Portable Air Purifier Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.69 Billion |

| Market Size (2031) | USD 20.51 Billion |

| Growth Rate (2026 - 2031) | 8.42% CAGR |

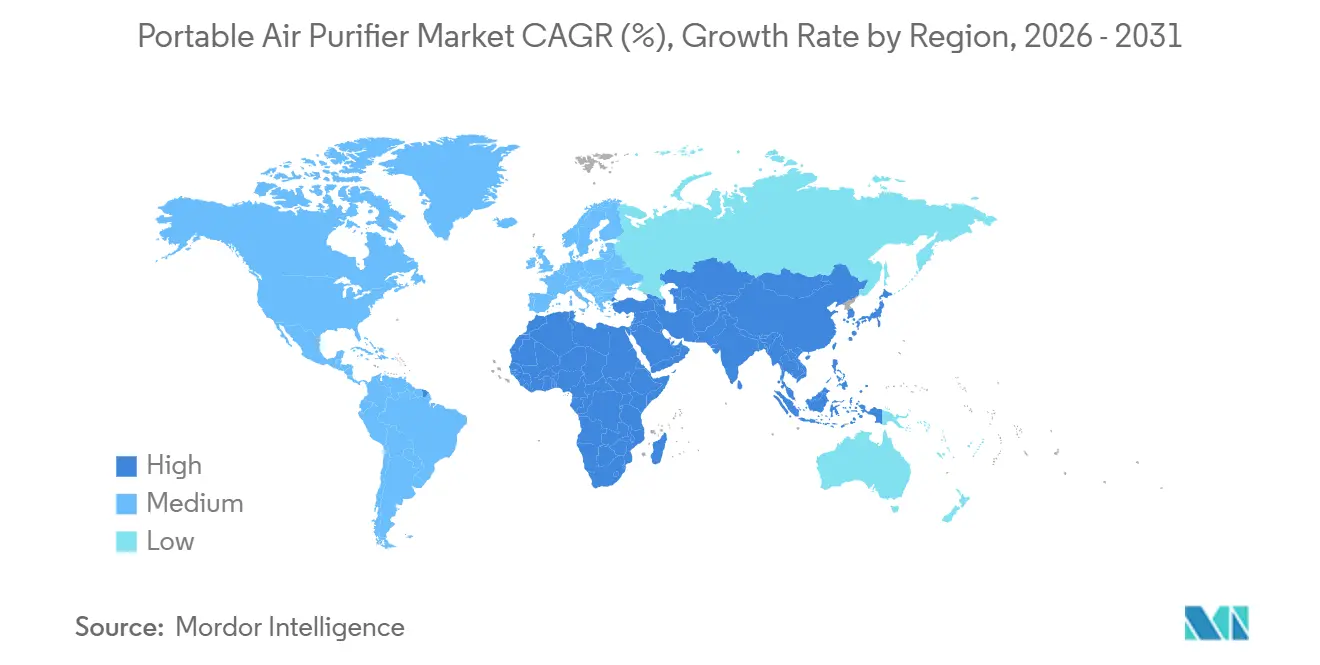

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

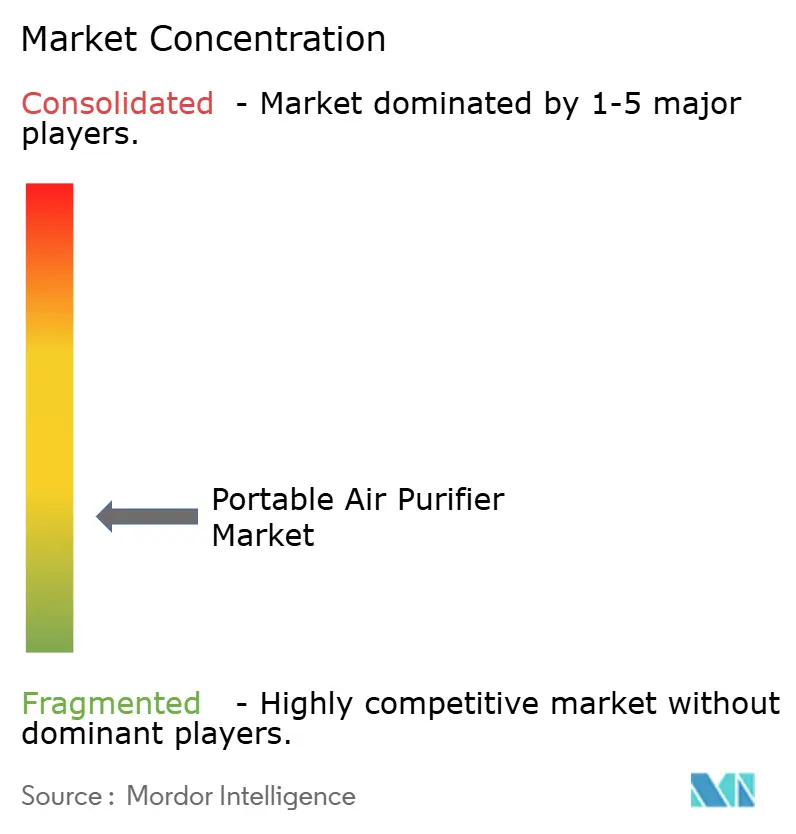

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portable Air Purifier Market Analysis by Mordor Intelligence

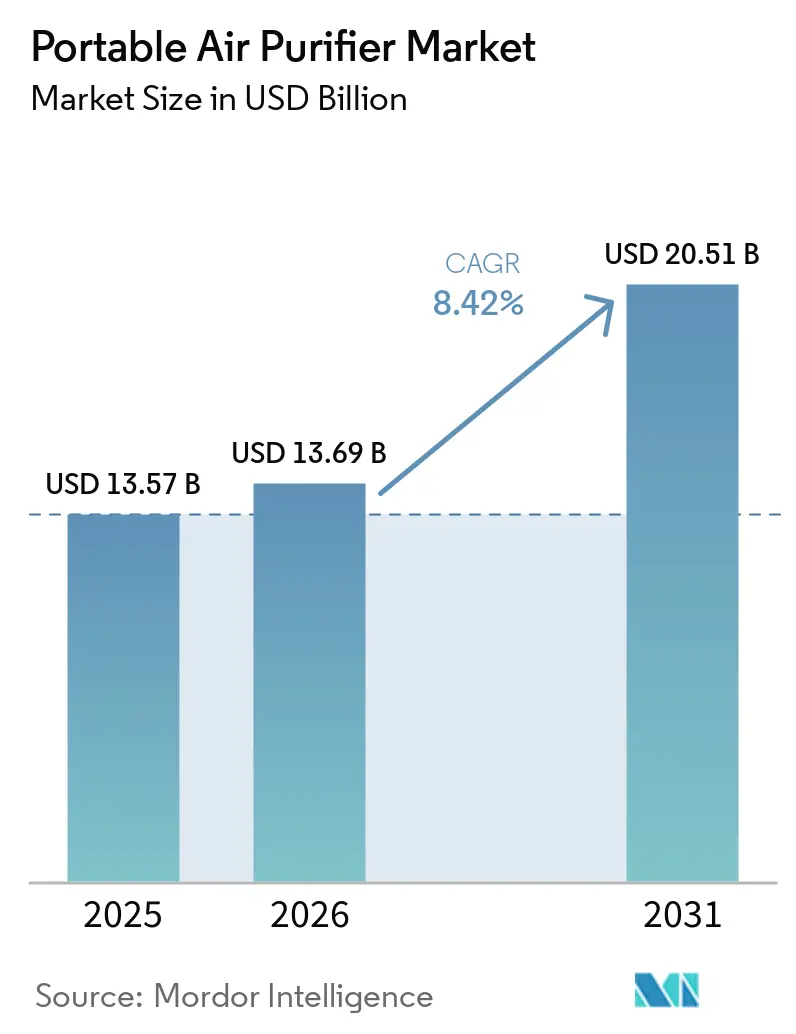

The portable air purifier market size is projected to expand from USD 13.57 billion in 2025 and USD 13.69 billion in 2026 to USD 20.51 billion by 2031, registering a CAGR of 8.42% between 2026 and 2031. Indoor air quality has moved from seasonal concern to year-round wellness behavior as consumers respond to recurrent wildfire smoke and persistent PM2.5 exposure in large Asian cities. Regulatory anchors such as CARB’s ozone-safety limit, together with AHAM’s replacement-filter verification, are shaping device choices toward HEPA-plus-carbon systems and improving trust at the point of sale. Portable units continue to benefit from guidance that prioritizes clean-air rooms for smoke events in schools and workplaces, which expands B2B adoption beyond household use. Connectivity and app-based visualization support predictive filter maintenance and tighten brand relationships, while verification programs reduce uncertainty over third-party filters and sustain repeat purchases at higher average selling prices[1]AHAM, “Breathe Easier: AHAM Launches Program to Confirm Air Filter Performance,” PR Newswire, prnewswire.com. Demand remains diversified across budget, mid-range, and premium tiers, and the portable air purifier market reflects fragmented competition with recognized brands and agile D2C entrants using online channels to reach targeted niches.

Key Report Takeaways

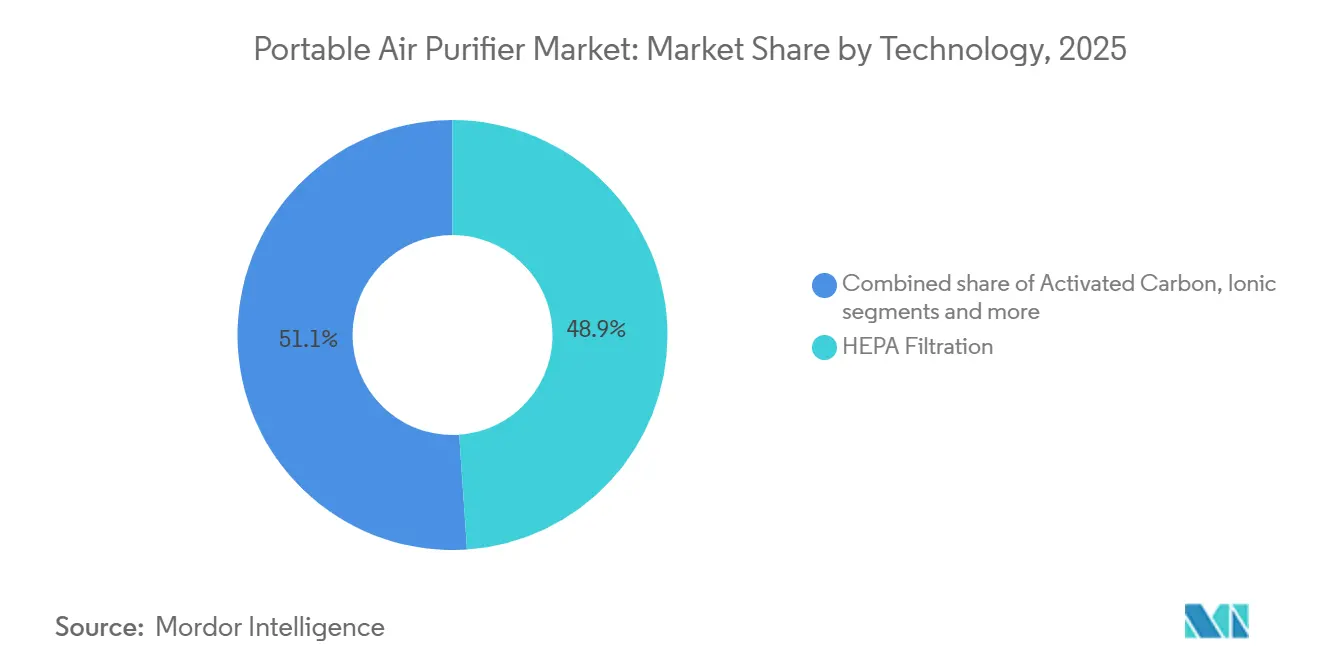

- By technology, HEPA filtration led the portable air purifier market with 48.92% market share in 2025, while activated carbon is projected to grow at an 8.64% CAGR through 2031.

- By connectivity, non-smart (manual/analog) held 78.52% of the portable air purifier market share in 2025, whereas smart or IoT-enabled purifiers are forecast to grow at a 10.09% CAGR through 2031.

- By functionality, single-function purifiers accounted for 70.81% of the market share in 2025, while multi-function devices are projected to expand at an 11.07% CAGR through 2031.

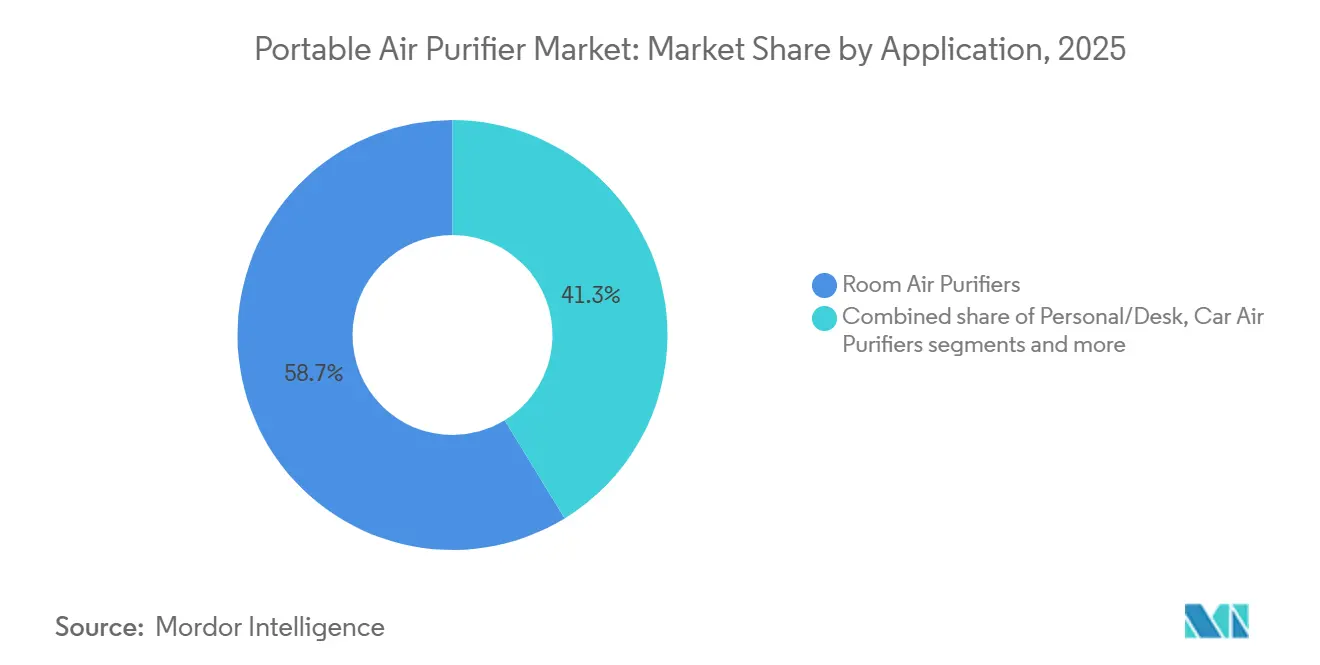

- By application, room air purifiers captured 58.74% of the portable air purifier market share in 2025, whereas travel or wearable devices are set to grow at a 10.81% CAGR through 2031.

- By distribution channel, B2C/retail commanded 64.61% of the market share in 2025, while B2B or direct-from-manufacturer sales are projected to increase at an 8.52% CAGR through 2031.

- By geography, North America accounted for 44.12% of the portable air purifier market share in 2025, while Asia-Pacific is projected to record the fastest CAGR of 8.79% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Portable Air Purifier Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HEPA adoption and performance verification (HEPA/CADR) drive mainstream trust and repeat purchases | +1.8% | Global, with North America and Europe leading third-party certification uptake | Medium term (2-4 years) |

| Wildfire-smoke preparedness accelerates portable HEPA uptake in homes, schools, and small businesses | +2.1% | North America core, spillover to Australia and Southern Europe | Short term (≤ 2 years) |

| Asia-Pacific urban PM2.5 exposure sustains baseline demand for room purifiers | +2.5% | APAC core, particularly India, Pakistan, China, and Southeast Asian megacities | Long term (≥ 4 years) |

| E-commerce and D2C expand access to mid-range and premium portables | +1.3% | Global, with accelerated penetration in India, Southeast Asia, and South America | Medium term (2-4 years) |

| Institutional clean-room kits become a recurring budget line in education and municipal response | +0.9% | North America and the EU, with early gains in key urban districts | Long term (≥ 4 years) |

| Ozone-safety labeling and third-party verification shift tech mix to HEPA+carbon, raising ASPs and filter annuities | +1.1% | National, with regulatory influence from CARB, EPA, and standardization frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

HEPA Adoption and Performance Verification Drive Mainstream Trust and Repeat Purchases

Recognition of standardized performance has moved from a niche differentiator to a core purchase requirement as buyers look for validated CADR and filter equivalency. AHAM’s replacement-filter verification program, launched in November 2025, addresses quality gaps in third-party filters and reduces the risk that off-brand replacements undermine device performance over time. Parallel ozone-safety labeling under California’s 0.050 ppm emission cap reinforces the shift toward mechanical or hybrid systems that prioritize low emissions and consistent results in homes, schools, and offices. This framework makes the portable air purifier market more predictable for households and institutions that plan for annual filter budgets and multi-year device use. As verification reduces uncertainty and aligns expectations, brands benefit from higher repeat-purchase rates for original filters and more stable retention in connected ecosystems. These developments support a premiumizing narrative in which trust, compliance, and transparent maintenance drive sustainable growth in the portable air purifier market.

Wildfire-Smoke Preparedness Accelerates Portable HEPA Uptake in Homes, Schools, and Small Businesses

Guidance in North America now emphasizes portable HEPA units alongside HVAC measures as part of smoke-readiness playbooks for buildings during wildfire events. Empirical research from Los Angeles homes during a fire event found that HEPA purifiers reduced indoor PM2.5 compared with non-HEPA controls, highlighting their role as practical mitigation tools in real-world conditions[2]Chen et al., “Fine Particulate Matter Levels and HEPA Filtration in Los Angeles Homes During a Wildland-Urban-Interface Fire,” Nature npj Clean Air, nature.com. School districts and municipal facilities are planning clean-room strategies that pair devices with standard operating procedures, which support steady institutional procurement rather than reactive emergency buys. These programs create repeatable deployment models, from classrooms to community shelters, where portable units are part of structured response plans. As wildfire seasons remain a recurring risk, the portable air purifier market is reinforced by budgets that treat clean air as essential infrastructure instead of a discretionary accessory.

Asia-Pacific Urban PM2.5 Exposure Sustains Baseline Demand for Room Purifiers

Chronic PM2.5 exposure across Asia-Pacific underpins steady year-round demand for room purifiers in the portable air purifier market. The 2025 World Air Quality Report, released in March 2026, highlighted that only a small portion of cities met the WHO guideline, with many Asian urban centers continuing to report annual averages far above the 5 µg/m³ limit, reinforcing the need for continuous purification at home and at work. As households and small businesses normalize purifier use throughout the year rather than during seasonal peaks, replacement filters, activated carbon upgrades, and maintenance services gain importance in overall category economics. Hospitality, education, and healthcare settings in heavily polluted corridors increasingly market high-efficiency filtration as a service feature, which raises baseline expectations for clean indoor air. The portable air purifier market, therefore, grows not only on first-time hardware adoption but also on the cadence of filter replenishment and fleet refresh cycles. These dynamics support stable multi-year demand trajectories independent of short-term weather patterns.

E-commerce and D2C Expand Access to Mid-Range and Premium Portables

E-commerce and direct-to-consumer routes continue to unlock mid-range and premium opportunities in the portable air purifier market by removing retail intermediation costs and enabling rapid delivery during localized air-quality shocks. Brands deepen engagement through apps that track filter life and display indoor air quality in real time, which supports recurring replenishment and boosts loyalty within connected ecosystems. The ability to control devices through established home platforms and voice assistants reduces perceived setup friction and supports cross-sell opportunities with adjacent smart-home categories[3]AWS and Blueair, “Building a Scalable IoT System for Connected Air Purifiers on AWS IoT,” AWS IoT Blog, aws.amazon.com. Faster fulfillment narrows the gap between purchase intent and protection during smoke events and pollen seasons, which improves the likelihood that first-time buyers become repeat customers. The portable air purifier market also sees a rise in institutional buyers using online procurement workflows, which streamlines bulk ordering and fleet management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership limits penetration in price-sensitive markets | -1.4% | Global, particularly in India, Southeast Asia, South America, and Sub-Saharan Africa | Long term (≥ 4 years) |

| Ozone or ionizer safety limits and scrutiny reduce demand for certain electronic technologies | -0.7% | National, with regulatory influence from CARB and public-health guidance | Medium term (2-4 years) |

| Enforcement against non-certified online SKUs raises seller compliance costs and narrows assortment | -0.5% | Global, with concentrated impact in the U.S. and EU e-commerce ecosystems | Medium term (2-4 years) |

| Noise, CADR, and power trade-offs cap usable runtime in bedrooms and offices | -0.6% | Global, particularly in North America, Europe, and urban APAC markets, prioritize sleep quality. | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership Limits Penetration in Price-Sensitive Markets

Ownership costs include the device, filter replacements, and electricity, and these expenses rise when a household needs multiple rooms covered. Where disposable incomes are constrained, users often prioritize a single room and limit runtime, which reduces the realized clean air delivery compared with rated performance. Institutions face similar considerations and weigh fleet filters, logistics, and replacement cycles when designing clean-room kits for recurring seasonal deployment[4]U.S. EPA, “Wildfires and Indoor Air Quality in Schools and Commercial Buildings,” U.S. Environmental Protection Agency, epa.gov. Manufacturers are addressing cost stress through washable pre-filters, subscription discounts for replacement media, and energy-efficient motors that cut ongoing draw without sacrificing CADR in day-to-day use. These actions help, yet total ownership outlays remain a key hurdle for broader penetration in emerging markets and for households balancing multi-room coverage with restrained budgets. As cost transparency and verified filter performance become standard, customers can better plan lifetime spend in the portable air purifier market.

Noise, CADR, and Power Trade-offs Cap Usable Runtime in Bedrooms and Offices

High CADR often requires higher fan speeds that add noise, which can limit overnight operation in bedrooms and focused use in quiet office spaces. Users frequently run purifiers at low settings for comfort, which lowers effective air changes per hour and leaves exposure benefits below the levels implied by lab-rated maximums. During wildfire smoke episodes, portable HEPA units support cleaner-room strategies that target specific rooms, but recommended air changes may not be achieved when noise limits keep speeds low. Energy draw adds to the trade-off, since sustained operation at higher speeds increases monthly consumption unless devices use efficient drive systems and airflow designs. Product engineering continues to focus on quiet motors, optimized ducting, and hybrid filtration that preserves performance while reducing acoustic footprints. These improvements increase the practicality of around-the-clock use, which is central to consistent exposure reduction in the portable air purifier market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Activated Carbon Gains Momentum for Dual-Pollutant Control

HEPA filtration led with 48.92% of the 2025 portable air purifier market share, and activated carbon media is projected to post an 8.64% CAGR through 2031 as buyers seek parallel control of particulates and gases. Standards and labeling help HEPA remain the default for fine particle removal, while CARB’s ozone-safety rules favor mechanical or hybrid filtration in residential and commercial environments. As urban dwellings face particulate exposure from traffic and wildfire smoke, and indoor sources emit VOCs from cleaning and materials, combined media stacks create a balanced proposition for year-round use. Buyers in the portable air purifier market weigh performance, filter longevity, and noise control as core decision points, which supports upgrades to HEPA-plus-carbon configurations when recurring filter costs are manageable. On the product side, manufacturers assemble modular stacks that allow users to choose smoke, odor, or allergen-optimized variants aligned with local conditions and seasonal shifts. These choices match well with verified replacement-filter programs that preserve system performance over time and reduce variance in real-world outcomes.

Activated carbon’s trajectory is amplified by wildfire smoke seasons that elevate odor and VOC concerns, which mechanical filtration alone does not address in living rooms and classrooms. Hybrid designs and advanced carbons extend VOC capture windows and mitigate formaldehyde or ammonia in select applications, which justifies a premium where indoor chemistry is a worry. As institutions build clean-room kits, filter standardization and safety labeling reduce risk, simplify procurement, and support predictable budgets for multi-month deployments. Over the forecast period, balanced stacks that integrate particulate and gas capture are expected to represent a larger share of the portable air purifier market, especially where guidance discourages ozone-producing options. As verification and safety frameworks mature, the portable air purifier industry aligns product design with long-run ownership value by clarifying performance, filter intervals, and compliance in everyday use.

By Connectivity: Smart or IoT Adoption Driven by Data Visualization and Predictive Maintenance

Non-smart manual or analog devices retained 78.52% share in 2025, although smart or IoT-enabled purifiers are forecast to expand at a 10.09% CAGR with app dashboards, voice assistants, and predictive filter prompts. Users respond to clear air quality visualization that links PM levels with fan speed, which reduces uncertainty and improves compliance during smoke intrusions and peak traffic periods. Platform integration is improving with support for interoperable standards, which alleviates lock-in fears, enables single-app control, and expands multi-device routines across brands. Commercial fleets use occupancy and scheduling features to reduce power when rooms are empty, which cuts energy use and extends filter life in high-traffic sites. The portable air purifier market benefits as connectivity shifts maintenance from calendar-based to condition-based cycles, which supports better timing for replacements and fewer unexpected performance dips. As price points fall and cloud costs spread across product portfolios, more mid-range devices are expected to include core smart features that strengthen brand retention.

Advanced connectivity also supports institutional procurement by enabling device grouping, location tagging, and remote status checks across classrooms or clinics. These tools help administrators assign filter inventories, schedule room cycles, and verify compliance with clean-room standard operating procedures during smoke or high-pollen days. Edge analytics can support privacy-sensitive sites by limiting cloud data while keeping key status functions, which suits schools and medical offices that restrict external traffic. Over time, the portable air purifier market will see growing overlap between hardware and software value as fleets shift to managed models with predictable filter and service events. This dynamic compresses perceived differences among devices without connectivity and increases the appeal of ecosystems with transparent performance histories and consistent app support.

By Functionality: Multi-Function Units Consolidate Appliance Footprints in Urban Dwellings

Single-function purifiers represented 70.81% of volumes in 2025, yet multi-function devices are projected to grow at 11.07% as urban households favor space-saving designs that operate year-round. Multi-function entrants bring humidification to dry seasons while preserving filtration for smoke and pollen periods, which smooths revenue beyond episodic purchase cycles. Premium lines that integrate purification and humidification showcase efficient evaporative systems combined with low-emission particle capture tailored for bedrooms and living rooms. Complementary models from global brands highlight cooling or heating features alongside filtration and present a consolidated option for minimalist homes that track utility usage and filter cadence in one device. The portable air purifier market responds well to designs that balance performance with maintenance simplicity, clear filter messaging, and quiet nighttime operation in compact footprints. Where humidification is a seasonal need, a combined device lowers the count of plugs and filters that a household must manage across the year.

These products address a visible gap in small apartments and shared spaces by reducing devices and surfaces covered by single-purpose appliances. Buyers also find value in unified dashboards that integrate humidity, PM levels, and scheduling, which makes daily management simpler. The most compelling options translate seasonal transitions into easy presets that shift airflow and moisture balances with minimal oversight. Verified safety and clear filter labeling support household confidence in continuous use and align with procurement criteria in institutional settings, where simplicity and compliance reduce training time. As a result, multi-function lines are expected to capture a larger share of the portable air purifier market, where space, maintenance, and energy trade-offs remain prominent evaluation criteria.

By Application: Travel or Wearable Segment Surges with Airline-Duty-Cycle and Personal-Zone Innovations

Room air purifiers accounted for 58.74% share in 2025, while travel or wearable devices are projected to grow at 10.81% as commuters and travelers seek personal zones of cleaner air. Wearable formats that combine audio features and personal air management reflect a convenience-first design that aims to increase adoption in transit and on the move. Necklace-style solutions deliver directed clean-air streams without obstructing the face and operate across flights and hotels with USB-C charging compatibility in lightweight form factors. These options complement, rather than replace, room purifiers and suit periods when users have limited control over building HVAC or cannot carry larger units. As design and battery life improve, personal devices are likely to attract new users who start with travel use cases before considering room devices for home. Momentum builds as devices demonstrate reliable runtimes and comfort for continuous wear in real situations that combine transit, shared offices, and temporary accommodations.

Room units remain the anchor of the portable air purifier market because they deliver the highest CADR and achieve more consistent exposure reduction during extended stays. Institutions maintain room purifiers for classrooms and faculty spaces and deploy them under clean-room procedures for smoke days, which ensures predictable coverage and verifiable compliance. Over the forecast period, hybrid usage that combines room units at home with wearables for travel will shape buying journeys and aftermarket filter subscriptions. Clear labeling, verified filter programs, and safe operation support retention across both form factors, since users want simple maintenance and transparent ownership costs. As design hardens and comfort improves, the portable air purifier market will likely see a steady expansion of personal-zone devices in commuter-heavy cities and business travel corridors.

By Distribution Channel: B2C Leads While B2B Direct Sales Gain Traction Through Institutional Procurement

B2C captured 64.61% of 2025 sales, and B2B or direct-from-manufacturer channels are projected to expand at 8.52% as schools and municipalities formalize clean-room kits and inventory strategies. Guidance that describes indoor air strategies for wildfire smoke supports a steady stream of institutional orders that include procurement templates, training materials, and room checklists. Direct sales models help vendors bundle units, filters, and support into multi-site deployments that align with annual budget cycles and seasonal risk periods. For B2C, marketplace transparency on filter costs and safety labeling influences conversion, as buyers weigh ownership across several years in households with different room sizes. The portable air purifier market also benefits from retail experiences that let users evaluate noise and profile in person before purchase. This improves satisfaction, supports realistic placement expectations, and reduces returns as households familiarize themselves with room coverage and maintenance needs.

Direct-from-manufacturer and fleet-focused channels mature as institutions measure outcomes and budget for filter inventories that carry over from year to year. Device management features and fleet dashboards address practical procurement requests such as room-level tagging, maintenance schedules, and documented SOP compliance. These features fit well with routine audits and support line-of-sight accountability for health and facilities teams during smoke or high-pollen intervals. As channels converge, vendors balance reach and margin by combining retail presence with web stores and B2B portals that present compliant SKUs with proper safety labeling. Over time, these structures expand the portable air purifier market by supporting institutional repeat orders that smooth seasonality seen in retail channels.

Geography Analysis

North America accounted for 44.12% of 2025 revenues, supported by wildfire preparedness programs, mature HVAC practices, and safety frameworks that shape consumer trust. Institutions use portable HEPA units to create cleaner rooms during smoke intrusions, which institutionalizes demand beyond households and supports multi-year fleet planning. CARB’s ozone-safety labeling sets clear compliance criteria for devices sold in California, which influences assortment decisions across national channels. These factors anchor a steady baseline for the portable air purifier market while reducing variability driven by one-time events. As seasonality becomes more predictable in procurement, ownership cost transparency and verified filters support longer retention and more consistent aftermarket volumes.

Asia-Pacific is projected to record the fastest expansion at an 8.79% CAGR, with persistent PM2.5 challenges across major urban corridors that sustain baseline room purifier demand. IQAir’s 2025 report documented widespread non-compliance with the WHO guideline, which reinforces the relevance of particulate removal and room coverage in daily life across key cities. As household use widens, the portable air purifier market adds personal and travel devices that bridge commuting and business travel needs where HVAC control is limited. Institutions such as universities and clinics allocate budgets to fleets that can be deployed during regional haze and high-traffic episodes, with SOPs guiding placement, runtime, and filter schedules. Over time, regional product mixes reflect a balance of HEPA-plus-carbon stacks, verified replacement media, and quiet designs that support overnight use in compact apartments.

Europe shows mixed patterns as mature Northern and Western markets tilt toward replacement cycles and premium innovations, while Southern and Eastern regions expand from lower baselines that react to dust events and biomass heating. Harmonized filtration classifications and safety awareness help align procurement across borders even when country-level standards differ, which reduces complexity for multinational brands serving several EU markets. Middle East buyers prioritize dust management and robust pre-filtration, and feature sets that support quick cleaning cycles align with higher background particulate loads in several cities. South America’s adoption remains focused in urban centers where geography and weather patterns can trap emissions, which creates episodic spikes that trigger portable clean-room tactics in public buildings. As institutional playbooks spread, the portable air purifier market adapts product bundles and training materials to region-specific implementation needs and facility configurations.

Competitive Landscape

The portable air purifier market includes global brands and many regional or D2C participants, which creates fragmented competition and multiple routes to serve household and institutional demand. Product differentiation leans on verified filter performance, ozone-safety labeling, and quiet designs that can run overnight while maintaining useful air changes. Industry verification reduces uncertainty about third-party filters and protects brand equity for original media, especially in connected ecosystems that prompt replacements through apps. Premium lines emphasize integrated purification and humidification to create year-round value, with examples that pair efficient evaporative systems with quiet particulate capture for bedrooms and living spaces. High-visibility launches in the upper tier also underscore design aesthetics, sustainability cues, and material choices that aim to build differentiation at first sight and in long-term room integration.

Leading brands use platform strategies that extend value through connectivity, predictive prompts, and clear guidance on safety and maintenance. Integration with widely adopted IoT platforms allows devices to fit into broader home routines and building management stacks, which lowers friction for new users and for facility teams that monitor several rooms. In the institutional space, clean-room kits organized around standard operating procedures and verified media align with procurement criteria that reward compliance and documentation. Car-focused technologies also evolve in parallel, where particle charging and optimized mechanical filters improve cabin air and offer cross-learning for room-device airflow and capture strategies. These developments encourage manufacturers to maintain coherent portfolios that cover personal, room, and fleet use cases in the portable air purifier market.

Product news highlights continued investment in filtration breakthroughs, format variety, and targeted use cases. Coway expanded cylindrical lines with units built around high-efficiency multi-stage capture and coverage footprints that support large rooms, which strengthens the brand in premium ranges where verified performance matters. Compact offerings also gain traction, with launches that emphasize light weight, low noise, and accessible pricing for first-time buyers and small spaces. Levoit has introduced products oriented to family scenarios and multi-sensor monitoring with verified VOC reduction claims in defined time windows, which suits wellness-focused positioning and app-managed households. Premium entrants such as IQAir also emphasize material and design choices that reflect sustainability and aesthetics while maintaining advanced particle capture, reinforcing the category’s shift toward year-round appeal. Together, these moves support a broadening of the portable air purifier market that spans personal devices, compact room models, and advanced connected systems for institutions.

Portable Air Purifier Industry Leaders

Dyson

Philips (Versuni)

Xiaomi

Coway

Blueair

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Sharp Business Systems (India) formed a strategic alliance with Amber Enterprises, marking a significant step toward local production of air conditioners. The units are set to feature advanced Plasmacluster ion air purification technology. Production is scheduled to commence at facilities in Dehradun and Sri City, with a targeted output of 500,000 units over the next 3 years. Select window AC models are expected to offer active purification in addition to traditional cooling.

- March 2026: Blueair, a subsidiary of Unilever, has taken a step into the sports marketing arena. The company partnered with the NY Knicks, becoming the team's official air care partner. As part of this collaboration, Blueair's purification systems will be installed in the Knicks' Tarrytown training center. Additionally, co-branded campaigns will be rolled out at Madison Square Garden. This strategic pivot aims to shift the perception of air purifiers from health-crisis solutions to essential tools for everyday performance optimization

- December 2025: Xiaomi unveiled the Mijia Air Purifier 6 Pro. This device has a dual-chip, dual-architecture design complemented by a 13-layer filtration system. With a particulate CADR of 1461 m³/h and a formaldehyde CADR of 1000 m³/h, the purifier is equipped with six sensors monitoring PM1, formaldehyde, dust, PM2.5, temperature, and humidity for precise real-time monitoring.

Global Portable Air Purifier Market Report Scope

| HEPA Filtration |

| Activated Carbon |

| Ionic / Ionizers |

| UV-C Light Purifiers |

| Others |

| Non-Smart (Manual/Analog) |

| Smart/IoT-Enabled (App and Voice Controlled) |

| Single-Function Air Purifiers |

| Multi-Function Units |

| Personal/Desk Purifiers |

| Car Air Purifiers |

| Room Air Purifiers |

| Travel or Wearable Purifiers |

| B2C/Retail | Multi-brand Stores (big box retailers, department stores, electronics chain, home improvement centers) |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B/Directly from the Manufacturers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Technology | HEPA Filtration | |

| Activated Carbon | ||

| Ionic / Ionizers | ||

| UV-C Light Purifiers | ||

| Others | ||

| By Connectivity | Non-Smart (Manual/Analog) | |

| Smart/IoT-Enabled (App and Voice Controlled) | ||

| By Functionality | Single-Function Air Purifiers | |

| Multi-Function Units | ||

| By Application | Personal/Desk Purifiers | |

| Car Air Purifiers | ||

| Room Air Purifiers | ||

| Travel or Wearable Purifiers | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores (big box retailers, department stores, electronics chain, home improvement centers) |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Directly from the Manufacturers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the portable air purifier market growth outlook to 2031?

The portable air purifier market size is set to reach USD 20.51 billion by 2031 on an 8.42% CAGR from 2026 to 2031.

Which segments lead and grow fastest in the portable air purifier market?

HEPA filtration led with 48.92% share in 2025, while activated carbon is projected to be the fastest-growing at an 8.64% CAGR through 2031.

How are institutions influencing demand in the portable air purifier market?

Schools and municipalities are adopting clean-room kits with SOPs, which steadies B2B demand and creates recurring filter budgets for smoke seasons.

What makes smart models attractive in the portable air purifier market?

Connected devices provide real-time air quality, predictive filter prompts, and fleet management, which improve compliance and cut energy waste in buildings.

Which regions are shaping future demand in the portable air purifier market?

Asia-Pacific is projected to expand fastest at an 8.79% CAGR, while North America holds a large share sustained by smoke-readiness programs and safety labeling.

How do regulations influence technology choices in the portable air purifier market?

CARB’s ozone-safety limit and verification programs steer adoption toward mechanical or hybrid systems, which increases trust and supports consistent performance.

Page last updated on: