Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.42 Billion |

| Market Size (2026) | USD 1.47 Billion |

| Market Size (2031) | USD 1.76 Billion |

| Growth Rate (2026 - 2031) | 3.69% CAGR |

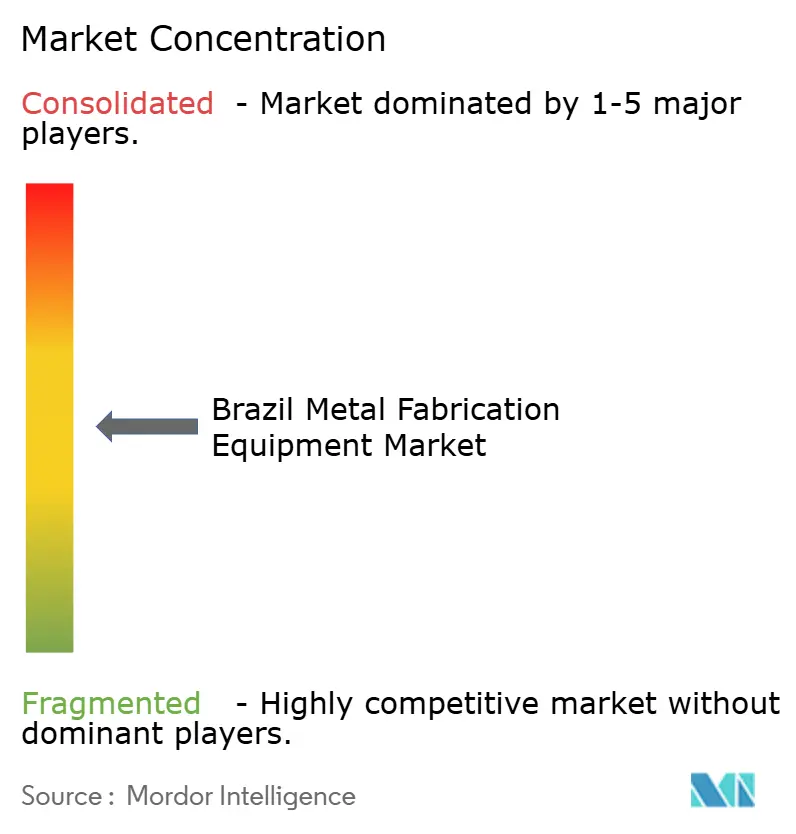

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Metal Fabrication Equipment Market Analysis by Mordor Intelligence

The Brazil Metal Fabrication Equipment Market size is expected to grow from USD 1.42 billion in 2025 to USD 1.47 billion in 2026 and is forecast to reach USD 1.76 billion by 2031 at 3.69% CAGR over 2026-2031. Rising infrastructure spending, robust vehicle production plans focused on electric and hybrid models, and intensive pre-salt oil and gas developments are combining to lift demand for precision machining, cutting, and welding systems. Public-sector programs such as PAC 2024-27 and Lei do Bem are widening access to modernization capital, while import tariffs of 14%–20% protect local manufacturers and give domestically produced equipment a pricing edge. Supply growth remains brisk in automatic systems as producers move toward connected, sensor-driven operations that reduce scrap and energy use. Conversely, volatile steel input prices, constrained grid reliability in the North and Northeast, and a persistent shortage of skilled CNC operators temper the short-term spending outlook.

Key Report Takeaways

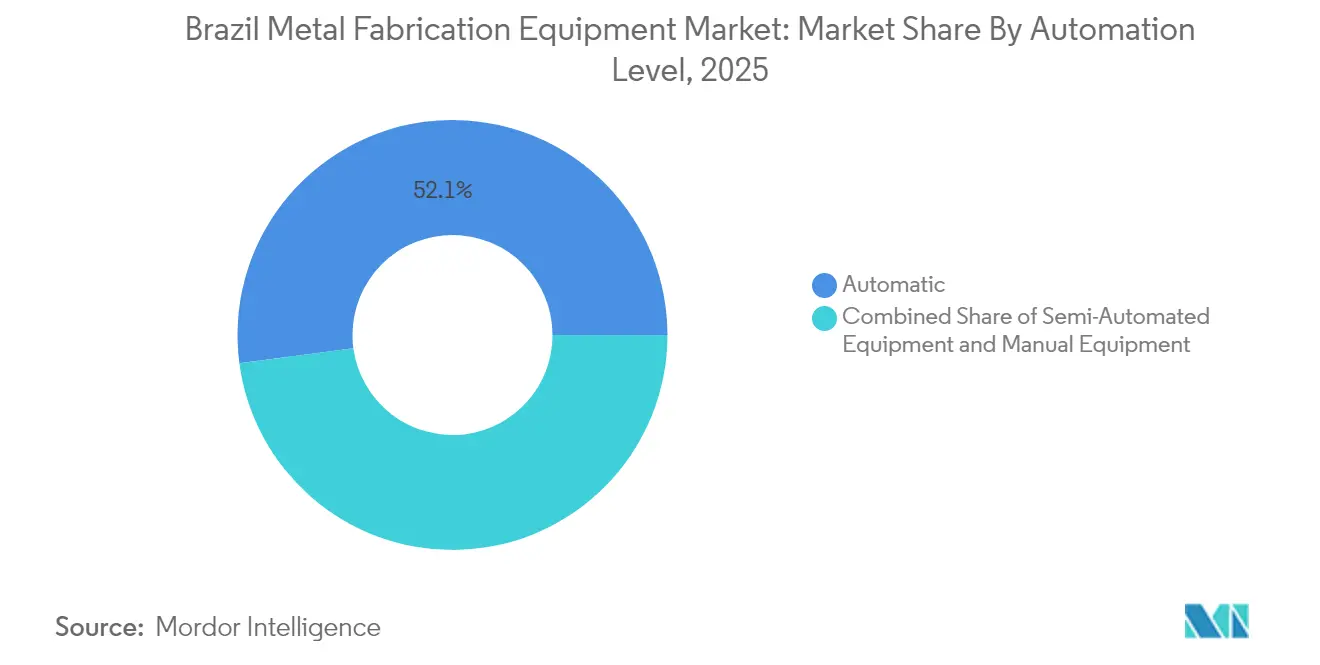

- By automation level, automatic systems commanded 52.10% of the Brazil metal fabrication equipment market size in 2025 and are expanding at a 4.55% CAGR through 2031.

- By equipment type, machining equipment led with 41.88% of the Brazil metal fabrication equipment market share in 2025; welding equipment is projected to grow at the fastest 5.05% CAGR to 2031.

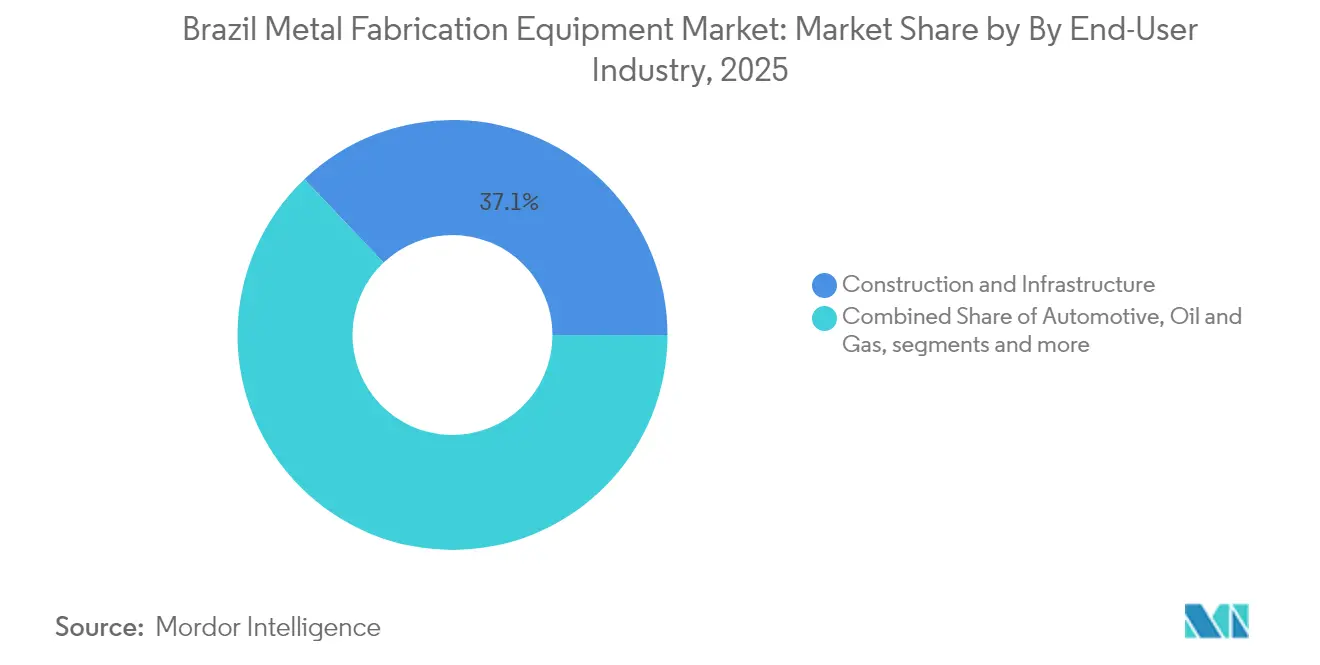

- By end-user, construction and infrastructure accounted for a 37.10% share of the Brazil metal fabrication equipment market size in 2025, while the diverse “others (electronics, General manufacturing, marine, railways, etc.)” category is set for the highest 4.66% CAGR to 2031.

- By region, Southeast captured 46.30% revenue share in 2025; Northeast is forecast to post a 4.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Metal Fabrication Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated pre-salt O&G field development boosting high-spec equipment demand | +0.8% | Southeast, South plus offshore zones | Medium term (2-4 years) |

| Expansion of Brazilian EV/automotive clusters spurring CNC adoption | +0.6% | Southeast, South | Short term (≤ 2 years) |

| PAC 2024-27 infrastructure pipeline driving large-scale steel fabrication | +0.5% | National, early gains in Northeast, North | Medium term (2-4 years) |

| Lei do Bem tax incentives catalyzing Industry 4.0 investments | +0.4% | Southeast, South, selective Northeast | Long term (≥ 4 years) |

| FINAME local-content mandates favoring domestic equipment purchases | +0.3% | National | Short term (≤ 2 years) |

| Rising Mercosur module exports requiring capacity upgrades | +0.2% | Southeast, South | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Pre-Salt O&G Field Development Boosting High-Spec Equipment Demand

Petrobras plans to drill 280 new wells by 2028 under a USD 102 billion spending program, driving unprecedented demand for ultra-high-tolerance cutting and welding systems that handle corrosion-resistant alloys for subsea pipelines and floating production units[1]World Oil Staff, “Petrobras Pre-Salt Program Drives Offshore Equipment Boom,” WorldOil, worldoil.com. Constellation Oil Services reports rig day rates nearing USD 500,000, evidence of premium equipment needs. Tenaris and Equinor recently delivered 83,000 tons of steel pipe for the Raia project, underscoring sustained Southeast demand for sophisticated fabrication.

Expansion of Brazilian EV/Automotive Clusters Spurring CNC Adoption

Automakers have announced more than USD 6 billion in fresh plant upgrades to build electric models. General Motors alone is committing USD 1.4 billion through 2029, while Toyota earmarked USD 2.22 billion, which includes USD 1 billion by 2026, for locally tailored vehicles. Precision CNC machines are central to new battery-pack frames and lightweight chassis components, lifting orders across São Paulo and Paraná.

PAC 2024-27 Infrastructure Pipeline Driving Large-Scale Steel Fabrication

The Growth Acceleration Program set aside BRL 186.6 billion(USD 35.45 billion) for nationwide industrial digitalization and allocated R$816 million(USD 155.04 million) from the Northeast Investment Fund toward the long-delayed Transnordestina railway[2]Secretariat for Industry, “Digitaliza Brasil: R$186,6 Bi Em Incentivos,” Brazilian Government, gov.br. Massive bridge girders, rail cars, and station structures demand thick-plate forming lines and multi-torch gantry cutting cells, boosting equipment suppliers with heavy-duty portfolios.

Lei do Bem Tax Incentives Catalyzing Industry 4.0 Investments

Companies that claim the Lei do Bem deduction recover up to 34% of qualifying R&D outlays, sharply lowering net costs for automation, sensor integration, and data-analytics upgrades. Academic studies show participants materially out-innovate peers, yet only 0.7% of eligible firms have used the benefit so far. Wider uptake would unlock a broad modernization wave, especially among mid-sized machining shops.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile steel input prices compressing capex budgets | -0.7% | National, acute in Southeast, South | Short term (≤ 2 years) |

| Grid instability in North/Northeast limiting high-power machine uptime | -0.4% | North, Northeast | Medium term (2-4 years) |

| CNC skilled-labour shortage restraining automation ROI | -0.3% | National, concentrated in Southeast, South | Long term (≥ 4 years) |

| Import tariffs inflating advanced equipment costs | -0.2% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Steel Input Prices Compressing Capex Budgets

Fluctuating coil prices and antidumping policy shifts are creating budgeting uncertainty for plants planning new lines. Gerdau cut its five-year outlay target to R$9.2 billion(USD 1.75 billion), blaming squeezed margins tied to cheap Asian imports. ArcelorMittal similarly paused its João Monlevade expansion, stalling orders for heavy presses and automated roll grinders.

Grid Instability in North/Northeast Limiting High-Power Machine Uptime

Voltage sags in Pará and Maranhão trigger average shutdown costs of USD 7,364 per incident for high-load laser cutters and induction-heating weld stations. Firms delay purchases of multi-kilowatt fiber-laser machines until reliability improves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Automation Level: Automatic Equipment Drives Digital Transformation

Automatic systems held 52.10% of the Brazil metal fabrication equipment market in 2025, and revenue is rising at a 4.55% CAGR to 2031. Factory owners see paybacks under three years when integrated robotics cuts rework and scrap. Semi-automated machines remain popular among medium enterprises taking a modular upgrade route, whereas fully manual benches survive in artisan workshops and for intricate stainless-steel finishes.

Government digitalization funding of BRL 186.6 billion(USD 35.45 billion) and the Brasil Mais Produtivo program’s BRL 560 million(USD 106.4 million) allocation for small manufacturers are accelerating control retrofits and sensor deployments. Nonetheless, surveys in the Sorocaba region found only 46% of firms familiar with core Industry 4.0 concepts. The gap suggests a long runway for automatic-equipment adoption as awareness programs expand.

By Equipment Type: Machining Dominance Amid Welding Innovation

Machining equipment captured 41.88% of the Brazil metal fabrication equipment market in 2025, reflecting the country’s deep heritage in turning, milling, and drilling for engines, gearboxes, and agricultural machinery. The machining Brazil metal fabrication equipment market size for this segment is projected to climb alongside EV-related lightweight components. Meanwhile, welding equipment revenue is increasing at a 5.05% CAGR, led by multiprocess power sources tailored to offshore alloy steels.

Exhibitors at FEIMEC 2024 highlighted integrated cells combining CNC mills with inline robotic welders and AI-driven inspection, moving the sector toward end-to-end digital lines. Cutting and forming machines continue to parallel overall market growth as construction orders for plate shears and press brakes track rail and port upgrades.

By End-User Industry: Construction Leadership Amid Diversification

Construction and infrastructure represented 37.10% of demand in 2025, underpinned by PAC 2024-27 outlays for highways, metros, and irrigation canals. The segment accounted for half of public procurement transactions for heavy press brakes and submerged-arc gantries last year. Automotive and transportation remains the second-largest buyer group, fueled by USD 6 billion earmarked for new electrified vehicle lines across existing clusters.

The diversified “others” segment electronics, general manufacturing, marine, railways shows the fastest 4.66% CAGR as Brazil pursues semiconductor self-sufficiency under the Brazil Semicon Act and coastal shipyards refit for offshore wind component fabrication. Heavy machinery suppliers serving agribusiness also drive consistent orders for large-capacity vertical lathes.

By Region: Southeast Dominance Amid Northeast Emergence

Southeast housed 46.30% of Brazil's metal fabrication equipment market revenue in 2025, thanks to dense automotive, steel, and capital-goods corridors in São Paulo and Minas Gerais. Gerdau’s R$5 billion(USD 950 million) modernization of flat-steel lines in Minas supports continuing demand for coil-processing equipment. The South keeps traction via Curitiba’s automotive base and diversified machinery exports.

Northeast is on track for a 4.61% CAGR to 2031 as the Transnordestina railway revives structural-steel demand and new logistics hubs court manufacturing relocations. Incentives tied to port-zone free-trade regimes in Ceará and Pernambuco lower the landed costs of imported subassemblies, thereby boosting equipment investments for module final assembly. Central-West benefits from grain-harvester fabrication growth, while the North taps mining-related cutting-edge crushers despite lingering grid hurdles.

Geography Analysis

The Brazil metal fabrication equipment market displays a clear industrial heartland, yet is gradually diffusing northward. Southeast remains the epicenter with a 46.30% share in 2025 because of integrated supply chains and skilled labor pools. ArcelorMittal’s USD 1.8 billion program to lift flat-product capability and quality underscores continued capex magnetism in the belt linking Belo Horizonte and Santos.

The South retains second-place status through vehicle and white-goods clusters in Rio Grande do Sul and Santa Catarina. Central-West’s Mato Grosso and Goiás show steady purchases of plate-rolling and laser-tube lines that feed farm-implement hubs serving an expanding soy and corn frontier.

Northeast’s growth arc stands out. Recent R$816 million(USD 155.04 million) disbursement from the Northeast Investment Fund to advance the 1,200 km Transnordestina railway has unlocked orders for beam drill lines, CNC plasma tables, and heavy profile benders. Steel fabricators in Pernambuco and Bahia are also bidding on wind-tower sections as offshore wind leasing blocks open.

The North’s Pará mines are scaling capacity for bauxite and copper, prompting procurement of wear-plate plasma cutters and robot-assisted gouging stations. Still, power-quality and logistics hold back broader adoption of multi-kilowatt fiber lasers, leading some buyers to specify redundant UPS systems or diesel back-up generation.

Competitive Landscape

Competitive Landscape

Competition remains moderately fragmented. Global majors such as DMG Mori, Trumpf, Amada, Lincoln Electric, ESAB, Hypertherm, and Bystronic lead in premium CNC, laser, and multi-process welding lines. Domestic firms, including BMA Brasil Equipamentos and Romi, leverage FINAME scoring advantages to supply cost-sensitive buyers of press brakes and manual lathes. Equipment tenders increasingly demand integrated IoT dashboards, nudging all vendors to embed edge analytics and OPC UA connectivity.

Strategic moves illustrate adaptation to local policy. Trumpf entered a joint venture with a São Paulo integrator to raise local content on 2D laser cutters and access subsidized credit. DMG Mori inaugurated a parts-and-training hub in Curitiba to shorten lead times for spindle rebuilds, while ESAB opened a robotics demonstration cell in Contagem to cross-sell cutting torches with collaborative welding arms.

White-space opportunities cluster around offshore alloy welding, in-situ pipe-buckle cladding, and additive repair of drilling components. Few suppliers combine 100+ kW power sources with automated seam tracking suitable for subsea spoolbases, giving first movers room to capture lucrative service contracts. Implementation of the new Tax on Goods and Services in 2026 is expected to compress effective import costs on software relative to hardware, favoring suppliers with strong digital toolboxes.

Brazil Metal Fabrication Equipment Industry Leaders

BMA Brazil

Colfax

DMG Mori

Trumpf GmbH

Amada Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Complementary Law 214/2025 established Brazil’s new Tax on Goods and Services, Contribution on Goods and Services, and Selective Tax regimes, reshaping indirect taxes on metal fabrication equipment.

- December 2024: The federal government pledged BRL 546.6 billion to boost sustainable agro-industrial chains, elevating demand for locally produced agricultural machinery.

- November 2024: Tenaris and Equinor completed fabrication of 83,000 tons of pipe for the USD 9 billion Raia offshore gas project in São Paulo.

- August 2024: ANDRITZ started up Suzano’s 2.55 million tpa eucalyptus pulp mill, the world’s largest single-line plant, showcasing advanced fabrication technologies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Brazil's metal fabrication equipment market as the annual sales value of new machines, cutting, machining, forming, and welding systems, along with their integrated CNC, laser, and plasma modules that are installed in fabrication shops and captive plants nationwide. Equipment rented, remanufactured, or used exclusively for additive manufacturing is excluded.

Scope Exclusion: Used, rebuilt, and purely 3-D printing units are outside report scope.

Segmentation Overview

- By Automation Level

- Automatic

- Semi-Automated Equipment

- Manual Equipment

- By Equipment Type

- Cutting (Laser, Plasma, Waterjet, Oxy-fuel, etc.)

- Machining (Lathes, Milling, Drilling, etc.)

- Forming (Press Brakes, Bending Machines, etc.)

- Welding (Arc Welding, Laser Welding, etc.)

- Other Equipment Types (Finishing, Handling, Tooling, etc.)

- By End-User Industry

- Automotive & Transportation

- Construction & Infrastructure

- Oil & Gas / Energy

- Aerospace & Defense

- Heavy Machinery & Industrial Equipment

- Others (Electronics, General Manufacturing, Marine, Railways, etc.)

- By Region

- Southeast (Sudeste)

- South (Sul)

- Northeast (Nordeste)

- North (Norte)

- Central-West (Centro-Oeste)

Detailed Research Methodology and Data Validation

Primary Research

Interviews with plant engineers, equipment distributors, leasing financiers, and regional industry bodies across São Paulo, Minas Gerais, Rio Grande do Sul, and Bahia helped us verify utilization rates, discount structures, and forward capex intentions, closing gaps that desk work alone could not bridge.

Desk Research

Our analysts sifted public datasets from IBGE industrial production tables, SECEX customs codes (HS 8461, 8462, 8463), and MDIC trade dashboards, then layered insights from ABIMAQ shipment bulletins, ANFAVEA vehicle build statistics, and CNI capital-goods confidence surveys. Company filings, investor decks, and reputable press archives were screened through Dow Jones Factiva, while D&B Hoovers supplied revenue splits for key OEMs. These sources illustrate demand cycles, import ratios, and average selling prices; the list is indicative, not exhaustive.

Market-Sizing & Forecasting

A top-down production and trade reconstruct quantified the 2024 baseline, which was then cross-checked through sampled supplier roll-ups and channel ASP × volume calculations. Core variables, import duty shifts, construction outlays, automotive output, PMI capital-goods sub-index, and machining-hour pricing drive our model. An ARIMA time-series, stress-tested with scenario panels from primary contacts, projects demand to 2030; bottom-up checks allow adjustments where OEM shipment data deviate beyond a 5% tolerance.

Data Validation & Update Cycle

Before sign-off, outputs pass a multi-analyst review that reconciles anomalies against external indicators such as steel price spreads and workshop capacity surveys. Reports refresh annually, with mid-cycle updates if currency swings, policy moves, or strike actions materially alter assumptions.

Why Our Brazil Metal Fabrication Equipment Baseline Is Trusted

Published estimates often diverge.

Differences in scope, pricing assumptions, and refresh cadence typically explain the gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.42 B (2025) | Mordor Intelligence | - |

| USD 1.50 B (2025) | Regional Consultancy A | Includes refurbished imports; limited primary validation |

| USD 0.91 B (2024) | Global Consultancy B | Uses machine-tools subset only; excludes forming and welding |

These comparisons show that Mordor's disciplined scope selection, annual refresh, and twin-track validation deliver a balanced baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current value of the Brazil metal fabrication equipment market?

The market stands at USD 1.47 billion in 2026 and is forecast to reach USD 1.76 billion by 2031.

Which equipment segment leads the Brazil metal fabrication equipment market?

Machining equipment holds the largest 41.88% share, while welding equipment is the fastest-growing segment with a 5.05% CAGR to 2031

How important is automation in Brazil’s metal fabrication sector?

Automatic systems already account for 52.10% of revenue and are expanding at a 4.55% CAGR, reflecting strong movement toward Industry 4.0 adoption.

Which region shows the fastest growth for metal fabrication equipment demand?

The Northeast is projected to grow at 4.61% annually through 2031, driven by major rail and port projects.

What government incentives support equipment modernization?

Lei do Bem offers tax deductions for R&D and technology spending, while FINAME provides subsidized financing for high-local-content machines.

What are the main challenges facing equipment buyers?

Steel price volatility, skilled-labor shortages, import tariffs on advanced machinery, and power-supply instability in northern regions are key obstacles to near-term investment.

Page last updated on: