Gin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 24.51 Billion |

| Market Size (2031) | USD 30.87 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

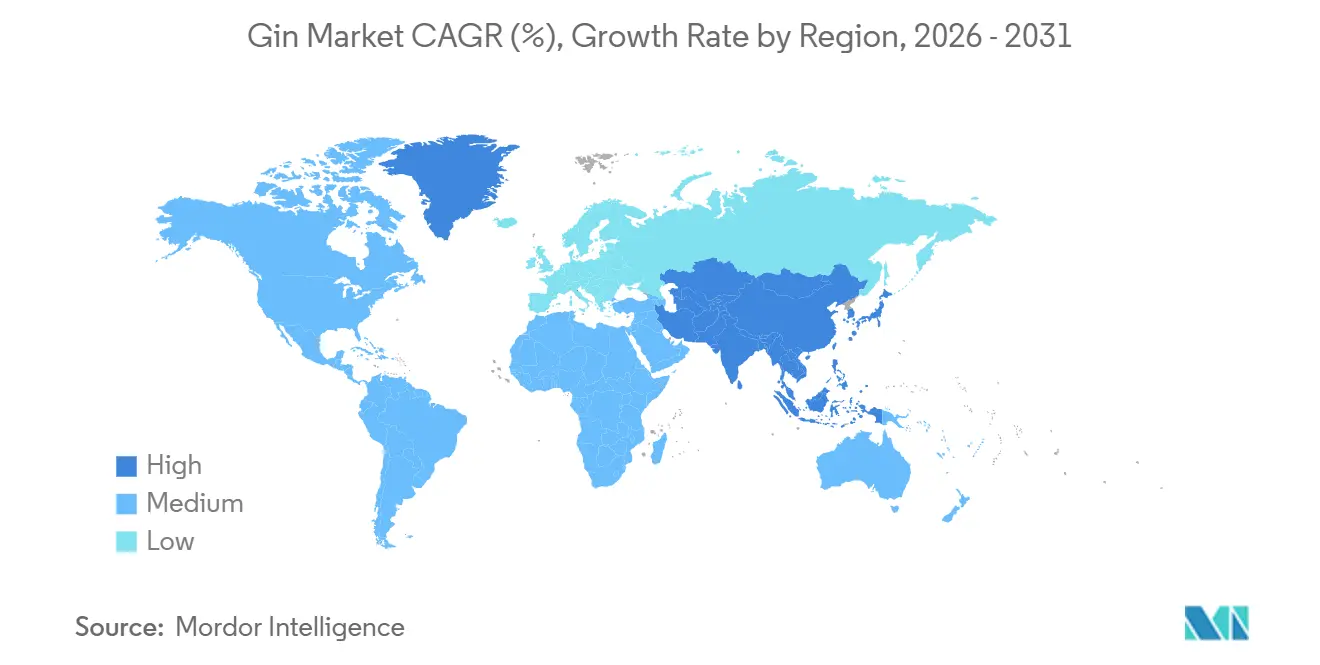

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

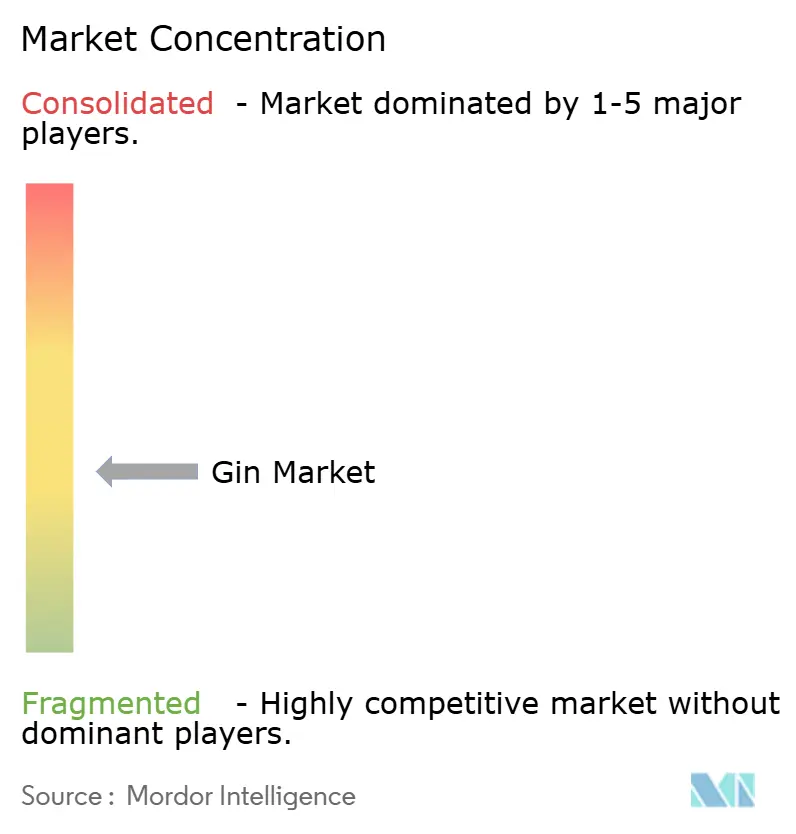

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gin Market Analysis by Mordor Intelligence

The gin market size is projected to be USD 23.56 billion in 2025, USD 24.51 billion in 2026, and reach USD 30.87 billion by 2031, growing at a CAGR of 4.72% from 2026 to 2031. This growth trajectory is attributed to several factors, including the rising demand for premium-quality products, the revival of cocktail culture, and increased experimentation with botanical ingredients. These drivers collectively outweigh the influence of health-conscious consumption trends, which have been gaining momentum in recent years. However, the market faces potential challenges, such as the advisory issued by the United States Surgeon General in January 2025, which links alcohol consumption to approximately 20,000 annual cancer-related deaths and recommends the inclusion of warning labels. Ireland is set to implement mandatory warning labels on alcohol products starting in May 2026, which could further impact market dynamics.

Key Report Takeaways

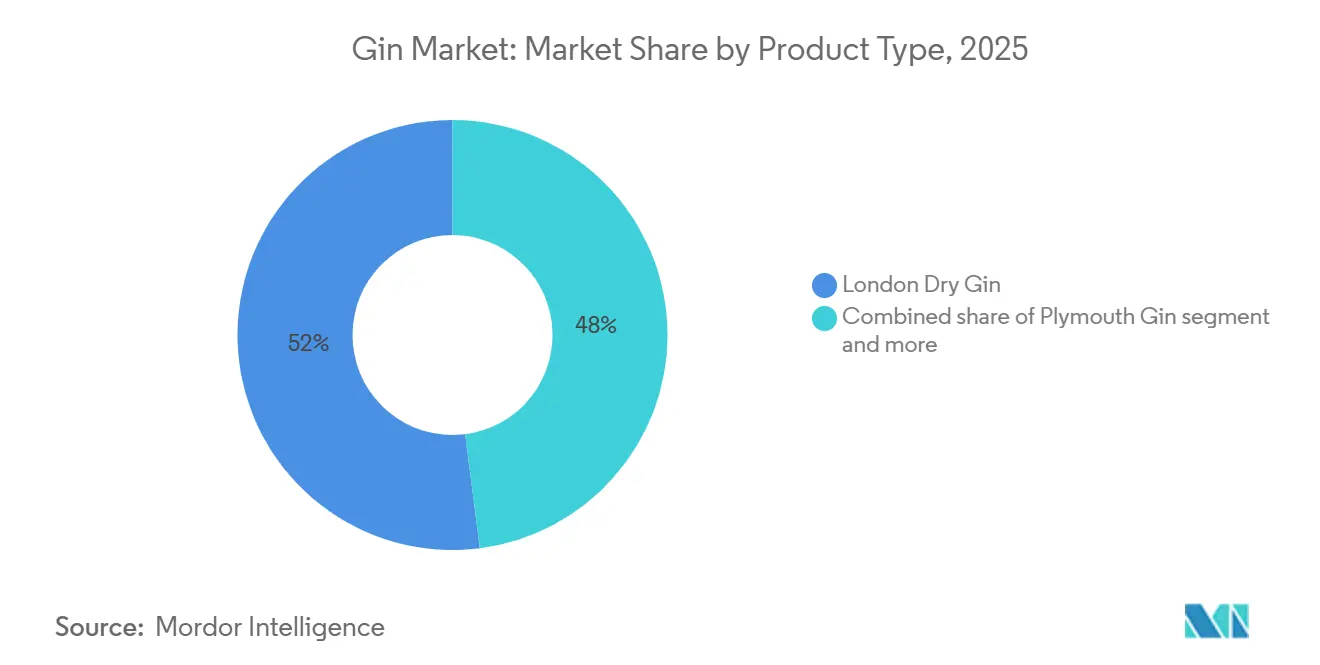

- By product type, London Dry Gin commanded 52.02% share in 2025, while Old Tom Gin is forecast to expand at a 5.12% CAGR through 2031.

- By consumer gender, men accounted for 70.72% of 2025 consumption; the women segment is projected to advance at a 5.51% CAGR through 2031.

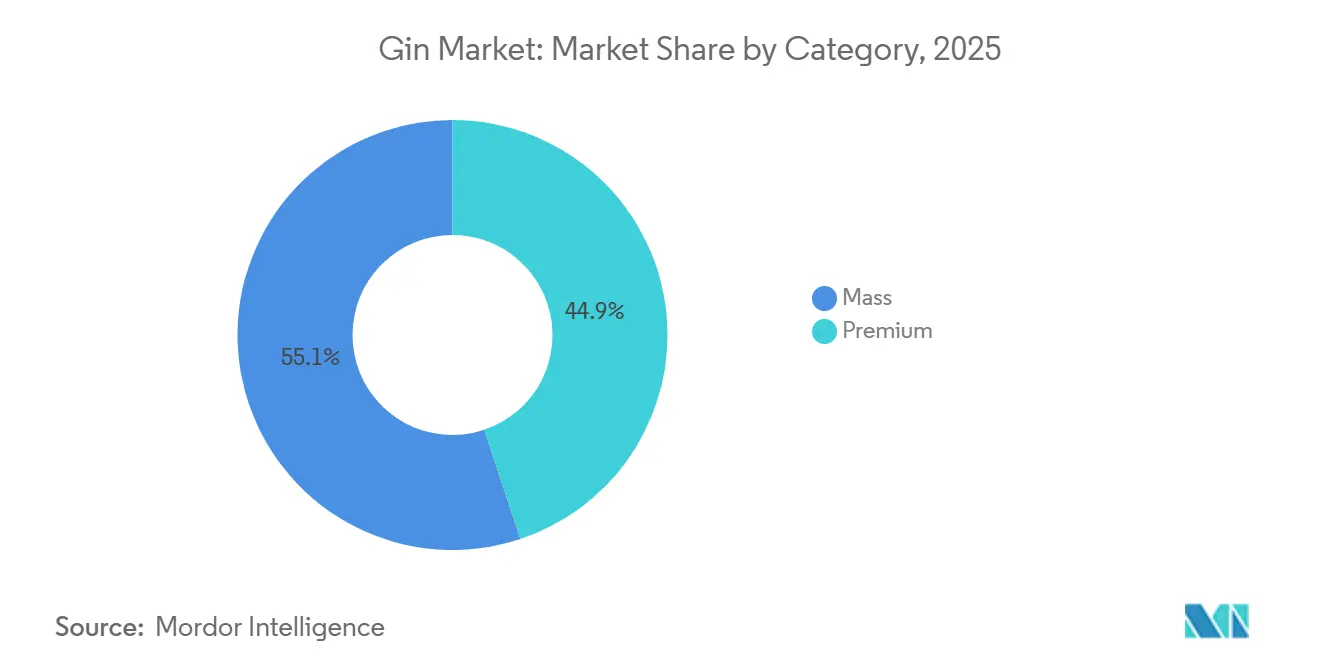

- By category, mass labels held 55.13% share in 2025, whereas premium gin is expected to grow at a 5.78% CAGR through 2031.

- By distribution channel, off-trade captured 59.91% revenue in 2025, while on-trade outlets are poised for a 5.01% CAGR over the forecast period.

- By geography, Europe contributed 44.01% of 2025 revenue as the leading region, and Asia-Pacific is set to rise at a 5.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization trend boosts demand for craft and small-batch gin | +1.5% | Global, with concentrated activity in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rising cocktail culture increases gin usage in bars and homes | +1.2% | Global, with early gains in United States, United Kingdom, Australia, and metropolitan Southeast Asia | Short term (≤2 years) |

| Innovation in botanicals creates distinctive flavor profiles and consumer excitement | +1.0% | Global, notably Argentina, Brazil, Australia, Japan, United Kingdom | Long term (≥4 years) |

| Low-ABV and alcohol-free gin appeal to mindful drinkers | +0.8% | North America and Europe lead, spillover to Asia-Pacific | Medium term (2-4 years) |

| Experiential tourism at distilleries enhances brand loyalty | +0.5% | Australia, Scotland, Japan, South America, select United States regions | Long term (≥4 years) |

| Flavoured gins bring new entrants from non-traditional spirit drinkers | +0.7% | Global, particularly North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Premiumization trend boosts demand for craft and small-batch gin

Small-batch distilleries are achieving premium pricing by positioning gin as a product that reflects its place of origin rather than a standardized neutral grain spirit. Suntory has announced a significant investment to expand Yamazaki’s gin production, targeting international markets where Japanese botanical flavor profiles command higher prices compared to traditional London Dry styles. Similarly, Pernod Ricard has increased operations at its Miltonduff distillery in Scotland to enhance gin production, focusing on super-premium offerings to offset declining volumes in the mainstream vodka category. In the United States, Middle West Spirits has expanded its production capacity and is utilizing direct-to-consumer channels to improve profit margins by retaining more value rather than sharing it with distributors. Meanwhile, Argentina’s craft gin industry has experienced rapid growth, with a notable increase in both the number of brands and consumption. Producers in Argentina are leveraging unique native botanicals, such as yerba mate, to differentiate themselves in global competitions. Additionally, Victorian distillers have emerged as significant contributors to this trend, accounting for 60.1% of the region's spirits export value through gin. This highlights the substantial economic impact of craft spirits in global markets.

Rising cocktail culture increases gin usage in bars and homes

Martini consumption in London's leading bars has grown notably in recent years, reflecting a shift from the traditional preference for vodka and strengthening Tanqueray's position in the on-trade channel relative to Bombay Sapphire. This resurgence, as noted by The Economist, is driven by innovative bartenders experimenting with variations such as dirty, Gibson, and espresso styles, redefining the Martini as a versatile and creative cocktail rather than a fixed recipe. Additionally, the introduction of smaller “mini-Martini” servings has gained traction in both the United States and the United Kingdom, enabling consumers to explore a wider variety of flavors while maintaining a balanced drinking experience. At the same time, the trend of at-home cocktail preparation, which gained prominence during pandemic lockdowns, continues to expand, supported by e-commerce platforms offering premium tonic waters and garnish kits. In Italy, the retail channel remains a key driver of gin sales, with online purchases steadily increasing. Similarly, growing online interest in gin in Thailand aligns with Bangkok's rise as a vibrant cocktail-tourism hub, featuring both locally distilled spirits and imported London Dry gins. Meanwhile, Spain's strong tourism industry, with an anticipated 95 million visitors in 2024, serves as a significant growth driver for on-premise gin sales [2]Source: U.S. Department of Agriculture, “Spain Hospitality Sector Update 2024,” fas.usda.gov.

Innovation in botanicals creates distinctive flavour profiles and consumer excitement

Craft distilleries are utilizing native botanicals to bypass multinational distribution networks and establish retail presence through authentic, origin-focused narratives. In Argentina, Príncipe de los Apóstoles gained international recognition at a prominent global spirits competition by highlighting the unique flavors of Patagonian juniper and pink grapefruit. Similarly, Bosque received acclaim in London for its blend of calafate berry and Andean mint. In Chile, Gin Elemental enhanced its premium positioning by incorporating botanicals from the Atacama Desert, leveraging terroir to justify higher retail prices compared to traditional imported gins. In Japan, Ki No Bi distillery expanded its production capacity to meet growing European demand for its distinctive profiles infused with yuzu, sansho pepper, and hinoki wood, setting it apart from conventional offerings. Australia’s Four Pillars introduced its Bloody Shiraz variant, which integrates whole grapes, achieved carbon-neutral certification, and attracted an increasing number of visitors engaging with the brand experience. Additionally, Pernod Ricard’s investment in Brazil’s Amázzoni Gin, featuring Amazonian botanicals such as jambu and cumaru, underscores a broader trend of targeting urban consumers who prioritize authenticity and provenance as key factors influencing value perception.

Low-ABV and alcohol-free gin appeal to mindful drinkers

Diageo's acquisition of Ritual Zero Proof in September 2024, the leading non-alcoholic spirit brand in the United States, highlights the growing recognition among industry players that abstinence occasions now represent structural demand rather than a niche preference. The United States non-alcoholic spirits market experienced a 31% CAGR over the past five years, driven by consumers participating in initiatives like Dry January and extending their moderation habits beyond the campaign month. In 2024, Beefeater introduced a 0.0% ABV variant, replicating its botanical profile through vacuum distillation, which preserves juniper and citrus notes without ethanol. In Germany, a Hamburg court ruling in July 2025 determined that alcohol-free alternatives cannot use protected spirit names, requiring brands to adopt terms such as "botanical spirit," which has fragmented category recognition. Additionally, the United Kingdom's Advertising Standards Authority issued guidance in May 2024 mandating that non-alcoholic gin advertisements avoid implying health benefits, restricting marketing to focus on taste and occasion messaging. In Australia, the National Health and Medical Research Council recommends a maximum of ten standard drinks per week. This has led retailers to stock low-ABV gins at 20% ABV, compared to the traditional 40%, catering to health-conscious consumers who prefer reduced alcohol consumption over complete abstinence [1]Source: National Health and Medical Research Council, "Australian guidelines to reduce health risks from drinking alcohol," nhmrc.gov.au.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns about alcohol reduce per-capita spirit consumption | -1.0% | Global, particularly acute in United Kingdom, United States, Australia | Long term (≥4 years) |

| Stringent advertising restrictions limit promotional options | -0.6% | Europe (United Kingdom, Ireland, Germany), North America | Short term (≤2 years) |

| Complex licensing processes deter new distillery entrants | -0.4% | North America, Europe, select Asia-Pacific markets | Long term (≥4 years) |

| Anti-alcohol campaigns discourage frequent consumption | -0.5% | Global, concentrated in United Kingdom, United States, Australia, Nordic countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health concerns about alcohol reduce per-capita spirit consumption

The United States Surgeon General has issued an advisory linking alcohol consumption to cancer-related deaths, alongside a proposal to implement mandatory warning labels. This approach has previously demonstrated effectiveness in reducing tobacco use. Ireland is poised to become the first country to mandate explicit cancer warnings on alcoholic beverages, a measure that industry groups predict may lead to reduced sales volumes due to diminished visibility on retail shelves. In the United Kingdom, an increase in alcohol-related fatalities has prompted the Chief Medical Officer to strengthen national guidelines on responsible drinking, encouraging on-trade establishments to incorporate these recommendations into their menus. The country’s gin category has experienced a significant decline, influenced by economic challenges and shifting public health narratives that increasingly frame spirits as occasional indulgences rather than regular purchases. On a global scale, the World Health Organization continues to highlight the substantial health and social costs of alcohol consumption, advocating moderation as a critical element of preventive healthcare and long-term well-being [3]Source: World Health Organization, “Alcohol,” who.int.

Stringent advertising restrictions limit promotional options

Washington, D.C. has introduced restrictions on issuing new distillery licenses in areas with a high concentration of producers. These measures include requiring community agreements for distillery pubs and limiting vertical integration, which collectively extend pre-production timelines and significantly increase legal and consulting costs. Under the United States Federal Alcohol Administration Act, producers of gin made through continuous distillation must disclose the proportion of neutral spirits on their labels. However, smaller micro-distilleries using pot stills are exempt from this requirement, creating a compliance framework that inadvertently benefits small-scale craft producers over larger industrial blenders. In the United Kingdom, obtaining a distillery license requires securing planning permission, completing environmental impact assessments, and receiving local authority approval. This process is lengthy and capital-intensive, often discouraging entrepreneurs without substantial financial resources. In Australia, the excise duty on spirits imposes a significant cost burden per bottle, even before accounting for production and distribution expenses. This creates a competitive advantage for larger operators with advanced hedging and financing capabilities. In India, under the India and United Kingdom Free Trade Agreement, duties on gin imports from the United Kingdom are being gradually reduced. However, the fragmented state-level licensing structure in India remains a challenge. Individual jurisdictions often require separate authorizations for production, bottling, and retail, further delaying overall market entry timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Old Tom Revival Challenges London Dry Hegemony

London dry gin accounted for 52.02% of the market share by 2025, supported by the extensive global distribution networks of brands such as Tanqueray, Bombay Sapphire, and Beefeater. In comparison, old tom gin was expected to grow at a compound annual growth rate (CAGR) of 5.12% through 2031, driven by its increasing use by craft bartenders in pre-Prohibition cocktail recipes. The resurgence of old tom gin was closely tied to the revival of historical cocktail culture. Bartenders in cities such as New York, London, and Sydney incorporated it into drinks like the Martinez and Tom Collins, highlighting its malt-forward sweetness. This created a niche market that remained largely untapped by mass producers. Old tom gin occupied a unique position within the premium gin market, supported by a limited number of brands globally. It was primarily utilized by craft distilleries seeking to differentiate themselves from competitors and avoid the intense price competition prevalent in the London dry gin segment.

Plymouth gin benefited from its protected geographic indication (PGI) status, which restricted its production to the city of Plymouth in England. This exclusivity appealed to consumers who valued authenticity and heritage, enabling the brand to command a premium price compared to standard London dry gins. However, its sales volume was inherently limited due to its single-distillery production model, which restricted scalability. Other gin varieties, including navy strength gin, sloe gin, and regional types like genever, represented the remaining segments of the market. Among these, navy strength gin gained significant popularity, particularly among cocktail enthusiasts who appreciated its higher alcohol content. This elevated alcohol content enhanced the flavor profile of cocktails such as the Martini, offering a more robust and intense experience. These niche gin varieties continued to attract a dedicated consumer base, contributing to the overall diversity and growth of the gin market.

By End User: Women Segment Outpaces Men Despite Lower Baseline

Men accounted for 70.72% of total consumption in 2025, driven by historical preferences for spirits and higher per-capita intake within this demographic. In contrast, women's consumption grew at a compound annual growth rate (CAGR) of 5.51% through 2031. This growth was attributed to brands reformulating products to include lower-alcohol-by-volume (ABV) options and floral botanicals, which aligned with female taste preferences. For example, Diageo's Tanqueray Flor de Sevilla, a blood-orange variant introduced in 2018 and slated for global expansion by 2024, specifically targeted women. The product's packaging highlighted Mediterranean aesthetics instead of traditional naval imagery, a strategy that increased female trial rates by 35% in the United Kingdom's off-trade channels.

Men's consumption remained primarily concentrated in on-trade venues, where the culture of Martini consumption and experimentation with craft cocktails continued to drive frequent visits. However, health campaigns targeting male drinkers, who accounted for 68% of alcohol-related deaths in the United Kingdom, posed challenges that could reduce per-capita intake. These campaigns aimed to raise awareness about the health risks of excessive alcohol consumption, potentially influencing drinking habits within this demographic.

By Category: Premium Gains Share as Mass Defends Volume

Mass gin accounted for 55.13% of the market value in 2025, driven by established brands such as Gordon's, Gilbey's, and Ginebra San Miguel. These brands focused on supermarket promotions and plastic-bottle packaging to maintain sales volumes in price-sensitive markets, including the Philippines and South Africa. These strategies were designed to remain competitive and address the needs of consumers prioritizing affordability and accessibility.

Premium gin was anticipated to grow at a compound annual growth rate of 5.78% through 2031. This growth was largely attributed to craft distilleries leveraging direct-to-consumer sales channels and promoting distillery tourism, which bypassed traditional distributor margins. These strategies enabled premium gin brands to achieve gross profit margins of 60%, significantly higher than the 35% margins typically observed for mass-market brands. In response, mass-market brands introduced flavored line extensions priced 10% to 15% higher than their core products. For example, Pernod Ricard launched Beefeater Pink Grapefruit to attract consumers transitioning from ready-to-drink alcoholic beverages, such as alcopops, while maintaining the sales of its London Dry gin. However, mass-market brands were under growing pressure to reduce profit margins as retailers demanded deeper discounts to offset declining sales volumes caused by health-conscious consumer behavior. To address this issue, companies like Diageo shifted marketing budgets from traditional broadcast advertising to experiential marketing activities, aiming to sustain a premium brand perception.

By Distribution Channel: On-Trade Recovery Outpaces Off-Trade Maturity

Off-trade channels were projected to account for 59.91% of the market value by 2025, driven by pandemic-induced at-home consumption trends and supermarket promotions. These factors increased the United Kingdom's off-trade volume share to 83% by 2024. On-trade venues were anticipated to grow at a CAGR of 5.01% through 2031, supported by the resurgence of Martini and the growing popularity of experiential cocktail bars, which influenced a shift away from work-from-home consumption habits. Within the on-trade segment, Tanqueray held a 24% share, compared to 17% for Bombay Sapphire.

Specialty liquor stores within the off-trade segment benefited from knowledgeable staff who assisted in converting casual browsers into premium buyers. Independent retailers leveraged this advantage to secure exclusive allocations from craft distilleries, which were not available in supermarket chains. Other off-trade channels, including e-commerce, convenience stores, and duty-free outlets, accounted for the remaining share. E-commerce, in particular, grew at an annual rate of 10% in Italy, driven by platforms such as Amazon and Drizly, which offered next-day delivery and subscription-based models.

Geography Analysis

Europe was expected to lead the gin market, contributing 44.01% of the revenue by 2025. This dominance was driven by the United Kingdom's production of 68 million bottles, despite a 29% decline since 2020. Key factors included Spain's thriving gin-and-tonic bar culture and the growing number of craft distilleries in Germany. Major investments, such as Pernod Ricard's EUR 25 million expansion of the Miltonduff distillery and Diageo's planned distribution overhaul in France by July 2024, recovering Tanqueray and Gordon's from the Moët Hennessy Diageo (MHD) joint venture, demonstrated the efforts of leading companies to retain market share against craft competitors. Furthermore, the Netherlands and Belgium capitalized on their genever heritage, positioning gin as a contemporary adaptation of traditional juniper spirits and attracting tourists through distillery museums and tasting experiences. Conversely, Poland and Sweden faced challenges from Nordic alcohol monopolies, which limited retail distribution and enforced minimum pricing. Despite these restrictions, premium gins gained traction in on-trade venues, supported by bartender advocacy that helped navigate state-controlled retail constraints.

The Asia-Pacific region is anticipated to be the fastest-growing segment, with a compound annual growth rate (CAGR) of 5.94% through 2031. China’s gin market is expected to experience robust growth, while Singapore has demonstrated steady performance in recent years. The Philippines remains the largest global market for gin. The Free Trade Agreement between India and the United Kingdom is projected to significantly reduce import tariffs in the coming years, enhancing the presence of British gin brands in India and driving the premium segment’s growth across major cities. In Australia, Asahi Group Holdings has expanded its premium spirits portfolio through the acquisition of Never Never Distillery, while Four Pillars Distillery continues to attract a significant number of visitors annually and has achieved carbon-neutral certification. This reflects the growing focus on sustainability within the spirits industry.

North America, South America, and the Middle East and Africa collectively represent the remaining regional market share, with South America showing particularly strong growth in the craft gin category. The region’s momentum is driven by a rapidly expanding distillery base and increasing consumer demand for premium and locally inspired products. In Brazil, the growing craft spirits movement is leading to higher production volumes and a shift toward premium pricing as consumers prioritize quality and authenticity. Argentina is also experiencing a rise in brand launches and consumption, supported by the use of unique native botanicals such as yerba mate and Patagonian juniper. These distinctive ingredients have gained international recognition, boosting the export appeal of locally produced gin.

Regulatory Landscape

Gin regulation is shaped by taxes, labeling rules, and channel controls that vary by jurisdiction and directly affect pricing and route-to-market. In the United States, the Federal Alcohol Administration Act sets labeling standards for gin, including disclosures on production methods for certain distillation styles, while local constraints such as Washington, DC, licensing limits can slow new distillery permissions. In May 2024, the United Kingdom Advertising Standards Authority issued guidance that limited health-related messaging for non-alcoholic gin. In Europe, rules enforced by bodies like EFSA require strict labeling and botanical sourcing criteria. Ireland will implement mandatory warning labels on alcohol products starting in May 2026, adding to the compliance burden.

Across Europe, protected designations and marketing controls influence how gin types are named and advertised. A Hamburg court ruling in July 2025 restricted alcohol-free alternatives from using protected spirit names, pushing brands toward descriptors such as botanical spirit. Canada also reflects cross-border compliance costs, as seen in the February 2026 LCBO settlement involving approximately CA$23 million related to local sales and distribution. In India, the India-UK Free Trade Agreement framework continues to shape trade flows for premium gin, making regulatory alignment a key factor for cross-border market access.

Value Chain Analysis

The gin value chain begins with agricultural inputs (neutral spirit feedstocks and botanicals such as juniper, citrus peels, and regionally distinctive ingredients), followed by distillation, blending, maturation where applicable, bottling, packaging, and multi-channel distribution to on-trade and off-trade channels. Global players like Diageo, Bacardi, and Pernod Ricard optimize this chain through centralized procurement, high-throughput bottling, and broad distributor reach. Craft distilleries tend to differentiate through smaller batches, provenance storytelling, and direct-to-consumer channels to protect margins.

Execution downstream depends heavily on route-to-market decisions and footprint optimization. Off-trade and on-trade channels require different activation models, with premium brands leaning on bartender advocacy and experiential programs, while craft producers use distillery tourism and direct-to-consumer sales. Capacity moves show how networks are reshaping: Diageo closed its Amherstburg, Ontario bottling facility in February 2026 under its Accelerate cost program and signed a sale in July 2026, indicating bottling capacity is being reallocated. Pernod Ricard continues to invest in Miltonduff with a EUR 25 million expansion to boost premium gin output, and Bacardi's portfolio actions, including the Teeling Whiskey acquisition, highlight scale advantages that carry into gin-related premiumization and distribution.

Competitive Landscape

The global gin market is highly fragmented, with key players such as Diageo, Pernod Ricard, and Bacardi operating alongside over 400 Argentine craft labels, 202 Brazilian distilleries, and independent producers like Australia's Four Pillars. Many smaller producers bypass traditional distributor networks by utilizing tourism and direct-to-consumer channels. Diageo's acquisition of Ritual Zero Proof in September 2024, a leading non-alcoholic spirit brand in the United States, underscores the increasing demand for abstinence-focused products. Similarly, Pernod Ricard's EUR 25 million investment in expanding Miltonduff and its minority stake in Brazil's Amázzoni Gin highlight the importance of botanical innovation in driving premiumization within the market.

Craft distilleries are utilizing local botanicals to differentiate their products and secure shelf space through origin-based storytelling. For instance, Argentina's Príncipe de los Apóstoles incorporates Patagonian juniper, Japan's Ki No Bi uses yuzu and sansho pepper, and Australia's Four Pillars infuses Shiraz grapes. These strategies allow craft producers to bypass multinational distribution networks and achieve gross margins of 60 percent, compared to 35 percent for mass-market brands. Significant growth opportunities are emerging in the Asia-Pacific region, where India's tariff reductions under the United Kingdom-India Free Trade Agreement and China's projected 20 percent gin market growth in 2024 are attracting new entrants, particularly those without legacy portfolios in whisky or vodka.

Emerging disruptors are leveraging experiential marketing strategies, such as Four Pillars' 200,000 annual visitors, which generate AUD 24 million in direct sales, accounting for 12 percent of its total turnover. Established players are reallocating budgets from traditional advertising to bartender training and on-trade activations to maintain premium positioning despite regulatory restrictions. Technology adoption in the gin market is focused on sustainability certifications and direct-to-consumer platforms. For example, Four Pillars achieved carbon-neutral status in 2022, while Middle West Spirits uses blockchain technology to verify grain provenance. These initiatives appeal to environmentally conscious consumers and help retain margins typically lost to distributor tiers. Vertical integration strategies are also gaining traction among established players. Pernod Ricard's July 2024 transformation of its France distribution network, which recovered Tanqueray and Gordon's from the Moët Hennessy Diageo joint venture, exemplifies efforts to eliminate intermediary costs and enhance market responsiveness. Regulatory compliance, including International Organization for Standardization (ISO) 9001 quality certifications, geographic indication protections for Plymouth Gin, and Ireland's upcoming cancer warning labels in May 2026, imposes fixed costs that favor large-scale operators. However, craft distilleries often circumvent these requirements through exemptions for small-batch production and direct sales, which fall outside retail labeling mandates.

Gin Industry Leaders

-

Diageo plc

-

Bacardi Limited

-

Pernod Ricard SA

-

William Grant & Sons Ltd

-

Davide Campari-Milano NV

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premiumization and provenance-driven gin create opportunity for both multinationals and craft producers, supported by botanical innovation, controlled allocations, and experiences that support premium pricing in on-trade and specialty retail. The evidence in the market includes Pernod Ricard expanding super-premium gin production at Miltonduff and taking a stake in Amázzoni Gin in Brazil, as well as Four Pillars visitor volumes that support direct sales. Across the broader market, premiumization in the United States and Europe continues to shift consumer expectations and commercial positioning.

The Global Premium Gin Market reached a value of 8.7 billion USD in 2026. Channel and geography opportunities are tied to trade policy and travel retail dynamics. The India-UK Free Trade Agreement lowers import duties on British gin and whisky from 150 percent to 75 percent initially, with further reductions over time, which improves access to premium gin in India. European travel retail partnerships, including Pernod Ricard’s collaborations with Gebr. Heinemann, broaden premium portfolio visibility in airports and duty-free nodes. On the regulatory side, Ireland’s 2026 warning-label implementation and ongoing European advertising guidelines keep packaging and claims discipline central to category expansion.

Recent Industry Developments

- July 2026: Launched the 'Something Blue' wedding season campaign for Bombay Sapphire in partnership with Cocktail Courier and Little Words Project. The campaign targets premium gin on-trade and wedding segment. Strengthens premium positioning and direct-to-consumer partner ecosystems for Bombay Sapphire.

- June 2026: Bombay Sapphire Distillery at Laverstoke Mill received Silver recertification from the Wildlife Habitat Council for biodiversity and conservation. The credentialing marks sustainability at production site. Enhances brand legitimacy and premium image through environmental stewardship as a differentiator in premium gin.

- May 2026: Pernod Ricard SA acquired British craft gin brands Cotswolds Distillery and Isle of Harris Distillers for approximately 85 million GBP to expand premium gin portfolio. The acquisition broadens the portfolio and botanicals for consumer choice. Strengthens Pernod Ricard's premium gin position and diversification through craft label assets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the value of gin sold for consumption across on-trade and off-trade channels, measured in USD for a global view. It covers standard gin styles and flavored gin where it is sold and labeled within the gin category.

Scope exclusions: Excludes ready-to-drink cocktails that contain gin and non-alcoholic gin alternatives when they are marketed as alcohol-free spirits.

Segmentation Overview

-

By Product Type

- London Dry Gin

- Plymouth Gin

- Old Tom Gin

- Other Product Types

-

By End User

- Men

- Women

-

By Category

- Mass

- Premium

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Specialty/Liquor Stores

- Others Off-Trade Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to establish the fact base for country-level alcohol context and to check that the demand signals we relied on match what is visible in public records. We leaned on official statistics and trade data to understand how gin moves across borders and how the category is reported over time.

Typical inputs came from sources such as UN Comtrade and the World Bank WITS portal for trade flows, the Alcohol and Tobacco Tax and Trade Bureau (TTB) for category definitions and regulatory references, and national statistics offices for consumer spending and inflation context. We also used trade association publications such as spirits councils for category snapshots, along with company annual reports and investor presentations to understand portfolio exposure and price mix movement. Select paid database subscriptions were used in a limited way for company financials, news and financials, and shipment-level import and export checks to validate the direction and timing of changes. This desk research source list is illustrative, and many other public and paid references were also used to collect data, validate assumptions, and clarify open points.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure-test the desk assumptions and translate volume signals into realistic value outcomes by country and channel. We spoke with a mix of brand owners, distributors, importers, retailers, and on-trade operators across major gin-consuming regions, so gaps on pricing, premium mix, and channel splits could be closed using respondent context rather than only desk estimates. Where inputs disagreed, follow-ups were done with additional respondents who see near-term order patterns and promotions, which helped narrow the final ranges.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | APAC: 48% |

| Mid tier: 50% | Functional/Unit leaders: 30% | EMEA: 30% |

| Smaller Players: 22% | Managers: 58% | Americas: 22% |

Market-Sizing & Forecasting

Market sizing starts with a top-down build where spirits consumption and trade data are used to reconstruct the gin demand pool by geography, then it is filtered through channel shares and price bands. To keep totals realistic, we corroborate them with selective bottom-up approximations such as sampled country price ladders by format, distributor channel checks, and a limited supplier revenue roll-up where disclosures allow it.

Key model inputs include gin volume indicators (for example, nine-liter case trends), on-trade versus off-trade mix, premium and mass share movement, average selling price progression by market, and inflation and currency conversion timing for USD reporting. Regulatory and labeling changes were also tracked because they can shift purchasing behavior and alter pack labeling and portfolio emphasis, which then changes the value mix.

For forecasting, we used scenario analysis supported by simple multivariate relationships between gin value growth, price mix shifts, and channel recovery patterns, and we validated the direction with expert inputs. Where bottom-up signals were incomplete for smaller markets, gaps were handled by using regional benchmarks for channel splits and price bands, then those assumptions were re-checked through targeted follow-up conversations.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, including trade flow direction, reported category trends, and observed pricing behavior in key countries. Large variances were flagged, reworked, and then reviewed again so unusual spikes from currency moves, one-time stock builds, or channel disruptions did not carry into the final series.

A multi-step review is followed before sign-off, including peer checks on assumptions and recalculation of key totals. Reports are refreshed annually, and interim updates are added when material events occur, such as major tax changes or step-changes in pricing. Before delivery, an analyst performs a fresh pass on the latest public updates so clients receive the most current view available.

Mordor Intelligence's Gin Market Size Versus Other Published Estimates

Published gin market estimates often differ even when they refer to the same product, because the counting rules are not always aligned. The biggest swings usually come from what is included in the market basket, how prices are converted into USD, and whether the latest year gets refreshed after new trade and consumption signals appear.

Ready-to-drink gin cocktails sit outside Mordor Intelligence's scope, which is why some published values that bundle mixed drinks, premix cans, and adjacent spirit-based RTDs land above the figure shown here. Other gaps come from using shipment value as a stand-in for consumption value, applying a single global price uplift instead of country price ladders, or keeping an older base year that misses recent premium mix shifts and channel normalization.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 24.51 B (2026) | |

| Trade Journal A | USD 23.60 B (2023) | Uses a category value point tied to a single reported year and may not normalize USD timing across countries, which can shift totals when exchange rates move. |

| Industry Publication B | USD 26.02 B (2025) | Often reflects a broader gin-category interpretation and forward value expectation, which can embed optimistic price mix assumptions and different treatment of flavored and adjacent products. |

The spread across the table is largely explained by differences in what is counted as gin and how year timing is handled for value conversion. By keeping the inputs tied to observable volume signals, channel splits, and country-level price mix, the resulting market value stays traceable and repeatable when the same steps are applied again.

Key Questions Answered in the Report

How large is the global gin segment in 2026 and how fast is it expanding?

Value reaches USD 24.51 billion in 2026 and is projected to hit USD 30.87 billion by 2031, reflecting a 4.72% compound annual growth rate.

Which region posts the quickest growth through 2031?

Asia-Pacific leads with a 5.94% CAGR, powered by rising cocktail culture in China, India, and Southeast Asia.

What product style currently holds the greatest share?

London Dry accounts for 52.02% of 2025 volume, though Old Tom is the fastest climber at a 5.12% CAGR to 2031.

Why are premium and super-premium labels gaining traction?

Premiumization and botanical innovation allow craft and upscale brands to command higher shelf prices and 60% gross margins versus 35% for mass labels.

Page last updated on: