Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.82 Billion |

| Market Size (2026) | USD 1.94 Billion |

| Market Size (2031) | USD 2.67 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Hair Oil Market Analysis by Mordor Intelligence

India hair oil market size in 2026 is estimated at USD 1.94 billion, growing from 2025 value of USD 1.82 billion with 2031 projections showing USD 2.67 billion, growing at 6.62% CAGR over 2026-2031. Consumer spending on daily grooming products remains robust, driven by a swift pivot to Ayurvedic formulations and broader online accessibility. While coconut oil holds deep cultural significance, specialized Ayurvedic blends like amla and almond are carving out a niche in metropolitan and Tier-I cities, buoyed by increasing disposable incomes and a growing preference for natural and traditional remedies. E-commerce is enhancing product visibility in Tier II and III regions, where modern trade is scarce, by enabling consumers to access a wider range of products and brands. Urban men's grooming segments are witnessing the fastest premiumization, driven by increasing awareness of personal grooming and the availability of high-end products. Policy measures ranging from stricter FSSAI labeling mandates to the Supreme Court's ruling on coconut oil classification are steering the market towards formal packaging, scientific endorsement, and heightened brand investment. These regulatory changes are reshaping competitive dynamics for both established FMCG giants and emerging digital-first brands, compelling them to innovate and adapt to evolving consumer preferences.

Key Report Takeaways

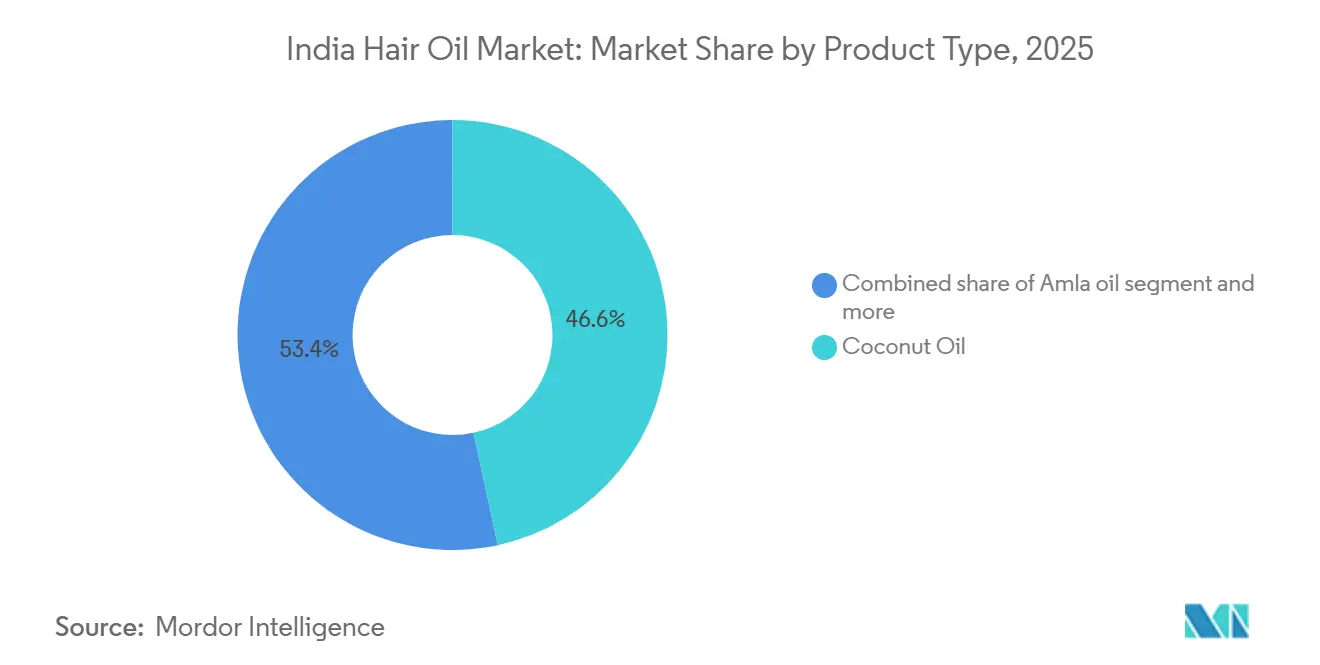

- By product type, coconut oil commanded 46.63% of India hair oil market share in 2025; amla oil is forecast to grow at a 6.86% CAGR between 2026-2031.

- By category, the mass segment held 80.94% share of India hair oil market size in 2025, while the premium segment is advancing at an 7.55% CAGR through 2031.

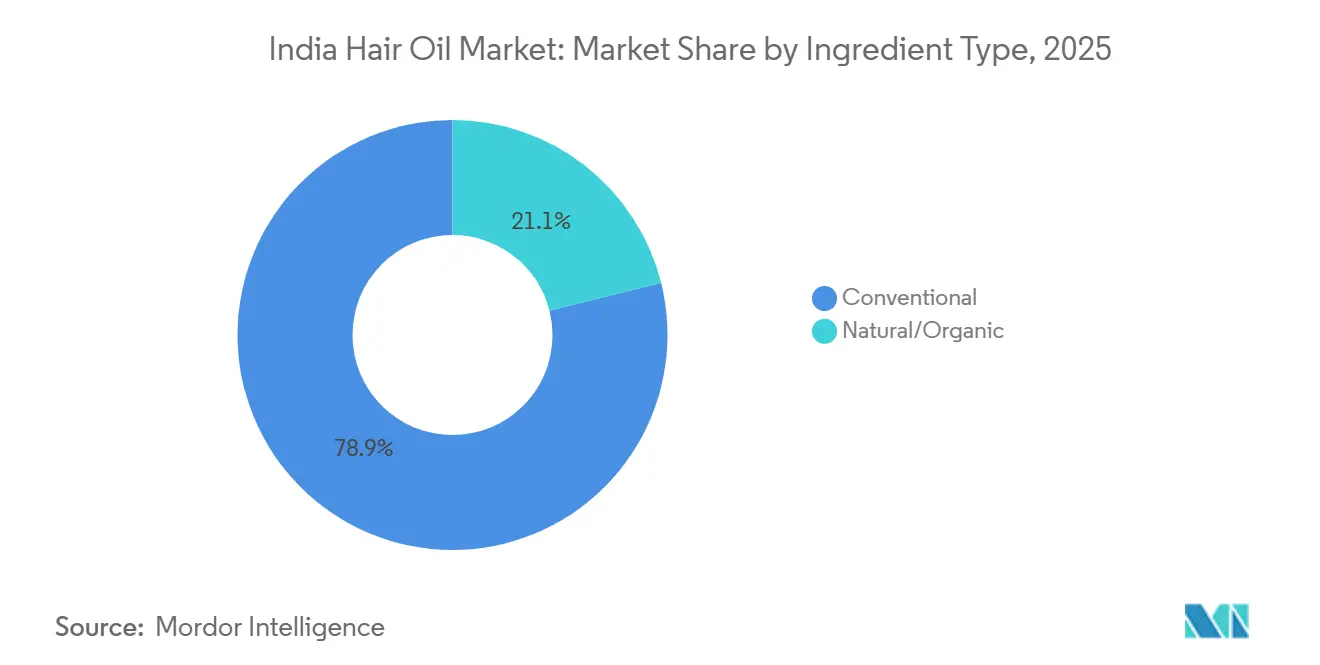

- By ingredient source, conventional formulations accounted for 78.88% of India hair oil market size in 2025; natural/organic variants are projected to expand at a 9.05% CAGR to 2031.

- By distribution channel, convenience and grocery stores led with 67.92% share of India hair oil market size in 2025, yet online retail is recording the highest CAGR at 8.95% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Hair Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes and grooming awareness | +1.8% | National, with early gains in metros and Tier-I cities | Medium term (2-4 years) |

| Surge in demand for Ayurvedic/natural formulations | +1.5% | Global, strongest in North India and urban centers | Long term (≥ 4 years) |

| E-commerce and D2C channels broadening reach | +1.2% | National, accelerated in Tier-II/III cities | Short term (≤ 2 years) |

| Shift from loose to packaged oils on safety/compliance | +1.0% | Rural India and Eastern states primarily | Medium term (2-4 years) |

| Growth of male-grooming and beard-care oil niches | +0.8% | Urban centers, expanding to semi-urban markets | Short term (≤ 2 years) |

| Microbiome-targeted scalp-care oil innovation | +0.6% | Premium urban segments, early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising disposable incomes drive premium hair care adoption

As household incomes rise, consumers are shifting from basic coconut oil to specialized blends targeting issues like hair fall, dandruff, and scalp health. These differentiated products cater to the growing demand for benefit-oriented solutions, reflecting a shift in consumer preferences toward premium offerings. Recognizing this trend, FMCG leaders are tailoring their portfolios, with value-added products now accounting for over 20% of revenue, albeit from smaller volumes. This shift highlights the increasing willingness of consumers to invest in products that promise enhanced benefits, such as improved hair and scalp health. Additionally, the booming male grooming sector, especially in affluent metro areas, finds added momentum. Here, strategic brand narratives, innovative product formulations, and tailored packaging sizes validate the premium pricing, further driving growth in this segment and creating opportunities for market expansion.

Ayurvedic renaissance transforms product formulations

Driven by a growing preference for natural oils, companies are increasingly turning to Ayurvedic botanicals like amla, bhringraj, and neem for their reformulation initiatives. These botanicals are known for their therapeutic properties, including promoting hair health, reducing scalp issues, and enhancing overall product efficacy, making them highly appealing to consumers seeking natural solutions. The strategic acquisitions of Indulekha by HUL and Sesa Care by Dabur underscore a strong belief in the long-term differentiation potential of scientifically validated Ayurveda. Such acquisitions not only expand product portfolios but also strengthen market positioning by leveraging the growing demand for Ayurvedic products. Furthermore, peer-reviewed studies highlighting the microbiome advantages of coconut oil bolster both consumer trust and regulatory standing, providing companies with a competitive edge in the natural oils market[1]Source: National Library of Medicine," Longitudinal study of the scalp microbiome suggests coconut oil to enrich healthy scalp commensals", pmc.ncbi.nlm.nih.gov.

E-commerce acceleration reshapes distribution dynamics

In 2024, online sales of beauty and personal-care products surged by 39%, boosting the digital channel's market share from 13% to 17% within just a year. This growth highlights the increasing consumer preference for the convenience and accessibility of e-commerce platforms. Quick-commerce services now offer deliveries in under an hour for items like sachets and travel packs, catering to the demand for instant gratification and last-minute purchases. Meanwhile, direct-to-consumer (D2C) brands are harnessing algorithmic targeting and content marketing, enabling them to achieve nationwide visibility without the burden of a vast retail infrastructure. These strategies allow D2C brands to personalize customer experiences and optimize their reach. In response, established players are enhancing their omnichannel strategies and integrating direct-store methods to accelerate last-mile deliveries, ensuring they remain competitive in a rapidly evolving market landscape.

Packaging innovation drives market formalization

In 2024, the Supreme Court's ruling on coconut oil, coupled with food-grade labeling mandates, is pushing the industry from loose dispensing to branded SKUs. This shift enhances visibility on ingredient lists and batch numbers, bolstering consumer confidence by ensuring transparency and traceability in product quality. It also has advantages for firms boasting strong quality systems and automated filling capabilities, enabling them to meet regulatory standards more efficiently while maintaining consistent product quality. In rural areas, tamper-proof sachets, priced at Rs 1-2, not only fit tight budgets but also reduce the risks of adulteration, addressing a critical concern for consumers in these regions. These sachets also provide an affordable entry point for branded products, helping companies expand their market reach and build trust among rural consumers.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense price competition among incumbents | -1.2% | National, particularly in mass segments | Short term (≤ 2 years) |

| Volatility in copra and other key oil-seed prices | -1.0% | South India production regions, national impact | Medium term (2-4 years) |

| Stricter scrutiny of exaggerated Ayurvedic claims | -0.8% | National, affecting premium Ayurvedic brands | Long term (≥ 4 years) |

| Urban switch to light serums cutting oil usage | -0.6% | Metro cities and urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw material price volatility pressures margins

In early 2025, retail prices for coconut oil surged to Rs 285-320/kg, driven by supply shortages that curtailed 65% of coconut availability. In January 2025, Kerala's Supplyco hiked coconut oil prices by Rs 33, bringing them to Rs 200 per liter. This move underscored the broader supply-demand imbalances, largely attributed to climate change and unpredictable weather patterns. Marico noted a temporary dip in volumes for its Parachute brand, citing elevated consumer prices and reduced pack sizes. However, management is optimistic about a rebound as copra prices seasonally stabilize. The volatility isn't limited to coconut oil alone; rising government import duties on edible oils have spurred substitution demand, further straining coconut oil supplies. In response, companies are engaging in forward buying, exploring alternative sourcing strategies, and implementing gradual price hikes. Yet, they grapple with margin compression, necessitating astute inventory and pricing management.

Regulatory tightening challenges ayurvedic claims

Hair oil manufacturers face mounting compliance challenges as governments intensify scrutiny on claims made by nutraceutical and Ayurvedic products. Expert panels, appointed by the government, are advocating for a shift in regulatory oversight of certain functional products from FSSAI to CDSCO. This shift comes with heightened demands for substantiating claims and bolstered post-market surveillance. Highlighting the quality control hurdles, the FDA's India Office has flagged heavy metals contamination in select Ayurvedic products, leading to their detention at U.S. ports[2]Source: Food and Drug Administration," FDA India Office Addresses Herbal and Ayurvedic Products", fda.gov. Meanwhile, FSSAI's revamped nutraceutical regulations mandate specific ingredient approvals, adherence to labeling standards, and strict manufacturing compliance. Non-compliance can lead to severe repercussions, including fines, product recalls, and even revocation of licenses. To navigate this landscape, companies are channeling investments into scientific validations, clinical studies, and building robust regulatory compliance frameworks. This proactive approach not only safeguards their market access but also steers them clear of exaggerated therapeutic claims that could invite regulatory scrutiny.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Coconut Oil Dominance Faces Specialized Competition

In 2025, cultural preferences and a robust distribution network in both urban and rural areas propelled coconut oil to command a 46.63% share of India's hair oil market. Marico's Parachute brand, benefiting from deep market penetration and strong consumer loyalty especially outside metro regions secured approximately 54% of the segment's volume, translating to annual revenues exceeding Rs 1,500 crore. Regional preferences, particularly in South India, not only keep coconut oil at the forefront but also shape local marketing initiatives and new product launches. The versatility of coconut oil supports its cross-category adoption, with demand remaining resilient despite fluctuations in pricing and input costs. Marico's extensive outlet reach and targeted promotions reinforce the brand's dominance, making coconut oil and Parachute nearly synonymous in the sector.

Amla oil is on a growth trajectory, boasting an impressive 6.86% CAGR through 2031, fueled by urban consumers' preference for Ayurvedic and anti-aging solutions. Dabur's aggressive marketing, especially with South India-centric variants like Dabur Amla Nelli and celebrity endorsements, has propelled annual amla oil revenues to nearly Rs 500 crore. Younger consumers and cosmetic enthusiasts, drawn to the allure of natural remedies and product innovations, are shaping this segment. While almond and castor oils cater to niche demands, Bajaj Corp's Almond Drops has carved out a dominant position, claiming 61% of the light hair oil value share through premium positioning and widespread retail presence. The expanding "Other Types" category, featuring botanical alternatives and imported blends, finds its strongest resonance in urban centers. Regional preferences play a pivotal role in brand and product development North India leans towards lighter and amla oils, whereas South India's deep-rooted coconut tradition ensures its sustained leadership in the market.

By Category: Mass Market Foundation Supports Premium Growth

In 2025, India's hair oil market saw the mass category dominate with an impressive 80.94% share. This dominance underscores the critical role of affordability, especially given the pronounced price sensitivity among urban and rural consumers alike. Success in this segment hinges on competitive pricing, brand recognition, and widespread distribution. Take Dabur, for instance: its reach extends to 2.5 million rural outlets, bolstered by the popularity of Rs 1–2 sachets that resonate with local preferences and budgets. Such strategies empower major brands to harness economies of scale, ensuring profitability and cementing brand loyalty, even amidst fierce price competition. Efficient logistics and traditional marketing bolster the growth of mass-market hair oils, driving consistent volume increases annually. Formats like blended and synthetic oils, prized for their convenience and non-sticky texture, find favor among budget-conscious consumers. These mass-market players are not resting on their laurels; they're continuously innovating in packaging and product formats, solidifying their hold on a vast and varied consumer base.

While the premium segment remains a smaller slice of the pie, it's carving out a name for itself, boasting the fastest growth rate at an impressive 7.55% CAGR from 2026 to 2031. This surge is largely attributed to rising disposable incomes, evolving grooming habits, and increasing urbanization. Premium brands differentiate themselves through a focus on scientific innovation and Ayurvedic principles, allowing them to command higher price points and cultivate unique brand identities. Take Indulekha, for example: priced at Rs 430, it's a stark contrast to the Rs 50–200 range of conventional alternatives, highlighting affluent consumers' readiness to invest in results, packaging, and perceived safety. Urban distribution channels, a nod to male grooming trends, robust digital marketing, and targeted product claims are pivotal to premium brands' success. Companies are pouring resources into research and development, crafting formulations backed by research, and using high-quality ingredients and chic packaging to validate their premium pricing. The allure of brand prestige and efficacy resonates deeply with aspirational consumers. Coupled with a growing metro population density and savvy social media campaigns, premium hair oils are steadily claiming a larger slice of India's dynamic beauty market.

By Ingredient Source: Natural Transformation Accelerates

In 2025, conventional hair oil formulations commanded a dominant 78.88% share of the Indian market. Their stronghold is attributed to established supply chains, cost efficiencies, and consumers' deep-rooted familiarity with synthetic ingredients. Mass-market brands, capitalizing on the predictable performance and affordability of these conventional products, ensure broad distribution. This strategy cements their preference, particularly in price-sensitive segments. Blended and mineral oil-based variants, celebrated for their non-sticky feel, convenience, and extended shelf life, have gained immense popularity. Such attributes position conventional oils as daily essentials in both rural and urban households. Even as market dynamics shift, legacy brand loyalty remains steadfast. Thanks to efficient distribution and aggressive marketing, these products not only sustain volume growth but also demonstrate resilience amidst changing consumer demands.

On the other hand, natural and organic hair oils are on an upward trajectory, boasting a robust 9.05% CAGR forecasted from 2026 to 2031. This surge is driven by ingredient-conscious consumers gravitating towards botanical, minimally processed, and sustainably sourced options. This trend resonates with global clean beauty movements, peer-reviewed validations of traditional botanicals, and an intensified consumer focus on ingredient safety. Scientific studies highlight coconut oil's benefits for scalp microbiome health and the growing interest in blends like rosemary-neem for anti-dandruff solutions. In response, brands are adopting transparent labeling, securing organic certifications, and forging supply partnerships to bolster authenticity and premium market positioning. Recent FSSAI labeling regulations emphasize clear ingredient disclosures, organic certification logos, and comprehensive nutritional labeling. This creates a compliance edge for brands genuinely offering natural products, while simultaneously posing challenges for those attempting greenwashing. The most pronounced growth is observed among urban millennials and Gen-Z consumers, whose purchasing decisions are heavily influenced by wellness, sustainability, and ingredient transparency. This shift is not only reshaping product innovation but also redefining marketing strategies across the sector.

By Distribution Channel: Digital Revolution Transforms Access

In 2025, convenience and grocery stores commanded a significant 67.92% share of the Indian hair oil market, underscoring the lasting dominance of traditional retail in both urban and rural locales. These outlets flourish due to their vast geographical reach, established trust, credit offerings, and the deep-rooted relationships between local retailers and their clientele. Their adeptness at catering to both planned purchases and impulse buys solidifies their role in everyday items like hair oil. Moreover, their competitive advantage is bolstered by regional and packaging diversity, offering everything from sachets to small bottles, enabling mass brands to cater to consumers across all income levels. The enduring strength of traditional retail is anchored in decades of community trust and agile inventory management, driving both high foot traffic and repeat business.

Online retail is emerging as the fastest-growing channel, boasting a 8.95% CAGR from 2026 to 2031, fueled by the expansion of e-commerce platforms and shifting consumer habits. In 2025, the beauty and personal care segment experienced a 39% online value growth, largely attributed to platforms like Nykaa. Nykaa not only achieved a commendable Rs 11,800 crore GMV in its beauty vertical but also facilitated same or next-day deliveries for most orders in major cities. Quick commerce models have surged, now representing two-thirds of e-grocery orders. They promise swift deliveries, often under an hour, for hair oil packs. This service is especially popular in Tier-II and Tier-III cities, which accounted for over 60% of e-commerce shipments in 2025. Furthermore, online retail serves as a powerful platform for both emerging D2C brands and established legacy companies. It allows them to sidestep traditional distribution hurdles, broadening market reach, accelerating product launches, and gaining deeper consumer insights. This swift ascent is reshaping brand-consumer interactions, particularly with tech-savvy shoppers prioritizing convenience, variety, and prompt service.

Geography Analysis

In South India, the coconut oil market thrives, thanks to its closeness to raw material sources and deep-rooted consumer habits. The region's reliance on coconut-centric oils is further bolstered by cultural practices and traditional rituals that have been passed down through generations. While Kerala boasts high per-capita consumption and strong brand loyalty, its players grapple with margin pressures due to fluctuations in copra prices, which are influenced by seasonal variations and global demand-supply dynamics. Meanwhile, regions in North and East India show a preference for amla and lighter oil compositions. This not only highlights their diversification potential but also serves as a hedge against commodity risks, providing manufacturers with opportunities to cater to varied consumer preferences. Across urban centers in India, there's a growing demand for international botanicals and microbiome-focused products, underscoring a trend towards premium segmentation driven by increasing awareness and disposable incomes.

Contrary to previous beliefs that premium products were solely in demand in metropolitan areas, Tier-II and Tier-III cities now account for over 60% of e-commerce shipments. This shift is further emphasized by rural markets, which, thanks to improved government road connectivity and mobile internet access, are increasingly turning to branded sachets. These sachets, offering affordability and convenience, are playing a pivotal role in driving market formalization and expanding the reach of branded products to previously untapped regions.

While export opportunities for Indian oils are still in their infancy, they hold significant promise. Communities in the Middle East and North America, well-acquainted with Indian oiling traditions, are showing a keen interest in clinically validated Ayurvedic oils. This presents a lucrative avenue for foreign-currency growth, contingent on strengthening domestic regulatory compliance. Additionally, the growing global focus on natural and organic products aligns well with the positioning of Ayurvedic oils, further enhancing their export potential in the long term.

Competitive Landscape

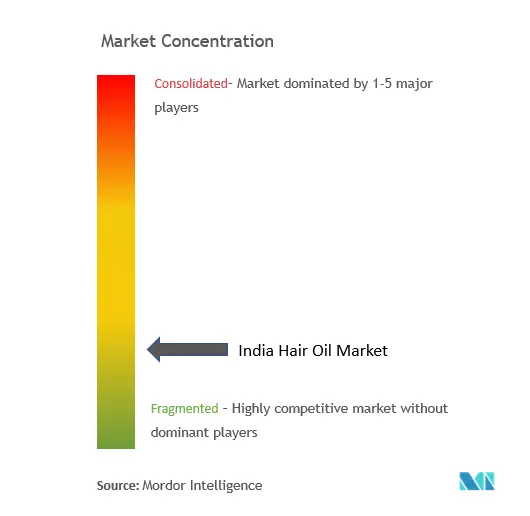

The India Hair Oil Market is moderately concentrated, with established FMCG giants holding significant market positions while facing growing competition from emerging D2C brands and regional players. Legacy FMCG giants Marico, Dabur, Patanjali, and HUL command a moderate market share but are increasingly challenged by agile D2C newcomers leveraging social commerce. While Marico, known for its coconut dominance, diversifies with value-added innovations and men's grooming acquisitions to expand its portfolio, Dabur is amplifying its Ayurvedic focus through the integration of Sesa, aiming to strengthen its position in the natural and herbal product segment. HUL's relaunch of Indulekha underscores the significance of consolidation in refreshing brand portfolios and maintaining relevance in a competitive market.

Scientific validation has become essential; companies now reference in-vitro or clinical studies to back their anti-hair-fall assertions, setting themselves apart from standard oils. This trend reflects the growing consumer demand for evidence-based claims, particularly in the personal care segment. As content-to-commerce strategies yield success in niche markets, companies are ramping up their digital marketing expenditures to engage consumers more effectively and drive conversions. Regional brands, tapping into cultural nuances and offering competitive pricing, often secure deep-rooted loyalty in specific states, leveraging their localized appeal to maintain a strong foothold.

With supply risk management taking center stage, strategies like multi-origin copra contracts, hedging tools, and direct involvement in smallholder coconut plantations are being employed to ensure margin stability and mitigate potential disruptions. Amid increasing scrutiny on ESG matters, corporate commitments to sustainability, such as using recycled PET and plant-based caps, are enhancing their public image and aligning with consumer expectations for environmentally responsible practices.

India Hair Oil Industry Leaders

-

Marico Limited

-

Emami Group

-

Dabur India Ltd.

-

Bajaj Consumer Care Ltd.

-

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Hindustan Unilever debuted its luxury segment product, Nexxus with Oil Resurrection Serum. Designed for the Indian climate, this serum promises to restore hair to its virgin quality in just six drops. It's crafted without sulfates and parabens, harnessing advanced proteomic technology for salon-quality results.

- February 2025: Havintha introduced its new herbal hair oil collection, highlighting ingredients like Kalonji, Ratanjot, Jatamansi, Rosemary, and Almond Oils. This chemical-free range emphasizes scalp health, regulates oil production, and deeply nourishes hair for a naturally radiant look.

- February 2025: Bajaj Consumer Care made a strategic move into the mass segment by acquiring the Banjara’s brand. They also rolled out a youth-centric campaign for Almond Drops Hair Oil, enlisting Kiara Advani as the ambassador to bolster brand leadership and appeal to younger consumers.

- August 2024: Marico introduced Hair & Care Oil in Serum. This innovative product combines the nourishing properties of almond oil with the styling benefits of a serum. Infused with Vitamin E, it tames frizz for a smooth, shiny finish and is attractively priced for budget-conscious shoppers in retail outlets across Eastern and Northeastern India.

India Hair Oil Market Report Scope

Hair oil is an oil-based personal care product intended to improve the condition of hair. The Indian hair oil market is segmented by type and distribution channel. By type, the market is segmented into coconut oil, almond oil, amla oil, castor oil, and other types. Further, based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience stores, online stores, and other distribution channels. For each segment, the market sizing and forecasts have been done on the basis of value (in USD).

By Product Type

| Coconut Oil |

| Almond Oil |

| Amla Oil |

| Castor Oil |

| Other Types |

By Category

| Mass |

| Premium |

By Ingredient Source

| Natural / Organic |

| Conventional |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Stores |

| Other Off-Trade Channels |

| By Product Type | Coconut Oil |

| Almond Oil | |

| Amla Oil | |

| Castor Oil | |

| Other Types | |

| By Category | Mass |

| Premium | |

| By Ingredient Source | Natural / Organic |

| Conventional | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Stores | |

| Other Off-Trade Channels |

Key Questions Answered in the Report

What is the projected value of India hair oil market by 2031?

It is forecast to reach USD 2.67 billion, reflecting a 6.62% CAGR over 2026-2031.

Which oil type is growing fastest in India?

Amla-based hair oils are expected to post a 6.86% CAGR, outpacing other segments.

How are online channels influencing sales?

E-commerce recorded 39% value growth in 2024 and is projected to log a 8.95% CAGR through 2031 as delivery networks deepen in Tier-II/III cities.

Why are input costs volatile?

Weather-linked coconut shortages drove prices to Rs 285-320/kg in 2025, pushing companies toward forward-buying and supply diversification.

Page last updated on: