Wi-Fi Router Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.49 Billion |

| Market Size (2031) | USD 26.08 Billion |

| Growth Rate (2026 - 2031) | 9.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

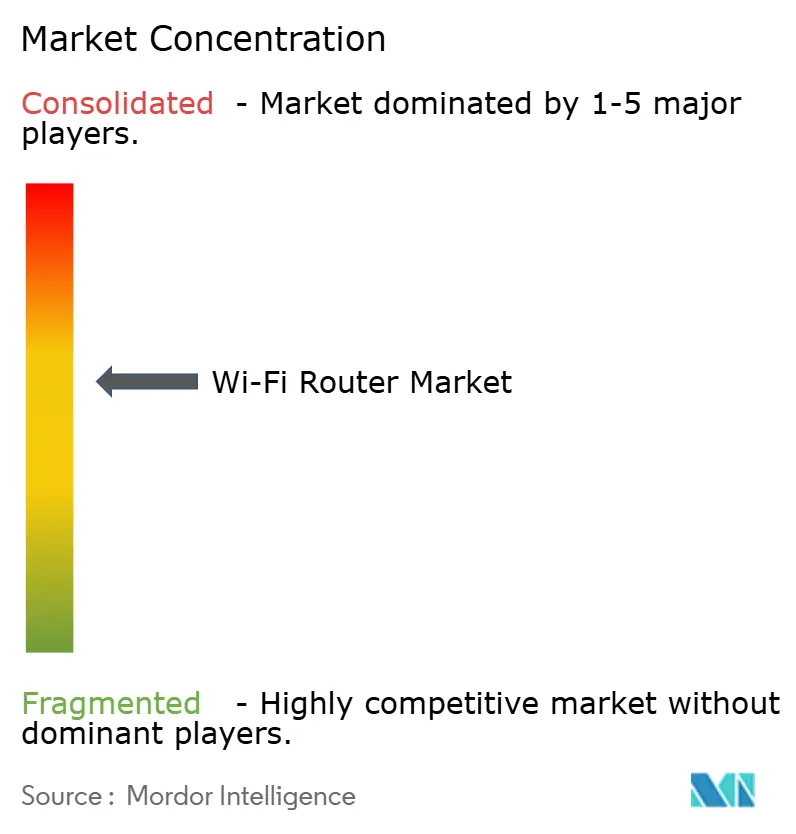

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wi-Fi Router Market Analysis by Mordor Intelligence

The Wi-Fi router market size was valued at USD 15.05 billion in 2025 and estimated to grow from USD 16.49 billion in 2026 to reach USD 26.08 billion by 2031, at a CAGR of 9.60% during the forecast period (2026-2031). Near-term growth reflects fiber-to-the-home rollouts that elevate multi-gigabit WAN demand, enterprise migration to Wi-Fi 7 for immersive collaboration, and government spectrum liberalization in the 6 GHz and 7 GHz bands. Intensifying bandwidth needs from cloud gaming, 8K streaming, and edge AI workloads are pushing internet service providers to refresh network-edge hardware, while residential users embrace mesh designs that remove coverage gaps. Vendors are embedding AI-driven traffic steering and cloud management to lower total cost of ownership for enterprises and service providers. Regulatory alignment around security baselines is lengthening device certification, but hardware-software convergence is emerging as a key differentiator across performance tiers.

Key Report Takeaways

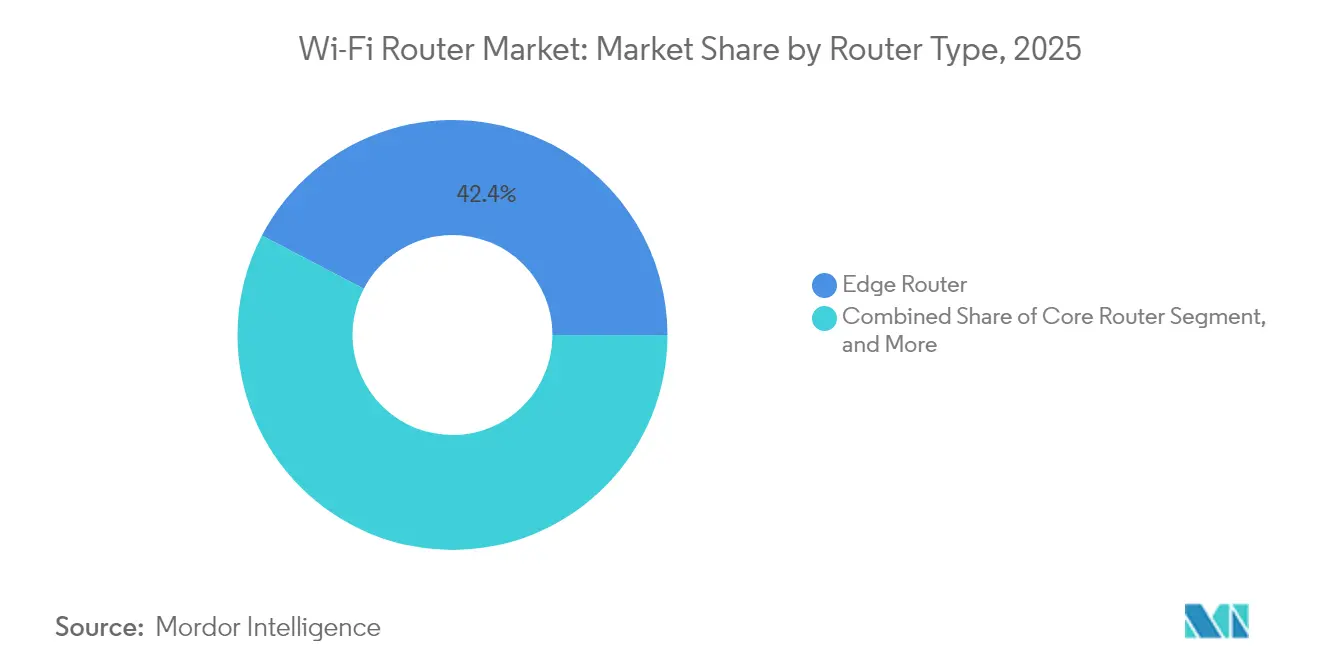

- By router type, edge infrastructure led with 42.35% revenue share in 2025; mesh devices are projected to expand at a 9.62% CAGR through 2031.

- By frequency band, dual-band products retained 47.55% of the Wi-Fi router market share in 2025, while tri-band units are forecast to register a 10.18% CAGR through 2031.

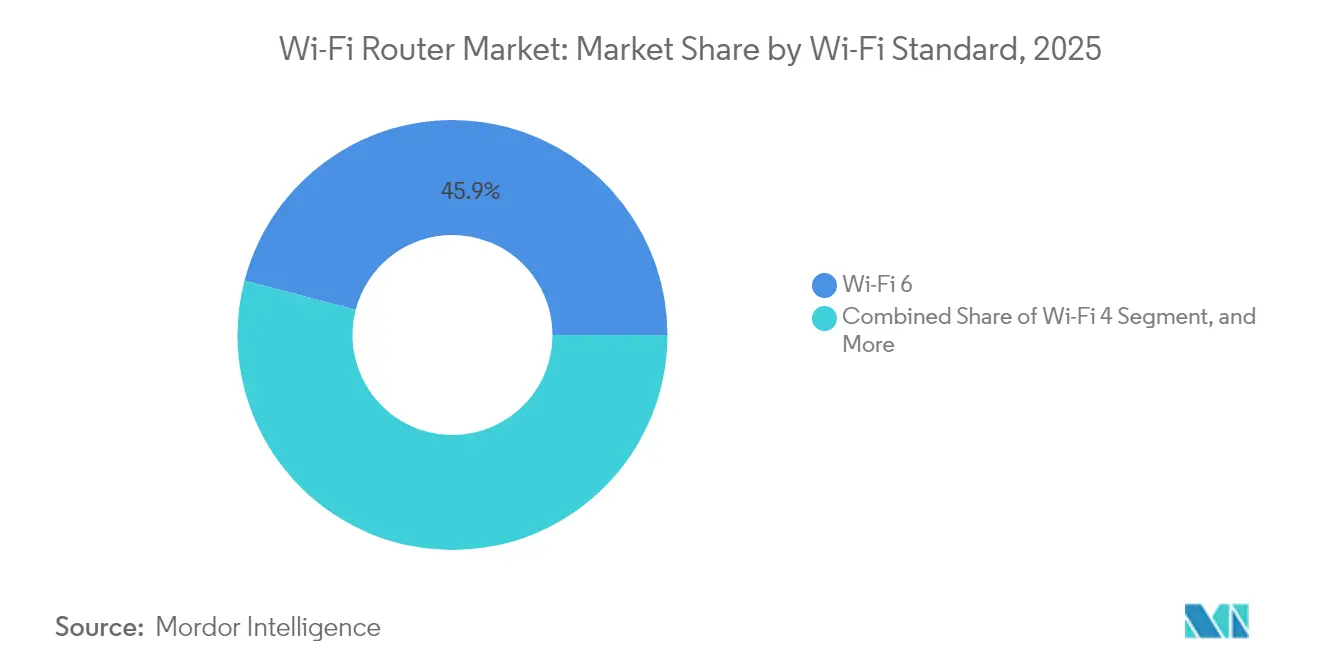

- By Wi-Fi standard, Wi-Fi 6 commanded 45.92% share of the Wi-Fi router market size in 2025, and Wi-Fi 7 is poised for 10.04% CAGR growth to 2031.

- By end-user, residential deployments accounted for a 56.40% share of the Wi-Fi router market size in 2025, and large enterprises are advancing at an 10.86% CAGR through 2031.

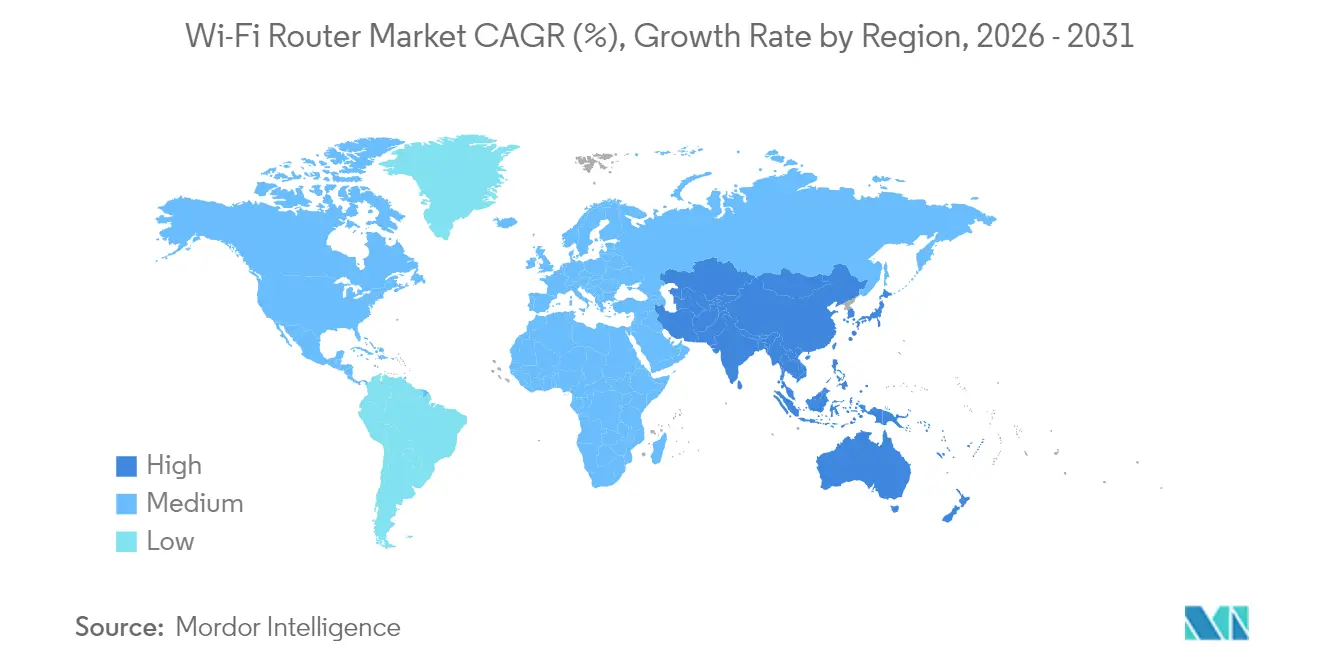

- By geography, North America accounted for 56.30% of the Wi-Fi router market size in 2025, while Asia-Pacific is advancing at a 11.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wi-Fi Router Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fiber-to-home build-outs lift multi-gig WAN demand | +2.1% | North America and Asia-Pacific core | Medium term (2-4 years) |

| Rapid home adoption of Wi-Fi 6 and 6E mesh systems | +1.8% | North America and Europe, expanding Asia-Pacific | Short term (≤ 2 years) |

| Corporate campuses upgrade to Wi-Fi 7 for AR/VR | +1.4% | North America and Europe, selective Asia-Pacific | Medium term (2-4 years) |

| Government spectrum releases fuel premium-band sales | +1.2% | Global | Long term (≥ 4 years) |

| Smart-city public Wi-Fi tenders bundle router buys | +0.9% | Asia-Pacific core | Medium term (2-4 years) |

| Edge-AI traffic steering reduces ISP churn | +0.8% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in fiber-to-home rollouts lifting demand for multi-gig WAN ports

National broadband subsidies and competitive gigabit service packages are driving volume purchases of routers with 2.5 GbE and 10 GbE uplinks. Service providers bundle premium hardware with subscription tiers to secure recurring equipment rentals, while vendors redesign power and thermal subsystems around higher-speed ASICs. The result is a pipeline of feature-rich gateways that bridge legacy Ethernet outlets and next-generation passive optical networks, sustaining momentum for the Wi-Fi router market.

Rapid residential adoption of Wi-Fi 6 and 6E mesh systems

Households now average more than 20 connected devices, prompting a shift from single-point routers to multi-node mesh kits. Wi-Fi 6E introduces a 6 GHz backhaul free from client interference, raising throughput and lowering latency in multistory homes. Government outreach and retailer demonstrations highlight dead-zone elimination, and chipset economies of scale have pulled entry pricing into mass-market ranges. Easy app-based onboarding further accelerates adoption, reinforcing volume growth for the Wi-Fi router market.[3]Commerce Commission New Zealand, “Revealed: the WiFi routers to rent, upgrade to or buy outright,” comcom.govt.nz

Corporate campus upgrades to Wi-Fi 7 to enable AR/VR collaboration suites

Hybrid work models are embedding augmented and virtual reality into daily workflows, demanding sub-10 ms latency and deterministic bandwidth per user. Wi-Fi 7’s multi-link operation and 320 MHz channels address these needs and integrate with existing PoE+ infrastructure. IT leaders are standardizing on Wi-Fi 7 to future-proof facility refresh cycles, propelling enterprise hardware refreshes that benefit the Wi-Fi router market.

Government spectrum releases accelerating premium-band router sales

Allocations of up to 1,200 MHz in the 6 GHz band offer wider channels and lower interference. Vendors add extra radio chains to exploit the new spectrum, and early adopters in urban settings pay premium prices for congestion-free performance. Policy coordination through bodies such as the ITU supports manufacturing scale, driving a virtuous cycle of demand and cost reduction.[2]Sourceability, “2025 Semiconductor Predictions,” sourceability.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from 5G FWA CPE devices in suburban areas | -1.6% | Global | Short term (≤ 2 years) |

| Persistent chipset shortages for Wi-Fi 7 tri-band SKUs | -1.3% | Global | Medium term (2-4 years) |

| Rising cyber-attack surface lengthens certification | -0.8% | Global | Long term (≥ 4 years) |

| Home-renter shift to ISP-leased gateways curbs retail demand | -0.7% | Developed rental markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from 5G FWA CPE devices in suburban areas

Mobile network operators leverage existing towers to deliver fixed-wireless broadband, bundling a cellular modem with integrated Wi-Fi, thereby displacing standalone routers. Attractive economics in fiber-scarce suburbs tighten price elasticity for retail hardware. Vendors counter with hybrid designs that fall back to cellular networks yet must absorb higher bill-of-materials costs, tempering the Wi-Fi router market expansion.

Persistent chipset shortages for Wi-Fi 7 tri-band SKUs

Advanced RF transceivers and front-end modules compete with automotive and handset capacity at 5 nm and below. Lead times frequently exceed six months, delaying volume launches of flagship tri-band routers. Manufacturers diversify sourcing and pre-buy wafers, but inventory buffers elevate working capital. Supply friction remains a material drag on the Wi-Fi router market.[1]Jabil, “Why the Chips Are Down: Navigating the Global Chip Shortages and Beyond,” jabil.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Router Type: Edge infrastructure drives market leadership

Edge units held the top spot with 42.35% of 2025 revenue. Their ability to aggregate multi-access traffic, support security overlays, and host edge-computing workloads keeps them indispensable to carriers and large enterprises. The Wi-Fi router market size for edge models is projected to widen in step with 5G backhaul and metro fiber densification. Mesh devices form the fastest-growing cohort, benefiting from consumer demand for seamless roaming and scalable node counts. Their 9.62% CAGR through 2031 stands out as service providers bundle three-pack kits into premium tiers. Core routers log steady but slower upgrades owing to longer depreciation cycles within tier-1 backbones. SOHO units attract price-sensitive micro-businesses yet face cannibalization from ISP gateways. The competitive field centers on software-defined networking, AI-powered diagnostics, and zero-touch provisioning, with enterprises valuing analytics that cut mean time to repair. Ecosystem APIs that integrate remote monitoring into IT service-management suites are becoming purchasing criteria, reinforcing stickiness for platform-centric vendors.

Second-tier telcos in emerging markets exhibit growing appetite for edge routers that consolidate subscriber management, quality-of-service, and security at a single touchpoint. Hardware refreshes coincide with regulatory pushes for IPv6 readiness and lawful-intercept compliance. Vendors leverage network-function virtualization to unlock subscription-based feature licensing, creating new monetization streams inside the Wi-Fi router market. Edge platforms are also evolving into containerized compute nodes that host CDN offloads and IoT gateways, increasing billable density per installation while aligning with operator sustainability targets through reduced power draw and space savings.

By Frequency Band: Dual-band dominance faces tri-band disruption

Dual-band designs held 47.55% share in 2025 and remain the mainstream choice for cost-balanced coverage across 2.4 GHz and 5 GHz. Ongoing device diversification and streaming adoption, however, strain bandwidth ceilings, catalyzing upgrade cycles toward tri-band solutions. Tri-band units, adding a 6 GHz radio, are forecast for a 10.18% CAGR and stand to capture a growing portion of the Wi-Fi router market size. Premium buyers seek dedicated backhaul throughput and reduced interference, especially in dense dwellings where neighbor networks congest legacy bands. Single-band routers linger in ultra-low-cost and industrial telemetry roles, while quad-band Wi-Fi 7 models debut in the enthusiast and SMB prosumer niches.

Consumer awareness remains pivotal: users often underutilize a third band without proper client steering or node placement. Retailers and ISPs are boosting education through interactive setup apps and augmented reality alignment tools. Cost headwinds include additional RF chains, antennas, and shielding that raise thermal loads, demanding novel heatsink designs to maintain consumer-grade acoustics. Regulatory certification in multi-band SKUs spans emissions, DFS compliance, and region-specific spectral masks, prolonging time to market. Nonetheless, economies of scale are funneling tri-band price points downward, narrowing the total cost of ownership delta and accelerating replacement demand inside the Wi-Fi router market.

By Wi-Fi Standard: Wi-Fi 6 leadership yields to Wi-Fi 7 innovation

Wi-Fi 6 maintained 45.92% share last year, carried by widespread smartphone compatibility and mature chipset supply. Gains in client density via OFDMA and lower battery drain through target-wake-time make Wi-Fi 6 routers still attractive for mainstream replacements. Yet Wi-Fi 7 units enjoy a 10.04% forecast CAGR, riding enterprise appetite for latency-critical collaboration and early-adopter households hungry for multi-gigabit wireless. Wi-Fi 5 persists in emerging markets seeking affordability, while industrial IoT nodes occasionally rely on even older standards for legacy protocol support.

Wi-Fi 7’s 4096-QAM modulation and 320 MHz channels push theoretical throughput above 30 Gbps, though real-world gains hinge on client silicon availability and regulatory channelization. Multi-Link Operation addresses reliability by bonding traffic across bands, a feature prized in healthcare and manufacturing deployments. Vendors differentiate through cloud analytics suites that visualize interference, automate RF tuning, and forecast capacity hot spots. Certification complexity rises due to expanded PHY and MAC features, yet early mover advantage remains compelling inside the Wi-Fi router market.

Entry-tier Wi-Fi 7 price erosion is tied to volume silicon ramps, which lag premium segments by roughly 12 months. Component shortages for advanced front-end modules lengthen lead times, directing OEMs toward flexible PCB and antenna designs that accommodate parts substitution, thereby preserving launch schedules.

By End-User: Residential dominance challenged by enterprise growth

Residential deployments captured 56.40% of 2025 sales, fueled by mesh conversions, smart-home gadget adoption, and remote work bandwidth spikes. Consumers value plug-and-play setup, parental controls, and security subscriptions bundled into app-centric interfaces. The Wi-Fi router market size is likely to keep a residential tilt, but enterprise demand shows steeper acceleration. Large organizations, projected at an 10.86% CAGR, are swapping legacy controllers for cloud-managed Wi-Fi 7 estates to serve conference-room AR/VR, digital twin modeling, and real-time analytics.

Small and medium businesses gravitate toward unified threat-management routers that fold firewall and SD-WAN features into a single appliance, preserving capital budgets. Public sector investments align with digital-government initiatives that mandate secure wireless in schools, clinics, and transport hubs. Industrial settings require rugged housings and extended temperature ratings, thereby calling for metal chassis, conformal-coated PCBs, and vibration-resistant connectors. Router vendors increase vertical alignment through certifications such as IEC 62443 for industrial security and HIPAA compliance modules for healthcare. This tailoring expands addressable revenue pools and raises switching barriers, reinforcing stickiness in the Wi-Fi router market.

Geography Analysis

North America, with 56.30% 2025 share, remains the hub of premium hardware adoption. Early availability of 6 GHz spectrum, aggressive fiber competition, and enterprise technology budgets accelerate refresh cycles. Consumers routinely upgrade on three-year cadences, and cable MSOs subsidize gateway swaps to defend against 5G FWA encroachment. Enterprises anchor Wi-Fi 7 pilots in U.S. campuses, generating reference designs that ripple through subsidiary offices worldwide.

Asia-Pacific remains the growth epicenter at a 11.62% CAGR. China drives scale through state-backed gigabit-city mandates, while India’s BharatNet and private fiber consortia expand rural connectivity. Local router OEMs benefit from favorable procurement policies, yet global brands retain share in premium tiers. Smart-city proofs in Singapore, Seoul, and Tokyo require high-density public Wi-Fi coupled with edge compute, widening opportunities for feature-rich platforms. Manufacturing clusters in Shenzhen and Penang expedite design iterations, shortening the time from concept to retail and benefiting the Wi-Fi router market.

Europe posts steady mid-single-digit expansion as enterprises modernize medieval campuses and households migrate to mesh. Fragmented language and regulatory landscapes compel vendors to invest in regional firmware localization and GDPR-aligned data handling. Multi-dwelling units across Germany and France shift toward ISP-managed gateways, slightly dampening retail turnover. Meanwhile, the Middle East and Africa see emerging urban corridors leveraging Wi-Fi for e-government kiosks and fintech POS terminals, while Latin America’s improving macroeconomic climate unlocks pent-up consumer router upgrades from Wi-Fi 4 to Wi-Fi 6. Currency volatility and import duties shape local pricing, leading OEMs to adopt in-region final assembly to sidestep tariffs and bolster the Wi-Fi router market.

Competitive Landscape

Competition is moderately fragmented: the top five vendors hold an estimated 54% combined share. Incumbents such as Cisco, Huawei, and TP-Link lean on vast channel networks and proprietary silicon partnerships to sustain cost leadership. They bundle subscription security and analytics to create annuity streams that hedge hardware cyclicality. Mid-tier players, including Netgear and ASUS, concentrate on gamer-centric and prosumer niches, using brand loyalty and industrial design flair to defend shelf space.

Cloud-native disruptors like Ubiquiti and Cambium differentiate through extensible management consoles, offering zero-touch provisioning and cross-site telemetry. White-label ODMs flood the entry tier, targeting value-driven emerging markets with Wi-Fi 6 chipsets. Technology roadmaps now prioritize on-device AI for real-time quality-of-experience scoring, WPA3 auto-patching, and spectrum sensing that pre-empts interference. Patent portfolios around beamforming, multi-link scheduling, and low-power IoT sidebands are increasingly deployed as bargaining chips in cross-licensing deals.

Strategic moves illustrate the landscape’s dynamism. Belkin’s USD 500 million acquisition of Linksys expands combined R&D in Wi-Fi 7 and strengthens big-box retail positioning. TP-Link’s 2025 Wi-Fi 7 lineup integrates third-party cybersecurity via F-Secure, demonstrating a pivot toward service ecosystems. Cisco earmarked USD 200 million for Wi-Fi 7 silicon and cloud orchestration, reinforcing enterprise resonance. Lantronix’s buyout of NetComm’s industrial business adds ruggedized cellular router depth, elevating its vertical specialization. Amazon’s eero unit released Wi-Fi 6E mesh with Thread backhaul to anchor smart-home networks. Collectively, these maneuvers underscore an industry balancing hardware innovation with platform-centric recurring revenue models that expand the Wi-Fi router market.

Wi-Fi Router Industry Leaders

Cisco Systems, Inc.

Huawei Technologies Co., Ltd.

TP-Link Technologies Co., Ltd.

ASUSTeK Computer Inc.

D-Link Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Belkin International completed its acquisition of Linksys Holdings for USD 500 million, targeting USD 50 million in annual cost synergies.

- January 2025: TP-Link unveiled a full Wi-Fi 7 portfolio with AI optimization and F-Secure cybersecurity integration.

- December 2024: Lantronix bought NetComm’s IoT networking arm for USD 25 million to deepen industrial router capability.

- November 2024: Cisco committed USD 200 million to Wi-Fi 7 silicon development and cloud management expansion.

Global Wi-Fi Router Market Report Scope

A Wi-Fi router is a device that performs the functions of a router and includes the functions of a wireless access point with the help of a single, dual, and tri-band. It is a device that provides access to the Internet, or computers, laptops, and tablets, to a network. It allows users to share an Internet connection, files, or printers in a local area network (LAN).

The global Wi-Fi router market is segmented by type ( edge router and core router), by organization size (small and medium enterprises and large enterprises), by end-user industry (healthcare, transportation & logistics, retail & e-commerce, manufacturing, government, BYFI, and other industries) and by geography (North America, Europe, Asia Pacific, Middle East and Africa, and Latin America).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Edge Router |

| Core Router |

| Mesh Router |

| SOHO Router |

| Single-Band (2.4 GHz) |

| Dual-Band (2.4 and 5 GHz) |

| Tri-Band (2.4 , 5 and 6 GHz) |

| Quad-Band (Wi-Fi 7) |

| Wi-Fi 4 (802.11n) |

| Wi-Fi 5 (802.11ac) |

| Wi-Fi 6 (802.11ax) |

| Wi-Fi 6E |

| Wi-Fi 7 (802.11be) |

| Residential |

| Small and Medium Enterprises |

| Large Enterprises |

| Public Sector and Government |

| Industrial and Manufacturing |

| Retail and E-commerce |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Router Type | Edge Router | ||

| Core Router | |||

| Mesh Router | |||

| SOHO Router | |||

| By Frequency Band | Single-Band (2.4 GHz) | ||

| Dual-Band (2.4 and 5 GHz) | |||

| Tri-Band (2.4 , 5 and 6 GHz) | |||

| Quad-Band (Wi-Fi 7) | |||

| By Wi-Fi Standard | Wi-Fi 4 (802.11n) | ||

| Wi-Fi 5 (802.11ac) | |||

| Wi-Fi 6 (802.11ax) | |||

| Wi-Fi 6E | |||

| Wi-Fi 7 (802.11be) | |||

| By End-User | Residential | ||

| Small and Medium Enterprises | |||

| Large Enterprises | |||

| Public Sector and Government | |||

| Industrial and Manufacturing | |||

| Retail and E-commerce | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Wi-Fi router market in 2026?

The Wi-Fi router market size reached USD 16.49 billion in 2026 and is set to climb to USD 26.08 billion by 2031.

What is the forecast growth rate for Wi-Fi routers to 2031?

The market is projected to expand at a 9.60% CAGR through the 2026-2031 period.

Which router type is growing fastest?

Mesh systems are the fastest-growing category, expected to post a 9.62% CAGR as households seek seamless whole-home coverage.

Why is tri-band adoption accelerating?

Tri-band routers add a 6 GHz channel that reduces interference and dedicates bandwidth for backhaul, addressing congestion in dual-band setups.

What drives enterprise demand for Wi-Fi 7 hardware?

Enterprises are upgrading to Wi-Fi 7 to enable latency-sensitive AR and VR collaboration that demands multi-gigabit speeds and deterministic performance.

Which region offers the highest growth opportunity?

Asia-Pacific is forecast for a 11.62% CAGR, supported by aggressive broadband infrastructure expansion and smart-city investments.

Page last updated on: