Wi-fi 6E Router Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

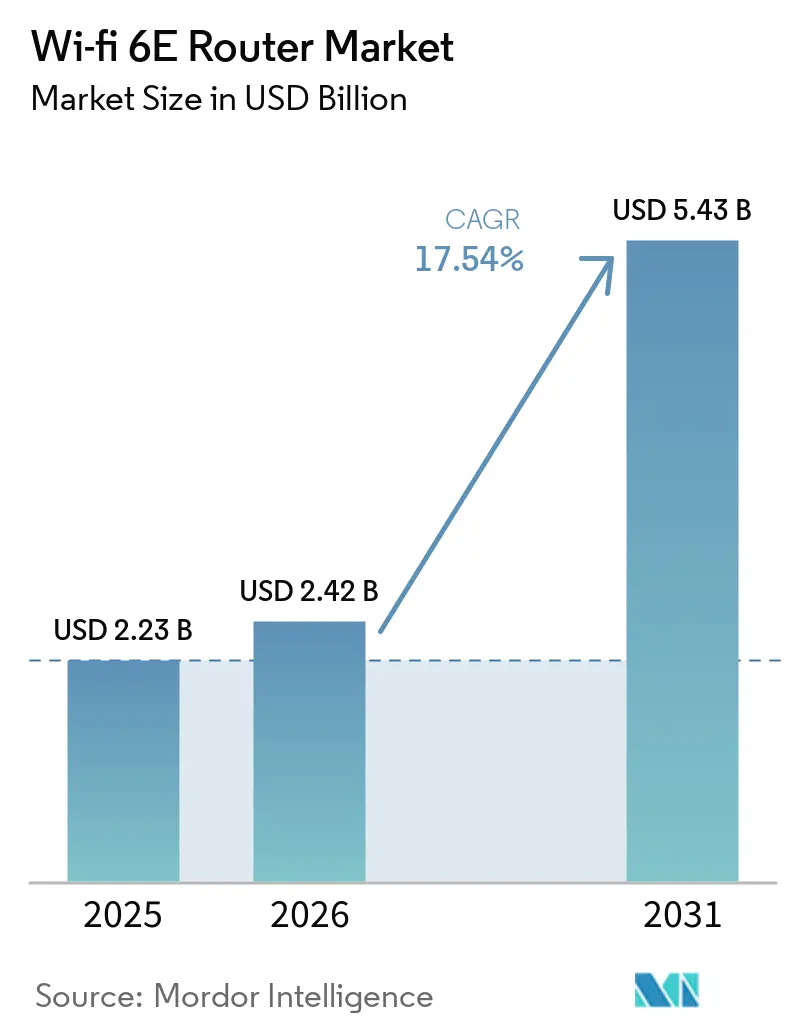

| Market Size (2026) | USD 2.42 Billion |

| Market Size (2031) | USD 5.43 Billion |

| Growth Rate (2026 - 2031) | 17.54% CAGR |

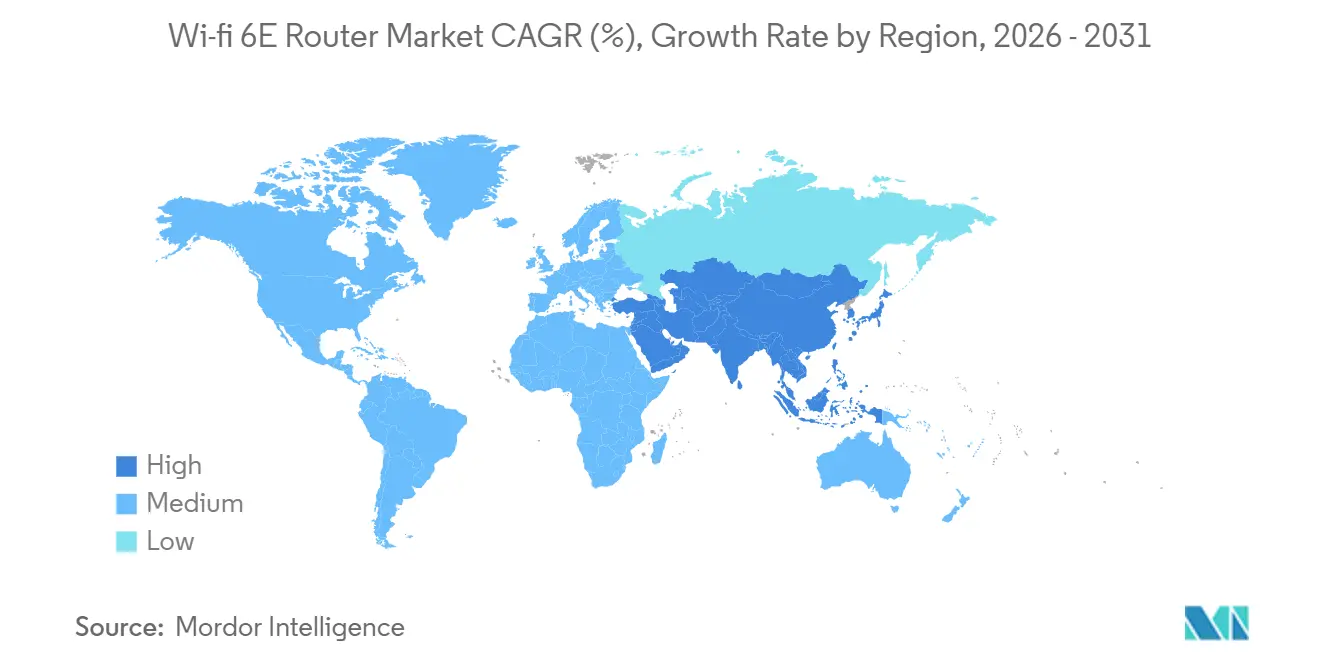

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

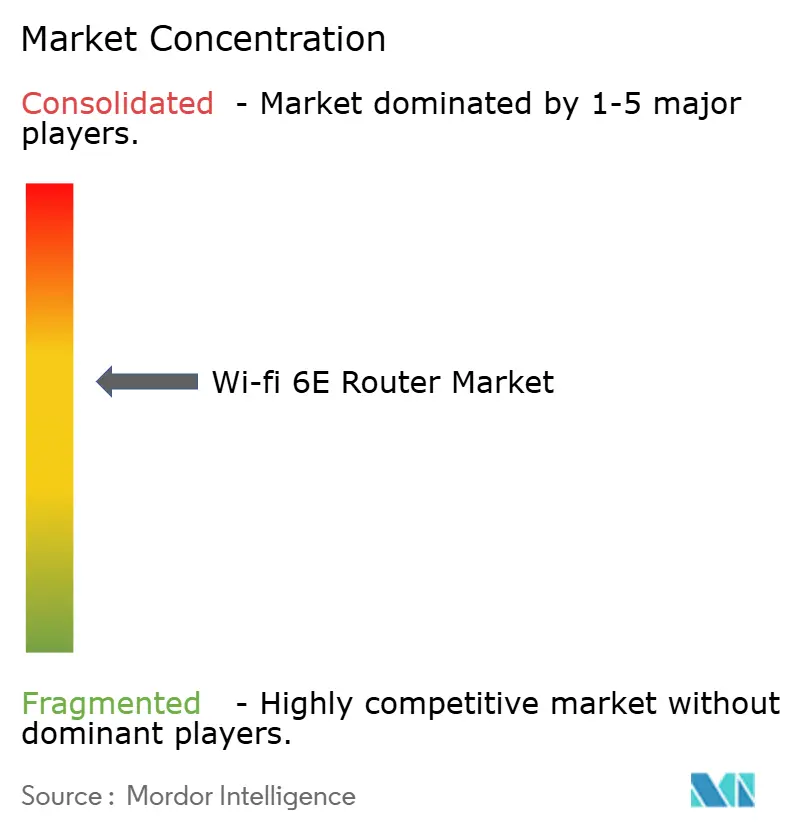

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wi-fi 6E Router Market Analysis by Mordor Intelligence

The Wi-Fi 6E router market size was valued at USD 2.23 billion in 2025 and estimated to grow from USD 2.42 billion in 2026 to reach USD 5.43 billion by 2031, at a CAGR of 17.54% during the forecast period (2026-2031). Gigabit fiber rollouts, clear regulatory pathways for the 6 GHz band, and the rapid rise of bandwidth-intensive applications have aligned to pull demand forward. Early 6 GHz authorizations in the United States, India, and nine other nations have removed the congestion ceiling that limited 2.4 GHz and 5 GHz networks, enabling high-density campus and smart-city designs at a lower total cost of ownership. Device ecosystems have also matured: by 2025, more than 2,000 WiFi 6E-certified products will be available, making endpoint scarcity a non-issue and shifting vendor competition toward software, security, and cloud management capabilities.

Key Report Takeaways

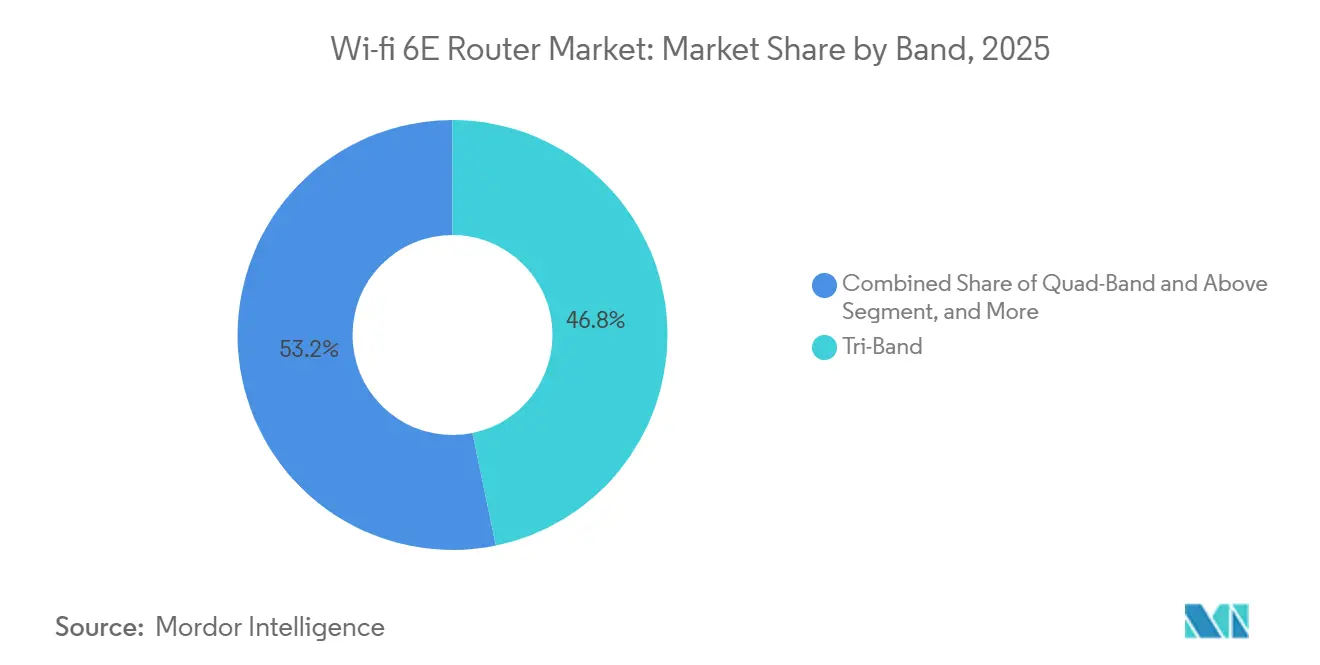

- By band, tri-band models led with 46.78% WiFi 6E router market share in 2025, while quad-band and above units are projected to expand at an 18.43% CAGR through 2031.

- By product type, consumer hardware generated 54.32% of 2025 revenue, whereas carrier-grade and ISP gateways are the fastest-growing segment at a 17.98% CAGR to 2031.

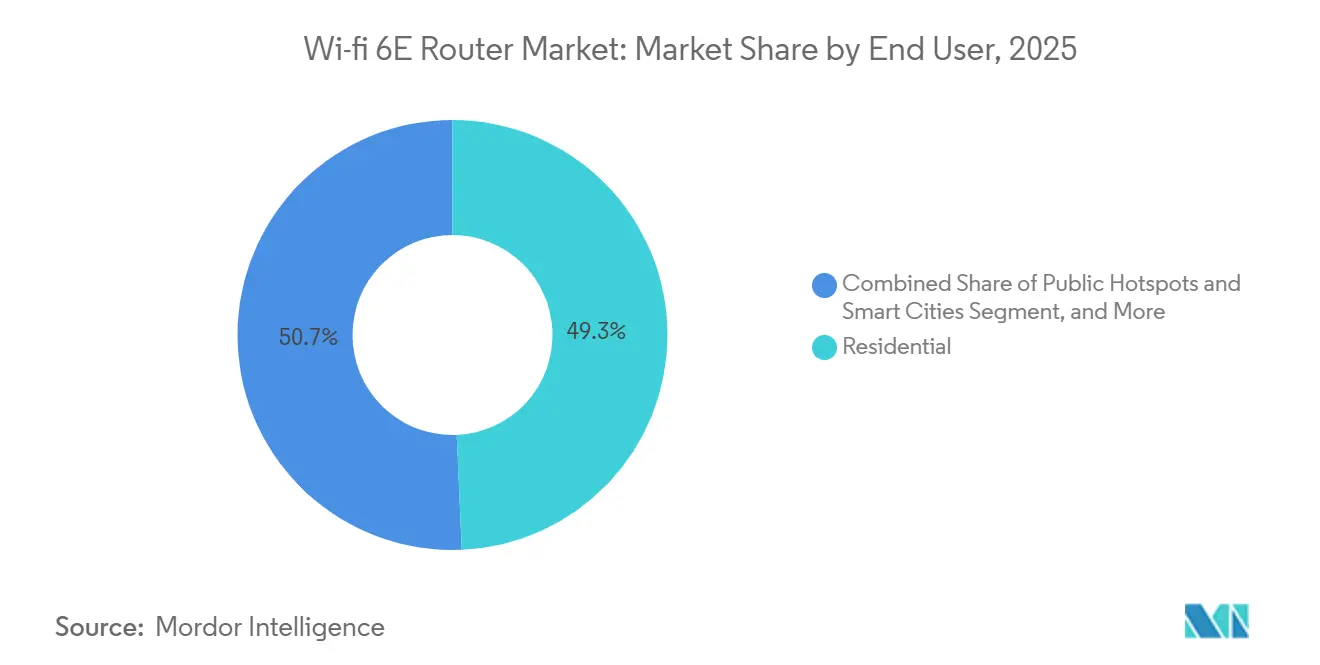

- By end user, residential deployments accounted for 49.32% of demand in 2025, yet public hotspots and smart-city installations are forecast to advance at a 19.64% CAGR over 2026-2031.

- By sales channel, online retail captured 41.41% of 2025 sales, and direct OEM or ODM agreements are poised to rise at an 18.54% CAGR to 2031.

- By geography, Asia-Pacific dominated with 37.44% revenue share in 2025, while the Middle East is expected to be the fastest-growing region at a 20.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wi-fi 6E Router Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of Gigabit Broadband Subscriptions | +4.2% | Global focus on North America, Europe, and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Enterprise Migration Toward Hybrid Work Models | +3.8% | North America, Europe, and Asia-Pacific enterprise hubs | Medium term (2-4 years) |

| Rapid Growth of WiFi 6E-Certified End-Devices | +3.5% | Global, led by North America and Asia-Pacific consumer markets | Short term (≤ 2 years) |

| Spectrum Liberalisation in 6 GHz Band by Regulators | +3.1% | North America, India, select Middle East and Asia-Pacific markets | Medium term (2-4 years) |

| Energy-Efficient Target Wake Time Adoption in IoT | +1.6% | Global smart home and industrial IoT | Long term (≥ 4 years) |

| Increasing Support for WPA3 Security Standard | +1.3% | Global, driven by enterprise and government mandates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosion Of Gigabit Broadband Subscriptions

Fiber-to-the-home penetration crossed critical thresholds in 2025, with operators in North America, Europe, and Asia-Pacific deploying symmetrical multi-gigabit services that render legacy Wi-Fi 5 routers a bottleneck. The projection of 626.9 million Wi-Fi 6E devices shipped in 2025 underscores the demand-side pull as consumers upgrade to hardware capable of saturating gigabit links. What matters strategically is the shift in ISP business models: rather than treating routers as commoditized customer-premises equipment, telcos now bundle premium Wi-Fi 6E gateways with fiber subscriptions to differentiate service tiers and reduce churn.[1]Federal Communications Commission, “Unlicensed Use of the 6 GHz Band,” fcc.gov This creates a flywheel effect: higher broadband speeds justify router upgrades, which in turn drive incremental revenue from value-added services such as parental controls and network security subscriptions. The implication for vendors is clear: partnerships with tier-1 ISPs unlock predictable volume, but also compress margins unless differentiated through software-defined networking features that enable operators to remotely optimize performance and troubleshoot issues without truck rolls.

Enterprise Migration Toward Hybrid Work Models

Hybrid work arrangements have entrenched themselves as the default operating model for knowledge workers, compelling enterprises to architect home-office connectivity with the same rigor previously reserved for corporate campuses. The reported 81.6 million Wi-Fi 6E access points shipped in 2025 indicate strong demand from distributed workforces requiring low-latency video conferencing and secure VPN tunneling.[2]Wi-Fi Alliance, “Wi-Fi 6E Certification List and Market Projection,” wi-fi.org The second-order insight involves the bifurcation of enterprise procurement: large corporations are standardizing on carrier-grade routers with centralized management consoles, while small and medium-sized businesses are gravitating toward consumer-grade hardware that offers enterprise-class security at prosumer price points. This bifurcation creates whitespace for vendors that can bridge the gap by offering cloud-managed platforms with zero-touch provisioning and role-based access controls, yet priced competitively enough to win SMB deals. Regulatory frameworks such as GDPR and emerging data-localization mandates further amplify demand for routers with built-in encryption and audit-logging capabilities, particularly in Europe and Asia-Pacific markets where compliance penalties are material.

Rapid Growth of Wi-Fi 6E Certified End-Devices

The certification of over 2,000 devices for 6 GHz operation by 2025, representing a 22% year-over-year increase, signals ecosystem maturity. Smartphones, tablets, laptops, and smart TVs now routinely ship with tri-band radios, eliminating the chicken-and-egg dilemma that constrained earlier Wi-Fi generations. The strategic implication is that router vendors can no longer rely on device scarcity to justify delayed product launches. Buyers now treat 6 GHz support as a baseline requirement, and vendors lagging certification pipelines risk losing shelf space to faster-moving competitors. The proliferation of Wi-Fi 6E endpoints also enables new use cases such as wireless VR headsets and 8K video streaming, which were impractical on congested 5 GHz channels. This shifts the value proposition from incremental speed improvements to tangible user experience gains, allowing retailers and ISPs to justify premium pricing and drive upgrades from Wi-Fi 5 hardware.

Spectrum Liberalisation in 6 GHz Band by Regulators

Regulatory momentum accelerated in 2024 and 2026, with the FCC authorizing very-low-power devices across the entire 6 GHz band in December 2024 and subsequently approving standard-power devices in January 2026. India followed suit in January 2026, de-licensing the 5,925-6,425 MHz range, while the United Kingdom’s Ofcom advanced consultations on upper 6 GHz sharing models. These policy shifts unlock 1,200 MHz of contiguous spectrum, more than double the capacity available in 5 GHz, enabling routers to operate 160 MHz-wide channels with minimal interference. The second-order effect is geopolitical fragmentation.[3]Department of Telecommunications, Government of India, “De-licensing of 6 GHz Spectrum,” dot.gov.in Markets that delay 6 GHz authorization risk falling behind, as vendors prioritize R&D and go-to-market investments in jurisdictions with clear regulatory frameworks. For multinational enterprises, this creates procurement complexity. Hardware certified for U.S. or Indian markets may not comply with European or Latin American power limits, forcing IT teams to maintain multiple SKU inventories and increasing the total cost of ownership.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Constraints of High-end Chipsets | -2.4% | Global, with acute pressure in North America and Europe due to lead-time volatility | Short term (≤ 2 years) |

| High Average Selling Price Versus Wi-Fi 5 Routers | -1.9% | Global, particularly in price-sensitive Asia-Pacific and South America markets | Medium term (2-4 years) |

| Interference with Fixed Satellite Services in 6 GHz | -0.9% | Europe, select Middle East markets, and parts of South America | Long term (≥ 4 years) |

| Limited Consumer Awareness Outside Tier-1 Economies | -0.7% | South America, Africa, and tier-2/tier-3 cities in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Constraints of High-end Chipsets

Wi-Fi 6E routers depend on advanced silicon from a concentrated supplier base, Broadcom, Qualcomm, and MediaTek, whose production schedules remain vulnerable to capacity constraints at Taiwan Semiconductor Manufacturing Company and geopolitical tensions in East Asia. Analysis indicates that connectivity integrated circuits are forecast to grow at an 11.6% CAGR, yet this growth lags data-center and automotive semiconductor demand, suggesting that foundry allocation decisions could periodically constrain supply to the WLAN market. The strategic risk is that chipset shortages compress vendor margins. Router manufacturers must either accept longer lead times, thereby risking market-share loss to competitors with stronger supply agreements, or pay spot-market prices.

High Average Selling Price Versus Wi-Fi 5 Routers

Wi-Fi 6E routers command price premiums of 30% to 50% over equivalent Wi-Fi 5 models, a gap that narrows adoption in price-sensitive segments and geographies where broadband speeds do not yet justify the incremental cost. The challenge is compounded by consumer confusion: many buyers perceive Wi-Fi 6 and Wi-Fi 6E as interchangeable, undermining vendors' ability to articulate the value of 6 GHz access. This awareness deficit is most acute in South America, Africa, and tier-2 cities across Asia-Pacific, where retail staff lack technical training and point-of-sale materials fail to demonstrate tangible benefits such as reduced latency in multi-device households. The implication for go-to-market strategy is that vendors must invest in channel education and in-store demonstration units that showcase real-world performance deltas, such as uninterrupted 4K streaming during peak usage hours, rather than relying on abstract specifications that resonate only with early adopters. Absent such investments, price-sensitive buyers will default to cheaper Wi-Fi 5 alternatives, deferring the market's transition to 6 GHz and prolonging the payback period for vendors' R&D expenditures.[4]Ofcom, “Consultation on Upper 6 GHz Spectrum Sharing,” ofcom.org.uk

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Band: Tri-Band Leads While Quad-Band Builds Momentum

Tri-band devices held 46.78% WiFi 6E router market share in 2025, validating their position as the default choice for mesh backhaul at a price point most households accept. In dense urban apartments, one tri-band node can fully saturate a gigabit fiber link, so incremental spending on additional radios brings little extra benefit. Quad-band and above models are forecast to expand at an 18.43% CAGR because enterprises, gamers, and content creators value the redundancy that two independent 6 GHz or 5 GHz radios provide. Markets that authorize only the lower 6 GHz block, such as India, narrow the real-world advantage of quad-band hardware, slowing adoption but not eliminating demand.

Strong device support also matters: as smartphones and laptops ship with multi-radio chipsets, households with ten or more active clients begin to notice the load-balancing advantage of an extra 6 GHz channel. Tri-band routers simplify inventory for retailers and ISPs, while quad-band units appeal to power users seeking future-proof capacity for AR, VR, and 8K streaming. Vendors, therefore, keep parallel SKU lines, price tri-band for mass upgrade cycles, and position quad-band as a premium tier that safeguards performance when dozens of clients connect simultaneously. This bifurcated strategy expands the WiFi 6E router market, boosting market size across both value and high-end price bands, helping manufacturers defend margins even as silicon costs fall. The approach also cushions supply-chain risk because chipset allocations can be shifted between tri- and quad-band models to match regional spectrum policies. Over the forecast window, continued spectrum liberalization will gradually tilt share toward quad-band, but tri-band is expected to remain the volume leader through 2031.

By Product Type: Consumer Dominates As Carrier Gateways Accelerate

Consumer hardware accounted for 54.32% of 2025 revenue, driven by thriving e-commerce and a large base of WiFi 5 replacements. Carrier-grade gateways, however, are the fastest-growing slice at a 17.98% CAGR, as telcos bundle WiFi 6E to differentiate multi-gig services. Enterprise-class routers continue to serve campuses but face longer refresh cycles that temper near-term growth.

Recurring software revenues attached to carrier gateways, including parental controls, security overlays, and remote diagnostics, shift profit pools from one-time hardware sales to multi-year service contracts. Vendors that secure ISP design wins effectively lock in volume, underpinning the trajectory of the WiFi 6E router market while balancing thinner hardware margins with annuity income streams.

By End User: Residential Still Largest, Smart-City Demand Surges

Residential networks represented 49.32% of demand in 2025 as hybrid work, 4K streaming, and smart-home proliferation taxed legacy routers. Public hotspots and smart cities are projected to grow at a 19.64% CAGR, catalyzed by municipal broadband and autonomous-vehicle corridors that require low latency and outdoor coverage. Small businesses lean toward prosumer gear, while large enterprises adopt controller-based architectures that extend refresh cycles.

Increasing outdoor 6 GHz allowances following the FCC’s 2026 ruling significantly enhance campus WiFi performance, delivering speeds and reliability comparable to 5 GHz deployments but with the added advantage of cleaner spectrum. This regulatory shift enables universities, stadiums, and municipal networks to expand coverage outdoors without congestion, supporting hybrid work, streaming, and smart-city applications. Collectively, these factors strengthen the WiFi 6E router market, ensuring robust growth across both consumer and enterprise segments.

By Sales Channel: Online Retail Leads, Direct OEM Contracts Expand

Online platforms captured 41.41% of 2025 WiFi 6E router sales, benefiting from comparison tools, fast delivery, and pandemic-driven online shopping habits. Direct OEM and ODM agreements are forecast to grow at an 18.54% CAGR as enterprises pursue bulk campus upgrades, and ISPs bypass distributors to control firmware and branding. Price transparency compresses margins, pushing vendors toward software, cloud services, and subscriptions to sustain competitiveness.

For high-volume OEM deals, customization costs are offset by predictable demand, stabilizing cash flows, and supporting long-term growth. Vendors increasingly rely on subscription services, cloud management, and bundled software features to differentiate beyond raw throughput. This shift balances thinner hardware margins with recurring revenue streams, ensuring sustainable profitability. Together, these dynamics reinforce the overall expansion of the WiFi 6E router market across consumer, enterprise, and carrier segments.

Geography Analysis

Asia-Pacific commanded 37.44% revenue in 2025, propelled by fiber-to-the-home expansion in China, India, and Southeast Asia. India’s January 2026 de-licensing of the lower 6 GHz band unlocks a vast residential and campus market, while China leverages its ODM base to deliver competitively priced hardware for domestic and Belt-and-Road destinations. Regional risk lies in potential trade friction that may split supply chains and certification regimes.

North America remains a replacement market but benefits from the FCC’s 2026 standard-power approval, which enables outdoor WiFi 6E for municipal WiFi and stadiums, broadening the addressable use cases. Satellite coexistence debates temper Europe’s adoption; Ofcom’s ongoing consultation keeps upper-6 GHz clarity in limbo through 2027, compelling vendors to ship multiple SKUs and slowing public-sector rollouts.

The Middle East, forecast to grow at 20.11% CAGR, leverages Vision 2030 agendas in Saudi Arabia and the United Arab Emirates that mandate smart-city connectivity. South America and Africa trail in broadband penetration, yet tier-1 cities show early demand for mid-priced tri-band models. Tailored regional portfolios, premium carrier gateways in the Gulf, value tri-band kits in South America, optimize the WiFi 6E router market penetration across diverse economic profiles.

Competitive Landscape

The WiFi 6E router market features moderate fragmentation: incumbents such as Cisco, Netgear, and ASUS battle Chinese ODMs including TP-Link, Xiaomi, and Huawei, while specialists like Ubiquiti serve prosumers. Certification pipelines dictate time-to-market; with more than 2,000 WiFi 6E-certified devices available, hardware differentiation has tightened, and vendors now compete on firmware cadence, AI-driven channel optimization, and cloud subscription bundles.

Carrier-grade gateways offer a strategic beachhead. ISPs require remote-management hooks and branded firmware, favoring vendors with robust R&D and support teams. Outdoor-rated routers gained momentum after the FCC’s 2026 ruling, opening a niche for ruggedized designs in stadiums and municipal WiFi. Supply-chain resilience further separates players; vertically integrated Chinese manufacturers that design their own chipsets face fewer shortages, challenging Western brands dependent on external fabs.

Overall, software ecosystems, subscription services, and ISP partnerships serve as defensible moats, while pure-play hardware speed is increasingly commoditized. Vendors unable to layer security, parental controls, or analytics risk margin erosion as price transparency rises in online channels.

Wi-fi 6E Router Industry Leaders

TP-Link Technologies Co., Ltd.

Netgear, Inc.

ASUSTeK Computer Inc.

Huawei Technologies Co., Ltd.

D-Link Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The FCC authorized standard-power 6 GHz devices, enabling outdoor WiFi 6E for municipal and stadium networks.

- January 2026: India’s Department of Telecommunications de-licensed 5,925-6,425 MHz for unlicensed use, accelerating enterprise and residential adoption.

- December 2025: The FCC permitted very-low-power operation across the entire 6 GHz band, catalyzing early indoor deployments.

- January 2025: Wi-Fi Alliance certified over 2,000 6 GHz devices, up 22% year over year, indicating ecosystem maturity and accelerated router replacement cycles.

Global Wi-fi 6E Router Market Report Scope

The Wi-Fi 6E router market comprises the development, production, and commercialization of wireless routers operating in the 6 GHz spectrum, extending Wi-Fi 6 capabilities to deliver higher bandwidth, lower latency, and reduced interference. It includes consumer, enterprise, and carrier-grade routers that enable high-density connectivity for applications such as streaming, gaming, hybrid work, and smart infrastructure, along with associated software, cloud management platforms, and value-added services.

The Wi-Fi 6E Router Market Report is Segmented by Band (Tri-Band, Dual-Band, and Quad-Band+), Product Type (Consumer, Enterprise, and Carrier-Grade), End User (Residential, SMB, Enterprise, and Public Hotspots), Sales Channel (Online, Retail, Resellers, and Direct OEM), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are in Value (USD).

| Tri-Band (2.4 GHz, 5 GHz, 6 GHz) |

| Dual-Band (2.4 GHz and 6 GHz) |

| Quad-Band and Above |

| Consumer-Grade Routers |

| Enterprise-Class Routers |

| Carrier-Grade and ISP Gateways |

| Residential |

| Small and Medium-Sized Businesses |

| Large Enterprises and Campuses |

| Public Hotspots and Smart Cities |

| Online Retail |

| Consumer Electronics Stores |

| Value-Added Resellers |

| Direct OEM / ODM Sales |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Band | Tri-Band (2.4 GHz, 5 GHz, 6 GHz) | |

| Dual-Band (2.4 GHz and 6 GHz) | ||

| Quad-Band and Above | ||

| By Product Type | Consumer-Grade Routers | |

| Enterprise-Class Routers | ||

| Carrier-Grade and ISP Gateways | ||

| By End User | Residential | |

| Small and Medium-Sized Businesses | ||

| Large Enterprises and Campuses | ||

| Public Hotspots and Smart Cities | ||

| By Sales Channel | Online Retail | |

| Consumer Electronics Stores | ||

| Value-Added Resellers | ||

| Direct OEM / ODM Sales | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the Wi-Fi 6E router market?

The Wi-Fi 6E router market size reached USD 2.42 billion in 2026.

How fast is the WiFi 6E router market projected to grow?

The market is expected to rise at a 17.54% CAGR from 2026 to 2031, supported by gigabit broadband and 6 GHz spectrum liberalization.

Which band configuration leads global sales?

Tri-band models held 46.78% WiFi 6E router market share in 2025, while quad-band units are the fastest-growing tier.

Which region dominates revenue?

Asia-Pacific accounted for 37.44% of 2025 revenue, thanks to extensive fiber-to-the-home rollouts.

Why are carrier-grade gateways growing so quickly?

Telcos bundle WiFi 6E gateways with multi-gig fiber plans to cut churn and upsell security services, driving a 17.98% CAGR in the segment.

What is the biggest supply-side risk?

Dependence on a concentrated chipset supply chain means geopolitical or allocation shocks could delay router production.

Page last updated on: