北美糖尿病药物市场规模及份额

市场概述

| 研究期 | 2019 - 2030 |

|---|---|

| 预测数据期 | 2025 - 2030 |

| 历史数据期 | 2019 - 2023 |

| 市场规模 (2025) | 42.08 十亿美元 |

| 市场规模 (2030) | 54.94 十亿美元 |

| 增长率 (2025 - 2030) | 5.48% CAGR |

| 市场集中度 | 高 |

主要参与者

*免责声明:主要玩家排序不分先后 图片 © Mordor Intelligence。重新使用需遵守 CC BY 4.0 并注明出处。 |

|

Mordor Intelligence北美糖尿病药物市场分析

北美糖尿病药物市场在2025年达到420.8亿美元,预计到2030年将达到549.4亿美元,期间复合年增长率为5.48%。糖尿病和肥胖症治疗的日益融合,加上新一代GLP-1受体激动剂的快速采用,提供了大部分前进动力。美国处方药支出在2024年攀升10.2%,GLP-1药物已成为最大且增长最快的治疗支出类别。[1]美国卫生系统药师协会,"美国2024年药物支出增长10.2%,减肥药物仍是主要驱动力,"ashp.org尽管注射剂创新加速,口服抗糖尿病药物仍控制着大部分治疗量,生物类似胰岛素的引入正在压缩关键细分市场的价格。严格的医疗保险谈判、州价格上限法规和付费方预先授权规则正在重塑处方选择,但治疗创新使总支出保持上升轨迹。墨西哥作为制造中心的崛起以及在线药房的扩张也在改变该地区的竞争经济学和患者准入。

关键报告要点

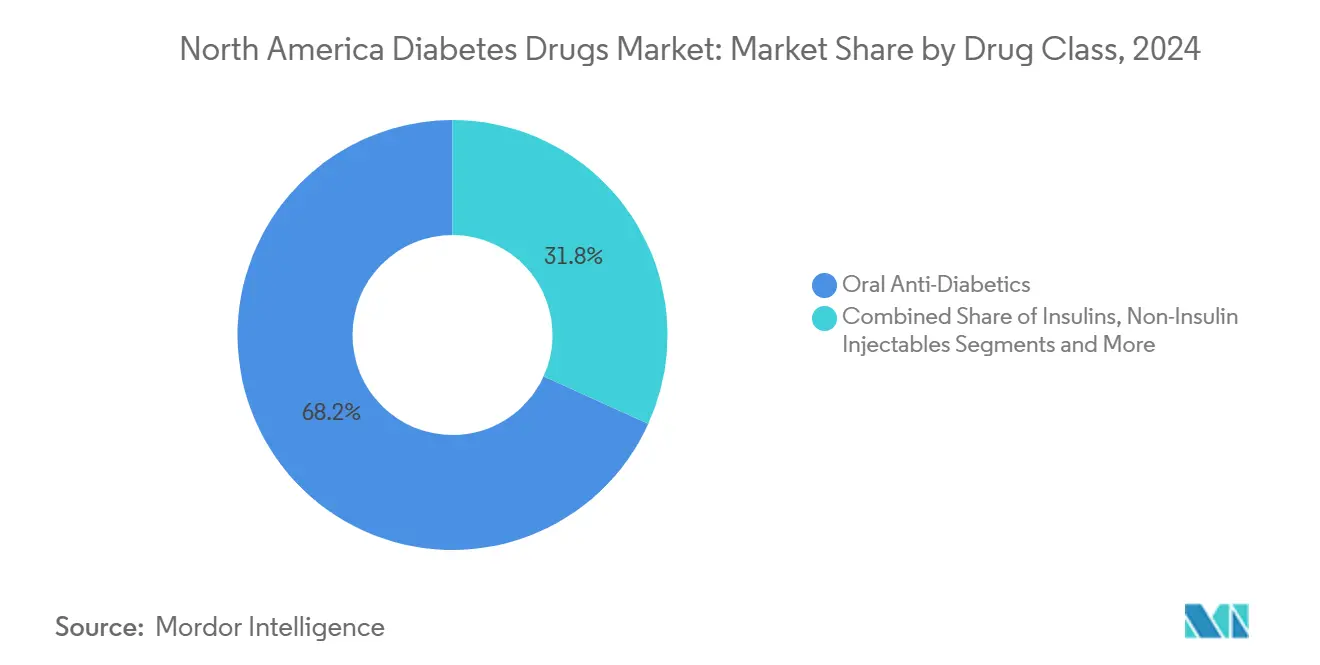

- 按药物类别,口服抗糖尿病药物在2024年以68.23%的收入份额领先;非胰岛素注射剂预计将在2030年前实现最高7.52%的复合年增长率。

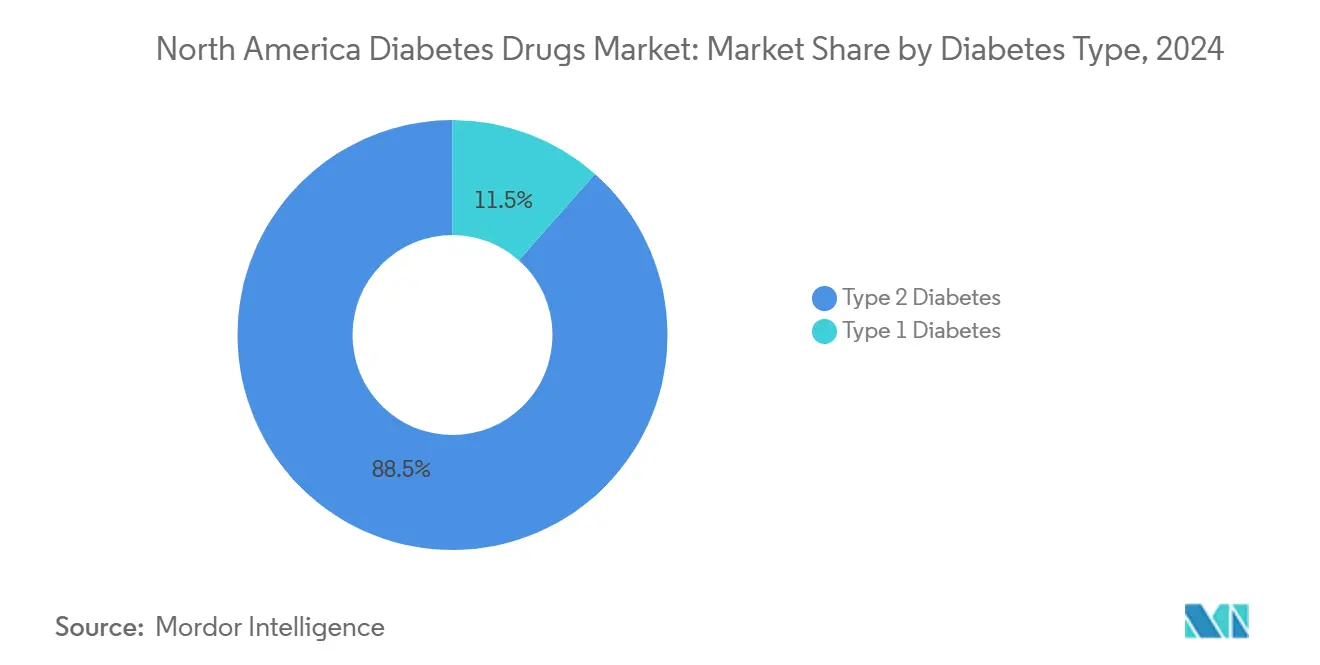

- 按糖尿病类型,2型治疗在2024年占治疗量的88.46%,而1型药物预计在2030年前以更快的6.32%复合年增长率推进。

- 按药物来源,品牌产品在2024年控制了79.35%的北美糖尿病药物市场份额,但通用药和生物类似药正以9.01%的复合年增长率发展。

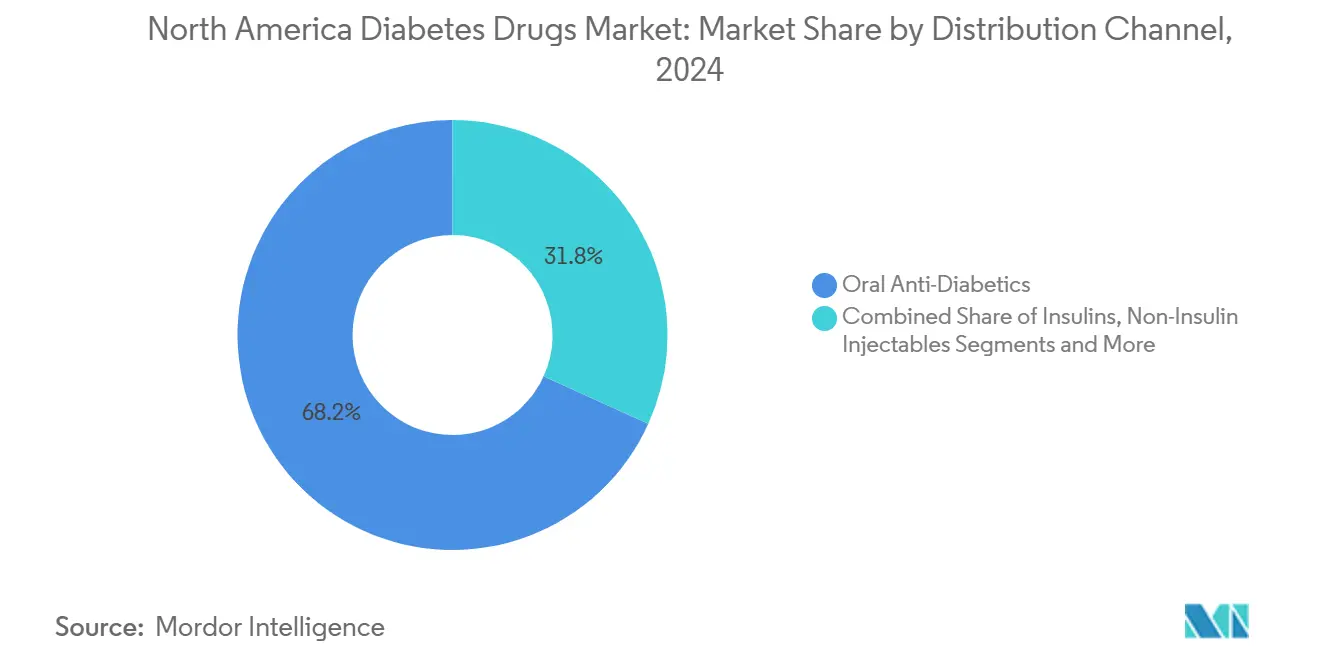

- 按销售渠道,零售药房在2024年占据51.23%的收入;在线药房以8.78%的复合年增长率增长最快。

- 按地理位置,美国在2024年占北美糖尿病药物市场规模的89.45%,而墨西哥预计到2030年将以6.39%的复合年增长率扩张。

北美糖尿病药物市场趋势与洞察

驱动因素影响分析

| 驱动因素 | (~)对复合年增长率预测的%影响 | 地理相关性 | 影响时间线 |

|---|---|---|---|

| 在肥胖T2DM中日益采用GLP-1 激动剂 | +1.2% | 美国和加拿大, 向墨西哥蔓延 | 中期(2-4年) |

| 双重及三重肠促胰素的 报销扩展 | +0.8% | 主要在美国,加拿大 选择性覆盖 | 短期(≤2年) |

| 生物类似胰岛素价格战 加速采用 | +0.6% | 北美范围内,在美国最强 | 长期(≥4年) |

| CGM关联的剂量算法促进 药物依从性 | +0.4% | 美国和加拿大,墨西哥 渗透率有限 | 中期(2-4年) |

| 雇主肥胖-糖尿病捆绑 合同 | +0.3% | 美国企业市场 | 短期(≤2年) |

| 美墨笔式注射器填充 生产线近岸化 | +0.2% | 美墨边境地区 | 长期(≥4年) |

| 来源: Mordor Intelligence | |||

在肥胖T2DM中日益采用GLP-1激动剂

GLP-1受体激动剂统一了肥胖和糖尿病管理,这一联系与88%以上的2型糖尿病患者相关。替尔泊肽在2023年底达到约12%的降糖药物处方份额,其在非糖尿病减肥用户中的受欢迎程度突显了代谢适应症之间的治疗模糊性。[2]Jaime Almandoz医学博士等,"讨论替尔泊肽在糖尿病、肥胖护理中的兴起,"ajmc.com双重GLP-1/GIP活性比单一靶点药物提供更大的体重和HbA1c降低,而新兴的三重激动剂如瑞塔鲁肽在48周时已取得24%的减肥效果,创下新的临床基准。FDA针对更广泛心脏代谢适应症的快速批准正在扩大报销范围,并鼓励处方医生在护理路径中更早采用这些疗法。

双重及三重肠促胰素的报销扩展

付费方正在重新调整处方集以认识双重和三重肠促胰素的心血管和肾脏益处。医疗保险的价格谈判对传统口服药物施加更大压力,而较新的GLP-1药物获得优选层级覆盖,从而降低老年人的自付费用。[3]医疗保险权利中心,"政府提供首批10种受价格谈判约束药物的更多数据,"medicarerights.org商业保险公司现在将肥胖归类为医疗疾病,解锁了之前保留给糖尿病的药物治疗预算。雇主健康计划正在捆绑与结果指标相关的肥胖和糖尿病护理合同,强化使用增长。

生物类似胰岛素价格战加速采用

自35美元胰岛素共付额上限生效以来,生物类似药制造商加速了市场准入和折扣策略,刺激了更广泛的患者采用,并迫使创新者调整定价。Teva在联邦采购协议下的产能扩张说明了在量上竞争的企业承诺。日益激烈的价格竞争正在扩大胰岛素获取并增加整体治疗量。

CGM关联的剂量算法促进药物依从性

将司美格鲁肽与实时连续血糖监测(CGM)结合使用,相比单独药物治疗额外产生了0.55个百分点的HbA1c降低。较新的CGM算法虽然偶尔低估低血糖风险,但提高了滴定准确性并促进依从性。现在获得FDA许可的非处方CGM设备有望扩大技术采用并强化药物依从性。

制约因素影响分析

| 制约因素 | (~)对复合年增长率预测的%影响 | 地理相关性 | 影响时间线 |

|---|---|---|---|

| 付费方预先授权抑制 GLP-1用量 | −0.9% | 主要在美国,对加拿大 影响有限 | 短期(≤2年) |

| 来自中国供应集中的 API关税风险 | −0.5% | 北美范围内 | 中期(2-4年) |

| 胰腺炎和甲状腺C细胞 肿瘤诉讼 | −0.3% | 美国司法管辖区 | 长期(≥4年) |

| 不断增加的州药物 价格上限立法 | −0.4% | 美国州级变化 | 中期(2-4年) |

| 来源: Mordor Intelligence | |||

付费方预先授权抑制GLP-1用量

美国付费方继续实施多步骤治疗规则,延迟或拒绝GLP-1启动,尽管临床特征良好,导致患者流失和整体市场渗透率较慢。医疗保险优势计划在批准减肥用途方面仍然特别谨慎,保持抑制早期增长的使用上限。

来自中国供应集中的API关税风险

全球糖尿病治疗原料药产量约三分之二仍源自中国。重新实施惩罚性关税可能会提高投入成本并扰乱下游供应,在替代采购规模化之前给北美糖尿病药物市场利润率带来压力。

细分市场分析

按药物类别:口服优势对抗注射剂创新

口服药物在2024年获得了68.23%的北美糖尿病药物市场份额,预计到2030年将以7.52%的复合年增长率扩张,尽管注射剂取得突破,仍保持领先地位。SGLT-2抑制剂如卡格列净基于心肾结局数据和加拿大卫生部标签更新继续获得支持。[4]加拿大卫生部,"Invokana决策摘要基础,"hpfb-dgpsa.c

非胰岛素注射剂在GLP-1、双重GIP/GLP-1和新兴三重激动剂类别的推动下快速攀升。三重机制药物被定位为提供体重、心血管和肾脏益处的高端治疗,从而提升北美糖尿病药物市场内每处方价值。α-葡萄糖苷酶抑制剂在老年群体中保持利基市场,合并多种机制的复合片剂旨在简化给药并提高依从性。

备注: 购买报告后可获得所有个别细分市场的细分份额

按糖尿病类型:1型创新加速增长

2型糖尿病治疗继续主导收入,但1型选择显示出最强的增量收益。每周司美格鲁肽与自动胰岛素输送的集成将血糖达标时间指标从69.4%提升至74.2%,这是有意义的临床进展。由此产生的热情正在扩大1型辅助药物的北美糖尿病药物市场规模。针对β细胞再生的基因治疗项目仍处于商业化前期,但突显了管线深度。

备注: 购买报告后可获得所有个别细分市场的细分份额

按药物来源:生物类似药势头挑战品牌主导地位

品牌药物仍占北美糖尿病药物市场份额的79.35%,但趋势偏向生物类似药。35美元胰岛素共付额上限削弱了传统品牌优势,允许后续制造商主要在可用性和服务方面竞争。联邦合同胜利和简化的FDA可互换性指南应该会加速生物类似胰岛素甘精胰岛素、赖脯胰岛素和门冬胰岛素在零售和专业渠道的渗透。

按销售渠道:数字化转型加速

零售药房在2024年保持51.23%的份额,但在线渠道以8.78%的复合年增长率扩张,因为患者倾向于订阅续费和送货上门。PBM拥有的邮购设施导向高成本GLP-1处方的不成比例量,"任何愿意的药房"规则扩大独立药房参与部分抵消了这一趋势。与远程医疗相关的电子药房的兴起预计将强化在便利性和共付额援助方面的竞争,而不是单纯的地理存在。

备注: 购买报告后可获得所有个别细分市场的细分份额

地理分析

美国在2024年产生了89.45%的北美糖尿病药物市场收入,由高人均医疗支出和广泛的保险覆盖推动。联邦药物价格谈判可能在十年内节省985亿美元,传统糖尿病品牌是首批10个计划实施价格上限的产品之一。州价格上限法律引入拼凑式合规负担,但可能刺激区域竞争折扣。

加拿大的市场由省级处方集和严格的卫生技术评估指导。虽然双重激动剂GLP-1正在获得增量覆盖,但各省采用情况不同,为品牌制造商通过结局证据展示成本效益留出空间。安大略省和魁北克省的通用药采用率相对较高,强化了对创新者的压力。

墨西哥是增长最快的地区,预计到2030年复合年增长率为6.39%。COFEPRIS快速通道批准的扩展和美墨注射笔装配生产线近岸化正在加强供应链、降低价格并改善当地可用性。随着边境集群附近制造业就业增长,国内保险渗透率正在扩大,进一步扩大现代抗糖尿病治疗的可及人口。

竞争格局

北美糖尿病领域适度集中,特点是少数拥有广泛GLP-1、SGLT-2和胰岛素产品组合的跨国现任者。创新者正通过在肥胖、心力衰竭和慢性肾病方面寻求多适应症数据来对冲生物类似药侵蚀--这些策略延长了专利期并增强品牌价值。礼来、诺和诺德和阿斯利康各自宣布八位数投资以扩大三重激动剂生产线和配套数字健康平台规模。

Viatris和Teva等生物类似药进入者正利用积极的合同签订和扩大的灌装能力在基础和速效胰岛素细分市场挑战份额。同时,Hims & Hers和Ro等数字优先药房正与制造商合作分销捆绑远程监测的GLP-1启动套件,扩大它们在北美糖尿病药物市场的足迹。

设备公司与制药公司之间的战略许可--以连续血糖监测数据集成为例--表明治疗和数字诊断之间联系日益紧密。在中期,能够提供与可测量结果相关的治疗-设备捆绑的公司有望获得优质报销层级。

北美糖尿病药物行业领导者

-

诺和诺德

-

赛诺菲

-

礼来

-

默克

-

阿斯利康plc

- *免责声明:主要玩家排序不分先后

近期行业发展

- 2025年2月:美国FDA批准Merilog(门冬胰岛素-szjj)作为诺和锐的生物类似药用于儿童和成人糖尿病治疗。

- 2024年12月:美国FDA批准首个参比Victoza(利拉鲁肽注射液)18 mg/3 mL的通用药。

- 2024年6月:阿斯利康的安达唐获得FDA批准用于10岁及以上儿童T2DM患者的血糖控制。

- 2024年2月:加拿大引入C-64法案,旨在对选定糖尿病药物实现全民、单一付费方覆盖。

北美糖尿病药物市场报告范围

糖尿病药物用于通过降低血液中的葡萄糖水平来治疗糖尿病。北美糖尿病药物市场按药物(胰岛素药物(基础或长效胰岛素、餐时或速效胰岛素、传统人胰岛素和生物类似胰岛素)、口服抗糖尿病药物(双胍类、α-葡萄糖苷酶抑制剂、多巴胺D2受体激动剂、SGLT-2抑制剂、DPP-4抑制剂、磺脲类和格列奈类)、非胰岛素注射药物(GLP-1受体激动剂和胰淀粉样蛋白类似物)和复合药物(胰岛素复合制剂和口服复合制剂))和地理位置(美国、加拿大和北美其他地区)进行细分。报告提供上述细分市场的价值(美元)和数量(单位)。

| 胰岛素 | 基础/长效 |

| 餐时/速效 | |

| 传统人胰岛素 | |

| 生物类似胰岛素 | |

| 非胰岛素注射剂 | GLP-1受体激动剂 |

| 双重/三重激动剂(如替尔泊肽、瑞塔鲁肽) | |

| 胰淀粉样蛋白类似物 | |

| 口服抗糖尿病药物 | 双胍类 |

| SGLT-2抑制剂 | |

| DPP-4抑制剂 | |

| α-葡萄糖苷酶抑制剂 | |

| 磺脲类 | |

| 格列奈类 | |

| 噻唑烷二酮类 | |

| 复合药物 |

| 1型糖尿病 |

| 2型糖尿病 |

| 品牌 |

| 通用/生物类似药 |

| 医院药房 |

| 零售药房 |

| 在线药房 |

| 美国 |

| 加拿大 |

| 墨西哥 |

| 按药物类别 | 胰岛素 | 基础/长效 |

| 餐时/速效 | ||

| 传统人胰岛素 | ||

| 生物类似胰岛素 | ||

| 非胰岛素注射剂 | GLP-1受体激动剂 | |

| 双重/三重激动剂(如替尔泊肽、瑞塔鲁肽) | ||

| 胰淀粉样蛋白类似物 | ||

| 口服抗糖尿病药物 | 双胍类 | |

| SGLT-2抑制剂 | ||

| DPP-4抑制剂 | ||

| α-葡萄糖苷酶抑制剂 | ||

| 磺脲类 | ||

| 格列奈类 | ||

| 噻唑烷二酮类 | ||

| 复合药物 | ||

| 按糖尿病类型 | 1型糖尿病 | |

| 2型糖尿病 | ||

| 按药物来源 | 品牌 | |

| 通用/生物类似药 | ||

| 按销售渠道 | 医院药房 | |

| 零售药房 | ||

| 在线药房 | ||

| 按地理位置 | 美国 | |

| 加拿大 | ||

| 墨西哥 | ||

报告中回答的关键问题

北美糖尿病药物市场有多大?

北美糖尿病药物市场规模预计将在2025年达到371.0亿美元,并以3.58%的复合年增长率增长,到2030年达到442.4亿美元。

1. 北美糖尿病药物市场当前规模如何?

该市场在2025年产生420.8亿美元,预计以5.48%的复合年增长率到2030年攀升至549.4亿美元。

2. 哪个药物类别目前领先市场?

口服抗糖尿病药物占销售额的68.23%,尽管GLP-1注射剂快速增长,但凭借熟悉的给药方式和较低成本得到支持

3. 生物类似药在该地区增长速度如何?

通用药和生物类似药预计到2030年将实现9.01%的复合年增长率,因为专利到期和医疗保险价格上限转移了需求。

4. 为什么GLP-1受体激动剂获得如此大的关注?

它们同时提供血糖、减肥、心血管和肾脏益处,将符合条件的患者群体扩展到传统糖尿病管理之外。

5. 哪个国家显示出最快的需求增长?

墨西哥以6.39%的复合年增长率领先,受新制造工厂、简化的COFEPRIS审查和改善的保险覆盖推动。

6. 医疗保险价格谈判将如何影响市场动态?

对老品牌的价格上限应该会释放付费方预算用于较新的双重和三重肠促胰素,加速向先进疗法的转变,同时削减整体系统成本。

页面最后更新于: