Flexible Frozen Food Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

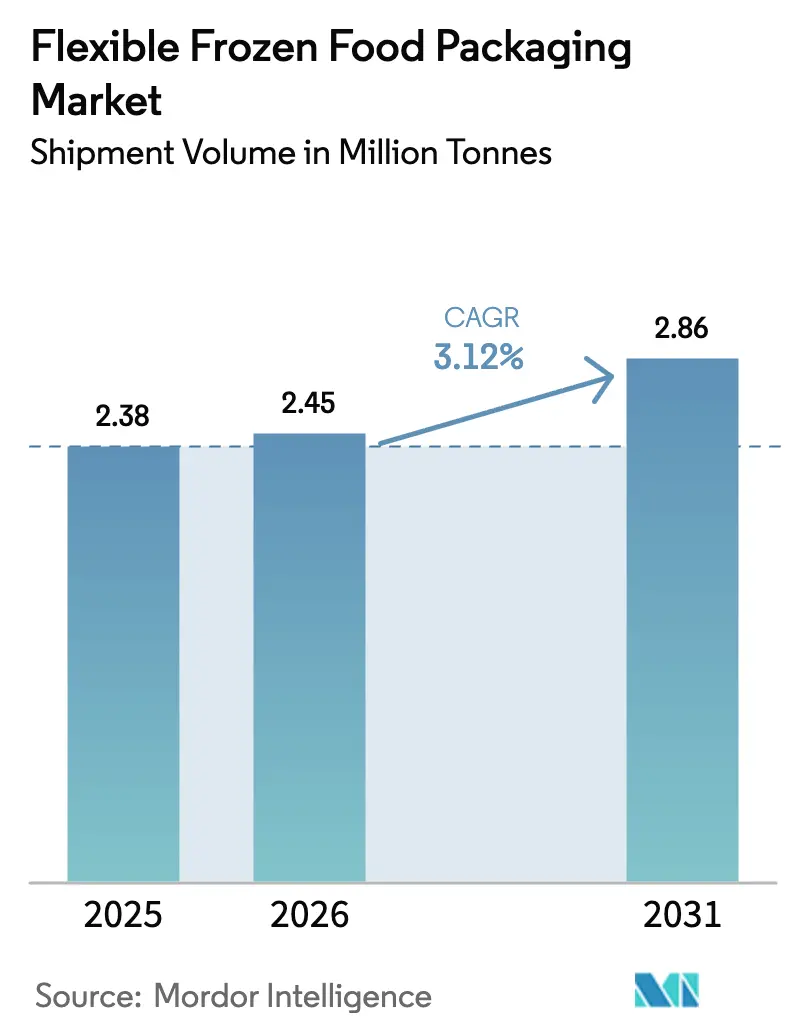

| Market Volume (2026) | 2.45 Million tonnes |

| Market Volume (2031) | 2.86 Million tonnes |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

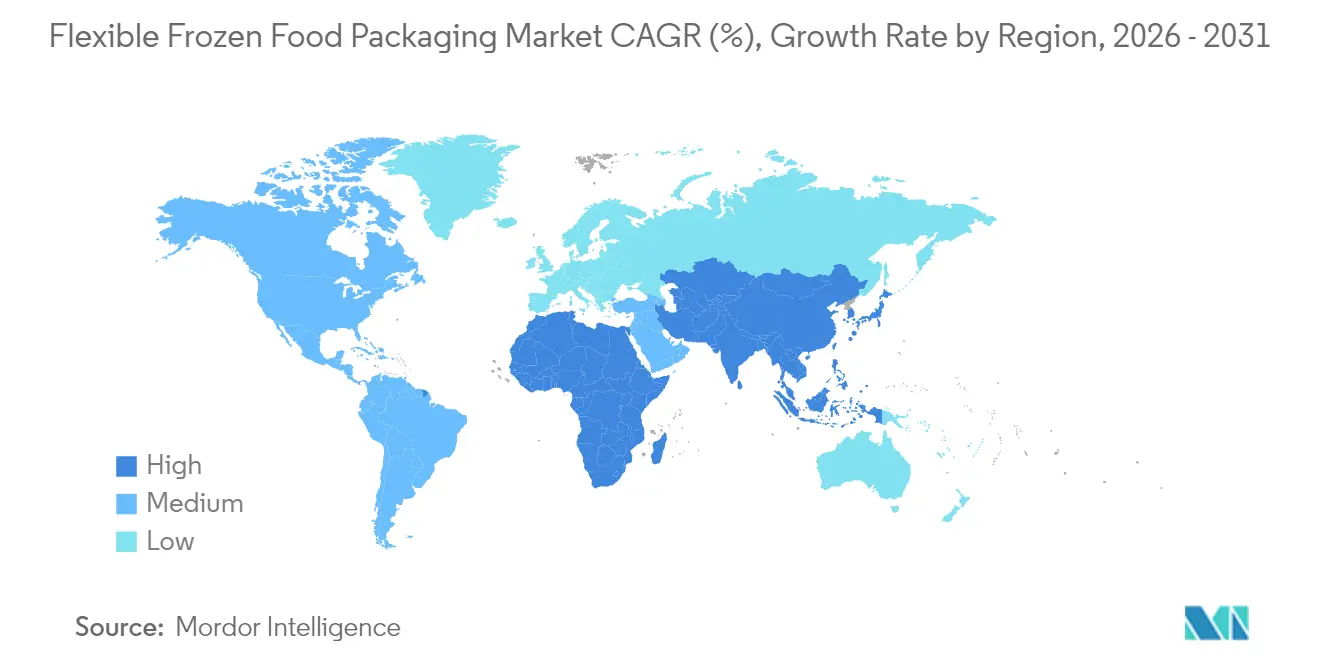

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

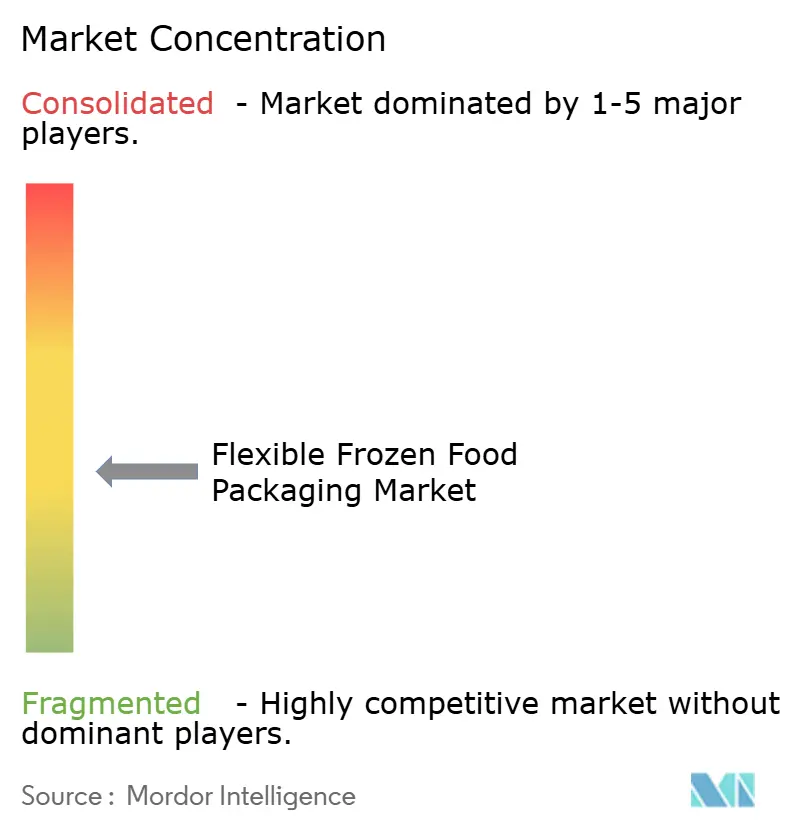

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Frozen Food Packaging Market Analysis by Mordor Intelligence

The flexible frozen food packaging market size was valued at 2.38 million tonnes in 2025 and estimated to grow from 2.45 million tonnes in 2026 to reach 2.86 million tonnes by 2031, at a CAGR of 3.12% during the forecast period (2026-2031). This pace confirms a mature market that still commands premium pricing because frozen formats demand high-barrier films, temperature resilience to –30 °C, and proven food-contact safety despite resin cost swings. Growth is rooted in quick-commerce expansion, evolving cold-chain infrastructure, and retailer pressure to free up freezer space for fresh SKUs. Consolidation among global converters amplifies technical capabilities while shrinking the pool of purely volume-based suppliers. Regulatory headwinds such as the EU plastics tax are simultaneously pruning non-compliant formats and steering investments into mono-material solutions that simplify post-consumer recycling.

Key Report Takeaways

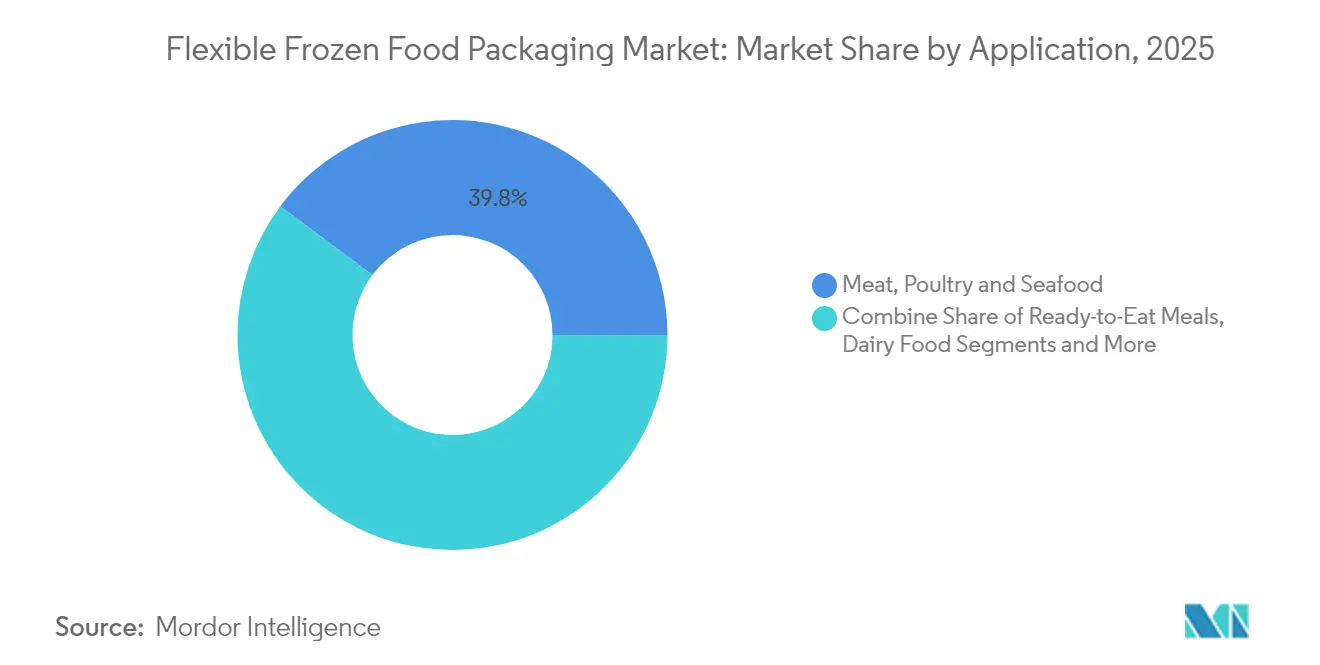

- By application, meat, poultry, and seafood commanded 39.78% of flexible frozen food packaging market share in 2025, while ready-to-eat meals are projected to outpace all other applications at a 6.48% CAGR to 2031.

- By packaging type, bags and pouches led with 34.98% revenue share in 2025; films and wraps are forecast to expand at a robust 6.92% CAGR through 2031.

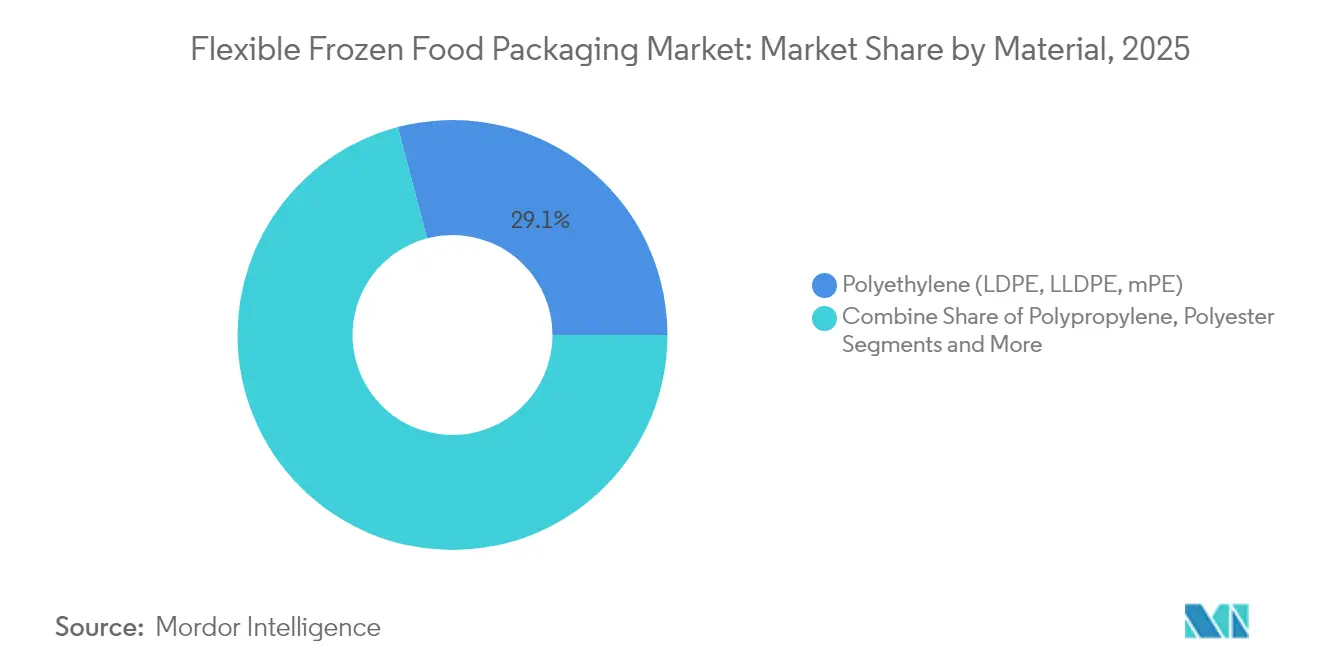

- By material, polyethylene retained 29.10% of the flexible frozen food packaging market size in 2025, whereas polypropylene is poised to grow 5.52% annually through 2031.

- By technology, modified atmosphere packaging held a 28.65% share in 2025, but microwave-steam vent pouches are advancing at a 6.27% CAGR across the forecast horizon.

- By region, North America led with 34.35% of 2025 volumes; Asia-Pacific is set to record the fastest 6.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flexible Frozen Food Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retail Freezer-Door Real-Estate Premiums Fuel Adoption of Slim Stand-Up Pouches in North America | +0.8% | North America, spill-over to EU | Medium term (2-4 years) |

| Rapid Expansion of Quick-Commerce Cold-Chain Networks Across ASEAN Elevates Demand for Lightweight Flexible Packs | +0.9% | ASEAN core, expansion to broader Asia-Pacific | Short term (≤ 2 years) |

| EU "Fit for 55" Plastics Tax Incentivising Shift toward Mono-Material PE/PP Frozen Food Films | +0.6% | EU primary, regulatory influence globally | Long term (≥ 4 years) |

| Nordic Consumers' Preference for Resealable Family-Size Frozen Veg Packs Spurs Zipper-Pouch Uptake | +0.4% | Nordic countries, Western Europe adoption | Medium term (2-4 years) |

| Rise of High-Protein Frozen Seafood Snacks in Japan Driving High-Barrier Retort Pouches | +0.5% | Japan primary, Asia-Pacific secondary | Short term (≤ 2 years) |

| OEM Integration of Laser-Scored Easy-Peel Lidding in Mexican Frozen Entrée Lines Accelerates Flexible Formats | +0.3% | Mexico, North America manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Retail freezer-door real-estate premiums fuel adoption of slim stand-up pouches in North America

Supermarket operators charge USD 15-25 per linear foot annually for prime frozen shelf placement, so brands migrate from rigid tubs to slim pouches that present 40% more facings per foot at –18 °C. Retailers shrinking freezer aisles to make room for fresh grab-and-go items intensify the shift. Conagra Brands linked a 122% jump in kids-meal volumes to the format transition, while logistic teams note 15-20% freight savings from higher case-pack density.

Rapid expansion of quick-commerce cold-chain networks across ASEAN elevates demand for lightweight flexible packs

Southeast Asia invests more than USD 2 billion a year in cold-chain assets that serve 15-minute grocery delivery models. Flexible packs weigh 60-70% less than rigid rivals, lowering last-mile costs and enabling riders on two-wheelers to carry larger SKU assortments. Indonesia’s packaged-food outlay is forecast to reach USD 66.7 billion by 2028, reinforcing volume upside for flexible packs. [1]Food Export, “Indonesia Market Assessment 2024,” foodexport.org

EU “Fit for 55” plastics tax incentivising shift toward mono-material PE/PP frozen food films

A EUR 800 per-tonne levy on unrecycled plastic triggers migration to mono-material designs that hit 95% recyclability versus 25% for legacy laminates. Klöckner Pentaplast’s PE films with 30% recycled content run at 120 packs per minute, proving scale economics for compliant structures. [2]Klöckner Pentaplast, “kp Launches Best-in-Class Duo of Recyclable, Barrier Flow Wrap Films,” kpfilms.com

Nordic consumers’ preference for resealable family-size frozen veg packs spurs zipper-pouch uptake

Households average 2.3 people in Scandinavia yet buy larger frozen packs to reduce store trips. Resealable zippers cut food waste and align with 79% of regional shoppers who demand recyclable solutions, accelerating a 35% yearly rise in zipper-pouch demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inter-polymer Layer Delamination Failures Below –25 °C in Certain Bi-Based Laminates | -0.7% | Global, severe in extreme cold regions | Short term (≤ 2 years) |

| Fragmented Curb-side Recycling Streams Limiting Recovery of Metallised PE Films in EU | -0.5% | EU primary, North America secondary | Long term (≥ 4 years) |

| Volatile EVA and Metallocene PE Resin Pricing Compressing Converter Margins | -0.8% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| Stringent GCC Halal-Compliance Labelling Rules Raising Rework Rates for Printed Pouches | -0.3% | GCC countries, Muslim-majority markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inter-polymer layer delamination failures below –25 °C in certain bio-based laminates

Polyurethane adhesive hydrolysis accelerates under deep-freeze cycling, causing cohesive bond failure in EVA-based structures and compromising barrier performance. Tie-layers thinner than 2 µm show premature fracture, forcing costly reformulations.

Fragmented curb-side recycling streams limiting recovery of metallised PE films in EU

Current sortation lines misclassify aluminum-coated films, pushing contamination rates beyond 15% and eroding bale values. Divergent national collection schemes further reduce scale for mechanical or chemical upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Protein products sustain lead while ready-to-eat meals surge

Meat, poultry, and seafood retained 39.78% of 2025 volume, underscoring the flexible frozen food packaging market reliance on high-protein staples that require oxygen-scavenging and anti-fog films for color stability. Lipid oxidation prevention is critical; vacuum skin and MAP systems together limit freezer burn, extending shelf life up to 18 months. The ready-to-eat meals niche is forecast to grow 6.48% annually as single-person urban households seek heat-and-eat convenience compatible with air fryers and microwaves. Many suppliers design dual-ovenable pouches that withstand 220 °C flash heating. Ichimasa’s 1.5-year frozen fish range illustrates technical advances in barrier control without artificial preservatives.

A wider assortment of frozen yogurt bites, smoothie cubes, and vegetable blends adds incremental tonnage, but baked goods have plateaued due to fresh bakery availability. Still, artisan premium desserts anchor a loyal buyer base, preserving niche opportunities. Across these applications, the flexible frozen food packaging market size for meat and seafood alone is projected to reach 1.12 million tonnes by 2031, enlarging its gap over other segments.

By Packaging Type: Films climb while pouches defend mass appeal

Bags and pouches generated 34.98% of 2025 sales, yet thin-gauge films and wraps are growing faster at 6.92% CAGR as retailers push for shelf-efficient block formats that stack. Amcor’s monomaterial pouch reduces carbon emissions 79% and water use 84%, aligning with scope-3 reporting needs. Flow-wrap films shave 75% weight versus clamshells, aiding e-grocery parcel economics. Lidding films with laser score lines add consumer convenience and bolster fridge-to-microwave usability. The flexible frozen food packaging market share for films is on track to overtake pouches by 2030 in North America as private labels migrate to recycle-ready flow wraps.

By Material: Polypropylene accelerates in mono-material transition

Polyethylene still accounted for 29.10% of 2025 volumes, but polypropylene’s 5.52% CAGR mirrors legislative pressure to deliver single-polymer packs that navigate curb-side recycling. PP is 30% lighter than PET, lowering freight weight while handling –30 °C service with minimal brittleness. Walki’s paper-poly hybrids offer freezer-grade stiffness and grease resistance, though uptake hinges on line adaptations. Bio-based PLA and PHA films command cost premiums but help brands avoid PFAS restrictions arriving in 2030. The flexible frozen food packaging market size attributed to polypropylene should surpass 845 000 tonnes by 2031 as converters down-spec multilayer PE or PET laminates.

By Technology: Convenience features spur microwave-friendly pouches

Modified atmosphere packaging retained a 28.65% position through proven shelf-life gains in protein and bakery sectors. Yet microwave-steam vent formats are scaling 6.27% annually because they deliver fresh-like textures in three minutes, keeping sauces from boiling over thanks to controlled pressure release. Kraft Heinz’s 360CRISP liner demonstrates crispiness from a frozen state using bespoke film geometry. Vacuum skin packs secure premium salmon filets and steak cuts, protecting surface integrity and reducing purge. Retort pouches now come in recycle-ready PE/barrier PE structures that withstand 121 °C cook-in-pack sterilisation before deep-freeze distribution.

Geography Analysis

North America captured 34.35% of 2025 shipments, supported by supermarket chains limiting freezer facings and thereby rewarding slim pouch adopters. The United States embraces premium claims around resealability and transparency windows, while Mexico’s laser-scored peelable lids for entrées illustrate near-shore innovation that feeds continental private labels. Tariff volatility for Canadian PE and PP imports remains a cost wildcard, yet extensive rail and intermodal infrastructures maintain efficient resin flow.

Asia-Pacific is the fastest-climbing region at 6.46% CAGR through 2031, spearheaded by ASEAN’s USD 2 billion yearly cold-chain build-out. Jakarta, Manila, and Bangkok now host micro-fulfilment hubs for 15-minute grocery, lifting demand for lightweight single-serve pouches. Japan’s high-protein seafood snacks need retortable high-barrier packs, while China’s excess PE output compresses resin spreads, benefiting converters but challenging upstream producers.

Europe holds a strong presence despite disparate curb-side recycling infrastructure. The EU Packaging and Packaging Waste Regulation sets a 30% recycled-content target by 2030, pushing brands to adopt mono-material films in advance of punitive fees. Nordic zipper-pouch uptake illustrates regional leadership on food-waste reduction. Southern European retailers lean on lidding-film reclose features to offset smaller freezer aisles. Eastern Europe’s growth is tempered by geopolitical friction, though Poland and the Baltics see niche opportunities in private-label exports to Germany and France.

Competitive Landscape

The flexible frozen food packaging market is moderately fragmented. Amcor’s USD 8.43 billion takeover of Berry Global forms the largest flexible converter, pooling USD 180 million in yearly R&D and more than 1,500 scientists to speed recyclable-film launches. Huhtamaki’s EUR 100 million cost-cut programme supports rollout of blueloop recycle-ready platforms, signalling an operational pivot toward margin protection in the face of resin volatility. ProAmpac, UFlex, and Constantia Flexibles invest in barrier-grade PE and PP, vying for private-label opportunities that hinge on sustainability claims.

Technology differentiation drives positioning. Suppliers with proprietary easy-open laser scoring, integrated zipper lines, and recycle-ready high-barrier chemistries win RFPs from multinational food brands. Mid-tier converters focus on region-specific strengths such as halal labelling expertise or high-graphic gravure for Japanese seafood SKUs. M&A appetite stays high as converters seek scale to absorb compliance spending on Lifecycle Assessment tools and PCR content certification.

Flexible Frozen Food Packaging Industry Leaders

Amcor Plc

Sealed Air Corporation

Mondi Group

Huhtamaki Oyj

ProAmpac Intermediate Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Daybreak positioned 2025 as the “Year of Frozen Sushi” by launching Art Lock Freezer technology.

- June 2025: Amcor closed its all-stock acquisition of Berry Global.

- February 2025: European Commission finalised rules mandating all packaging be recyclable by 2030 with 30% recycled content for plastics.

- January 2025: UFlex announced USD 200 million for PET chips and aseptic packs in Egypt to supply Middle East and Europe.

Global Flexible Frozen Food Packaging Market Report Scope

Flexible frozen food packaging encompasses lightweight and adaptable solutions, including bags, pouches, films, and wraps, specifically crafted to store, protect, and preserve frozen foods. These packaging materials are typically made from plastic, paper, and foil. The study monitors key market parameters, identifies growth influencers, and highlights major industry vendors, all of which bolster market estimations and projected growth rates. Additionally, the study evaluates how geopolitical developments influence the market, considering prevailing scenarios, key themes, and demand cycles related to applications.

The flexible frozen food packaging market is segmented by application (dairy food, ready-to-eat-meals, meat, poultry and seafood, fruits and vegetables, baked food, and other applications), type of packaging (bags and pouches, films and wraps, and other types of packaging), and geography (North America (United States and Canada), Europe (United Kingdom, Germany, France, Italy, and Rest of Europe), Asia Pacific (China, Japan, India, and Rest of Asia Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa and Rest of Middle East and Africa)). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Dairy Food |

| Ready-to-Eat Meals |

| Meat, Poultry and Seafood |

| Fruits and Vegetables |

| Baked Food |

| Other Applications |

| Bags and Pouches |

| Films and Wraps |

| Lidding Films and Top Web |

| Other Packaging Type |

| Polyethylene (LDPE, LLDPE, mPE) |

| Polypropylene (CPP, BOPP) |

| Polyester (BOPET) |

| Paper and Paperboard |

| Bio-based and Compostable Films (PLA, PBS, PHA) |

| Vacuum Skin Packaging (VSP) |

| Modified Atmosphere Packaging (MAP) |

| Retort and Aseptic Pouching |

| Microwave-Steam Vent Pouches |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Application | Dairy Food | ||

| Ready-to-Eat Meals | |||

| Meat, Poultry and Seafood | |||

| Fruits and Vegetables | |||

| Baked Food | |||

| Other Applications | |||

| By Packaging Type | Bags and Pouches | ||

| Films and Wraps | |||

| Lidding Films and Top Web | |||

| Other Packaging Type | |||

| By Material | Polyethylene (LDPE, LLDPE, mPE) | ||

| Polypropylene (CPP, BOPP) | |||

| Polyester (BOPET) | |||

| Paper and Paperboard | |||

| Bio-based and Compostable Films (PLA, PBS, PHA) | |||

| By Technology | Vacuum Skin Packaging (VSP) | ||

| Modified Atmosphere Packaging (MAP) | |||

| Retort and Aseptic Pouching | |||

| Microwave-Steam Vent Pouches | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the flexible frozen food packaging market?

The flexible frozen food packaging market reached 2.45 million tonnes in 2026 and is projected to hit 2.86 million tonnes by 2031.

Which region is forecast to grow the fastest through 2031?

Asia-Pacific is projected to expand at a 6.46% CAGR thanks to rapid cold-chain investments and quick-commerce adoption.

Why are mono-material films gaining traction in frozen applications?

EU plastics taxes and global retailer demands for recycle-ready solutions are pushing converters to shift from multilayer laminates to mono-material PE or PP films that achieve recyclability rates above 90%.

Which application segment offers the highest growth opportunity?

Ready-to-eat meals are expected to expand at a 6.48% CAGR as single-serve convenience and air-fryer preparation formats multiply.

How will resin price volatility influence the market?

Price swings in EVA and metallocene PE compress converter margins, encouraging down-gauging, material substitution, and strategic procurement contracts to protect profitability.

Page last updated on: