Personal Care Chemicals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 18.31 Billion |

| Market Size (2031) | USD 23.30 Billion |

| Growth Rate (2026 - 2031) | 4.94% CAGR |

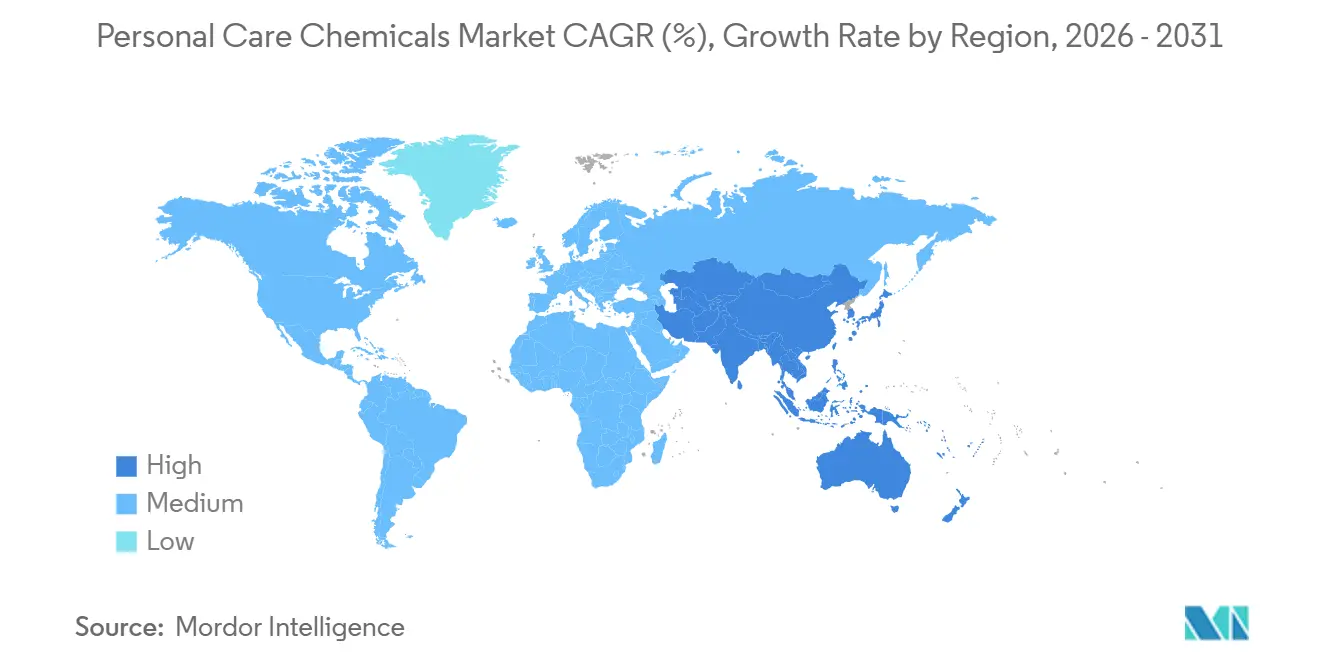

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

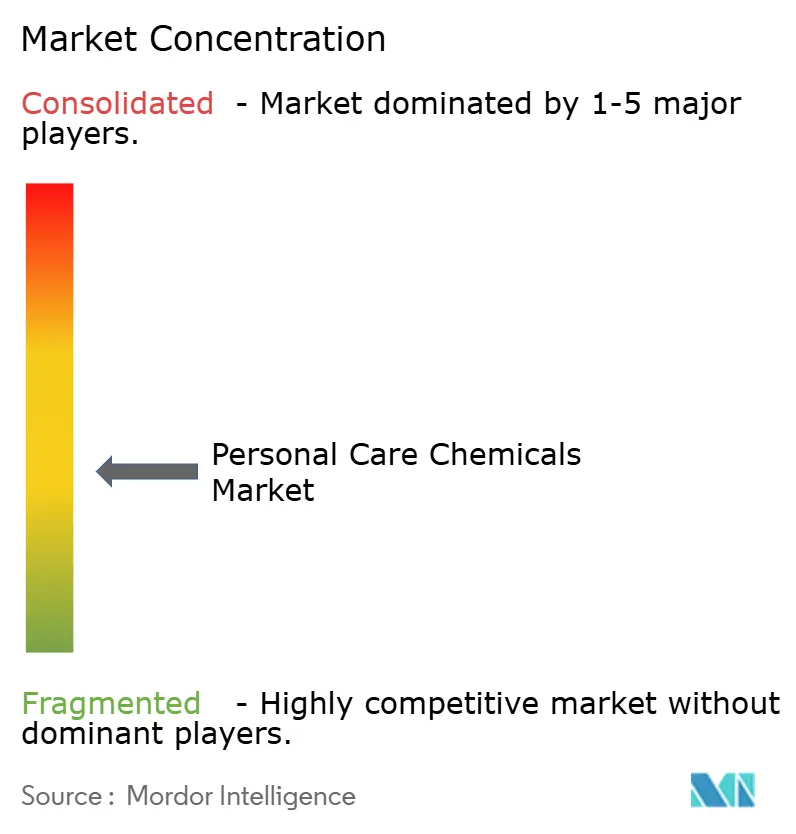

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personal Care Chemicals Market Analysis by Mordor Intelligence

The Personal Care Chemicals Market size is expected to increase from USD 17.45 billion in 2025 to USD 18.31 billion in 2026 and reach USD 23.30 billion by 2031, growing at a CAGR of 4.94% over 2026-2031. Brands are tilting their ingredient budgets toward clinically validated actives, which explains why active-ingredient demand is rising faster than inactives, even though surfactants, emulsifiers, and emollients still dominate formulation volumes. Asia-Pacific’s expanding middle class, streamlined Chinese registration rules, and K-beauty exports underpin regional leadership, while North American and European players absorb compliance costs tied to MoCRA and updated EU Cosmetics Regulation requirements. Feedstock price swings for palm derivatives and ethylene oxide continue to squeeze margins for commodity surfactant suppliers, accelerating the shift toward fermentation-based actives that offer lower carbon footprints and steadier input costs. At the same time, e-commerce beauty brands source specialty actives in smaller lots, rewarding flexible suppliers with digital ordering portals and just-in-time logistics.

Key Report Takeaways

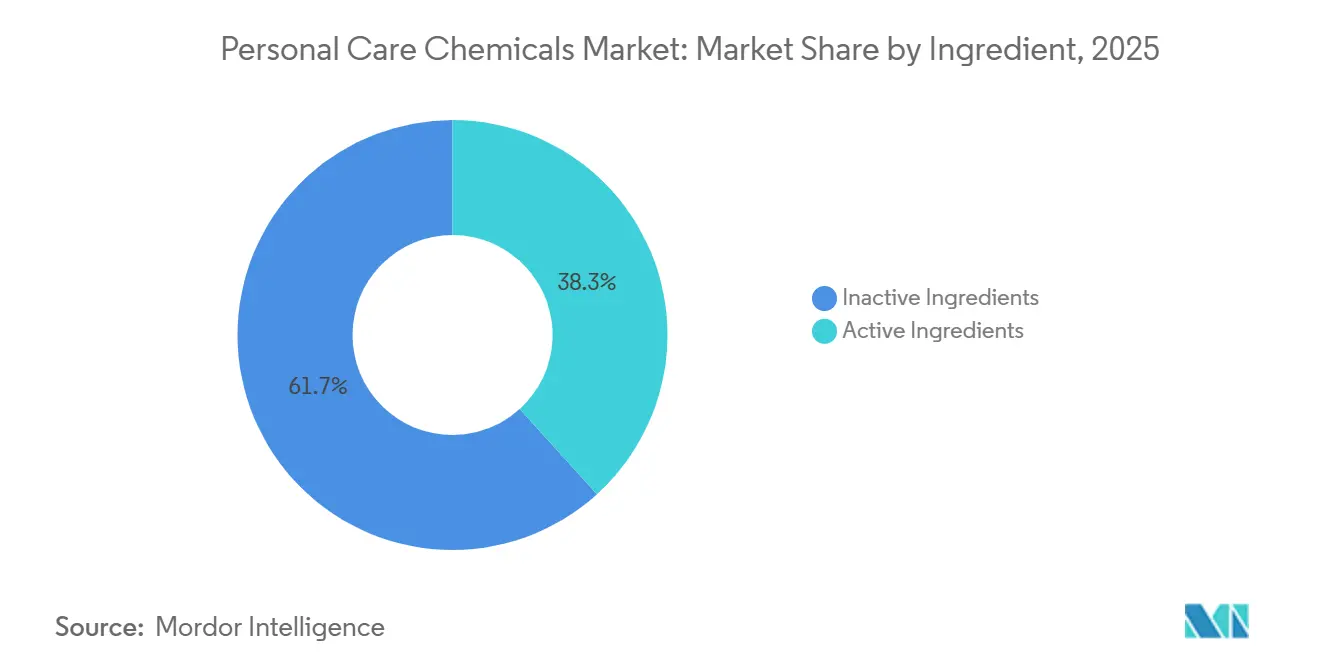

- By ingredient, inactive ingredients led with 61.72% of personal care chemicals market share in 2025; active ingredients are projected to expand at a 5.31% CAGR through 2031.

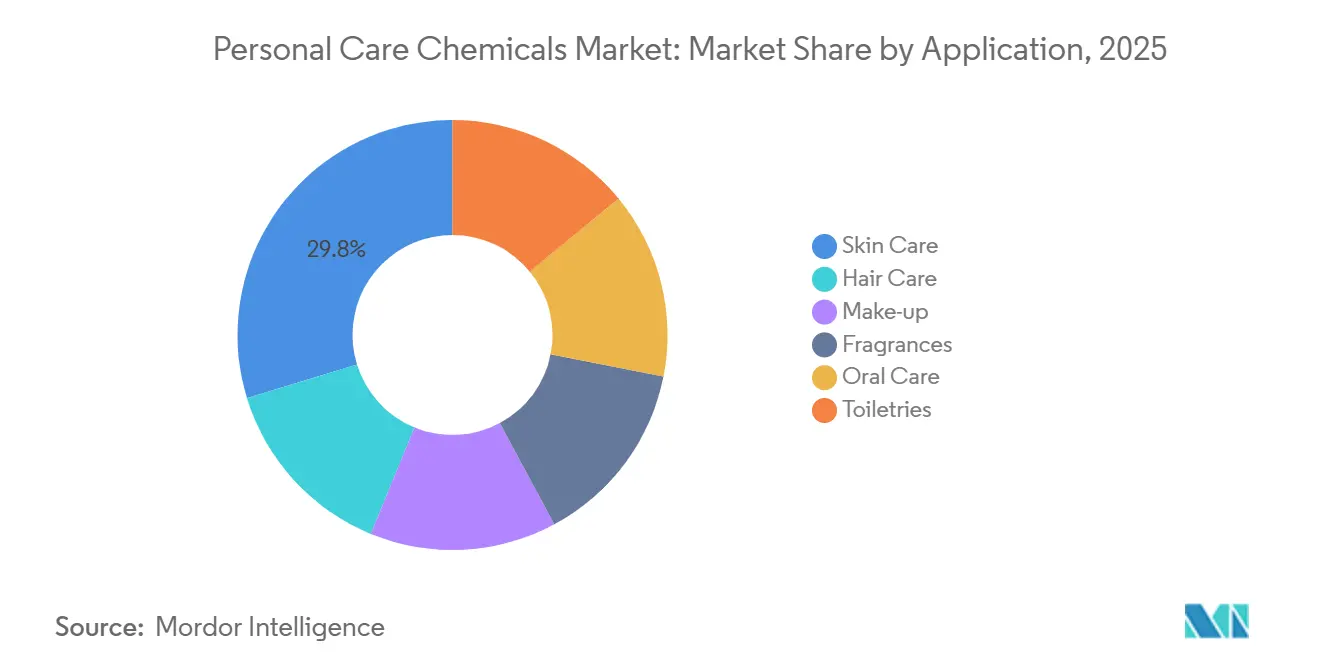

- By application, skin care held 29.75% of personal care chemicals market size in 2025, and oral care is advancing at a 5.46% CAGR through 2031.

- By geography, Asia-Pacific accounted for 30.21% of personal care chemicals market value in 2025, while the region is forecast to grow at a 6.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personal Care Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Asia-Pacific middle-class spending boom | +1.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Natural and sustainable ingredient shift (RSPO, COSMOS) | +0.9% | Global, with early gains in Europe and North America | Long term (≥ 4 years) |

| E-commerce acceleration of niche beauty brands | +0.7% | Global, concentrated in North America, Europe, China | Short term (≤ 2 years) |

| AI-driven formulation and predictive toxicology | +0.5% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Fermentation-based carbon-upcycled actives | +0.6% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Asia-Pacific Middle-Class Spending Boom

Urban household disposable income in India and China rose 7-9% annually during 2024-2025, lifting per-capita spending on premium skin-care and color-cosmetics products that rely on niacinamide, tranexamic acid, and encapsulated retinol. South Korea’s K-beauty exports increased 14% in 2025, driving peptide and centella asiatica orders across ASEAN markets. Japan’s functional-cosmetics category—which requires quasi-drug approval—grew 11% in 2024, steering suppliers toward clinical-grade actives that meet MHLW standards. The ISO 22716 GMP framework is gaining traction region-wide, smoothing multi-country product registrations. Collectively, these shifts underpin the personal care chemicals market’s fastest regional expansion.

Natural and Sustainable Ingredient Shift (RSPO, COSMOS)

RSPO-certified palm-derived inputs reached 1.2 million metric tons in 2024 after L’Oréal, Unilever, and Procter & Gamble pledged 100% certification by 2026. COSMOS approvals climbed 22% in 2025, prompting BASF to invest EUR 50 million in bio-based surfactant capacity at Ludwigshafen[1]BASF SE, “BASF Expands Bio-Based Surfactant Capacity,” basf.com . Croda’s 2024 acquisition of Alban Muller secured upcycled plant actives from grape pomace and olive-mill waste, broadening its sustainable portfolio. Brands now ask for carbon-footprint data at the ingredient level, a transparency leap that favors suppliers with integrated traceability platforms. EU Ecolabel and REACH updates reinforce this trajectory in Europe.

E-Commerce Acceleration of Niche Beauty Brands

Digitally native beauty brands captured 28% of U.S. prestige sales in 2025, and suppliers report typical 200-500 kg specialty-active orders versus multi-ton legacy CPG volumes. Seppic’s 2025 digital portal lets formulators filter by COSMOS status and carbon footprint, trimming sample cycles from weeks to days. Ingredient origin disclosure by brands such as The Ordinary pressures peers to match transparency, while MoCRA’s ingredient-listing rule cements this practice in the United States. The result is a faster product-development cadence that rewards agile chemical manufacturers within the personal care chemicals market.

AI-Driven Formulation and Predictive Toxicology

L’Oréal’s internal SimplifIA tool processed 40,000 formulation permutations in 2024, cutting launch timelines by six months. Shiseido’s January 2025 collaboration with IBM Research applies quantum-inspired algorithms to predict skin penetration of novel peptides, improving candidate selection. Unilever’s Digital Twin simulates ingredient interactions to reduce physical prototyping by 30-40%. Predictive toxicology models draw on OECD QSAR datasets and in-vitro assays, enabling earlier screening of sensitizers, while ISO 10993 and REACH provide reference frameworks. These advances shrink cost and risk across the personal care chemicals market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petro-derivative cost volatility | -0.8% | Global, acute in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Water-scarcity limits on rinse-off formats | -0.4% | Middle-East, North Africa, Western US, Australia | Medium term (2-4 years) |

| Traceability mandates (MoCRA-style) squeezing SME margins | -0.5% | North America, expanding to EU and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Petro-Derivative Cost Volatility

Palm-oil prices ranged between USD 950 and USD 1,180 per metric ton during 2024-2025, driven by Indonesia’s biodiesel mandate and El Niño yield losses, raising costs for sodium lauryl sulfate and other palm-kernel-based surfactants. Ethylene oxide spot spikes added pressure to ethoxylated emulsifiers, and Stepan’s surfactant margin dropped 240 basis points in 2024. Larger suppliers hedge volatility, but smaller formulators often pass costs to consumers or exit, accelerating consolidation such as Nouryon’s 2024 purchase of two Southeast Asian toll manufacturers. Bio-based surfactants offer a partial buffer but remain premium-priced for mass-market products.

Water-Scarcity Limits on Rinse-Off Formats

Municipal water restrictions in California, South Africa, and Gulf states spur reformulation of shampoos, body washes, and cleansers into waterless bars, powders, and concentrates, cutting consumer water use 50-70%. Procter & Gamble’s Waterless line debuted in 2024 with solid shampoo bars, while Kao introduced 5× concentrate refills that reduce plastic by 60% per use. These formats boost demand for emollients and powder surfactants, shifting the ingredient mix inside the personal care chemicals market. ISO 14046 water-footprint disclosures and CDP Water Security reporting underscore the urgency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient: Biotech Actives Narrow the Growth Gap with Commodity Surfactants

Inactive ingredients captured 61.72% of personal care chemicals market value in 2025, led by surfactants, emulsifiers, and emollients that supply critical cleansing, stabilization, and sensorial functions. Emulsifiers such as polysorbates and glyceryl stearates stabilize oil-in-water creams, while emollients—fatty alcohols, esters, and silicones—deliver glide and barrier repair. Rising consumer preference for clean-label cosmetics is pushing the shift from synthetic colorants toward natural beetroot and turmeric pigments, especially in Europe and North America. Rheology modifiers, including carbomers and xanthan gum, maintain viscosity across a wide pH range.

Active ingredients, forecast to grow at 5.31% CAGR, are closing the revenue gap as brands emphasize clinical efficacy. Conditioning agents such as quats and silicone derivatives remain staples for hair-care products, and bond-repair polymer adoption has expanded beyond salon channels. UV filters command premium pricing; regulatory scrutiny of avobenzone and octocrylene is hastening mineral alternative uptake. Powerful anti-aging actives—retinoids, peptides, niacinamide, antioxidants—win price premiums because they deliver measurable benefits, as shown by Croda’s Matrigenics.14G peptide improving skin elasticity by 23% in a 12-week trial. Exfoliants such as alpha- and beta-hydroxy acids are thriving in Asia-Pacific brightening regimens. ISO 22716 and COSMOS certifications increasingly shape procurement decisions, aligning suppliers with premium-brand expectations for safety and sustainability within the personal care chemicals market.

By Application: Oral Care Actives and Skin Care Peptides Lead Growth Trajectories

Skin care accounted for 29.75% of personal care chemicals market value in 2025 as premium serums, sunscreens, and moisturizers adopt encapsulated peptides, ceramides, and multiple-weight hyaluronic acids to enhance efficacy. Hair care demand is boosted by scalp-microbiome actives and bond-building polymers that restore chemically treated hair. Makeup uses pigments, film formers, and plant-based waxes, and clean-beauty claims are driving the replacement of synthetic colorants with iron oxides and mica blends. Fragrance remains niche by volume but demands high-purity essential oils; Symrise’s naturals business rose 12% in 2024.

Oral care is the fastest-growing application at a 5.46% CAGR, reflecting uptake of fluoride alternatives such as nano-hydroxyapatite and PAP whitening enzymes. Probiotic toothpastes featuring Lactobacillus strains gain traction in Japan and South Korea, while mouthwashes incorporate cetylpyridinium chloride for antibacterial action. Toiletries—deodorants, bath products, intimate hygiene—benefit from aluminum-free antiperspirants and pH-balanced actives. Regulatory monographs from the FDA and EU Cosmetics Annex III steer formulation boundaries, but rising consumer awareness of ingredient safety continues to influence the direction of the personal care chemicals market.

Geography Analysis

Asia-Pacific contributed 30.21% of personal care chemicals market value in 2025 and is set to grow at 6.12% CAGR, fueled by income growth, urbanization, and regulatory streamlining. China’s 2024 NMPA reforms waived animal testing for many imported products when ISO 22716 is in place, accelerating ingredient launches[2]National Medical Products Administration, “2024 Cosmetics Supervision Regulation Update,” nmpa.gov.cn . India’s cosmetics sales grew 11% in 2024, and local brands increasingly procure sustainable turmeric and neem actives, while global suppliers invest in bio-based surfactant plants to meet large rinse-off demand. South Korea’s K-beauty exports and Japan’s quasi-drug approvals propel demand for clinical-grade actives across ASEAN, where Solvay and Nouryon recently added capacity. Contract manufacturing hubs in Thailand and Vietnam cater to regional and Australian requirements, and ISO 22716 certification is becoming a passport for premium-brand entry.

North America remains an innovation center, though growth trails global averages. MoCRA mandates facility registration and adverse-event reporting, adding 8-12% compliance overhead for mid-tier formulators. California’s Proposition 65 and forthcoming New York disclosure rules increase state-level complexity, while Canadian harmonization supports cross-border trade. Europe’s REACH and Cosmetics Regulation continue to shape global standards; recent restrictions on octocrylene, homosalate, and parabens pivot R&D toward mineral UV filters and microbiome-friendly preservatives. Germany, France, and the United Kingdom spearhead RSPO adoption, and Nordic countries pioneer waterless formats and circular-economy sourcing.

South America and Middle-East and Africa contribute smaller share but show niche potential. Brazil’s ingredient imports are growing, supporting textured-hair surfactants and conditioning agents. Argentina’s volatile macro climate curbs demand, but local soy- and sunflower-based surfactants serve regional needs. Gulf Cooperation Council markets combine high disposable income with halal and water-conservation priorities, boosting anhydrous formats suited to arid climates. South Africa’s brands exploit indigenous botanicals such as marula and rooibos for local and export use, reinforcing biodiversity as a differentiator in the personal care chemicals market.

Value Chain Analysis

The personal care chemicals value chain begins with upstream feedstocks from petrochemicals (naphtha-derived ethylene/propylene, ethylene oxide) and oleochemicals (palm and coconut derivatives), along with biotech inputs (sugars and fermentation nutrients) used for newer bio-based surfactants and actives. Ingredient manufacturers then synthesize or blend surfactants, emulsifiers, emollients, rheology modifiers, preservatives, UV filters, and higher-value actives such as peptides and bio-identical proteins. These ingredients flow into brand and contract-manufacturer formulation plants that convert them into finished personal care products.

Downstream, supply is split between direct sourcing by large multinational brands and a fast-growing channel of specialty distributors and digital portals serving smaller, e-commerce-led brands that purchase in smaller lots. Recent distributor consolidation and capability upgrades, such as Safic-Alcan expanding its North American platform via the Deveraux Specialties acquisition and DKSH Performance Materials acquiring Italy-based Gale and Cosm, underline how regional distributors support formulation work, manage regulatory documentation, and enable just-in-time delivery. The chain remains sensitive to logistics and packaging availability, where freight volatility and plastic resin constraints can extend lead times and increase working capital needs for both ingredient suppliers and brand manufacturers.

Competitive Landscape

The personal care chemicals market displays moderate concentration: the top 5 suppliers—BASF, Croda, Evonik, Dow, and Ashland—held roughly 42% revenue share in 2025. Incumbents are buying sustainable-ingredient specialists to secure COSMOS and RSPO portfolios, epitomized by Croda’s 2024 purchase of Alban Muller. Biotech startups like Amyris, Genomatica, and Geltor commercialize fermentation-derived squalene, collagen, and peptides at near-petrochemical cost, eroding legacy advantages. Technology platforms are decisive: L’Oréal’s SimplifIA and Unilever’s Digital Twin shorten formulation cycles, allowing proprietary blends that lock rivals out of fast-moving niches. Regulations favor vertically integrated players with full traceability, and smaller surfactant and emollient manufacturers face margin pressure that may accelerate further consolidation.

Patent filings in encapsulation and peptide synthesis jumped 18% during 2024-2025, signaling intensifying R&D competition. ISO TC 217 and ASTM develop test methods for microbiome safety and biodegradability, shaping next-generation ingredient standards. White-space opportunities persist in reef-safe UV filters, microbiome-friendly preservatives, and waterless-format actives where supply is tight and demand robust. Given that the combined top-five share remains below 50%, the competitive field is dynamic but not dominated by a single firm, sustaining healthy innovation within the personal care chemicals market.

Personal Care Chemicals Industry Leaders

BASF

Dow

Evonik Industries AG

Croda International Plc

Ashland

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Reformulation pressure and substantiation requirements are creating opportunities for suppliers that can offer compliant, documentation-ready alternatives to restricted or scrutinized ingredients, with especially clear demand in Europe. Regulation (EU) 2026/909 introduces new bans and restrictions, including Triphenyl Phosphate and limits for certain fragrance allergens, while Regulation (EU) 2026/78 tightens the finished-product warning threshold for formaldehyde to 0.001% (10 ppm), effective 15 July 2026. This sequence of regulatory changes is lifting demand for preservative systems, fragrance design approaches, and multifunctional additives that can meet performance targets while reducing labeling and compliance friction.

Biotechnology-enabled actives and biosurfactants are also broadening from niche sourcing into more regular innovation roadmaps, with both named commercial and pre-commercial programs. Ajinomoto is developing fermentation-based amino-acid biosurfactants using sugars instead of petroleum or palm oil, with prototype shipments planned for 2026, and Kensing is introducing an upcycled biosurfactant platform based on microbial fermentation of edible-oils side streams. BASF, with Bota Biosciences, is launching a bio-identical recombinant Collagen III fragment for skin care positioning. In parallel, suppliers are expanding branded bio-based ingredient lines, including Wacker Chemie launching the BELNEXT brand (a cationic emulsifier and an emollient), which supports procurement focused on traceability, carbon-footprint disclosure, and premium positioning across skin care, hair care, and concentrate or waterless formats driven by water scarcity.

Recent Industry Developments

- June 2026: BASF and Bota Biosciences commercially launched SkinNexus Collag3n, a 100% human-identical recombinant Collagen III fragment produced via AI-enabled biomanufacturing. The launch reinforces the shift toward clinically positioned, fermentation-derived actives and provides a scalable alternative to animal-derived collagen inputs for premium skin care formulations.

- November 2025: Evonik finalized the divestment of its betaines business in Bekasi, Indonesia, to Aekyung Chemical Co., Ltd. The transaction reshapes supply in a key surfactant category and signals portfolio reallocation toward higher-value personal care specialties, while transferring the regional manufacturing footprint and customer relationships to the new owner. The change concentrates regional surfactant supply and redefines customer access in Southeast Asia.

- September 2024: L'Oreal Groupe, Abolis Biotechnologies, and Evonik entered into a tri-party agreement to scale the development and manufacturing of next-generation bio-based ingredients. The partnership links brand demand with industrial biotech scale-up and specialty chemical production, advancing commercialization pathways for fermentation-derived personal care ingredients.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of chemicals and ingredients used to formulate personal care products, where demand is created by finished goods such as skin care, hair care, makeup, fragrances, oral care, and toiletries.

Scope exclusions: We exclude packaging materials, finished personal care product retail value, and third-party manufacturing services that are not sold as chemical ingredients.

Segmentation Overview

- By Ingredient

- Inactive Ingredients

- Surfactants

- Emulsifiers

- Emollients

- Colorants and Preservatives

- Rheology Control Agents

- Other Inactive Ingredients

- Active Ingredients

- Conditioning Agents

- UV Ingredients

- Anti-ageing Agents

- Exfoliants

- Other Active Ingredients

- Inactive Ingredients

- By Application

- Skin Care

- Hair Care

- Make-up

- Fragrances

- Oral Care

- Toiletries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping the ingredient universe and the demand drivers behind it, before any numbers were modeled. We leaned on public sources such as the US FDA (including MoCRA updates), the European Commission materials on the EU Cosmetics Regulation, and national statistics offices for production and trade direction.

To keep assumptions realistic, we also reviewed sources such as UN Comtrade trade series, World Bank macro indicators, and peer reviewed journals that discuss surfactants, preservatives, UV filters, and other cosmetic ingredients. Company annual reports, investor presentations, and credible industry press were used to understand portfolio mix shifts and pricing commentary. For areas where public disclosures are thin, we used paid database subscription sources for company financials, patent databases, and shipment level import-export data to confirm activity patterns and avoid double counting. These desk sources are illustrative rather than exhaustive, and additional public references were used throughout to collect, cross-check, and clarify specific data points.

Primary Interviews and Surveys

Primary inputs were collected from ingredient suppliers, formulators, and downstream buyers, so gaps in public pricing and mix could be closed with real market context. We tested application level demand signals across APAC, EMEA, and the Americas, and then rechecked sensitive assumptions such as active ingredient adoption, surfactant price cycles, and regulatory driven reformulation impacts.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 37% |

| Mid tier: 48% | Functional/Unit leaders: 41% | EMEA: 36% |

| Smaller Players: 21% | Managers: 47% | Americas: 27% |

Market-Sizing & Forecasting

The core model uses a top-down approach where personal care finished goods activity is translated into an ingredient demand pool through usage intensity and formulation shifts, and then sized in USD. To keep totals grounded, we corroborated outputs with selective bottom-up checks, such as sampled volume by ingredient family multiplied by typical price bands, followed by channel checks on where the material is sold.

Key inputs included the pace of skin care and hair care consumption, the mix shift between inactive and active ingredients, and adoption rates of functions such as UV protection and anti-aging actives. We also tracked feedstock linked movement for major ingredient families, for example surfactants and emollients, reformulation triggers tied to cosmetics regulation updates, and regional manufacturing and trade direction that can move supply availability. When interview feedback suggested a structural change, such as faster penetration of fermentation based actives, the assumptions were adjusted and rerun.

For forecasting, scenario analysis was used, with base, conservative, and upside views built from macro demand direction, regulatory timing, and expected price normalization. Where bottom-up checks had gaps, we used ranges from comparable applications and then narrowed them through expert feedback, so the final totals remained traceable and repeatable.

Data Validation & Update Cycle

Validation was done through multiple checks so the final values do not depend on a single data stream. Our team compared outputs against independent signals such as trade direction, public company commentary on volumes and pricing, and observed shifts in key applications, and then outliers were investigated before sign-off.

If a variance was large, the step that created it was revisited, and we re-contacted selected respondents to confirm whether it reflected real market movement or a modeling issue. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes or sharp feedstock price swings. Before a client receives the report, a fresh review pass is completed so the latest available information is reflected in the final numbers.

Mordor Intelligence's Personal Care Chemicals Market Estimate Compared With Other Published Estimates

Published market sizes for personal care chemicals can look different even when they refer to the same topic, because the included ingredient set, the year used for pricing, and the way actives are treated are not consistent across sources.

The table shows a noticeable spread in current and forecast values, and in Mordor Intelligence's model the market is counted as ingredient value across inactive and active chemical families used in personal care applications, rather than mixing in finished product value or adjacent service revenues. Differences also come from how each publisher treats price progression for surfactants and emollients during feedstock swings, whether regulatory driven reformulation is modeled as a mix shift or a volume jump, and how often currency conversion rates are refreshed in the time series.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.45 B (2025) | |

| Industry Publisher A | USD 16.60 B (2024) | Uses an earlier base year and a longer horizon, and the definition leans toward broader end-use framing, which can shift what is counted as chemical value versus downstream spending. |

| Trade Journal B | USD 13.63 B (2022) | Relies on an older starting point and a lower growth assumption set, with fewer explicit checks on mix upgrades in actives and regulatory led reformulation timing across regions. |

Taken together, the variance is largely explained by scope boundaries, base year selection, and how pricing and mix are moved forward over time. By keeping the model tied to clear ingredient families, application demand signals, and repeatable pricing assumptions that can be rechecked in interviews, we end up with a balanced number that is easier for decision makers to use and revisit.

Key Questions Answered in the Report

What is the projected size of the personal care chemicals market by 2031?

The market is forecast to reach USD 23.30 billion by 2031, expanding at a 4.94% CAGR during 2026-2031.

Why is Asia-Pacific the fastest-growing region for personal care chemicals?

Rising disposable income, streamlined Chinese NMPA rules, and robust K-beauty exports are propelling a 6.12% regional CAGR through 2031.

What regulatory changes are most affecting North American suppliers?

The Modernization of Cosmetics Regulation Act (MoCRA) requires U.S. facility registration by the end of 2024 and mandates adverse-event reporting starting 2025, adding 8-12% compliance overhead for mid-tier formulators.

Which application segment is expected to record the highest CAGR through 2031?

Oral care leads with a 5.46% CAGR on the back of fluoride alternatives, probiotic actives, and new whitening technologies.

Page last updated on: