Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.34 Billion |

| Market Size (2026) | USD 3.55 Billion |

| Market Size (2031) | USD 4.89 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Sealants Market Analysis by Mordor Intelligence

The China Sealants Market size is expected to grow from USD 3.34 billion in 2025 to USD 3.55 billion in 2026 and is forecast to reach USD 4.89 billion by 2031 at 6.61% CAGR over 2026-2031. A progressive shift toward specialty chemistries for electric-vehicle assembly, photovoltaic modules, and high-density electronics is lifting average selling prices even as overall construction growth levels out. Regulatory tightening on volatile organic compounds (VOCs) is accelerating product reformulation, favoring low-VOC alcohol-cure silicones and reactive polyurethane hybrids that align with green-building codes. Upstream feedstock volatility, especially in dimethyl-cyclosiloxane and D4 intermediates, continues to squeeze gross margins of small and mid-sized producers that lack hedging tools or captive siloxane capacity. Meanwhile, multinationals are doubling down on local-for-local strategies, adding research and development centers and pilot lines that shorten development cycles and tailor performance to domestic standards. Mid-decade growth opportunities increasingly center on automation-ready, one-component UV-curable materials that support lights-out manufacturing and smart-factory validation, supporting a broader digitalization push within the China sealants market.

Key Report Takeaways

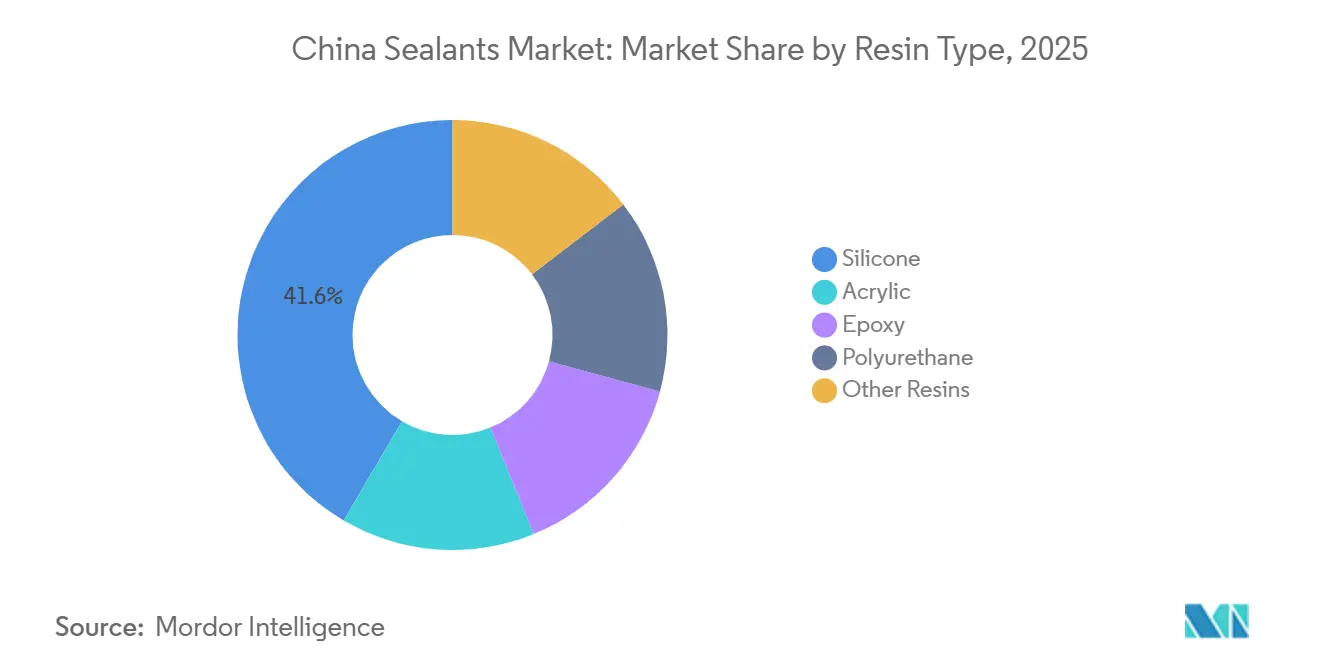

- By resin type, silicone sealants led with 41.55% of the China Sealants market share in 2025, while polyurethane is forecast to expand at a 7.56% CAGR through 2031.

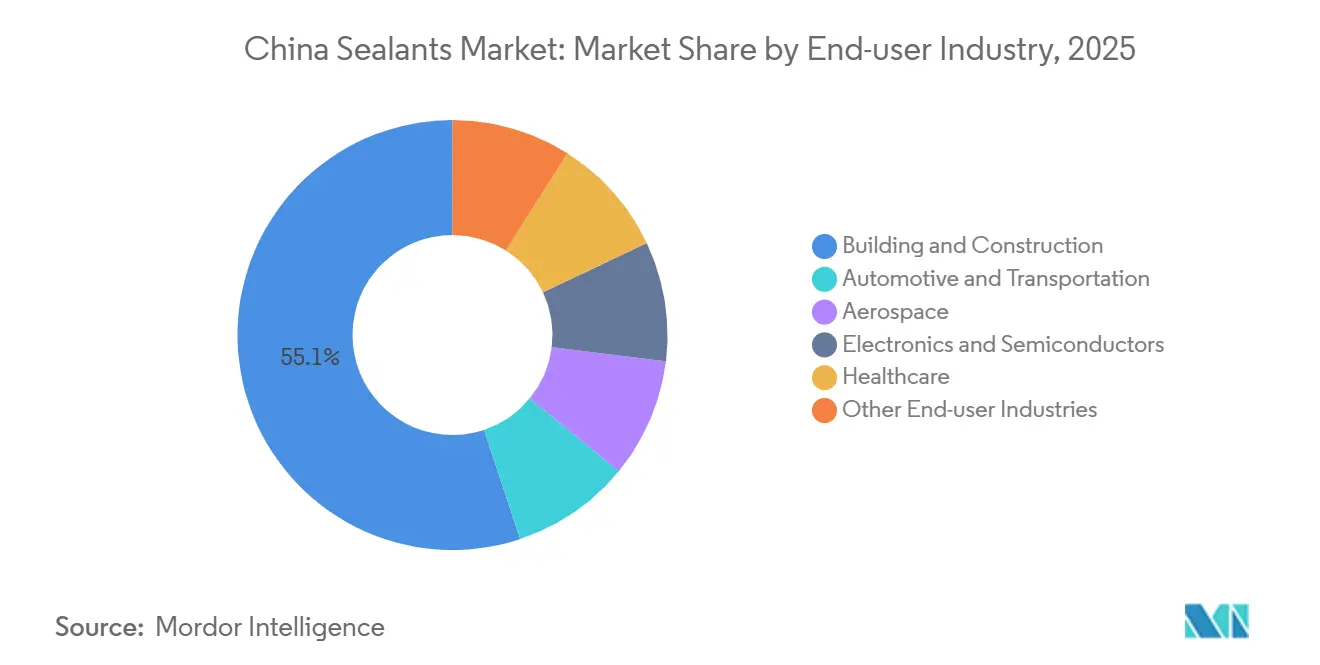

- By end-user, building and construction accounted for 55.10% of the China Sealants market size in 2025; electronics and semiconductors are advancing at a 7.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green-building code enforcement accelerates premium, low-VOC sealant demand | +1.2% | Nationwide, strongest in tier-1 cities and Yangtze River Delta | Medium term (2-4 years) |

| Automotive light-weighting drives multi-substrate bonding shift | +1.5% | Yangtze Delta, Pearl River Delta, Chengdu-Chongqing clusters | Medium term (2-4 years) |

| E-commerce warehousing boom raises floor-joint and cold-storage sealant use | +0.8% | Tier-2/3 logistics hubs, coastal cold-chain nodes | Short term (≤ 2 years) |

| Rapid expansion of China’s commercial aerospace MRO ecosystem | +0.4% | Shanghai, Xi’an, Chengdu bases | Long term (≥ 4 years) |

| Smart-factory adoption spurs one-component UV-curable sealants | +1.0% | Jiangsu, Shandong, Anhui, Hubei, Hunan, Guangdong | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Green-Building Code Enforcement Accelerates Premium, Low-VOC Sealant Demand

Mandatory national standard GB 30981.1-2025, effective June 2026, tightens limits on VOCs, semi-volatile compounds, biocides, and heavy metals in architectural coatings and accessory materials, forcing producers to reformulate or face higher environmental-protection taxes and provincial audits[1]State Administration for Market Regulation, “GB 30981.1-2025 Text,” samr.gov.cn. Life-cycle assessment requirements in group standard T/CBMF 297-2024 heighten procurement scrutiny for public-sector projects, propelling alcohol-cure silicones and water-based acrylics in curtain-wall and prefabricated-building joints. Complementary frameworks such as GB/T 35609-2025 embed environmental metrics into green-product labeling, accelerating market bifurcation where legacy oxime-cure silicones compete mainly on price in residential retrofit channels. Tier-1 cities are already mandating digital VOC-emission reporting via real-time monitoring, giving an early-mover advantage to companies that invested in low-emission pilot lines. As compliance costs rise, the China Sealants market increasingly rewards vertically integrated suppliers capable of rapid formulation pivots and cradle-to-gate traceability.

Automotive Light-Weighting Drives Multi-Substrate Bonding Shift

China’s electric-vehicle segment is migrating from mechanical fasteners to adhesive-intensive aluminum and mixed-material bodies to meet stringent range and efficiency targets. The automotive aluminum-alloy body connection-process market was roughly RMB 86 billion (USD 12 billion) in 2024 and is expected to climb to RMB 230 billion (USD 32 billion) by 2030 as aluminum-body penetration rises toward 40%[2]Sina Finance, “Aluminum-Body Connection Cost Forecast,” finance.sina.com.cn. Structural polyurethane adhesives are favored for ambient-temperature cure and vibration damping, supporting higher takt times on robotized lines. Flagship EV platforms such as the NIO ET7 feature more than 120 meters of crash-toughened structural adhesive per vehicle, a threefold increase from first-generation models. Domestic Tier-1s co-developing proprietary bonding recipes with automakers shorten design iterations and retain intellectual property in-country, strengthening the technology spine of the China Sealants market.

E-Commerce Warehousing Boom Raises Floor-Joint and Cold-Storage Sealant Use

Cold-chain storage capacity reached 277 million m³ in 2025, up 5.53% year-on-year, and refrigerated truck fleets expanded 19% to 587,900 units. National policy incentives subsidize county-level logistics parks, translating into higher consumption of flexible polyurethane and polysulfide sealants for insulated-panel joints and silicone gaskets for -30°C doors. MEDLOG’s March 2026 joint venture in Lingang integrates 80,000 tonnes of capacity with automated warehouse-management systems, illustrating how new projects bake in performance specifications such as -60°C glass-transition temperatures for floor joints. Every 10,000 m² of cold-storage flooring consumes roughly 2.5 tonnes of low-temperature-resistant acrylic sealant, offering a measurable volume lever for the China Sealants market.

Rapid Expansion of China’s Commercial Aerospace MRO Ecosystem

As COMAC C919 deliveries scale, domestic maintenance, repair, and overhaul (MRO) centers require polysulfide and polythioether sealants approved under Boeing- and Airbus-equivalent material specifications. Qualification cycles of three to five years create a high moat, but once approved, annual resealing demand for a narrow-body fleet of 500 aircraft can exceed 400 tonnes. Co-location of sealant pilot lines inside composite-fuselage fabrication parks in Shanghai and Xi’an reduces transport-induced shelf-life losses, positioning the China sealants market for a long-run aerospace annuity stream.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile silicone monomer pricing squeezes margins | -0.90% | National, affecting all silicone-dependent manufacturers | Short term (≤ 2 years) |

| Intensifying provincial environmental audits on solvent emissions | -0.60% | National, with strictest enforcement in Beijing-Tianjin-Hebei, Yangtze River Delta, Pearl River Delta | Medium term (2–4 years) |

| Over-capacity in low-grade construction silicones | -0.60% | National, particularly acute in interior provinces and tier-3/4 cities where commodity-grade products dominate | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Silicone Monomer Pricing Squeezes Margins

Spot prices for dimethyl-cyclosiloxane (DMC) jumped 20% in November 2025 to RMB 13,200 (USD 1,892.88) per ton after monomer producers coordinated 30% output cuts. Hydropower curtailments in Southwest China and higher industrial-silicon costs pushed quotes further to RMB 13,775 (USD 1,975.33) per ton by January 2026. Smaller formulators, lacking long-term contracts or financial hedges, saw gross margins compress by up to 450 basis points. Large integrated players such as Wacker leveraged captive siloxane capacity to buffer cost spikes, widening competitive gaps within the China Sealants market.

Intensifying Provincial Environmental Audits on Solvent Emissions

Following Ministry of Ecology and Environment guidance, local inspectors mandate continuous VOC (Volatile Organic Compound) monitoring and third-party safety reviews every three years for solvent-based production lines. Compliance retrofits, regenerative thermal oxidizers, activated-carbon beds, and solvent-recovery systems add 3%-6% to operating expenses for mid-sized plants. Non-compliant lines risk immediate shutdowns, driving a structural shift toward water-based and 100%-solids chemistries. As environmental levies expand to include more VOC species in 2026, solvent-heavy product portfolios risk stranded-asset write-downs, tempering near-term growth for parts of the China Sealants industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Silicone Dominance Faces Polyurethane Challenge

Silicone products commanded 41.55% of the China Sealants market share in 2025, supported by proven durability in curtain-wall glazing, façade panels, and photovoltaic modules. Polyurethane’s 7.56% forecast CAGR through 2031 is propelled by direct-glazing in new-energy vehicles and by cold-storage insulation panels that demand flexibility at sub-zero temperatures. Epoxy, acrylic, and MS-hybrid chemistries remain growth niches, yet MS-hybrids are adding 80 basis points of share per year thanks to isocyanate-free safety and faster green strength.

Silicone’s cost disadvantage widens when D4 intermediates surge, but formulation science, neutral-cure catalysts, adhesion promoters, and UV-stability packages continue to raise performance ceilings. Wacker’s Zhangjiagang specialty silicones hub supplies high-purity fluids initially imported from Germany, shortening lead times for electronics encapsulation grades. Domestic challengers, such as Guangzhou Jointas, are promoting MS-hybrids with Shore-A hardness tunable from 20 to 50 and primer-less adhesion to galvanized steel, a compelling proposal in modular-construction factories that switch substrates several times per shift. Over the forecast window, the China sealants market will tilt toward diversified resin portfolios rather than single-chemistry dominance.

By End-User Industry: Electronics Outpaces Construction

Building and construction absorbed 55.10% of 2025 demand, but its contribution to incremental volume will slide down by 2031 as real estate plateaus and infrastructure shifts toward maintenance. Electronics and semiconductors, the smallest end-user a decade ago, are now the fastest-growing at 7.88% CAGR during the forecast period (2026-2031), fueled by underfill and thermal-interface materials for AI accelerators and 5G base stations. Automotive and transportation remain the third pillar, its trajectory dictated by battery-pack design evolution and new safety codes that require flame-retardant, low-outgassing materials. Aerospace and healthcare combined account for very little of current consumption but produce gross margins 1.7-2.0 times construction products, sustaining R&D budgets and justifying certification investments.

Growing silicon-carbide power modules in EVs need thermal gels exceeding 6 W/mK conductivity while meeting vibration standards for 8-year/160,000 km warranties. Domestic suppliers such as Huitian introduced a 7 W/mK silicone gap filler in 2025, validated by a leading battery-pack assembler within six months. Such wins illustrate how the China Sealants market is becoming an innovation testbed rather than merely a volume-driven arena.

Geography Analysis

Regional consumption concentrates in three coastal megaclusters, yet is dispersing inland with industrial relocation. The Yangtze River Delta represents the majority of the national demand and is expanding at a steady yearly pace. A dense ecosystem of automotive plants in Shanghai and Suzhou, advanced semiconductor fabs in Wuxi and Kunshan, plus aggressive metro-rail projects, sustain broad-spectrum sealant uptake. Henkel’s EUR 60 million Inspiration Center in Shanghai employs more than 500 scientists who co-create specialty grades for domestic line qualifications, highlighting confidence in the corridor’s innovation depth.

The Pearl River Delta enjoys the highest electronics assembly density. Guangzhou Baiyun Technology’s 600-plus patent portfolio anchors regional technical leadership, and its participation in Guangzhou Baiyun International Airport Terminal 3 underlines construction credentials. Shenzhen’s EV battery hub further boosts demand for flame-retardant potting compounds, lifting polyurethane and MS-hybrid penetration.

The Bohai Rim, Beijing, Tianjin, Hebei, and Shandong lag coastal peers in growth but benefit from petrochemical feedstock synergies and government-led logistics hubs. Stricter environmental audits here accelerate low-VOC transitions faster than national averages. Interior provinces such as Sichuan, Chongqing, and Hubei offer double-digit consumption growth off a small base, as relocation policies attract electronics subcontracting and lightweight-vehicle assembly inland.

Uniform national regulations coexist with uneven enforcement. Tier-1 cities deploy real-time VOC sensors and levy fines within days of breaches, whereas some inland prefectures still rely on quarterly manual sampling. Consequently, premium low-VOC products are pulled into coastal regions first, then cascade inland as enforcement catches up. This staggered compliance curve lengthens the overall upgrade cycle of the China sealants market, smoothing demand volatility.

Competitive Landscape

The China Sealants market is moderately fragmented. Digital disruptors, typically spin-offs from university research labs, are piloting blockchain-enabled batch traceability and AI-driven viscosity control, challenging legacy producers that still rely on paper certificates and manual QC logs. Overall, innovation velocity is intensifying, and suppliers unable to meet fast prototype cycles risk being displaced, underscoring an increasingly dynamic China Sealants market.

China Sealants Industry Leaders

Chengdu Guibao Science and Technology Co., Ltd.

Sika AG

Dow

Henkel AG & Co. KGaA

Guangzhou Baiyun Technology Co, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: WACKER and SICO Performance Material inaugurated an application development center in Jining, China. The facility focuses on developing high-performance additives for plastics, coatings, and adhesives, with organofunctional silanes enhancing high-performance sealants' properties.

- September 2025: Henkel AG & Co. KGaA announced the opening of its new Inspiration Center for Adhesive Technologies in Shanghai. The site brings together more than 500 scientists and technical experts and supports customers across a broad range of industries with leading solutions in adhesives, sealants, and functional coatings.

China Sealants Market Report Scope

Sealants, flexible and paste-like, fill gaps, joints, and cracks between surfaces, effectively blocking air, water, moisture, and dust. Widely utilized in aerospace, construction, automotive, and healthcare, sealants protect joints. Unlike adhesives, sealants focus on providing water resistance and sealing, rather than structural bonding.

The China Sealants market report is segmented by resin and end-user industry. By resin, the market is segmented into acrylic, epoxy, polyurethane, silicone, and other resins. By end-user industry, the market is segmented into aerospace, automotive and transportation, building and construction, healthcare, electronics and semiconductors, and other end-user industries. The market size and forecasts are provided in terms of value (USD).

By Resin Type

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Other Resins |

By End-user Industry

| Building and Construction |

| Automotive and Transportation |

| Aerospace |

| Electronics and Semiconductors |

| Healthcare |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| By End-user Industry | Building and Construction |

| Automotive and Transportation | |

| Aerospace | |

| Electronics and Semiconductors | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms