Workforce Management (WFM) In Hospitality Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.57 Billion |

| Market Size (2031) | USD 1.04 Billion |

| Growth Rate (2026 - 2031) | 12.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Workforce Management (WFM) In Hospitality Market Analysis by Mordor Intelligence

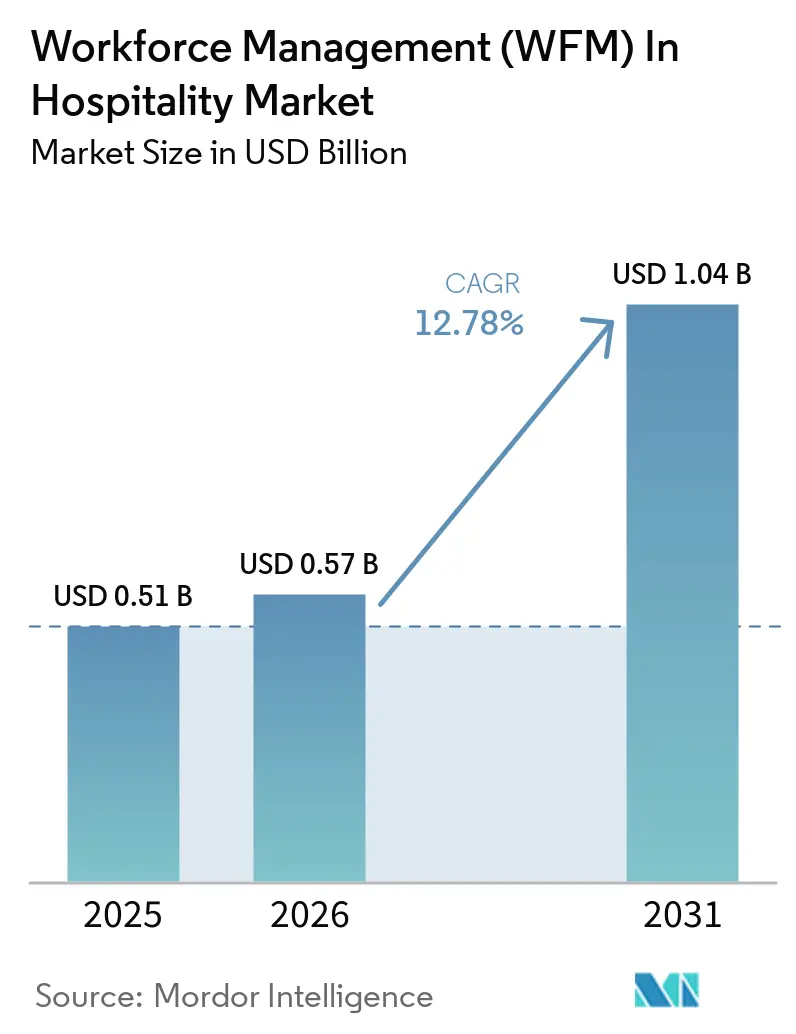

The workforce management (WFM) in hospitality market was valued at USD 0.51 billion in 2025 and estimated to grow from USD 0.57 billion in 2026 to reach USD 1.04 billion by 2031, at a CAGR of 12.78% during the forecast period (2026-2031). Growth is being shaped by a steady move away from manual and reactive rostering toward labor planning that is tied more closely to occupancy, sales, and intraday demand shifts. Labor remains the largest controllable cost item for many hospitality operators, which is pushing workforce platforms from a discretionary software purchase into a core operating tool. Compliance pressure is also raising the value of scheduling, time capture, and audit-ready recordkeeping, especially where predictive scheduling and rest-period rules are becoming harder to manage through manual processes. North America remains the current center of demand because of its large installed base of hotel and restaurant operators, while Asia-Pacific is opening the strongest medium-term expansion path through hotel development and digital adoption. Competition is becoming sharper around AI-based forecasting, cloud delivery, integration depth, and regional data-residency alignment, which is lifting the standard for vendor selection across the market.

Key Report Takeaways

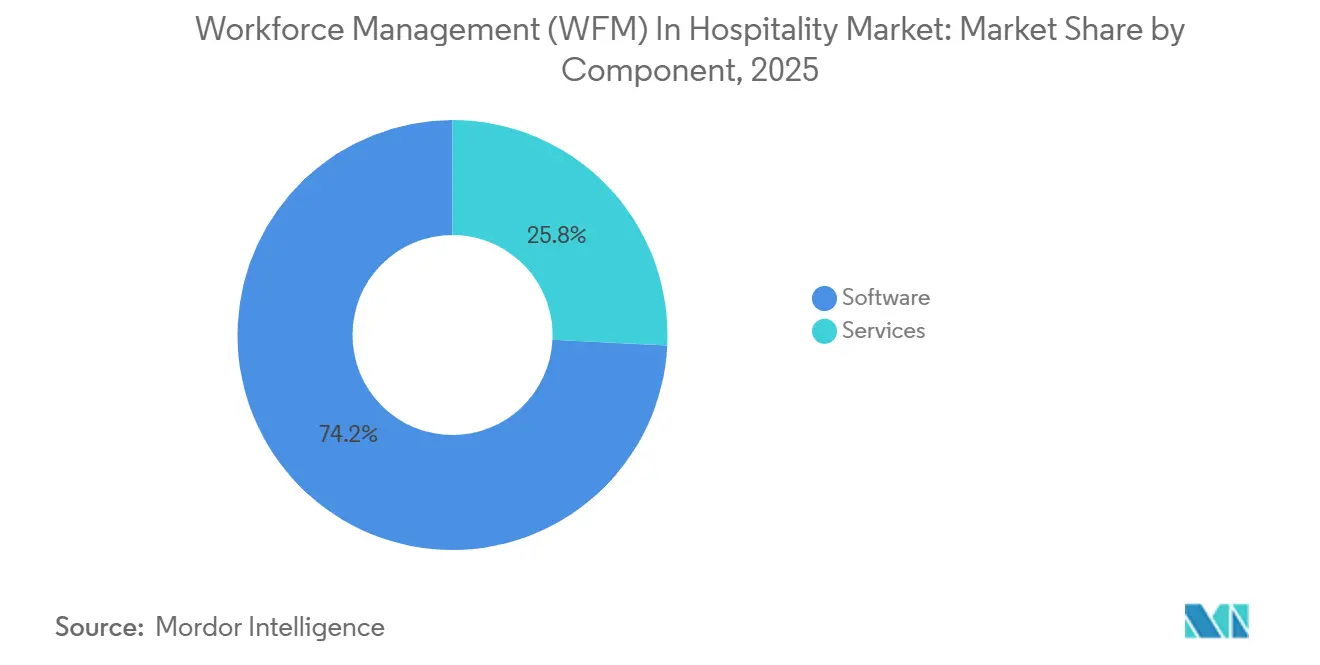

- By component, software led with a 74.22% share of the workforce management (WFM) in hospitality market in 2025, while services are projected to expand at a 13.12% CAGR through 2031.

- By deployment mode, cloud-based deployment held a 69.41% share of the WFM in hospitality market in 2025, while hybrid deployment recorded the fastest projected CAGR at 14.37% through 2031.

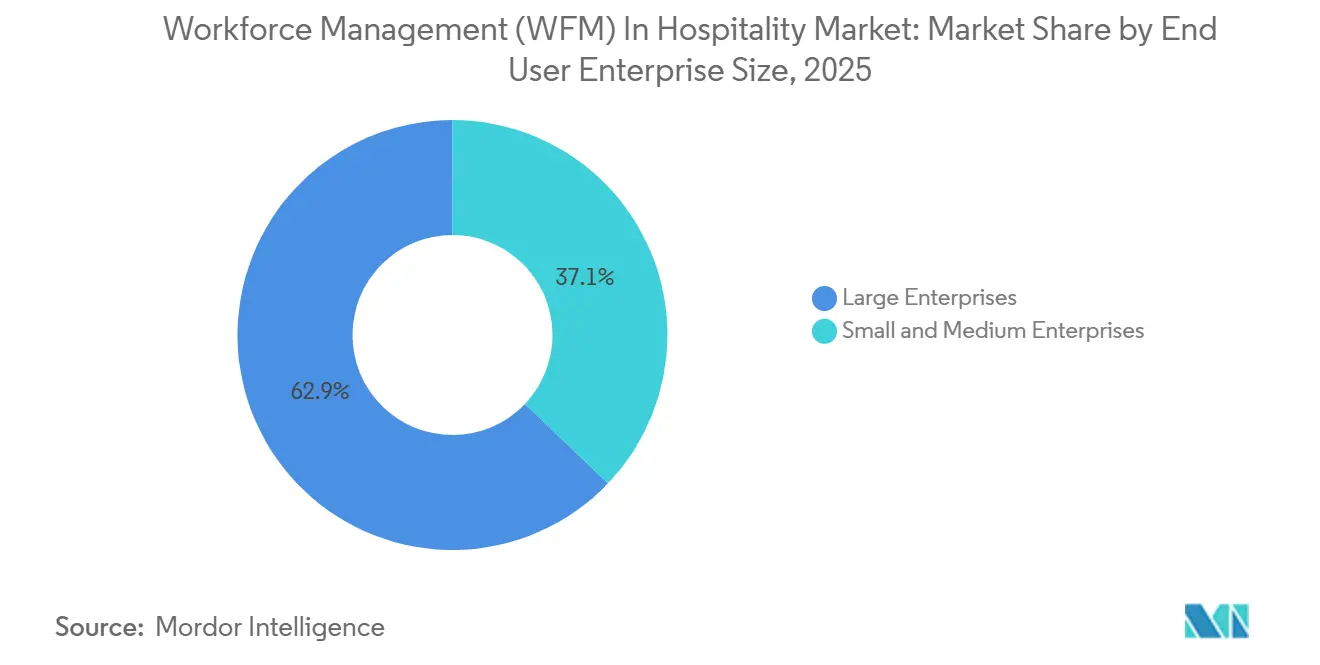

- By end user enterprise size, large enterprises accounted for a 62.88% share of the workforce management in hospitality market in 2025, while SMEs are forecast to grow at a 15.23% CAGR through 2031.

- By end user, hotels held a 34.56% share of the workforce management (WFM) in hospitality market in 2025, while restaurants are projected to advance at a 15.48% CAGR through 2031.

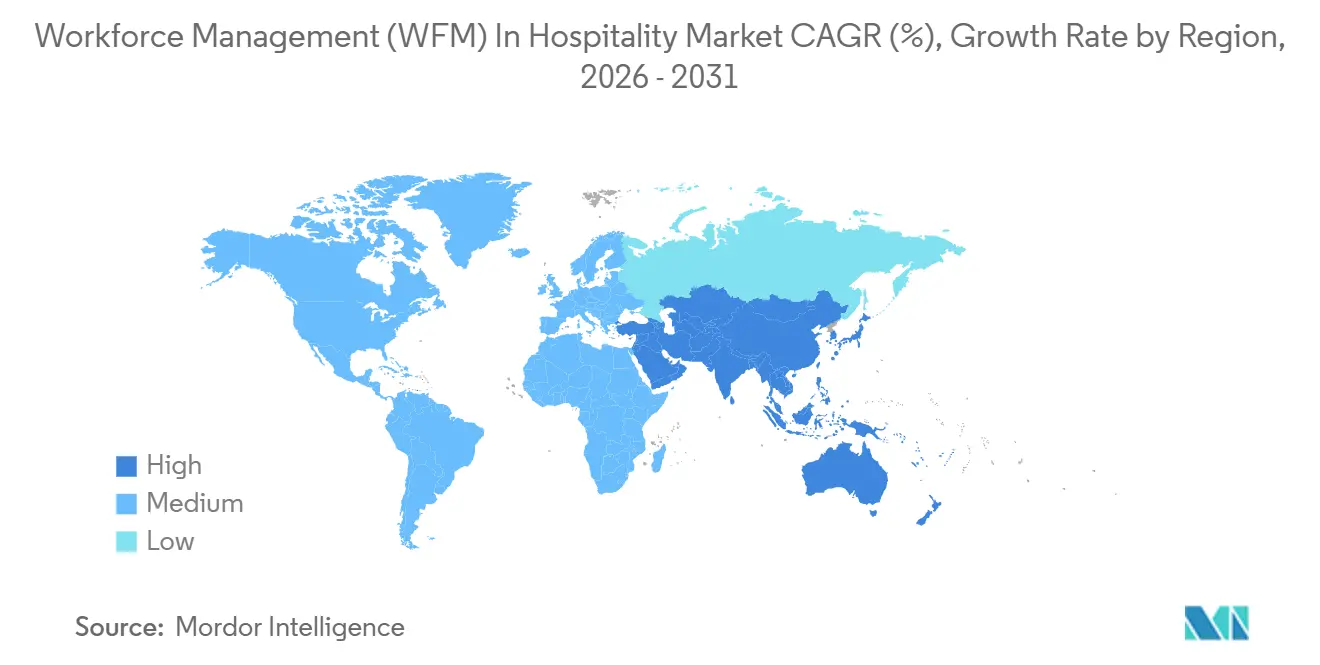

- By geography, North America held a 41.02% share of the WFM in hospitality market in 2025, while Asia-Pacific is forecast to expand at a 15.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Workforce Management (WFM) In Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Pressure to Optimize Labor Costs and Overtime | +3.8% | Global, most acute in North America and Europe where labor represents 30-40% of revenue | Short term (≤ 2 years) |

| AI-Driven Forecasting and Schedule Optimization Improving Labor Productivity | +3.0% | Global, North America leads adoption, Asia-Pacific is accelerating | Medium term (2-4 years) |

| Growing Adoption of Cloud-Based and Mobile WFM Platforms | +2.2% | Global, Asia-Pacific and SME segments are driving incremental growth | Short term (≤ 2 years) |

| Tightening Labor Compliance and Predictive Scheduling Requirements | +1.8% | North America is the core market, Europe is seeing spillover, and Asia-Pacific is expanding | Short term (≤ 2 years) to Medium term (2-4 years) |

| Occupancy and Daypart Volatility Is Raising the Value of Intra-Day Staffing Precision | +0.8% | Global, with higher relevance in resort, casino, and full-service hotel segments | Medium term (2-4 years) |

| Cross-Property Labor Sharing and Internal Shift Marketplaces Are Expanding Coverage Flexibility | +0.5% | North America and Europe, mainly among large hotel groups and franchise networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pressure To Optimize Labor Costs And Overtime

Labor cost management remains the clearest adoption trigger in the workforce management (WFM) in hospitality market because operators can act on it directly and measure the outcome quickly. Labor typically accounts for 28% to 40% of revenue in hospitality, keeping staffing discipline at the center of operating decisions.[1]Fourth Enterprises LLC, “Fair Workweek and Scheduling Compliance Guide for Restaurants,” fourth.com Shifting 220 weekly labor hours from 5 employees working 44 hours each to 8 employees can remove 20 overtime hours and save USD 170 to USD 250 per week per location at median wage rates. That arithmetic becomes more important in multi-unit operations because the same scheduling leakage repeats across a larger estate. Buyers in the workforce management in hospitality market are therefore moving past basic roster creation and are asking for labor tools that connect staffing decisions to occupied rooms, service periods, and overtime exposure. This is keeping labor-cost visibility and overtime control near the front of procurement decisions across the hospitality workforce management market.

AI-Driven Forecasting And Schedule Optimization Improving Labor Productivity

AI-driven scheduling is moving from the pilot stage to daily operations in the workforce management (WFM) in hospitality market.[2]Fourth Enterprises LLC, “Fair Workweek and Scheduling Compliance Guide for Restaurants,” fourth.com Platforms are now processing 1.6 billion data points weekly, training 300,000 models, and generating 1.2 million shifts per week, which shows how forecast-led scheduling is scaling in live environments. Customers using employee engagement suites have recorded an average 33% improvement in frontline retention. Surveys also show that 65% of managers in the UK believe AI could simplify scheduling, while only 19% currently use such tools, leaving ample room for further adoption. Open beta launches in 2025 have demonstrated how agentic systems can block non-compliant rosters and suggest assignments using availability and historical sales patterns. These capabilities are raising expectations in the hospitality workforce management market from static forecast support to real-time schedule intervention and automated compliance controls.

Growing Adoption Of Cloud-Based And Mobile WFM Platforms

Cloud and mobile delivery continue to gain adoption in theworkforce management (WFM) in hospitality market because hospitality teams are deskless and must be notified of schedule changes immediately. Managers across UK hospitality businesses lost 286 hours per year switching between disconnected systems, while 13% of operating costs were affected by system fragmentation. Surveys show that 72% of hourly staff view schedule flexibility as their primary job consideration, which strengthens the case for mobile self-service and instant shift visibility. In Japan, hotel operators implementing combined cloud attendance and AI shift-management systems reduced shift-creation labor by up to 80%. That pattern shows that cloud migration in the hospitality workforce management market can be driven by compliance, cost control, and workforce experience simultaneously. It also explains why cloud architecture still leads while hybrid models rise, where local hardware and local data handling remain important in the workforce management in the hospitality market.

Tightening Labor Compliance And Predictive Scheduling Requirements

Labor compliance is becoming a stronger buying trigger in the hospitality workforce management market as scheduling rules expand across more jurisdictions. Oregon remains the only state with a statewide predictive scheduling law in the United States, while Chicago, New York City, Seattle, Philadelphia, and Los Angeles County enforce municipal rules covering advance notice, rest protections, and predictability pay. Additional legislation was under consideration in Connecticut, New Jersey, and Minnesota as of April 2026. In the UK, phased implementation from April 2026 is adding pressure around guaranteed hours and short-notice shift cancellations. Vendors that can automatically flag rest-period breaches, calculate predictability pay, and preserve audit-ready records are therefore drawing stronger interest from enterprise buyers in the workforce management in hospitality market. Compliance features are shifting from add-on capabilities to core platform expectations across the workforce management (WFM) in hospitality market.[3]The Access Group, “How AI Is Helping UK Hospitality Businesses Improve Efficiency and Guest Experience,” theaccessgroup.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Integration Complexity Across PMS, POS, Payroll, and Time Clocks | -2.1% | Global, most acute in large multi-property hotel groups and franchise networks with long technology depreciation cycles | Medium term (2-4 years) |

| Data Privacy and Cybersecurity Risks Around Employee Data | -1.5% | Europe is the core market under GDPR, with expansion under China’s PIPL and U.S. state privacy rules | Short term (= 2 years) to Medium term (2-4 years) |

| High-Churn, Multilingual Frontline Workforces Can Limit Daily System Adoption Discipline | -0.9% | Global, most severe in regions with high seasonal labor dependency, including Mediterranean Europe, Southeast Asia, and South America | Long term (= 4 years) |

| Franchise and Management-Contract Operating Models Slow Portfolio-Wide Standardization | -0.6% | North America, Middle East, and Asia-Pacific in franchise-heavy QSR networks | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Legacy Integration Complexity Across PMS, POS, Payroll, And Time Clocks

Integration complexity remains the most material near-term drag on workforce management in the hospitality market, as hotel and restaurant groups often run mixed technology estates built over many years.[4]Zellis, “Hospitality, AI-Enabled HR, WFM and Payroll Software,” zellis.com Only 1 in 3 hospitality operators trusts the data produced by their current systems, which weakens forecast quality before labor optimization even begins. A single property can still rely on separate PMS, payroll, HR, POS, and time-capture systems that were chosen at different points in the operating cycle. This slows rollouts in the workforce management market for hospitality and stretches implementation programs to 6 to 12 months for full hospitality deployments. Some vendors have tried to reduce that friction by expanding their partner ecosystems to include major consulting and technology firms. Even so, integration work continues to delay time-to-value in the hospitality workforce management market for large multi-property groups and franchise networks.

Data Privacy And Cybersecurity Risks Around Employee Data

Data privacy and cybersecurity concerns are also slowing workforce management in the hospitality market because these platforms hold biometric, payroll, location, scheduling, and absence data in a single environment. iHR360 stated that China’s 2025 enforcement environment requires encrypted storage for biometric attendance data, liveness detection certification, and deletion cycles of no more than 30 days. Hospitality operators in regulated regions are therefore asking vendors to prove where employee data is stored and how it is protected before contracts move forward. Security reviews extend procurement cycles in the workforce management in the hospitality market, especially for smaller vendors that lack pre-certified cloud infrastructure or dedicated compliance teams. The risk is asymmetric because a single breach involving biometric or financial employee data can cause regulatory and reputational damage that outweighs the original software spend. This keeps trust, residency controls, and security posture near the center of platform choice in the workforce management (WFM) in hospitality market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Time And Attendance Management Anchors Software Dominance

Software held 74.23% of the workforce management (WFM) in hospitality market share in 2025, making it a core component across deployments. Within software, time and attendance management accounted for 25.22% of the software sub-segment in 2025, underscoring the continued importance of precise time capture for overtime control, payroll accuracy, and compliance recordkeeping. Scheduling, labor optimization, and analytics are moving from reporting support to everyday decision-making tools in the hospitality workforce management market. Leave, absence, and task management are gaining traction in multi-department hotel environments, where a single staffing gap can affect several teams simultaneously. Employee self-service and communication modules are also gaining ground because retention plans depend more on shift visibility, flexibility, and mobile access.

Services are projected to expand at a 13.12% CAGR through 2031, making them the faster-moving component of the WFM in the hospitality market. This growth reflects the workload associated with integration, training, change management, and ongoing support, rather than just software demand. Hospitality operators often need 6 to 12 months of support to connect PMS, POS, payroll, and time data into a usable operating flow. That makes services a practical differentiator in the workforce management in the hospitality market, especially when operators want faster adoption, cleaner implementation, and more reliable use at the property level.

By Deployment Mode: Cloud-Based Architecture Leads While Hybrid Gains Ground

Cloud-based deployment accounted for 69.41% of the workforce management (WFM) in hospitality market in 2025, reflecting the appeal of centralized labor control across distributed properties. The model suits workforce management in the hospitality market because managers can adjust staffing mid-shift via mobile dashboards and shared data layers. Providers serve millions of workers across hundreds of thousands of workplaces in over 100 countries, and new infrastructure launches in late 2025 added support for AI capability. Automatic compliance updates and lower infrastructure burden are also continuing to pull operators away from fully local deployment models. These advantages explain why the workforce management in the hospitality market still leans heavily toward SaaS delivery in current buying cycles.

Hybrid deployment is projected to grow at a 14.37% CAGR through 2031, the fastest pace among deployment modes in the workforce management in hospitality market. Large hotels and casino properties still need local hardware for biometric capture and secure clock-in workflows, even when scheduling and analytics move to the cloud. Some vendors have highlighted this model through architectures that combine on-site Face ID verification with cloud forecasting linked to PMS occupancy data. As a result, hybrid designs are becoming the transition path in the workforce management market in the hospitality industry, where on-site control and cloud flexibility must coexist.

By End User Enterprise Size: Large Enterprises Lead While SMEs Accelerate

Sign in. Large enterprises accounted for 62.88% of workforce management in hospitality market in 2025, reflecting the scale of procurement for branded hotel chains, global restaurant groups, and integrated resort operators. These buyers can spread software costs across large workforces and justify deeper automation because scheduling errors repeat across many sites. Aimbridge Hospitality, for example, deployed workforce platforms across 45,000 hourly U.S. employees at 1,100 properties, and more than 30% of that hourly workforce had traded shifts since the model launched. AI-assisted scheduling can cut scheduling time by up to 75%, which matters most when managers oversee large labor pools. This keeps large operators at the center of current revenue in the hospitality workforce management market.

SMEs are projected to advance at a 15.23% CAGR through 2031, the fastest pace by enterprise size in the WFM in hospitality market. Tiered SaaS pricing and simpler onboarding are opening enterprise-style labor tools to independent hotel groups and multi-unit restaurant operators. In 2025, more than 47% of smaller U.S. restaurant operators still used paper schedules, and 57% relied on group text messages for team communication, leaving ample room for digital migration. This gap provides a long runway for workforce management in the hospitality market's SME tier, as compliance and labor control become harder to manage manually.

By End User: Hotels Anchor Demand While Restaurants Drive Growth

Hotels held a 34.56% share of the workforce management (WFM) in hospitality market in 2025, giving them the largest end-user position. A full-service hotel manages housekeeping, front desk, food and beverage, maintenance, and security rosters simultaneously, making labor orchestration a daily operational task. Metrics such as cost per occupied room and labor cost as a share of revenue are already embedded in hotel operating practice. That operating structure keeps hotel demand steady in the hospitality workforce management market because staffing decisions can be linked directly to occupancy and service levels. Mobile check-in and other self-service tools are also raising the need for more precise front-desk and guest-services staffing rather than blanket overstaffing.

Restaurants are projected to grow at a 15.48% CAGR through 2031, making them the fastest-growing end-user vertical in the workforce management in hospitality market. Tight margins, high hourly labor exposure, and compliance obligations are pushing restaurant groups toward automated scheduling and time control. Resort properties add another demanding use case because seasonal swings can push required headcount up by 200% between peak and off-season periods. Cruise lines remain fewer in number, but their 24/7 operations and multi-jurisdiction staffing needs make them high-value clients in the hospitality workforce management market.

Geography Analysis

North America held 41.02% of the workforce management (WFM) in the hospitality market share in 2025, making it the leading regional cluster. The region benefits from dense franchise networks in restaurants and hotels, where standardized labor rules and consistent scheduling tools help reduce variance across locations. Compliance pressure is another strong tailwind because the U.S. Department of Labor recovered USD 34.7 million in back wages from the food-service industry in 2024, while Fair Workweek requirements continue to spread across major cities. North America also hosts many of the best-known vendors in the hospitality workforce management market, including UKG, Fourth, Legion, Harri, and 7shifts. That vendor density supports faster product iteration and keeps the region at the forefront of enterprise replacement cycles in the hospitality workforce management market.

Europe held the second-largest share of the hospitality workforce management market, with the United Kingdom and Germany as active deployment centers. In the UK, phased labor rule changes from April 2026 are increasing the value of systems that can handle guaranteed hours, sick pay obligations, and short-notice schedule changes. EU data-residency expectations are also shaping buying behavior, supporting vendors that can demonstrate compliant hosting and audit-ready controls. ATOSS reported FY2025 revenue of EUR 189.3 million (USD 198.7 million), with cloud and subscription revenue growing 28% year over year, indicating healthy demand for compliant cloud workforce tools in Europe.

Asia-Pacific is projected to expand at a 15.21% CAGR through 2031, making it the fastest-growing geography in the workforce management in hospitality market. In Japan, compliance with Work Style Reform rules is supporting the adoption of cloud attendance and shift systems, and tourism SaaS platforms had expanded to 171 hotel facilities by January 2026. In China, AI-driven deployments across hotel groups increased scheduling efficiency by 20% and reduced coordination time by 25%. India and Australia are adding momentum through hotel supply growth and complex shift-loading rules, while the Middle East and Africa are seeing selective demand from tourism build-outs led by international hotel chains. South America contributes incremental growth through urban hotel chains and franchise restaurant networks, but currency volatility and a thinner local vendor base still limit faster adoption in the hospitality workforce management market.

Competitive Landscape

The workforce management in hospitality market remains moderately fragmented, as specialist hospitality vendors and broader HCM platforms compete across different customer tiers. UKG holds the clearest scale advantage in enterprise portfolios, and its Pro Workforce Management suite had been ranked a Leader in the Nucleus Research WFM Technology Value Matrix for 7 consecutive years by May 2026. In early 2026, UKG launched Dynamic Workforce Operations to give frontline managers real-time, AI-guided labor control. Fourth, Harri, Unifocus, Rotaready, and Legion continue to defend their vertical positions by tailoring scheduling logic to hospitality realities such as split shifts, compliance requirements, and rapid demand swings. That specialization keeps the workforce management in the hospitality market from consolidating around a single generic platform.

Competition in the workforce management in the hospitality market is now centered on AI depth, payroll expansion, and ecosystem reach. Fourth expanded its portfolio-level AI offering with iQ 3.0 in February 2026, while Legion launched more than 90 AI workforce management innovations in January 2026 and said revenue rose 216% in 2025. Harri added agentic AI in open beta in September 2025, and Deputy strengthened its platform stack with AI on AWS and U.S. payroll integration across 2025 and 2026. These moves show that workforce management in the hospitality market is shifting from standalone scheduling toward broader operating systems that combine labor, compliance, and payroll workflows.

White space remains in workforce management in the hospitality market for mid-market hotel groups that are too complex for point solutions but too small for enterprise-grade suites. A second gap sits in international compliance automation, where many vendors still lead with U.S. rules and only later adapt for other jurisdictions. ATOSS is responding through broader partner-led integration, while Legion has used certified ecosystem positioning with SAP to strengthen enterprise credibility. Smaller niche players still matter because focused products can win where regional labor rules, local hosting, or multi-site restaurant workflows demand a tighter fit. This mix of scale platforms and focused specialists should keep the workforce management in the hospitality market competitive through 2031.

Workforce Management (WFM) In Hospitality Industry Leaders

UKG Inc.

Fourth Enterprises LLC

Harri (US) LLC

Quinyx AB

Deputy Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: UKG launched Dynamic Workforce Operations and Rapid Hire, automating 90% of hiring tasks and cutting time-to-interview to minutes.

- May 2026: Restaurant365 introduced R365 AI, reducing labor forecast error by 15% and saving approximately USD 100K annually across 10 sites.

- April 2026: Crunchtime added AI Analyst, Voice Inventory, Photo Intelligence, and AI Actions, deployed in 150K+ locations.

- April 2026: Actabl integrated ProfitSword budgets with Hotel Effectiveness scheduling for hotel portfolios.

Global Workforce Management (WFM) In Hospitality Market Report Scope

The Workforce Management (WFM) in the Hospitality Market refers to software and service platforms that streamline workforce operations across hotels, restaurants, resorts, casinos, and cruise lines. These solutions include employee scheduling, time and attendance management, workforce analytics and forecasting, leave and absence management, task execution, and employee self-service communication. Delivered via cloud-based, on-premise, or hybrid models, WFM platforms support both large and small enterprises in the hospitality sector, helping optimize labor costs, ensure compliance, enhance productivity, and improve employee engagement to deliver seamless guest experiences worldwide.

The Workforce Management (WFM) in Hospitality Market is segmented by Component (Software, [Employee Scheduling and Labor Optimization, Time and Attendance Management, Workforce Analytics and Forecasting, Leave and Absence Management, Task and Execution Management, and Employee Self-service and Communication] and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises and Small and Medium Enterprises), End User (Hotels, Restaurants, Resorts, Casinos, and Cruise Lines), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Employee Scheduling and Labor Optimization |

| Time and Attendance Management | |

| Workforce Analytics and Forecasting | |

| Leave and Absence Management | |

| Task and Execution Management | |

| Employee Self-service and Communication | |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Hotels |

| Restaurants |

| Resorts |

| Casinos |

| Cruise Lines |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | Employee Scheduling and Labor Optimization |

| Time and Attendance Management | ||

| Workforce Analytics and Forecasting | ||

| Leave and Absence Management | ||

| Task and Execution Management | ||

| Employee Self-service and Communication | ||

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End User | Hotels | |

| Restaurants | ||

| Resorts | ||

| Casinos | ||

| Cruise Lines | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the wWorkforce Management (WFM) In Hospitality Market?

It was valued at USD 0.51 billion in 2025, reached USD 0.57 billion in 2026, and is forecast to reach USD 1.04 billion by 2031 at a 12.78% CAGR.

Which region leads current demand?

North America leads with a 41.02% share in 2025, supported by large hotel and restaurant chains, active compliance requirements, and a strong vendor base.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region, with a projected 15.21% CAGR through 2031, supported by hotel development and rising digital adoption.

Which deployment model is most widely used?

Cloud-based deployment leads with a 69.41% share in 2025 because operators want centralized visibility, mobile access, and automatic compliance updates.

Which end users are driving the strongest adoption?

Hotels remain the largest end user with a 34.56% share in 2025, while restaurants are growing the fastest at a 15.48% CAGR because of labor pressure and compliance needs.

Why are AI tools becoming important for hospitality workforce operations?

AI tools are helping operators forecast demand, automate schedules, reduce manual planning time, and improve compliance control, which is becoming more important across multi-site operations.

Page last updated on: