Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.20 Billion |

| Market Size (2031) | USD 1.61 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

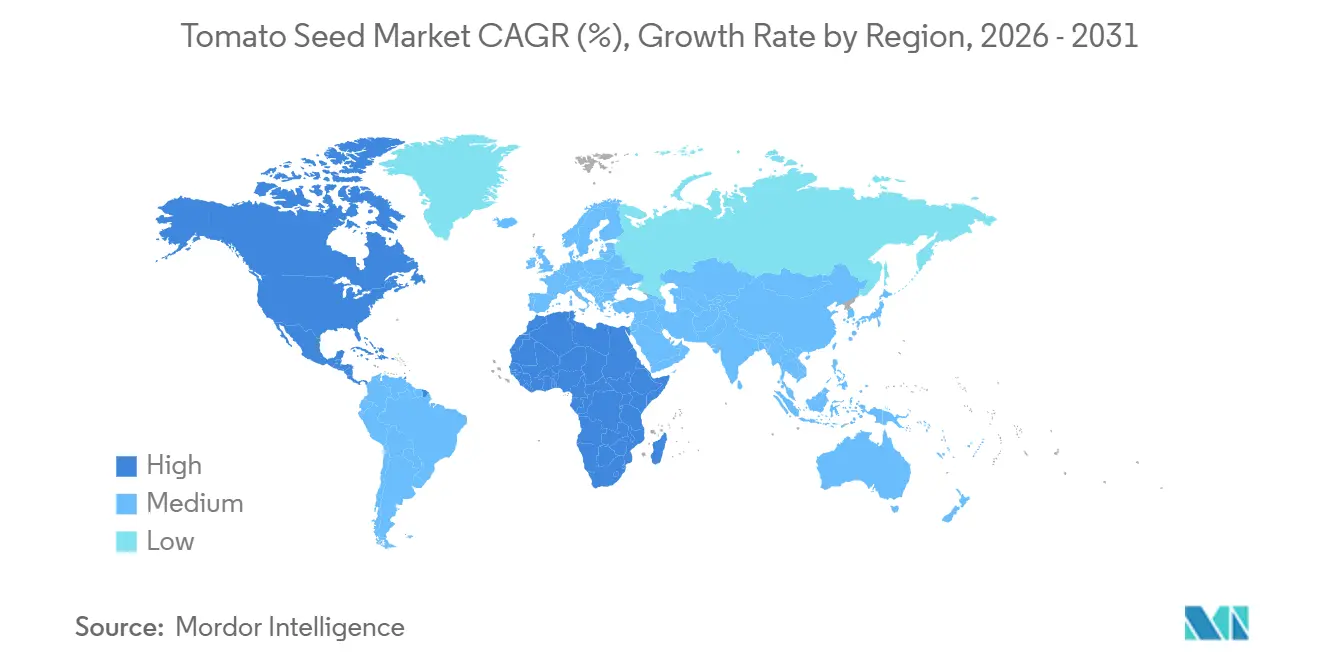

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

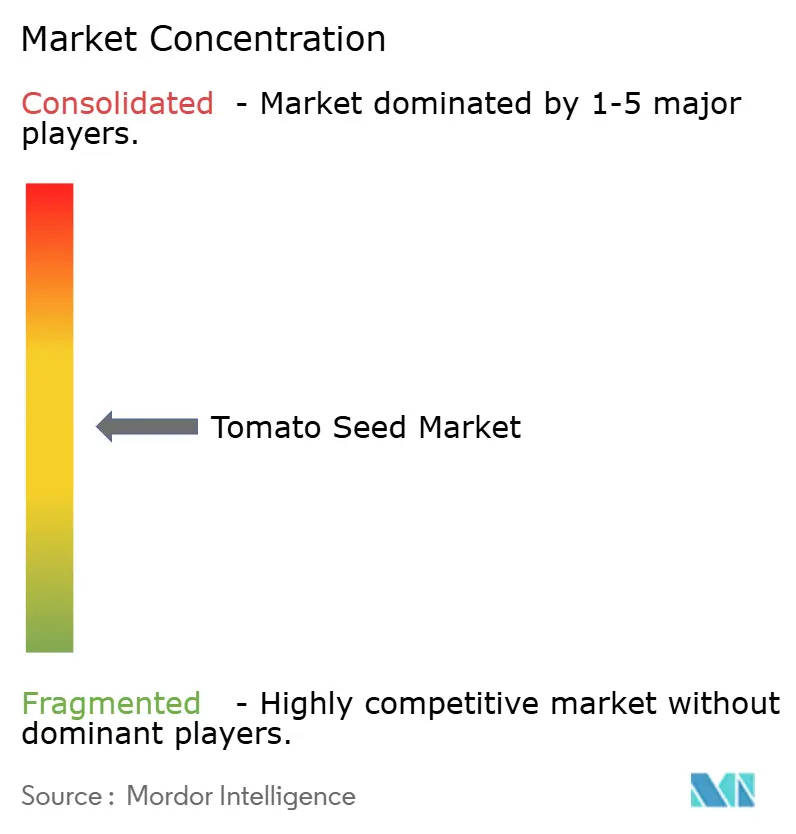

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tomato Seed Market Analysis by Mordor Intelligence

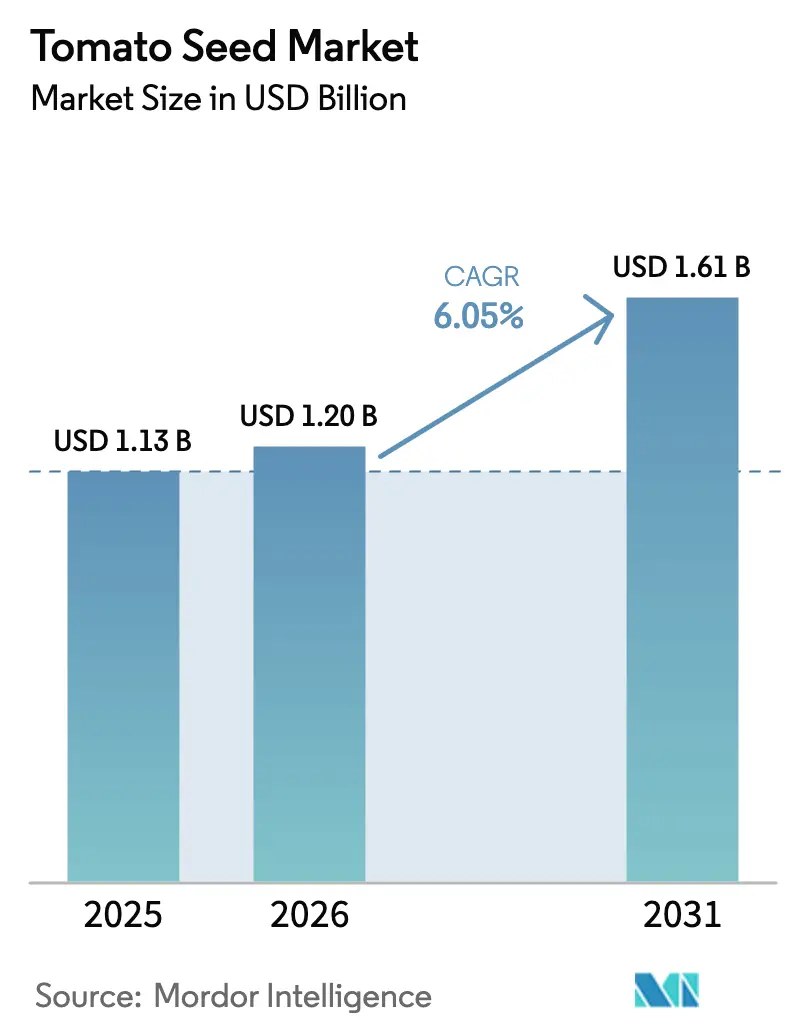

The Tomato Seed Market size is projected to be USD 1.13 billion in 2025, USD 1.20 billion in 2026, and reach USD 1.61 billion by 2031, growing at a CAGR of 6.05% from 2026 to 2031. Performance hinges on breeding innovation that keeps pace with rapidly scaling protected-cultivation acreage, rising industrial demand for high-soluble-solids cultivars, and the steady release of disease-resistant hybrids. Multinational breeders maintain double-digit research spending to protect margins, yet royalty inflation and smallholder seed-saving practices weigh on revenue capture. Controlled-environment agriculture projects in Canada and the United States signal a geographic shift in premium-seed demand, while China’s fast-growing processing segment underlines the link between industrial output and hybrid uptake. Regulatory divergence on gene-edited traits introduces both launch windows and market delays, shaping pipeline prioritization across regions.

Key Report Takeaways

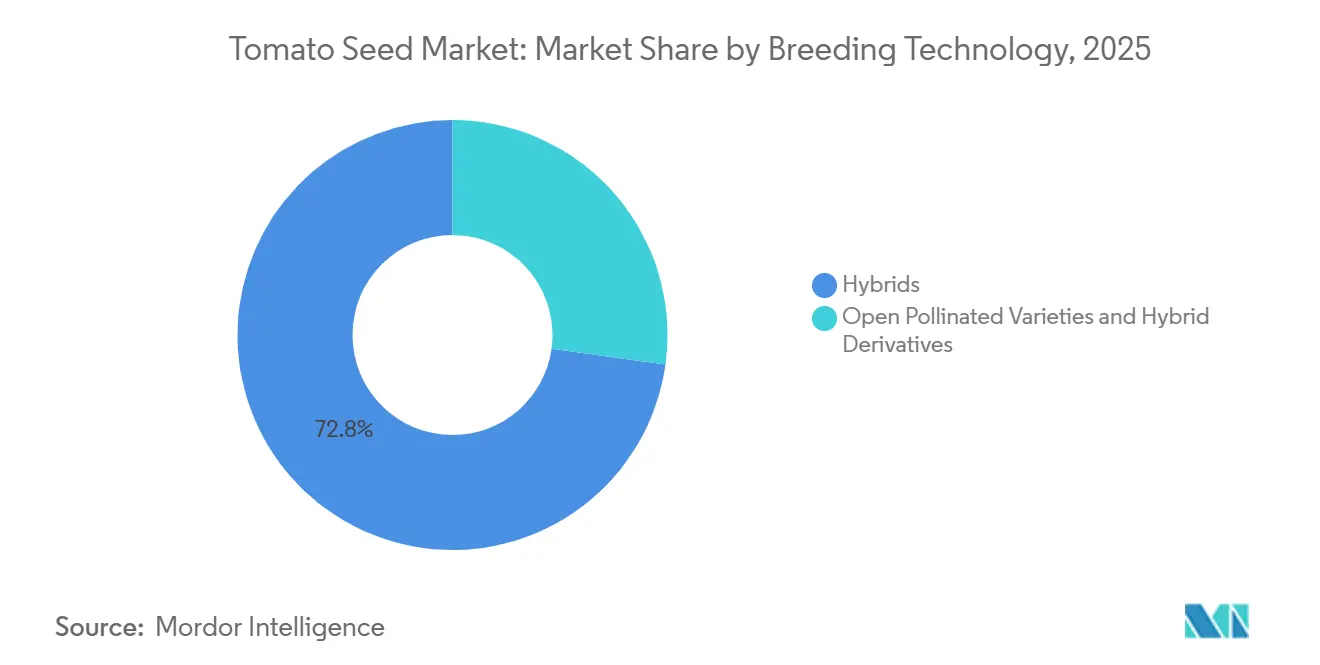

- By breeding technology, hybrids led with 72.8% of the tomato seed market share in 2025, and are projected to grow at a 6.1% CAGR through 2031.

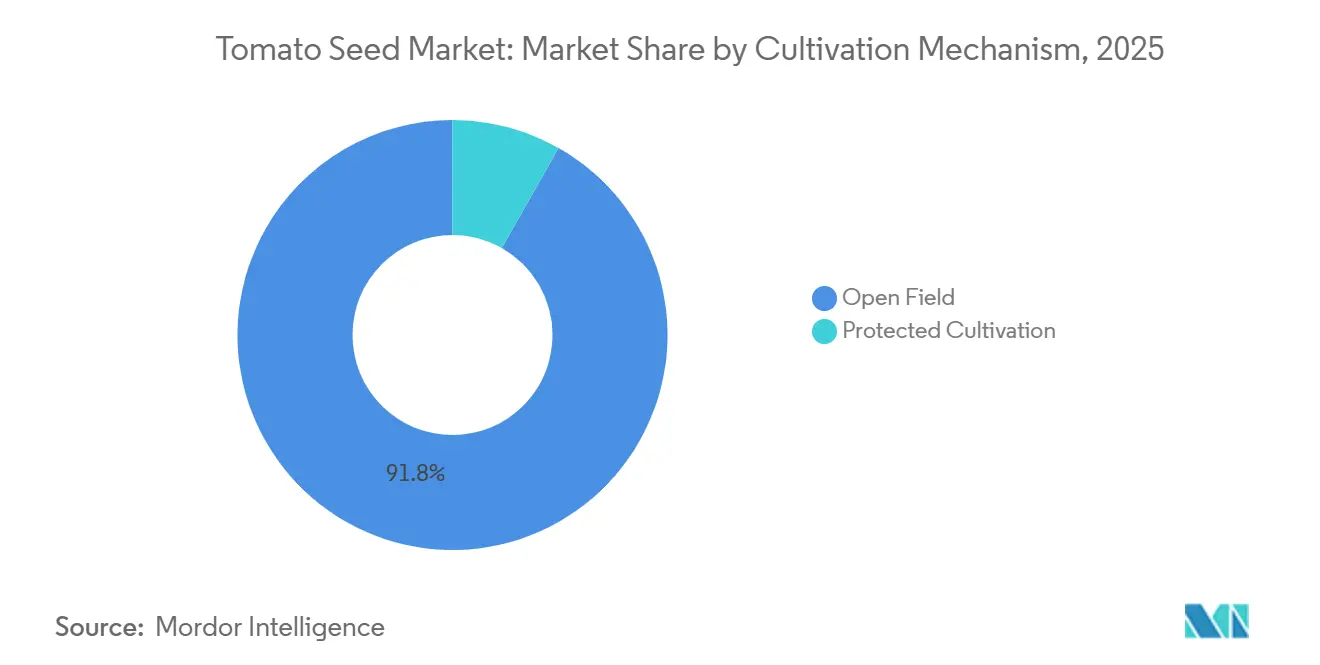

- By cultivation mechanism, open-field production held 91.8% of the tomato seed market size in 2025, while protected cultivation advanced at the fastest 8.5% CAGR through 2031.

- By geography, Asia-Pacific captured 36.4% revenue share in 2025, and North America registered the highest regional CAGR of 7.6% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tomato Seed Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high-yield hybrid cultivars | +1.2% | Asia-Pacific and North America | Medium term (2-4 years) |

| Expansion of protected cultivation acreage | +1.5% | North America, Middle East, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Increasing adoption of disease-resistant traits | +1.0% | Europe, North America, and Asia-Pacific | Short term (≤ 2 years) |

| Rapid growth of processed-tomato industries | +0.9% | Asia-Pacific, North America, and South America | Medium term (2-4 years) |

| CRISPR-enabled trait stacking for taste and shelf-life | +0.7% | Asia-Pacific, North America, selected European Union markets | Long term (≥ 4 years) |

| Surge in seed-bank led climate-resilient genotype collaborations | +0.5% | Africa, Asia-Pacific, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Yield Hybrid Cultivars

Growers continue shifting toward hybrids that deliver 15–25% higher yields than open-pollinated lines, justifying the higher costs of tomato seeds, which are three to five times greater. China harvested 70.21 million metric tons of tomatoes in 2024 with hybrid penetration above 85% in greenhouse and processing operations, while India’s main tomato states posted adoption rates near 70%[1]Source: Food and Agriculture Organization of the United Nations, “FAOSTAT,” FAO.org. Egypt’s 2024 varietal list featured 269 private hybrids against only five public open-pollinated lines, underscoring near-total hybrid dominance in irrigated systems. Processing contracts that demand uniform soluble-solids content and size uniformity reinforce this trend, driving sustained tomato hybrid-seed revenue growth.

Expansion of Protected Cultivation Acreage

Protected cultivation is growing 8.52% annually through 2031, faster than open-field systems, and reshapes trait demand toward parthenocarpy and compact architecture. Saudi Arabia achieved 76% tomato self-sufficiency in 2025 from 23,000 dunums of greenhouse area[2]Source: Saudi Arabia Ministry of Environment, Water and Agriculture, “Agricultural Statistics,” Mewa.gov.sa. In Canada, Ontario Plants Propagation opened a USD 75 million greenhouse in 2024 that supplies climate-controlled seedlings to regional growers. High yields of 60–70 kilograms per square meter recorded in the Netherlands set benchmarks now pursued across Gulf Cooperation Council markets.

Increasing Adoption of Disease-Resistant Traits

Tomato brown rugose fruit virus (ToBRFV) remains the leading breeding target, with five resistant hybrids released by Rijk Zwaan BV between 2024 and early 2025[3]Source: Rijk Zwaan, “Seed Connect Centre,” Rijkzwaan.com. Public programs also play a significant role in advancing agricultural research. For instance, East-West Seed's July 2024 launch of Harmony F1 in Kenya targeted bacterial wilt and early blight, the two most economically damaging pathogens in East African smallholder systems, where fungicide access is limited, and crop rotation is constrained by land scarcity. Additionally, marker-assisted selection has significantly reduced the traditional breeding cycle by half, enabling faster and more efficient deployment of multigenic resistance packages, which are crucial for addressing evolving agricultural challenges.

Rapid Growth of Processed-Tomato Industries

Global processed tomato production reached 45.7 million metric tons in 2024, supported by a 30% year-on-year increase in China’s output, which totaled 10.45 million metric tons. Brazil contributed 1.65 million metric tons, while Argentina produced 631,000 metric tons, establishing South America as a counter-seasonal supplier. Fluctuations in California's acreage have increased the demand for hybrids resistant to water stress, while the need for high soluble solids content ensures specific hybrid requirements for factory supply chains.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of saved-seed practices among smallholders | -0.8% | Africa, Asia-Pacific, and South America | Medium term (2-4 years) |

| Stringent biotech variety approval timelines | -0.6% | European Union, selected Asia-Pacific and South American markets | Long term (≥ 4 years) |

| Consolidation-driven royalty inflation in seed pricing | -0.5% | North America and Europe | Short term (≤ 2 years) |

| Rising consumer pushback against patent-protected traits in heirloom markets | -0.4% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Saved-Seed Practices Among Smallholders

On-farm tomato seed saving accounted for 33% of planting needs in Vermont in 2024 and remains more prevalent in sub-Saharan Africa and South Asia due to limited distribution networks. In these regions, the lack of access to formal tomato seed systems compels farmers to rely heavily on saved seeds, which are often less expensive but may yield lower results. In Kenya, growers returned to using saved seed after a January 2026 price slump, leading to a decline in hybrid seed adoption despite its demonstrated yield advantages. This shift highlights the economic pressures farmers face, particularly in developing regions. Informal seed multiplication undermines royalties, driving up tomato hybrid seed prices and creating a cycle that further discourages marginal farmers from purchasing. This feedback loop exacerbates the challenges of promoting hybrid tomato seed adoption among resource-constrained growers.

Stringent Biotech Variety Approval Timelines

The European Union's comprehensive assessment process takes over two years, whereas Japan's notification approach is completed within months. These extended timelines deter investment in region-specific traits, force breeders to postpone European releases, disrupt global pipelines, and increase per-variety costs by up to 40%. The lengthy approval process in the European Union also creates uncertainty for stakeholders, discouraging innovation and reducing the region's competitiveness in the global market. This delay impacts the timely introduction of new varieties, which could otherwise address evolving consumer demands and environmental challenges more effectively.

Segment Analysis

By Breeding Technology: Hybrid Dominance Anchors Revenue Growth

Hybrids captured 72.8% of the tomato seed market in 2025, and this share is projected to widen as the hybrid tomato seed market size grows at a 6.1% CAGR through 2031. Processing companies mandate mechanized-harvest compatibility and stacked disease resistance that open-pollinated lines cannot match. Rijk Zwaan BV invested heavily in genomic selection at its Seed Connect Centre in 2025, illustrating the capital barrier that shields hybrid market share.

Open-pollinated varieties retain relevance in heirloom and low-input systems. The tomato seed market share for these varieties remains slow growth due to yield gaps and seed-saving practices. Public releases such as Mannon’s Majesty show that targeted funding can deliver competitive disease packages, though resource scarcity limits their frequency. West Virginia University's Mannon's Majesty, an open-pollinated cultivar released in 2023 with late-blight, Septoria leaf spot, Fusarium, and Verticillium resistance, demonstrates that public breeding can deliver multi-trait packages competitive with private hybrids, yet the scarcity of such releases only 5 public cultivars among Egypt's 274 registered varieties, underscores the resource constraints facing public programs.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Cultivation Mechanism: Protected Systems Redefine Trait Priorities

By cultivation mechanism, open-field production accounted for 91.8% of the tomato seed market size in 2025, driving the growth of the market for greenhouse-specific hybrids. High-tech facilities in Saudi Arabia and controlled-environment projects in Canada indicate increasing demand for seeds with traits such as parthenocarpy and compact growth habits. The Netherlands' greenhouse yields, reaching 60-70 kilograms per square meter annually through hydroponic systems, LED supplemental lighting, and CO₂ enrichment, are now being pursued in GCC markets, where controlled environments are more cost-effective compared to open-field irrigation due to favorable energy costs.

Protected cultivation advanced at the fastest 8.5% CAGR through 2031. Open-field demand remains tied to processing corridors in China, California, and Italy. Drought-driven acreage swings in California increase interest in deficit-irrigation-tolerant genetics, while China’s 100,000 hectares of processing plantings channel volume toward paste-specific cultivars. The regulatory landscape is also diverging, and protected-cultivation systems in the European Union face stringent pesticide-residue limits and integrated-pest-management mandates that favor biological control and disease-resistant varieties, whereas open-field systems in China and South America operate under less restrictive frameworks that permit broader fungicide and insecticide use, a gap that is shaping regional breeding priorities.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific accounted for 36.4% of the tomato seed market in 2025, led by China’s production and near-total reliance on hybrids in protected and processing sectors. India, Bangladesh, and Pakistan exhibit lower hybrid uptake due to saved-seed traditions, keeping growth moderate. Japan's 2024 approval of Sanatech Seed's CRISPR-derived Sicilian Rouge High GABA tomato, the first gene-edited fresh-market tomato cleared for retail sale, signals the region's regulatory openness to novel breeding technologies, a stance that contrasts sharply with the European Union's two-year approval timelines and is channeling trait-development investment toward Asia-Pacific launches.

North America posts the fastest forecast growth at a 7.6% CAGR during the forecast period (2026-2031). Controlled-environment investments, such as Ontario Plants Propagation’s USD 75 million greenhouse in 2024 and Syngenta’s USD 15 million Pasco upgrade, tighten local supply chains and increase demand for premium tomato seed in August 2024. United States organic transition funding adds ancillary momentum, even as acreage volatility persists. East-West Seed's July 2024 launch of Harmony F1 in Kenya, targeting bacterial wilt and early blight, illustrates the extension of Asian breeding platforms into African markets, leveraging heat-tolerant germplasm developed for Southeast Asian conditions.

Europe focuses on disease management, adopting ToBRFV-resistant hybrids after outbreaks cut greenhouse yields in the European Union by up to 50%. The Middle East utilizes hydroponic systems to achieve self-sufficiency objectives, whereas Africa presents a contrasting scenario. Egypt depends heavily on imported hybrid seeds, while many sub-Saharan farmers continue to use saved seeds. In South America, processing capabilities enable the region to serve as a counter-seasonal exporter, driven by demand for long-shelf-life hybrids.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The tomato seed market is moderately concentrated, with Bayer AG, Syngenta Group, BASF SE, Groupe Limagrain, and Rijk Zwaan BV in 2025. These companies operate vertically integrated pipelines that span germplasm discovery, trait platforms, and regional tomato seed multiplication, delivering cost and speed advantages over smaller rivals. Research spending ranges from 15% to 30% of annual sales, sustaining rapid varietal turnover and creating a high financial barrier to new entrants. Utility patents reinforce this edge by limiting research use and enabling per-hectare royalty fees above USD 50 for stacked-trait hybrids. Independent firms have fallen in 2024, evidence that rising licensing costs are squeezing margins and accelerating market exits.

Strategic realignment continues as leaders reshape portfolios and acquire novel genetics. In early 2022, an Israeli private-equity fund bought TomaTech and Nirit Seeds, consolidating key tomato brown rugose fruit virus resistance lines for European and Middle Eastern greenhouse markets. Rijk Zwaan BV opened its largest Seed Connect Centre in April 2025, pairing genomic selection with automated phenotyping to compress breeding cycles. Syngenta invested USD 15 million in July 2024 to expand greenhouse capacity at Pasco, Washington, aligning tomato seed production with rising controlled-environment acreage in North America.

White-space opportunities remain in climate-resilient germplasm for sub-Saharan Africa and South Asia, gene-edited cultivars for protected systems, and organic-certified hybrids for premium retail channels. East West Seed seized this space by launching Harmony F1 in Kenya in July 2024, a hybrid tolerant to bacterial wilt and early blight for smallholder systems where multinationals have underinvested. The Open Source Seed Initiative lists 180 pledged tomato varieties that offer royalty-free options for growers who value seed-saving rights and varietal transparency. As biological-control rules tighten in European greenhouses and water deficits persist in California fields, demand grows for niche breeders that can rapidly stack disease resistance and water-use-efficiency traits, keeping the competitive landscape dynamic despite moderate concentration.

Tomato Seed Industry Leaders

Bayer AG

Syngenta Group

BASF SE

Groupe Limagrain

Rijk Zwaan BV

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: NRGene has developed and commercialized tomato varieties resistant to Tomato Brown Rugose Fruit Virus (ToBRFV). These varieties provide growers with an effective solution to protect their crops from the virus, which poses a significant threat to tomato production worldwide.

- July 2025: DENSO acquired Axia Vegetable Seeds, a Netherlands-based company specializing in greenhouse tomato seeds, to broaden its agricultural technology portfolio. This acquisition allows DENSO to advance sustainable tomato cultivation by leveraging artificial intelligence, robotics, and environmental control systems.

- May 2025: Sakata Seed Corporation has established a new research station in Antalya, Türkiye, specializing in tomato and pepper breeding. The facility is dedicated to developing high-performing varieties tailored to various global markets.

Global Tomato Seed Market Report Scope

Tomato seeds are the small, nutrient-rich reproductive embryos found within the fruit's gelatinous core that facilitate the growth of new tomato plants. The Tomato Seed Market Report is Segmented by Breeding Technology (Hybrids and Open Pollinated Varieties and Hybrid Derivatives), Cultivation Mechanism (Open Field and Protected Cultivation), and Geography (Africa, Asia-Pacific, Europe, Middle East, North America, and South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Breeding Technology

| Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives |

Cultivation Mechanism

| Open Field |

| Protected Cultivation |

Geography

| Africa | By Breeding Technology | |

| By Cultivation Mechanism | ||

| By Country | Egypt | |

| Ethiopia | ||

| Ghana | ||

| Kenya | ||

| Nigeria | ||

| South Africa | ||

| Tanzania | ||

| Rest of Africa | ||

| Asia-Pacific | By Breeding Technology | |

| By Cultivation Mechanism | ||

| Australia | ||

| Bangladesh | ||

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Myanmar | ||

| Pakistan | ||

| Philippines | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | By Breeding Technology | |

| By Cultivation Mechanism | ||

| France | ||

| Germany | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Romania | ||

| Russia | ||

| Spain | ||

| Ukraine | ||

| United Kingdom | ||

| Rest of Europe | ||

| Middle East | By Breeding Technology | |

| By Cultivation Mechanism | ||

| Iran | ||

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| North America | By Breeding Technology | |

| By Cultivation Mechanism | ||

| Canada | ||

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | By Breeding Technology | |

| By Cultivation Mechanism | ||

| Argentina | ||

| Brazil | ||

| Rest of South America | ||

| Breeding Technology | Hybrids | ||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| Cultivation Mechanism | Open Field | ||

| Protected Cultivation | |||

| Geography | Africa | By Breeding Technology | |

| By Cultivation Mechanism | |||

| By Country | Egypt | ||

| Ethiopia | |||

| Ghana | |||

| Kenya | |||

| Nigeria | |||

| South Africa | |||

| Tanzania | |||

| Rest of Africa | |||

| Asia-Pacific | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| Australia | |||

| Bangladesh | |||

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Myanmar | |||

| Pakistan | |||

| Philippines | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| Europe | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| France | |||

| Germany | |||

| Italy | |||

| Netherlands | |||

| Poland | |||

| Romania | |||

| Russia | |||

| Spain | |||

| Ukraine | |||

| United Kingdom | |||

| Rest of Europe | |||

| Middle East | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| Iran | |||

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| North America | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| Canada | |||

| Mexico | |||

| United States | |||

| Rest of North America | |||

| South America | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| Argentina | |||

| Brazil | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms

Get More Details On Research Methodology

Download PDF