Market Overview

| Study Period | 2021 - 2031 |

|---|---|

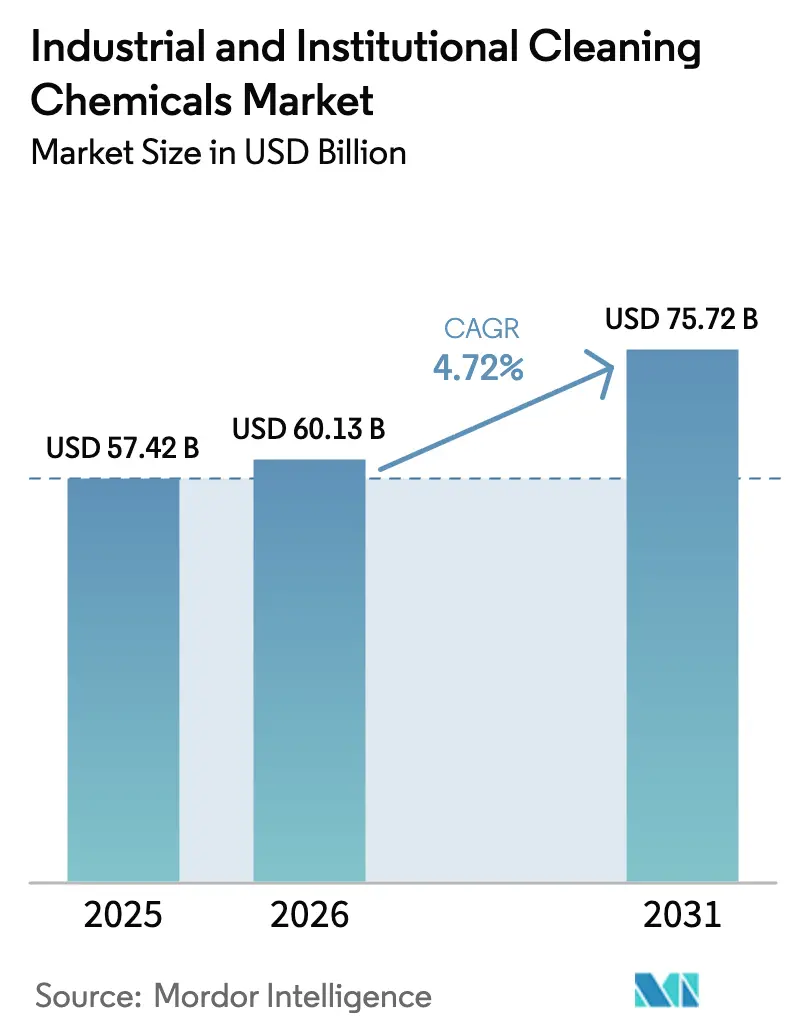

| Market Size (2026) | USD 60.13 Billion |

| Market Size (2031) | USD 75.72 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

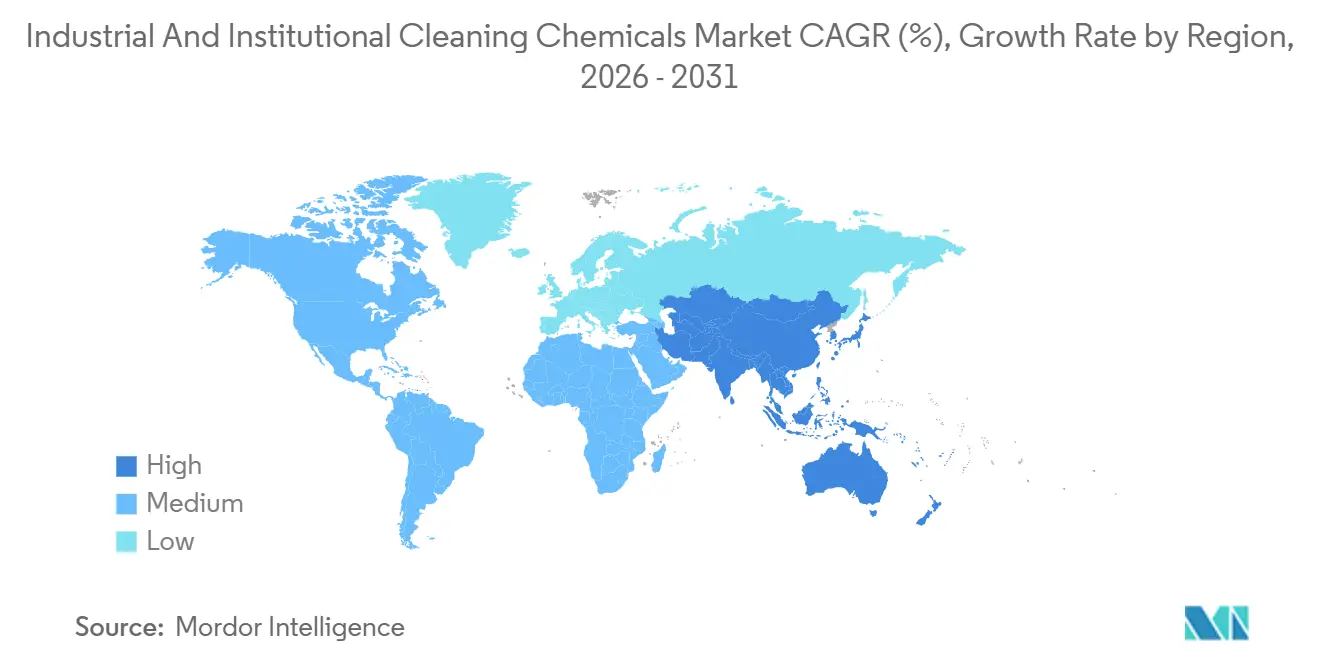

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial And Institutional Cleaning Chemicals Market Analysis by Mordor Intelligence

The Industrial And Institutional Cleaning Chemicals Market size was valued at USD 57.42 billion in 2025 and is estimated to grow from USD 60.13 billion in 2026 to reach USD 75.72 billion by 2031, at a CAGR of 4.72% during the forecast period (2026-2031). Tighter infection-control rules in hospitals and nursing homes, automated dosing in quick-service restaurants, and ultra-pure blends demanded by advanced semiconductor nodes are propelling volume growth. Surfactants still dominate raw-material spend, but precision-cleaning solvents are gaining share as electronics assembly and metal-fabrication customers shift toward low-residue formulations. Bio-based surfactants certified under RSPO Mass Balance protocols are scaling rapidly as European Union Ecolabel and California Safer Consumer Products criteria reshape sourcing decisions. Digital dispensers that record dilution ratios and feed alerts into safety-management systems are cutting chemical waste by up to 20% while easing OSHA Hazard Communication audits. At the same time, PFAS and VOC limits in the United States and the European Union are accelerating reformulation, nudging formulators toward fluorine-free surfactants and aqueous alkaline blends.

Key Report Takeaways

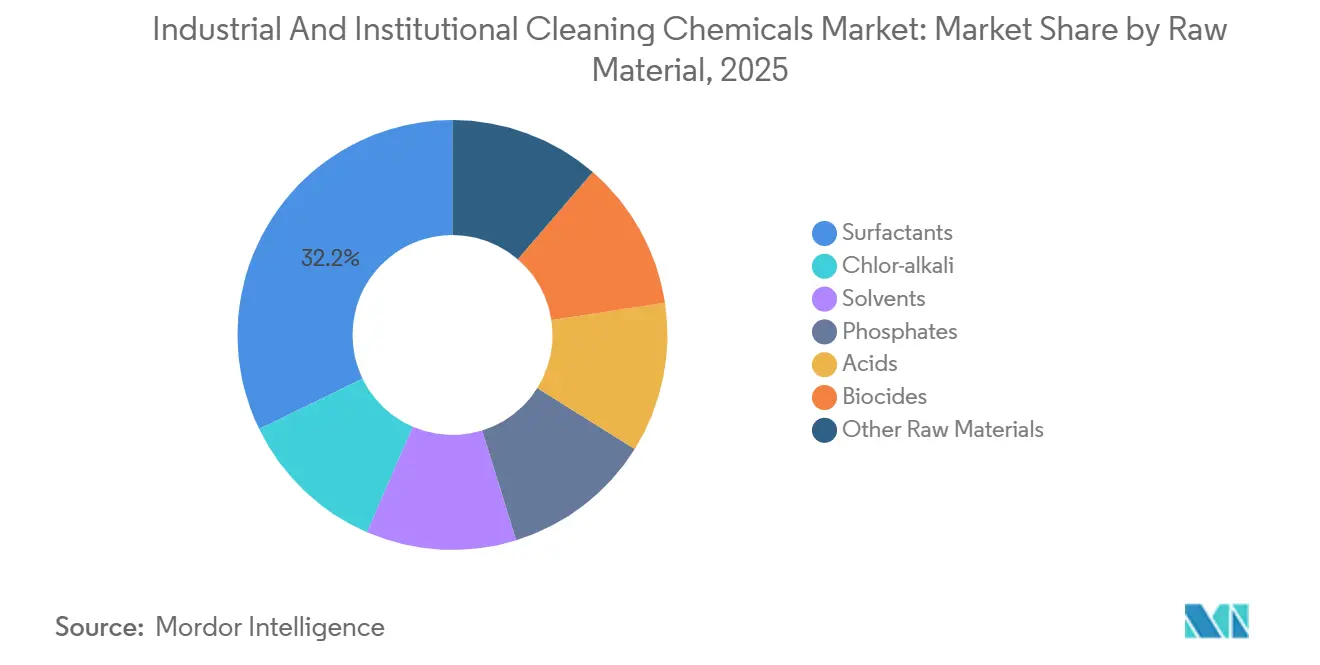

- By raw material, surfactants led with 32.18% of the industrial and institutional cleaning chemicals market share in 2025; solvents are set to expand at a 6.41% CAGR through 2031.

- By product type, general-purpose cleaners commanded 35.65% of the industrial and institutional cleaning chemicals market size in 2025, while disinfectants and sanitizers are growing at a 6.76% CAGR to 2031.

- By ingredient origin, conventional / petrochemical-based products accounted for 70.34% share of the industrial and institutional cleaning chemicals market size in 2025; bio-based / green are forecast to rise at 7.33% CAGR over 2026-2031.

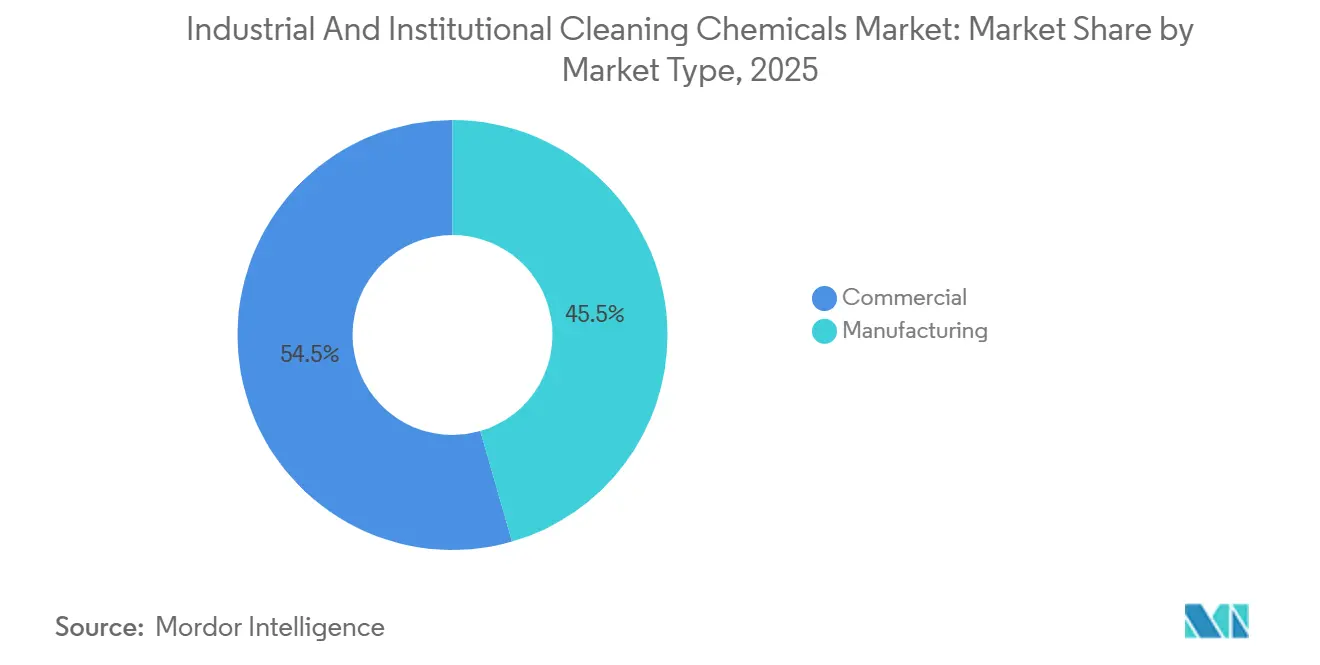

- By market type, the commercial sector held 54.46% revenue share in 2025 and is advancing at a 5.56% CAGR through 2031.

- By geography, North America maintained a 34.49% share in 2025, whereas the Asia-Pacific is projected to grow at a 6.98% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial And Institutional Cleaning Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infection-Control Protocols in Acute and Long-Term Care Facilities | +0.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Sanitizer Adoption in Asian Meat and Seafood Processing | +0.6% | APAC core—China, Thailand, Vietnam, Indonesia | Medium term (2-4 years) |

| Quick-Service Restaurant Boom Requiring Automated Ware-wash Dosing | +0.7% | Global, with North America and APAC hotspots | Short term (≤ 2 years) |

| Global Tourism and Hospitality Recovery | +0.5% | Europe, North America, APAC tourism hubs | Short term (≤ 2 years) |

| Semiconductor Clean-room Expansion Driving Ultra-Low-Residue Blends | +0.9% | APAC (China, South Korea, Taiwan), North America (Arizona, Texas) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infection-Control Protocols in Acute and Long-Term Care Facilities

Hospital environmental-services teams are replacing quaternary-ammonium disinfectants with hydrogen-peroxide and peracetic-acid blends that satisfy EPA List N emerging-pathogen criteria without triggering asthma liabilities[1]Centers for Disease Control and Prevention, “Guidelines for Environmental Infection Control in Health-Care Facilities,” cdc.gov. The Centers for Disease Control and Prevention updated its environmental infection-control guidelines in 2024, recommending sporicidal agents for high-touch surfaces, a change that lifts per-gallon chemical spend by up to 40% but cuts hospital-acquired infection penalties under Medicare’s Hospital-Acquired Condition Reduction Program. Long-term care operators face parallel mandates from state regulators that require logged contact times, driving uptake of ready-to-use sprayers with built-in timers. The World Health Organization’s 2024 IPC guidance links rigorous surface disinfection to antimicrobial resistance mitigation, reinforcing the shift toward premium chemistries. Demand for low-irritation actives also benefits acute-care renovations that incorporate automated UV-C robots and electrostatic sprayers.

Sanitizer Adoption in Asian Meat and Seafood Processing

Processors in China, Thailand, Vietnam, and Indonesia are investing in Clean-in-Place systems that pair foaming alkaline detergents with peracetic-acid rinses to clear export inspections for HACCP certification[2]State Administration for Market Regulation, “Food-Safety Inspection Protocols,” samr.gov.cn. China’s State Administration for Market Regulation began enforcing ATP bioluminescence verification in 2024, pushing operators to document chemical concentration for every shift. Trials by Meat & Livestock Australia showed that peracetic-acid carcass rinses combined with chlorine-dioxide flume treatments lowered Salmonella and E. coli prevalence by 1.5–2.0 log CFU/cm², justifying a 25% cost premium. Rising scrutiny from US FDA import alerts and EU Rapid Alert System notices further pressures Southeast Asian exporters to adopt validated quaternary-ammonium foamers and iodophor dips.

Quick-Service Restaurant Boom Requiring Automated Ware-wash Dosing

IoT-enabled ware-wash dispensers that auto-adjust detergent and rinse-aid flow based on water hardness and soil load are lowering chemical waste by up to 20% while ensuring NSF/ANSI 3 compliance. Ecolab’s DishIQ platform, launched in 2024, alerts managers when rinse temperatures dip below the 180°F sanitization threshold, reducing health department violations. Turnover in the U.S. quick-service sector averaged 150% in 2025, so color-coded, pre-portioned systems that cut training time to under eight hours have become essential. Robotics is also entering back-of-house cleaning: autonomous scrubbers fitted with on-board detergent tanks and UV-C modules are trimming labor hours by 35% and lowering slip-and-fall claims.

Global Tourism and Hospitality Recovery

Hotel occupancy in North America and Europe rebounded to 95% of 2019 levels by mid-2025, prompting housekeeping units to deploy electrostatic sprayers that sanitize rooms in under 10 minutes. The American Hotel & Lodging Association’s 2024 Safe Stay update requires EPA-registered disinfectants with 10-minute contact times and digital checklists for proof-of-service. Chemical spend per room has risen by USD 2–3 per night, but guest cleanliness complaints have fallen by roughly 45%. In the Asia-Pacific region, international arrivals surpassed pre-pandemic counts in 2025, and eco-labeled wipes compliant with Green Key and EarthCheck standards are now standard amenities. Medical-tourism clusters in Thailand are adopting pharmaceutical-grade cleaning regimes, supporting premium sporicidal demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating Petrochemical Feedstock Prices | -0.6% | North America and Middle East petrochemical hubs | Short term (≤ 2 years) |

| Ethylene-Oxide Volatility Elevating Surfactant Costs | -0.5% | Global regions dependent on ethoxylated surfactants | Medium term (2-4 years) |

| Stringent PFAS and VOC Regulations | -0.7% | North America and Europe, led by California and the European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuating Petrochemical Feedstock Prices

Ethylene-oxide spot values swung between USD 900 and USD 1,400/t in 2024-2025 after outages at Gulf Coast crackers, directly impacting ethoxylated alcohol costs. Propylene contracts traced similar volatility, pushing linear alkylbenzene sulfonate prices up or down by 30% each quarter. Small and mid-sized formulators without sophisticated hedging lost as much as five margin points during peak swings, whereas multinationals leveraged inventory buffers. European caustic-soda supply tightened when energy-intensive chlor-alkali units curtailed output, lifting prices by nearly 20% year-over-year.

Ethylene-Oxide Volatility Elevating Surfactant Costs

Extended maintenance at major US ethylene-oxide facilities restricted nonionic surfactant availability, elongating lead times to six weeks for contract customers. Latin American buyers paid premiums as spot cargoes diverted to North America. Contract clauses that peg quarterly price adjustments to ethylene-oxide indices are becoming standard, transferring some risk to end-users but amplifying budgeting complexity for institutional purchasers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Solvents Surge on Precision-Cleaning Demand

Surfactants, while holding a 32.18% 2025 industrial and institutional cleaning chemicals market share, will cede incremental ground to these fast-evaporating systems. Chlor-alkali derivatives remain staples for alkaline Clean-in-Place cycles in dairy, brewery, and beverage plants. Solvents are poised to grow at a 6.41% CAGR through 2031, lifted by electronics and metal-fabrication users that require ether- and alcohol-based blends leaving <10 µg/cm² residue.

Phosphate use is now largely restricted to heavy-duty degreasing in aerospace and automotive segments after bans in the European Union and multiple U.S. states. Meanwhile, citric acid is displacing mineral acids in descaling because it is stainless-steel-friendly and biodegradable. Biocides such as isothiazolinones make up only 0.5% of finished formulations, yet they are indispensable for microbial control in bulk concentrate storage, an attribute closely regulated under the EU Biocidal Products Regulation.

By Product Type: Disinfectants Accelerate Amid Infection-Control Mandates

General-purpose cleaners retained a 35.65% slice of the industrial and institutional cleaning chemicals market size in 2025. Hydrogen-peroxide and peracetic-acid blends achieve 1-5 minute kill times versus the 10 minutes needed for legacy quats, making them the disinfectant of choice for hospitals seeking to speed room turnover. General-purpose formulations compete on fragrance, color, and eco-label score, with Green Seal GS-37 certification now a default tender requirement for many US school districts. Disinfectants and sanitizers are expanding at a 6.76% CAGR by 2031.

Laundry-care powders and liquids face pressure from on-premise dosing systems that shave 15% off chemical cost per kilogram of linen. Vehicle-wash pre-soaks are pivoting toward touchless chemistries containing chelants and high-foaming amphoterics so tunnel operators can satisfy insurance underwriters that now demand quarterly slip-risk audits.

By Ingredient Origin: Bio-based Formulations Capture Sustainability Premiums

Conventional feedstocks held a 70.34% share in 2025, but bio-based blends sourced from coconut, palm kernel, and corn glucose are advancing 7.33% annually, the fastest within the industrial and institutional cleaning chemicals market. Alkyl-polyglucoside surfactants degrade >60% within 28 days under OECD 301, aligning with EU Ecolabel Wash-Off limits. Croda’s RSPO-certified fatty-alcohol ethoxylates let contract cleaners add “mass-balance” claims without segregated logistics.

Price sensitivity remains a barrier in vehicle-wash and industrial degreasing, where end-users resist premiums beyond 10%, yet corporate Scope 3 targets are tipping more hotel and foodservice chains toward greener sourcing. BASF’s bio-chelants, introduced in 2025, help laundry-formulators meet phosphate bans while matching sequestration performance at similar treat rates.

By Market Type: Commercial Segments Outpace Manufacturing on Labor Dynamics

Commercial establishments generated 54.46% of 2025 revenue and are forecast to log a 5.56% CAGR, outstripping manufacturing lines. Quick-service restaurants value automated ware-wash dosing that halves training hours for staff with 150% annual turnover. Hospitals and nursing homes prioritize EPA-registered sporicidal disinfectants and electrostatic sprayers to meet Medicare penalties tied to infection rates. Retailers and malls are adopting fragrance-free floor finishes to address chemical sensitivity litigation.

Manufacturing plants still rely on high-alkali or solvent formulations but are implementing recycling loops that recover 70-80% of spent solvent, compressing fresh-chemical demand. Semiconductor assemblers insist on particle-count certificates for each drum, elevating quality-assurance costs. Textile mills and pulp-and-paper operations upgrade enzymatic sizing removal systems, which cut caustic use by 25%, thereby redefining consumption patterns.

Geography Analysis

North America commanded 34.49% of the industrial and institutional cleaning chemicals market in 2025, thanks to entrenched distribution networks, stringent EPA and FDA standards, and high per-capita chemical use in healthcare and hospitality. Quick-service operators in the United States, facing 150% labor churn, rely on pre-measured sachets to maintain hygiene when onboarding windows shrink. Canada’s food-processing clusters and Mexico’s automotive corridors add steady solvent and degreaser demand.

Asia-Pacific is the fastest-growing region at a 6.98% CAGR through 2031, propelled by China’s semiconductor wet-cleaning boom and India’s foodservice sector. Tier-2 Indian cities are rolling out automated ware-wash systems, while Southeast Asian shrimp and poultry processors invest in validated sanitation protocols to avoid US FDA import alerts. Thailand’s manufacturing sector, contributing 44% of 2024 GDP, sustains alkaline and solvent uptake in electronics and automotive facilities.

Europe posts moderate growth, constrained by mature consumption but lifted by sustainability premiums under EU Ecolabel and REACH. South America endures currency headwinds, yet agricultural exports keep sanitation volumes healthy in Brazil and Argentina. The Middle East and Africa show nascent uptake; water-scarce GCC nations favor low-rinse concentrates, while Egypt and South Africa deploy chlor-alkali cleaners in food-processing and hospitality builds linked to tourism diversification drives.

Competitive Landscape

The Industrial and Institutional Cleaning Chemicals market remains moderately fragmented. Ecolab’s January 2024 purchase of Purolite’s ion-exchange resins integrated water-treatment know-how with cleaning portfolios, enabling bundled RO pretreatment and wastewater recycling for beverage bottlers. BASF and Croda expanded bio-surfactant capacity, targeting customers seeking RSPO-certified mass-balance supply. Technology adoption is reshaping service models: IoT dispensers feed dilution data into ERP systems, triggering automated re-orders and ensuring OSHA Hazard Communication compliance.

Industrial And Institutional Cleaning Chemicals Industry Leaders

3M

BASF

Ecolab

Henkel AG & Co. KGaA

Reckitt

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Evonik Industries AG forged an exclusive partnership with Sea-Land Chemical Company to distribute its eco-friendly cleaning solutions across the United States. Evonik's innovative offerings cater to diverse sectors, including home care, vehicle care, and institutional cleaning, with a notable emphasis on sustainability.

- February 2025: First Quality Enterprises made a move into the detergents, fabric finishers, and dishwash categories by acquiring Henkel AG & Co. KGaA’s Retailer Brands business in North America. This newly acquired business will be housed under a fresh division named First Quality Home Care Products, set to function as an independent entity within the First Quality Group.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the industrial and institutional cleaning chemicals market as formulated agents, detergents, disinfectants, sanitizers, surfactants, solvents, laundry aids, and vehicle-wash fluids sold to non-residential facilities for surface, equipment, and textile hygiene in factories, hospitals, food-service outlets, offices, and public institutions.

Scope Exclusion: Household consumer cleaners and fee-based janitorial service revenues are excluded.

Segmentation Overview

- By Raw Material

- Chlor-alkali

- Caustic Soda

- Soda Ash

- Chlorine

- Surfactants

- Non-ionic

- Anionic

- Cationic

- Amphoteric

- Solvents

- Alcohols

- Hydrocarbons

- Chlorinated

- Ethers

- Phosphates

- Acids

- Biocides

- Other Raw Materials (Chelants, Rheology Modifiers, Opacifiers, Dispersants, Ketones, Esters)

- Chlor-alkali

- By Product Type

- General-Purpose Cleaners

- Disinfectants and Sanitizers

- Laundry Care Products

- Vehicle Wash Products

- By Ingredient Origin

- Bio-based / Green

- Conventional / Petrochemical

- By Market Type

- Commercial

- Foodservice

- Retail

- Laundry and Dry-Cleaning

- Healthcare

- Car Washes

- Offices, Hotels and Lodging

- Manufacturing

- Food and Beverage Processing

- Fabricated Metal Products

- Electronic Components

- Other Manufacturing (Textile, Pulp and Paper, Petrochemical)

- Commercial

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Turkey

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Egypt

- South Africa

- Nigeria

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with formulators, contract cleaners, hospital procurement officers, distributors, and safety regulators across North America, Europe, and Asia. Their views on dosage rates, sustainability premiums, and channel margins closed data gaps and anchored assumptions before triangulation.

Desk Research

We gather baseline signals from open datasets such as US EPA Chemical Data Reporting, Eurostat PRODCOM, China Customs HS-3402 exports, and association digests from ISSA and AISE, which map output volumes, ingredient demand, and facility counts. Company 10-Ks, investor slides, and reputable news further refine raw-material splits and average prices. Paid libraries, D&B Hoovers, Dow Jones Factiva, and Questel supply revenue tranches, news velocity, and patent flow. Numerous other credible records also informed the model.

Market-Sizing & Forecasting

A top-down demand pool derived from facility counts and typical chemistry usage is cross-checked with sampled ASP × volume roll-ups from supplier calls. Key variables include installed hospital beds, global food-service floor area, chlor-alkali production, surfactant price indices, and bio-based adoption rates. Forecasts employ multivariate regression combined with scenario analysis to reflect regulation tightening and feedstock swings.

Data Validation & Update Cycle

Outputs face anomaly checks, historical stress tests, and a multi-level review. We refresh values each year and issue interim updates when regulation or price shocks warrant.

Why Mordor's Industrial And Institutional Cleaning Chemicals Baseline Commands Reliability

Published figures differ because some studies mix consumer volumes, apply aggressive penetration curves, or convert currencies at outdated rates.

Mordor's disciplined scope, annual refresh, and dual-view modeling keep our baseline realistic.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 57.44 B (2025) | Mordor Intelligence | |

| USD 80.05 B (2024) | Global Consultancy A | Includes household cleaners and higher ASP uplift |

| USD 90.14 B (2025) | Regional Publisher B | Bundles adjacent specialty chemicals and uniform growth |

This comparison shows how Mordor's clear scope and refreshed data yield a balanced, transparent baseline trusted by decision-makers.

Key Questions Answered in the Report

How large will the industrial and institutional cleaning chemicals market be by 2031?

It is projected to reach USD 75.72 billion, expanding at a 4.72% CAGR during 2026-2031.

Which raw-material category is growing fastest?

Solvents are set to rise at a 6.41% CAGR as precision-cleaning needs in electronics and metal-fabrication escalate.

Why are disinfectants outpacing general-purpose cleaners?

Hospitals, foodservice, and hospitality operators now prioritize EPA-registered sporicidal efficacy, lifting disinfectants and sanitizers at a 6.76% CAGR.

What is driving Asia-Pacific demand?

China’s semiconductor fabs and India’s quick-service restaurant build-out are propelling regional growth at a 6.98% CAGR.

How are regulations influencing product reformulation?

The EPA’s 4 ppt PFAS limit and EU REACH VOC rules are accelerating a shift to fluorine-free surfactants and low-VOC solvents across multiple applications.

Page last updated on: