Wi-fi 7 Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

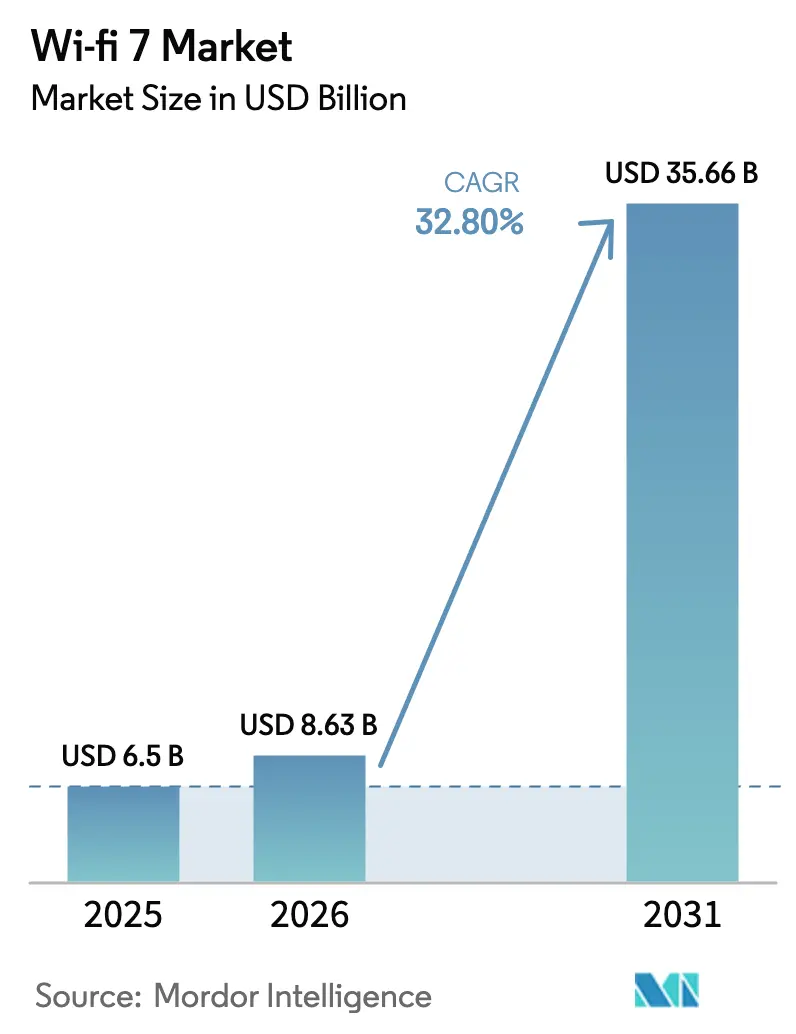

| Market Size (2026) | USD 8.63 Billion |

| Market Size (2031) | USD 35.66 Billion |

| Growth Rate (2026 - 2031) | 32.80% CAGR |

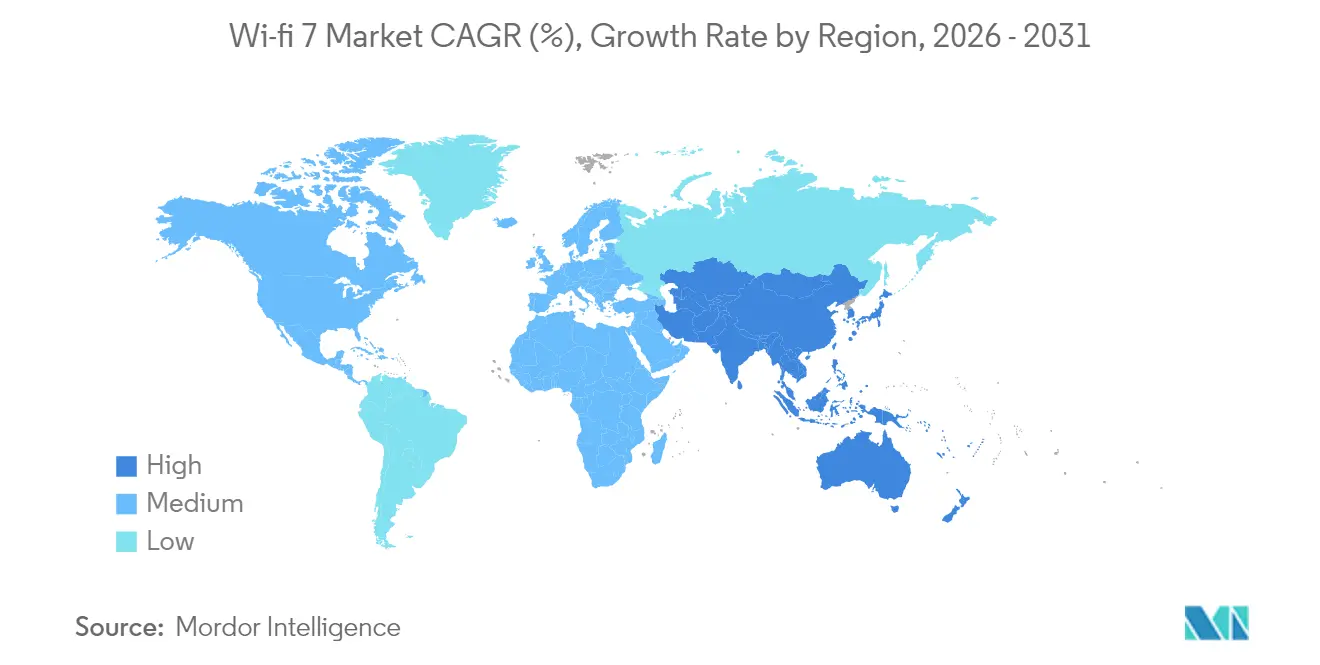

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

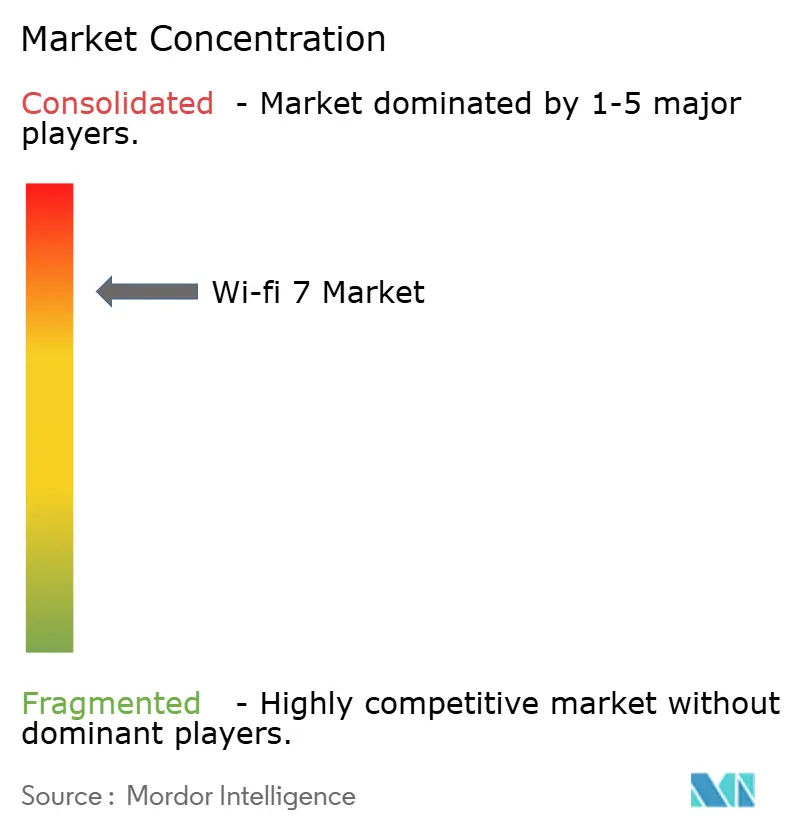

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wi-fi 7 Market Analysis by Mordor Intelligence

The Wi-Fi 7 market size was valued at USD 6.5 billion in 2025 and estimated to grow from USD 8.63 billion in 2026 to reach USD 35.66 billion by 2031, at a CAGR of 32.8% during the forecast period (2026-2031). The acceleration mirrors surging enterprise digital-transformation budgets, consumer demand for multi-gigabit connectivity, and the domino effect of 6 GHz spectrum allocations in multiple economies.[1]Wi-Fi Alliance, “Wi-Fi 7 Momentum Builds With Certification Launch,” wifi.org Chipset and gateway vendors shipped 233 million Wi-Fi 7 devices during 2024, demonstrating that mainstream adoption has already begun. The proliferation of AI-centric devices that need sustained throughput above 5 Gbps, China’s fiber-to-the-room roll-outs that shorten gateway refresh cycles to 18 months, and in-vehicle zonal architectures integrating 802.11be all reinforce the growth trajectory. Services tied to managed connectivity are scaling fastest as tier-1 ISPs monetize fiber backbones, while hardware still commands the bulk of spending thanks to access-point and gateway overhauls.

Key Report Takeaways

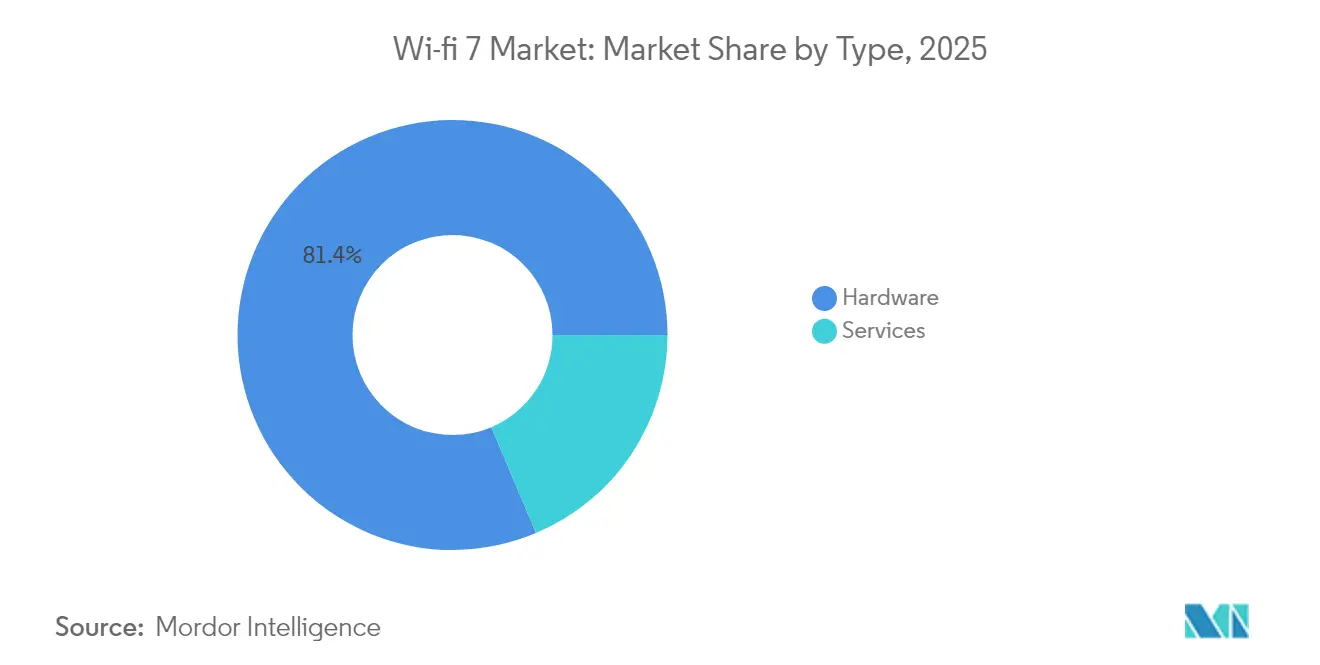

- By type, hardware held 81.35% Wi-Fi 7 market share in 2025; services are expected to expand at a 40.2% CAGR through 2031.

- By application, indoor deployments led with 66.20% revenue share in 2025 in the Wi-fi 7 market; outdoor projects are projected to grow at a 39.4% CAGR to 2031.

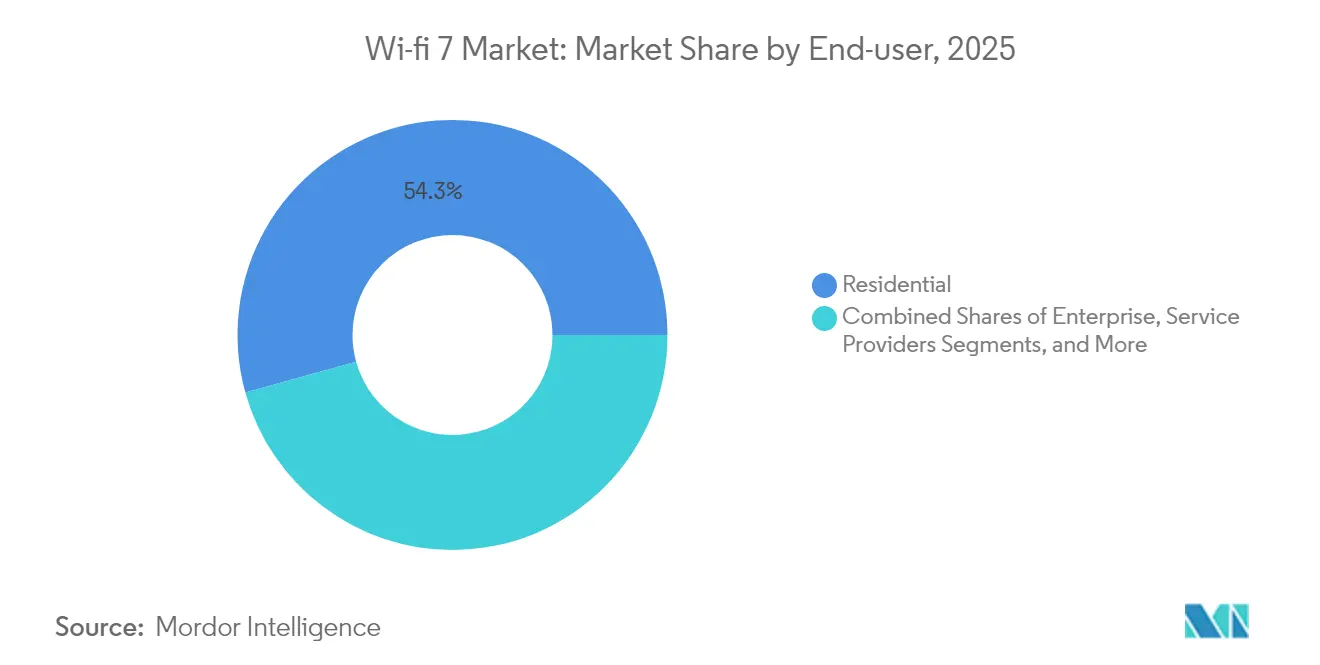

- By end user, residential accounted for 54.30% of the Wi-Fi 7 market size in 2025; industrial and manufacturing use cases are advancing at a 41.6% CAGR to 2031.

- By frequency-band configuration, dual-band captured 79.10% share of the Wi-Fi 7 market size in 2025, whereas tri-band systems are forecast to rise at a 45.5% CAGR through 2031.

- By geography, Asia-Pacific led with 40.60% revenue share in 2025 in Wi-Fi 7 market; theAsia-Pacific is the fastest-growing region with a 34.7% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wi-fi 7 Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tri-band CPE bundling by Tier-1 ISPs accelerates household upgrade cycles | + 8.5% | Global, with early gains in North America and Europe | Short term (≤ 2 years) |

| Wi-Fi Alliance "Wi-Fi CERTIFIED 7" labeling reduces enterprise-grade interoperability risk | + 6.2% | Global | Medium term (2-4 years) |

| 6 GHz spectrum release mandates in EU and Brazil open 1.2 GHz of new air-waves | + 7.8% | Europe, Latin America, spill-over to APAC | Medium term (2-4 years) |

| OEM race to ship AI-PCs and XR headsets that exceed 5 Gbps throughput ceiling | + 9.1% | Global, concentrated in North America and APAC | Long term (≥ 4 years) |

| Fiber-to-the-room (FTTR) roll-outs in China driving gateway refresh every below 18 months | + 5.4% | China, with expansion to broader APAC region | Short term (≤ 2 years) |

| Automotive zonal-architecture adoption of 802.11be for in-cabin streaming | + 3.2% | Global, led by premium automotive markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tri-band CPE Bundling by Tier-1 ISPs Accelerates Household Upgrade Cycles

Tri-band CPE bundling by tier-1 ISPs accelerates household upgrade cycles. Service providers such as Charter Communications began shipping Advanced Wi-Fi 7 routers in late 2024, bypassing the usual four-year consumer replacement cadence and ensuring that expensive fiber lines deliver full in-home speeds. Lumen Technologies followed with an internally designed Wi-Fi 7 gateway, proving how operator subsidies can erase upfront hardware costs for subscribers. The strategy locks customers into premium broadband tiers, widens average revenue per user, and seeds millions of tri-band endpoints that lift the entire Wi-Fi 7 market.

Wi-Fi Alliance “Wi-Fi CERTIFIED 7” Labeling Lowers Enterprise Interoperability Risk

Wi-Fi Alliance “Wi-Fi CERTIFIED 7” labeling reduces enterprise interoperability risk. The January 2024 certification launch ended buyer hesitation by validating 320 MHz channels, Multi-Link Operation, and 4K QAM features in a vendor-neutral process. Cisco’s intelligent access points released in December 2024 are built around the program, adding AI-driven self-configuration that slashes deployment times.[2]Cisco Systems, “Cisco Catalyst Wi-Fi 7 Access Points Data Sheet,” cisco.com Large organizations now treat Wi-Fi 7 gear as standards-compliant, enabling multi-site purchases that were on hold for ratification.

6 GHz Spectrum Release Mandates In The EU and Brazil Open 1.2 GHz of New Airwaves

6 GHz spectrum release mandates in the EU and Brazil open 1.2 GHz of new airwaves. Brussels harmonized the 5,945–6,425 MHz band for unlicensed use, effectively tripling the spectrum available versus legacy 2.4 GHz and 5 GHz allocations. Brazil mirrored the decision, allowing equipment makers to build global SKUs, while Ofcom’s draft UK rules prioritize unlicensed indoor Wi-Fi, further lowering certification hurdles. Together, these moves make 320 MHz channels commercially viable and sustain the Wi-Fi 7 market momentum.

OEMs Race to Ship AI-PCs and XR Headsets That Exceed 5 GBPS Throughput

OEMs race to ship AI-PCs and XR headsets that exceed the 5 Gbps throughput ceiling. Qualcomm’s FastConnect 7900 integrates AI optimization to keep latency below 2 ms during multi-link operation, a must for cloud-assisted XR workloads.[3]Qualcomm, “FastConnect 7900 Fact Sheet,” qualcomm.com Apple’s in-house Wi-Fi 7 silicon for iPhone 17 underlines how crucial radio performance is for on-device AI and immersive apps. As vendors link premium user experience to multi-gigabit wireless, design wins for Wi-Fi 7 chipsets spike across handsets, laptops, and wearables, expanding the addressable Wi-Fi 7 market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High incremental BoM cost vs. Wi-Fi 6E in entry-level smartphones | - 4.3% | Global, particularly APAC manufacturing hubs | Short term (≤ 2 years) |

| AFC‐related certification delay for outdoor APs in US and EMEA | - 3.7% | North America and Europe | Medium term (2-4 years) |

| Power-consumption penalty (above 30%) in battery-constrained IoT sensors | - 2.8% | Global, concentrated in Industrial IoT deployments | Long term (≥ 4 years) |

| Channel-occupancy compliance risk in unlicensed 6 GHz in India and Russia | - 1.9% | India, Russia, and similar regulatory environments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Incremental BoM Versus Wi-Fi 6E in Entry-Level Smartphones

High incremental BoM cost versus Wi-Fi 6E in entry-level smartphones. Support for 320 MHz channels and 4,096-QAM requires advanced RF front-end designs; vendors such as Qorvo supply multi-antenna modules that raise handset costs by 15-25%, which budget-phone makers cannot absorb.[4]Qorvo, “Tri-Band Wi-Fi 7 Front-End Module Portfolio,” qorvo.com The gap confines early Wi-Fi 7 adoption to flagship models until component prices fall, delaying volume scale in the mass market.

AFC-related Certification Delay for Outdoor APs in the US and EMEA

AFC-related certification delay for outdoor APs in the US and EMEA. Although the FCC approved standard-power operations in February 2024, real-time coordination with incumbent microwave users adds months of lab testing and system integration. Enterprises planning stadium or campus-wide coverage must wait for cleared automated-frequency-coordination databases, pushing revenue recognition for outdoor Wi-Fi 7 projects into future fiscal cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hardware Dominance Drives Infrastructure Refresh

The hardware segment generated 81.35% of overall revenue in 2025, underscoring the capital intensity linked to new RF architectures that cannot be retrofitted. Access points, gateways, and chipsets account for the bulk of this spending, while software analytics and managed services sit on top of the installed base and are growing at a 40.2% CAGR. The Wi-Fi 7 market size for hardware is projected to stretch from USD 5.29 billion in 2025 to USD 29.02 billion in 2031, validating supplier focus on silicon, antennas, and front-end modules. Services still represent the fastest-climbing slice of the Wi-Fi 7 industry as ISPs bundle cloud portals, device-as-a-service plans, and automated optimization tools.

Access points remain the largest hardware sub-segment thanks to enterprise refresh cycles and high-density venues that demand tri-radio designs. Gateways follow closely, propelled by tri-band CPE subsidies. Chipsets set the pace for innovation: Broadcom’s BCM 6765 and MediaTek’s Filogic platforms exemplify purpose-built silicon tuned to specific deployment environments.

By Application: Indoor Deployments Lead Market Penetration

Indoor use cases captured 66.20% of 2025 revenue as offices, universities, and high-rise apartments needed multi-gigabit coverage without recabling. This segment leads because Wi-Fi 7 features, such as Multi-Link Operation, excel at mitigating interference in dense device clusters. Outdoor applications, including stadiums, municipal Wi-Fi, and smart-city corridors, trail in absolute value but are forecast to grow at 39.4% CAGR through 2031.

Extreme Networks showcased Wi-Fi 7 tri-radio APs at the Zwarte Cross 2024 festival, delivering consistent bandwidth to tens of thousands of concurrent users. Such proof points validate outdoor performance, setting the stage for service-provider offload and city-wide backhaul upgrades. As regulatory AFC hurdles clear, outdoor roll-outs will underpin incremental revenue streams for the Wi-Fi 7 market.

By End User: Residential Base Supports Enterprise Innovation

Residential deployments held a 54.30% share of 2025 revenue, illustrating how ISP-bundled gateways create large installed bases quickly. Industrial and manufacturing plants, however, log the highest growth at 41.6% CAGR via wireless time-sensitive-networking that needs deterministic latency. Enterprises sit in the middle: their budgets fund advanced features first, which then trickle down to consumer hardware once cost curves improve.

Healthcare environments offer a specialized sub-segment where real-time telemetry and mixed-reality surgery training depend on consistent gigabit throughputs. These demanding scenarios highlight the upside for Wi-Fi 7 vendors that can optimize power efficiency while meeting regulatory compliance.

By Frequency Band Configuration: Tri-Band Architecture Drives Performance

Dual-band gear still dominates shipments with 79.10% revenue share in 2025 because enterprises can layer Wi-Fi 7 efficiency gains onto existing 2.4 GHz and 5 GHz footprints without coordinating 6 GHz channels. Tri-band configurations, however, outpace all other categories at a 45.5% CAGR since they unlock 320 MHz channels to hit double-digit gigabit peaks. Intel notes that more than 1 200 device models already support Wi-Fi 7 across three bands, a number that doubled in under 12 months.

MaxLinear’s single-chip tri-band solution reaches 11.5 Gbps on the 6 GHz lane, demonstrating the head-room needed for AI edge workloads and immersive media. High-density enterprises and event venues increasingly specify tri-band designs in bid documents, a trend that will redistribute revenue toward higher-value SKUs within the overall Wi-Fi 7 market.

Geography Analysis

Asia-Pacific commanded 40.60% of 2025 revenue as Chinese operators turned fiber-to-the-room into a de-facto baseline. China Telecom alone grew to 193 million broadband lines with 27.3% gigabit penetration, which forces a nation-wide gateway upgrade cadence far shorter than Western norms. Supply-chain proximity aids quick iterations, allowing vendors to push successive Wi-Fi 7 reference designs into contract manufacturers within months.

North America remains a premium early adopter region. The FCC’s approval of standard-power operation above 5,945 MHz unlocks outdoor deployments, even though the AFC database still imposes friction on. Service providers such as Charter and Lumen position tri-band gateways as a differentiator in crowded gigabit tiers. Enterprise refresh cycles pick up as Cisco, HPE Aruba, and CommScope ship certified gear.

Europe approaches adoption through regulatory cohesion. The European Commission harmonized the lower 6 GHz band in 2024, allowing ISPs and enterprises to roll out 6 GHz channels across national borders without re-certification. Vodafone UK completed Wi-Fi 7 router testing in 2024, flagging a 2025 commercial debut.

The Middle East shows a signficjant growth through 2031. Governments bundle Wi-Fi 7 into smart-city tenders that feature AI video surveillance, connected transit, and immersive tourist experiences. A public demonstration in Dubai logged 3.7 Gbps downlink on pre-production equipment, underscoring favorable propagation in open urban layouts. South America benefits from Brazil’s proactive spectrum release, while African markets wait for regional regulators to echo ITU guidelines.

Competitive Landscape

The chipset layer is moderately concentrated. Broadcom, Qualcomm, MediaTek, and Intel together control a majority of design wins, leveraging decades of intellectual property, foundry contracts, and software stacks. Broadcom’s second-generation portfolio targets residential gateways and enterprise APs. Qualcomm integrates AI processing in FastConnect 7900, chasing mobile and XR form factors. MediaTek compresses bill-of-materials costs for mass-market Android devices, whereas Intel prioritizes PC and enterprise certifications. Apple’s internal silicon project for Wi-Fi 7 radios in iPhone 17 signals deeper vertical integration that could shift bargaining power away from merchant suppliers.

Equipment vendors differentiate on cloud orchestration, AI assurance, and vertical expertise. Cisco’s intelligent APs adjust channel plans autonomously and bundle zero-trust security. Extreme Networks positions tri-radio hardware at sports arenas, while Arista Networks extends deterministic scheduling into campus fabrics. Start-ups such as Synaptics target IoT nodes with purpose-built low-power Wi-Fi 7 chipsets.

Patent filings on Multi-Link Operation, target-wake-time algorithms, and spectral masks suggest sustained R&D races. Meta and Microsoft both lodged claims that adapt Wi-Fi 7 for AR/VR, hinting that horizontal players could cross over into silicon design, further intensifying rivalry. The Wi-Fi 7 market thus rewards ecosystem control as much as raw radio performance

Wi-fi 7 Industry Leaders

Intel Corporation

Broadcom Inc.

Cisco Systems Inc.

MediaTek Inc.

Qualcomm Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Broadcom disclosed Q2 earnings of USD 15 billion, a 20% jump attributed partly to Wi-Fi 7 silicon sales.

- April 2025: Furuno Systems unveiled the ACERA EW750 access point targeting 9 335 Mbps peak throughput and 30 000 unit annual shipments.

- March 2025: Arista Networks introduced Wi-Fi 7 series APs with 4×4 MIMO across three bands for stadium-grade density.

- February 2025: Qualcomm posted Q1 revenue of USD 11.67 billion, up 18%, citing premium-handset demand for Wi-Fi 7 radios.

Global Wi-fi 7 Market Report Scope

Wi-Fi, short for wireless fidelity, is a wireless technology that connects devices to the internet or local networks via radio waves. It enables wireless communication for various devices in homes, businesses, and public spaces.

The global Wi-Fi 7 market is segmented by type (hardware and service), by application (indoor and outdoor), and by region (North America, Europe, Asia-Pacific, Latin America and Middle East and Africa).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware | Access Points |

| Gateways | |

| Routers and Extenders | |

| Chipsets / Modules | |

| Services |

| Indoor |

| Outdoor |

| Residential |

| Enterprise |

| Industrial and Manufacturing |

| Service Providers / Smart-City |

| Dual-band (2.4/5 GHz) |

| Tri-band (2.4/5/6 GHz) |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Type | Hardware | Access Points |

| Gateways | ||

| Routers and Extenders | ||

| Chipsets / Modules | ||

| Services | ||

| By Application | Indoor | |

| Outdoor | ||

| By End User | Residential | |

| Enterprise | ||

| Industrial and Manufacturing | ||

| Service Providers / Smart-City | ||

| By Frequency Band Configuration | Dual-band (2.4/5 GHz) | |

| Tri-band (2.4/5/6 GHz) | ||

| By Geography | North America | |

| South America | ||

| Europe | ||

| Asia-Pacific | ||

| Middle East and Africa |

Key Questions Answered in the Report

What is the projected value of the Wi-Fi 7 market by 2031?

The Wi-Fi 7 market is expected to reach USD 35.66 billion by 2031 on a 32.8% CAGR trajectory.

Which region leads current Wi-Fi 7 spending?

Asia-Pacific leads with 40.60% revenue share thanks to large-scale fiber-to-the-room gateway upgrades in China.

Why are ISPs bundling tri-band Wi-Fi 7 routers?

Bundling guarantees subscribers experience multi-gigabit speeds across the home, supporting higher-priced broadband tiers while seeding the equipment base for the Wi-Fi 7 market.

What hampers roll-out of outdoor Wi-Fi 7 access points?

Automated-frequency-coordination approval processes in the 6 GHz band add months to certification, delaying deployments in stadiums and smart cities.

How fast are industrial and manufacturing Wi-Fi 7 deployments growing?

Industrial and manufacturing applications are forecast to expand at a 41.6% CAGR between 2026 and 2031, driven by wireless time-sensitive-networking requirements.

Which configuration is growing faster, dual-band or tri-band?

Tri-band Wi-Fi 7 equipment is advancing at a 45.5% CAGR because only three-band radios unlock 320 MHz channels and peak throughput above 10 Gbps.

Page last updated on: