Outdoor Wi-Fi Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

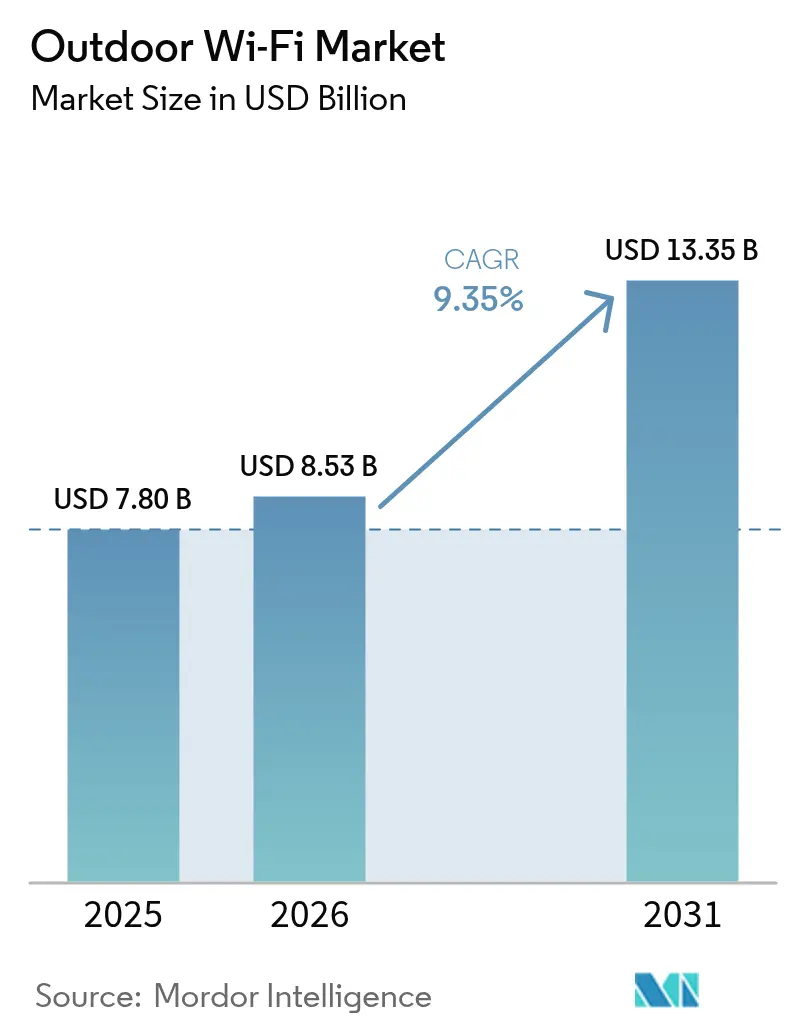

| Market Size (2026) | USD 8.53 Billion |

| Market Size (2031) | USD 13.35 Billion |

| Growth Rate (2026 - 2031) | 9.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Outdoor Wi-Fi Market Analysis by Mordor Intelligence

The Outdoor Wi-Fi market size is expected to grow from USD 7.80 billion in 2025 to USD 8.53 billion in 2026 and is forecast to reach USD 13.35 billion by 2031 at 9.35% CAGR over 2026-2031. Continued evolution from simple hotspots to strategic, IoT-ready infrastructure elevates outdoor connectivity into a core layer of municipal and enterprise digital transformation. Accelerating deployments across smart-city corridors, transportation hubs, and heavy-industry sites support steady capital expenditure, while Wi-Fi 6/6E and early Wi-Fi 7 rollouts enhance spectrum efficiency and device density. Vendors differentiate through AI-native management, ruggedized hardware, and integrated security features that align with rising compliance mandates. Climate-hardening requirements, spectrum congestion, and privacy legislation temper roll-out speeds, steering demand toward managed-service models and holistic solution providers. Regional momentum is bifurcated: North America sustains leadership through mature smart-city budgets and 6 GHz regulatory frameworks, while Asia-Pacific fuels incremental volume through urbanization programs and government-sponsored digitization.

Key Report Takeaways

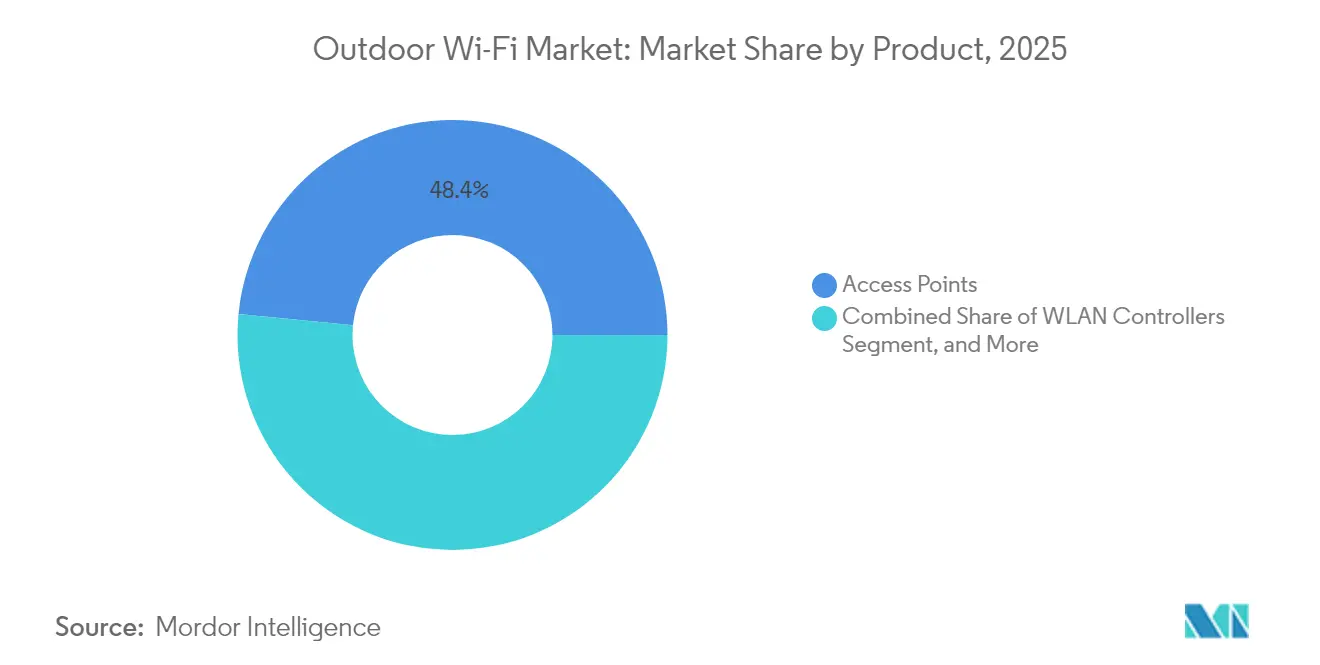

- By product category, access points led with 48.44% revenue share in 2025 in the outdoor Wi-Fi market; outdoor wireless bridges are projected to expand at a 10.08% CAGR through 2031.

- By service, installation and support accounted for 52.52% of the outdoor Wi-Fi market share in 2025, while managed services record the fastest trajectory at 10.12% CAGR through 2031.

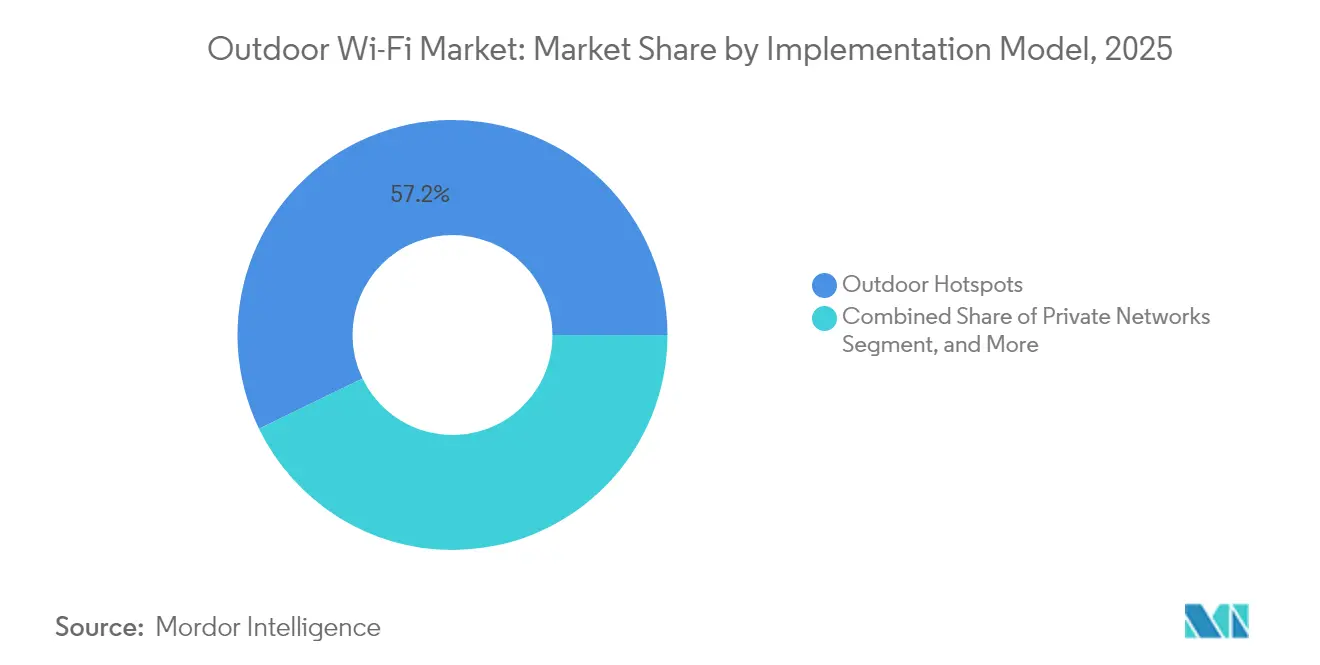

- By implementation model, traditional outdoor hotspots commanded 57.18% of the outdoor Wi-Fi market size in 2025; IoT backhaul networks are forecast to rise at a 10.24% CAGR to 2031.

- By end-user industry, smart cities and municipalities captured 34.78% revenue share in 2025 in the outdoor Wi-Fi market, whereas oil and gas/mining is advancing at a 9.56% CAGR between 2026-2031.

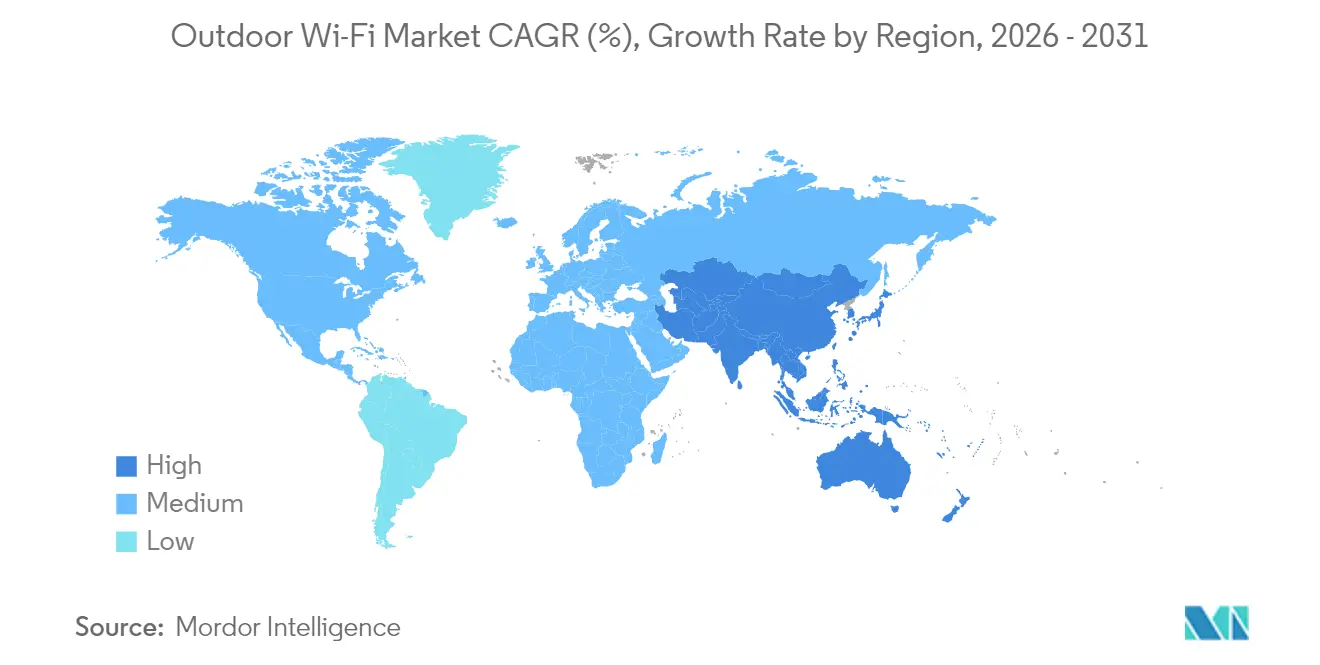

- By geography, North America maintained a 38.33% share in 2025 in the outdoor Wi-Fi market; Asia-Pacific is set to accelerate at a 9.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Outdoor Wi-Fi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth of IoT edge devices | +2.1% | Global, with APAC leading adoption | Medium term (2-4 years) |

| Rapid roll-out of smart-city Wi-Fi projects | +1.8% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Transportation-hub demand for seamless connectivity | +1.4% | Global, concentrated in major metropolitan areas | Medium term (2-4 years) |

| Wi-Fi 6/6E as cost-effective 5G offload | +1.7% | North America and EU, with regulatory variations | Short term (≤ 2 years) |

| EV-charging stations bundling outdoor Wi-Fi | +0.9% | North America and EU primarily | Long term (≥ 4 years) |

| Wi-Fi HaLow-enabled long-range industrial sensing | +1.2% | Global, with industrial concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of IoT Edge Devices

Billions of low-power sensors require continuous, cost-effective outdoor coverage, shifting architecture from user-centric hotspots to machine-centric grids. Qualcomm’s 2024 alliance with STMicro embeds tri-radio SoCs and on-board AI in MCU modules, enabling outdoor access points to handle thousands of concurrent links. Milesight and Morse Micro validated sub-1 GHz Wi-Fi HaLow for long-range smart-city sensing, underscoring the Outdoor Wi-Fi market pivot toward extended-range, low-energy backhaul. Device density intensifies demand for APs with optimized receive sensitivity, advanced scheduling, and cloud analytics that pre-empt congestion.

Rapid Roll-out of Smart-City Wi-Fi Projects

Municipal budgets increasingly earmark outdoor connectivity as critical infrastructure. Calix’s Passpoint-driven SmartTown Alliance delivered 75% connectivity gains and 3% ARPU uplift for U.S. rural broadband providers in 2024.[1]Calix Press Office, “Calix SmartTown Alliance Extends Secure Wi-Fi,” calix.com Extreme Networks’ Rome deployment and Huawei-Telconet’s 1,700-AP Ecuador rollout illustrate the scale and diversity of municipal initiatives. Such programs anchor long-term service contracts, foster public-private funding models, and catalyze adoption of AI-native network operations platforms that slash field-maintenance cycles.

Transportation-Hub Demand for Seamless Connectivity

Airports, rail terminals, and bus interchanges extend passenger experience beyond indoor concourses. Boingo broadened footprints at O’Hare and Las Vegas, integrating outdoor APs with private LTE, DAS, and neutral-host 5G fabrics. Seoul’s subway Wi-Fi corridors illustrate transit agencies’ move toward platform-to-street continuity, while LAX’s open RFP signals competitive stakes for large-venue contracts. Connectivity bundles now incorporate asset-tracking, curbside ride-share orchestration, and EV-charging telemetry, positioning the Outdoor Wi-Fi market as an operational backbone for multimodal mobility.

Wi-Fi 6/6E as Cost-Effective 5G Offload

Operators leverage six-gigahertz spectrum and OFDMA to divert high-density traffic from costly mid-band 5G. The Wi-Fi Alliance found that Wi-Fi already transports 80% of indoor data; extending this paradigm outdoors curbs RAN capital intensity. Juniper’s ruggedized AP64 and Extreme’s 6E certifications showcase hardware readiness, though AFC approval gates full-power outdoor launches in the United States of America.[2]Jeff Aaron, “Juniper announces outdoor Wi-Fi 6E AP,” juniper.net Convergence with Wi-Fi 7 and 5G network slicing enables differentiated latency tiers for AR wayfinding and real-time security feeds, reinforcing the Outdoor Wi-Fi market’s strategic relevance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating security and privacy concerns | -1.3% | Global, with heightened EU regulatory focus | Short term (≤ 2 years) |

| Spectrum congestion and RF interference | -0.9% | Dense urban areas globally | Medium term (2-4 years) |

| Climate-hardening costs for rugged APs | -0.7% | Extreme climate regions globally | Long term (≥ 4 years) |

| Country-specific EIRP limits curbing range | -0.6% | EU and regulated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Security and Privacy Concerns

Mandatory WPA3, GDPR compliance, and zero-trust mandates heighten deployment complexity. Outdoor topologies lack physical perimeter controls, making identity-centric policies and AI-driven anomaly detection essential. Juniper’s Mist embeds machine-learning threat scoring to automate containment, while healthcare campus rollouts illustrate HIPAA-grade encryption requirements for outdoor patient zones. Regulatory scrutiny, particularly in Europe, raises audit costs yet spurs demand for integrated security stacks, favoring vendors that bundle policy engines, SASE on-ramps, and edge firewalls.

Spectrum Congestion and RF Interference

Urban canyons witness mounting co-channel contention as Wi-Fi, 5G fixed wireless, and private LTE vie for spectrum. CableLabs warned that 6 GHz channels could saturate within five years at current AP densities, compelling reliance on dynamic power control and interference-aware mesh routing. Automated Frequency Coordination adds operational overhead but mitigates incumbent-protection risks. Intelligent spectrum analytics, beam-steering antennas, and AI-optimized channel plans are emerging prerequisites for sustained Outdoor Wi-Fi market performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Access Points Anchor a Diversifying Portfolio

Access Points generated 48.44% of 2025 revenue, underlining their centrality to the Outdoor Wi-Fi market size. Multi-radio, IP67-rated units with integrated edge compute now support concurrent client traffic and IoT backhaul, blending user and machine workloads. Rugged designs withstand temperature swings and moisture, while cloud telemetry enables predictive maintenance. Juniper, Extreme Networks, and Cisco refresh portfolios with Wi-Fi 6E/7 radios, tri-band scanning, and integrated GPS for location services. Growing client capacity aligns with smart-city sensor surges, cementing Access Points as the nexus of outdoor digital infrastructure.

Outdoor Wireless Bridges, advancing at a 10.08% CAGR, respond to industrial point-to-point video, backhaul for 5G small cells, and fiber-replacement in budget-sensitive regions. Ceragon’s planned integration of Siklu expands millimeter-wave options, pushing multi-gigabit throughput over 2-kilometer links. The Outdoor Wi-Fi market benefits as bridge vendors embed Wi-Fi radios for rapid mesh formation, reducing truck rolls and time-to-service. Controllers and hotspot gateways retain niche relevance where centralized session management or captive portals remain in force, particularly across hospitality and transport hubs.

By Service: Managed Offerings Accelerate Operational Efficiency

Installation and Support services held 52.52% share in 2025, reflecting the labor-intensive nature of pole mounts, cabling, and RF tuning. Yet Managed Services are forecast to expand 10.12% annually, mirroring enterprises’ lean IT staffing and the complexity of multi-site, multi-vendor ecosystems. Managed providers bundle 24×7 monitoring, over-the-air firmware, and compliance reporting, slashing mean-time-to-repair and CapEx risk. The Outdoor Wi-Fi industry sees telcos extending NOC capabilities into subscription-based Wi-Fi operations, while MSPs such as Calix’s SmartTown Alliance pool footprints for rural economies of scale.

Network Planning and Design persists as a consultative growth niche, incorporating 3-D RF modeling, LiDAR-based obstructions, and spectrum coexistence simulations for 6 GHz AFC. Training and Consulting fill a widening skills gap, focusing on AI-driven troubleshooting, security posture hardening, and cross-domain orchestration that blends Wi-Fi with private 5G.

By Implementation Model: IoT Backhaul Networks Redefine Architecture

Outdoor Hotspots still represent 57.18% of today’s Outdoor Wi-Fi market size, covering parks, plazas, and retail forecourts. However, IoT Backhaul Networks are climbing 10.24% per year, reflecting sensor-dense smart-city grids and industrial telemetry. Wi-Fi HaLow’s sub-1 GHz links extend connectivity across warehouses, mining pits, and farmland; Edgecore’s EAP112 launch underscores commercial availability. Private outdoor networks proliferate across campuses that require deterministic latency and on-prem data sovereignty, while community mesh solutions tap government subsidies to bridge digital divides.

Community Wi-Fi meshes, powered by solar poles and partner backhaul, provide last-meter access for underserved populations. Edge analytics at APs prioritizes low-bandwidth sensor traffic, while tiered QoS ensures equitable consumer internet. The Outdoor Wi-Fi market thus converges toward hybrid topologies combining public access, private slices, and low-power backhaul within a unified management plane.

By End-User Industry: Industrial Verticals Accelerate Digital Field Operations

Smart Cities and Municipalities controlled 34.78% revenue in 2025, leveraging outdoor networks for traffic analytics, environmental monitoring, and citizen portals. Municipal CIOs increasingly award multi-year contracts with performance-based SLAs that tie uptime to service payments. Oil and Gas/Mining is the fastest-growing vertical at 9.56% CAGR, deploying rugged Wi-Fi for real-time equipment telemetry, worker safety tracking, and autonomous vehicle guidance. Saudi Aramco’s adoption of outdoor mesh backbones highlights resource-sector demand for telemetry in corrosive, remote environments.

Education and Healthcare institutions extend coverage to courtyards, stadiums, and temporary triage tents, boosting patient engagement and hybrid learning. Logistics operators wire distribution yards for yard-management systems and gate automation, intertwining Wi-Fi with RFID and UWB. Retailers favor curbside fulfillment and parking-lot engagement, while Public Utilities overlay Wi-Fi on smart grids, water meters, and street-light poles, embedding connectivity into critical infrastructure, a growing slice of the Outdoor Wi-Fi market.

Geography Analysis

North America, with 38.33% revenue in 2025, capitalizes on longstanding broadband initiatives, smart-city grants, and 6 GHz spectrum clarity. Projects such as Aldine ISD’s 8,000-AP rollout underscore education’s role in volume deployments. Airport consortia, utility cooperatives, and hospital systems sustain strong pipeline demand. The Outdoor Wi-Fi market here still faces spectrum-coordination bottlenecks as the FCC finalizes AFC rules for standard-power 6 GHz, but vendor readiness and public funding mitigate adoption headwinds.

Asia-Pacific is the Outdoor Wi-Fi market’s growth engine, advancing 9.70% CAGR. Massive urbanization in China, India, and Southeast Asia drives municipal connectivity, while Japan pioneers Wi-Fi 7 pilots and OpenRoaming adoption. National spectrum allocations expedite deployments, and governmental digitization mandates encourage multivendor participation. Investments by carriers such as Claro Brasil (USD 7.7 billion through 2029) signal large-scale outdoor wireless expansion. Government-backed rural broadband, including Huawei’s Smart Village Showcase in Zambia, illustrates use cases beyond dense metros, extending Outdoor Wi-Fi market reach into agrarian communities.

Europe registers steady yet regulation-focused expansion. GDPR, AI Act provisions, and ETSI power limits influence design choices, prompting privacy-centric zero-trust architectures. Early OpenRoaming projects in Belgium and London demonstrate traction for seamless authentication models. Public-private partnerships bolster deployments in transport corridors and historical districts, balancing heritage preservation with modern connectivity. South America and the Middle East and Africa remain emerging but strategic, fueled by government connectivity targets. Morocco’s 25% 5G coverage goal by 2025 positions Outdoor Wi-Fi as complementary offload. Satellite-backhauled Wi-Fi, illustrated by Gilat’s USD 3 million Latin American contract, extends reach in sparsely populated zones.

Regulatory Landscape

Outdoor Wi-Fi deployments are increasingly shaped by 6 GHz unlicensed rules that determine whether standard-power operation is allowed outdoors and what coordination controls apply. In the United States, the FCC expanded the 6 GHz framework beyond low-power modes through actions such as permitting very low power devices across portions of the band (December 2024) and finalizing Geofenced Variable Power device rules in February 2026, with effectiveness from April 27, 2026. These rules introduce defined EIRP and PSD limits and compliance requirements tied to exclusion zones.

Across Europe, harmonization is anchored in ETSI-aligned equipment standards, including the citation of EN 303 687 V1.1.1 in the Official Journal of the European Union in May 2025, which formalizes technical requirements for 6 GHz Wi-Fi 6E/7 equipment. Outdoor standard-power 6 GHz operation remains constrained under current EU approaches that prioritize LPI and VLP modes, while the UK has moved on a separate track through Ofcom enabling standard-power Wi-Fi in the lower 6 GHz band using AFC (January 2026). This regulatory split affects outdoor product planning, channel strategy, and managed-service compliance workflows.

Value Chain Analysis

The outdoor Wi-Fi value chain starts with RF and baseband silicon for multi-band radios spanning 2.4/5/6 GHz, and in some deployments sub-1 GHz IoT connectivity, then moves through OEM design, ruggedization, certification, and field integration. Semiconductor providers supply chipsets and front-end components, while OEMs turn them into hardened platforms, commonly built to IP66 to IP68 classes and engineered for wind loading and extreme temperature operation, before distribution through direct enterprise channels, distributors, and value-added resellers.

System integration, siting, and backhaul represent a large downstream value pool because pole mounting, power, fiber or wireless backhaul, and RF planning drive outdoor performance and total cost of ownership. Municipal and transit programs also use existing public assets (street furniture, power infrastructure, and transit corridors) to shorten deployment cycles, while service partners provide ongoing monitoring, firmware management, and compliance reporting. OpenRoaming federation activity sits above the hardware layer, as shown by the Tokyo Metropolitan Government signing an MoU with the Wireless Broadband Alliance in January 2026 to accelerate OpenRoaming deployments using public assets, reinforcing the move toward identity-based access, interoperability, and recurring managed operations.

Competitive Landscape

The Outdoor Wi-Fi market features moderate fragmentation, with no single vendor exceeding a one-third revenue share. Cisco, HPE-Aruba-Juniper, and Cambium anchor the top tier, leveraging enterprise channels, AI-driven cloud management, and extensive field services. HPE’s USD 14 billion Juniper acquisition consolidates Aruba’s portfolio with Mist’s AIops, intensifying competition with Cisco and enabling broader outdoor SKUs. The DOJ-mandated divestiture of Aruba Instant On creates white-label opportunities for mid-tier providers, potentially redistributing market influence.

Specialists such as Ubiquiti, Ruckus (CommScope), and Cambium emphasize price-performance and community-mesh features, targeting municipalities and WISPs. Amphenol’s acquisition of CommScope’s outdoor networks unit repositions passive infrastructure under a connectivity conglomerate, suggesting vertical integration synergies for antennas and enclosures. Emerging innovators like Edgecore and Morse Micro commercialize Wi-Fi HaLow, carving niches in low-power IoT backhaul. Managed-service aggregators integrate multi-vendor estates, fueling service-led differentiation.

Strategic moves revolve around portfolio expansion, AI-native platforms, and geographic diversification. Integration of satellite backhaul (ANTlabs–Starlink), tower partnerships (Millicom–SBA), and microwave backhaul acquisitions (Ceragon–Siklu) underscore cross-domain convergence. Vendors that marry rugged hardware with predictive analytics, SASE, and open-roaming federation are positioned to seize the Outdoor Wi-Fi market’s next growth wave.

Outdoor Wi-Fi Industry Leaders

Aerohive Networks LLC

Airspan Networks Holdings Inc.

Alvarion Technologies Ltd.

Cisco Systems, Inc.

Fortinet, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace in outdoor Wi-Fi is the upgrade cycle from Wi-Fi 6/6E to Wi-Fi 7-class rugged access points and bridges that can support higher client density while keeping operations manageable across distributed outdoor estates. Wi-Fi 7 features such as Multi-Link Operation and wider 6 GHz channels are being productized for outdoor conditions, and vendor roadmaps are aligning with this direction, for example Edgecore previewing an outdoor Wi-Fi 7 access point (OAP106) with tri-band capability and rugged design (November 2025). This supports an opportunity for municipalities, venues, and industrial operators to consolidate public access and machine connectivity on fewer sites, paired with cloud management, security policy enforcement, and lifecycle services.

Regulatory and permitting frameworks also create room for faster outdoor network expansion where rights-of-way and site approvals are a bottleneck. The EU Gigabit Infrastructure Act (Regulation EU 2024/1309) targets streamlined permitting for very high-capacity networks, and country-specific 6 GHz policy choices, including AFC-enabled models, shape how quickly outdoor standard-power designs can be used. Execution patterns in cities also point to operational pull-through for smart-city use cases, such as Carmel, Indiana deploying outdoor Wi-Fi 6E across public venues (September 2025), which provides a repeatable template for other municipalities to add sensor backhaul, video, and citizen services alongside managed operations and security compliance.

Recent Industry Developments

- June 2026: Cisco introduced new outdoor Wi-Fi 7 hardware as part of an updated networking portfolio. The refresh supports higher-density outdoor connectivity and aligns product roadmaps with emerging 6 GHz operating models, strengthening competitive positioning in municipal, venue, and industrial deployments.

- February 2026: Airspan launched its MobileAccess Digital DAS platform across Europe, including the UK, to support unified public and private network deployments. By tightening integration between outdoor radio infrastructure and broader neutral-host or private-network builds, the platform expands options for operators and enterprises bundling outdoor Wi-Fi with cellular coverage and backhaul.

- December 2024: Airspan was selected by AWTG as the RAN partner for the Connected Heartland Railways project in the UK, deploying AirSpeed 1900 outdoor small cells to support connectivity including onboard Wi-Fi. The win reinforces rail and transit corridors as a demand center for rugged outdoor wireless infrastructure and multi-year rollout programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the outdoor Wi-Fi market is defined as revenue earned from outdoor Wi-Fi networking products and related services used to deliver wireless connectivity in open-air or harsh environment locations, across public and private deployments.

Scope exclusions: We exclude indoor-only Wi-Fi equipment and consumer home networking gear unless it is explicitly sold and deployed for outdoor-grade use cases.

Segmentation Overview

- By Product

- WLAN Controllers

- Access Points

- Outdoor Wireless Bridges

- Wireless Hotspot Gateways

- By Service

- Network Planning and Design

- Installation and Support

- Managed Services

- Training and Consulting

- By Implementation Model

- Outdoor Hotspots

- Private Networks

- Community Wi-Fi Mesh

- IoT Backhaul Networks

- By End-user Industry

- Healthcare

- Education

- Logistics and Transportation

- Travel and Hospitality

- Public Utilities

- Smart Cities and Municipalities

- Retail

- Oil and Gas / Mining

- Other End-user Industries

- By Geography

- North America

- South America

- Europe

- Asia-Pacific

- Middle East and Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, build the starting demand pool, and pressure-test early assumptions that would otherwise be too optimistic. We relied on public references such as FCC spectrum and equipment authorization information, ITU materials on wireless standards, OECD and World Bank connectivity indicators, and national telecom regulator releases that track broadband and Wi-Fi policy direction.

To connect these signals to revenue, we also reviewed company filings, investor decks, product catalogs, and reputable press for rollout timelines, typical configuration mixes, and price movement by Wi-Fi generation. Where public reporting was thin, we used paid subscriptions for company financials and intelligence, plus news and financials, to cross-check business line splits and recent contract wins without forcing one source to do all the work. These desk sources are illustrative only, and many other public and subscription sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what is really being deployed outdoors and how pricing is changing when Wi-Fi 6/6E, early Wi-Fi 7 readiness, ruggedization, and security features are bundled. We spoke with a mix of equipment suppliers, system integrators, managed service providers, and large end users across major regions so that coverage gaps from desk inputs could be closed before assumptions were finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 17% | APAC: 42% |

| Mid tier: 49% | Functional/Unit leaders: 39% | EMEA: 31% |

| Smaller Players: 19% | Managers: 44% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where the addressable outdoor demand pool is reconstructed from deployment drivers, and then translated into spend using typical configuration and pricing. In practice, we map likely outdoor site counts and refresh needs across hotspots and private networks, and then apply adoption and replacement cycles to estimate annual unit demand and related services revenue.

Key inputs used in the model include outdoor hotspot rollout pace, private network penetration by venue type, the mix shift toward Wi-Fi 6/6E and early Wi-Fi 7 capable hardware, average selling price (ASP) changes tied to rugged specs and security features, and the share of projects that include planning, installation, and support services. To keep totals grounded, we do selective bottom-up checks, such as sampling ASP estimates against unit volume ranges, plus channel and tender checks where available. We then adjust the totals when the implied spend does not match what interviews described as typical project budgets. When company disclosures do not separate outdoor lines cleanly, gaps are handled through conservative allocation rules that are reviewed with multiple interviewees.

For forecasting, we use scenario analysis supported by regression-style relationships between deployment activity and unit pricing, then refine those paths based on what practitioners expect for refresh cycles, standard upgrades, and budget timing. The forecast is kept consistent with the expected pace of public venue digitization, municipal connectivity plans, and enterprise campus expansion, while still allowing for slower years when broader spending tightens.

Data Validation & Update Cycle

Validation is done through multiple checks so that one noisy input does not drive the full outcome. We compare outputs against independent signals such as project cadence, observed price points, and the implied equipment mix, then investigate outliers before the model is finalized through internal review steps.

Reports are refreshed annually, and interim updates are triggered when major events can shift pricing or adoption, such as a new Wi-Fi generation ramp, large policy changes, or sharp currency movement. Before delivery, the latest public releases are rechecked and assumptions are revalidated through follow-up outreach so the numbers reflect the most current view available at the time.

Mordor Intelligence's Outdoor Wi Fi Market Size Measured Against Other Published Estimates

Published market values for outdoor Wi-Fi do not always match because each publisher chooses its own timing, scope boundary, and pricing logic. Differences become more visible when one estimate is anchored on a single base year, while another leans on a later refresh window or uses a different currency conversion point.

The biggest gap drivers in this market are usually whether services are counted alongside equipment, how aggressively ASP declines are applied as Wi-Fi 6/6E becomes mainstream, and whether private network deployments are sized from realistic site counts or from broad connectivity targets. In this study, currency timing and ASP refresh checks are applied close to publication, which helps keep the 2026 value aligned with the most recent price bands and rollout cadence, a step handled explicitly within Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.53 B (2026) | |

| Market Publisher A | USD 7.38 B (2024) | Uses an earlier value year, and the timeline references shift between base and forecast windows, which can change implied refresh cycles and price assumptions when compared across years. |

| Industry Publisher B | USD 7.20 B (2024) | Reported as equipment-only, which typically excludes planning, installation, and support services, and it may also apply a different ASP decline path by technology generation. |

The spread in the table is mostly explained by timing and scope, not by one single growth rate assumption. When the counted revenue lines are kept consistent and pricing is refreshed with the same currency timing, the market total becomes easier to trace back to site demand, replacement cycles, and realistic project configurations.

Key Questions Answered in the Report

What is the Outdoor Wi-Fi market outlook through 2031?

The Outdoor Wi-Fi market size should climb from USD 7.80 billion in 2025 to roughly USD 13.35 billion by 2031, reflecting a 9.35% CAGR driven by smart-city adoption and IoT backhaul demand.

Which product type dominates Outdoor Wi-Fi deployments?

Access Points hold nearly 48% revenue share due to their versatility in user connectivity and IoT support.

Which region will grow fastest in Outdoor Wi-Fi?

Asia-Pacific is set to expand at about 9.70% CAGR on the back of urbanization and government digitization mandates.

Why are managed services gaining traction?

Complex multi-site outdoor networks require 24×7 monitoring and rapid firmware updates, so enterprises increasingly outsource operations to managed-service providers offering AI-driven automation.

How does Wi-Fi 6E influence outdoor connectivity?

Six-gigahertz spectrum and OFDMA features make Wi-Fi 6E a cost-efficient offload for 5G, enabling higher throughput and lower latency in dense outdoor venues.

Page last updated on: