Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

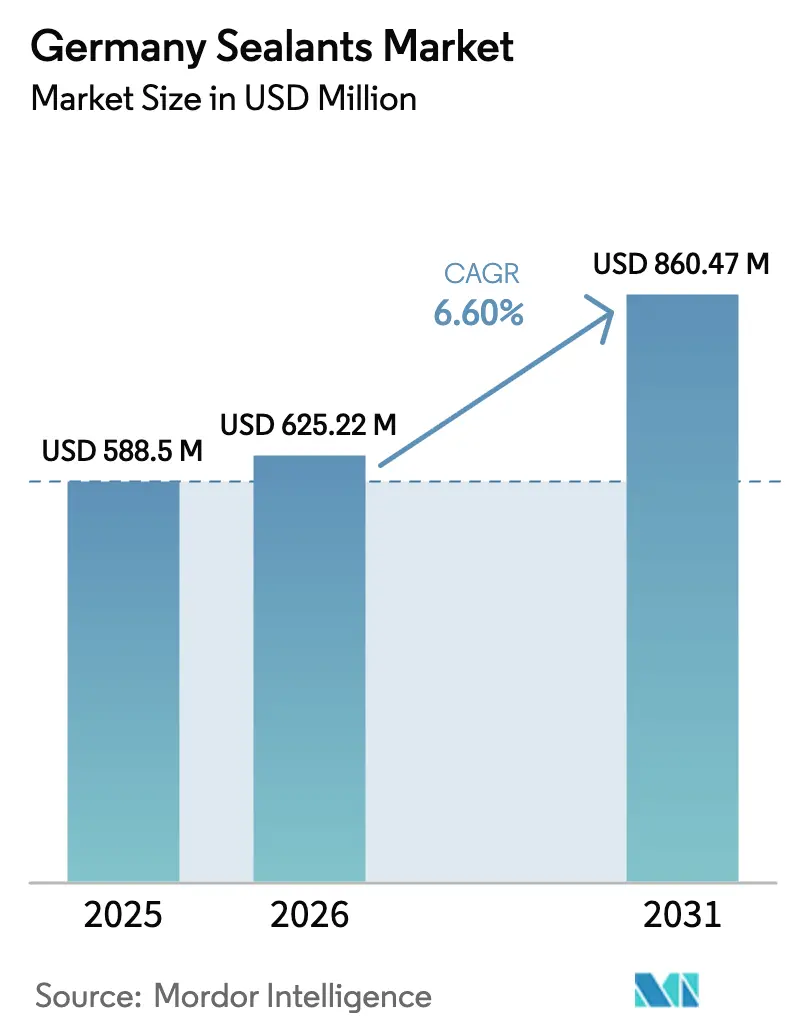

| Base Year Market Size (2025) | USD 588.5 Million |

| Market Size (2026) | USD 625.22 Million |

| Market Size (2031) | USD 860.47 Million |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Sealants Market Analysis by Mordor Intelligence

The Germany Sealants Market size was valued at USD 588.5 million in 2025 and is estimated to grow from USD 625.22 million in 2026 to reach USD 860.47 million by 2031, at a CAGR of 6.60% during the forecast period (2026-2031). The pivot toward high-performance chemistries is being pulled by Germany’s EUR 500 billion infrastructure plan, a strengthening pipeline of thermal-retrofit projects, and the rapid electrification of the domestic automotive supply chain. At the same time, the Blue Angel ecolabel, the EU Construction Products Regulation digital-passport mandate, and tightening Bauordnungen VOC limits are steering procurement toward silane-terminated polymer (STP) and other isocyanate-free technologies. Suppliers able to document lower embodied carbon and certified indoor-air emissions are winning specification contests in publicly funded bridge, tunnel, rail, and social-housing works. Feedstock volatility for silicone dimethyl carbonate and isocyanates remains the leading cost risk, yet technical-service intensity and multi-year framework agreements allow leading vendors to preserve pricing power in specialty grades.

Key Report Takeaways

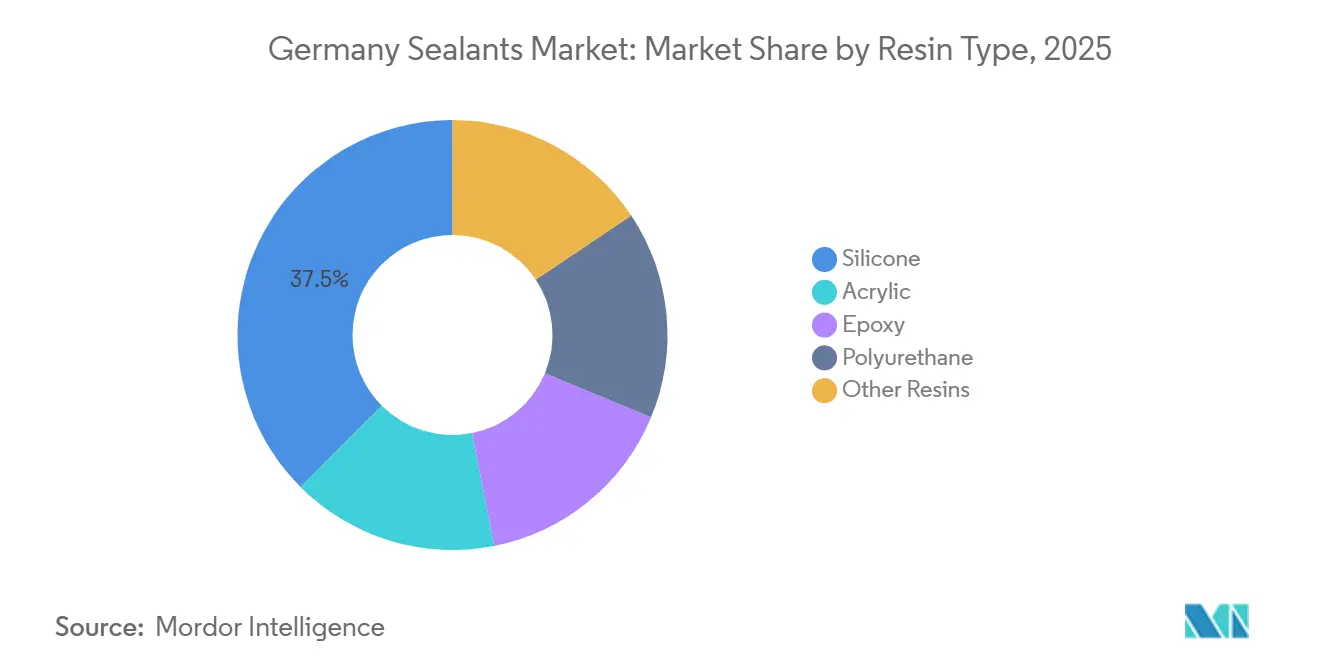

- By resin type, silicone held 37.5% of the Germany sealants market share in 2025. Polyurethane is forecast to post the fastest 7.24% CAGR through 2031.

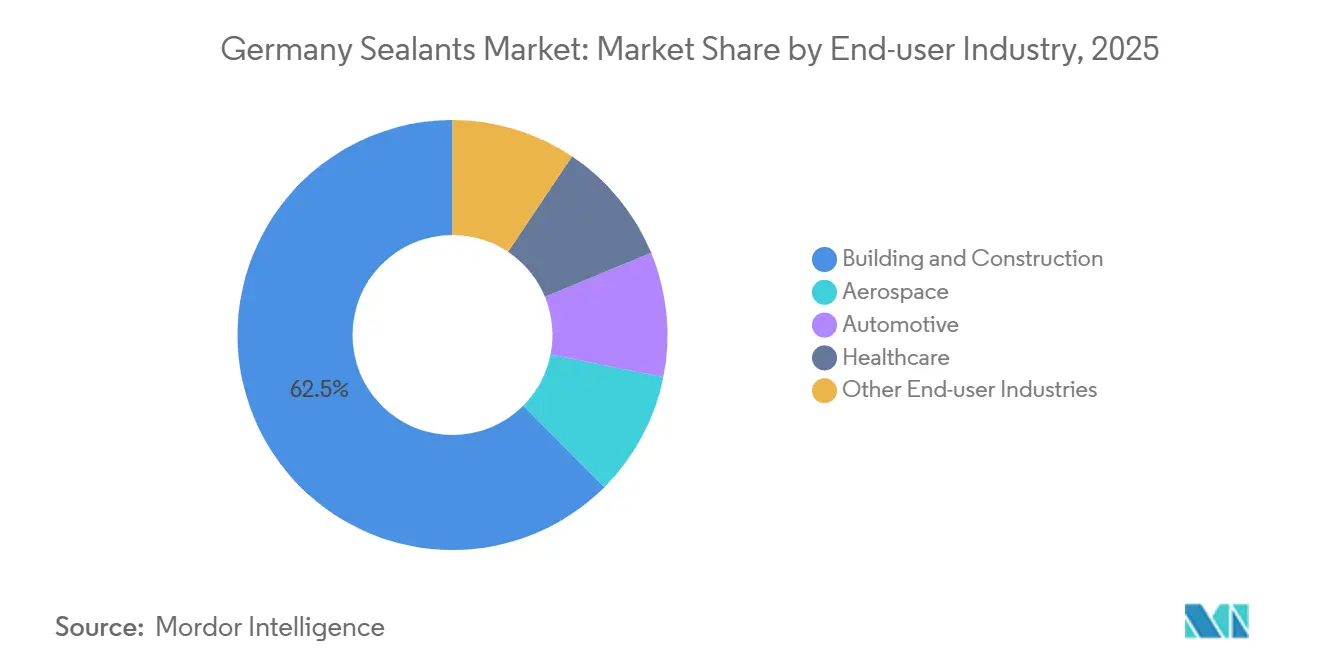

- By end-user industry, building and construction commanded 62.5% of the Germany sealants market size in 2025. Healthcare is projected to expand at an 7.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction boom in energy-efficient renovations | +1.8% | National, with concentration in North Rhine-Westphalia, Bavaria, Baden-Württemberg | Medium term (2-4 years) |

| Automotive lightweighting and e-mobility gasketing needs | +1.5% | National, export-oriented production clusters in Baden-Württemberg, Lower Saxony | Short term (≤ 2 years) |

| Healthcare single-use devices and pharma packaging growth | +1.2% | National, with research and development hubs in Bavaria, Hesse | Medium term (2-4 years) |

| Stricter Bauordnungen pushing low-VOC / bio-based sealants | +1.0% | National, early adoption in Berlin, Hamburg, Bremen | Long term (≥ 4 years) |

| Offshore wind-turbine blade repair sealants demand | +0.9% | Northern coastal states (Lower Saxony, Schleswig-Holstein, Mecklenburg-Vorpommern) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Construction Boom in Energy-Efficient Renovations

Germany’s renovation-rate gap, 0.67% in 2025 versus the 2% policy target, creates pent-up demand for airtight membranes, window-frame expansion joints and façade seals that survive -20 °C to +80 °C without plasticizer migration[1]Building Energy Act targets and renovation rate,” Federal Ministry for Economic Affairs and Climate Action, bmwk.de. The EUR 500 billion modernization plan earmarks EUR 2 billion a year to 2029 for social-housing upgrades plus EUR 3.25 billion for bridge and tunnel refurbishment, locking in multi-year visibility for infrastructure-grade sealants. BEG subsidies extend to 2029 and now cover photovoltaic penetrations, heat-pump ducts and mechanical-ventilation interfaces, each requiring specialized gaskets. Digital product passports under CPR 2024/3110 start phasing in from 2026, forcing vendors to disclose embodied-carbon and recyclability credentials that already influence public tenders. Sika’s low-emission systems on Munich’s Marienhof S-Bahn project illustrate how lifecycle reporting is turning sustainability data into a hard-bid differentiator.

Automotive Lightweighting and E-Mobility Gasketing Needs

Battery housings, power-electronics cases and cell-to-pack designs impose dielectric strength above 20 kV/mm and coolant resistance from -40 °C to +105 °C, prompting a switch to isocyanate-free polyurethane and STP chemistries that also meet upcoming PFAS restrictions. Henkel’s Düsseldorf Battery Engineering Centre enables rapid prototyping of thermal-interface and sealing compounds customized for multi-material bodies[2]Battery Engineering Centre Düsseldorf,” Henkel, henkel.com. ElringKlinger’s MetaloBond hybrid gasket delivers peel strength over 15 N/mm at 200 °C, supporting high-speed e-motor housings. Germany’s Tier-1s increasingly export these solutions to Chinese EV makers, expected to hold one-third of global sales by 2030, amplifying growth beyond domestic vehicle production. Early movers with flame-retardant, voltage-isolation compliant platforms are locking in global design wins that underpin the Germany sealants market long term.

Healthcare Single-Use Devices and Pharma Packaging Growth

Oliver Healthcare Packaging’s 2025 launch of LumaPeel peelable films at Wiggensbach targets ISO 11607 sterile-barrier systems for injectable-drug pouches and implant kits. Henkel’s 2026 buyout of ATP Adhesive Systems adds water-based tapes for diagnostic strips, wound dressings, and transdermal patches, opening a high-margin adjacency outside traditional construction sealants. Single-use bioreactors replacing stainless steel drive demand for gamma-stable, leachables-controlled sealants that operate after 25-50 kGy irradiation. EMA extractables guidance under ICH Q3D favors suppliers with complete ISO 10993 data sets, effectively raising entry barriers and consolidating the Germany sealants market around established global players. Investment in cleanroom compounding and analytical labs translates into price premiums that offset raw-material inflation.

Stricter Bauordnungen Pushing Low-VOC / Bio-Based Sealants

The Umweltbundesamt indoor-air target of 950 µg/m³ TVOC and Blue Angel ≤1% VOC threshold are steering buyers toward water-dispersion and moisture-cure products. CPR digital-passport rules add embodied-carbon transparency from 2026, making bio-attributed inputs a procurement plus. BASF’s 2026 biomass-balance polyether polyols, certified under ISCC PLUS, permit drop-in replacement of fossil feedstocks in CASE applications without reformulation penalties. Sika and BASF’s Baxxodur EC 151 epoxy hardener achieves up to 90% VOC reduction, satisfying contractor concerns over confined-space application. Industry groups are lobbying to adjust TVOC test protocols that currently penalize low-toxicity plant-based terpenes, an unintended barrier to wider bio-content adoption.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile isocyanate and silicone feedstock prices | -1.3% | Global, acute impact on German import-dependent producers | Short term (≤ 2 years) |

| Availability of high-performance pressure-sensitive tapes as substitutes | -0.8% | National, concentrated in automotive and electronics assembly | Medium term (2-4 years) |

| EU micro-plastic restriction proposals for reactive resins | -0.6% | EU-wide, with Germany as early compliance leader | Medium term (2-4 years) |

| Skilled-labour shortage for correct sealant installation | -0.5% | National, particularly acute in Bavaria, Baden-Württemberg, North Rhine-Westphalia construction markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Isocyanate and Silicone Feedstock Prices

Silicone DMC climbed 28% year-on-year in Q1 2026 as solar-grade demand hit 28% of total silicone output while Dow’s Barry, Wales shutdown removed 150 kt of European supply. China provides over 70% of silicon metal, leaving German formulators exposed to Xinjiang and Sichuan power rationing disruptions. Parallel spikes in TDI and MDI, driven by oil volatility and environmental inspections, squeeze polyurethane margins. Firms lacking backward integration are retreating from commodity caulks to focus on the specification-led Germany sealants market, but mid-tier players still face working-capital strain from longer raw-material lead times.

Availability of High-Performance Pressure-Sensitive Tapes as Substitutes

Die-cut acrylic-foam and silicone tapes eliminate mixing and cure stages, cutting labor on automotive body-in-white or electronics-module lines. Henkel’s ATP acquisition underscores the strategic shift toward tape platforms that offer immediate handling strength and automation-friendly processing. Nevertheless, tapes cost up to 30% more per linear meter, cannot fill gaps, and lose hold above +150 °C, preserving liquid-sealant dominance in façade expansion joints, battery packs, and engine bays. Hybrid approaches, pre-applied tape gaskets with over-beaded liquid sealant, are likely to coexist, limiting but not displacing growth of the Germany sealants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Hybrid Silanes Accelerate Polyurethane Upswing

Polyurethane formulations are growing at 7.24% CAGR through 2031, anchored by STP hybrids that eliminate isocyanate handling. Silicone maintained a 37.5% Germany sealants market share in 2025 owing to unmatched -60 °C to +250 °C service windows in façade glazing and battery-pack gasketing. Wacker Chemie’s new STP-E line at Nünchritz adds 15 kiloton incremental capacity and illustrates a capital pivot into hybrids that bridge silicone UV stability and polyurethane toughness. Epoxy sealants keep a niche in industrial-floor joints and aerospace composite fuel tanks, while acrylics remain preferred for interior trim owing to paintability at low cost. Supplier research and development increasingly merges chemistries, epoxy-polyurethane networks or silane-modified polyethers, blurring hard resin boundaries yet widening application coverage across the Germany sealants market.

By End-User Industry: Construction Dominates, Healthcare Scales Value

Building and construction accounted for 62.5% of the 2025 Germany sealants market size, propelled by curtain-wall engineering excellence and an EUR 500 billion public-works queue. Healthcare is the fastest-growing segment with 7.56% CAGR during 2026-2031 as sterile packaging and single-use bioreactors multiply. Automotive demand pivots to battery enclosures and e-powertrain gaskets, sustaining spend even as ICE powertrains decline. Aerospace stays a low-volume, high-margin niche dependent on certified chemistries with 20-year life cycles. Electronics, white goods and marine collectively track GDP, while offshore wind repair gains outsized attention in coastal states, further diversifying the Germany sealants market.

Geography Analysis

Baden-Württemberg and Bavaria contribute a significant share of national value through dense automotive and life-science clusters that require premium polyurethane, silicone, and STP systems. North Rhine-Westphalia couples chemical production scale with retrofit-heavy urban stock, making it the single largest distribution hub in the Germany sealants market. Northern coastal states, led by Lower Saxony and Schleswig-Holstein, generate double-digit growth from offshore wind blade repair and shipbuilding sealants. Eastern states benefit from investment incentives; Wacker’s STP-E expansion in Saxony underscores shifting capacity eastward. Metropolitan retrofits in Berlin, Hamburg and Munich prioritize low-VOC, low-odor formulations to meet Blue Angel criteria, accelerating bio-based adoption. Landesbauordnungen in these cities also require intumescent cable-penetration and acoustic partition seals, increasing product-mix complexity and favoring suppliers with technical-service teams close to job sites. Overall, regional heterogeneity rewards multi-plant footprints and just-in-time logistics networks able to balance volume along Germany sealants market corridors.

Competitive Landscape

The Germany sealants market is moderately consolidated. Henkel’s EUR 270 million purchase of ATP shifts its mix toward water-based tapes for medical-device and electronics assembly, broadening beyond construction. Sika’s CHF 220 million Akkim deal extends reach into Eastern Europe and the Middle East while providing cross-selling of repair mortars alongside sealants, reinforcing the Germany sealants market export pillar. Wacker’s hybrid-polymer lines and BASF’s biomass-balance feedstocks illustrate feedstock strategy diversification responding to VOC and carbon scrutiny. Dow’s earlier Barry plant closure tightened silicone supply yet freed capital for higher-margin specialty elastomers. Regional challengers Tremco Illbruck and Otto Chemie defend contractor loyalty through fast delivery and field-tech support, especially for niche acoustical and glazing caulks. Startups exploiting CO₂-based polyurethane precursors or mussel-protein adhesion may disrupt long-term but remain below commercial scale.

Germany Sealants Industry Leaders

3M

Henkel AG & Co. KGaA

Sika AG

Wacker Chemie AG

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Henkel completed the acquisition of ATP Adhesive Systems, adding EUR 270 million in annual water-based tape revenue to its Adhesive Technologies portfolio.

- December 2025: Sika AG announced its "Fast Forward" strategic investment and efficiency program at an investor and media conference, targeting CHF 150-200 million (USD 169-225 million) in annual cost savings by 2028 through digital transformation, supply-chain strengthening, and operational efficiency improvements.

Germany Sealants Market Report Scope

Sealants are elastomeric materials used to fill gaps, joints, or cracks, preventing water, air, dust, and fluid passage. Widely applied in construction and industrial sectors, they ensure waterproofing and structural flexibility in buildings, windows, automotive components, and appliances.

The Germany sealants market is segmented by resin type and end-user industry. By resin type, the market is segmented into acrylic, epoxy, polyurethane, silicone, and other resins. By end-user industry, the market is segmented into aerospace, automotive, building and construction, healthcare, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Resin Type

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Other Resins |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms