Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

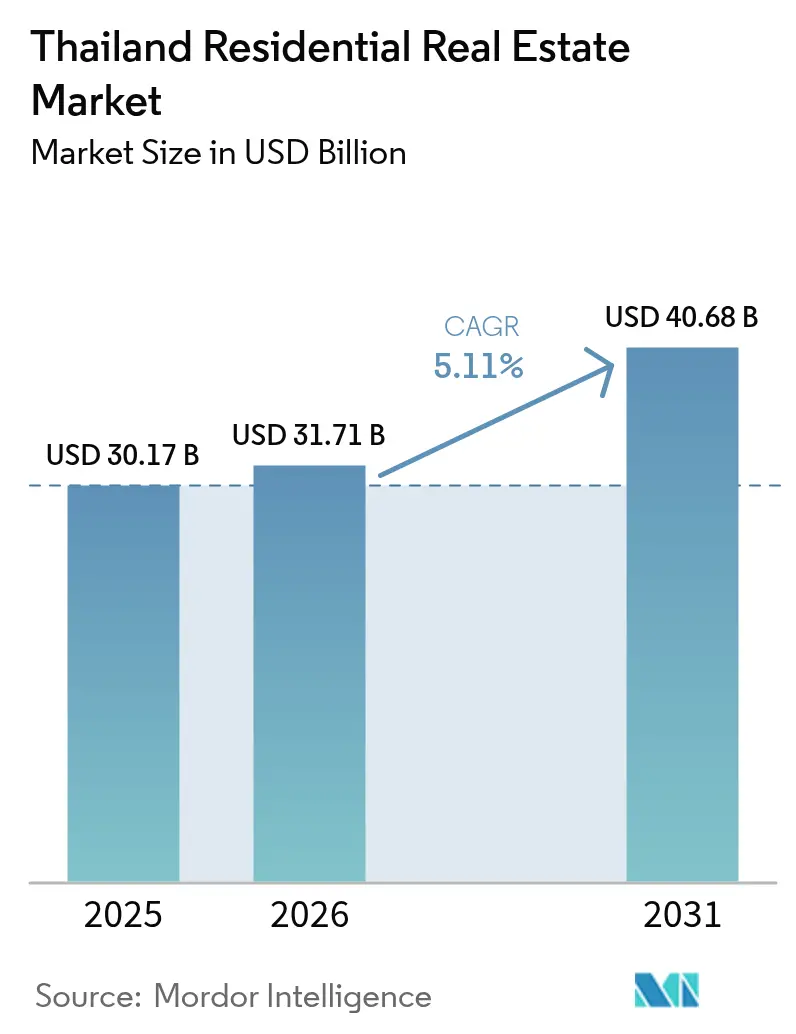

| Base Year Market Size (2025) | USD 30.17 Billion |

| Market Size (2026) | USD 31.71 Billion |

| Market Size (2031) | USD 40.68 Billion |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

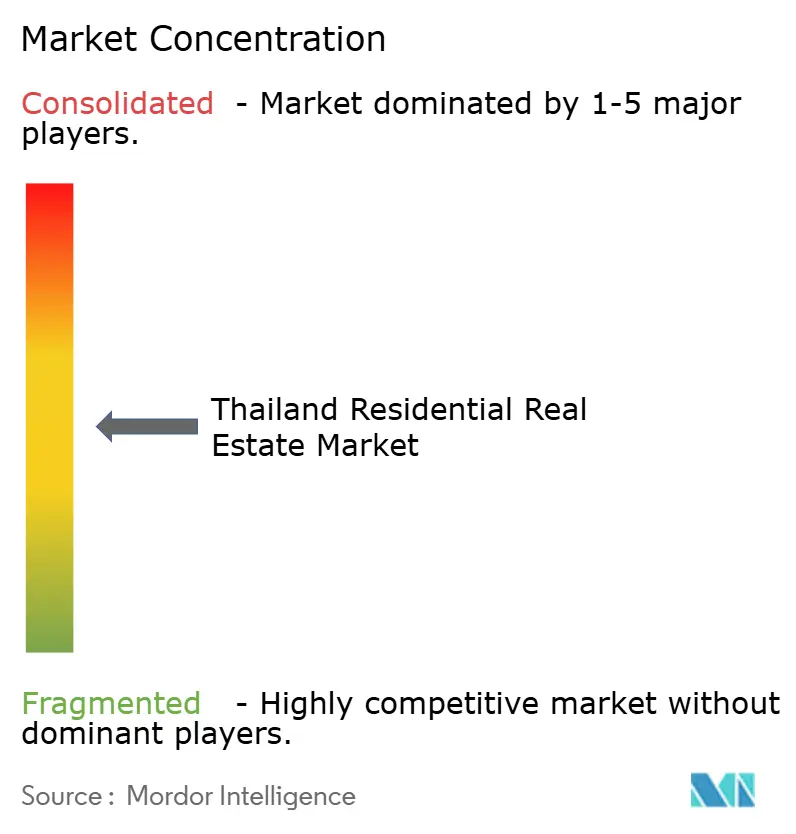

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Residential Real Estate Market Analysis by Mordor Intelligence

The Thailand residential real estate market size is projected to be USD 30.17 billion in 2025, USD 31.71 billion in 2026, and reach USD 40.68 billion by 2031, growing at a CAGR of 5.11% from 2026 to 2031. Momentum is shifting toward landed housing and build-to-rent formats as government mortgage holidays, fee waivers, and the roll-out of new mass-transit lines draw buyers away from speculative condominiums. Developers are recalibrating pipelines to align with the Long-Term Resident (LTR) and Digital Nomad visas, which introduce a predictable stream of foreign demand insulated from volatile domestic credit cycles[1]Bangkok Post, “Visa Reforms Spark Property Demand,” bangkokpost.com. Simultaneously, institutional investors, pension funds, insurance portfolios, and REITs, are scaling rental inventories that deliver 4-6% yields, moderating cash-flow risk during slower sales periods. Structural headwinds remain: household debt hovers near 91% of GDP, while a 53,000-unit condo glut in Bangkok elongates absorption timelines and flattens resale prices in the mid-tier.

Key Report Takeaways

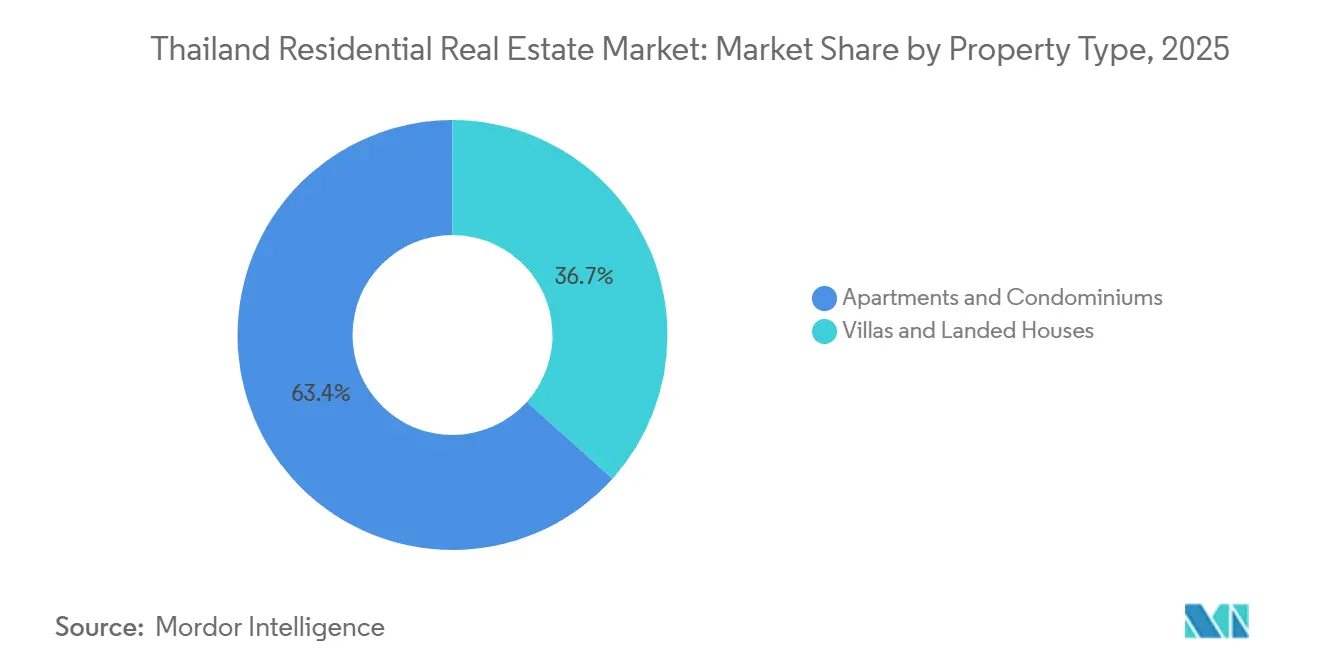

- By property type, apartments and condominiums accounted for 63.35% of the Thailand residential real estate market size in 2025, and villas and landed houses are set to grow at a 5.66% CAGR through 2031.

- By price band, the affordable segment held 59.35% of the Thailand residential real estate market share in 2025, while the same affordable segment is anticipated to advance at a 5.71% CAGR between 2026 and 2031.

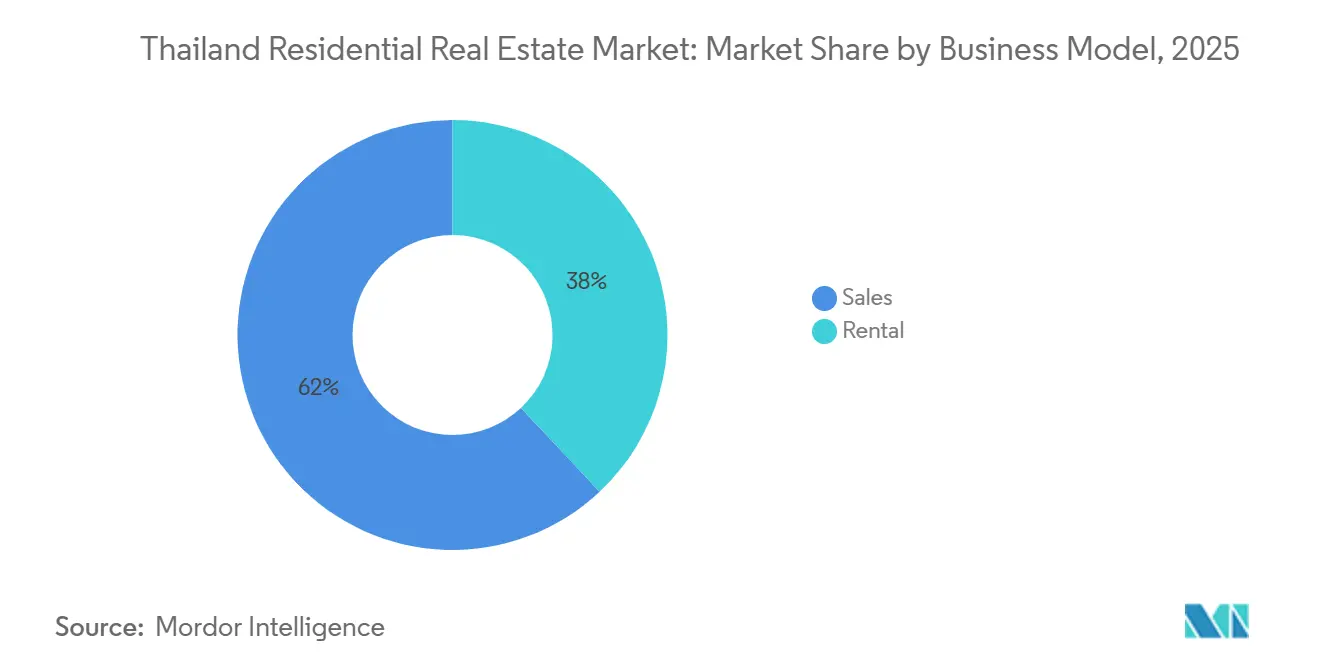

- By business model, sales represented 62% of the Thailand residential real estate market size in 2025, and rental assets are expected to register a 5.88% CAGR over the forecast period.

- By mode of sale, secondary exchanges captured 65.21% of the Thailand residential real estate market share in 2025, whereas primary launches are likely to grow at a 5.85% CAGR through the forecast period.

- By cities, Bangkok recorded 45.45% of the Thailand residential real estate market size in 2025, and Phuket is poised to expand at a 5.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| New rail corridors opening peri-urban plots | +1.2% | Bangkok Metro Region and fringe provinces | Long term (≥ 4 years) |

| First-time-buyer incentives and fee relief | +1.0% | National, strongest in affordable provinces | Short term (≤ 2 years) |

| Wage gains and aging demographics | +0.9% | Nationwide with Bangkok, Chonburi, Chiang Mai hot spots | Medium term (2-4 years) |

| LTR and Digital-Nomad visas widening the foreign-buyer pool | +0.8% | Bangkok, Phuket, Chiang Mai | Medium term (2-4 years) |

| Tourism rebound and expatriate resettlement | +0.7% | Phuket, Pattaya, Samui, Bangkok | Short term (≤ 2 years) |

| Secondary-city urbanization | +0.6% | Chiang Mai, Khon Kaen, Hat Yai, Bangkok | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

New Rail Corridors Opening Peri-Urban Plots

The Mass Rapid Transit Authority has allocated USD 11.4 billion for track expansion through 2027, with the Pink and Yellow lines already shaving up to 40 minutes off suburb-to-CBD commutes. Newly minted TOD zoning grants taller floor ratios within a 500-meter radius of stations, prompting MQDC to incorporate retail, office, and residential phases into master-planned nodes. Land in Pathum Thani and Samut Prakan remains 50-60% cheaper than downtown plots, enabling affordable townhouse pricing even after infrastructure premiums. Because commercial amenities and feeder buses mature gradually, full value-capture materializes three to five years post-opening, justifying the 1.2% long-range lift.

First-Time-Buyer Incentives and Fee Relief

The 100% LTV scheme covering homes under USD 86,000 and a 0.01% transfer fee remains effective through mid-2026. Entry buyers save roughly USD 1,714 on a USD 86,000 property, redirecting cash toward furnishings and closing gaps left by high household leverage. Developers' time launches before policy sunsets, accelerating affordable-segment bookings and providing a near-term 1.0% tailwind.

Wage Gains and Aging Demographics

The minimum wage moved to USD 11.4 a day in 2025, improving mortgage eligibility for roughly eight million formal employees. Thailand’s over-60 population now tops 20%, speeding demand for single-story villas with accessibility features and medical proximity. Builders such as Land & Houses are marketing dual-key layouts so adult children and elderly parents can co-reside without sacrificing privacy. Labor shortages triggered by a shrinking workforce nudge contractors toward prefab modules that reduce on-site crews. The combined demographic and income backdrop contributes a 0.9% medium-term boost.

LTR and Digital-Nomad Visas Widening the Foreign-Buyer Pool

More than 7,000 LTR permits had cleared by late 2025, injecting USD 657 million into Thailand’s economy and re-energizing luxury-condo demand in Sukhumvit and Sathorn. The companion Digital Nomad Visa logged 35,000 approvals during its inaugural year, steering higher-income remote workers toward Chiang Mai and Phuket co-working enclaves. Developers optimize the 49% foreign-ownership quota in towers by selling remaining inventory to local investors and structuring 30-year leaseholds for villas where freehold is off-limits. While quotas cap upside, stable overseas inflows help clear premium stock that domestic buyers bypass. Medium-term support hinges on streamlined processing and tax neutrality.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy household leverage weighing on mortgages | -1.1% | National—with sharper stress in North and Northeast | Short term (≤ 2 years) |

| Prolonged condo overhang and muted take-up | -0.9% | Bangkok, Pattaya, radiating into Chonburi | Medium term (2-4 years) |

| Flood-risk zoning and drainage upgrades | -0.4% | Bangkok, Pathum Thani, Samut Prakan, Ayutthaya | Long term (≥ 4 years) |

| Energy-saving mandates inflating CAPEX | -0.3% | Nationwide, acute in Bangkok and Phuket | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heavy Household Leverage Weighing on Mortgages

Household obligations hover at 90.6% of GDP; mortgage NPLs ticked up to 3.2% in 2025[2]Bank of Thailand, “Household Debt Dashboard Q2 2025,” bot.or.th. Debt-service ceilings of 40% screen out many informal earners, even under fee cuts. Bangkok and Chonburi log debt-to-income ratios above 120%, while the Northeastern provinces flirt with 100%. Developer financing at 0% for two years helps pass the gate, but can trigger balloon defaults later. The constraint removes 1.1% from short-run growth.

Prolonged Condo Overhang and Muted Take-Up

Bangkok’s 53,000-unit backlog equates to 2.5 years of absorption, heavy in mid-rise blocks priced USD 86,000-171,000. Pattaya towers opened in 2023-24 have only 50% presales, forcing discounting and longer installment plans. Bank of Thailand caps LTV at 90% for tickets above USD 286,000, tightening credit just as inflation lifts living costs. Developers are bulk-selling to REITs or re-marketing units as rentals, yet relief is unlikely before 2028, creating a temporary drag on market growth in the meantime.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Condo Dominance Meets Landed-House Momentum

Apartments and condominiums accounted for 63.35% of Thailand's residential real estate market share in 2025. Despite that lead, villas & landed houses are projected to log a 5.66% CAGR to 2031 as households prioritize freehold ownership and outdoor space. New rail links cut commuting penalties, so plots in Nonthaburi or Pathum Thani cost half of CBD equivalents, letting developers bundle clubhouses and security into entry-level estates.

Condos still anchor Sukhumvit, Silom, and Sathorn, where walkability and BTS proximity trump square footage. Prime towers are expected to see a 15% upswing in 2026 if inbound tourism meets projections, though fringe projects may offer discounts of 20–25% due to oversupply. Hybrid low-rise condos with private gardens blur the divide, appealing to middle-income families that value green space without sacrificing vertical convenience.

By Price Band: Affordable Tier Anchors Demand

Affordable units held 59.35% of the Thailand residential real estate market size in 2025. Government LTV waivers and slashed fees feed a 5.71% CAGR outlook through 2031. Townhouses and 25-35 sq m studios near the Pink or Yellow Lines list at USD 43,000-71,000, keeping monthly payments inside the 40% debt-service cap.

Mid-market dwellings priced at USD 86,000–286,000 continue to expand as leverage caps pressure salaried professionals. Luxury homes above USD 286,000 rely on long-term rentals (LTR) and expatriate buyers, though demand remains steady. Coastal villas in Phuket and Samui command USD 429,000-1.43 million and routinely sidestep domestic credit issues by selling to cash buyers or through offshore funding channels.

By Business Model: Rental Portfolios Gain Institutional Traction

Sales still generated 62% of 2025 receipts, but rental assets should post the fastest 5.88% CAGR as pension funds, insurers, and REITs chase inflation-hedged yields. MQDC’s USD 1.4 billion Forestias reserves 30% of units for long-term leasing, backed by a USD 629 million Siam Commercial Bank facility. Phuket owners achieve 8-12% gross yields in peak season through short-stay platforms, reinforcing the investment narrative.

Outright sales rise more modestly at 4.8% because mortgage approvals trail wage growth. Hybrid “buy-to-let” programs now offer a deed plus three-year income floor, merging ownership prestige with passive returns. Foreigners exceeding condo quotas pivot to 30-year renewable leases on villas, swelling the structured rental stock.

By Mode of Sale: Primary Supply Accelerates on Rail Openings

Secondary deals dominated 65.21% of 2025 turnover, but primary launches are projected to surge at a 5.85% CAGR as the 2027 Orange Line unlocks 35 kilometers of fresh corridors. Government fee waivers apply only to new stock, creating a pricing delta that funnels first-time purchasers into freshly completed projects.

Secondary condos inside the 2016-19 cycle trade 15-20% under launch price, drawing yield-focused buyers comfortable with cosmetic refurbishments. For developers, rental guarantees and furniture packages accelerate take-up, minimizing financing carry costs. The two channels, therefore, coexist, balancing liquidity across the Thailand residential real estate market.

Geography Analysis

Bangkok captured 45.45% of the 2025 value, underpinned by its 11.2 million residents and the most extensive BTS/MRT grid in Southeast Asia[3]United Nations Population Division, “World Urbanization Prospects 2025,” un.org. Luxury condos between USD 286,000 and USD 857,000 line Sukhumvit and Sathorn, while gated estates thrive in rail-served suburbs such as Nonthaburi. The Pink and Yellow lines reduced outer-district commutes by 40 minutes, lifting land valuations near stations by 20-30% and enabling premium TOD pricing. Yet a condo stockpile and steep household leverage in Bangkok dampen velocity until the 2027 Orange Line opens new sub-markets.

Phuket leads growth with a projected 5.91% CAGR through 2031. Visitor counts touched 10 million in 2025, and digital nomads target USD 229,000-343,000 sea-view condos. If 2026 tourist forecasts verify, CBRE projects a 15% uptick in prime urban values; conversely, affordable periphery projects may slide 10% on weak occupancy. Developers hedge by framing units for flexible rental income via platforms such as Airbnb, capturing 8-12% annual yields.

Pattaya’s beach towers attract weekend buyers from Bangkok, while Chiang Mai’s revamped airport precinct, Central Pattana’s USD 34 million mixed-use venture, draws retirees and remote workers. Secondary nodes like Khon Kaen and Hat Yai gain from logistics corridors and mortgage subsidies, offering starting prices impossible in the capital. Together, these shifts funnel demand beyond Bangkok, moderating systemic risk in the Thailand residential real estate market.

Competitive Landscape

The Thailand residential real estate market is moderately consolidated, with major developers such as Pruksa, Sansiri, AP Thai, Land & Houses, and MQDC. Despite the presence of these leading players, a wide competitive fringe of smaller regional developers continues to operate across the market. Sansiri spent USD 13.9 million on a Sukhumvit plot in November 2025 to seed four high-rise LTR-friendly projects. Noble Development and STECON teamed up 50:50 on the NUE EPIC Asok-Rama 9 TOD adjacent to the Orange Line, reflecting the necessity of engineering heft in mixed-use builds.

Township plays dominate the high end: MQDC’s Forestias, already 70% erected, marries condos, villas, and forested retail, funded by USD 629 million in bank lines. Non-bank lenders are breaking into mortgages with zero-interest teaser periods, stealing market share from commercial banks, but heightening downstream default risk. Digitized brokerages accelerate unit turnover through 360-degree virtual tours and blockchain receipts, trimming sales cost per unit by up to 30%.

Cost pressure from TREES-NC codes pushes smaller builders to embrace prefab alliances or offload land banks. WHA’s USD 25.7 million industrial-linked housing purchase near the EEC illustrates diversification from logistics into worker homes. Competitive depth should persist, but credit discipline and land-bank quality will separate winners from laggards.

Thailand Residential Real Estate Industry Leaders

Pruksa Real Estate

Supalai

Sansiri

AP Thai

Origin Property

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: WHA Industrial Development secured logistics-adjacent land for USD 25.7 million to build workforce housing.

- October 2025: MQDC unveiled Aspen Tree, a smart, green-certified condominium in eastern Bangkok.

- September 2025: Noble Development and STECON closed a 50:50 venture for the NUE EPIC Asok-Rama 9 TOD.

- August 2025: Sansiri added USD 1.3 million in land near upcoming train stations, betting on TOD premiums.

Thailand Residential Real Estate Market Report Scope

Residential real estate includes housing for individuals, families, or groups of people to live on. Furthermore, the report provides key insights into the Thai residential real estate market. It includes technological developments, trends, and initiatives taken by the government in this sector. It also focuses on the market dynamics, such as factors driving the market, restraints to the market growth, and opportunities going forward. Additionally, the competitive landscape of the Thai residential real estate market is depicted through the profiles of active key players. In the report, the Thai Residential Real Estate market is segmented by Property Type (Apartments and Condominiums, Landed Houses, and Villas) and by Key Cities (Bangkok, Chiang Mais, Nontha Buri, and Samut Prakan). The report offers market size and forecasts for the Thai Residential Real Estate Market in value (USD billion) for all the above segments.

By Property Type

| Apartments and Condominiums |

| Villas and Landed Houses |

By Price Band

| Affordable |

| Mid-Market |

| Luxury |

By Business Model

| Sales |

| Rental |

By Mode of Sale

| Primary (New-Build) |

| Secondary (Resale) |

By Cities

| Bangkok |

| Phuket |

| Pattaya |

| Chiang Mai |

| Rest of Thailand |

| By Property Type | Apartments and Condominiums |

| Villas and Landed Houses | |

| By Price Band | Affordable |

| Mid-Market | |

| Luxury | |

| By Business Model | Sales |

| Rental | |

| By Mode of Sale | Primary (New-Build) |

| Secondary (Resale) | |

| By Cities | Bangkok |

| Phuket | |

| Pattaya | |

| Chiang Mai | |

| Rest of Thailand |

Key Questions Answered in the Report

What is the projected value of the Thailand residential real estate market by 2031?

Forecasts indicate USD 40.68 billion, reflecting a 5.11% CAGR from 2026-2031.

Which property type dominates current transactions?

Apartments and condominiums account for 63.35% of 2025 sales value in the Thailand residential real estate market.

Where is the fastest geographic growth expected?

Phuket should register the quickest progress, with a 5.91% CAGR through 2031 as tourism and remote-worker inflows accelerate

Why are institutional investors focusing on rentals?

Build-to-rent assets deliver 4-6% yields, providing steady cash-flows while sales cycles lengthen in oversupplied condo sub-markets.

How do new visa regimes affect property demand?

LTR and Digital Nomad visas broaden the foreign-buyer base, stabilizing luxury-condo absorption and boosting villa sales in resort provinces.

What incentives help first-time Thai buyers?

A 100% loan-to-value mortgage option for homes under USD 86,000 and a 0.01% transfer fee, both extended through June 2026, sharply cut upfront costs.

Page last updated on: