Wireless Intercoms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

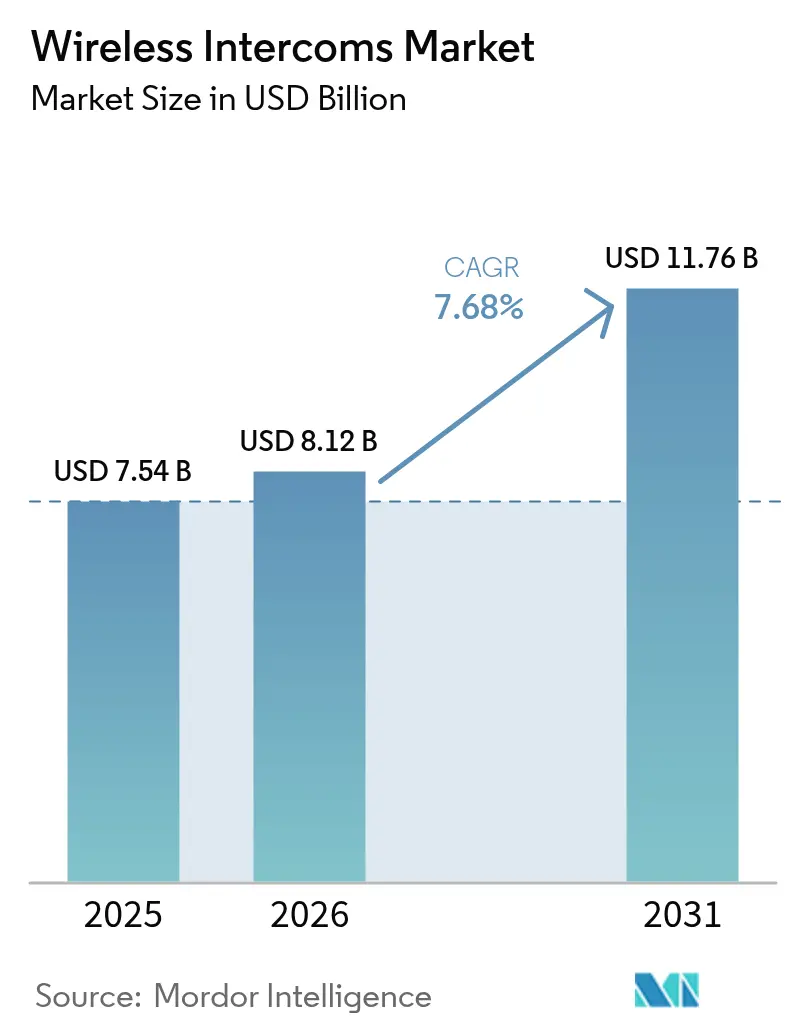

| Market Size (2026) | USD 8.12 Billion |

| Market Size (2031) | USD 11.76 Billion |

| Growth Rate (2026 - 2031) | 7.68% CAGR |

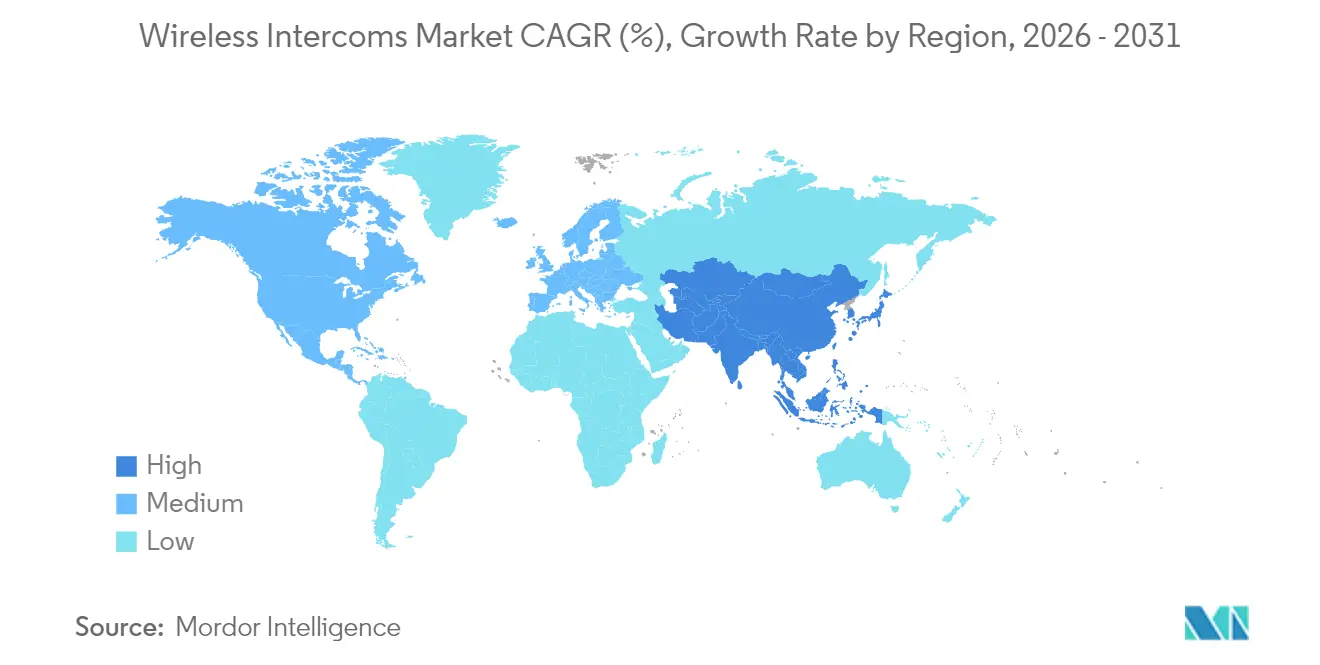

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wireless Intercoms Market Analysis by Mordor Intelligence

The Wireless Intercoms market size is expected to grow from USD 7.54 billion in 2025 to USD 8.12 billion in 2026 and is forecast to reach USD 11.76 billion by 2031 at 7.68% CAGR over 2026-2031.

Demand follows the steady shift from hard-wired voice panels to IP-enabled, multi-modal systems that blend audio, video, and data across the same network backbone. Widespread digitization of building infrastructure, improved affordability of Wi-Fi 6E and private 5G radios, and occupational-safety rules that formalize hands-free communication are the primary growth levers. Competitive intensity is rising as cloud-native entrants bundle device management and analytics with hardware, creating lifetime value propositions that appeal to facility owners who lack in-house IT resources. Procurement patterns also favor scalable architectures that limit tooling downtime, trimming installation labor in an environment where RF-certified technicians remain scarce.

Key Report Takeaways

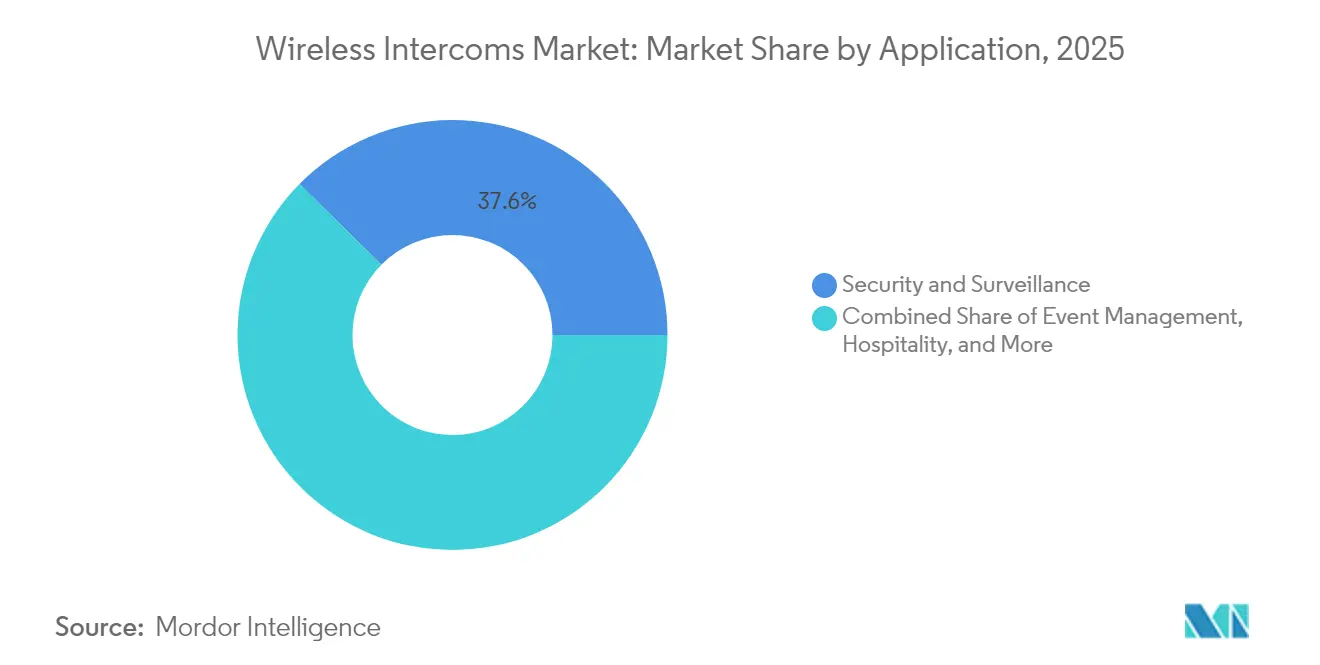

- By application, security and surveillance led with 37.60% revenue share in 2025, while event management applications are projected to expand at a 9.14% CAGR to 2031.

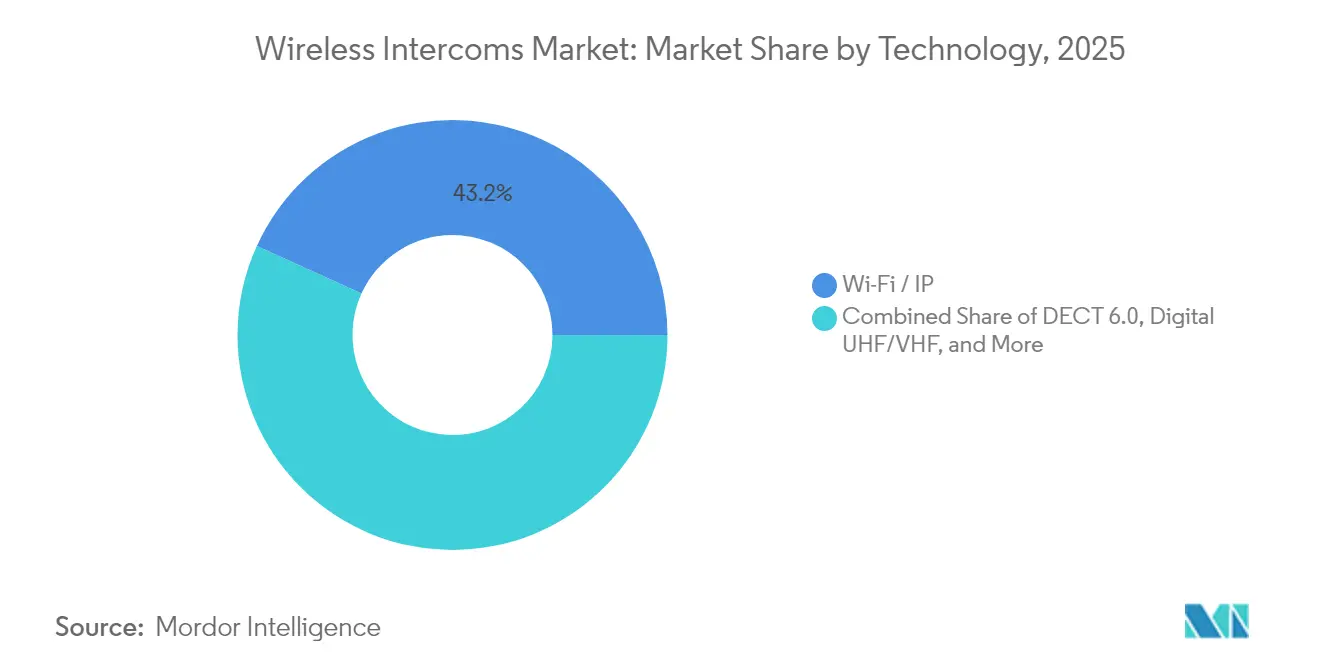

- By technology, Wi-Fi/IP solutions held a 43.20% share in 2025; LTE/5G systems post the fastest 10.72% CAGR through 2031.

- By end-use sector, residential installations commanded 40.60% of the wireless intercoms market share in 2025; enterprise and campus deployments are forecast to grow at 8.23% CAGR by 2031.

- By region, North America accounted for 35.70% of 2025 revenue; Asia Pacific is advancing at a 10.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wireless Intercoms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding demand for security and surveillance solutions | +2.10% | Global, strong in North America & Europe | Medium term (2-4 years) |

| Proliferation of Wi-Fi/IP-based smart-home intercoms | +1.80% | North America, Europe, APAC urban centers | Short term (≤2 years) |

| Smart-building and infrastructure modernization wave | +1.50% | APAC core, spill-over to MEA | Long term (≥4 years) |

| Shift to full-duplex mesh intercoms in live events | +1.20% | Global, major event venues | Medium term (2-4 years) |

| Occupational-safety rules mandating hands-free comms | +0.9% | North America & EU, moving to APAC | Short term (≤2 years) |

| LTE/5G site-based systems for temporary job sites | +0.8% | Early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding demand for security and surveillance solutions

Integrated intercom platforms now feed audio streams directly into video analytics consoles so control-room operators can correlate spoken commands with visual alerts. Hospitals illustrate this convergence as Zenitel systems automatically escalate a distress call to security staff and lock designated access doors when embedded speech engines detect specific keywords. At major airports, Ericsson’s private LTE backbone supports mission-critical push-to-talk between tarmac crews and tower staff, reducing taxi-time deviations and improving incident traceability. High-purity quartz shortages during 2024 highlighted supply-chain fragility, prompting facility owners to favor modular devices that can be swapped without re-certifying the entire array. Tight pairing of voice, video, and analytics shortens forensic investigation cycles, a decisive benefit for operators facing budget scrutiny. The result is a firm linkage between security-centric capital expenditure and wireless intercom adoption.

Proliferation of Wi-Fi/IP-based smart-home intercoms

Residential builders increasingly bundle voice panels with door cameras on the same Wi-Fi 6E network, simplifying low-voltage wiring plans and cutting commissioning time. CableLabs research confirms that the 6 GHz band alleviates earlier congestion that degraded voice quality in dense apartment blocks[1]CableLabs, “Wi-Fi 6E Capacity Modeling Paper,” cablelabs.com. AiphoneCloud lets installers troubleshoot devices remotely, lowering truck-roll costs and making subscription models more attractive to property managers. Hotels echo this IP trend; Stryker’s Vocera badge integrates with property-management back-ends, allowing staff to receive housekeeping tasks as secure voice prompts rather than mobile app notifications that require screen interaction. The cumulative effect is faster refresh cycles for legacy analog door stations, reinforcing demand nodes for the wireless intercoms market.

Smart-building and infrastructure modernization wave

China’s national “Signal Upgrade” projects earmark 120,000 public venues for multi-operator indoor coverage, forming an ample substrate for IP intercom retrofits in train stations and civic buildings. In healthcare, ultra-low-latency 6G pilots showed that bedside diagnostics and nurse calling can share the same wideband audio link without packet loss, validating multi-service convergence. Industrial plants add explosion-proof stations from INDUSTRONIC that tie into distributed control systems and trigger alarms if gas thresholds exceed preset limits. Aviation schemes adopt multi-bearer communication combining 5G, satcom, and Wi-Fi to maintain coverage even when one path is impaired, a model detailed in MDPI Aerospace field trials. Densification places fresh emphasis on spectrum-sharing protocols that boost channel reuse by up to 140%, according to MDPI Sensors simulations.

Shift to full-duplex mesh intercoms in live events

Nodal mesh topologies eliminate the push-to-talk lag common to half-duplex radios, a critical upgrade for broadcast directors juggling multiple camera teams. At Super Bowl LVII, Green-GO’s LTE Private Wireless handled 60 beltpacks without audio clipping despite heavy RF competition in the stadium bowl. London’s Royal Albert Hall retrofitted Riedel Bolero sets that roam seamlessly across foyers and backstage corridors where thick masonry previously blocked line-of-sight signals. Clear-Com’s FreeSpeak platform scans 1.9 GHz, 2.4 GHz, and 5 GHz in real time and auto-hops to the cleanest slot, sustaining command latency below 25 ms under full house lighting. Mesh kits slash rigging time for touring production firms, a bottom-line incentive that accelerates unit turnover in the wireless intercoms market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RF interference and spectrum congestion | -1.40% | Global, acute in dense urban areas | Short term (≤2 years) |

| Cyber-security vulnerabilities in IP devices | -1.10% | Global, heightened in enterprise segments | Medium term (2-4 years) |

| Shortage of RF-IT skilled installers | -0.8% | North America & Europe | Short term (≤2 years) |

| Global spectrum-licence fragmentation | -0.6% | Varies by jurisdiction | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

RF interference and spectrum congestion

Six-gigahertz Wi-Fi channels are nearing saturation in high-rise dwellings, a problem visualized in CableLabs multi-floor simulations that reveal head-of-line blocking for low-latency traffic such as intercom voice. Shared-spectrum policies offer partial relief but add coordination overhead. Japan’s Technical Regulations Conformity Certification requires each wireless appliance to pass separate band tests at 315 MHz, 400 MHz, 920 MHz, and 2.4 GHz, lengthening approval cycles. The US National Spectrum R&D Plan stresses dynamic sensing as a remedy, but large-scale deployment remains years away[2]NITRD, “National Spectrum Research & Development Plan,” nitrd.gov. In the interim, vendors integrate interference-rejection antennas that raise the bill of materials.

Cyber-security vulnerabilities in IP devices

A 2024 vulnerability in Hikvision door stations let attackers trigger hidden microphones remotely, exposing tenants to eavesdropping. Because intercoms now sit on the same VLAN as building-management controllers, a breach can cascade. Healthcare operators must verify that firmware updates do not disturb FDA device certifications, slowing patch rollouts and keeping risk windows open. Blockchain-anchored audit trails show promise yet add processor overhead that raises power draw an issue for battery-backed stations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Security Dominance Drives Innovation

Security and surveillance accounted for 37.60% of the wireless intercoms market in 2025, underscoring the modality’s central role in layered defense architectures. The segment benefits from mandatory access-control upgrades in airports, hospitals, and data centers, where voice verification now complements biometric scans. Suppliers differentiate by embedding noise cancellation and AI keyword spotting that escalate alerts without operator input. Event management, while smaller in absolute revenue, is forecast to post a 9.14% CAGR, propelled by full-duplex mesh radios that let show directors coordinate light cues, pyrotechnics, and broadcast links in real time. Healthcare keeps adopting intercom-driven workflow automation; Zenitel’s turbine units integrate with nurse-call middleware so staff can triage before entering isolation wards, cutting personal-protective gear use. Logistics firms deploy truck-scale intercoms that pair with weigh-bridge software, slashing idle time and minimizing driver-dock interactions, a feature validated in Zenitel–B-TEK pilots.

Event production’s embrace of wireless comms is visible in multi-venue contracts that specify roaming capability across auditoriums, stadiums, and temporary marquees. Hospitality chains gravitate toward discreet badge-style devices that mesh with property-management software, ensuring housekeeping can signal engineering without two-way radios that may disturb guests. Heavy-industry sites demand intrinsically safe housings and wide-area horns linked to the same talk paths, an offering INDUSTRONIC couches as a “one network, all alarms” proposition. Education campuses opt for mass-notification integration, enabling simultaneous lockdown announcements and intercom overrides from a single GUI. Collectively, application diversity cements multiprotocol compatibility as a must-have feature across the wireless intercoms market.

By Technology: Cellular Networks Challenge Wi-Fi Dominance

Wi-Fi/IP frameworks held a 43.20% share in 2025 through natural adjacency to existing LANs. Ease of Power-over-Ethernet cabling and centralized authentication make Wi-Fi attractive for retrofits. However, LTE/5G gateways now log the strongest 10.72% CAGR as contractors adopt private 5G slices that offer licensed-grade performance without monthly carrier fees. The wireless intercoms market size for LTE/5G deployments in events is projected to reach USD 2.28 billion by 2031, supported by spectrum-sharing frameworks that accommodate pop-up cell sites in sports arenas. DECT 6.0 remains popular in elder-care facilities for its immunity to Wi-Fi congestion, yet chipset roadmaps show limited bandwidth expansion, steering greenfield projects toward OFDMA-based alternatives. Digital UHF/VHF persists within petrochemical clusters where metallic superstructures attenuate higher-frequency waves.

Mesh-based cellular kits demonstrated spectacular reliability during Super Bowl LVII, where Green-GO managed 60 concurrent talk groups on a dedicated 700 MHz slice with no packet loss. Meta’s published patents on coexistence algorithms aim to let AR headsets and intercoms share narrow 60 GHz beams without mutual jamming, foreshadowing new industrial-XR use cases. Sony’s multi-link scheme combines 2.4 GHz control with 5 GHz media payloads, increasing throughput by 55% in laboratory trials. Technology suppliers stress open APIs so customers can snap intercom presence into broader workplace-collaboration dashboards.

By End-use Sector: Enterprise Growth Outpaces Residential

The residential segment retained 40.60% of 2025 revenue by virtue of sheer dwelling volume and the bundling of door stations with smart-lock sales. Growth moderates as early-adopter homes reach saturation, but refresh cycles are shortening because app-controlled deliveries and aging-in-place requirements push owners to upgrade analog doorbells. The enterprise and campus segment is the expansion engine, forecast to climb 8.23% CAGR through 2031. Facilities managers prioritize devices that provide audit trails and integrate with visitor-management kiosks. The wireless intercoms market size for enterprise sites is projected to command USD 5.25 billion by 2031, underpinned by safety-critical roles in warehouses and semiconductor fabs.

Motorola Solutions’ USD 10.8 billion 2024 revenue, mainly from land-mobile radios, signals enterprises’ willingness to pay a premium for rugged hardware and the analytics stack that accompanies it. Government agencies adopt encryption-capable units that dovetail with public-safety LTE corridors, ensuring interoperability during emergencies. Education districts still retrofit analog PA systems, but budgets increasingly earmark SIP gateway cards that let voice alerts bridge into VoIP trunks, expanding the wireless intercoms industry footprint in public sector budgets.

Geography Analysis

North America generated 35.70% of 2025 revenue, buoyed by stringent OSHA mandates and mature indoor-coverage infrastructure that favors early adoption of private 5G intercoms. Large system integrators lock in long-term maintenance contracts, enabling sustained upgrade cycles. Fiscal 2025 procurement sees airports prioritizing redundant talk paths after FAA ground-stop incidents underscored voice resiliency gaps. The National Spectrum R&D Plan’s backing for dynamic sharing experiments adds policy certainty that encourages vendor R&D spend.

Asia Pacific posts the fastest 10.42% CAGR. China’s “Signal Upgrade” mission funnels state and private capital into indoor mobile coverage across 120,000 venues, creating a platform for wireless intercom rollouts. India’s telecom sector, worth INR 2.4 trillion (USD 29.0 billion) in FY24, benefits from a regulatory quality-rating tool that prods landlords to install high-availability connectivity, lifting intercom attach rates. Japanese compliance testing ensures low emissions gear, spurring domestic suppliers to embed interference-mitigation filters that later become export advantages.

Europe registers steady growth on the back of energy-efficient smart-building retrofits. Directive-led targets for carbon neutrality by 2030 require converged networks that reduce cabling duplication. EU Worker Safety regulations classify full-duplex voice as a critical control measure in high-noise zones, energizing demand for ATEX-rated intercoms. South America and the Middle East & Africa see intercom adoption ride on transportation upgrades, metros in São Paulo and Riyadh specify IP voice along platform edges, and hospitality expansions linked to tourism corridors.

Regulatory Landscape

Wireless intercoms sit at the intersection of radio approvals, building-system safety requirements, and cybersecurity expectations, which vary by region and shape product SKUs and certification lead times. In the United States, FCC actions such as the February 2024 Report and Order (FCC-24-22) that enabled Wireless Multichannel Audio Systems to operate with wider bandwidths (up to 20 MHz) underscore how rule evolution continues to affect professional wireless audio and intercom-like use cases in dense venues. In Europe, the consolidated Radio Equipment Directive (2014/53/EU) remains the access anchor through essential requirements on health and safety, EMC, and effective spectrum use, which pushes vendors toward consistent test and technical documentation packages across member states.

Standards bodies are also tightening intercom-specific requirements that feed into design choices for IP-enabled, building-integrated products. EN IEC 62820-1-1:2026 was published in May 2026 as a foundational building intercom systems standard, updating baseline system requirements alongside references to newer safety and EMC frameworks, which raises compliance expectations for products sold into regulated building and critical-facility deployments. For professional audio and events, European spectrum governance for PMSE devices was updated via European Commission Implementing Decision (EU) 2025/105 (published January 2025, with the prior regime repealed effective July 1, 2025), reinforcing the need for vendors to track spectrum rules alongside RF performance and roaming capabilities.

Value Chain Analysis

The wireless intercoms value chain starts upstream with RF chipsets, antennas, batteries, optics (for video intercoms), and ruggedized enclosures, then extends through ODM/OEM manufacturing and firmware development, followed by certification and systems integration. Differentiation increasingly shifts into software layers, including device provisioning, identity and certificate management, and cloud administration portals, as intercom endpoints connect via SIP/WebRTC media planes and integrate into access control, video management, and broader building-management ecosystems. Standards development and conformance testing serve as gating steps, with bodies such as ETSI (DECT and DECT-2020 NR specifications) and IEC (building intercom system requirements) shaping product roadmaps and regional compliance variants.

Midstream, vendors combine dedicated RF (DECT, UHF/VHF, mesh) with IP transport (Wi-Fi/IP and LTE/5G), shifting sourcing and partner expectations toward carrier-grade modems, SIM/eSIM workflows, and cybersecurity hardening for enterprise buyers. Downstream, specialized distributors and system integrators drive enterprise, campus, transportation, and public-venue deployments by bundling intercom hardware with network design, RF surveys, and commissioning, then monetizing recurring service through maintenance and remote management. Recent launches such as Clear-Com FreeSpeak Cell (LTE/5G-based production communications) and software scaling updates for matrix and central-station platforms show how suppliers are moving toward ecosystems rather than single endpoints, tying beltpacks, base stations, cloud dashboards, and IP gateways into unified offerings.

Competitive Landscape

The wireless intercoms market shows moderate fragmentation. The top five suppliers hold an estimated 47% combined share, with Motorola Solutions, Zenitel, Clear-Com, Aiphone, and Riedel at the front. Motorola leverages vertical integration from chipset to SaaS dashboards, helping cushion semiconductor supply shocks that lifted 2024 component costs by 13.1%. Zenitel focuses on harsh-environment audio with IECEx-rated housings for oil rigs, earning sole-source status in certain Norwegian shelf tenders. Clear-Com differentiates through multi-band roaming radios that automatically dodge interference, winning long-term broadcast contracts at Olympic venues.

Start-ups such as Theatro, recently acquired by Motorola, inject AI speech analytics that parse frontline-worker requests in retail aisles. Aiphone’s SaaS pivot enables recurring revenue. Patent filings from Meta and Sony illustrate a pivot toward ultra-wideband coexistence and dual-link throughput gains, foreshadowing new entrants from consumer electronics backgrounds. Partnerships also flourish; Ericsson joins Streamwide to deliver mission-critical push-to-talk over private LTE at Charles de Gaulle, a template now eyed by Asian hubs. M&A activity intensifies as vendors hedge component price volatility by bringing PCB assembly and antenna design in-house.

Competition centers on three axes: spectrum efficiency, cloud manageability, and cybersecurity hardening. Vendors with zero-trust firmware roadmaps and automatic certificate rotation gain traction with enterprise CISOs. Meanwhile, supply-chain localization strategies prioritize near-shore electronics plants to sidestep freight delays and tariff exposure.

Wireless Intercoms Industry Leaders

Panasonic Corporation

Motorola Solutions Inc.

Clear-Com, LLC

Telephonics Corporation

Commend international GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Standardization is creating whitespace for interoperable, security-graded building intercom deployments that connect residential, commercial, and campus networks. The publication of IEC 62820-1-1:2026 in March 2026 formalizes system requirements for building intercom equipment and adds a clearer framework for specifying performance and security-related requirements, which supports procurement standardization for multi-site facility owners and systems integrators. Vendors that map products and documentation to this baseline, while also aligning with regional radio compliance regimes, can position for scaled rollouts where buyers want repeatable designs across portfolios.

Another opportunity is converged communications, where intercom functions connect to broadband push-to-talk and legacy radio networks used by public safety, transportation, and industrial operators. 2026 activity around interoperability, including LA-RICS work integrating broadband MCPTT with P25 LMR via ESChat for Government and Blount County, Alabama Communications District using Southern Linc and a gateway to bridge existing VHF/P25 infrastructure with LTE, reflects active investment in hybrid architectures rather than isolated voice islands. In parallel, DECT-2020 NR momentum is being reinforced by the German Federal Ministry of Research, Technology and Space launching the OpenDECT-X project in May 2026 to produce a modular, interoperable reference implementation, giving vendors and integrators a practical on-ramp to open-standard full-duplex voice and device connectivity alongside Wi-Fi/IP and LTE/5G.

Recent Industry Developments

- June 2026: Clear-Com reported successful field testing of FreeSpeak Cell in a 5G network with RTL Deutschland at the Nurburgring race circuit. The validation of cellular-based intercom workflows in a demanding live production environment expands the addressable footprint beyond venue-limited RF setups and strengthens the case for LTE/5G-backed intercom deployments.

- May 2025: Motorola Solutions entered a definitive agreement to acquire Silvus Technologies for USD 4.4 billion, adding MANET capabilities used for mobile, resilient voice and data networking. The move supports intercom-adjacent deployments that need self-forming networks in complex sites where Wi-Fi or fixed infrastructure coverage is constrained.

- September 2024: Aiphone launched AiphoneCloud remote management along with a telephone-entry kit, extending its portfolio toward centrally managed deployments. Remote provisioning and troubleshooting reduce on-site service visits, making subscription-led lifecycle management more viable for multi-property residential and commercial operators.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the wireless intercoms market covers devices and system components that enable two-way voice communication without hard wiring, typically over Wi-Fi/IP, DECT, RF, Bluetooth, or cellular networks. Revenue is counted from intercom hardware sold for residential, commercial, industrial, and public safety use.

Scope exclusions: Wired-only intercom systems and unrelated access control hardware that does not provide intercom communication are excluded.

Segmentation Overview

- By Application

- Security and Surveillance

- Event Management

- Hospitality

- Transportation and Logistics

- Healthcare

- Industrial and Manufacturing

- Education

- Others

- By Technology (Connectivity)

- Wi-Fi/IP

- DECT 6.0

- Digital UHF/VHF (MURS, FRS, etc.)

- LTE/5G Cellular

- Zigbee/Bluetooth

- By End-use Sector

- Residential

- Commercial

- Enterprise/Corporate Campuses

- Government and Public Safety

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Argentina

- Brazil

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with setting the market boundary and building basic demand signals that can be tracked each year. We rely on public sources such as FCC equipment authorization databases, US Census construction spending indicators, Bureau of Labor Statistics wage and employment series for installation and security related roles, and trade and shipment statistics from UN Comtrade for relevant electronics categories.

Along with this, we review company annual reports, investor presentations, product catalogs, and reputable press to map use cases like hospitality, events, industrial sites, and public safety. Patent databases are also checked to see which wireless technologies are being adopted over time. The sources listed here are illustrative only, and many other public documents were used for collection, cross checks, and clarifying gaps.

Primary Interviews and Surveys

Primary interviews and surveys are used to pressure test adoption rates, typical replacement cycles, and pricing movement across Wi-Fi/IP, DECT, RF, and cellular based systems. We speak with manufacturers, channel partners, installers, and large end users across major regions, and the goal is to correct assumptions from desk research and then align the model to what is actually seen in orders and deployments.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 47% |

| Mid tier: 60% | Functional/Unit leaders: 34% | EMEA: 31% |

| Smaller Players: 15% | Managers: 54% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where shipment and adoption indicators are used to reconstruct the addressable installed base by end use, and then converted to annual demand using replacement and new installation rates. This total is then corroborated with selective bottom-up approximations, where sampled average selling prices are multiplied by estimated unit volumes from channel checks, and then adjusted when the two views show persistent gaps.

Key inputs in the model include construction and renovation activity, security and surveillance deployment intensity, event venue and transportation hub usage, technology mix shifts (Wi-Fi/IP versus DECT and RF), and average selling price movement by system complexity and channel type. Where unit data is patchy, gaps are handled by using proxy indicators such as installer capacity trends and import patterns, followed by a reality check with expert feedback.

Forecasts are produced using scenario analysis supported by short trend models, where drivers like construction cycles, enterprise site expansions, and wireless connectivity preference are stress tested under conservative and base cases. Assumptions on technology mix and pricing are refreshed through interviews before finalizing the forward curve.

Data Validation & Update Cycle

Outputs are checked against independent signals like import trends for relevant electronics, construction related indicators, and observed pricing bands across key regions. If the model produces sharp jumps that do not match these signals, the driver inputs are rechecked, and follow up calls are done to confirm whether a real market change happened.

Before sign-off, the work goes through multi step analyst review where calculations, conversions, and assumptions are revalidated and documented. Reports are refreshed annually, and interim updates are made when material events occur such as major regulatory changes, technology shifts, or sudden demand swings. Right before delivery, we do a fresh pass to ensure the latest public data and expert notes are reflected.

Mordor Intelligence's Wireless Intercoms Market Size Versus Other Published Estimates

Published market values for wireless intercoms can look different across sources because the included product scope, the assumed technology mix, and the timing of currency and price updates are not always aligned. Differences also show up when one estimate leans more on long range forecasts, while another stays closer to near term deployment signals.

The main gap comes from whether adjacent categories like wired intercoms and broader access control bundles are mixed into the number, along with how quickly ASP erosion or premiumization is applied across Wi-Fi/IP, DECT, RF, and cellular systems. In our case, wired-only systems are kept out and prices are refreshed by channel feedback each cycle, and this is why Mordor Intelligence reports USD 8.12 B (2026) for the wireless intercoms market while some other sources land higher or lower depending on their scope and base year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.12 B (2026) | |

| Global Consultancy A | USD 8.00 B (2026) | Uses a different base-year build where the 2026 value is projected from a 2025 starting point, and some segment splits emphasize indoor and hospitality shares, which can shift the weighting of technology mix and pricing. |

| Industry Publisher B | USD 7.99 B (2025) | Anchors on a 2025 value and applies a single growth path through the forecast, with limited clarity on pricing refresh timing and on whether bundled solutions and non-intercom security hardware are screened out consistently. |

Overall, the spread is explained by base year choice, how tightly the scope is kept to wireless intercom communication hardware, and how pricing and technology mix are updated. By keeping inputs tied to observable deployment signals and then cross checking them with interviews, the final number stays traceable and repeatable even when public data is incomplete.

Key Questions Answered in the Report

What is the current size of the wireless intercoms market?

The market reached USD 8.12 billion in 2026 and is projected to hit USD 11.76 billion by 2031.

Which application segment leads the wireless intercoms market?

Security and surveillance applications led with a 37.60% share in 2025, reflecting their role in integrated safety ecosystems.

Why are LTE/5G intercom systems gaining traction?

LTE/5G systems offer rapid, cable-free deployments and superior interference immunity, supporting an 10.72% CAGR through 2031.

Which region is expanding the fastest in wireless intercom adoption?

Asia Pacific shows the fastest 10.42% CAGR, driven by China’s indoor-coverage initiatives and India’s connectivity quality programs.

How are vendors addressing spectrum congestion challenges?

Solutions include multi-band radios, dynamic channel selection, and private 5G slices that operate in licensed bands to avoid Wi-Fi crowding.

Page last updated on: