerns from soy-based emulsifiers | -0.7% | National, allergy-sensitive cohorts | Short term (≤ 2 years) |

| Rising demand for emulsifier-free whole-food products | -0.5% | Premium segments | Long term (≥ 4 years) |

| Stringent FDA compliance requirements | -0.4% | National | Medium term (2-4 years) |

| Use limitations in select categories | -0.3% | Category-specific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Allergen concerns from soy-based emulsifiers

Although soy lecithin remains a widely used food emulsifier, increasing regulatory scrutiny and allergen concerns are creating operational challenges for manufacturers. The University of Nebraska's Food Allergen Research and Resource Program indicates that while soy lecithin contains minimal soy proteins, most soy-allergic consumers are unaffected due to protein removal during production. However, the FDA's Food Allergen Labeling and Consumer Protection Act mandates soy lecithin labeling, with limited exemptions such as for release agents. This regulatory requirement has heightened consumer awareness, driving demand for alternative emulsifiers. Businesses focusing on sunflower lecithin and other plant-based substitutes are well-positioned to capitalize on this shift. Research highlights the effectiveness of modified sunflower lecithin in stabilizing nanoemulsions, particularly for omega-3 delivery applications. The strategic priority for manufacturers is to develop cost-effective, functionally equivalent alternatives that comply with allergen labeling regulations while maintaining competitive pricing against established soy-based systems.

Increasing demand for emulsifier-free, whole food-based products

Growing consumer demand for minimally processed foods is driving the market for emulsifier-free formulations, presenting manufacturers with the challenge of maintaining product stability and texture through alternative methods. Non-thermal technologies, such as high-pressure processing and pulsed electric fields, enable manufacturers to achieve microbial control and texture modification without synthetic emulsifiers. However, these technologies require substantial capital investment and process optimization. The complexity increases in applications where emulsifiers deliver essential functionalities beyond stabilization, such as freeze-thaw stability in frozen products or oil-water interface management in sophisticated formulations. Companies effectively addressing this trend are focusing on ingredient transparency and process innovation. Rather than eliminating emulsifiers entirely, they are positioning natural and minimally processed emulsifiers as premium alternatives to synthetic options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialty Emulsifiers Drive Innovation

In 2025, mono- and di-glycerides accounted for 34.68% of the U.S. food emulsifiers market, driven by their adaptability and cost efficiency. The specialty "others" category, encompassing PGPR, sucrose esters, and cellulose nanocrystal systems, is anticipated to grow at a 5.88% CAGR, fueled by the increasing alignment of plant-based claims with performance requirements. The transition of lecithin from soy to sunflower is accelerating, while sorbate esters are gaining adoption in acidic confectionery applications due to their pH-specific solubility, which outperforms competing materials.

Meanwhile, pickering emulsions are disrupting traditional approaches, enabling niche suppliers to secure high-value contracts within the U.S. food emulsifiers market. Chocolate manufacturers are leveraging proprietary blends of PGPR and lecithin to reduce dependency on cocoa butter and manage price fluctuations. This strategy not only delivers cost advantages but also enhances texture control. Suppliers that combine application laboratories with flexible pilot production lines are effectively shortening product development cycles and establishing long-term supply agreements.

By Form: Processing Efficiency Drives Liquid Growth

Powder products captured 66.35% of the U.S. food emulsifiers market share in 2025, thanks to ambient-temperature stability and automated dry-mix handling in mega-bakery plants. Yet liquid formats clock a 5.42% CAGR as ready-to-use dispersions cut batching times and eliminate dust concerns. Microfluidization studies show liquid lecithin achieving narrower droplet curves than high-pressure valve homogenization, boosting mouthfeel and oxidative stability in omega-3 fortified drinks

As flexible packaging gains popularity among co-packers, totes of liquid mono-glycerides improve plant throughput. Conversely, powders remain indispensable in premix sachets and dry bakery blends where water activity limits microbial growth. This balanced demand keeps both formats central to the U.S. food emulsifiers market, though capital spending trends favor incremental liquid capacity in the next planning cycle.

By Source: Plant-Based Dominance Accelerates

Plant origins commanded a 64.25% share in 2025 and track the fastest 6.31% CAGR, propelled by vegan claims, religious dietary conformity, and lower greenhouse-gas footprints. Enzymatically modified oat and pea proteins yield amphiphilic structures with attractive foaming and interfacial tension profiles. The FDA’s GRAS reform heightens scrutiny on novel synthetics, indirectly favoring botanical options that enjoy historical exposure and consumer trust.

The adoption of gelatin substitutes is driving a decline in the use of animal-derived emulsifiers. Synthetic alternatives continue to dominate in high-stress applications, such as retort soups, where thermal stability outweighs the demand for clean-label products. Meanwhile, branded manufacturers are securing multi-source contracts to enhance supply chain reliability and strengthen resilience in the predominantly plant-based U.S. food emulsifiers market.

By Application: Dairy Innovation Outpaces Traditional Segments

In 2025, the U.S. food emulsifiers market sees bakery and confectionery accounting for 33.52% of the market share. However, this segment faces significant challenges, including rising grain prices and increasing pressure to reformulate products to align with evolving health trends. On the other hand, the dairy and desserts segment is experiencing robust growth, driven by advancements in frozen dessert innovations and the expanding popularity of plant-based yogurt. This segment is projected to grow at a compound annual growth rate of 6.02% during the forecast period.

In the functional beverages segment, manufacturers are incorporating bilayer nanoemulsions to deliver vitamin D and curcumin, leveraging high hydrophilic-lipophilic balance (HLB) systems that outperform traditional lecithin-based solutions. Similarly, the meat analogues segment is utilizing protein-polysaccharide complexes to replicate the juiciness and texture of animal fat, addressing consumer demand for high-quality alternatives. These diverse applications across end-use industries not only enhance the market's volume potential but also provide a buffer against cyclical fluctuations, ensuring stability within the U.S. food emulsifiers market.

Geography Analysis

Regional consumption patterns mirror food-processing capacity, logistics, and consumer demographics. The Midwest dominates volume on the back of dense bakery, snack, and confectionery plants clustered near grain belts. Chicago and Minneapolis house major research centers, giving suppliers proximity to pilot lines and QA staff. The U.S. food emulsifiers market size in this corridor benefits from integrated rail and interstate links that curtail freight costs.

California and the broader West Coast drive premium and plant-based innovation. Silicon Valley ventures partner with ingredient companies to prototype low-carb pastry or algae-oil ice-cream using advanced emulsifiers for mouthfeel. Nutraceutical beverage makers around Los Angeles favor microfluidized sunflower lecithin for clean-label marketing, boosting regional value share despite lower tonnage.

The Northeast excels in craft chocolate and specialty bakery segments that tolerate higher cost inputs. Fast-casual brands headquartered in New York source allergen-free emulsifier blends to meet diverse customer bases. Meanwhile, the Southeast’s booming population underpins new greenfield dairy and frozen-meal facilities that amplify future demand. Suppliers with Gulf-Coast port access leverage import resin flexibility for PGPR and succinate esters, reinforcing logistical advantages within the expansive U.S. food emulsifiers market.

Competitive Landscape

The U.S. food emulsifiers market shows moderate concentration, with a handful of vertically integrated multinationals flanked by nimble specialists. Emphasis is given to the merger, expansion, acquisition, and partnership of companies, along with new product development, as strategic approaches adopted by leading companies to boost their brand presence among consumers. Key players dominating the country's market include Lecital LLC, National Lecithin Inc., Cargill, Incorporated, Kerry Group plc, and BASF SE, among others.

Following its merger, IFF divested its food-texture portfolio, creating growth opportunities for Danish specialist Palsgaard and German lecithin producer Lecico. Smaller players are competing by leveraging their expertise in applications, such as developing custom bakery blends and operating high-shear beverage labs, while maintaining agile lead times. Although intellectual property barriers are relatively low, competitive differentiation in the U.S. food emulsifiers market is driven by robust documentation, advanced sensory analytics, and sustainability metrics that are increasingly demanded by multinational clients.

Regulatory expertise remains a critical competitive advantage. Established GRAS dossiers streamline approval processes, particularly for line extensions. Companies are prioritizing investments in carbon-footprint data to meet the scope-3 transparency requirements of ESG-focused retailers. Additionally, the adoption of digital twin modeling for emulsion stability accelerates customer formulation timelines, translating scientific advancements into operational efficiencies and strengthening supplier relationships.

US Food Emulsifiers Industry Leaders

Lecital LLC

National Lecithin Inc

Cargill, Incorporated

Kerry Group plc

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Aditya Birla Group, through its subsidiary Aditya Birla Chemicals (USA) Inc., has strategically entered the United States chemicals market by acquiring Cargill's specialty chemical manufacturing facility in Dalton, Georgia. This acquisition aligns with the group's objective to strengthen its presence in the US manufacturing landscape.

- June 2025: Indorama Ventures introduced a food-grade emulsifier portfolio. The ALKEST SP 80 K and ALKEST SP 60 K product lines are strategically developed to serve key applications in bread, confectionery, oils, dairy, and beverages. These solutions deliver critical emulsifying and emollient properties, enhancing product quality and operational performance.

- October 2024: Tate & Lyle acquired CP Kelco for £1.48 billion, bolstering its portfolio in specialty chemicals and additives vital to the food emulsifiers market. This strategic acquisition paves the way for innovations in healthier, more functional food products.

- April 2024: Private investment firm Kingswood Capital Management LP has acquired Corbion’s emulsifier business for a cash price of US$362 million. The deal includes two manufacturing plants in the U.S., underscoring Kingswood’s strategy to bolster its operational capabilities and market footprint.

US Food Emulsifiers Market Report Scope

The United States food emulsifier market has been segmented by type into lecithin, monoglyceride, diglyceride, and derivatives, sorbitan ester, polyglycerol ester, and other types; and by application into dairy and frozen products, bakery, meat, poultry, and seafood, beverage, confectionery, and other applications.

By Product Type

| Mono- Di-Glycerides and Derivatives |

| Lecithin |

| Sorbate Esters |

| Other Emulsifier |

By Form

| Powder |

| Liquid |

By Source

| Plant |

| Synthetic/Bio-based |

| Animal |

By Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Meat and Meat Products |

| Soups, Sauces, and Dressings |

| Other Applications |

| By Product Type | Mono- Di-Glycerides and Derivatives |

| Lecithin | |

| Sorbate Esters | |

| Other Emulsifier | |

| By Form | Powder |

| Liquid | |

| By Source | Plant |

| Synthetic/Bio-based | |

| Animal | |

| By Application | Bakery and Confectionery |

| Dairy and Desserts | |

| Beverages | |

| Meat and Meat Products | |

| Soups, Sauces, and Dressings | |

| Other Applications |

Key Questions Answered in the Report

What is the current value of the U.S. food emulsifiers market?

The market stands at USD 0.87 billion in 2026 and is projected to reach USD 1.09 billion by 2031.

Which emulsifier type leads the U.S. food emulsifiers market?

Mono- and di-glycerides hold the largest 34.68% share thanks to versatility in bakery, confectionery, and dairy.

Why are plant-based emulsifiers growing faster than synthetic ones?

Consumer preference for clean labels, vegan diets, and the FDA’s stricter GRAS pathway propel a 6.31% CAGR for plant-based options.

Which application segment is expanding the fastest?

Dairy and desserts are advancing at a 6.02% CAGR, driven by premium ice cream, plant-based yogurt, and fortified frozen treats that rely on advanced emulsifiers for texture and stability.

Page last updated on: