Wi-Fi 6 Router Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.25 Billion |

| Market Size (2031) | USD 11.74 Billion |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

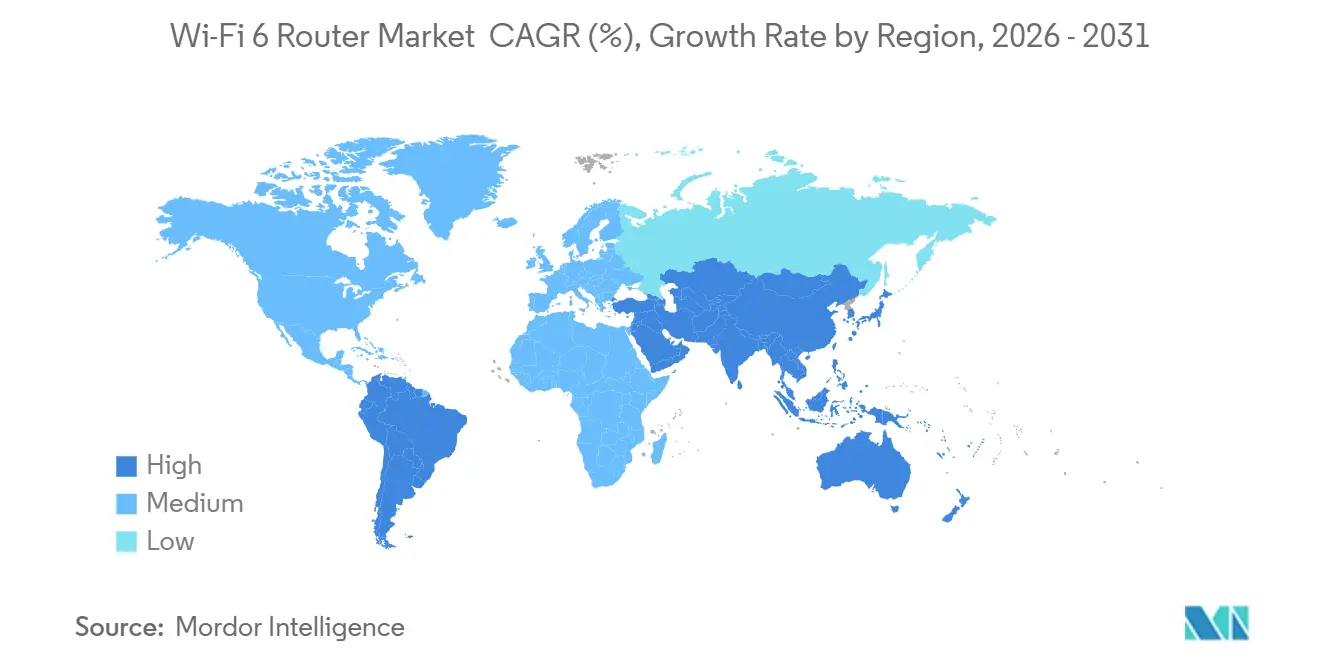

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

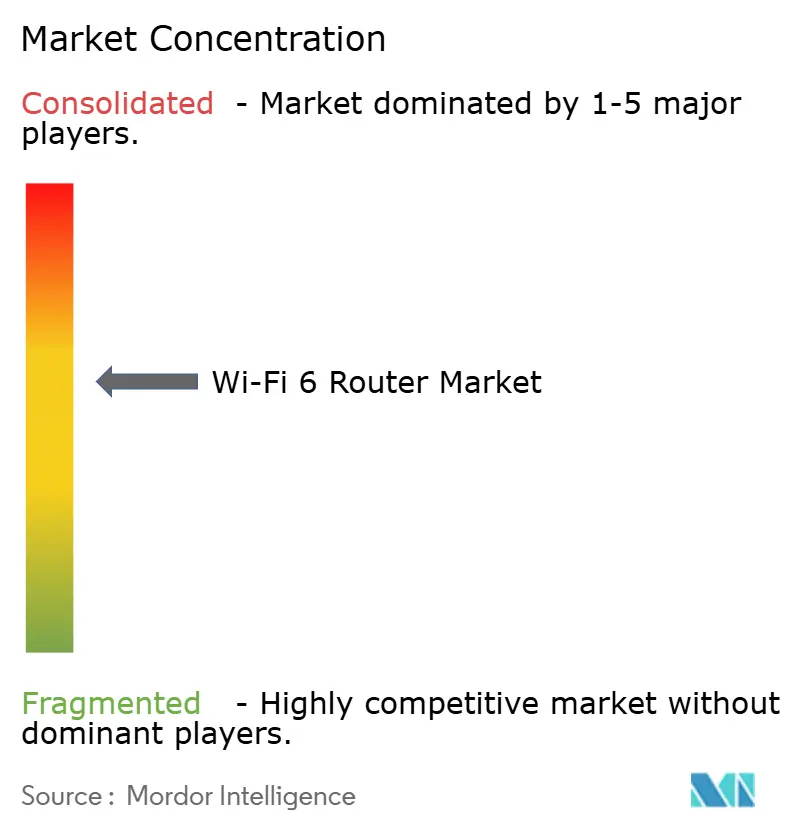

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wi-Fi 6 Router Market Analysis by Mordor Intelligence

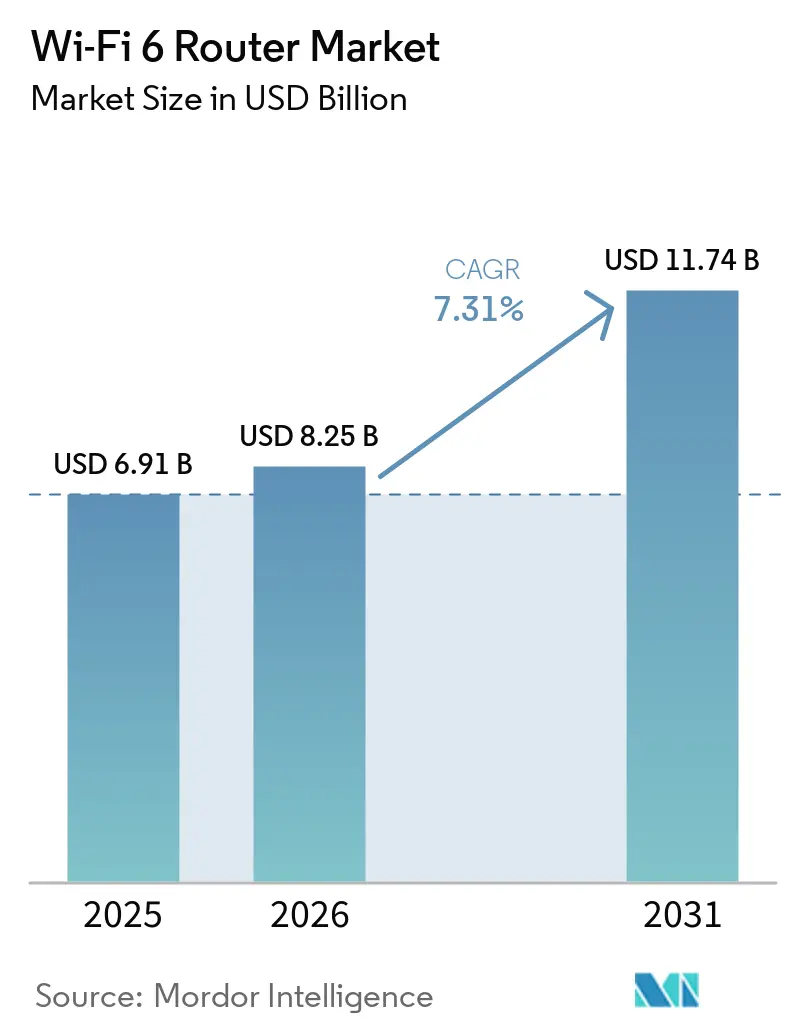

The Wi-Fi 6 router market size was valued at USD 6.91 billion in 2025 and is estimated to grow from USD 8.25 billion in 2026 to reach USD 11.74 billion by 2031, at a CAGR of 7.31% during the forecast period (2026-2031). Growing recognition of gateways as long-term broadband infrastructure, brisk regulatory alignment around the 6 GHz band, and expanding gigabit fiber coverage are reshaping vendor roadmaps and purchase triggers. Internet service providers now bundle tri-band routers into subscription plans, effectively decoupling household upgrade cycles from personal spending decisions. Equipment makers are converging global stock-keeping units after the United States, United Kingdom, and India all cleared indoor 6 GHz use, slashing certification costs and compressing time-to-market. Meanwhile, mesh backhaul performance is a headline differentiator as smart-home IoT nodes climb past 18 devices per U.S. household.

Key Report Takeaways

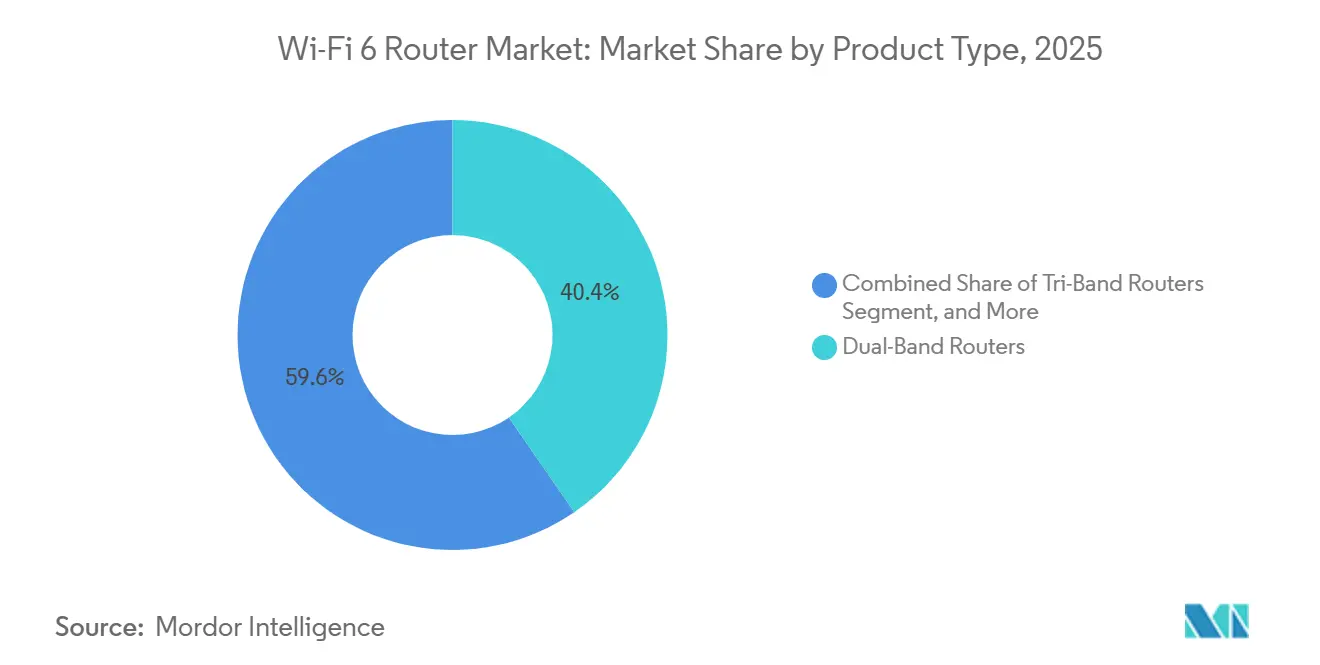

- By product type, dual-band devices led with 40.43% of the Wi-Fi 6 router market share in 2025, while tri-band units are projected to grow at a 9.62% CAGR to 2031.

- By frequency band, the 5 GHz segment accounted for 47.32% share of the Wi-Fi 6 router market size in 2025, yet 6 GHz shipments are advancing at 9.83% CAGR through 2031

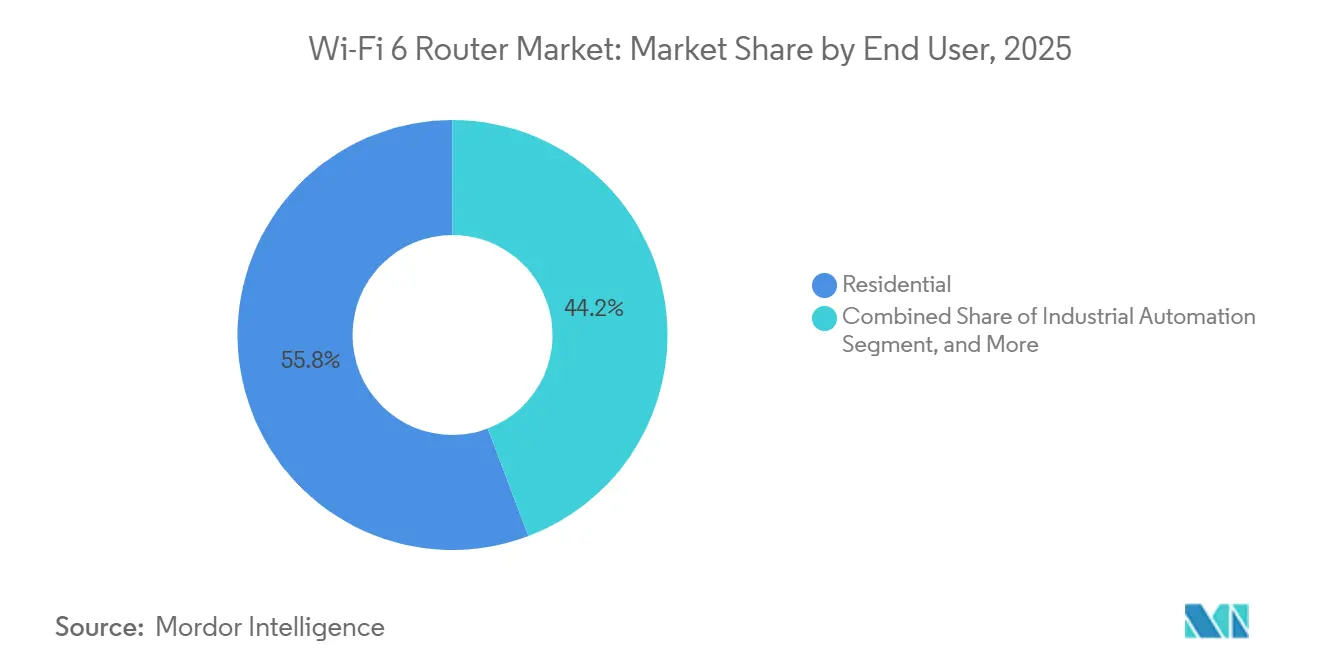

- By end user, residential deployments accounted for 56.31% of revenue share in 2025; industrial installations are expanding at an 8.93% CAGR between 2026 and 2031.

- By distribution channel, online stores captured 52.23% of 2025 revenue and are poised for an 11.42% CAGR through 2031.

- By geography, North America dominated with a 35.43% revenue share in 2025, whereas Asia-Pacific recorded the fastest growth at a 12.43% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wi-Fi 6 Router Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Broadband Upgrades to Gigabit-Class Services | +1.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Mandatory Transition of ISPs to Wi-Fi 6 Gateways After 2025 Spectrum Re-allocation | +1.5% | North America, Europe, Asia-Pacific | Short term (= 2 years) |

| Explosive Growth of Smart-Home IoT Node Density | +1.3% | Global, led by North America and Asia-Pacific | Long term (= 4 years) |

| Government-Backed Rural Fiber Roll-outs in South America and Africa | +1.1% | South America and Africa | Long term (= 4 years) |

| Enterprise Network Refresh Cycles Driven by Hybrid Work Policies | +0.9% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Regulatory Approvals for 6 GHz Band Unleashing Wi-Fi 6E Capacity | +0.7% | Global | Short term (= 2 years) |

| Source: Mordor Intelligence | |||

Surging Broadband Upgrades To Gigabit-Class Service

Fiber penetration reached 89.58% of United Kingdom premises in 2025, according to Ofcom, accelerating operator-led replacement of legacy VDSL gateways that constrain throughput below gigabit levels. Charter Communications reinforced this shift by deploying multi-gigabit gateways to 1.2 million United States subscribers in late 2024, indicating cable incumbents are pre-empting fiber competition with next-generation Wi-Fi hardware.[1]Charter Communications, “Charter Deploys Wi-Fi 7 Gateways to 1.2 Million Subscribers,” charter.com Bundled lease pricing embeds router upgrades within service fees, eliminating upfront costs and compressing replacement cycles. Concurrently, vendors delivering integrated DOCSIS and Wi-Fi platforms lock in multi-year supply contracts, improving demand visibility. As symmetrical gigabit plans expand across Europe and East Asia, the Wi-Fi 6 router market gains sustained volume momentum and pricing resilience.

Mandatory Transition Of ISPs To Wi-Fi 6 Gateways After 2025 Spectrum Re-allocation

The January 2026 decision by the Federal Communications Commission to release the full 1,200 MHz of 6 GHz spectrum forces operators to phase out Wi-Fi 5 hardware that cannot utilize these channels. In parallel, the European Telecommunications Standards Institute aligned lower-band rules, enabling vendors to standardize tri-band platforms across major EU markets. Operators are absorbing near-term write-offs on legacy inventory in 2026 financials but expect higher ARPU from premium speed tiers supported by 6 GHz backhaul. Similar regulatory actions in India and South Korea are compressing product-development cycles to 12-18 months, accelerating revenue conversion for chipset vendors.

Explosive Growth Of Smart-Home IoT Node Density

United States households averaged 18 connected devices in 2025, according to Cisco Systems, a density that saturates legacy 2.4 GHz channels and exposes quality-of-service constraints in older routers. Wi-Fi 6 addresses this through orthogonal frequency-division multiple access, allocating deterministic airtime to each device and improving performance for low-power endpoints such as doorbells and thermostats, as well as high-bandwidth streaming nodes. Global IoT installations reached 21.1 billion units in 2025, with 35% in residential settings, shifting demand drivers toward device density rather than pure broadband penetration.[2] Cisco Systems, “State of Wireless Report 2026,” cisco.com Industrial environments share similar requirements, where sub-10 millisecond latency is critical for coordinating autonomous mobile robots in mixed human-machine operations, reinforcing enterprise-grade adoption.

Government-Backed Rural Fiber Roll-outs In South America And Africa

Brazil’s universal service fund, administered by ANATEL, committed BRL 3.2 billion (USD 640 million) in 2025 to connect 770,000 households and 17,000 schools, triggering demand for mesh-capable routers suited to dispersed premises. Nigeria is advancing a comparable model through Project BRIDGE, supported by the African Development Bank. In parallel, South Africa approved an USD 8.2 billion broadband plan extending to 2035 via the Development Bank of Southern Africa. Given rural layouts with multiple detached structures, vendors gain share by offering outdoor-rated nodes, extended-range 2.4 GHz fallback, and bundled tri-band mesh systems optimized for wide-area coverage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Pricing of Wi-Fi 6E Tri-Band Models Above USD 400 | -0.6% | Global, acute in Asia-Pacific and South America | Medium term (2-4 years) |

| Fragmented 6 GHz Rules Forcing Multi-SKU Compliance Costs | -0.5% | Europe, Asia-Pacific, Middle East | Short term (≤ 2 years) |

| Semiconductor Lead-Times Exceeding 30 Weeks for Key Chipsets | -0.4% | Global | Short term (≤ 2 years) |

| Limited Consumer Awareness of Standard Benefits Slowing Adoption | -0.3% | Emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Of Wi-Fi 6E Tri-Band Models Above USD 400

NETGEAR’s Orbi 870 three-pack launched at USD 1,499.99, highlighting a substantial price delta versus sub-USD 200 dual-band systems, while TP-Link positions mid-tier tri-band units around USD 333.99, a threshold typically justified only when broadband speeds exceed 500 Mbps.[3] NETGEAR Inc., “NETGEAR Launches Orbi 870 Mesh System,” netgear.com The elevated bill of materials reflects an additional RF chain, larger thermal assemblies, and more complex band-steering firmware spanning 2.4, 5, and 6 GHz. Although ongoing chipset integration is expected to compress entry-level tri-band pricing below USD 250 by late 2027, the current premium suppresses unit volumes in price-sensitive markets, particularly across emerging economies.

Fragmented 6 GHz Rules Forcing Multi-SKU Compliance Costs

Transmit-power limits vary materially across jurisdictions, creating engineering and commercial friction. The Federal Communications Commission permits up to 30 dBm indoors in portions of the 6 GHz band, whereas the Ofcom enforces caps near 24 dBm, and South Korea restricts very-low-power devices to about 14 dBm. This divergence forces vendors to maintain region-specific firmware, labeling, and certification workflows, increasing launch costs by roughly 8% to 10%. For multinational enterprises, channel availability can contract from seven 160 MHz channels in one market to effectively 80 MHz operation in another, producing throughput asymmetry, complicating standardized network designs, and deferring near-term procurement decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Enterprises Steer Toward Tri-Band Platforms

Tri-band hardware is projected to expand at a 9.62% CAGR through 2031, driven by enterprise willingness to pay for dedicated 6 GHz backhaul that segregates mesh traffic from client streams and improves throughput determinism. Cisco Systems referenced campus-refresh momentum in its FY 2026 earnings, linking demand to hybrid work environments that require seamless roaming and stable video quality.[4]Cisco Systems, “State of Wireless Report 2026,” cisco.com Despite this, dual-band units retained 40.43% share in 2025 as residential buyers prioritized coverage and delayed 6 GHz adoption until gigabit fiber availability improved. Quad-band devices remain niche, largely confined to gaming use cases with limited ecosystem support.

Vendors are advancing early Wi-Fi 8 development, with ASUSTeK Computer Inc. introducing a prototype router aligned with draft IEEE 802.11bn specifications and peak speeds approaching 30 Gbps. Regional preferences remain differentiated: North American households favor integrated units bundled with subscription-based security, while European consumers opt for modular systems that separate routing and wireless functions to address structural interference constraints. Certification by the Wi-Fi Alliance for automatic frequency coordination strengthens buyer confidence by ensuring coexistence within the 6 GHz band, supporting sustained uptake of tri-band architectures.

By Frequency Band: 6 GHz Anchors Next-Generation Throughput

The 6 GHz segment is expanding at a 9.83% CAGR through 2031, outpacing the 5 GHz band, which held a 47.32% share in 2025. The Federal Communications Commission enabled this shift by opening a contiguous 1,200 MHz block from 5.925 to 6.875 GHz, creating seven interference-free 160 MHz channels capable of sustaining multi-gigabit throughput. The Department of Telecommunications reinforced global-scale economics by delicensing 500 MHz in December 2024, allowing vendors to standardize designs across key markets. Automated frequency coordination frameworks further extend 6 GHz usability to outdoor environments, including logistics yards and enterprise campuses, without disrupting incumbent microwave systems.

The Wi-Fi 6 router market still depends on 2.4 GHz for low-power, long-range IoT applications, although its throughput ceiling of 600 Mbps limits high-bandwidth use cases. The 5 GHz band remains the practical midpoint in dense residential settings, balancing capacity and wall penetration, despite interruptions from dynamic frequency selection triggered by radar detection. In contrast, 6 GHz is increasingly reserved for latency-sensitive enterprise and industrial workloads, where jitter must remain below 3 milliseconds to support deterministic networking. This segmentation highlights a clear functional stratification, with each band optimized for distinct performance and deployment requirements.

By End User: Industrial Automation Drives Low-Latency Requirements

Residential buyers accounted for 56.31% of 2025 revenue, but industrial demand is scaling as factories migrate programmable logic controllers to wireless architectures, driving an 8.93% CAGR through 2031. Huawei Technologies demonstrated feasibility at its Songshan Lake campus by connecting 10,000 endpoints over Wi-Fi 6 with 99.99% uptime, validating wireless as a substitute for Ethernet in controlled environments. Similarly, SEW-Eurodrive deployed sub-10 millisecond links for autonomous mobile robots, confirming latency thresholds required for industrial automation. Enterprises standardize on WPA3-Enterprise with RADIUS authentication, while residential users lag on segmentation, prompting vendors to embed simplified guest-network controls.

Commercial segments such as hospitality and retail operate defined refresh cycles of approximately 5 years to retain vendor support and security compliance, creating predictable replacement demand. Hybrid work models are expanding campus footprints and increasing reliance on seamless roaming, which drives procurement of access points capable of low-loss handoffs across dense node environments. These structural shifts elevate enterprise and industrial segments as durable growth contributors, partially offsetting the slower upgrade cadence and price sensitivity observed in the residential base.

By Distribution Channel: E-Commerce Consolidates Direct-To-Consumer Momentum

Online channels accounted for 52.23% of 2025 sales and are projected to grow at an 11.42% CAGR through 2031, the fastest among distribution modes. Algorithmic pricing on marketplaces compresses margins but accelerates inventory turnover, reducing exposure to chipset obsolescence within 12-18 month product cycles. TP-Link’s January 2026 VoIP bundle with Freshtel illustrates a shift toward embedding routers within subscription-led offerings, converting transactional hardware sales into recurring revenue streams. Enterprise procurement remains relationship-driven, emphasizing negotiated pricing and integration with centralized network management platforms, while offline retail persists in markets where buyers require physical demonstrations before committing to higher-cost tri-band systems.

Return-policy asymmetry further shifts demand online, as consumers can trial devices for 30 days with minimal friction and reverse purchases without penalty. In contrast, physical retailers often impose restocking fees, discouraging experimentation with premium hardware. As broadband literacy and digital purchasing confidence increase, this structural convenience advantage is expected to widen. The implication is clear: vendors must prioritize digital merchandising, dynamic pricing strategies, and fulfillment efficiency to capture share, while selectively maintaining offline presence for high-touch, high-value product education.

Geography Analysis

North America generated 35.43% of global revenue in 2025, supported by cable operators that lease gateways to defend against fiber overbuild competition. This model shifts entry into the Wi-Fi 6 router market from retail to carrier provisioning, sustaining higher average selling prices and faster upgrade cycles. Charter Communications and Comcast Corporation exemplify this approach by bundling advanced gateways within service plans, including early Wi-Fi 7 deployments to retain high-value subscribers. The region also benefits from higher broadband penetration and willingness to pay for performance tiers, reinforcing premium segment growth and accelerating adoption of next-generation standards ahead of global peers.

Asia-Pacific is expected to record the fastest CAGR of 12.43% between 2026 and 2031, driven by regulatory alignment and cost-efficient manufacturing ecosystems. The Department of Telecommunications enabled 6 GHz delicensing, aligned spectrum policy with the United States and Europe, and reduced compliance complexity for vendors. Chinese manufacturers, particularly those based in Shenzhen, dominate sub-USD 50 dual-band exports, while suppliers in Taiwan and South Korea focus on higher-margin tri-band systems. Concurrently, government-backed fiber rollouts in Indonesia and Vietnam expand broadband access, increasing router volumes even as price sensitivity moderates per-unit revenue growth.

South America and Africa represent emerging growth corridors, where public funding is translating connectivity ambitions into tangible infrastructure deployment. ANATEL is channeling BRL 3.2 billion (USD 640 million) into rural connectivity, while initiatives such as Nigeria’s Project BRIDGE, supported by the African Development Bank, and South Africa’s broadband expansion led by the Development Bank of Southern Africa are scaling last-mile access. Although absolute revenues remain lower than mature markets, sustained double-digit shipment growth is prompting vendors to pprioritize ruggedized, temperature-resilient designs suited to diverse environmental conditions.

Competitive Landscape

The Wi-Fi 6 router market exhibits mid-level concentration, with the top five suppliers holding under 50% combined share, favoring rapid feature iteration over pure scale advantages. TP-Link leverages China-based contract manufacturing to dominate sub-USD 50 dual-band segments across Asia-Pacific, Africa, and Latin America. NETGEAR focuses on premium tri-band mesh systems bundled with cybersecurity subscriptions, targeting prosumer and small-office demand above USD 400. ASUSTeK Computer Inc. differentiates via gaming-optimized firmware and ecosystem integration, extracting higher willingness to pay from latency-sensitive users.

Huawei Technologies retains strong enterprise positioning in Asia-Pacific and the Middle East, offering bundled campus solutions that integrate routing, switching, and cloud management under unified service-level agreements. Ubiquiti Inc. targets wireless ISPs with ruggedized, integrated-antenna systems suited for outdoor deployments, while Xiaomi Corporation competes aggressively on pricing through vertically integrated Wi-Fi 7 products positioned roughly 30% below peers. Upstream, chipset suppliers such as Broadcom Inc., Qualcomm, and MediaTek shape cost structures via licensing and integration frameworks.

White-space opportunities remain in industrial and infrastructure-led deployments, including agriculture, mining, and smart-city lighting, where demand for ingress-protected and temperature-resilient routers is underserved. Vendors that adapt existing tri-band reference architectures to meet industrial-grade specifications can capture incremental margins while diversifying revenue away from saturated residential segments. The strategic implication is clear: moving up the value chain through ruggedization, vertical-specific firmware, and managed-service layers offers a path to differentiation beyond price-led competition, particularly as core consumer markets approach maturity and margin compression intensifies.

Wi-Fi 6 Router Industry Leaders

TP-Link Technologies Co., Ltd.

NETGEAR, Inc.

ASUSTeK Computer Inc.

D-Link Corporation

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: South Africa Development Bank announced an USD 8.2 billion broadband plan running to 2035, creating long-term demand for mesh-capable gigabit routers.

- March 2026: Xiaomi launched the BE19000 Pro Wi-Fi 7 router with 320 MHz channels, priced 30% below incumbents to accelerate share gains in Asia-Pacific.

- March 2026: D-Link released Wi-Fi 7 routers aimed at small-office and prosumer segments, signaling a leap over Wi-Fi 6E.

- January 2026: ASUSTeK unveiled the ROG Wi-Fi 8 router at CES, supporting the draft IEEE 802.11bn standard 18 months ahead of ratification.

Global Wi-Fi 6 Router Market Report Scope

The Wi-Fi 6 router market comprises the global ecosystem of hardware, software, and associated services that enable wireless local area network (WLAN) connectivity using the IEEE 802.11ax standard. These routers operate across 2.4 GHz, 5 GHz, and, in extended variants (Wi-Fi 6E), the 6 GHz spectrum, delivering higher throughput, lower latency, and improved spectral efficiency through technologies such as orthogonal frequency-division multiple access (OFDMA), multi-user multiple-input multiple-output (MU-MIMO), and target wake time. The market includes standalone routers, mesh systems, and carrier-supplied gateways deployed across residential, commercial, and industrial environments.

The Wi-Fi 6 Router Market Report is Segmented by Product Type (Dual-Band Routers, Tri-Band Routers, and Quad-Band Routers), Frequency Band (2.4 GHz, 5 GHz, and 6 GHz), End User (Residential, Commercial, and Industrial), Distribution Channel (Online Stores, Offline Retail, and Direct Enterprise Procurement), and Geography (North America, South America, Europe, Asia-Pacific Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Dual-Band Routers |

| Tri-Band Routers |

| Quad-Band Routers |

| 2.4 GHz |

| 5 GHz |

| 6 GHz (Wi-Fi 6E) |

| Residential |

| Commercial |

| Industrial |

| Online Stores |

| Offline Retail |

| Direct Enterprise Procurement |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Dual-Band Routers | |

| Tri-Band Routers | ||

| Quad-Band Routers | ||

| By Frequency Band | 2.4 GHz | |

| 5 GHz | ||

| 6 GHz (Wi-Fi 6E) | ||

| By End User | Residential | |

| Commercial | ||

| Industrial | ||

| By Distribution Channel | Online Stores | |

| Offline Retail | ||

| Direct Enterprise Procurement | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Wi-Fi 6 router market in 2026?

The Wi-Fi 6 router market size stands at USD 8.25 billion in 2026, on track to reach USD 11.74 billion by 2031.

Which product type is growing fastest through 2031?

Tri-band routers are projected to post a 9.62% CAGR between 2026-2031, driven by enterprise demand for dedicated 6 GHz backhaul.

What share do online stores hold in the current channel mix?

Online retailers captured 52.23% of global revenue in 2025 and are expected to grow at an 11.42% CAGR to 2031.

Why is Asia-Pacific the fastest-growing region?

Harmonized 6 GHz regulations, government fiber subsidies, and lower entry-level pricing push Asia-Pacific Wi-Fi 6 router shipments at a 12.43% CAGR through 2031.

How fragmented is the competitive landscape?

The top five vendors control under 50% of shipments, indicating moderate concentration and room for niche specialization.

What is the main price restraint on household adoption?

Tri-band Wi-Fi 6E models still list above USD 400, a premium that discourages upgrades in price-sensitive markets until chipset integration lowers costs.

Page last updated on: