Workforce Management (WFM) In Contact Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.34 Billion |

| Market Size (2031) | USD 0.57 Billion |

| Growth Rate (2026 - 2031) | 10.89% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Workforce Management (WFM) In Contact Centers Market Analysis by Mordor Intelligence

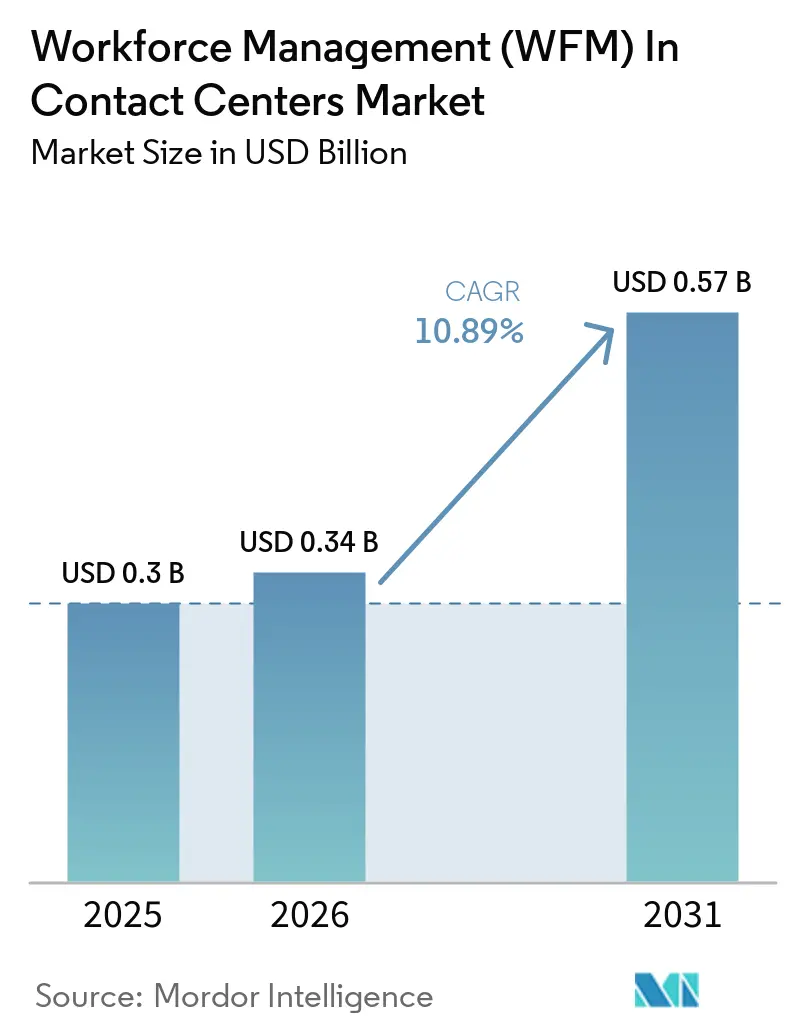

The workforce management (WFM) in contact centers market was valued at USD 0.30 billion in 2025 and is estimated to grow from USD 0.34 billion in 2026 to USD 0.57 billion by 2031, at a CAGR of 10.89% during the forecast period (2026-2031). The market is expanding because contact center operators are shifting from reactive staffing to continuous workforce planning that relies on forecasting, scheduling, and intraday control within a single operating layer. The workforce management (WFM) in contact centers market is also changing, as enterprises now need to coordinate human agents, AI virtual agents, and outsourced teams simultaneously, which raises planning complexity far beyond what older tools were built to handle. Product competition is driving measurable gains in forecast accuracy, faster configuration, and tighter integration with broader customer experience platforms, pushing vendors to refresh their roadmaps more quickly. Cloud delivery, AI-enabled workflows, and the spread of contact center-as-a-service platforms are widening adoption across both mature and developing contact center environments. Even with slower legacy replacement and rising compliance efforts, the WFM market in contact centers retains strong momentum because buyers still need better visibility into labor use, service levels, and operational flexibility.

Key Report Takeaways

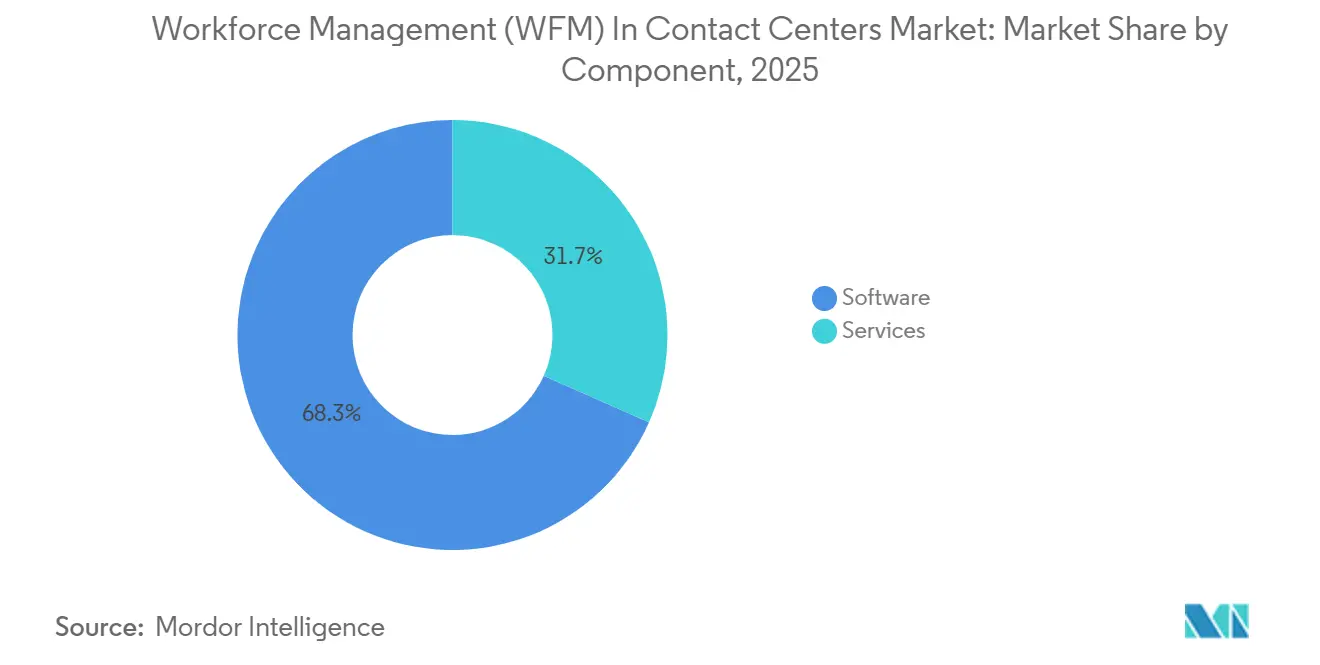

- By component, software led with a 68.34% share of the workforce management (WFM) in contact centers market in 2025, while services are forecast to expand at a 12.34% CAGR during 2026-2031.

- By deployment model, cloud held a 63.21% share of the workforce management (WFM) in contact centers market in 2025, while hybrid is projected to grow at a 10.92% CAGR during 2026-2031.

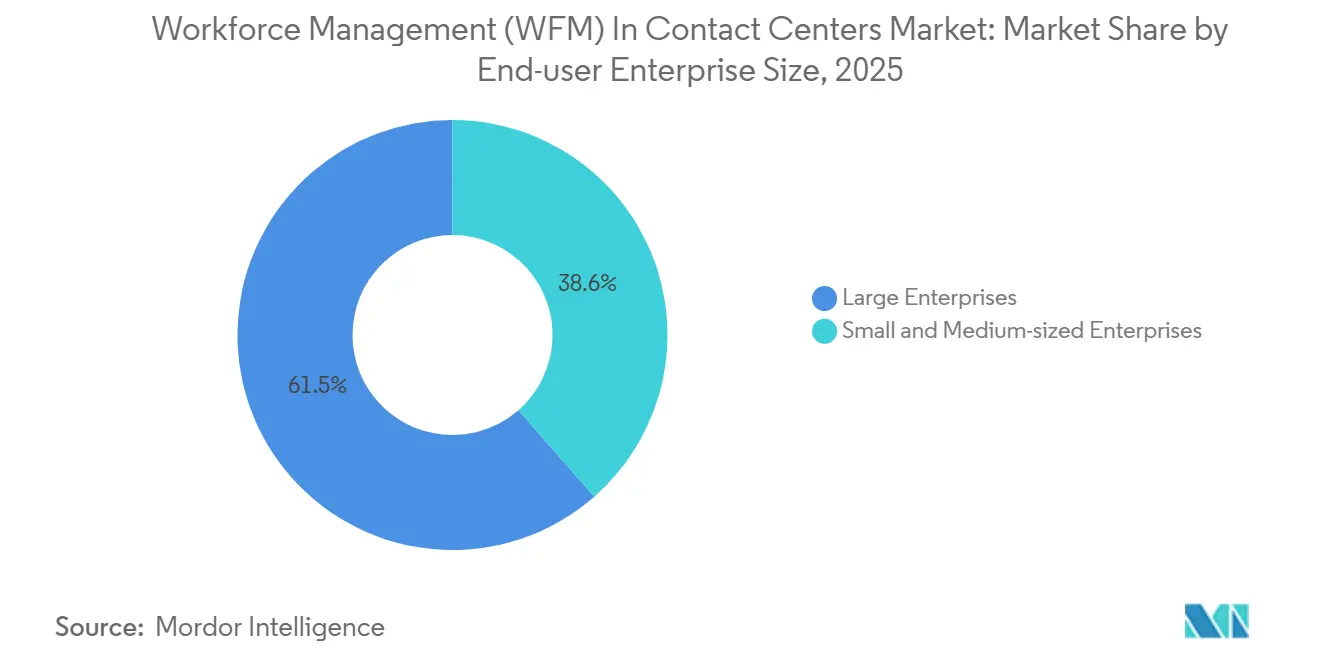

- By enterprise size, large enterprises accounted for 61.45% of the workforce management (WFM) market in contact centers in 2025, while small and medium-sized enterprises are expected to advance at a 11.33% CAGR through 2031.

- By end-user industry, outsourced contact centers and BPOs captured 27.88% share of the WFM in the contact centers market in 2025, while healthcare is projected to record an 11.44% CAGR during 2026-2031.

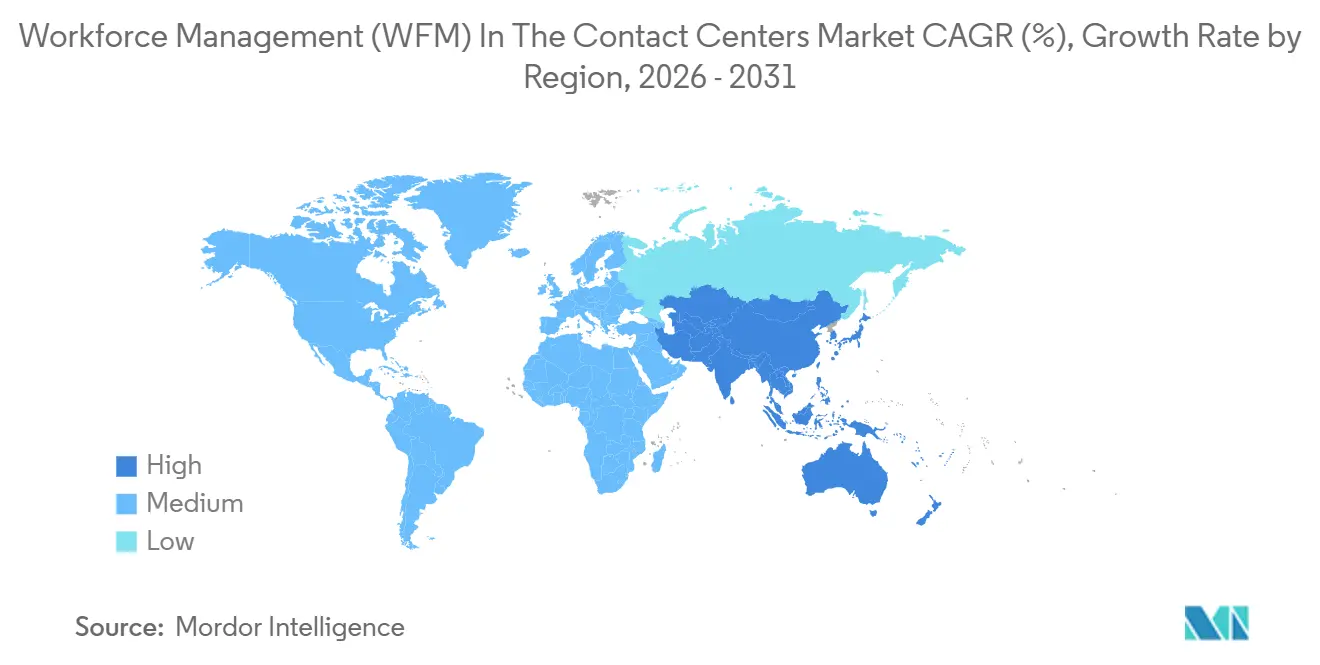

- By geography, North America held 42.17% share of the workforce management (WFM) in contact centers market in 2025, while the Asia-Pacific is forecast to grow at a 12.14% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Workforce Management (WFM) In Contact Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Forecasting and Scheduling Adoption | +2.5% | Global, with early gains in North America, APAC, and Northern Europe | Short term (≤ 2 years) |

| Rising Cloud-Native CCaaS Migration | +2.2% | Global, highest velocity in APAC and North America | Short term (≤ 2 years) |

| Omnichannel and Asynchronous Workload Complexity | +1.5% | Global, most acute in North America and Western Europe | Medium term (2-4 years) |

| Agent Flexibility and Retention Prioritization | +1.2% | Global, with emphasis in high-attrition markets, North America, Australia, and South America | Medium term (2-4 years) |

| Human and AI-Agent Capacity Planning Convergence | +0.9% | Global, early adopters in IT and telecom, and BFSI in North America and APAC | Medium term (2-4 years) |

| WFM as The Orchestration Layer Across CCaaS, CRM, HR, And QA | +0.7% | North America and Europe core, with spillover to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Forecasting and Scheduling Adoption

AI-led forecasting has become a core buying requirement in the workforce management (WFM) in contact centers market, rather than an optional feature added late in a procurement cycle. NICE states that AI-based forecasting and scheduling in contact centers can narrow forecasting error from the typical legacy range of ±20% to ±5-8%, thereby directly affecting staffing costs and service performance.[1]NICE Ltd., “AI-Powered Workforce Management Software for Contact Centers,” NICE, nice.com That improvement is also changing the day-to-day role of planning teams because the platform handles more of the routine model work, while analysts spend more time on interpretation, exception handling, and operational decisions. Verint linked its roadmap to Amazon Web Services and Amazon Bedrock for large language model workloads, and the company said customers may see up to 50% better forecasting accuracy over the next 24 months. This raises the standard for the wider workforce management market in contact centers, as buyers now expect tangible accuracy gains, not just broader feature lists. A 2026 peer-reviewed study in the International Journal of Intelligent Systems and Applications in Engineering also found that real-time demand prediction and natural-language access to operational data are moving workforce planning away from static planning toward continuous operational control.[2]Vikas Prasad, “AI-Driven Workforce Optimization in Enterprise Contact Centers: From Static Planning to Continuous, Human-Centered Operations,” International Journal of Intelligent Systems and Applications in Engineering, ijisae.org

Rising Cloud-Native CCaaS Migration

Cloud migration is one of the clearest growth drivers for the workforce management (WFM) in contact centers market, as WFM replacements often occur alongside broader contact center platform renewals. NICE describes cloud-based workforce management as a way to deliver AI-powered forecasting, scheduling, and intraday management with continuous updates, which matches the operating model enterprises now want from broader contact center software.[3]NICE Ltd., “Forecasting and Scheduling with AI in Contact Centers,” NICE, nice.com Aspect’s 2025 transition guidance also points to phased cloud adoption as a practical route for moving core WFM workloads away from legacy environments without disrupting day-to-day operations. That migration path matters because workforce management in the contact center market benefits when buyers replace outdated infrastructure and seek tighter integration between interaction data, staffing logic, and real-time automation. The March 2026 partnership between Aspect Software and Five9 demonstrated how vendors are tying WFM more closely to cloud interaction platforms through real-time agent-state data and automated intraday staffing adjustments. As more enterprises commit to cloud ecosystems, platform choice increasingly shapes the WFM pathway they follow throughout the deployment lifecycle.

Omnichannel and Asynchronous Workload Complexity

The workforce management (WFM) in contact centers market is gaining traction amid the shift toward digital, asynchronous work that no longer fits the old voice-first planning model. Genesys added workitem support to workforce management in September 2025, including forecasting, capacity planning, and intraday monitoring for ACD-routed workitems, demonstrating how vendors are adapting their planning logic to newer forms of contact center demand. This matters because email, ticketing, and other queued digital tasks create uneven workloads that need workload-state planning rather than simple queue-based assumptions. NICE also highlights capabilities such as concurrent chat scheduling and discrete event simulation, which point to a broader move toward more granular planning for blended interaction types. In practice, the workforce management market in contact centers is being driven by operators that need a single planning layer for voice, digital, back-office, and hybrid work, without losing visibility into skill use or schedule performance. As a result, vendors that handle mixed work types well are better placed to win deployments where service goals depend on flexibility across multiple channels simultaneously.

Agent Flexibility and Retention Prioritization

Retention pressure is now shaping buying behavior in the workforce management (WFM) in contact centers market, as scheduling quality directly affects agent experience and supervisor workload. Calabrio’s Agent Assist supports natural-language schedule self-service in more than 50 languages, demonstrating how vendors are building ease of use into the scheduling layer rather than leaving those tasks to manual supervisor effort. This changes the value discussion because self-service scheduling is no longer only an employee convenience; it also reduces routine admin work that limits coaching time and slows decision-making. A May 2025 GPAI and OECD study across five South American markets found that AI augmentation in call centers was associated with a 10% reduction in average handle time while headcount remained broadly stable, suggesting that human tasks are becoming more complex as automation absorbs simpler interactions. That pattern supports greater investment in flexible scheduling, intraday changes, and improved workload visibility across the contact center workforce management market. It also means planners need tools that respond to changes in interaction difficulty, not only changes in contact volume.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Stack Integration Complexity | -1.4% | Global, most severe in North America and Europe where 10+ year proprietary ACD-WFM integrations persist | Medium term (2-4 years) |

| Data Privacy and Algorithmic Governance Burden | -1.0% | Europe, North America, and other regulated markets | Short term (≤ 2 years) |

| Fragmented Scheduling Rules Across In-House and Outsourced Teams | -0.7% | Global, amplified in multi-geography BPO operations in APAC and South America | Medium term (2-4 years) |

| Agent Pushback Against Intraday Automation and Perceived Fairness Risks | -0.4% | North America and Western Europe, especially unionized settings and the DACH region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Stack Integration Complexity

Legacy integration remains one of the most persistent barriers in the workforce management (WFM) in contact centers market because many large contact centers still rely on deeply customized connections between ACDs, WFM tools, QA platforms, and HR systems. Aspect’s cloud transition guidance supports phased migration precisely because many organizations cannot move all workforce processes at once without risking disruption to scheduling, adherence, and reporting.[4]Aspect, “5 Steps to Transition to a Cloud-Based WEM Solution,” Aspect, aspect.com NICE also positions its platform around broad integration with forecasting, scheduling, intraday management, and channel-level planning, which reflects how much buyers now care about unifying disconnected operational workflows. The difficulty is not only technical, because legacy rule sets often contain years of overtime policies, site practices, and compliance logic that need to be accurately rebuilt in the new system. That slows deal conversion and extends deployment work across the workforce management in contact centers market, especially in large enterprises with multiple sites and business units. Vendors with stronger connectors, migration services, and deeper configuration are therefore better placed when procurement teams see implementation risk as the main decision point.

Data Privacy and Algorithmic Governance Burden

Governance demands are becoming a more visible restraint on workforce management (WFM) in contact centers market, as buyers want clearer evidence that AI-led decisions can be explained, monitored, and managed responsibly. Calabrio announced in September 2025 that it had achieved ISO 42001:2023 certification for responsible AI management, and that move is becoming increasingly relevant as procurement teams increasingly view AI governance as part of product readiness rather than solely a legal review item. This is especially important when scheduling, adherence, or performance logic depends on machine-generated recommendations that directly affect employees. Verint’s focus on agentic AI and large language model support also points to a market where governance expectations will rise as automation becomes more central to daily planning decisions. The effect is a longer review cycle for some deployments because technical fit now sits alongside questions about controls, documentation, and human oversight. In the workforce management (WFM) in contact centers market, it does not remove demand; rather, it adds more work before enterprise buyers move from pilot activity to wider production use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Reframes The Revenue Model

Software accounted for 68.34% of the workforce management (WFM) in contact centers market in 2025, underscoring that platforms remain the primary focus of spending even as service demand rises. Employee scheduling and labor optimization accounted for 32.56% of software revenue, making it the largest software sub-segment in the current revenue mix. Workforce analytics and forecasting, along with time and attendance management, also remain important, as AI investment is boosting buyer interest in tools that improve planning accuracy and give supervisors better operational visibility. NICE positions its workforce management suite around AI-powered scheduling, forecasting, and simulation for contact centers, which reflects the feature depth enterprise buyers now expect from the software layer. The software side of workforce management in the contact center industry also benefits from growing demand for self-service access and clearer schedule transparency, particularly as hybrid work has made schedule changes more frequent.

Services are the fastest-growing component of the workforce management (WFM) in contact centers market, with a 12.34% CAGR during 2026-2031, indicating that buyers increasingly need help after the software sale. Many deployments now require configuration, integration, governance setup, and ongoing optimization support before enterprises can realize the full value of the platform. This is especially relevant in large BPO environments where operational rules are complex and in-house WFM expertise is often stretched across several client programs. Assembled’s August 2025 launch of Support Orchestration, built to balance AI agents, human teams, and BPO partners in a single operating view, points to a service-heavy environment where rollout and operating design matter as much as the software itself. As workforce management (WFM) in the contact center market matures, vendors with strong implementation and post-deployment teams are likely to capture more value than providers that rely solely on license revenue.

By Deployment Model: Hybrid Adoption Reflects Regulatory And Operating Needs

Cloud accounted for 63.21% of the workforce management (WFM) in contact centers market in 2025, underscoring buyers' preference for scalable delivery and faster product updates. The appeal of the cloud is not only lower operational friction; it also enables WFM platforms to more easily use real-time data from contact centers, CRM, and HR systems than in older on-premises environments. NICE presents cloud-based workforce management as part of a broader operating stack that supports forecasting, scheduling, intraday management, and omnichannel control in one environment. That architecture matters because workforce management in the contact center market now depends on faster release cycles and closer integration with the wider customer experience technology stack. In practical terms, cloud has become the default model where enterprises want regular AI updates and simpler access for distributed teams.

Hybrid is expanding at a 10.92% CAGR during 2026-2031, which makes it the fastest-growing deployment model in the market. The pattern reflects buyers in healthcare, government, and BFSI that still need some data or process controls to remain on local infrastructure while adopting cloud analytics and planning logic where possible. Aspect’s 2025 migration guidance outlined a phased approach that begins with less critical WEM workloads before moving core functions later, supporting the idea that hybrid is a deliberate architecture rather than merely a temporary stage. On-premises tools remain relevant in highly regulated settings, but the hardest remaining migrations are also the slowest because old audit rules, governance models, and internal approval structures do not change quickly. The workforce management (WFM) in contact centers market, therefore, shows a split pattern: cloud leads overall adoption, while hybrid captures the strongest growth, where regulation and operational pragmatism both matter.

By End-User Enterprise Size: SME Adoption Broadens The Buyer Base

Large enterprises accounted for 61.45% of the workforce management (WFM) in contact centers market in 2025, supported by their broader site networks, higher agent counts, and more complex scheduling demands. These buyers typically need multi-skill planning, integration with QA and HR systems, and stronger reporting across several operating units, which keeps them at the center of premium WFM spending. NICE said its workforce management solutions are deployed across more than 3.3 million seats globally, and the company also cited a 33.8% seat share in DMG Consulting’s 2025 workforce management report, which shows how concentrated large-enterprise demand remains around a few leading vendors. The workforce management market in contact centers continues to rely on this buyer group for high-value deals because implementation depth and integration breadth matter most at scale. Large enterprise demand also shapes roadmap priorities, as these customers often require back-office planning, governance controls, and advanced intraday functionality within the same deployment.

Small and medium-sized enterprises are the fastest-growing segment, with a 11.33% CAGR through 2031, and that shift is broadening the addressable base for vendors. SaaS packaging and easier access to AI-enabled forecasting have reduced the need for smaller operators to build specialist planning teams before adopting WFM tools. The market is also benefiting from growth in mid-sized BPO operations, which face complex scheduling needs without the budget or IT depth required for heavyweight enterprise platforms. Assembled’s product positioning around unified planning across in-house teams, BPO partners, and AI agents is especially relevant for these smaller operations because they need simpler deployment without losing visibility into changing demand. This leaves the workforce management (WFM) in contact centers market with a wider buyer mix than before, where ease of use and fast time to value matter almost as much as feature depth.

By End-User Industry: BPO Scale And Healthcare Demand Create A Two-Speed Pattern

Outsourced contact centers and BPOs held a 27.88% share in 2025, making them the largest vertical in the workforce management (WFM) in contact centers market. Their lead reflects the operational intensity of multi-client delivery, where staffing rules, service targets, and data handling requirements can vary across accounts and geographies. In these settings, workforce planning has direct commercial value because missed schedules or weak intraday control can simultaneously affect service levels, client retention, and margins. Assembled’s Support Orchestration launch in August 2025 was explicitly designed to manage in-house teams, BPO partners, and AI agents in a single view, demonstrating how vendor strategy is aligning with the actual operating model used by outsourced service providers. The workforce management market in contact centers, therefore, continues to depend on BPO demand as a large, structurally complex source of recurring spending.

Healthcare is projected to grow at an 11.44% CAGR during 2026-2031, making it the fastest-growing vertical in the market. Growth in this segment comes from the need to document staffing discipline, support patient access, and manage after-hours and multilingual service environments more carefully than before. These contact centers face workload swings that are hard to plan with static tools, which increases the value of forecasting, schedule transparency, and intraday control. Other verticals remain important, but they exhibit different demand patterns: BFSI and government are more shaped by data controls, while retail and e-commerce benefit from tools that can respond quickly to promotional peaks and seasonal surges. That leaves the workforce management (WFM) market in the contact centers with a clear two-speed structure, where outsourced operations drive scale and healthcare drives some of the strongest incremental growth.

Geography Analysis

North America accounted for 42.17% of the workforce management (WFM) in contact centers market share in 2025, making it the largest regional contributor. The region benefits from dense contact center infrastructure, established buying cycles, and high demand for scheduling records that support labor compliance and operational accountability. The United States remains the anchor market because large enterprise contact centers and major vendors are concentrated there, while Canada adds complexity through bilingual service requirements, and Mexico supports growth through expanding nearshore service operations. Within the workforce management (WFM) market in the contact centers market, North American demand is also shaped by the need to modernize legacy environments without disrupting live operations, which keeps migration and service support central to most deployments.

Europe ranked second in 2025, supported by mature contact center operations across the United Kingdom, Germany, France, and the Nordic countries. The region combines strong demand for workforce control with a tighter regulatory environment, which raises the value of auditability while also extending deployment effort for AI-enabled functions. Western European buyers are therefore showing greater interest in hybrid architectures that can balance data handling expectations with access to newer forecasting and analytics tools. This pattern is meaningful for the workforce management (WFM) market in the contact centers market because vendors with regional infrastructure and stronger governance can compete more effectively when compliance reviews are a major part of procurement.

Asia-Pacific is the fastest-growing region, with a 12.14% CAGR during 2026-2031, led by continued expansion in India and the Philippines, where BPO capacity and cloud-first deployment practices support faster adoption. The region benefits from newer contact center estates across many markets, making platform replacement and cloud-based rollouts easier than in regions with greater legacy technical debt. Japan, South Korea, and Australia add enterprise-grade demand, with Australia standing out for workforce compliance complexity that has pushed vendors to build more specialized planning support. Nimbus positions its contact center platform around softphone integration and compliance-focused workforce management for this environment, reflecting how local labor and operating rules can shape product design.CLOUD. South America, the Middle East, and Africa remain smaller in revenue terms, but they remain relevant because nearshore BPO activity, government digitization programs, and expanding service operations continue to create new opportunities for workforce management (WFM) in contact centers market.

Competitive Landscape

The workforce management (WFM) in contact centers market entered 2026 with a more concentrated top tier following the Thoma Bravo-led combination of Verint and Calabrio, which closed in late 2025 at an enterprise value of USD 2 billion. Verint later said the combined organization serves workflows for around 5 million agents across more than 100 countries, while preserving Calabrio product lines and customer workflows under the Verint brand. NICE still holds a strong leadership position, and the company cited a 33.8% total WFM seat share in DMG Consulting’s 2025 report, which reinforces its scale in large enterprise deployments. This leaves the workforce management (WFM) in contact centers market with a leadership group that is both larger and more integrated than before the recent round of consolidation.

The next competitive layer is being shaped by product expansion and ecosystem reach rather than only raw feature count. Genesys added AI time-off management agents and work team management via natural language commands in April 2026, demonstrating how major vendors are extending workforce functionality into more agentic operating models. NICE also deepened its Salesforce relationship in August 2025 by participating in the Salesforce Zero Copy Partner Network, which supports stronger data movement for customer service workflow orchestration and can improve planning visibility for workforce management use cases. The March 2026 partnership between Aspect Software and Five9 is another example of strategic alignment around real-time agent data and automated staffing actions, which is becoming a key selling point in cloud-led deals. In the workforce management (WFM) in contact centers market, these moves show that integration strength and workflow orchestration now matter as much as classic forecasting and scheduling capabilities. Vendors that connect naturally with CCaaS, CRM, QA, and HR platforms are likely to convert enterprise opportunities more effectively than providers that still rely on narrow, standalone positioning.

The challenger field remains active even as the upper tier becomes more concentrated. Talkdesk launched the CXA Operations Center in March 2026 to provide unified oversight of AI and human agents as one workforce, signaling how quickly the market is moving toward mixed-capacity planning rather than human-only scheduling. Alvaria’s September 2025 restructuring reduced debt by more than 75% and attracted new investment, giving the company more room to accelerate product development and compete more aggressively in workforce management and contact center automation. The workforce management (WFM) in contact centers market in contact centers, therefore, remains competitive at the lower tiers, but current momentum favors vendors that combine product breadth, partner reach, and the ability to manage both human and AI operating models in a single environment.

Workforce Management (WFM) In Contact Centers Industry Leaders

NICE Ltd.

Genesys Cloud Services, Inc.

Verint Systems Inc.

Calabrio, Inc.

Alvaria, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Microsoft added Service Operations Agent in Dynamics 365 Contact Center, automating queue setup, prioritization, and diagnostics.

- April 2026: Verint and Calabrio merger completed under Verint brand, now serving 5M agents across 100+ countries.

- March 2026: Aspect partnered with Five9 to integrate real-time agent data and automate staffing adjustments.

- March 2026: Talkdesk launched CXA Operations Center, unifying oversight of AI and human agents with observability and automation mining.

Global Workforce Management (WFM) In Contact Centers Market Report Scope

The Workforce Management (WFM) in Contact Centers Market refers to software and service platforms designed to optimize workforce operations across customer service and support environments. These solutions include employee scheduling, time and attendance management, workforce analytics and forecasting, leave and absence management, task execution, and employee self-service communication. Delivered through cloud, on-premises, or hybrid models, WFM platforms serve both large enterprises and SMEs across industries such as BFSI, IT and telecom, healthcare, retail, travel, government, and outsourced BPOs. They help improve agent productivity, ensure compliance, reduce labor costs, and enhance customer experience by aligning staffing with demand in real time.

The Workforce Management (WFM) in Contact Centers Market is segmented by Component (Software [Employee Scheduling and Labor Optimization, Time and Attendance Management, Workforce Analytics and Forecasting, Leave and Absence Management, Task and Execution Management, and Employee Self-service and Communication], and Services), Deployment Model (Cloud, On-premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-sized Enterprises), End-user Industry (BFSI, IT and Telecom, Healthcare, Retail and E-commerce, Travel and Hospitality, Government and Public Sector, and Outsourced Contact Centers and BPOs), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Employee Scheduling and Labor Optimization |

| Time and Attendance Management | |

| Workforce Analytics and Forecasting | |

| Leave and Absence Management | |

| Task and Execution Management | |

| Employee Self-service and Communication | |

| Services |

| Cloud |

| On-premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| BFSI |

| IT and Telecom |

| Healthcare |

| Retail and E-commerce |

| Travel and Hospitality |

| Government and Public Sector |

| Outsourced Contact Centers and BPOs |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | Employee Scheduling and Labor Optimization |

| Time and Attendance Management | ||

| Workforce Analytics and Forecasting | ||

| Leave and Absence Management | ||

| Task and Execution Management | ||

| Employee Self-service and Communication | ||

| Services | ||

| By Deployment Model | Cloud | |

| On-premises | ||

| Hybrid | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By End-user Industry | BFSI | |

| IT and Telecom | ||

| Healthcare | ||

| Retail and E-commerce | ||

| Travel and Hospitality | ||

| Government and Public Sector | ||

| Outsourced Contact Centers and BPOs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and projected size of the workforce management (WFM) in contact centers market?

The workforce management (WFM) in contact centers market was valued at USD 0.30 billion in 2025, stood at USD 0.34 billion in 2026, and is forecast to reach USD 0.57 billion by 2031 at a CAGR of 10.89%.

Which component leads revenue in workforce management (WFM) in contact centers market?

Software led the market with 68.34% share in 2025, while services is growing faster at a 12.34% CAGR as buyers seek integration, configuration, and optimization support.

Why are cloud and hybrid deployments gaining traction in contact center WFM?

Cloud held 63.21% share in 2025 because buyers want scalability and faster updates. Hybrid is growing fastest at 10.92% CAGR because regulated sectors still need partial local control over data and workflows.

Which customer group is expanding fastest in workforce management (WFM) in contact centers market?

Small and medium-sized enterprises are growing fastest at an 11.33% CAGR through 2031, supported by SaaS delivery, easier AI access, and lower upfront commitment.

Which end-user vertical creates the strongest demand for these solutions?

Outsourced contact centers and BPOs held the largest share at 27.88% in 2025 because they manage complex multi-client staffing models. Healthcare is the fastest-growing vertical at 11.44% CAGR due to patient service, compliance, and scheduling complexity.

Which region offers the strongest growth opportunity through 2031?

Asia-Pacific is the fastest-growing region at a 12.14% CAGR, supported by BPO expansion in India and the Philippines, newer contact center estates, and strong cloud-first adoption patterns.

Page last updated on: