Workforce Management (WFM) In Retail Market Size and Share

Market Overview

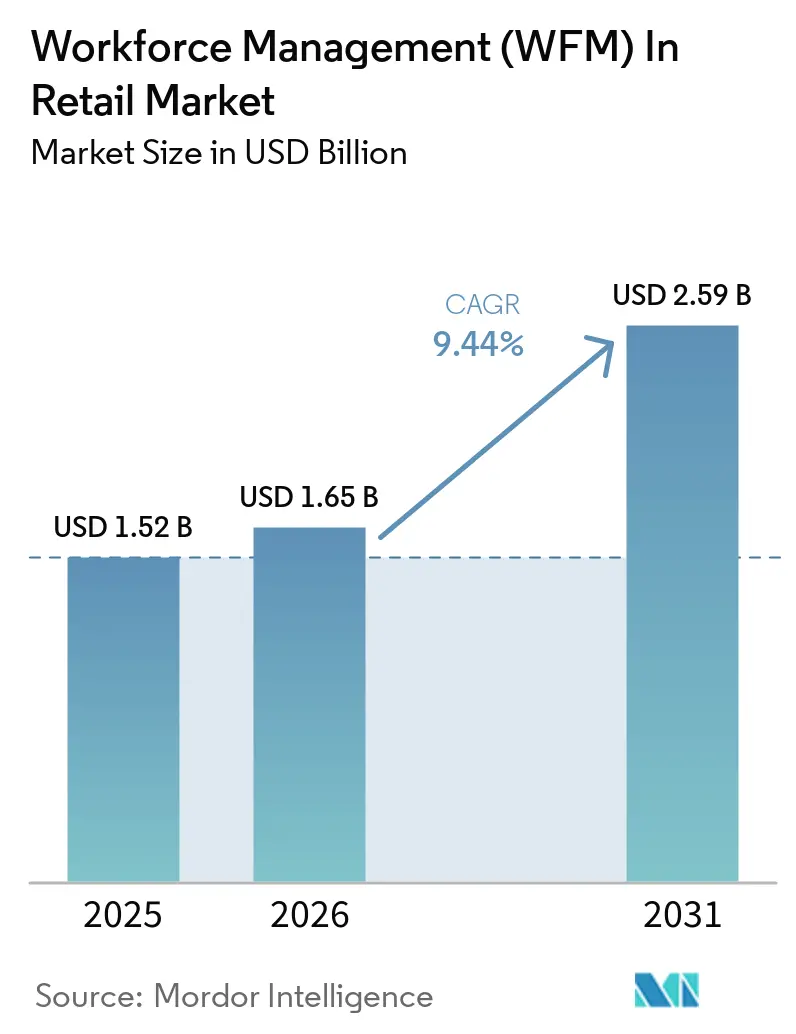

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 2.59 Billion |

| Growth Rate (2026 - 2031) | 9.44% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Workforce Management (WFM) In Retail Market Analysis by Mordor Intelligence

The workforce management (WFM) in retail market size was valued at USD 1.54 billion in 2025 and is estimated to grow from USD 1.73 billion in 2026 to reach USD 3.09 billion by 2031, at a CAGR of 12.30% during the forecast period (2026-2031). The workforce management in retail market is expanding because labor planning has moved from a back-office activity to a direct lever for cost control, service quality, and store execution. Manual scheduling is giving way to AI-native systems that can respond to traffic changes, promotion cycles, and staffing constraints with much greater speed. Wage pressure, fair workweek rules, and omnichannel fulfillment are making labor mistakes more expensive, which raises the value of scheduling accuracy and compliance automation. Competition is tightening as vendors try to stand out through stronger AI models, wider integration coverage, and more reliable multi-jurisdiction compliance tools. The WFM in retail market also has room to grow through implementation services, hybrid deployments, and lower-cost SaaS offers that are opening adoption to a wider base of retail operators.

Key Report Takeaways

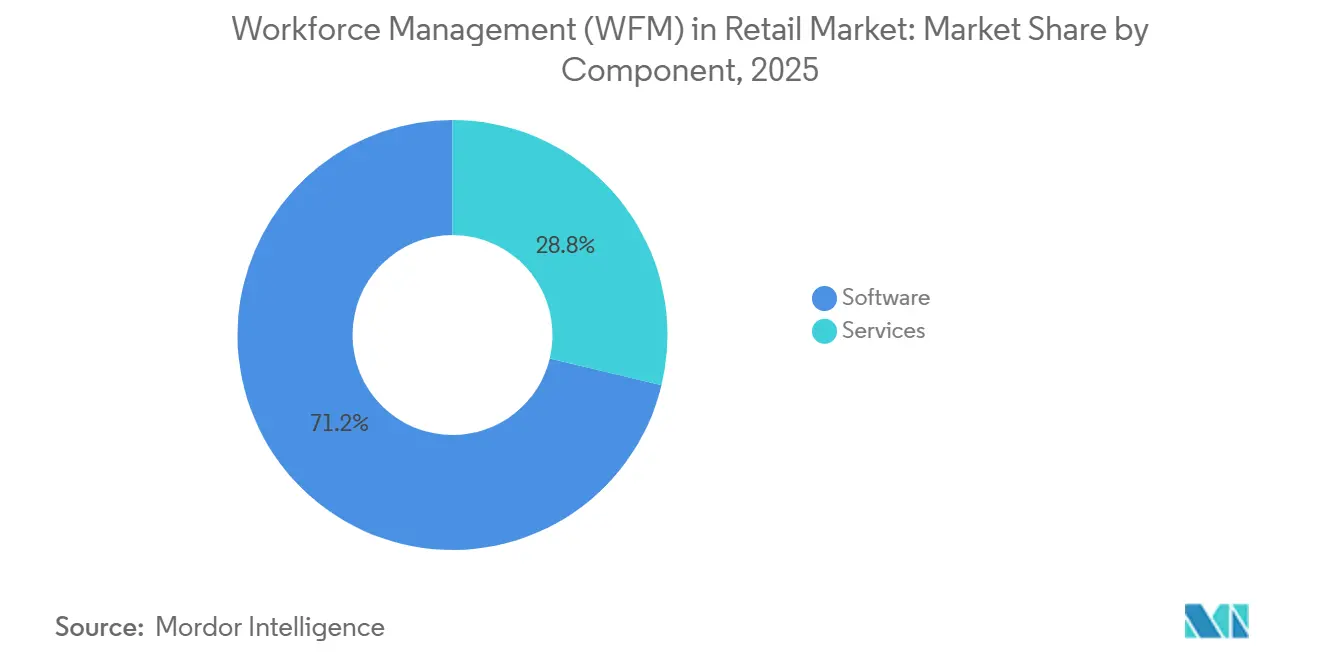

- By component, software held 71.24% of the workforce management (WFM) in retail market in 2025, while services are forecast to expand at a 14.12% CAGR through 2031.

- By deployment mode, cloud held 66.38% share of the WFM in retail market in 2025, while hybrid deployment is projected to record the fastest CAGR at 13.23% over 2026-2031.

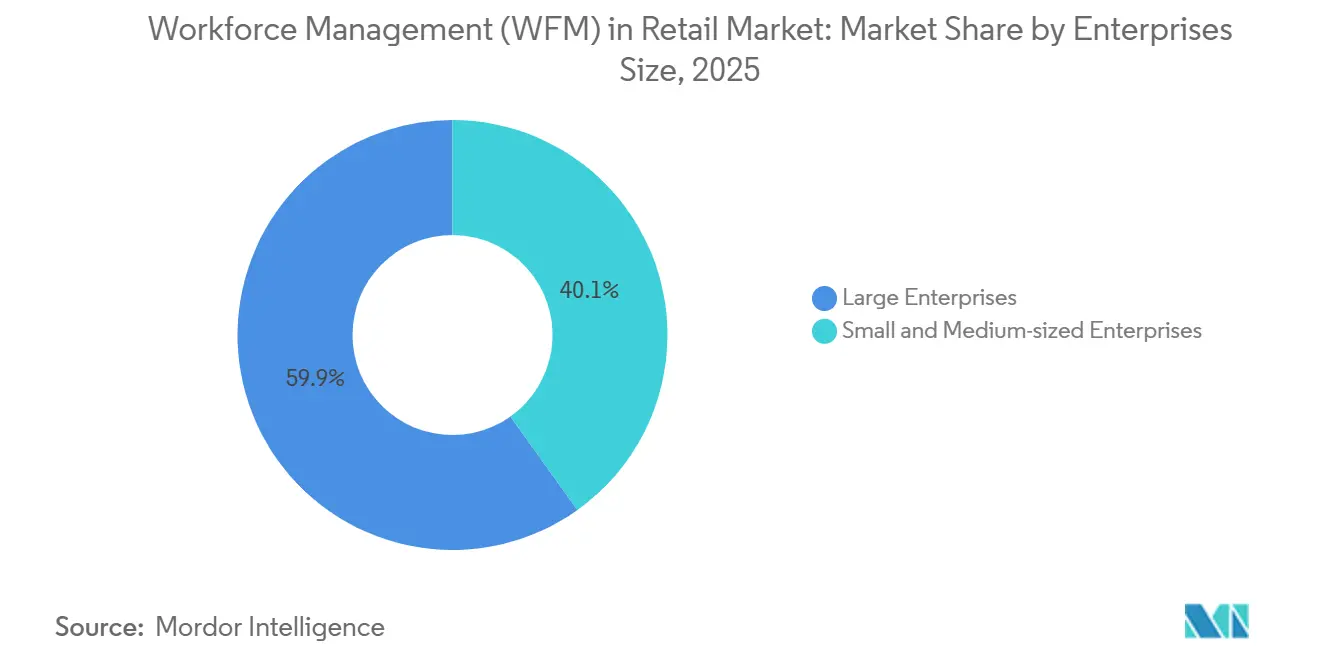

- By enterprise size, large enterprises accounted for 59.87% of the market share in 2025, while small and medium-sized enterprises are expected to grow at a 15.11% CAGR through 2031.

- By retail format, grocery and supermarkets held 23.31% share of the workforce management market in 2025, while e-commerce retailers are forecast to advance at a 15.41% CAGR over 2026-2031.

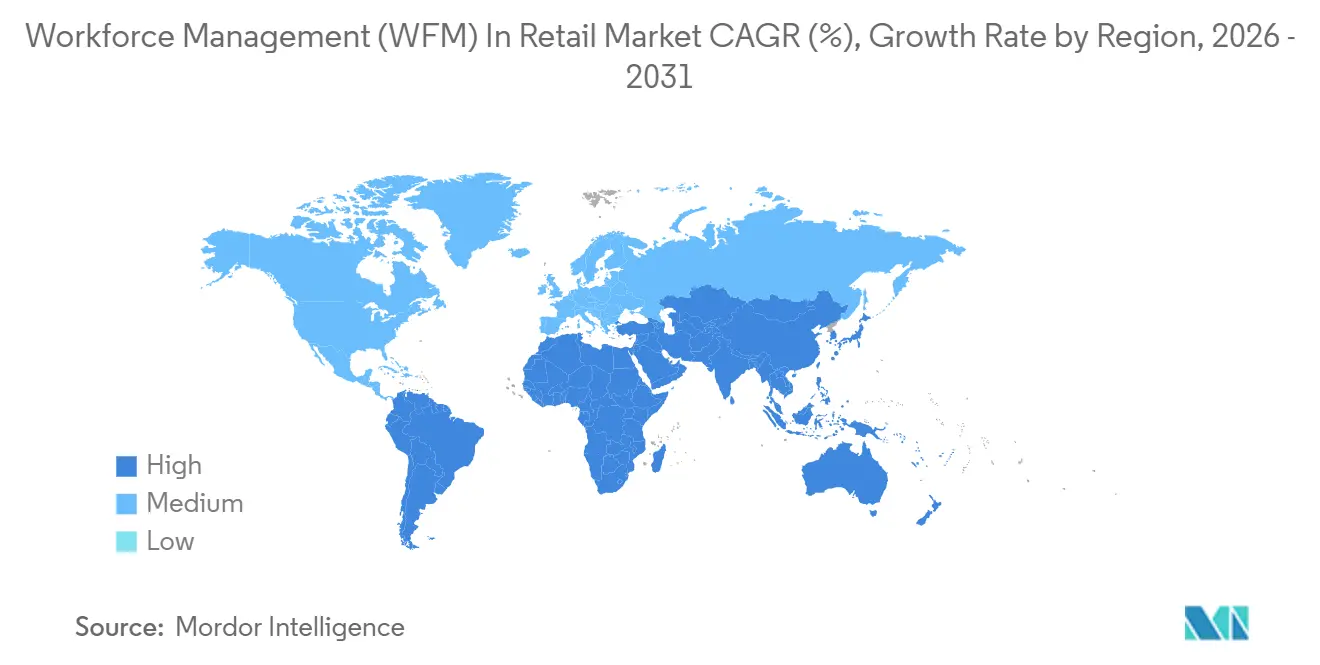

- By geography, North America accounted for 38.92% of the market in 2025, while Asia-Pacific is projected to expand at a 13.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Workforce Management (WFM) In Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-Based and AI-Native Scheduling Adoption | +3.2% | Global, with early concentration in North America and Western Europe | Short term (≤ 2 years) |

| Omnichannel Retail Complexity and Labor Optimization Needs | +2.6% | Global, strongest in North America, Asia-Pacific, and UK | Short term (≤ 2 years) |

| Rising Retail Wage Costs and Margin Pressure | +2.3% | North America and Europe, with spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Fair Workweek and Labor Compliance Automation Demand | +1.6% | North America, Western Europe, with spill-over to Asia-Pacific | Medium term (2-4 years) |

| Task-Level Labor Planning for Click-and-Collect and Micro-Fulfillment | +1.1% | North America, UK, Australia, and Southeast Asia | Medium term (2-4 years) |

| Cross-Store Labor Pooling and Gig-Like Shift Flexibility | +0.8% | Global, with early adoption in North America and Northern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-Based and AI-Native Scheduling Adoption

Cloud migration remains the strongest near-term force behind the workforce management (WFM) in retail market. AI scheduling tools can process foot traffic, local weather, promotion calendars, and employee availability in 15-minute or 30-minute intervals, giving retailers a planning depth that older systems could not handle well. Adoption friction is also easing on the labor side, with reports showing that 77% of retail associates would trust AI to recommend schedules that match their preferences. Cloud and subscription revenue rose 28% in FY2025 to EUR 92.7 million (USD 100.1 million), equal to 49% of total group revenue, which shows that enterprise buyers are shifting budget toward subscription-led models. As these capabilities become standard expectations, the workforce management in retail market is moving away from basic digitization and toward real-time labor orchestration.[1]Logile, “Retail Labor Plans Fall Short on the Front Line, Logile Survey Finds,” Logile, logile.com

Omnichannel Retail Complexity and Labor Optimization Needs

Omnichannel retail has made labor planning significantly more complex, and that complexity is fueling demand in the WFM in retail market. Store teams now divide their time across in-store service, click‑and‑collect, curbside handoff, e‑commerce picking, and replenishment, meaning a single shift often carries multiple task types. Industry leaders have emphasized that in‑store fulfillment works best when retailers create dedicated fulfillment roles or time blocks, which points directly to task‑level scheduling rather than static weekly rosters. The challenge is no longer just labor cost. Poor scheduling now undermines order throughput, pickup speed, and customer service simultaneously. Retailers that can align labor deployment with order‑wave patterns are better positioned to protect both margin and fulfillment revenue, making advanced workforce management tools central to omnichannel success.[2]Fisher Phillips LLP, “Predictive Scheduling Laws Are a Growing Challenge for Retailers: Answers to Your Top 5 Questions,” Fisher Phillips, fisherphillips.com

Rising Retail Wage Costs and Margin Pressure

Rising wage bills continue to strengthen the business case for labor optimization across the workforce management in retail market. XShift AI stated that labor represents 50-60% of total retail operating costs, which means even small efficiency gains can materially change store profitability. In the United States, Chicago’s minimum wage rose to USD 16.60 per hour in July 2025, and similar increases have affected several other major retail states and cities. XShift AI also placed the fully loaded replacement cost of a frontline retail employee at USD 8,300 to USD 18,800, which links poor schedule quality directly to higher turnover expense. Legion Technologies cited a Forrester Total Economic Impact study that reported a 13x return for its platform, which shows why retailers increasingly frame workforce software as a margin defense tool rather than a support system.[3]Malysa O'Connor, “Navigating Retail's 2025 Storm: 10 Reasons Why Workforce Management Is Key to Resilience and Growth,” Legion Technologies, legion.co

Fair Workweek and Labor Compliance Automation Demand

Compliance automation has become a clear commercial driver for the workforce management (WMF) in retail market. Los Angeles County’s Fair Workweek Ordinance took effect on July 1, 2025, and it requires large retailers to post schedules 14 calendar days in advance and pay predictability premiums for certain short-notice changes. Fisher Phillips noted that predictive scheduling laws are spreading across major retail cities, and penalties and restitution can rise quickly when schedule changes are not managed properly. GaiaWorks also pointed to labor-rule changes in Asia, including Singapore’s retirement and re-employment updates from July 1, 2026, which are pushing retailers to revise workforce policies and compliance workflows. As labor regulation becomes more localized and more detailed, retailers are favoring platforms that can embed rule logic into schedule creation rather than rely on manual review after the fact.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity Across POS, Payroll, HRIS, and E-commerce Systems | -1.8% | Global, most acute in North America and Europe where legacy system debt is highest | Medium term (2-4 years) |

| Data Privacy and Employee Monitoring Concerns | -1.2% | Global, most restrictive in the EU, with spill-over to Asia-Pacific and Canada | Long term (= 4 years) |

| Forecast Drift from Promotion-Led Demand Spikes and Returns Surges | -0.9% | Global, highest severity in North America and Asia-Pacific e-commerce markets | Short term (= 2 years) |

| Frontline Manager Override Bias and Low Trust in AI Schedules | -0.7% | Global, most pronounced in markets with weaker AI literacy at the store level | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity Across POS, Payroll, HRIS, and E-commerce Systems

Integration burden remains the largest structural restraint on the WFM in retail market. A scheduling engine can optimize labor on paper, but it loses value when it cannot exchange data smoothly with point-of-sale systems, payroll engines, HRIS platforms, and order management tools. Shopify cited EY analysis showing that unified retail infrastructure can reduce implementation costs by 11% and middleware expenses by 27%, which highlights the hidden cost of disconnected technology estates. The problem is sharper where privacy and AI disclosure rules require controlled data movement across systems, including GDPR, CCPA, and Ontario’s January 2026 AI transparency requirement for employers with 25 or more staff. That is why vendors are competing harder on certified payroll links, prebuilt connectors, and deployment flexibility, as shown by ATOSS references to DATEV-certified interfaces and SAP-certified modules.

Data Privacy and Employee Monitoring Concerns

Data governance concerns could slow adoption in parts of the workforce management in retail market even as demand for automation rises. Modern WFM systems can capture detailed data such as biometric time records, location signals, productivity metrics, and performance outputs at the employee level. GaiaWorks noted that the EU Pay Transparency Directive, which member states must transpose by June 7, 2026, increases the need for auditable and bias-free analytics tied to pay and workforce data. Retail Gazette reported that the UK retail sector faces annual staff turnover near 50%, and poorly governed monitoring practices can worsen that instability by reducing worker trust. Vendors in the workforce management (WFM) in retail market therefore need stronger explainability, tighter data minimization, and clearer employee communication if they want enterprise adoption to scale smoothly.[4]Alexandra Blake, “Ship-from-Store in Omnichannel Retail - Case Studies and Key Insights 2024-2025,” GetTransport Blog, blog.gettransport.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Scale Meets Services Momentum

Software held 71.24% of the workforce management in retail market share in 2025, and employee scheduling and labor optimization remained the largest software sub-segment at 32.52% of the total market. This position reflects how directly schedule quality affects store coverage, labor cost, and lost sales. Logile reported that 77% of associates believe stores regularly lose sales due to poor scheduling, while 74% are open to AI-driven scheduling based on traffic patterns. Time and attendance, analytics and forecasting, and leave management remain important because they connect scheduling decisions to payroll accuracy and labor visibility. Within the workforce management in retail industry, software has become the control layer that ties labor planning to daily store execution.

Services are forecast to grow at a 14.12% CAGR through 2031, making them the fastest-growing component of the workforce management (WFM) in retail market. This reflects the fact that platform value depends on rollout quality, local rule configuration, and change management across large store networks. UKG stated that 57% of frontline workers prefer employer communication only through mobile, and 70% said their employer does not offer on-demand pay, which shows how implementation scope is widening beyond core scheduling into engagement and pay-adjacent functions. As the workforce management in retail industry becomes more platform-led, services are gaining weight because retailers need sustained support to make advanced features work across hundreds of locations.

By Deployment Mode: Cloud Leads While Hybrid Gains Ground

Cloud accounted for 66.38% of the workforce management (WFM) in retail market size in 2025, which reflects the continued shift away from heavy on-premises infrastructure. Retailers favor cloud because it lowers upfront technology burden and speeds access to new AI and compliance features. Quinyx stated that more than 65% of WFM deployments are now cloud-based and pointed to returns above 10 times the original investment over 3 years through better scheduling, lower overtime, and reduced administration. Cloud also fits the regulatory reality of retail labor management, because rule updates can be pushed centrally instead of patched location by location. On-premises systems still retain some relevance where data sovereignty, internal control, or union requirements keep sensitive data closer to local infrastructure.

Hybrid deployment is projected to grow at a 13.23% CAGR through 2031, making it the fastest-growing deployment mode in the workforce management in retail market. This pattern reflects a practical compromise for large retailers that want cloud agility but still need tighter control over payroll or HR data. ATOSS Software SE’s FY2025 results showed a two-track approach that supports enterprise clients with governance constraints while still encouraging fuller cloud adoption through AI-led capabilities. Hybrid growth also makes sense because many retailers still run core payroll or HRIS functions on older systems, and a mixed architecture reduces the risk of latency, data duplication, and integration friction.

By Enterprise Size: Large Retailers Lead, SMEs Accelerate Fastest

Large enterprises held 59.87% of the market in 2025, which keeps them at the center of the workforce management in retail market. Their scale, store density, union complexity, and cross-border labor rules create the strongest need for advanced scheduling and compliance automation. WorkForce Software highlighted potential annual benefits of USD 109.1 million for an organization with 50,000 employees and USD 227.6 million for one with 100,000 employees, which helps explain why large chains can justify broader deployments. UKG also noted that its platform serves 69 of the NRF Top 100 retailers, which underlines how embedded major providers already are in large retail accounts. The workforce management (WFM) in retail market remains concentrated in enterprise spending, even though growth is widening beyond that base.

Small and medium-sized enterprises are projected to grow at a 15.11% CAGR through 2031, which makes them the fastest-expanding enterprise-size group in the WFM in retail market. Lower SaaS pricing is reducing the entry barrier for independent operators and regional chains that were previously priced out of advanced workforce software. XShift AI noted that entry-level AI scheduling can now start near USD 1 per employee per month, which has made forecasting and schedule optimization more reachable for smaller retailers. ATOSS Software SE also stated that its Crewmeister product surpassed 2,000 customers with 99.98% uptime, which shows that smaller business demand is no longer a niche part of the addressable base.

By Retail Format: Grocery Anchors Demand While E-Commerce Surges

Grocery and supermarkets accounted for 23.31% of the market in 2025, giving them the largest retail-format position in the workforce management (WFM) in retail market. Their labor intensity is higher because they manage perishables, longer trading hours, fresh food operations, and a mix of part-time staffing. GFOS stated that grocery operators increasingly need AI forecasting calibrated to 15-minute intervals and linked to seasonal traffic, promotions, and store-specific staffing patterns. Fashion, specialty, electronics, and department-store formats also require skill-based scheduling, but grocery remains the clearest fit for demand-led labor optimization because service failure is visible almost immediately. That combination keeps grocery at the center of vendor sales efforts and product design.

E-commerce retailers are forecast to expand at a 15.41% CAGR through 2031, which makes them the fastest-growing retail format in the workforce management in retail market. Growth is tied to the labor demands of picking, packing, returns, and short fulfillment windows, which create planning conditions that traditional store rosters were not built to manage. Alibaba announced in March 2026 that it would deploy AI digital workforce agents for millions of Taobao and Tmall merchants, showing how quickly large e-commerce ecosystems in Asia are moving toward AI-supported labor models. DingTalk also highlighted how promotion spikes and operational volatility can strain schedules without real-time order-linked planning, which is why e-commerce growth is pushing vendors toward tighter execution and fulfillment integration.

Geography Analysis

North America held 38.92% of workforce management in retail market share in 2025, which kept it as the largest regional contributor. The region benefits from higher enterprise software spending, earlier adoption of AI-led labor tools, and the widest spread of predictive scheduling rules. UKG stated that it serves 69 of the NRF Top 100 retailers, which shows how deeply enterprise workforce platforms are already embedded in the North American retail base. Legion’s rollout with Dollar Tree across more than 9,000 stores and 18 distribution centers shows the scale at which large North American deployments now operate. The regulatory environment continues to support demand, because cities such as Seattle, New York, Chicago, San Francisco, Portland, and Los Angeles County have turned compliance automation into a practical requirement rather than an optional add-on.

Europe remains a structurally important region for the workforce management (WFM) in retail market because labor regulation, time recording, and data governance requirements are forcing upgrade cycles. ATOSS Software SE highlighted retail customers such as OBI, C&A, Decathlon, and Primark, which shows that the region combines deep enterprise demand with long implementation cycles. The June 7, 2026 deadline for national transposition of the EU Pay Transparency Directive is adding another layer of reporting and audit pressure to workforce analytics. South America, the Middle East, and Africa are still earlier in adoption, but organized retail expansion and tighter labor oversight are creating greenfield openings for cloud-native vendors with multilingual and multi-country support.

Asia-Pacific is forecast to grow at a 13.02% CAGR, making it the fastest-growing geography in the WFM in retail market size through 2031. GaiaWorks stated that it serves more than 1,800 enterprises across 34 countries, and one 3C retail case delivered a 10.8% improvement in sales conversion and a 28% reduction in wasted labor hours through traffic-based scheduling. A separate GaiaWorks case study on a Chinese convenience chain reported a 20% reduction in labor costs after deployment of AI smart scheduling tied to store-level demand models. The region’s growth is also supported by labor-rule updates such as Hong Kong’s 468 transition and by the wider spread of AI-led retail execution in markets such as India, where organized retail is scaling fast.

Competitive Landscape

The workforce management in retail market is moderately fragmented, with a group of global providers competing alongside specialist retail vendors. UKG Inc., Dayforce, WorkForce Software, and ATOSS Software SE remain prominent in large enterprise mandates, while Legion Technologies, Quinyx, Logile, and Orquest are pushing harder in the mid-market and in retail-heavy use cases. Competition is centered on 3 themes, stronger AI scheduling, better mobile self-service, and broader integration across payroll, HRIS, and store systems. UKG’s October 2025 rebrand around a Workforce Operating Platform and its ecosystem of more than 350 marketplace partners show how major vendors are trying to move from application provider to infrastructure layer. ATOSS Software SE also disclosed more than EUR 120 million (USD 129.6 million) in liquidity reserved for organic investment and possible bolt-on acquisitions, which signals continued competitive pressure in Europe.

Strategic white space remains strongest in SME-ready SaaS platforms, Asia-Pacific localized offerings, and tools that connect labor scheduling with fulfillment execution inside the workforce management in retail market. Dayforce’s agreement to be acquired by Thoma Bravo in a USD 12.3 billion all-cash deal was one of the biggest strategic events in 2025 and created fresh uncertainty around future positioning in the mid-market. Legion strengthened its competitive position in January 2026 by launching more than 90 AI innovations across forecasting, scheduling, time and attendance, and labor optimization. Logile’s Leader recognition in the 2026 Nucleus Research WFM Value Matrix also shows that retailers still reward vendors that join forecasting, scheduling, and store execution in one environment.

The competitive pattern suggests that scale alone is not enough in the workforce management (WFM) in retail market. Large vendors hold an advantage in installed base and ecosystem reach, but specialist providers are still winning business when they show stronger predictive accuracy or deeper retail workflows. Switching costs are rising as retailers standardize labor, payroll, communication, and compliance tools in a single environment, which makes integration breadth a major barrier for new entrants. At the same time, the market still leaves room for targeted disruption because many retailers continue to struggle with fragmented systems, uneven store execution, and weak trust in schedule quality.

Workforce Management (WFM) In Retail Industry Leaders

UKG Inc.

Dayforce

WorkForce Software, LLC

Quinyx AB

Legion Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Logile named Leader in Nucleus Research WFM Value Matrix for unified AI platform across 40,000+ locations.

- March 2026: UKG showcased AI-led Workforce Operating Platform with optimization, attrition detection, payroll integrity, and hiring tools.

- January 2026: ATOSS posted record FY2025 revenue EUR 189.3 million (USD 204.4 million), guided FY2026 at approximately EUR 215 million (USD 232.2 million), driven by cloud growth.

- January 2026: Legion launched 90+ AI innovations, reported 216% revenue growth, expanded to 35 countries.

Global Workforce Management (WFM) In Retail Market Report Scope

The Workforce Management (WFM) in Retail Market refers to software and service platforms designed to optimize workforce operations across retail enterprises. These solutions include employee scheduling, time and attendance management, workforce analytics and forecasting, leave and absence management, task execution, and employee self-service communication. Deployed via cloud, on-premises, or hybrid models, WFM platforms serve both large and small retailers across formats such as grocery, fashion, electronics, department stores, specialty retail, convenience stores, and e-commerce. They enhance labor efficiency, ensure compliance, reduce costs, and improve employee engagement to support seamless retail operations globally.

The Workforce Management (WFM) in Retail Market is segmented by Component (Software [Employee Scheduling and Labor Optimization, Time and Attendance Management, Workforce Analytics and Forecasting, Leave and Absence Management, Task and Execution Management, Employee Self-service and Communication] and Services), Deployment Mode (Cloud, On-premises, and Hybrid), Enterprise Size (Large Enterprises and Small and Medium-sized Enterprises), Retail Format (Grocery and Supermarkets, Fashion and Apparel, Electronics Retail, Department Stores, Specialty Retail, Convenience Stores, and E-commerce Retailers), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Employee Scheduling and Labor Optimization |

| Time and Attendance Management | |

| Workforce Analytics and Forecasting | |

| Leave and Absence Management | |

| Task and Execution Management | |

| Employee Self-service and Communication | |

| Services |

| Cloud |

| On-premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Grocery & Supermarkets |

| Fashion & Apparel |

| Electronics Retail |

| Department Stores |

| Specialty Retail |

| Convenience Stores |

| E-commerce Retailers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Component | Software | Employee Scheduling and Labor Optimization |

| Time and Attendance Management | ||

| Workforce Analytics and Forecasting | ||

| Leave and Absence Management | ||

| Task and Execution Management | ||

| Employee Self-service and Communication | ||

| Services | ||

| By Deployment Mode | Cloud | |

| On-premises | ||

| Hybrid | ||

| By Enterprises Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By Retail Format | Grocery & Supermarkets | |

| Fashion & Apparel | ||

| Electronics Retail | ||

| Department Stores | ||

| Specialty Retail | ||

| Convenience Stores | ||

| E-commerce Retailers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the workforce management (WFM) in retail market?

The workforce management (WFM) in retail market was valued at USD 1.54 billion in 2025 and is projected to grow from USD 1.73 billion in 2026 to USD 3.09 billion by 2031 at a CAGR of 12.30%.

Which component leads spending in retail workforce platforms?

Software led the market with 71.24% share in 2025, reflecting retailer focus on scheduling, labor optimization, analytics, and payroll-linked execution.

Why are retailers adopting AI-based scheduling faster now?

Retailers are facing tighter labor budgets, more complex omnichannel tasks, and stricter compliance rules. AI scheduling helps improve roster accuracy, reduce overtime, and respond faster to demand changes.

Which deployment model is most widely used by retailers?

Cloud remained the leading deployment model with 66.38% share in 2025 because it supports faster updates, easier scaling, and quicker access to AI and compliance features.

Which retail format is growing fastest for workforce management tools?

E-commerce retailers are expected to post the fastest growth at a 15.41% CAGR through 2031 because fulfillment labor, returns management, and order spikes require more dynamic scheduling.

Which region is creating the strongest growth opportunity through 2031?

Asia-Pacific is forecast to grow the fastest at a 13.02% CAGR, supported by organized retail expansion, rising AI adoption, and broader formalization of labor planning across regional markets.

Page last updated on: