Gaming Mouse Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

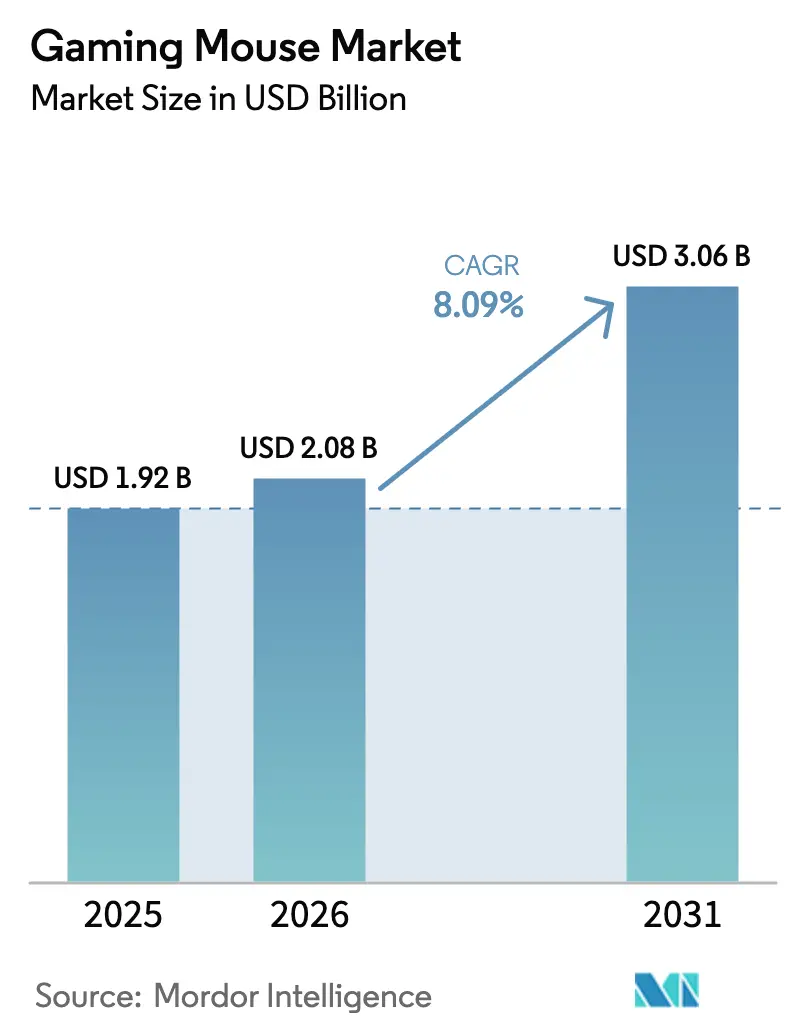

| Market Size (2026) | USD 2.08 Billion |

| Market Size (2031) | USD 3.06 Billion |

| Growth Rate (2026 - 2031) | 8.09% CAGR |

| Fastest Growing Market | Asia |

| Largest Market | Middle East |

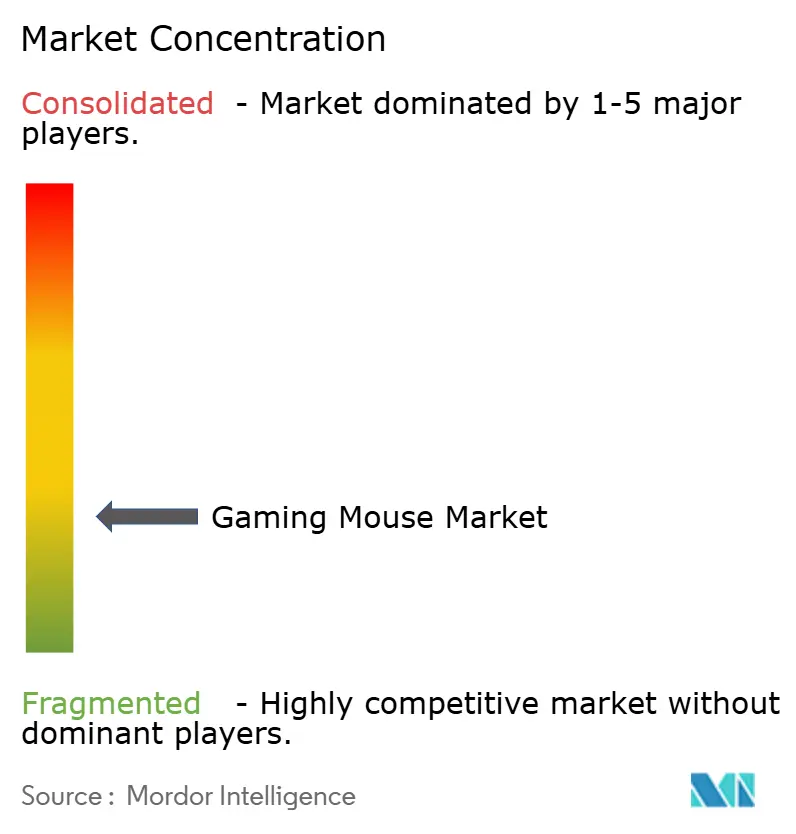

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gaming Mouse Market Analysis by Mordor Intelligence

The Gaming Mouse market size in 2026 is estimated at USD 2.08 billion, growing from 2025 value of USD 1.92 billion with 2031 projections showing USD 3.06 billion, growing at 8.09% CAGR over 2026-2031. Momentum held in 2024 even as desktop and console categories saw cyclical softness; single-digit declines in performance-mouse sell-through confirmed that this peripheral segment now upgrades on its own timetable, independent of full-system replacement cycles. An expanding calendar of amateur tournaments, the blurring of home-office and gaming desks, and consumers’ readiness to pay for innovations such as 8 kHz polling or magnesium-alloy shells keep revenue per unit rising. Premium positioning shields brands from raw-material swings, while geographically diversified production—sensors in East Asia, shells in ASEAN, final assembly near end-markets—continues to tighten lead times. As designers refine lighter frames and adaptive buttons, the mouse increasingly doubles as a style statement, mirroring sneaker and mechanical-keyboard culture and widening the Gaming Mouse market addressable base.

Key Report Takeaways

- By product type, FPS-oriented models led revenue in 2024, while MMO designs recorded double-digit growth during 2024-2025.

- By sensor technology, optical units held more than 80.78% of the 2025 share; laser variants showed a modest resurgence tied to hybrid office-gaming use.

- By connectivity, wired devices retained the largest slice, yet wireless registered the highest double-digit growth through 2024-2025.

- By price range, the USD 51-100 tier captured more than 60.58% of the 2025 Gaming Mouse market share, whereas the premium USD 150-plus tier logged the fastest growth.

- By distribution channel, online storefronts accounted for over 63.85% of 2025 shipments, but experiential retail zones foster loyalty for in-store buyers.

- By end-user, individual consumers dominated 2024 unit volumes; co-working gaming lounges delivered double-digit gains and now outpace other institutional demand groups.

- By geography, Asia-Pacific contributed nearly 49.42% of 2025 sales, whereas the Middle East is forecast to post the highest CAGR into 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gaming Mouse Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FPS-centric tournament boom | +2.1% | Asia-Pacific with global spillover | Medium term (2-4 years) |

| Customisable high-DPI wireless demand | +1.5% | North America, global influence | Short term (≤ 2 years) |

| Ultra-lightweight adoption | +1.3% | Europe first, global later | Medium term (2-4 years) |

| Laptop-bundle strategy in Middle East | +1.0% | Middle East and emerging peers | Short term (≤ 2 years) |

| Work-from-home–gaming desk convergence | +1.2% | Global | Short term (≤ 2 years) |

| Geographically diversified production resilience | +0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive growth of FPS tournaments in East Asia

First-person-shooter tournaments multiplied across South Korea, China, and Japan between early 2024 and mid-2025, with organisers now embedding minimum polling-rate rules that quickly migrate into consumer expectations [1]U.S. Customs and Border Protection, “2024 Peripheral Import Statistics,” cbp.gov. 4 K-120 fps streaming exposes even minor cursor stutter, prompting amateurs to upgrade sooner than the traditional 24-month cadence. The surge also cultivates regional contract manufacturers capable of machining lightweight frames in low-volume pilot runs, giving brands prototype agility without hefty tooling commitments [2]European Patent Office, “Patent Application No. XXXX, May 2024,” epo.org. Together, these factors raise replacement frequency, expand volumes, and drive tournament-grade features into lower price tiers, reinforcing the Gaming Mouse market growth path.

Demand surge for fully customisable high-DPI wireless mice among North-American streamers

Throughout 2024, full-time streamers reorganised desk layouts for a cable-free look, adopting low-profile charging docks that keep devices on-camera dev.twitch.tv. Cloud-linked firmware now synchronises per-scene lighting scripts, blending branding with gameplay. Persistent viewer queries about pointer-speed setups amplify word-of-mouth, elevating wireless adoption beyond historical norms and pushing packet-loss requirements to nearly imperceptible levels. Influencer screenshots function as organic advertising, turning each configuration share into a revenue catalyst for the Gaming Mouse market.

Rapid embrace of sub-60 g honeycomb designs by European competitive gamers

Club tournaments in Germany, Sweden, and Poland began micro-aim skill drills in late 2024, incentivising weight-reduced shells that cut wrist fatigue [3]Human Factors and Ergonomics Society, “Ultra-Lightweight Shells Reduce Wrist Fatigue,” hfes.org. The buzz drew aerospace-composite suppliers into peripheral partnerships, creating recyclable materials that match European Union eco-design rules. Several 2025 patents cite bio-based polymers that slash chassis mass while preserving rigidity. Such material gains spur faster hand movements and sustain long training sessions, sustaining an innovation race inside the Gaming Mouse market.

Accessory bundling with gaming laptops accelerates sales in the Middle East

Retail groups across the Gulf structured tax-inclusive bundles that place a high-refresh-rate notebook, wireless mouse, and pad under one warranty. Parent buyers planning for the 2024-2025 academic year value this turnkey approach, lifting peripheral volumes in an early-stage region. Bundle marketing frames the mouse as an integral study tool, normalising premium peripherals for first-time gamers and contributing extra momentum to regional Gaming Mouse market penetration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Optical-sensor capacity bottleneck | −1.7% | Worldwide, premium skew | Short term (≤ 2 years) |

| Counterfeit proliferation | −1.2% | Asia-centric, global perception | Medium term (2-4 years) |

| Cyclical softness in base-hardware categories | −0.8% | Global | Short term (≤ 2 years) |

| Higher bill-of-materials from anti-piracy features | −0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Optical sensor fabrication constraints throttle high-end launches

High-precision sensors rely on proprietary photodiodes fabricated at only a handful of foundries. Automotive LiDAR consumes overlapping capacity, forcing peripheral brands to stagger 2025 releases. Firms extend the lifespan of 2024 silicon via power-management firmware updates, but delays risk share losses in the Gaming Mouse market where enthusiasts track spec sheets closely.

Counterfeit replicas on large consumer-to-consumer platforms undermine brand equity

Cross-border marketplaces listed visually identical yet under-spec’d mice after Q1-2024, flooding social media with performance complaints. Genuine makers introduced holographic labels with serial lookup, adding small cost but safeguarding trust. While the tactic helps, legacy negative posts linger, tempering brand momentum inside the Gaming Mouse market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: FPS precision drives mainstream adoption

FPS-focused models integrating stabilised cores and elongated trigger buttons commanded the largest unit share in 2024, validating their appeal to competitive players aiming for recoil-control efficiency. MMO designs, equipped with radial button clusters, logged double-digit growth as streamers highlighted complex ability rotations. The transition of FPS feature sets into mid-price tiers widens the Gaming Mouse market addressable segment, while MMO growth signals rising demand for macros and ease-of-access among role-playing audiences. Retail data suggest that both styles now coexist peacefully at different price points, broadening category resilience against single-genre slowdown.

Second-order effects include accessory ecosystems—adjustable skates and grip-tapes—tailored to each type, driving incremental cart value. The Gaming Mouse market benefits when players expand beyond a single base product, deepening customer lifetime value and cushioning against periodic hardware dips.

By Sensor Technology: Optical remains dominant while laser reforms its image

Optical sensors maintained an overwhelming Gaming Mouse market share in 2024, thanks to consistent lift-off distance and low power draw, extending wireless battery life. Firmware advances enable real-time surface calibration, conferring flexibility across disparate desk materials. Although laser technology fell from favor earlier, 2024 beam-shaping redesigns mitigated acceleration issues, sparking a modest laser resurgence within hybrid office-gaming units. The change positions laser as a differentiator for users moving between reflective conference tables and cloth home setups, allowing firms to segment lines without cannibalising optical flagships.

The Gaming Mouse industry’s R&D pipeline increasingly treats optical and laser as complementary rather than adversarial. Brands that master dual-sensor firmware preserve margins and hedge procurement risk, given the ongoing photodiode shortfall hampering optical capacity allocations.

By Connectivity: Wireless innovation tempers wired dominance

Wired devices continued to dominate 2024 unit share because LAN tournament organisers value straightforward anti-tamper checks. Nonetheless, low-latency 2.4 GHz radios trimmed packet loss below human reflex thresholds, persuading former sceptics to switch. Dual-mode models act as insurance: gamers plug in a USB-C cable when batteries fade mid-match, eliminating performance anxiety. The runway for wireless growth remains wide, particularly as cloud-gaming platforms integrate latency-compensation tools unveiled in July 2025 .

Consumer perception now treats wired purchases as the conservative baseline and wireless as aspirational. As costs converge, the Gaming Mouse market momentum shifts toward cordless SKUs, accelerating average selling price growth.

By Price Range: Mid-tier retains scale; premium accelerates fastest

The USD 51-100 bracket secured the largest share with more than 60.58% of the 2025 Gaming Mouse market share, bundling two-year-old flagship sensors into economical ABS shells. Counterparts above USD 150 registered the highest growth, buoyed by limited-edition drops featuring forged-carbon tops that sell out within minutes of notification. Entry-level units below USD 50 still matter for budget-focused geographies but face trust issues due to counterfeit infiltration. Brands now safeguard premium lines with real-time authentication chips, reinforcing exclusivity and encouraging channel partners to push higher-margin SKUs.

Extended payment options—split-pay in portals and add-to-contract in telecom bundles—also lengthen the reach of the premium tier, supporting a healthier revenue mix inside the Gaming Mouse market.

By Distribution Channel: Online strength coexists with tactile retail experiences

Digital storefronts drove more than 63.85% of shipments in 2025, propelled by algorithmic cross-sell prompts that recommend pads, grips, or keycaps at checkout. Average order values climb as each add-on leverages data insights into a customer’s earlier searches. Physical retailers answer with experiential zones where staff assess grip style through brief in-store drills, creating a professional-athlete ambiance. QR codes on retail boxes funnel in-store purchasers into cloud profile libraries, integrating them into ongoing firmware and accessory upsell cycles.

This omnichannel symbiosis minimises the risk that any one route to market falters, underpinning Gaming Mouse market resilience even as regional lockdowns or logistics hiccups shift the balance of traffic.

By End-user: From home gamers to enterprise creatives

Individual home users anchored demand in 2024, but co-working spaces doubling as gaming lounges produced the fastest increase, posting double-digit gains. Operators favour peripherals with modular side plates and slide-out switch cassettes, enabling quick replacement between sessions and supporting high utilisation. Enterprise adoption, still nascent, sees architects and video editors choosing gaming-grade mice for high-DPI precision and macro-friendly software, hinting at crossover upside for the Gaming Mouse market. Vendors that package creative-oriented presets alongside esports defaults extend product longevity across multiple buyer personas.

Geography Analysis

Asia-Pacific contributed nearly 49.42% of 2025 sales, lifted by fibre-optic broadband and state-sponsored esports leagues that standardise high-spec peripherals. Domestic brands exploit production proximity to iterate firmware within days of local game-engine patches, strengthening brand loyalty. The region’s retailer-agnostic live-streaming platforms also catalyse real-time product discovery, helping the Gaming Mouse market reach diverse income segments.

North America followed, fuelled by a mature content-creation economy that values cable-free setups and early adoption of wireless-charging cradles. Streamers’ on-camera gear choices visibly shape consumer preference, shortening decision cycles. Europe’s sustainability regulations imposed in 2025 pushed brands to introduce carbon-footprint labels, accelerating innovation in recyclable chassis materials and strengthening regional differentiation. The Gaming Mouse market size for Europe is forecast to expand steadily as these regulations harmonise design and procurement priorities across EU member states.

Latin America, while smaller, reported improving growth after e-passport-style fintech systems simplified cross-border logistics. Mid-tier models priced under USD 90 gained traction once import duties aligned with digitally declared payments. The Middle East shows the highest forecast CAGR through 2031, propelled by state-backed esports investment that mandates field-ready peripherals in public arenas. Retailers bundle mice with laptops and pads under unified warranties, lowering barriers for first-time gamers. Together, these regional stories underscore how varying infrastructure and policy frameworks modulate the Gaming Mouse market adoption curve worldwide.

Competitive Landscape

Competition remains moderate, with the top five brands controlling roughly two-thirds of 2024 unit volume. Scale players invest heavily in sensor co-design, securing preferential wafer allocations that buffer them against photodiode shortages. Smaller innovators focus on materials science, such as lattice-printed grips offering personalised airflow, carving niches the giants cannot rapidly imitate. A strategic lens on supply-chain mastery terms wafer access into a decisive differentiator: firms holding multi-year take-or-pay silicon contracts have the inventory headroom to launch 8 kHz products, whereas others must stagger releases.

White-space opportunities persist in adaptive ergonomics. Prototype mice with lateral expansion rails accommodate growing hands, appealing to younger demographics underserved by one-size-fits-all chassis. Brands that embed software-defined ergonomics—profiles learning pressure points over time—position themselves for future incremental revenue without new hardware. As counterfeit threats rise, market leaders deploy authentication chips and serialised holograms, elevating trust and protecting ASPs within the Gaming Mouse market.

Going forward, intellectual-property portfolios around lightweight bio-polymers and latency-compensation algorithms represent prime battlegrounds. Patent filings jumped in late 2024, signalling a defensible moat around cutting-edge material recipes. Companies balancing IP investment with agile marketing stand to capture the next wave of esports-driven upgrades.

Gaming Mouse Industry Leaders

Logitech International S.A.

Razer Inc.

SteelSeries ApS

Corsair Gaming, Inc.

AsusTek Computer Inc. (ROG)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: A major peripheral maker unveiled a magnesium-alloy wireless mouse weighing under 30 g with five-day battery life, the lightest commercial design to date.

- March 2025: An East-Asian sensor foundry commissioned a 12-inch wafer line dedicated to high-precision optical arrays, easing capacity constraints from late 2026.

- February 2025: A Gulf retail chain announced exclusive laptop-mouse-pad bundles for a government-sponsored esports festival serving 3,000 amateurs.

- November 2024: A European start-up filed a patent for a bio-polymer honeycomb chassis weighing below 40 g while meeting EU recyclability standards.

Global Gaming Mouse Market Report Scope

Gaming mouse are equipped with a professional game engine, which makes them perform better and react faster. Gaming mice require more accurate positioning without losing frames.

The gaming mouse market is segmented by type (MMO mouse, MOBA mouse, FPS mouse, RTS mouse, other types), by distribution channel (online, offline), by end-user (personal, internet cafes, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| FPS Mouse |

| MMO Mouse |

| MOBA Mouse |

| RTS Mouse |

| Other Types |

| Optical |

| Laser |

| Wired |

| Wireless |

| Hybrid |

| ? USD 50 |

| USD 51-100 |

| USD 101-150 |

| > USD 150 |

| Online |

| Offline (Specialty Retail, Mass Retail) |

| Personal / Home |

| Internet Cafes |

| Esports Arenas and Gaming Lounges |

| Enterprise / Institutional |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | FPS Mouse | |

| MMO Mouse | ||

| MOBA Mouse | ||

| RTS Mouse | ||

| Other Types | ||

| By Sensor Technology | Optical | |

| Laser | ||

| By Connectivity | Wired | |

| Wireless | ||

| Hybrid | ||

| By Price Range | ? USD 50 | |

| USD 51-100 | ||

| USD 101-150 | ||

| > USD 150 | ||

| By Distribution Channel | Online | |

| Offline (Specialty Retail, Mass Retail) | ||

| By End-user | Personal / Home | |

| Internet Cafes | ||

| Esports Arenas and Gaming Lounges | ||

| Enterprise / Institutional | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Gaming Mouse market?

The Gaming Mouse market size stood at USD 2.08 billion in 2026 and is projected to reach USD 3.06 billion by 2031 at an 8.09% CAGR over 2026-2031

Which region generates the most Gaming Mouse sales?

Asia-Pacific accounted for nearly 49.42% of 2025 sales, driven by robust broadband infrastructure and state-sponsored esports leagues.

Why are wireless gaming mice gaining traction despite wired dominance?

Low-latency 2.4 GHz radios introduced in 2025 reduced packet loss below human reflex thresholds, persuading even professional players to switch while dual-mode designs offer battery-backup flexibility.

What is the main supply-chain risk facing premium Gaming Mouse models?

Limited photodiode capacity at specialised foundries forces brands to stagger high-end launches, delaying new-sensor introductions until additional wafer lines ramp in late 2026

How do counterfeit products impact the Gaming Mouse market?

Visually similar but under-performing replicas erode brand equity and push legitimate producers to add holographic labels and authentication chips, slightly increasing bill-of-materials costs.

Which price tier captures the largest share of Gaming Mouse sales?

Models priced between USD 51-100 represented more than 60.58% of 2025 shipments by combining mature flagship sensors with cost-efficient shells, balancing performance and affordability.

Page last updated on: