Window Air Conditioner (AC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.93 Billion |

| Market Size (2031) | USD 25.24 Billion |

| Growth Rate (2026 - 2031) | 3.81% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

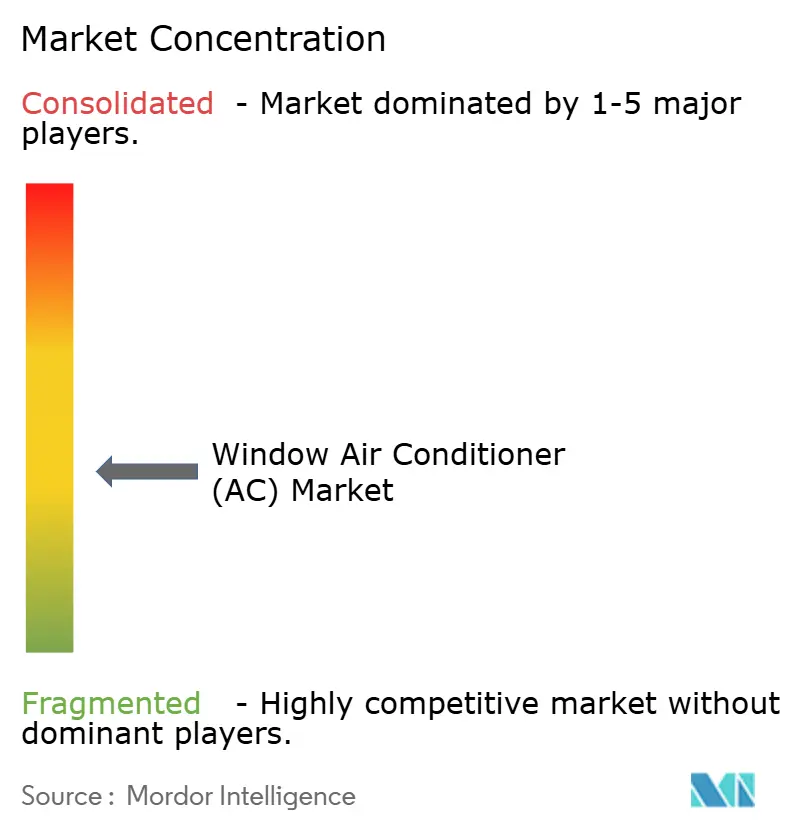

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Window Air Conditioner (AC) Market Analysis by Mordor Intelligence

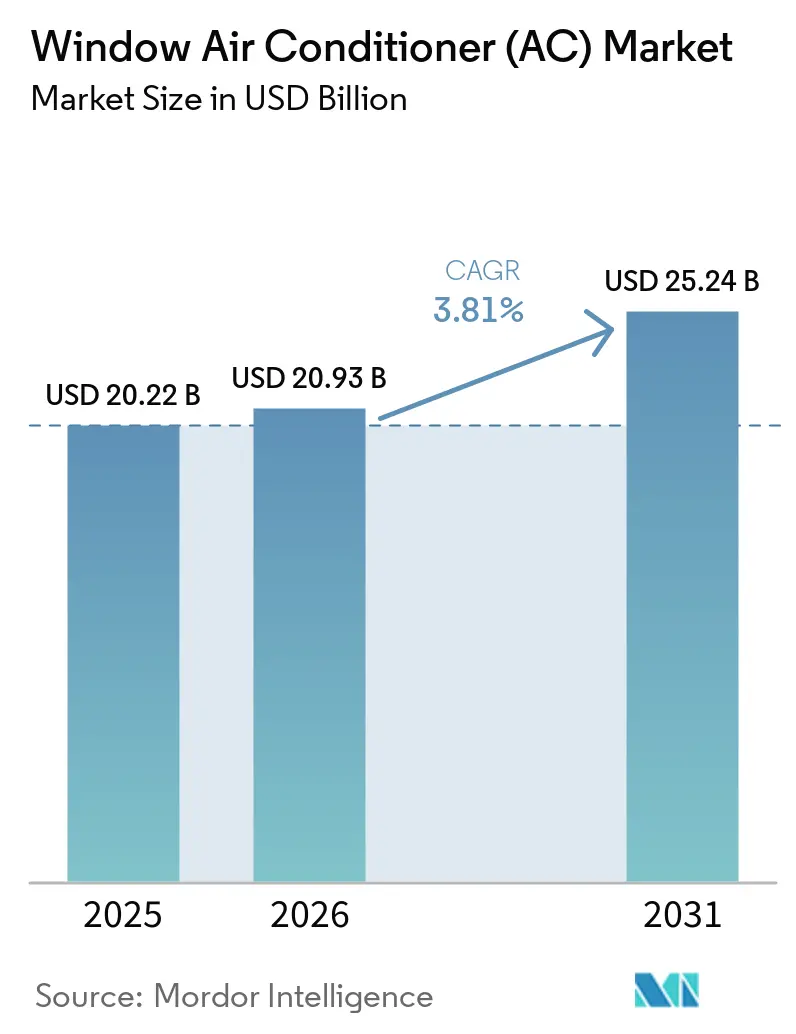

The window air conditioner market size was valued at USD 20.22 billion in 2025 and is estimated to grow from USD 20.93 billion in 2026 to reach USD 25.24 billion by 2031, at a CAGR of 3.81% during the forecast period 2026-2031. Growth continues to rest on the product’s simple installation model, as the unit combines the full cooling system into a single enclosure and fits spaces where ductwork, wall penetrations, and outdoor compressor placement are difficult or costly. Demand in the window air conditioner market is being supported by first-time household purchases in emerging economies and by replacement demand in mature countries where older room cooling units are nearing the end of their normal operating life. Higher summer heat is also keeping purchase urgency elevated, and the International Energy Agency linked each 1°C rise in India’s outdoor temperatures to nearly 7 gigawatts of additional peak electricity demand, which supports continued room AC adoption and efficiency upgrades [1]International Energy Agency, “Cooling,” International Energy Agency, iea.org. Regulatory changes are tightening the replacement cycle because the United States Department of Energy updated room air conditioner efficiency standards for units manufactured or imported on or after May 26, 2026, and India’s 2026 BEE rules also pushed portfolio refreshes across brands. Even with rising competition from split systems in higher-income urban households, the window air conditioner market retains a durable role in compact housing, rental units, and budget-led purchases where installation speed and lower upfront cost still matter most.

Key Report Takeaways

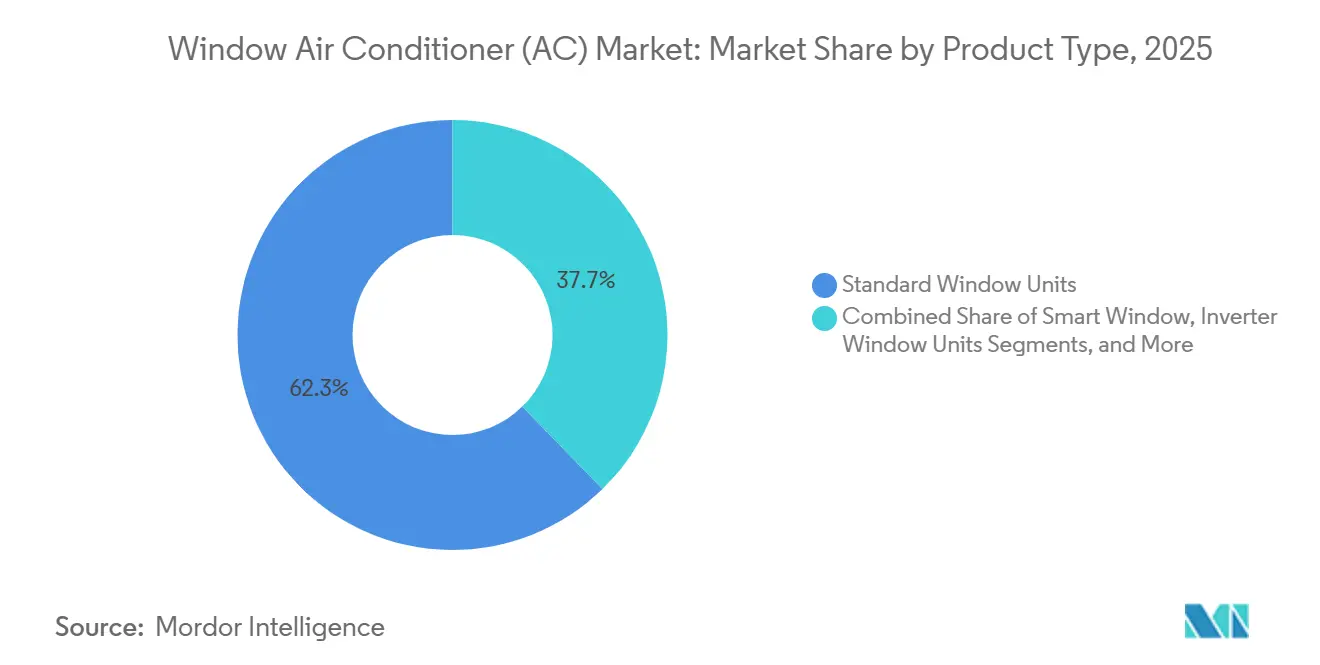

- By product type, standard window units accounted for 62.3% of revenue in the window air conditioner market in 2025, while smart window units are projected to rise at a 4.89% CAGR through 2031.

- By capacity, the 5,000 to 8,000 BTU band accounted for 58.1% of revenue in 2025 in the window air conditioner market, while the above 20,000 BTU band is forecast to grow at a 4.54% CAGR through 2031.

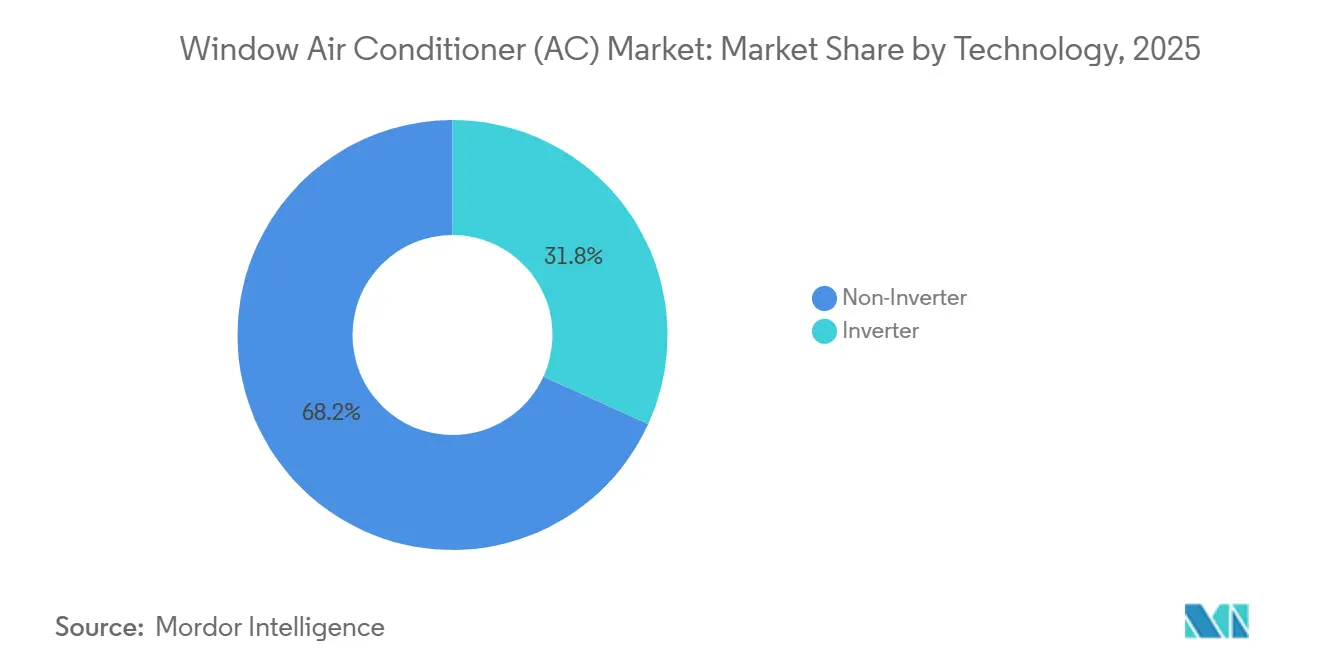

- By technology, non-inverter units captured 68.2% of the window air conditioner market share in 2025 in the window air conditioner market, while inverter units are expected to record the highest CAGR at 5.11% through 2031.

- By end user, residential users accounted for 72.1% of revenue in the window air conditioner market in 2025, while commercial users are projected to grow at a 4.48% CAGR through 2031.

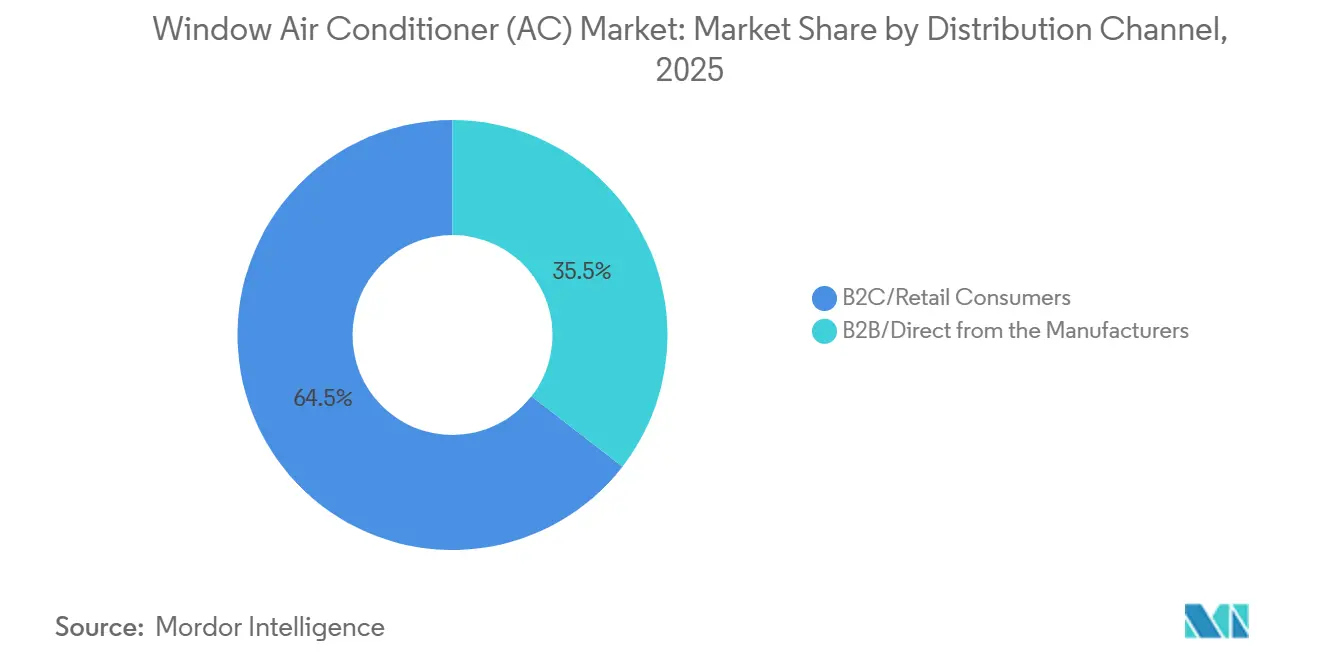

- By distribution channel, B2C and retail consumers accounted for 64.5% of revenue in 2025 in the window air conditioner market, while B2B and direct-from-manufacturer channels are set to expand at a 4.15% CAGR through 2031.

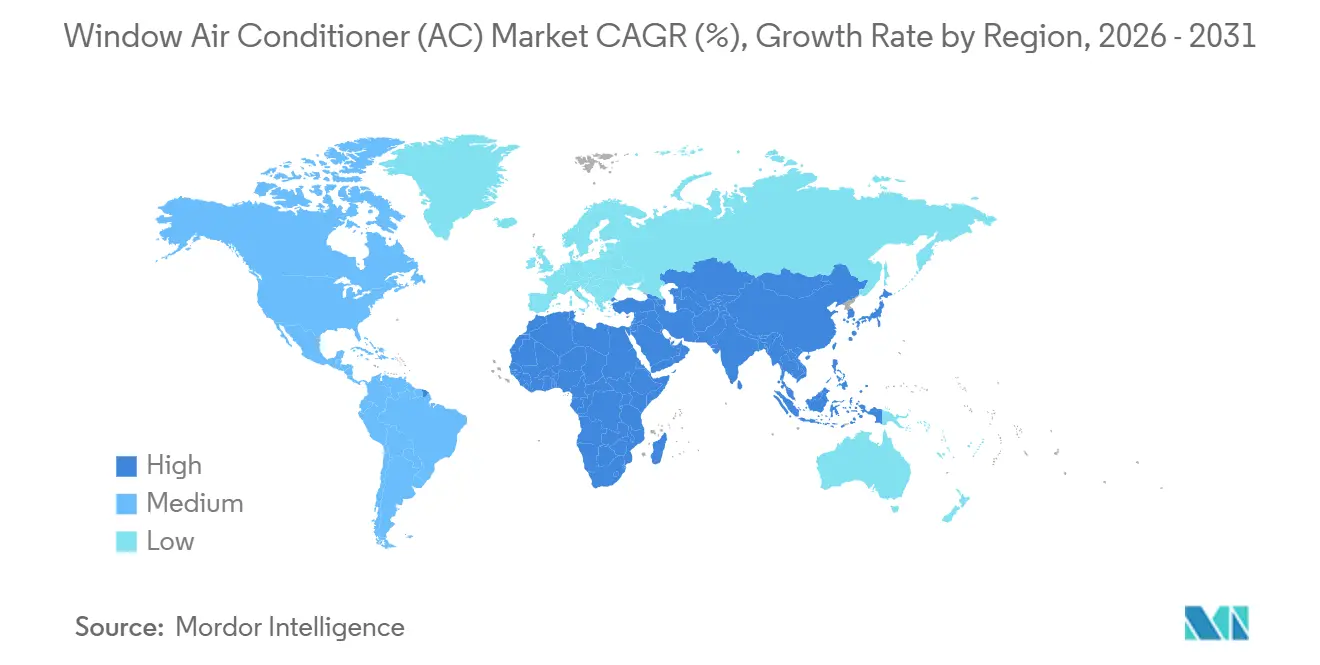

- By geography, Asia-Pacific accounted for 41.3% of the window air conditioner market size in 2025 and is projected to expand at a 5.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Window Air Conditioner (AC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Heat Stress And Longer Cooling Seasons | +1.0% | Global, concentrated in South Asia, MENA, Sub-Saharan Africa, and Southeast Asia | Short term (≤ 2 years) |

| Replacement Demand From Aging Room Cooling Stock | +0.7% | North America, India, China, and Japan | Medium term (2-4 years) |

| Energy Efficiency Standards Pushing Technology Upgrades | +0.5% | North America, India, and Europe | Medium term (2-4 years) |

| Space-Constrained Urban Housing Favoring Window ACs | +0.4% | India, Southeast Asia, North America, and West Africa | Long term (≥ 4 years) |

| Low-GWP Refrigerant Transition Unlocking Premium Replacements | +0.3% | North America, Europe, India, and Southeast Asia | Medium term (2-4 years) |

| Rental Housing And Temporary Occupancy Demand | +0.2% | North America, Western Europe, and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Heat Stress And Longer Cooling Seasons

The window air conditioner market is benefiting from stronger cooling demand as high-temperature periods become more frequent across several large population centers. Delhi and nearby areas recorded peak outdoor temperatures of 46°C in 2026, which kept room-cooling demand elevated and heightened urgency around seasonal purchases. The International Energy Agency stated that each 1°C rise in India’s outdoor temperatures adds nearly 7 gigawatts to peak electricity demand, underscoring how closely heat intensity and cooling demand now move together. Longer active cooling seasons also strengthen the case for buying room air conditioners, as more months of use shorten the effective payback period for many households. This pattern supports the window air conditioner market because the category remains well-positioned for first-purchase demand, where lower upfront costs and faster setup matter. It also strengthens future replacement demand as new buyers enter later upgrade cycles and shift toward better-rated units.

Replacement Demand From Aging Room Cooling Stock

The window air conditioner market is also supported by replacement demand in mature countries with large existing room-cooling fleets. In the United States, revised Department of Energy standards for room air conditioners took effect for units manufactured or imported on or after May 26, 2026, accelerating the move away from older, non-compliant stock [2]U.S. Department of Energy, “Room Air Conditioners,” Energy.gov, energy.gov. This is shifting demand from simple replacement purchases toward models that also offer stronger energy performance and updated controls. In India, 2026 model launches were similarly tied to fresh compliance cycles and seasonal portfolio updates from major suppliers. As a result, replacement demand not only preserves sales volume in the window air conditioner market but also upgrades the average technical specification of the category. This favors brands that can adapt products to local room sizes, voltage conditions, and efficiency thresholds simultaneously.

Energy Efficiency Standards Pushing Technology Upgrades

The window air conditioner market is moving toward higher-efficiency models more quickly because regulations are changing product economics across key markets. The United States Department of Energy updated CEER requirements in 2026, and ENERGY STAR also revised the specifications for room air conditioners to align with the new federal baseline. In India, revised BEE star rating norms took effect on January 1, 2026, and major brands introduced new product lines that comply with the updated framework. GE Appliances marketed a Profile inverter smart window AC with a 15 CEER rating and a 37% efficiency advantage over the current DOE minimum for its class, demonstrating how performance benchmarks are rising. This is widening the gap between legacy fixed-speed products and new launches that combine efficiency, connectivity, and quieter operation. The window air conditioner market is therefore shifting toward lifecycle cost comparison rather than simple upfront price comparison alone.

Space-Constrained Urban Housing Favoring Window ACs

The window air conditioner market maintains a structural advantage in dense urban housing, where building layouts make split-system installation harder or more expensive. This remains relevant in India and parts of Southeast Asia, where multi-story concrete housing has expanded and where individual outdoor unit placement can be difficult for tenants. The window format also meets the needs of buyers who want minimal construction work, a faster setup, and simpler servicing after installation. Product launches in 2026 show that suppliers are still designing specifically for compact urban homes, including smaller inverter models and premium window units with added features. This supports the window air conditioner market because compact housing and budget sensitivity often coexist, keeping the category competitive even as incomes rise gradually. It also preserves future replacement demand once these households move into normal upgrade cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition From Split, Portable, And Central HVAC Systems | -0.6% | Global, most acute in East Asia, urban Europe, and affluent North American segments | Short term (≤ 2 years) |

| High Noise And Aesthetics Sensitivity In Urban Households | -0.2% | Urban markets in North America, Western Europe, and East Asia | Medium term (2-4 years) |

| Grid Instability And Voltage Fluctuation In Emerging Markets | -0.3% | Sub-Saharan Africa, South Asia, and parts of MENA | Long term (≥ 4 years) |

| Retrofit Constraints In Older Window Frames And Building Codes | -0.2% | North America, Western Europe, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition From Split, Portable, And Central HVAC Systems

The main restraint on the window air conditioner market remains pressure from other cooling formats that appeal to different buyer priorities. Split systems continue to attract higher-income urban households that value lower noise and a cleaner indoor appearance more than ease of installation. Portable units also create pressure at the low-commitment end of the category, and the U.S. Federal Register published a 2025 proposal to withdraw portable ACs from the covered product category under EPCA, if finalized [3]Federal Register, “Energy Conservation Program For Consumer Products, Portable Air Conditioners,” Federal Register, federalregister.gov. This leaves the window air conditioner market competing with better aesthetics at the premium end and greater mobility at the value end. Manufacturers are responding with inverter controls, smart connectivity, improved energy performance, and quieter operation to protect category relevance. Even so, the category continues to face substitution risk in urban markets, where rising incomes make alternative formats easier to adopt.

Grid Instability And Voltage Fluctuation In Emerging Markets

Grid instability remains a significant restraint on the window air conditioner market in several highly promising developing regions. In parts of Sub-Saharan Africa and South Asia, households often make cooling decisions based on outage patterns, backup power availability, and voltage tolerance rather than only on energy efficiency. This weakens the operating advantage of inverter units, because those models perform best under more stable power conditions. Manufacturers are therefore adding auto-restart, surge protection, and wider voltage operating ranges to products intended for these markets. While these features improve usability, they also add cost pressure in demand tiers that remain highly price sensitive. The result is slower conversion of latent demand into actual unit sales in some regions that otherwise offer the longest runway for window air conditioner market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Connectivity Edges Into a Standard-Unit Market

Standard window units accounted for 62.3% of product type revenue in 2025, giving them the largest share in the window air conditioner market, as the installed base in India, China, and North America still leans heavily toward conventional room AC replacements. This leading share reflects scale and familiarity more than technical stagnation, because many basic units are still being refreshed with better energy performance and updated control systems. Regulatory changes in the United States and India are gradually raising the technical floor for even mainstream models, meaning the standard category is improving without losing its price-led role. In practical terms, buyers who once chose a basic replacement are now more likely to receive a unit with stronger compliance credentials, better airflow management, or simplified digital control. This helps preserve the relevance of standard units inside the window air conditioner industry even as premium subsegments expand.

Smart window units are projected to grow at a 4.89% CAGR through 2031, making them the fastest-expanding product subsegment in the window air conditioner market as connectivity shifts from a premium feature to a mid-tier expectation. TCL highlighted this shift in 2026 with a Matter-certified smart inverter window AC that works with Alexa, Google Assistant, and Apple HomeKit, showing how interoperability is becoming part of mainstream product positioning [4]TCL, “Smart Inverter Window Air Conditioner Product Information,” TCL, tcl.com. GE Appliances followed the same direction with an inverter smart model that combined high efficiency with connected controls, which shows that smart and inverter features are increasingly being launched together rather than sold as separate upgrades. Sharp also widened the premium window proposition in India by launching the Ryohu series with active air purification, which adds health-related value beyond cooling output alone. Through-the-wall models and portable window-mounted variants still serve narrower use cases. Still, their roles remain smaller than the large standard installed base and the rising smart segment in the window air conditioner market.

By Capacity: Mid-Range BTU Anchors Volume, High-Capacity Tiers Gain Commercial Traction

The 5,000 to 8,000 BTU band accounted for 58.1% of capacity segment revenue in 2025, making it the largest-volume anchor in the window air conditioner market, as it matches common room sizes across apartments and smaller urban homes. This range fits a broad set of residential use cases, especially where buyers want the lowest workable capacity that can still cool bedrooms, compact living rooms, and small office spaces. Its strength also reflects the window air conditioner market’s heavy exposure to first-purchase demand, where affordability tends to outweigh oversizing for faster cooldown. Mid-range units, therefore, continue to hold the center of mass for the category even while higher efficiency and smart control features move down into these bands. The result is steady volume retention at the core of the window air conditioner industry while technical value rises around it.

The above 20,000 BTU band is forecast to grow at a 4.54% CAGR through 2031, making it the fastest-growing capacity tier in the window air conditioner market as more commercial sites adopt high-output room cooling for targeted zones. Retail outlets, hotel corridors, waiting areas, and other light commercial spaces often prefer a single larger window unit over multiple smaller installations when a central HVAC extension is expensive or disruptive. Growth in the 9,000 to 12,000 BTU band remains important as well, because it serves households that are upgrading room size expectations and shifting from smaller one-ton equivalents to higher cooling output. Lower capacity bands still have a role in very compact rooms, but they remain limited in revenue contribution and have a narrower application range. United States efficiency rules also matter here, because CEER thresholds increase by capacity class and encourage businesses to replace older large units with compliant successors rather than continue running outdated equipment.

By Technology: Efficiency Mandates Drive the Inverter Transition

Non-inverter technology accounted for 68.2% of revenue in 2025, indicating that the window air conditioner market still relied heavily on the installed base of fixed-speed products. This share reflects the legacy structure of the category more than the direction of current product development, because new compliance rules are increasing pressure on lower-efficiency designs. In price-sensitive markets, non-inverter units continue to attract buyers who prioritize lower upfront purchase costs and simpler maintenance patterns. Even so, the technical gap between compliant fixed-speed models and newer inverter options is becoming easier for consumers to see as brands emphasize lower running costs and stronger ratings. This keeps non-inverter units large in volume today, but it also leaves them exposed to faster mix change over the forecast period in the window air conditioner market.

Inverter units are projected to expand at a 5.11% CAGR through 2031, making them the fastest-growing technology type in the window air conditioner market as regulations and consumer operating costs begin to align. TCL stated that its 8,000 BTU smart inverter window AC can deliver up to 49% in energy cost savings over comparable fixed-speed models, sending a clear commercial message to households facing higher electricity bills. The inverter transition is also moving in step with broader efficiency programs, including India’s revised BEE framework and the aligned United States standards environment, which increasingly favor better-performing designs. In practice, this is shifting the window air conditioner industry from a legacy comparison based mostly on purchase price toward a fuller comparison based on power use, comfort control, and connected operation. Over time, the gap between inverter adoption in split systems and inverter adoption in the window air conditioner market should narrow, especially as brands continue to introduce more compliant models across entry- and mid-priced bands.

By End-User: Residential Drives Volume, Commercial Verticals Diversify Revenue Mix

Residential users accounted for 72.1% of end-user revenue in 2025, keeping homes as the clear volume base of the window air conditioner market, as compact apartments, rental units, and first-time purchases still dominate category demand. This concentration is supported by the format’s low installation complexity, which suits tenants and homeowners who want cooling without large structural changes. Residential demand is also the part of the window air conditioner market most exposed to heat stress, rising urban density, and affordability-led product choice. As a result, household purchases continue to drive the category’s base volume, even as premium alternatives gain attention in higher-income neighborhoods. The same pattern supports recurring replacement demand because large installed household fleets eventually feed future upgrade cycles for better-rated or smarter units.

Commercial users are forecast to grow at a 4.48% CAGR through 2031, making them the fastest-growing end-user segment in the window air conditioner market, as selected business settings seek zone-level cooling with limited retrofit work. Hospitality, healthcare, and retail applications remain central because these sites often value quick installation and individual room control over wider system integration. Hotels can use window or through-the-wall units in room retrofits when a central HVAC overhaul would cost more and cause more disruption than a direct room-level replacement. Healthcare growth is also notable in smaller clinics and local hospital wings, where separated cooling can support operational flexibility and reduce the complexity of broader building work. Offices and education sites add steady demand as institutions expand cooling coverage and increasingly prefer units with scheduling and connectivity features that support basic energy management.

By Distribution Channel: Retail Channels Retain Majority, B2B Channels Build Structural Momentum

B2C and retail consumers accounted for 64.5% of distribution channel revenue in 2025, making them the largest route to market in the window air conditioner market, as most purchases still come from households and small commercial buyers. This share reflects the continued importance of traditional dealer networks, brand stores, and multi-brand online platforms that make model comparison easy before the cooling season begins. Retail channels also remain important because installation booking, delivery scheduling, and seasonal promotions still influence final purchase timing in room AC categories. In India, online listings for current model lines have made the category easier to reach across smaller cities where specialized AC stores are less dense. This keeps retail dominant, even as procurement patterns are starting to broaden in the broader window air conditioner market.

B2B and direct-from-manufacturer channels are projected to grow at a 4.15% CAGR through 2031, making them the fastest-growing distribution paths in the window air conditioner market as institutional and project-based buying becomes more visible. Residential developers, social housing authorities, and public procurement programs are beginning to place larger orders for energy-compliant units rather than leaving the entire decision to individual households. New York City and NYCHA announced a USD 38.4 million commitment in 2026 to install window heat pump units, and the program had already moved into a multi-thousand-unit procurement stage with designated suppliers. That project matters because it provides the window air conditioner market with a visible institutional template that could be replicated in other housing systems where electrification and efficient room-level heating and cooling are both policy goals. The B2B shift may reduce unit margins compared with retail sales, but it favors manufacturers that can manage scale, compliance, and dependable supply for large tenders.

Geography Analysis

North America remains a core part of the window air conditioner market because the region has a large installed base of residential room ACs and a demand profile heavily weighted toward replacement activity. The 2026 DOE efficiency update is now shaping channel behavior, as retailers are moving away from older stock and toward inverter-smart models that meet the revised performance baseline. This makes North America a less volatile but still important revenue pool for suppliers that can serve premium replacement demand more efficiently, with digital controls and lower-noise positioning. South America follows a more affordability-led path, where urbanization and rising middle-class household cooling needs keep the window air conditioner market relevant in settings that still prioritize simpler installation and accessible pricing.

Europe shows a lower growth profile in the window air conditioner market because split systems and heat pumps are more structurally favored in many higher-income countries. At the same time, window-mounted units also face visual and building code constraints. Southern European heatwaves still create seasonal demand, but the region does not show the same broad first-purchase depth as Asia-Pacific. The updated EU F-Gas framework from 2026 adds another layer of change, as higher-GWP legacy products face a tighter compliance environment and low-GWP alternatives become more relevant in remaining use cases. In the Middle East and Africa, the window air conditioner market shows a sharper contrast between higher growth in Gulf construction activity and lower base demand in parts of Sub-Saharan Africa, where affordability and infrastructure still limit conversion.

Asia-Pacific led the window air conditioner market with a 41.3% market share in 2025 and is expected to grow at a 5.23% CAGR through 2031, making it both the largest and the fastest-growing regional market. India remains the single most important growth engine in this region because low AC penetration, compact housing, and price sensitivity together support sustained first purchase demand for window formats. China contributes through a mixed pattern, with some coastal cities already in a more mature replacement phase. At the same time, inland areas still offer room for new household adoption at mass-market price points. Japan and South Korea offer more limited upside in volume because split systems play a stronger role there, but older multi-family housing still offers selected opportunities for window installations. Southeast Asia continues to strengthen its position in the window air conditioner market, as dense urban development, rising disposable incomes, and still-low penetration rates create a steady base for unit sales. Product launches in 2026 also show that companies are designing more directly for Indian and Asian urban needs, including premium window units with enhanced air filtration and models for compact rooms, rather than simply adapting Western products later.

Competitive Landscape

The window air conditioner market remains moderately fragmented, with large Chinese OEMs such as Midea, Haier, Gree, Hisense, and TCL accounting for the bulk of volume. At the same time, regional brands and technology-focused suppliers continue to hold meaningful positions in selected geographies. This structure reflects scale in compressors, manufacturing, and sourcing. However, it does not produce a winner-take-all outcome because brand relevance still depends on local compliance, seasonal distribution, and model mix. The market therefore supports both global volume players and locally strong brands that tailor products to grid conditions, room sizes, and local efficiency rules. Competition in the window air conditioner market is increasingly shaped by who can combine affordability with better ratings, quieter operation, and digital usability, rather than by who can offer the lowest sticker price.

One important strategic move came from public procurement, as New York City and NYCHA committed USD 38.4 million in 2026 for a window heat pump rollout and named Midea and Gradient Comfort as suppliers under the Clean Heat for All program. That decision matters because it shifts part of the window air conditioner market narrative from single-appliance retail sales toward building-scale procurement, where performance, electrification, and ease of installation are evaluated together. Gradient strengthened that position further by launching Gradient Nexus in February 2026, a fleet management and intelligent energy control platform for multifamily window heat pump deployments, and the company said beta testing achieved a 25% reduction in energy consumption. LG also expanded its HVAC commitment in 2026 through higher capex, a new product development center, and a third India AC factory, which shows that large appliance companies still see room to grow through localized scale and product development. Blue Star took a similar market-defense approach by launching 125 new room air conditioner models for Summer 2026, including window ACs aligned with the updated BEE framework.

These moves show that competition in the window air conditioner market is not limited to hardware capacity alone, because software, compliance timing, and institutional channel access are becoming more important. Smart features and energy management now help brands answer the main objections that push some households toward split systems, especially concerning energy use, convenience, and year-round functionality. Air treatment and premium room comfort are also becoming meaningful differentiators, as seen in Sharp’s 2026 Ryohu series launch in India. The best-positioned companies in the window air conditioner market are therefore those that can serve both mass retail demand and rising project-based demand without losing price discipline. At the same time, the category still faces substitution risk in wealthier urban segments, so sustained competitiveness will depend on whether suppliers continue to improve noise levels, digital controls, and efficiency while protecting the core value proposition that made the format durable in the first place.

Window Air Conditioner (AC) Industry Leaders

Midea Group Co., Ltd.

LG Electronics Inc.

Haier Smart Home Co., Ltd.

Whirlpool Corporation

Carrier Global Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Blue Star Limited launched 125 new Room Air Conditioner models for Summer 2026, including inverter, fixed-speed, and window ACs, all compliant with new BEE standards effective January 1, 2026. The portfolio introduced the premium "Iconia" series in Midnight Silver finish, targeting the aspirational residential segment.

- March 2026: LG Electronics disclosed 2026 capex of over USD 2.8 billion, KRW 4.045 trillion, including a 141% year-on-year increase in HVAC investment to KRW 394.6 billion. A new product development center and LG's third India AC factory are scheduled to open at Sri City and near Noida in the second half of 2026, supporting both domestic and export demand.

- February 2026: New York City Mayor's Office and NYCHA announced a USD 38.4 million investment to install window heat pumps at Beach 41st Street Houses, serving 712 homes. The Clean Heat for All initiative aims to install 30,000 window heat pump units across NYCHA properties. Pilot data from Woodside Houses showed 86% less energy use for space heating and a 50% reduction in heating costs. NYCHA has purchased 5,000 units to date.

- February 2026: Gradient Comfort launched Gradient Nexus, a fleet management and intelligent energy control software platform for multifamily window heat pump deployments. Beta testing achieved a 25% reduction in energy consumption. The platform is deployed across 200-plus residential units in Boston, Detroit, and Washington, D.C.

Global Window Air Conditioner (AC) Market Report Scope

This report covers the global window air conditioner market and examines demand across replacement purchases and first-time adoption. It studies the category as self-contained room cooling systems installed in window openings, including standard, smart, inverter, and related window-mounted formats. The analysis reviews market size, growth outlook, key demand drivers, competitive positioning, channel trends, technology shifts, and regional performance for the forecast period.

The Global Window Air Conditioner (AC) Market is Segmented by Product Type (Standard, Smart, Inverter, Portable, and Through-the-Wall), Capacity (Below 5,000 BTU, 5,000 to 8,000 BTU, and Others ), Technology (Inverter, and Non-Inverter), End-User (Residential, and Commercial), Distribution Channel (B2B/Direct, and B2C/Retail), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are in Value (USD).

| Standard Window Units |

| Smart Window Units |

| Inverter Window Units |

| Portable Window-Mounted Systems |

| Through-the-Wall Models |

| Below 5,000 BTU |

| 5,000 to 8,000 BTU |

| 9,000 to 12,000 BTU |

| 13,000 to 16,000 BTU |

| 17,000 to 20,000 BTU |

| Above 20,000 BTU |

| Inverter |

| Non-Inverter |

| Residential | |

| Commercial | Hospitality |

| Healthcare | |

| Retail | |

| Corporate Offices | |

| Educational Institutes | |

| Other Commercial Applications |

| B2B/Direct from the Manufacturers | |

| B2C/Retail Consumers | Multi-Brand Stores |

| Exclusive Brand Stores (EBOs) | |

| Online | |

| Other Distribution Channels |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of the Middle East and Africa |

| By Product Type | Standard Window Units | |

| Smart Window Units | ||

| Inverter Window Units | ||

| Portable Window-Mounted Systems | ||

| Through-the-Wall Models | ||

| By Capacity | Below 5,000 BTU | |

| 5,000 to 8,000 BTU | ||

| 9,000 to 12,000 BTU | ||

| 13,000 to 16,000 BTU | ||

| 17,000 to 20,000 BTU | ||

| Above 20,000 BTU | ||

| By Technology | Inverter | |

| Non-Inverter | ||

| By End-User | Residential | |

| Commercial | Hospitality | |

| Healthcare | ||

| Retail | ||

| Corporate Offices | ||

| Educational Institutes | ||

| Other Commercial Applications | ||

| By Distribution Channel | B2B/Direct from the Manufacturers | |

| B2C/Retail Consumers | Multi-Brand Stores | |

| Exclusive Brand Stores (EBOs) | ||

| Online | ||

| Other Distribution Channels | ||

| By Region | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the window air conditioner market?

The window air conditioner market size stood at USD 20.22 billion in 2025, reached USD 20.93 billion in 2026, and is expected to reach USD 25.24 billion by 2031 at a 3.81% CAGR.

Which region leads global demand for window air conditioners?

Asia-Pacific leads the window air conditioner market with 41.3% revenue share in 2025 and is also the fastest-growing region, with a projected 5.23% CAGR through 2031.

Why are window air conditioners still relevant when split systems are growing?

The category remains relevant because it fits compact housing, rental units, and budget-led purchases where buyers value lower upfront cost, faster installation, and simpler servicing.

Which product segment is growing the fastest?

Smart window units are the fastest-growing product type, with a projected 4.89% CAGR through 2031, as brands combine connectivity with inverter-based efficiency upgrades.

Which technology trend is changing product competition the most?

The strongest shift is toward inverter technology, which is projected to grow at a 5.11% CAGR through 2031 as BEE, DOE, and ENERGY STAR-related efficiency changes raise the performance bar.

How are institutional buyers affecting future demand?

Institutional procurement is becoming more important through direct tenders and social housing programs, with NYCHA’s 2026 window heat pump initiative showing how large orders can create a new growth channel beyond retail.

Page last updated on: