Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

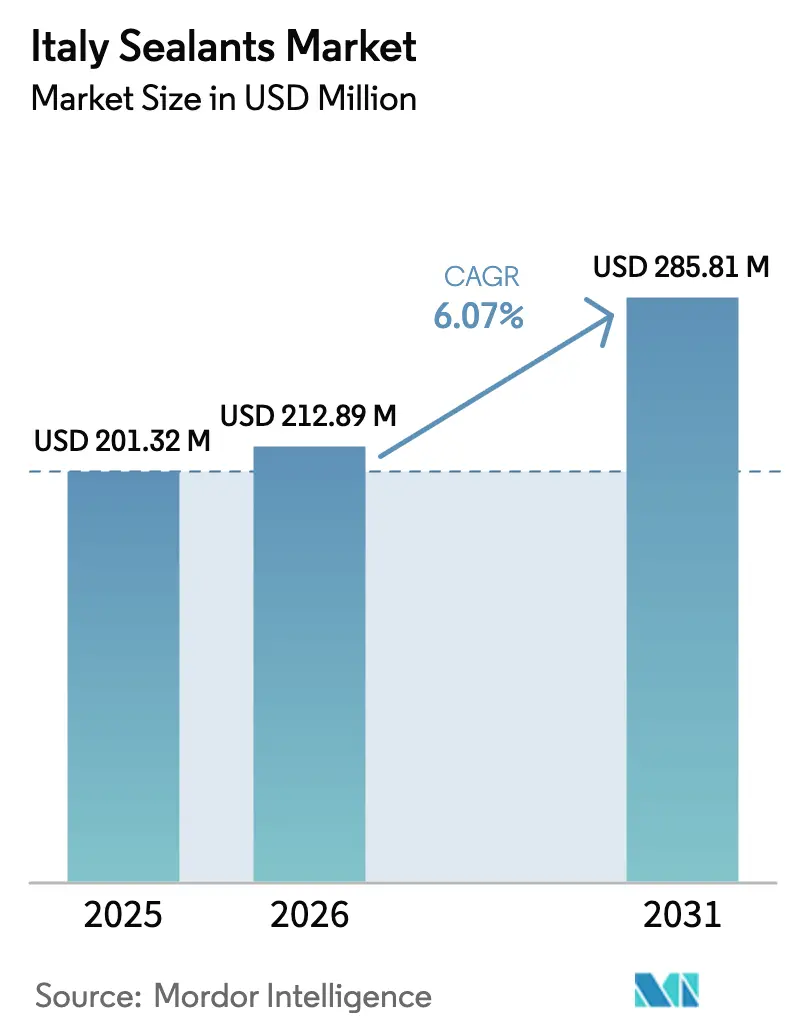

| Base Year Market Size (2025) | USD 201.32 Million |

| Market Size (2026) | USD 212.89 Million |

| Market Size (2031) | USD 285.81 Million |

| Growth Rate (2026 - 2031) | 6.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Sealants Market Analysis by Mordor Intelligence

The Italy Sealants Market size is expected to increase from USD 201.32 million in 2025 to USD 212.89 million in 2026 and reach USD 285.81 million by 2031, growing at a CAGR of 6.07% over 2026-2031. Higher retrofit spending under the Superbonus program, tightening VOC limits, and the pivot toward prefabricated building methods together elevate near-term demand across the Italy Sealants market while reshaping product specifications toward low-odor, waterborne chemistries. Construction incentives worth EUR 13.95 billion, channeled through the Renovation Wave initiative, anchor renovation volume and keep the Italy Sealants market tightly correlated with policy continuity. Rising healthcare construction and battery-assembly investments add specialized demand for disinfectant-resistant and thermally conductive grades, moving the Italy Sealants market into higher-value niches. Multinational formulators accelerate local capacity and acquisitions, seeking cost resilience against feedstock volatility and a labor market that increasingly favors factory-applied or pre-gasketed systems over on-site gun-grade installation.

Key Report Takeaways

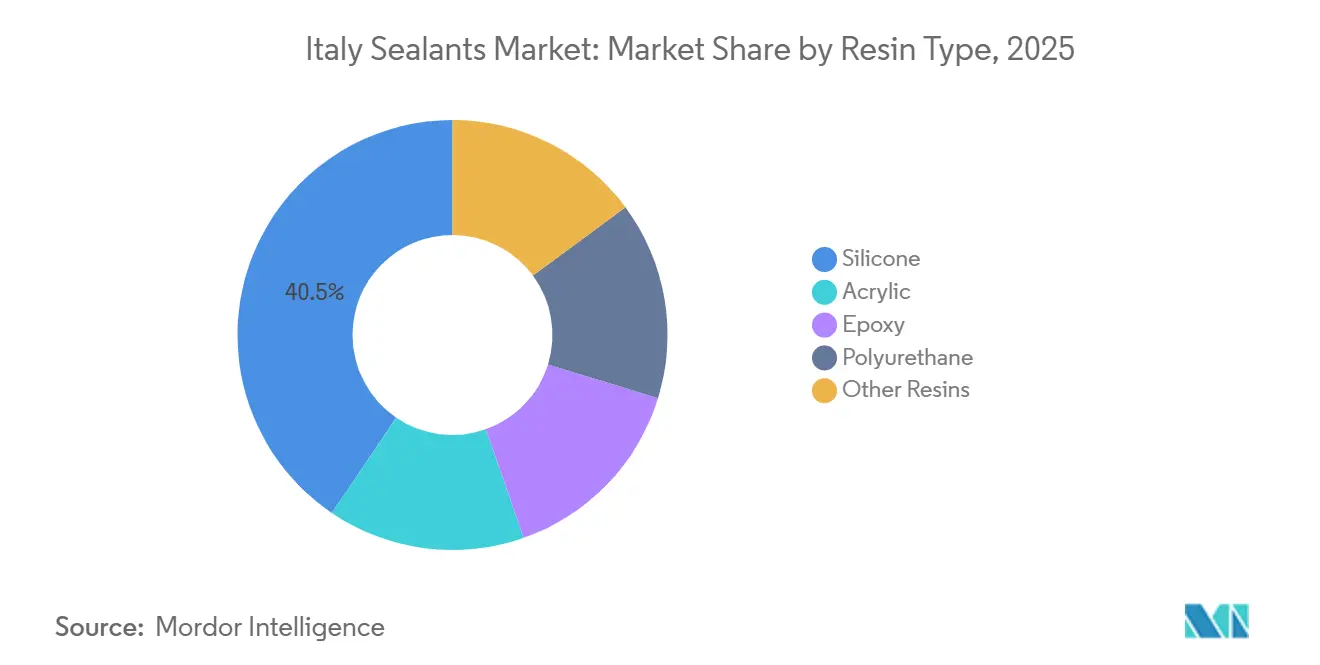

- By resin type, silicone led with 40.50% of the Italy Sealants market share in 2025, whereas acrylic is projected to record the fastest 7.12% CAGR through 2031.

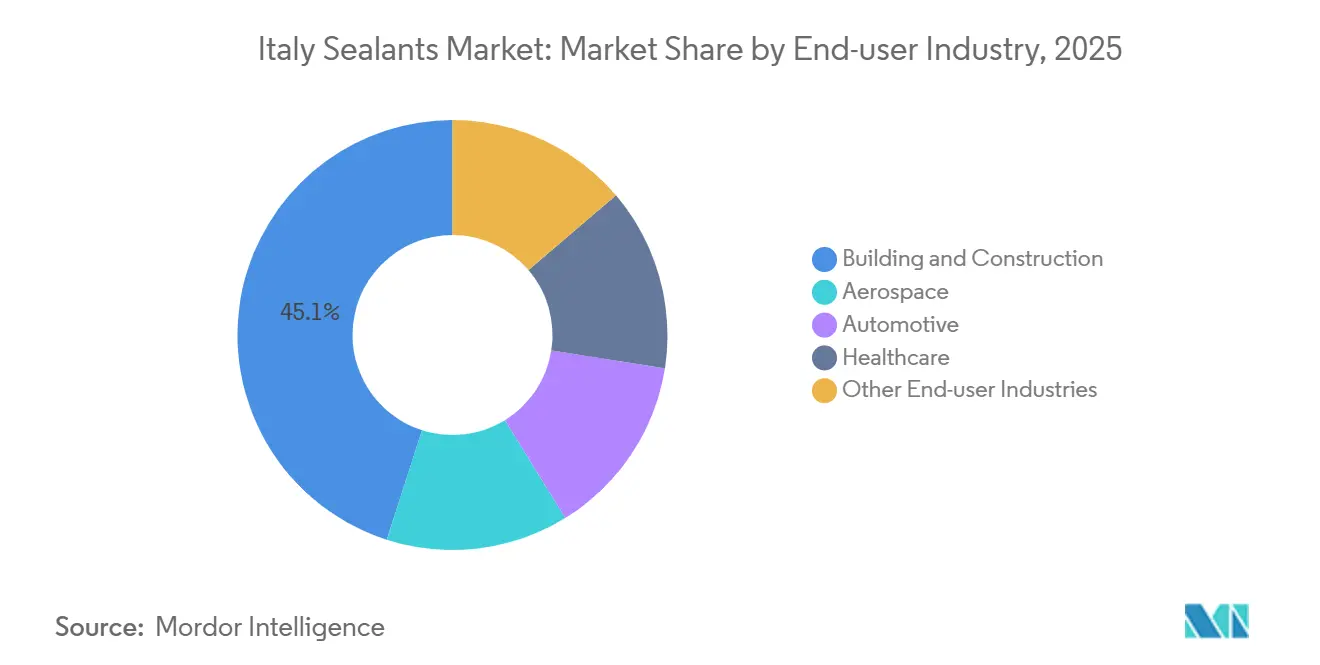

- By end-user industry, building and construction held 45.05% of the Italy Sealants market size in 2025, while healthcare is forecast to expand at a 7.40% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Renovation Wave-fuelled retrofit demand | +1.2% | National, concentrated in Lombardy, Lazio, Campania | Medium term (2-4 years) |

| EV-battery lightweighting sealant needs | +0.8% | National, with clusters in Piedmont (Turin automotive corridor) | Long term (≥ 4 years) |

| Stricter VOC limits accelerating water-based chemistries | +1.0% | EU-wide, Italy early adopter via Superbonus CAM criteria | Short term (≤ 2 years) |

| BIPV façades requiring edge-seal longevity | +0.7% | National, pilot projects in Milan, Rome, Bologna | Long term (≥ 4 years) |

| Robotic/3D-printed construction compatible hybrid sealants | +0.8% | National, early gains in Campania (Montalto di Castro), Emilia-Romagna | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Renovation Wave-Fuelled Retrofit Demand

Planned spending of EUR 13.95 billion under Italy’s Recovery and Resilience Plan covers more than 100,000 buildings and 36 million m² of upgrades, sustaining retrofit momentum for the Italy Sealants market[1]European Commission, “Recovery and Resilience Facility,” ec.europa.eu . The 2026 budget continues a 50% tax bonus on primary-residence renovations, guaranteeing steady pull-through for acrylic and low-VOC polyurethane systems. EN 16516 and CDPH v1.2 thresholds (less than or equal to 300 µg/m³ total VOC and less than or equal to 10 µg/m³ formaldehyde at 28 days) tighten qualifying formulations, favoring waterborne products that also mitigate amine-cure odor. Lombardy, Lazio, and Campania together host nearly half of the eligible building stock, concentrating logistics advantages for distributors with dense regional hubs. Demand shifts away from conventional silicone façade joints toward hybrid sealants able to bond mixed legacy substrates without primers, reducing skilled labor hours in a market already short 265,000 workers.

EV-Battery Lightweighting Sealant Needs

Stellantis targets a 50% battery-weight cut by 2030 and has invested USD 40 million in a Turin Battery Technology Center that boosts local demand for thermally conductive and dielectric sealants[2]Stellantis, “Battery Technology Center Turin,” stellantis.com. Current electric vehicles carry roughly 8 lb of adhesives and sealants; new cell-to-pack designs may lift content toward 12 lb by 2030, supporting long-run volume upside for the Italy Sealants market. Two-component polyurea systems from Collano deliver 30-s fixture times, eliminating mechanical fasteners in modules now entering series production. Dow’s VORATRON polyurethane grades add 0.3-3.1 W/mK thermal conductivity, allowing passive cooling that slashes pack weight and volume. These specifications demand service from -40°C to 85°C and dielectric strength more than or equal to 20 kV/mm, steering formulators toward silicone and specialty polyurethane chemistries.

Stricter VOC Limits Accelerating Water-Based Chemistries

Revised EU Ecolabel criteria, effective February 2026, cap total VOC at 300 µg/m³ and formaldehyde at 10 µg/m³, banning many solvent-borne sealants. BASF’s Acronal 5036 waterborne acrylic delivers more than or equal to 40% elastic recovery with less than or equal to 50 g/L VOC, matching silicone movement while remaining APEO-free. Acronal ECO 7806 offers no-ammonia, low-odor performance suitable for occupied retrofits. Superbonus CAM criteria adopt the same emissions tests, cementing regulatory pull in the Italy Sealants market. Waterborne systems face freeze-thaw hurdles in alpine regions, so dual-pack solutions retain share in colder provinces.

BIPV Façades Requiring Edge-Seal Longevity

Edge-seal durability governs power retention in building-integrated photovoltaics, demanding 25-year joint integrity under 200 thermal cycles from -40°C to 85°C. Pilot projects across Milan, Rome, and Bologna specify two-component silicone with Shore A 25-35, mitigating differential expansion between glass, aluminum, and concrete. Hybrid MS polymers win non-structural joints where paintability and fast cure lower façade installation cost. Italy’s National Recovery and Resilience Plan earmarks EUR 2.2 billion for renewables in buildings, encouraging BIPV adoption over rooftop arrays in historic centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silicone-monomer price volatility | -0.6% | Global, acute impact on Italy via import dependency | Short term (≤ 2 years) |

| CE-mark/CPR compliance cost burden for SMEs | -0.5% | EU-wide, disproportionate impact on Italian regional formulators | Medium term (2-4 years) |

| Trade-skills shortage shifting demand to pre-gasketed systems | -0.4% | National, concentrated in Veneto, Piemonte, Lombardy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Silicone-Monomer Price Volatility

Wacker Chemie raised silicone prices twice in 2026 after platinum catalysts doubled YoY and Middle-East feedstock disruptions reduced dimethyldichlorosilane supply, squeezing Italian formulators who import 85% of intermediates. Platinum represents up to 20% of silicone sealant COGS, and spot prices climbed from USD 900/oz in 2025 to USD 1,850/oz by March 2026. Dow’s announced closure of its Barry, UK, siloxanes unit in mid-2026 removes European capacity, amplifying cost swings that depress margins for regional firms such as Fassa Bortolo and Kerakoll.

CE-Mark/CPR Compliance Cost Burden for SMEs

The Construction Products Regulation 2024/3110 mandates Digital Product Passports and annual EN 15651 audits, costing SMEs EUR 15,000-25,000 per family while also demanding seismic-cycle testing under Italian NTC 2018 rules. Kerakoll’s planned Basilicata plant shows how vertical integration spreads compliance overhead across larger volumes. Blockchain traceability further advantages multinationals equipped with enterprise systems, quickening consolidation across the Italy Sealants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Gains on Silicone’s Weatherproofing Franchise

Silicone commanded a 40.50% hold on the Italy Sealants market share in 2025, supported by unrivaled UV stability across -60°C to 200°C service windows. The Italy Sealants market size for acrylic formulations is projected to climb at a 7.12% CAGR through 2031, buoyed by BASF’s waterborne Acronal 5036 that delivers more than or equal to 40% elastic recovery without amine-cure odor. Hybrid MS polymers and polysulfides together remain below 10% of volume, yet retain footholds in specialty joints such as airport pavements and submerged structures.

Acrylic’s rising penetration links directly to Superbonus CAM criteria that cap VOC at 50 g/L, a threshold that solvent-borne polyurethane struggles to meet without primer sacrifices. Polyurethane continues to dominate structural glazing with tensile strengths of more than 2 MPa and Shore A 40-60, crucial to industrial flooring and façade anchor joints. Epoxy holds a niche in pharmaceutical floors and cleanrooms, leveraging chemical impermeability despite mixing complexity.

By End-User Industry: Healthcare Outpaces Construction’s Volume Base

Building and construction represented 45.05% of the Italy Sealants market size in 2025, owing to sustained retrofit incentives. Healthcare facilities, however, are forecast to register a 7.40% CAGR through 2031 as LEED-targeted hospitals like Treviso demand low-emission, disinfectant-proof sealants meeting EN 16516 and CDPH v1.2. Automotive uptake intensifies around Turin, where cell-to-pack EV batteries spur demand for thermally conductive silicone and polyurethane grades.

Aerospace remains small yet lucrative, with Leonardo producing 2,700 A321 fuselage sections and adding A220 rear-fuselage lines that specify MIL-S-8802 compliant polysulfide fuel-tank sealants. Marine clusters in Tuscany and Liguria continue to use polyurethane deck sealants, resisting saltwater over 10-year cycles. Together, these shifts strengthen revenue density even as traditional building volumes flatten.

Geography Analysis

Northern provinces drive the majority of the total Italy sealants market demand, with Lombardy, Lazio, and Campania absorbing the lion’s share of the EUR 13.95 billion Superbonus allocation. Lombardy faces a 50% talent-shortage ratio, prompting rapid uptake of pre-gasketed façade panels that lower on-site labor intensity. Piemonte’s difficulty-to-fill rate compounds pressure in the automotive corridor, where Stellantis’s Battery Technology Center anchors a cluster of sealant-rich EV projects.

Southern regions show faster percentage growth as new plants from Kerakoll in Basilicata and MAPEI in Bari pull production capacity closer to high-growth local markets. Campania’s first 3D-printed earthquake-resistant factory demonstrates appetite for automated construction paired with hybrid sealants tailored for robotic dispensing. Alpine provinces impose freeze-thaw stress that keeps solvent- and two-component chemistries in use despite national VOC pressure.

BIPV pilots concentrated in Milan, Rome, and Bologna draw upon EUR 2.2 billion earmarked for building-integrated renewables, using long-life silicone edge seals to guarantee 25-year power warranties. Venice’s 56.34% foreign-worker share highlights demographic shifts that elevate products with visual cure indicators and simplified surface prep, further shaping regional product mix. Overall, southern catch-up growth offsets a steadier ascent in northern industrial hubs, averaging the national 6.07% CAGR that defines the Italy sealants market trajectory.

Competitive Landscape

The Italy Sealants market is moderately consolidated. Urethane hybrids compatible with automated metering now headline research and development roadmaps, promising quality consistency amid persistent labor shortages. Feedstock turbulence, led by platinum and siloxane volatility, nudges formulators toward backward integration, hedging, and strategic stockpiling, especially for SMEs (Small and Medium Enterprises) vulnerable to price spikes.

Italy Sealants Industry Leaders

Henkel AG & Co. KGaA

MAPEI S.p.A.

Sika AG

Soudal Holding N.V.

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Henkel AG & Co. KGaA announced a new generation of its Darex COV sealants in the global market (including Italy). These sealants do not contain phthalate-based plasticizers and ensure sealing of metal packaging with improved health and environmental credentials.

- May 2025: Italian Exhibition Group (IEG) and A151 teamed up to launch ADHESIVES BONDING & SEALANTS - ABS EUROPE 2026. This new event, dedicated to integrated technologies and solutions in the sealant and other bonding industry, is set for the Vicenza Expo Centre from October 27th to 29th, 2026.

Italy Sealants Market Report Scope

Sealants, flexible and paste-like, fill gaps, joints, and cracks between surfaces, effectively blocking air, water, moisture, and dust. Widely utilized in aerospace, construction, automotive, and healthcare, sealants protect joints. Unlike adhesives, sealants focus on providing water resistance and sealing, rather than structural bonding.

The Italy Sealants market report is segmented by resin and end-user industry. Byresin, the market is segmented into acrylic, epoxy, polyurethane, silicone, and other resins. By end-user industry, the market is segmented into aerospace, automotive, building and construction, healthcare, and other end-user industries. The market size and forecasts are provided in terms of value (USD).

By Resin Type

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Other Resins |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms