Home Wi-fi Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.22 Billion |

| Market Size (2031) | USD 21.88 Billion |

| Growth Rate (2026 - 2031) | 7.53% CAGR |

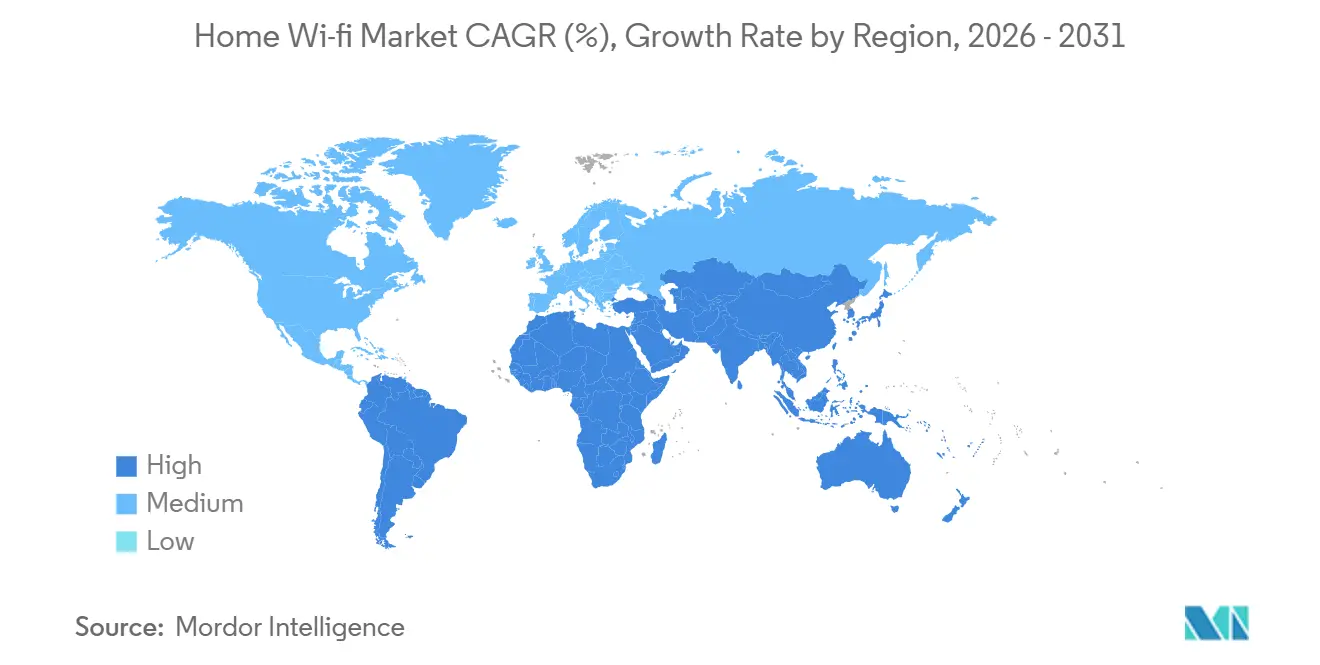

| Fastest Growing Market | Africa |

| Largest Market | Asia-Pacific |

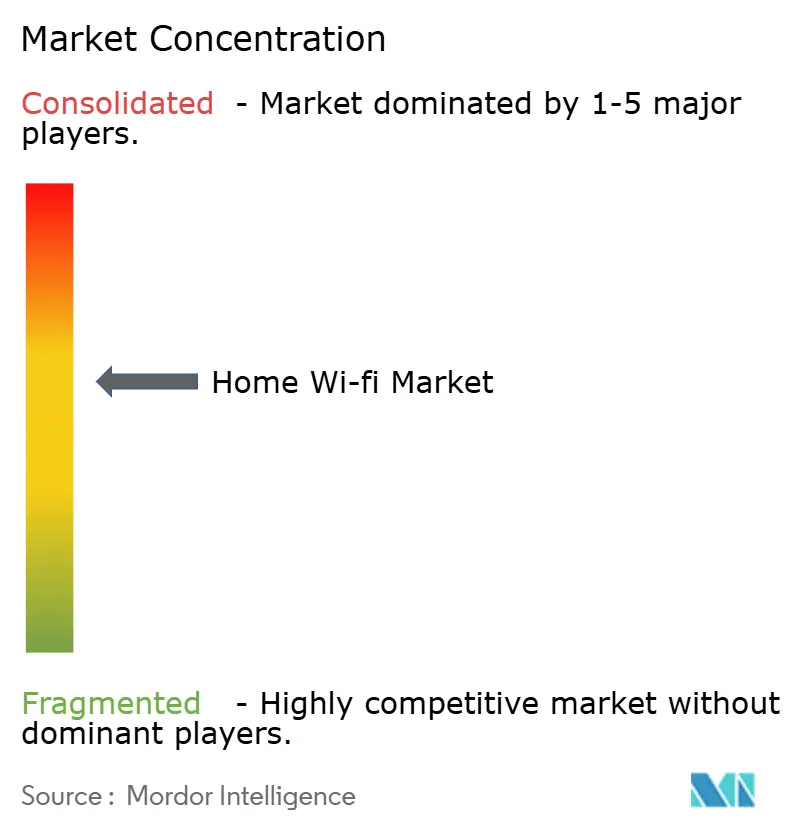

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Wi-fi Market Analysis by Mordor Intelligence

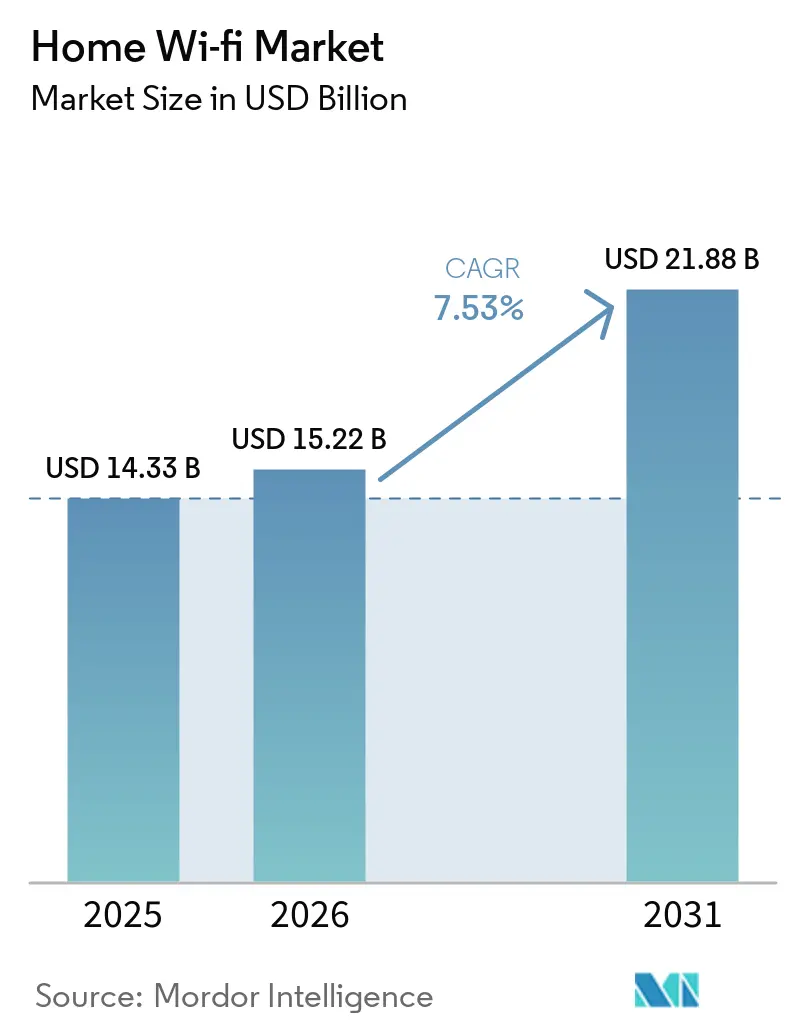

The Home Wi-Fi market size is expected to increase from USD 14.33 billion in 2025 to USD 15.22 billion in 2026 and reach USD 21.88 billion by 2031, growing at a CAGR of 7.53% over 2026-2031. Rising fiber-to-the-home (FTTH) coverage in Europe and North America is pushing gigabit-class connectivity into living rooms, exposing legacy routers as the new bottleneck. Vendors are responding with tri-band mesh and Wi-Fi 7 gateways that match multi-gigabit broadband tiers, while chipset suppliers have already signaled a rapid pivot to Wi-Fi 8. Managed Wi-Fi subscriptions offered by internet service providers (ISPs) are shifting value capture from one-time router sales to recurring service revenue, compressing online retail margins yet improving customer experience. Security remains a flashpoint as consumer gateways register a higher vulnerability count than enterprise gear, driving regulatory scrutiny and reinforcing the appeal of carrier-managed firmware pipelines.

Key Report Takeaways

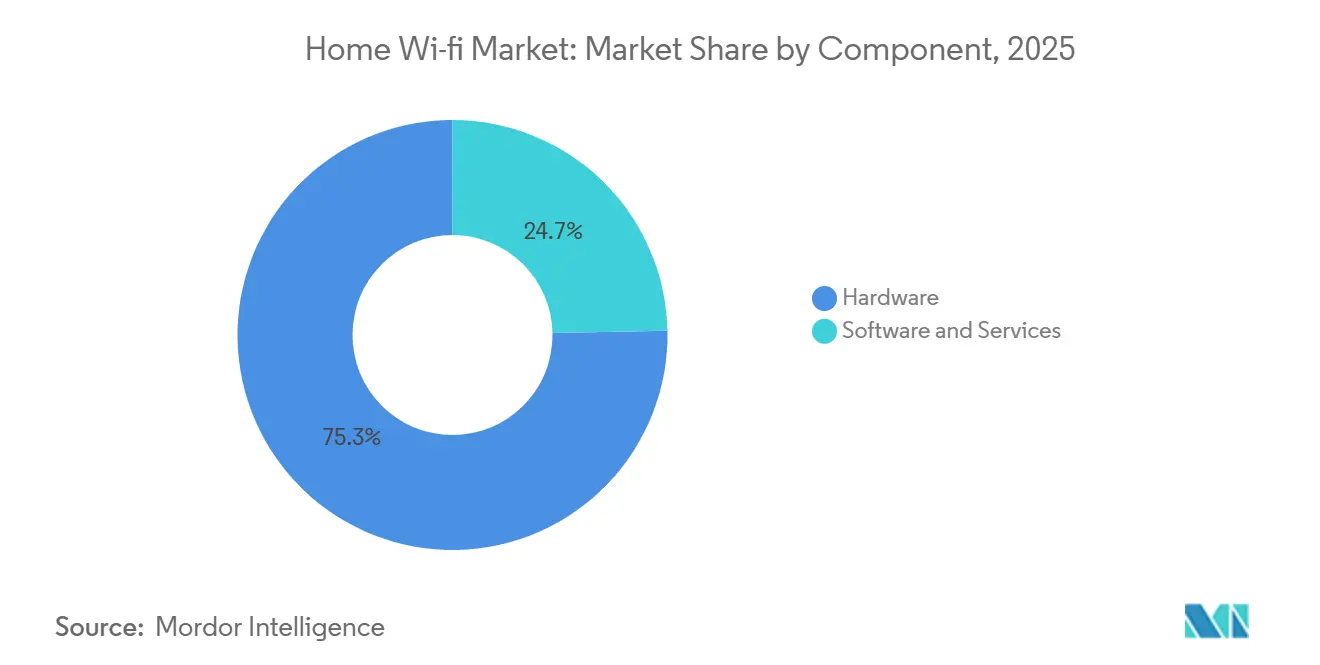

- Hardware led with 75.32% of the Home Wi-Fi market share in 2025, whereas software and services are advancing at an 11.84% CAGR through 2031, outpacing the overall market by 430 basis points.

- Wi-Fi 6 captured 40.31% of 2025 unit shipments, while Wi-Fi 7 is projected to grow at a 20.67% CAGR, the fastest among all standards.

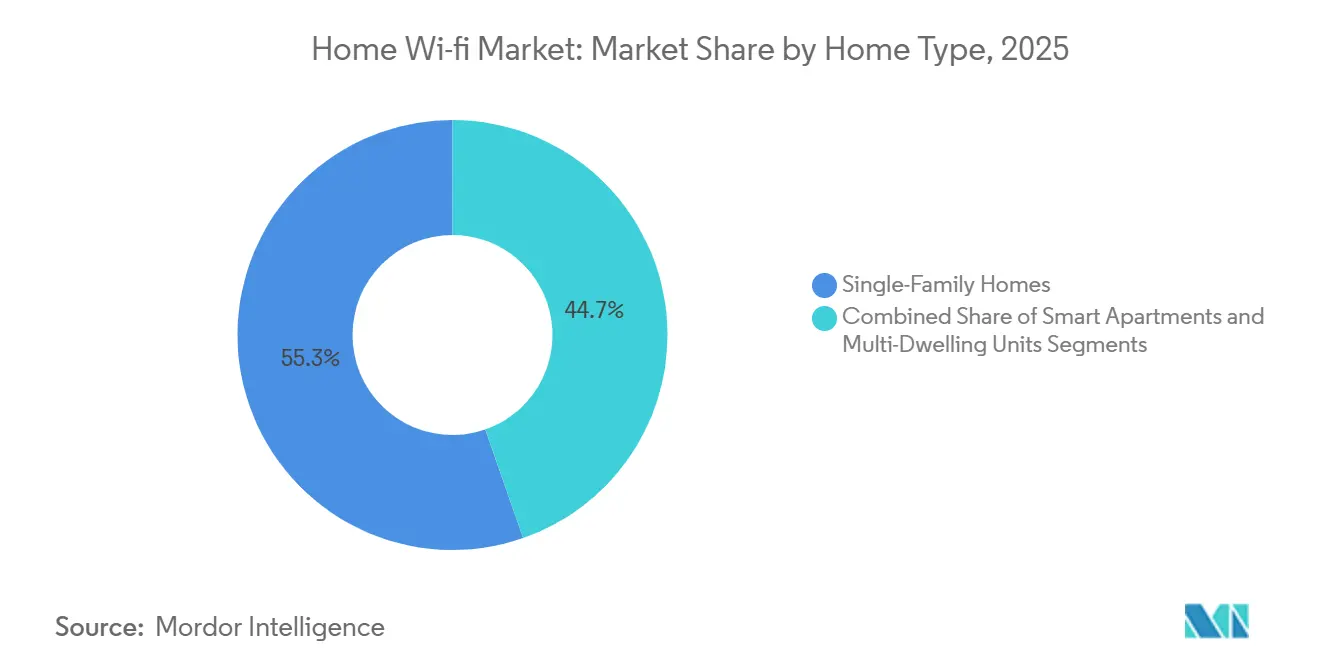

- Single-family homes accounted for 55.42% of 2025 deployments, while smart apartments are the fastest-growing segment, with a 13.53% CAGR to 2031.

- Single-family homes accounted for 55.22% of 2025 deployments, while smart apartments are the forecasted at a 13.53% CAGR to 2031.

- Online retail accounted for 46.11% of 2025 sales, but ISP and carrier bundles are forecast to grow at 12.52% annually, steadily compressing retail hardware margins.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Home Wi-fi Market Trends and Insights

Restraints Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of smart home devices | +2.10% | Global, strongest in North America and Asia-Pacific metros | Medium term (2-4 years) |

| FTTH penetration elevating in-home Wi-Fi demand | +1.80% | Europe, North America, East Asia | Long term (≥4 years) |

| Expansion of hybrid work culture | +1.30% | North America and Europe | Short term (≤2 years) |

| Adoption of Wi-Fi 6, 6E and 7 | +1.50% | Global | Medium term (2-4 years) |

| Emergence of low-power Wi-Fi modules | +0.40% | North America and Europe first movers | Long term (≥4 years) |

| Government-subsidized broadband programs | +0.50% | United States, India, selected EU states | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Proliferation Of Smart Home Devices

Smart home ecosystems have moved from one-off gadgets to always-connected platforms that require uninterrupted, low-latency links for cameras, speakers, and thermostats. Average connected devices per U.S. household reached the high-teens by 2025, and Matter 1.5, ratified in 2026, unifies 30 device categories across Apple, Google, Amazon, and Samsung, reducing interoperability friction. Larger device counts strain single-band routers, so tri-band mesh with Wi-Fi 6E backhaul is becoming the default in new single-family homes above 2,000 square feet. Vendors are increasingly embedding AI-driven troubleshooting that optimizes channel selection, reduces support costs, and extends device lifecycles, supporting higher ASPs.[1]FTTH Council Europe, “Market Panorama 2025,” ftthcouncil.eu

Growing FTTH Penetration Elevating In-Home Wi-Fi Demand

Europe reached 79% FTTH coverage by late 2025, passing 295 million homes and adding 160 million subscribers. Symmetric gigabit tiers expose the limitations of legacy 802.11ac gateways, which fall short of 1 Gbps throughput, prompting ISPs to bundle Wi-Fi 7 gateways such as Comcast’s XB10 with new multi-gigabit plans. Similar dynamics are evident in the United States, where fiber deployments surpassed 100 million locations by 2025. Hardware subsidies tied to premium broadband tiers are accelerating refresh cycles and structurally linking the home Wi-Fi market to ongoing fiber network expansion.[2]Federal Communications Commission, “6 GHz Very-Low-Power Rules 2024,” fcc.gov

Expansion Of Hybrid Work Culture

Roughly one-third of U.S. workers operated in hybrid work models in 2025, with sustained video conferencing increasing demand for resilient home connectivity, including segmented virtual networks and cellular failover. Features such as dual-WAN, application-aware quality of service, and WPA3-Enterprise security, previously limited to small business routers, are now standard in advanced residential gateways. ISPs are monetizing this shift through managed Wi-Fi subscriptions that bundle remote diagnostics, performance optimization, and automated firmware updates, thereby establishing a recurring service revenue stream in the home Wi-Fi market.[3]Wi-Fi Alliance, “Wi-Fi 7 Adoption Outlook 2026,” wi-fi.org

Increasing Adoption Of Wi-Fi 6 And Beyond

Wi-Fi 7 device shipments are projected to rise from 583 million units in 2025 to 1.1 billion in 2026, significantly compressing the adoption cycle relative to Wi-Fi 6. Chinese OEMs are introducing sub-USD 250 Wi-Fi 7 routers, undercutting prior Wi-Fi 6E price benchmarks and accelerating mass-market access to multi-gigabit performance. Concurrently, Broadcom and Qualcomm unveiled early Wi-Fi 8 chipsets in early 2026, indicating a faster innovation cadence. This rapid upgrade cycle sustains continuous hardware refresh demand in the home Wi-Fi market, supporting vendor revenues despite declining per-unit pricing.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interference and congestion in unlicensed spectrum | -0.90% | High-density urban MDUs worldwide | Short term (≤2 years) |

| Security vulnerabilities in consumer routers | -0.70% | North America and Europe regulators | Medium term (2-4 years) |

| Supply-chain disruptions for chipsets | -0.30% | Asia-Pacific fabs | Short term (≤2 years) |

| Substitution by 5G fixed wireless access | -0.60% | Rural North America, selected Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interference And Congestion In Unlicensed Spectrum

Urban multi-dwelling units (MDUs) routinely host dozens of overlapping 2.4 GHz and 5 GHz networks, degrading throughput and increasing latency due to spectrum congestion and co-channel interference. Regulatory expansion of very-low-power usage across the 6 GHz band has provided incremental relief, but indoor power constraints limit signal propagation, necessitating higher access-point density to maintain coverage. In response, building owners are increasingly adopting centralized, cloud-managed Wi-Fi architectures that dynamically optimize channel allocation and transmit power. While this improves network performance and user experience, it introduces higher upfront capital expenditure and increases dependency on specific vendors, raising long-term lock-in and switching risks within the home Wi-Fi ecosystem.

Security Vulnerabilities In Consumer Routers

D-Link, Netgear, and TP-Link have collectively accumulated over 1,000 CVEs over the past decade, underscoring persistent security vulnerabilities in consumer routers. A surge in authentication-bypass flaws during 2024-2025 triggered a March 2026 action by the Federal Communications Commission that restricted the import of foreign-manufactured devices, forcing vendors to reconfigure their supply chains and seek approvals. This shift favors ISP-managed gateways with automatic updates, improving patch compliance but concentrating systemic risk if widely deployed models are compromised.[4]Ministry of Industry and Information Technology, “China Fiber Stats 2025,” miit.gov.cn

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Layer Drives Recurring Revenue

Software and services, expanding at a CAGR of 11.84%, are capturing a rising share of consumer spend as ISPs bundle parental controls, network security, and mesh extensions into recurring subscription plans. Comcast’s xFi platform alone generated approximately USD 2 billion in annual recurring revenue in 2025, illustrating the scale of monetization. Although hardware accounted for nearly 75% of total revenue in 2025, sustained price compression in standalone routers is shifting profit pools toward software-led offerings. As a result, services are expected to outpace hardware growth across regions, indicating a structural transition toward subscription-based economics in the home Wi-Fi market.

Consumers are increasingly opting to rent ISP-supplied gateways that include guaranteed upgrades every 24-36 months, reducing upfront costs and ensuring performance parity with evolving standards. This trend is weakening online retail channels while creating predictable annuity streams for telecom operators. For OEMs, white-label manufacturing agreements with ISPs partially offset declining branded sales volumes but exert downward pressure on gross margins. In parallel, managed Wi-Fi platforms in multi-dwelling units are reinforcing the service model, where landlords pay per-unit fees for centralized control and analytics, repositioning connectivity as a bundled amenity rather than a tenant-managed utility expense.

By Standard: Wi-Fi 7 Overtakes Wi-Fi 6 On Speed And Economics

Wi-Fi 6 held the largest share of the home Wi-Fi market in 2025 at 40.31%, but Wi-Fi 7, growing at a 20.67% CAGR, is positioned to overtake it well before the end of the forecast period. Aggressive pricing, below USD 250 in China and under EUR 100 in parts of Europe, is accelerating early adoption. Device ecosystems are reinforcing this transition, with 2026 flagship smartphones expected to integrate Wi-Fi 7 chipsets by default. Concurrently, Broadcom’s planned Wi-Fi 8 silicon sampling in 2H 2026 signals shorter innovation cycles, reducing hardware differentiation windows and shifting competitive focus toward software capabilities.

Mesh systems leveraging 320 MHz channels in the 6 GHz band are delivering near-gigabit real-world speeds across multiple rooms, directly addressing performance constraints for hybrid work, streaming, and gaming. However, tri-band architectures significantly increase the bill of materials, making ISP subsidies critical for broader consumer adoption. This dynamic strengthens the carrier's influence over distribution and product design. Vendors lacking strong ISP partnerships face constrained scale, as retail demand increasingly concentrates in premium segments, limiting volume growth and compressing margins for standalone hardware offerings.

By Home Type: Smart Apartments Monetize Connectivity

Single-family homes dominated installations in 2025, driven by do-it-yourself buyers and larger floor plans requiring multi-node mesh deployments to ensure consistent coverage. However, smart apartments are expanding at a 13.53% CAGR as multi-dwelling units deploy building-wide mesh networks with virtual segmentation for residents, IoT devices, and building systems. This model allows landlords to bundle connectivity into rent, reducing tenant churn and improving net operating income. The shift also repositions connectivity from a tenant-managed utility to a property-level managed service with centralized control and monetization.

Brownfield retrofits represent a market roughly 4 times larger than new construction, but high wall-fishing and rewiring costs are pushing property owners toward alternatives such as Wi-Fi 7 backhaul over existing coaxial or powerline infrastructure. Regulatory developments, including California AB 1414, which mandates opt-out provisions for tenants, may moderate adoption in certain regions. However, with 24 additional states evaluating similar frameworks that still permit revenue-sharing models, managed Wi-Fi deployments remain structurally viable, particularly when landlords can align service pricing with tenants' value perceptions.

By Distribution Channel: ISP Bundles Compress Retail Margins

Online retail accounted for 46.11% of shipments in 2025, but ISP-led rental models are expanding faster, supported by a 12.52% CAGR in carrier bundles. A typical USD 14 monthly rental recovers the cost of a USD 300 gateway within 24 months while ensuring periodic upgrades, making the model economically rational for both operators and consumers. Retail channels are countering with extended warranties and bundled services, but transparent pricing on e-commerce platforms continues to compress margins. This dynamic is shifting value capture away from one-time hardware sales toward recurring service-based revenue streams.

Carrier control over firmware and network management enables faster deployment of security patches and performance updates, an advantage increasingly emphasized by regulators. As a result, bundled gateway offerings are projected to exceed 50% of total North American volumes over the forecast period. This structural shift forces hardware-centric vendors to reassess go-to-market strategies, with greater reliance on ISP partnerships, white-label manufacturing, and integrated service layers to remain competitive in an ecosystem increasingly dominated by carrier-controlled distribution and lifecycle management.

Geography Analysis

Asia-Pacific accounted for 35.26% of the global home Wi-Fi market revenue in 2025, anchored by China’s base of approximately 280 million fiber-connected homes and India’s BharatNet expansion into rural broadband infrastructure. Mid-range mesh systems priced between CNY 500 and CNY 2,000 (USD 69-275) are gaining traction among middle-class consumers upgrading to multi-story residential units, where coverage gaps necessitate multi-node deployments. In parallel, Japan and South Korea are leading early adoption of Wi-Fi 7-enabled smartphones, creating a demand pull effect that accelerates router replacement cycles and strengthens ecosystem alignment between devices and network infrastructure.

North America and Europe together contributed roughly 50% of global sales, supported by high fiber penetration and strong carrier ecosystems. Europe achieved 79% FTTH coverage with a 54% subscriber take rate by late 2025, indicating both infrastructure maturity and strong consumer uptake. The United States surpassed 100 million fiber passings, with federal broadband programs such as BEAD allocating funds for in-unit Wi-Fi equipment for underserved populations. Increasing regulatory scrutiny around cybersecurity and supply chains is tightening vendor requirements, but widespread adoption of carrier-managed gateways shields end users from operational complexity while reinforcing ISP control over device lifecycles.

Africa represents the fastest-growing region, with a 14.21% CAGR, albeit from a lower broadband penetration base. Markets such as Kenya and Nigeria are prioritizing 5G fixed wireless access as a cost-effective alternative to fiber deployment, driving demand for hybrid gateways that combine Wi-Fi 7 local networks with 5G wide-area connectivity. In the Middle East, government-led smart city initiatives are embedding advanced connectivity infrastructure into urban planning, while South America is benefiting from continued fiber rollouts in dense metropolitan areas. These trends collectively emphasize geographic diversification as a core strategic lever for vendors seeking sustained growth.

Competitive Landscape

The home Wi-Fi market remains moderately fragmented, with leading retail brands such as TP-Link, Netgear, D-Link, ASUS, and Xiaomi competing alongside ISP-driven distribution. Telecom operators increasingly deploy white-label gateways, including solutions from Comcast and Charter Communications, which compress margins for retail vendors. Platform ecosystems from Amazon (Eero) and Google (Nest) integrate cloud services and smart home controls, strengthening user lock-in and shifting competition toward ecosystem ownership rather than standalone hardware performance.

Regulatory intervention is reshaping supply chains and competitive positioning. The March 2026 action by the Federal Communications Commission restricting unapproved foreign-manufactured routers has forced vendors to diversify manufacturing footprints across multiple geographies. At the same time, chipset innovation cycles are accelerating, with Broadcom and Qualcomm advancing Wi-Fi 8 development, reducing hardware differentiation windows. As a result, vendors are shifting emphasis toward software layers, including network management, security, and interoperability, to maintain competitive relevance.

Managed Wi-Fi deployments in multi-dwelling units remain under-penetrated in North America, leaving a clear growth opportunity for specialized providers such as Calix and Datavalet. These platforms offer centralized control, analytics, and property-level service monetization, aligning with landlord incentives. Going forward, competitive advantage will depend on integrating hardware, cloud orchestration, and recurring service layers, rather than relying on standalone router margins, which continue to face structural compression.

Home Wi-fi Industry Leaders

TP-Link Technologies Co., Ltd.

Netgear, Inc.

D-Link Corporation

ASUSTeK Computer Inc.

Linksys Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Xiaomi debuted the BE3600 Pro Wi-Fi 7 router at CNY 1,799 (USD 247) in China and rolled out European variants priced at EUR 99-249.

- April 2026: P-Link secured conditional FCC approval after the agency’s import ban, highlighting its United States ownership and Vietnam assembly lines.

- March 2025: The FCC prohibited sales of new foreign-manufactured consumer routers without explicit authorization, citing national security and firmware risk.

- March 2026: D-Link unveiled four Wi-Fi 7 routers, with the flagship G572 adding integrated 5G backup for hybrid fixed-mobile resilience.

Global Home Wi-fi Market Report Scope

The home Wi-Fi market comprises hardware, software, and services that enable wireless broadband connectivity within residential environments using standards such as IEEE 802.11. It includes standalone routers, mesh systems, gateways, extenders, and integrated platforms that deliver coverage, capacity, and security across multiple devices. The market also incorporates cloud-based management, cybersecurity features, and ISP-managed services that support installation, optimization, and lifecycle maintenance. Rising connected device density, high-bandwidth applications, smart home integration, and the transition toward subscription-based connectivity models drive demand.

The Home Wi-Fi Market Report is Segmented by Component (Hardware, Software and Services), Standard (Wi-Fi 4, Wi-Fi 5, Wi-Fi 6, Wi-Fi 6E, and Wi-Fi 7), Home Type (Single-Family Homes, Multi-Dwelling Units, and Smart Apartments), Distribution Channel (Online Retail, Brick-and-Mortar Retail, ISP and Carrier Bundles), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software and Services |

| Wi-Fi 4 (802.11n) |

| Wi-Fi 5 (802.11ac) |

| Wi-Fi 6 (802.11ax) |

| Wi-Fi 6E |

| Wi-Fi 7 |

| Single-Family Homes |

| Multi-Dwelling Units |

| Smart Apartments |

| Online Retail |

| Brick-and-Mortar Retail |

| ISP and Carrier Bundles |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Hardware | |

| Software and Services | ||

| By Standard | Wi-Fi 4 (802.11n) | |

| Wi-Fi 5 (802.11ac) | ||

| Wi-Fi 6 (802.11ax) | ||

| Wi-Fi 6E | ||

| Wi-Fi 7 | ||

| By Home Type | Single-Family Homes | |

| Multi-Dwelling Units | ||

| Smart Apartments | ||

| By Distribution Channel | Online Retail | |

| Brick-and-Mortar Retail | ||

| ISP and Carrier Bundles | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the Home Wi-Fi market be by 2031?

The home wi-fi market size is projected to reach USD 21.88 billion by 2031, expanding at a 7.53% CAGR over 2026-2031.

Which component segment is growing fastest?

Software and services are forecast to rise at an 11.84% CAGR, outstripping hardware demand as ISPs monetize managed Wi-Fi bundles.

What is the current share of Wi-Fi 7 devices?

Wi-Fi 7 shipments are accelerating rapidly and are expected to surpass 1.1 billion units in 2026, giving the standard a rising slice of home wi-fi market share.

Why are ISPs bundling routers with broadband plans?

Carrier-supplied gateways cut support calls, ensure timely security patches and create recurring rental revenue that offsets falling retail margins.

Which region offers the strongest growth outlook?

Africa leads regional growth with a 14.21% CAGR through 2031 as nations leapfrog to fiber and 5G fixed wireless.

How is regulation affecting hardware sourcing?

The FCCs 2026 import restrictions require conditional approvals for foreign-made routers, prompting vendors to diversify assembly into Vietnam, Mexico and the United States.

Page last updated on: