Mining Chemicals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.32 Billion |

| Market Size (2031) | USD 9 Billion |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

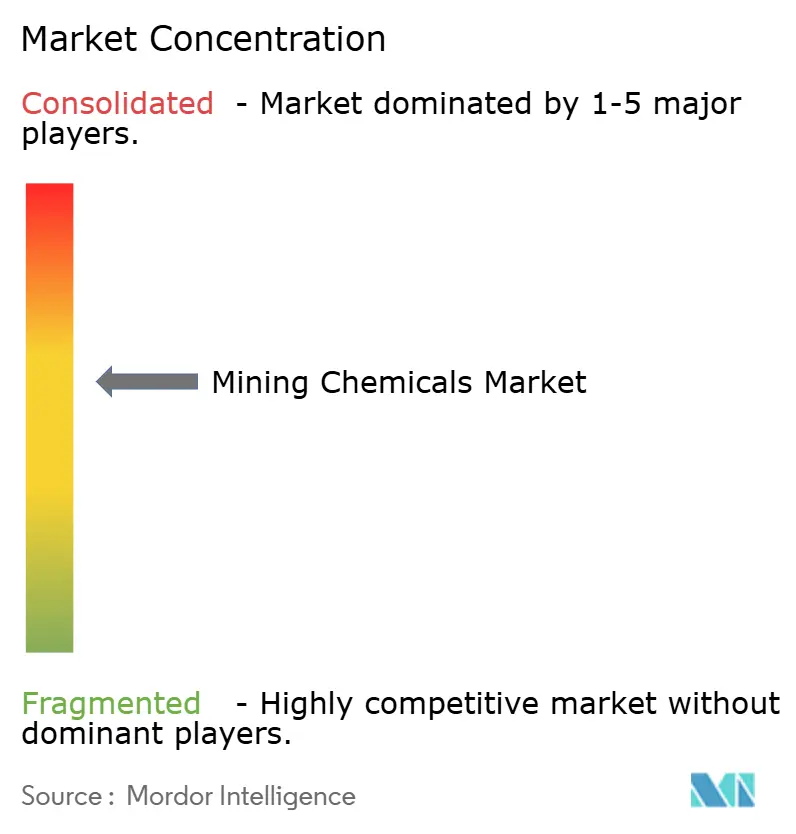

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mining Chemicals Market Analysis by Mordor Intelligence

The mining chemicals market size is expected to increase from USD 7.02 billion in 2025 to USD 7.32 billion in 2026 and reach USD 9 billion by 2031, growing at a CAGR of 4.22% over 2026-2031. Flotation reagents remain the anchor of demand, yet direct-lithium-extraction (DLE) modules and solvent-extraction cascades for battery metals are redrawing global procurement maps. Sovereign manufacturing mandates in China, the United States, and the European Union are compelling mine operators to dual-source collectors and extractants, tempering the traditional dominance of center-led purchasing. Capital expenditure on nickel laterite, lithium spodumene, and porphyry-copper expansions is sustaining reagent volumes even as sensor-based ore sorting trims per-ton consumption. Meanwhile, accelerated tailings-management rules and water-recycling targets are channeling fresh spending toward high-molecular-weight flocculants that fit closed-loop circuits.

Key Report Takeaways

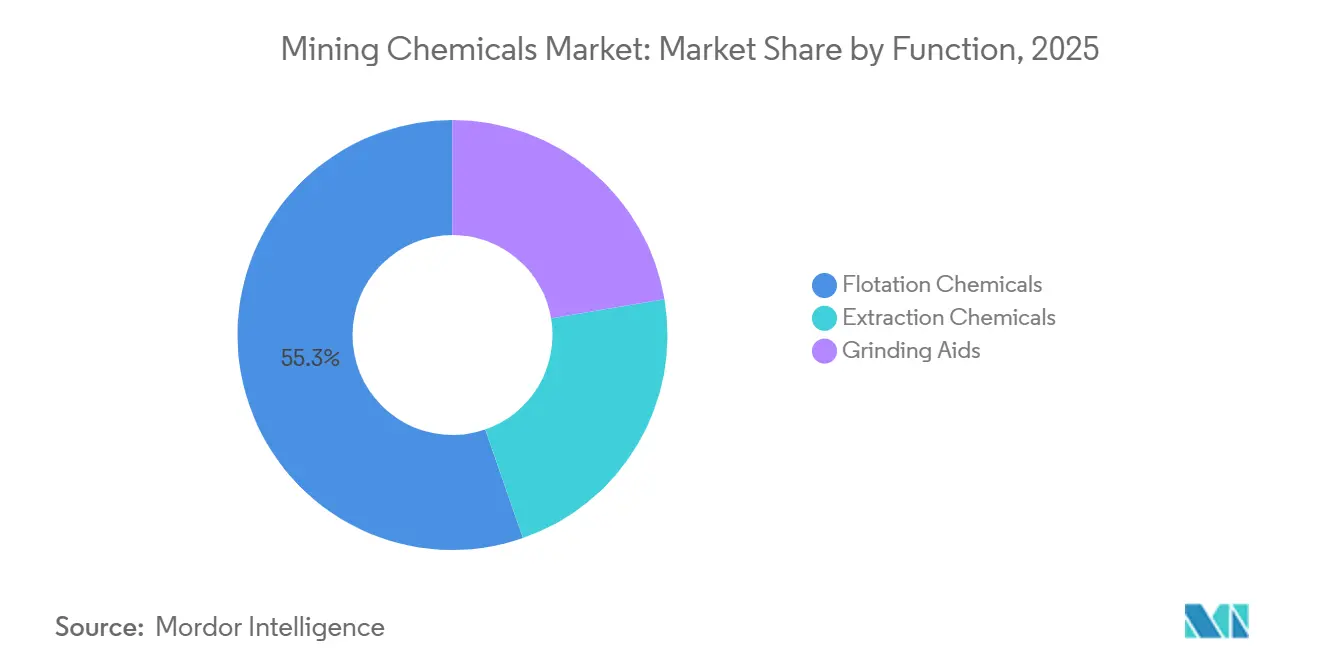

- By function, flotation chemicals held 55.33% of the mining chemicals market share in 2025. Extraction chemicals recorded the fastest expansion at a 4.33% CAGR through 2031.

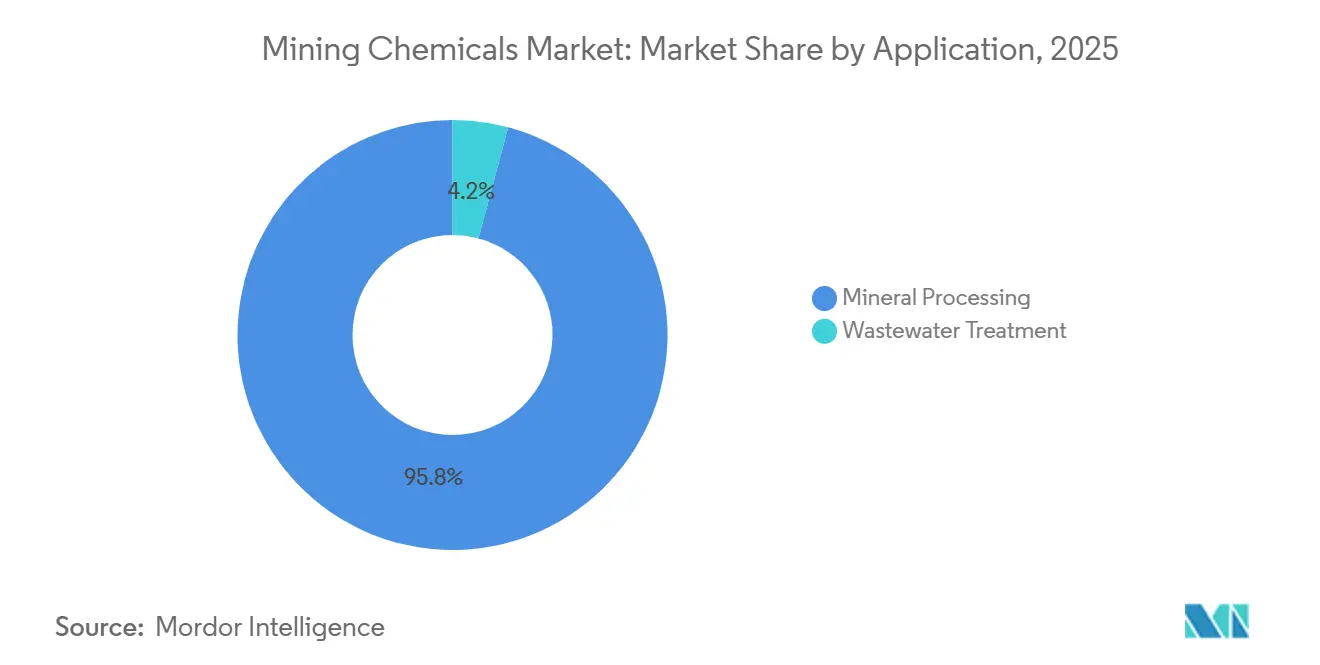

- By application, mineral processing accounted for 95.82% of the mining chemicals market size in 2025. Wastewater treatment posted the highest projected CAGR at 4.86% during 2026-2031.

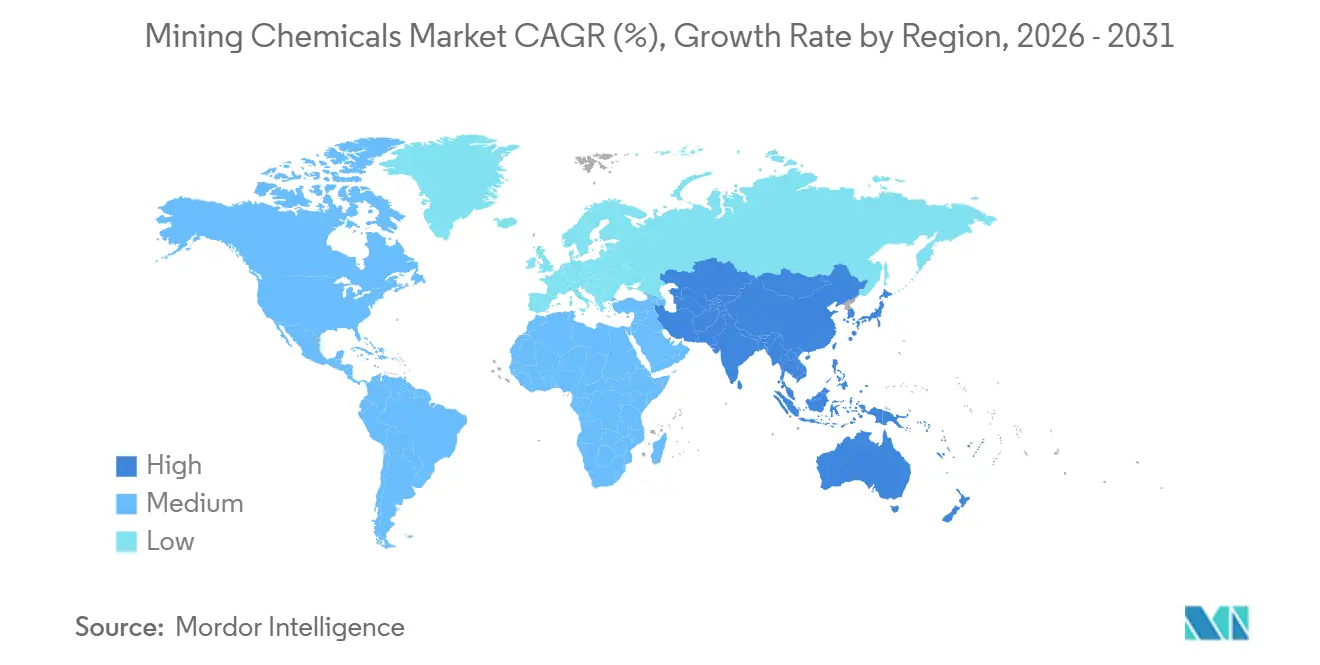

- By region, Asia-Pacific led with 54.13% revenue share in 2025, while it is also set to grow at a 5.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mining Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Mining CAPEX in Asia-Pacific and North America | +1.2% | Asia-Pacific core (China, Indonesia, Australia), North America (Canada, United States) | Medium term (2-4 years) |

| Surging Mineral Demand from Electric Vehicle and Renewable-Energy Supply Chains | +1.5% | Global, with concentration in Asia-Pacific lithium/nickel processing and South American copper operations | Long term (≥ 4 years) |

| Stricter Water-Recycling Norms in Large Mines | +0.8% | Chile, Australia, South Africa, Peru—arid and water-stressed jurisdictions | Short term (≤ 2 years) |

| Commodity-Price Rebound Sustaining Exploration Budgets | +0.6% | Global, with emphasis on copper belts (Chile, Peru, Zambia) and gold districts (Canada, Australia) | Medium term (2-4 years) |

| Shift to Bio-Based Collectors for ESG Compliance | +0.4% | Europe, Canada, Scandinavia—jurisdictions with carbon-disclosure mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Mining CAPEX in Asia-Pacific and North America

New nickel HPAL lines in Indonesia and lithium DLE pilots in Nevada and Alberta are lifting annual demand for sulfuric acid, tributyl phosphate, and crown-ether extractants. Copper expansions in Chile’s Atacama Desert and Canada’s Ring of Fire are adding collectors and frothers, although widespread ore-sorting retrofits are moderating reagent intensity.

Surging Mineral Demand from Electric Vehicle and Renewable-Energy Supply Chains

Through flotation or solvent extraction, battery metals are purified into intermediates. In China, lithium-iron-phosphate cells have surpassed cobalt-rich chemistries. Meanwhile, in Western Australia, spodumene flotation continues to use fatty-acid collectors. With projected copper deficits by 2030, the demand for xanthate and dithiophosphate collectors remains stable.

Stricter Water-Recycling Norms in Large Mines

Chile's DGA has mandated water recycling in new permits. This push is driving the installation of high-throughput thickeners, which are dosed with anionic polyacrylamide flocculants. In Australia and South Africa, similar regulations are accelerating the adoption of closed-loop circuits. These circuits can reduce freshwater intake. However, they also increase dissolved-salt loads, necessitating the use of specialty dispersants[1]Gobierno de Chile, “Reglamento de Recirculación de Agua en Minería,” mma.gob.cl .

Commodity-Price Rebound Sustaining Exploration Budgets

With copper prices hovering around a high level and gold surpassing a significant threshold, exploration expenditures for 2025 remained steady. In response to these market conditions, junior explorers increased their budgets, bolstering the demand for drilling fluids and pilot-scale flotation reagents, both of which are crucial for feasibility studies extending into 2027.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Global Regulations on Toxic Reagents | -0.7% | Europe (REACH), North America (EPA Toxic Substances Control Act), China (MEE chemical inventory) | Medium term (2-4 years) |

| Volatile Crude-Derived Raw-Material Costs | -0.5% | Global, with acute impact on petrochemical hubs in Middle East, Asia-Pacific, and U.S. Gulf Coast | Short term (≤ 2 years) |

| Emerging Dry-Processing Technologies that Bypass Wet Reagents | -0.9% | Australia, Canada, South Africa—jurisdictions with high labor costs and water scarcity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Regulations on Toxic Reagents

In 2024, ECHA added sodium ethyl xanthate to the REACH Candidate List, setting off an authorization sunset for 2026. Meanwhile, the U.S. EPA is scrutinizing potassium amyl xanthate, and China's MEE is now requiring fresh toxicity dossiers for 47 flotation reagents. These compliance costs are siphoning off research and development budgets, potentially hindering the adoption of new collectors, especially in jurisdictions that are cautious[2]European Chemicals Agency, “Candidate List of Substances of Very High Concern,” echa.europa.eu.

Volatile Crude-Derived Raw-Material Costs

Brent crude's fluctuations have driven up costs for carbon disulfide and alcohol, leading to a rise in xanthate prices. Meanwhile, contract outages at Gulf Coast crackers have tightened the supply of ethylene and propylene. In response, mines are extending their inventory cycles and exploring toll-blending options as a hedge against feedstock risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Extraction Chemicals Advance on DLE Momentum

In 2025, flotation chemicals are projected to account for 55.33% of the mining chemicals market revenue. While collectors, frothers, and depressants lead in value, there's a notable rise in the adoption of hydroxamate and bio-based collectors, especially in oxide-copper and nickel laterite circuits. Extraction chemicals, representing diluents and organophosphorus extractants, are riding the direct-lithium-extraction wave at a 4.33% CAGR, underscoring a subtle shift in the mining chemicals market size allocation across functional lines. DLE initiatives in Arkansas and Bolivia, showcasing substantial water savings and expedited cycle times, are driving up the demand for crown-ether and phosphate-based extractants. Concurrently, rare-earth facilities in China and the U.S. are now utilizing significant volumes of C6-C12 diluents to maintain stable mixer-settler temperature profiles.

Grinding aids, though the smallest segment in the mining chemicals arena, are witnessing promising trials. In Chilean copper and Mongolian gold concentrators, these aids have led to notable increases in throughput and reductions in energy consumption. However, broader adoption is contingent on demonstrating a return on investment, especially with varying ore hardness. In a related trend, suppliers are now offering digital dosage valves alongside reagents. This strategy not only curbs overdosing but also resonates with the industry's pivot towards performance-centric purchasing.

By Application: Wastewater Treatment Gains Regulatory Tailwind

Mineral processing captured 95.82% of 2025 application revenue, cementing its role as the prime consumer segment within the mining chemicals market. Large sulfide concentrators produce process water for every metric ton of ore. With closed-loop mandates in play, operators are now channeling investments into thickeners and high-charge-density polyacrylamides, aiming to reduce turbidity levels. This trend solidifies mineral processing's pivotal role in the mining chemicals market, a position expected to endure through 2031.

While wastewater treatment represented a modest portion of the 2025 market, is expanding at a 4.86% CAGR. Projects addressing acid mine drainage in legacy coal basins, alongside tailings dam upgrades in South America, are utilizing lime, coagulants, and flocculants in their staged neutralization processes. Moreover, instrumented polymer make-up systems are being employed to fine-tune viscosity and dosage, a trend that leans towards suppliers offering both chemical and digital solutions. Given this growth disparity, a gradual market rebalancing seems imminent, especially as ESG-linked financial pressures compel mines to be transparent about their water intensity metrics.

Geography Analysis

Asia-Pacific dominated the mining chemicals market with 54.13% of 2025 revenue and is advancing at a 5.12% CAGR to 2031. Indonesia has rolled out new HPAL lines, each with significant annual consumption of sulfuric acid and extractants. In Jiangxi and Inner Mongolia, China has boosted its copper-ore processing capacity, utilizing domestically produced xanthates that are priced lower than their imported counterparts. Australia has ramped up its lithium hydroxide output, with spodumene flotation increasingly relying on fatty-acid collectors due to finer ore feeds. Meanwhile, Japan and South Korea have positioned themselves as key blending hubs, importing pine-oil frothers and redistributing them to nickel smelters in Indonesia.

North America accounted for a notable portion of the market's 2025 revenue. In Nevada’s Clayton Valley and Alberta’s Leduc Formation, pilot projects are testing DLE columns, which require specialty ion-exchange resins and tributyl phosphate diluents. Expansions in copper production in Arizona and British Columbia, along with potash debottlenecking in Saskatchewan, are driving sustained demand for collectors. While Mexico’s silver and gold belts continue to be consistent consumers, community pushback has postponed cyanide-based projects, leading to a dip in short-term reagent orders.

Europe, South America, and the combined regions of the Middle East and Africa account for the remaining share of the mining chemicals market. In 2025, Chile and Peru made joint purchases of xanthates and dithiophosphates. However, due to escalating water scarcity issues, there's a swift shift towards high-throughput thickeners treated with anionic polyacrylamide. Operators in South Africa’s Bushveld region are now opting for intricate depressant blends to adeptly handle both Merensky and UG2 mineralogy. Furthermore, Scandinavian mines are testing bio-collectors, which hold the potential to set global standards, especially with impending REACH restrictions tightening post-2026.

Competitive Landscape

The mining chemicals market remains moderately consolidated. SNF Group maintains a dominant position in high-molecular-weight flocculants through backward integration into acrylamide monomer. White-space opportunities revolve around DLE extractants expected to create a niche by 2030 if the technology captures a significant share of global lithium output. Digital dosing platforms from Ecolab’s Nalco Water integrate flowmeters and AI-driven set-point control, reducing polymer overdosing and differentiating on total-cost-of-ownership rather than reagent price alone. Patent filings covering bio-collectors and lithium-selective extractants surged between 2023 and 2025, underscoring the innovation race that will shape competitive dynamics through the forecast period.

Mining Chemicals Industry Leaders

Syensqo

BASF

Clariant

Nouryon

Orica Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Solenis acquired BASF's global flocculant mining business. This divestiture, which encompasses key mining trademarks such as Magnafloc, Rheomax, and Alclar, bolsters Solenis's portfolio in solid-liquid separation. Meanwhile, BASF is shifting its focus towards flotation reagents, leaching, and solvent extraction technologies.

- February 2024: Orica Limited announced the acquisition of Cyanco, a US-based company primarily serving the gold mining industries. Through the acquisition, the company plans to strengthen its mining chemicals business.

Global Mining Chemicals Market Report Scope

Mineral and ore mining requires chemicals. These chemicals take rich minerals and metals from ore and convert them for industrial use. Flotation reagents remove minerals from waste rock and other ore contaminants. Cyanide extracts gold from ore, and acids dissolve and recover copper and nickel.

The mining chemicals market is segmented by function, application, and geography. By function, the market is segmented into flotation chemicals, extraction chemicals, and grinding aids. By application, the market is segmented into mineral processing and wastewater treatment. The report also covers the market size and forecasts for the mining chemicals market in 18 countries across major regions. Each segment's market sizing and forecasts are based on revenue (USD).

| Flotation Chemicals | Collectors |

| Depressants | |

| Flocculants | |

| Frothers | |

| Dispersants | |

| Extraction Chemicals | Diluents |

| Extractants | |

| Grinding Aids |

| Mineral Processing |

| Wastewater Treatment |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Malaysia | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Function | Flotation Chemicals | Collectors |

| Depressants | ||

| Flocculants | ||

| Frothers | ||

| Dispersants | ||

| Extraction Chemicals | Diluents | |

| Extractants | ||

| Grinding Aids | ||

| By Application | Mineral Processing | |

| Wastewater Treatment | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Malaysia | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for the mining chemicals market between 2026 and 2031?

The sector is projected to advance at a 4.22% CAGR from USD 7.32 billion in 2026 to USD 9.00 billion.

Which region leads global demand for mining reagents?

Asia-Pacific contributed 54.13% of 2025 revenue and is growing faster than the worldwide average at a 5.12% CAGR to 2031.

Why are extraction chemicals gaining momentum relative to flotation reagents?

Direct-lithium-extraction modules and rare-earth solvent-extraction circuits are expanding, lifting demand for organophosphorus extractants at a forecast 4.33% CAGR.

How are water-recycling mandates shaping reagent consumption?

New rules in Chile, Australia, and South Africa require 80% or higher water recycling, boosting flocculant volumes for closed-loop circuits.

Page last updated on: