Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

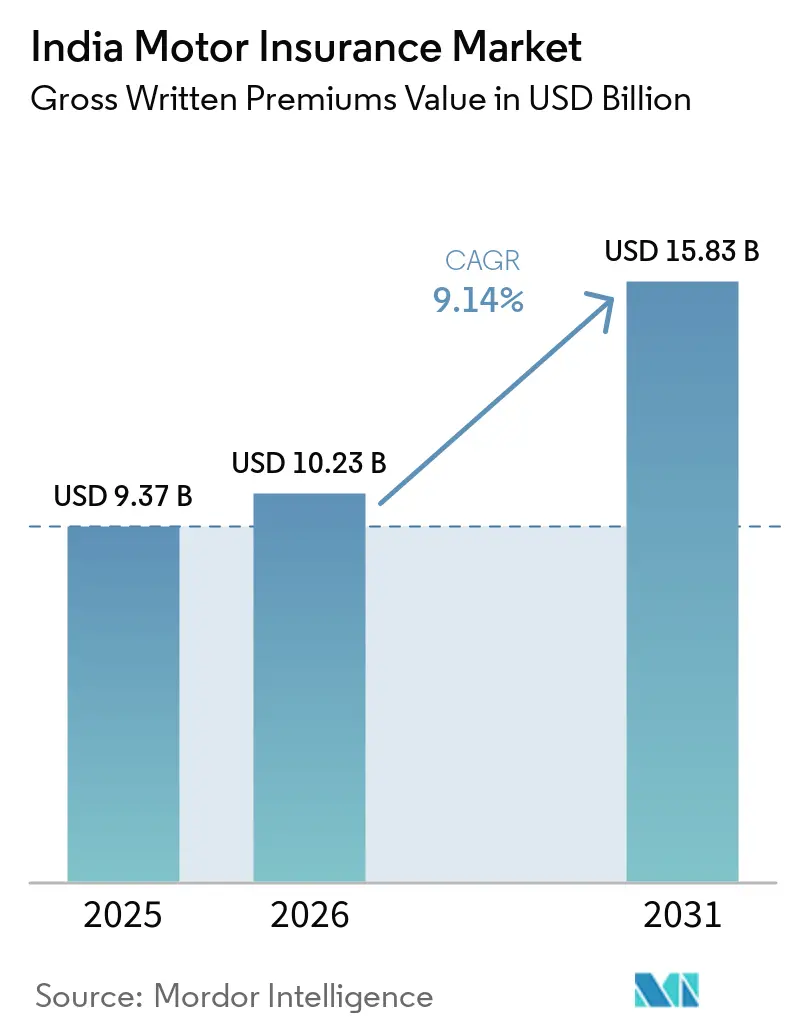

| Base Year Market Size (2025) | USD 9.37 Billion |

| Market Size (2026) | USD 10.23 Billion |

| Market Size (2031) | USD 15.83 Billion |

| Growth Rate (2026 - 2031) | 9.14% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Motor Insurance Market Analysis by Mordor Intelligence

The India Motor Insurance Market size in terms of gross written premiums value is expected to grow from USD 9.37 billion in 2025 to USD 10.23 billion in 2026 and is forecast to reach USD 15.83 billion by 2031 at 9.14% CAGR over 2026-2031.

Regulatory obligations that expand third-party cover, sustain new-vehicle production, and ramp up digital distribution are shaping product mix and pricing strategies in 2026. Insurers are prioritizing reach into underserved commercial fleets and semi-urban districts while tightening claims controls to offset fraud-driven loss pressures. Third-party policies remain dominant due to statutory requirements and price sensitivity, although comprehensive covers are gaining traction as climate risks trigger more own-damage claims. Digital-first journeys are accelerating through the Insurance Regulatory and Development Authority of India (IRDAI)-backed Bima Sugam marketplace, which standardizes comparison, issuance, and servicing for motor policies.

Key Report Takeaways

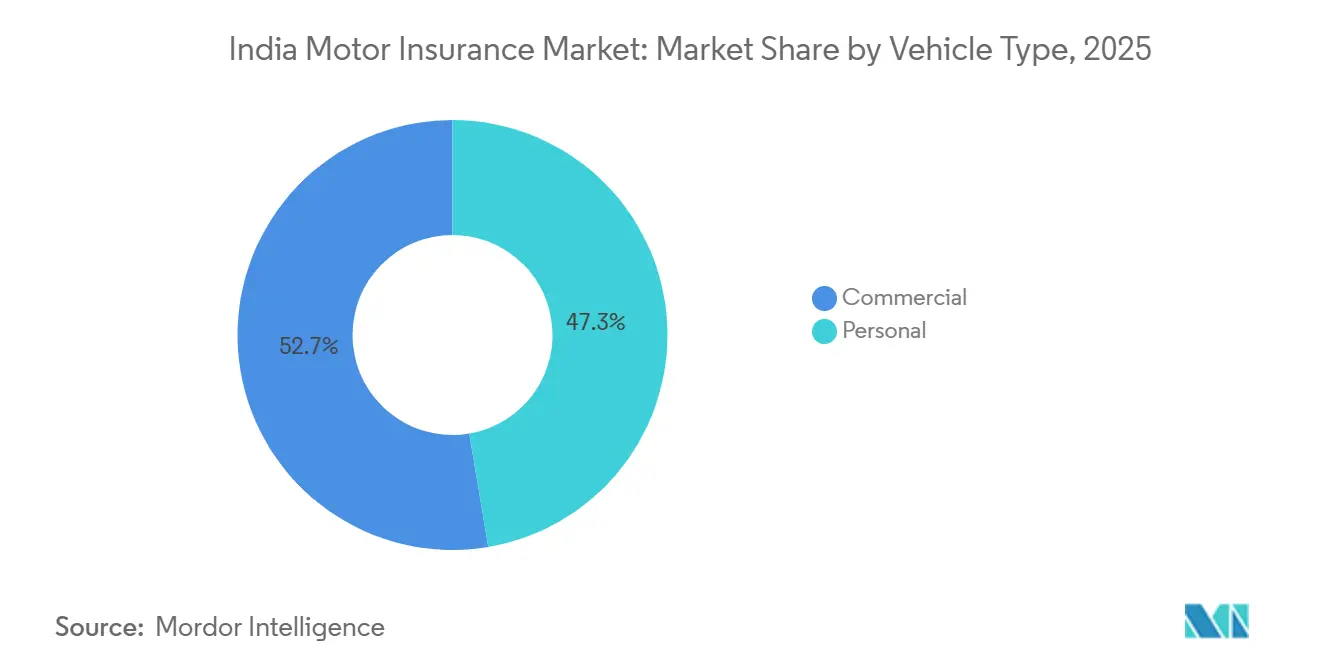

- By vehicle type, personal vehicles (two-wheelers) accounted for 47.34% of the India motor insurance market share in 2025, while commercial vehicles are projected to expand at an 11.33% CAGR through 2031.

- By insurance type, third-party held 66.34% of the India motor insurance market share in 2025, whereas comprehensive is forecast to grow at a 12.35% CAGR through 2031.

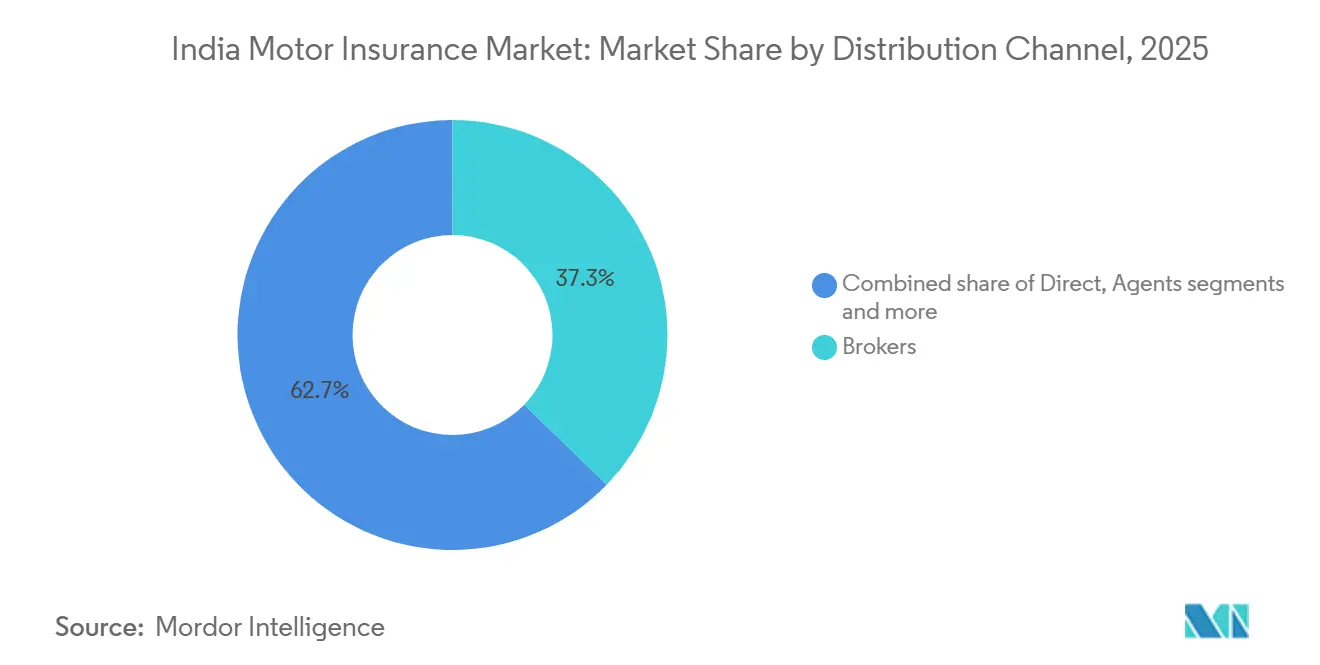

- By distribution channel, brokers commanded 37.26% of the India motor insurance market share in 2025, and direct digital channels are projected to grow at a 13.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Motor Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle ownership & new-vehicle sales growth | +2.8% | National, with peak gains in tier-2/tier-3 cities | Medium term (2-4 years) |

| Mandatory third-party cover under the Motor Vehicles Act & IRDAI enforcement | +1.9% | National enforcement concentrated in urban centers with digital integration. | Short term (≤ 2 years) |

| Digital distribution & aggregator platforms expanding reach | +1.5% | Urban tier-1 initially, cascading to tier-2/tier-3 | Short term (≤ 2 years), Medium term (2-4 years) |

| Higher demand for comprehensive cover amid climate-related loss events | +1.7% | Coastal corridors and flood-prone northern states | Medium term (2-4 years) |

| Telematics-based usage-based insurance pilots receiving regulatory support | +0.9% | Metros first, expanding to commercial hubs | Long term (≥ 4 years) |

| Embedded micro-motor insurance via ride-hailing/e-commerce partnerships | +0.7% | Urban tier-1 and tier-2 gig-economy hubs | Medium term (2-4 years), Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Ownership & New-Vehicle Sales Growth

Production strength and ongoing model launches sustain premium inflows as vehicle additions continue in FY 2025–2026. India’s domestic automobile output in FY 2024–2025 reached 3.10 crore units, anchored by 1.96 crore two-wheelers and 43.02 lakh passenger vehicles, signaling a durable flow of insurable assets [1]Source: SIAM, "Auto Industry Sales Performance of September 2025 and Q2 (July–September 2025)", SIAM.IN. New-sales momentum in Q2 FY 2025–2026 included 8.3% year-on-year growth in commercial vehicle sales to 2,39,781 units and a 7.4% lift in two-wheeler volumes, reinforcing near-term premium expansion. Each registration ties into mandatory third-party coverage under prevailing motor law, translating showroom activity into base policy issuance and supporting the India motor insurance market[2]Source: Ministry of Road Transport and Highways, “Annual Report 2024–25,” Ministry of Road Transport and Highways, morth.nic.in. The India motor insurance market also benefits from premium front-loading in long-term third-party covers for new vehicles, which redirects annual engagement incentives toward comprehensive upsells. Industrial policy, including the Ministry of Heavy Industries’ Production Linked Incentive (PLI) scheme with an outlay of INR 25,938 crore (USD 3.03 billion), is catalyzing domestic supply capacity and reinforcing the insurable base through the current plan period.

Mandatory Third-Party Cover Under the Motor Vehicles Act & IRDAI Enforcement

Statutory third-party liability insurance applies to all vehicles in use, ensuring continued coverage flow even when consumer budgets are tight, which anchors the motor insurance market in India. IRDAI’s 2024 Motor Third Party Obligations framework directs general insurers to underwrite a stepped-up volume of goods-carrying and passenger-carrying vehicles, materially focusing effort on segments with persistent protection gaps. Enforcement capability has improved through digital integration across transport databases, enabling verification of insurance status at the point of use and during compliance checks. Linkages with emergency treatment programs for road accident victims create additional compliance cues by connecting coverage to cashless care pathways supported by dedicated funds. These measures concentrate near-term growth in the India motor insurance market, especially across commercial fleets that historically presented higher uninsured shares.

Digital Distribution & Aggregator Platforms Expanding Reach

The April 2024 rollout of the Bima Sugam Insurance Electronic Marketplace is standardizing policy discovery and purchase, lowering acquisition friction for insurers and improving customer access in smaller cities[3]Source: IRDAI, "Bima Sugam- Insurance Electronic Marketplace", IRDAI.GOV.IN. Digital direct channels, including insurer-owned portals and regulated web aggregators, are expected to outpace agency-led distribution growth through 2030, reinforcing the multi-channel reach of the India motor insurance market. IRDAI’s evolving distribution and onboarding norms around Point of Sales Persons (PoSPs) and Account Aggregator integration enable remote KYC and paperless journeys, which reduce cycle time and support scale economics for carriers. Public sector general insurers have government backing to adopt AI-driven claim settlement for motor own-damage, which can increase customer satisfaction and throughput while curbing operational losses[4]Source: PIB, "Union Finance Minister also emphasised the urgent need for digital transformation across all PSGICs to improve service delivery and efficiency"PIB.GOV.IN. As digital behavior spreads beyond metros, the India motor insurance market gains new access to tier-2 and tier-3 demand with localized interfaces and streamlined app flows.

Higher Demand for Comprehensive Cover Amid Climate-Related Loss Events

India’s climate risk profile continues to drive own-damage claims due to floods and cyclonic rainfall that affect vehicles parked in open or low-lying areas, which draws attention to comprehensive cover in the motor insurance market in India. During 2024, extreme rainfall events in northern states, including Punjab and Uttarakhand, created claim spikes and nudged policy upgrades in flood-prone districts where vehicles are exposed to water ingress and electrical damage. Wider use of Impact-Based Forecasting and improved early-warning systems at the Ministry of Earth Sciences helps reduce casualties and secondary losses, but property and vehicle damage during severe events continues to persist. The Ministry of Home Affairs has reported consistent improvements in preparedness, yet repeated weather shocks keep the demand baseline firm for comprehensive cover in coastal and riverine states in the India motor insurance market. These conditions create favorable upsell dynamics for add-ons such as engine protection, zero depreciation, and roadside assistance in exposed zones across the India motor insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-Sensitive Consumers Favouring Bare-Minimum Third-Party Policies | -1.4% | National; most acute in rural regions and low-income urban clusters | Short term (≤ 2 years), Medium term (2–4 years) |

| Rising Fraudulent Claims Inflating Loss Ratios | -1.1% | Urban high-frequency corridors (Delhi NCR, Mumbai, Bengaluru, Chennai) | Short term (≤ 2 years) |

| Data-Privacy Pushback Slowing Telematics Adoption | -0.6% | Metro and Tier-1 cities with higher digital insurance penetration | Medium term (2–4 years) |

| Spare-Parts Supply-Chain Inflation Squeezing Underwriting Margins | -0.9% | Pan-India; sharper impact in import-dependent OEM and EV-heavy markets | Short term (≤ 2 years), Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Price-Sensitive Consumers Favouring Bare-Minimum Third-Party Policies

Third-party policies accounted for 66.34% of policies in 2025, which shows how statutory compliance and affordability shape selection across large owner cohorts in the India motor insurance market. Long-term third-party mandates for new vehicles front-load premiums and reduce annual touchpoints, which slows comprehensive conversion in early years of ownership, where the market relies on upsell momentum. Rural obligations set by IRDAI aim to expand coverage in gram panchayats, yet these targets can be met with low-margin third-party policies that perpetuate a price-first mix for the India motor insurance market. Income constraints and uneven enforcement encourage many owners to focus on legal minimums, which limit broader protection in vehicle segments with higher accident frequency. Insurers are using digital nudges, simplified add-ons, and transparent claim experience education to encourage upgrades to comprehensive cover in the market.

Rising Fraudulent Claims Inflating Loss Ratios

Fraudulent claims inflate loss ratios and push combined ratios above sustainable levels, driving the adoption of analytics and cross-insurer data sharing in the India motor insurance market. The Insurance Fraud Monitoring Framework Guidelines 2025 mandate dedicated fraud units and participation in information exchange via the Insurance Information Bureau to strengthen detection in the market. Urban corridors with dense traffic and higher claim frequency, including Delhi NCR, Mumbai, and Bengaluru, require tighter repair network audits and identity verification to deter organized fraud. Public sector general insurers are implementing AI-driven claim settlement for motor own-damage, which shortens processing time and flags anomalies more consistently at scale in the India motor insurance market. Incurred claims ratios for state-owned carriers moderated by FY2024, although underwriting pressure and urban claim severities remain active execution priorities in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Two-Wheelers Lead Volume, Commercial Vehicles Accelerate Growth

Personal vehicles (two-wheelers) held 47.34% of the India motor insurance market share in 2025, reflecting their significant presence in registrations and premium volume across both urban and rural mobility. Production and sales momentum continued through Q2 FY2025–FY2026, where two-wheeler volumes rose 7.4% year on year and reinforced a large policy base that sustains renewal flows in the market. Long-term third-party requirements for new two-wheelers sustain initial premium intake, but they reduce annual engagement frequency and move the focus to timed comprehensive upsells in the India motor insurance market. In denser urban zones, risk of theft and accident frequency typically increase the appeal of comprehensive cover and add-ons, especially during monsoon months that elevate water damage claims. Insurers are testing telematics-lite constructs and app-based nudges to lift own-damage conversion among two-wheeler owners in the India motor insurance market.

Commercial vehicles are projected to be the fastest-growing cohort, with an 11.33% CAGR through 2031, supported by logistics expansion and regulatory underwriting obligations that target uninsured goods and passenger carriers in the India motor insurance market. In Q2 FY2025–FY2026, commercial vehicle sales rose 8.3% year on year to 2,39,781 units, extending the premium base for fleet and single-owner operators who require higher liability limits and broader coverage. IRDAI’s obligations framework compels a step-up in coverage across these classes, which narrows uninsured pockets and lifts premium yield in the market. States have adopted vehicle scrapping incentives that include motor vehicle tax concessions up to 25% for non-transport vehicles and 15% for transport vehicles in many jurisdictions, which support fleet refresh and new policy issuance while improving risk quality in the India motor insurance market. Passenger vehicles recorded 43.02 lakh units in FY2024–FY2025, and a higher share of utility vehicles raises average premiums due to higher on-road values and safety feature mandates in the market.

Electric vehicle adoption introduces a growing sub-segment that will require battery and charging-related coverage features tailored to distinct risk profiles in the motor insurance industry in India. EV penetration in new sales reached 7.66% in 2024, with strong commercial adoption pockets such as Chandigarh and rising private adoption in several states, which initiates product variety needs for EV owners. Pricing frameworks for EVs are evolving because claims history, battery durability, and repair network maturity are still developing for consistent actuarial models in the market. State-level leadership in EV adoption, such as Kerala’s higher electric car penetration and Chandigarh’s commercial EV leadership, creates regional demand for specialized products earlier than national averages in the India motor insurance market. Insurers are piloting cover for battery degradation and charging infrastructure liability, which becomes more relevant as EV fleets scale. Over time, growing EV volumes will diversify the premium base and change claims patterns in the market.

By Insurance Type: Third-Party Dominates, Comprehensive Gains Ground

Third-party insurance held a 66.34% share in 2025 and remains the backbone of policy counts due to statutory requirements and buyer price sensitivity in the India motor insurance market. Gross Direct Premium Income for motor third-party reached INR 60,871.70 crore (USD 7.11 billion) in FY2024–FY2025, supported by long-term coverage mandates and focused enforcement that stabilize premium inflow in the market. IRDAI’s ongoing refinements to premium accounting and obligations reporting help maintain clarity and policy discipline in a segment that underwrites road risk at a national scale in the market. As carriers seek balanced growth, they are refining pricing and renewal tactics to defend margins while lifting retention over policy life cycles in the India motor insurance market. Over the forecast period, compliance-driven issuance is expected to continue anchoring the market even as product mix shifts with climate exposure and asset values.

Comprehensive insurance is projected to grow at a 12.35% CAGR between 2026 and 2031, as perceived asset risk and climate volatility push more owners to seek broader protection in the India motor insurance market. Motor own-damage premiums totaled INR 40,435.78 crore (USD 4.73 billion) in FY2024–FY2025, representing a meaningful share of motor line premiums with cross-sell headroom in high-exposure districts of the market. Demand spikes often follow extreme weather forecasts and flood advisories, especially in coastal and riverine states where vehicle water damage is recurrent in the India motor insurance market. Regulatory sandbox pilots enable usage-based propositions that reward low mileage and safe driving behavior, which may improve conversion for comprehensive cover among private owners. Updated cybersecurity guidance in 2025 is helping address privacy concerns that have slowed the adoption of data-driven pricing models in the India motor insurance market.

By Distribution Channel: Brokers Lead, Direct Digital Surges

Brokers captured 37.26% of premium distribution in 2025 and continue to anchor advisory-led placements with claims support that is valued by small fleets and first-time buyers across semi-urban districts in the motor insurance industry in India. The India motor insurance industry relies on hybrid models where brokers and agents complement digital journeys to extend reach and maintain service quality for complex claims. Corporate agency via banks and auto dealership tie-ups sustains flow for private cars and fleet renewals that often require expanded limits or add-on bundles, which support quality growth in the India motor insurance market. PoSP networks enable last-mile enrollment and are being used to embed micro-motor products with related financial services in villages and small towns. As straight-through processing improves, brokers are adopting digital service tools that shorten cycle times and improve transparency across the India motor insurance market.

Direct digital channels that include insurer portals, mobile apps, and regulated aggregators are projected to grow at a 13.76% CAGR through 2031, which positions them to capture a higher share of new policy sales in the India motor insurance market. The Bima Sugam marketplace provides common rails for discovery and servicing and supports paperless onboarding and guided KYC at scale in the market. Public sector general insurers are implementing AI-driven claim settlement for motor own-damage, which can shorten payout cycles and boost customer confidence in digital servicing. Account Aggregator integration enables consent-based data sharing that reduces manual documentation, which improves throughput and lowers drop-off during purchase and claims in the India motor insurance market. Embedded micro-motor propositions on mobility platforms remain early-stage but provide tactical access to gig drivers in tier-1 and tier-2 urban clusters in the market.

Geography Analysis

Maharashtra leads with an 18% share, reflecting high vehicle density in Mumbai and Pune and a broad commercial base that supports steady premium volumes in the India motor insurance market. Tamil Nadu and Karnataka follow with strong automotive manufacturing ecosystems and large IT employment bases that drive private car ownership and higher average comprehensive premiums in the market. Uttar Pradesh holds the largest vehicle base and crossed 1.1 million EVs by early 2025, yet its premium share trails due to lower average vehicle values and a larger two-wheeler mix that skews toward mandatory-only cover in the India motor insurance market. Gujarat’s logistics corridors and financial services activity in GIFT City sustain demand for fleet and private policies that require tailored coverage in the market. Urban premium levels are higher in metros because congestion, theft risk, and advanced repair network costs influence pricing and comprehensive adoption in the market.

Northern states anchored by Delhi NCR, Haryana, Punjab, and Uttarakhand generate strong premium flow from affluent ownership and logistics activity around Gurugram and Noida in the India motor insurance market. Extreme rainfall events recorded in 2024 increased claims in several northern districts and triggered a visible shift toward comprehensive covers where parking exposure and waterlogging are recurrent. Chandigarh led commercial EV adoption in 2024 and is shaping early designs for EV-specific motor cover, which can influence product development in the India motor insurance market. Haryana recorded steady EV adoption across private and commercial categories and is building a base for battery and charging liability products for fleets. These regional patterns require responsive pricing and claim logistics to keep service levels consistent in the India motor insurance market.

Southern and eastern coastal states continue to show elevated demand for comprehensive cover due to repeated cyclone exposure and heavy monsoon flooding in the India motor insurance market. Kerala’s 2024 monsoon season, with reported weather-related casualties and widespread flooding, correlated with increased own-damage claims and policy upgrades in coastal districts in the India motor insurance market. Andhra Pradesh documented significant property damages during recent extreme weather events, which serve as a proxy for motor exposure in the same flood-prone zones that drive cover upgrades. Telangana and Goa recorded meaningful private EV penetration in 2024, which supports early uptake of EV-focused policies, while Tripura’s high overall EV adoption demonstrates how smaller states can become early test beds for specialized products in the market. As insurers refine zonal rating by exposure, premiums are becoming more location-sensitive, where flood gradients are more granular in the India motor insurance market.

Competitive Landscape

India’s motor line operates in a moderately fragmented non-life sector where public sector carriers and leading private players compete on pricing, speed, and digital service in the India motor insurance market. New India Assurance led non-life premiums up to October 2025 with a 13.19% share and INR 25,653.35 crore (USD 3.00 billion), confirming its position among top-tier carriers in the India motor insurance market. ICICI Lombard held an 8.69% share with INR 16,907.38 crore (USD 1.98 billion) and sustained disciplined underwriting in high-loss segments. Bajaj Allianz had 6.92% with INR 13,464.46 crore (USD 1.57 billion), reflecting selective risk appetite across fleet pools and urban corridors. Private carrier adoption of analytics and digital tools is expanding while public sector players are also scaling similar capabilities in the India motor insurance market.

Operational strengthening continues across public sector insurers under government direction, including AI-driven claim settlement for motor own-damage, Account Aggregator-based digital KYC, and refined fraud triage that can curtail leakage in the India motor insurance market. IRDAI’s Insurance Fraud Monitoring Framework makes data sharing through the Insurance Information Bureau mandatory, which supports cross-insurer verification and blocklisting of repeat offenders in the India motor insurance market. State-owned carriers moderated incurred claims ratios by FY2024, though urban accident severity and parts inflation keep loss pressures active in the market. The auto component aftermarket reached INR 99,948 crore (USD 11.68 billion) in FY2025, and ocean freight disruptions increased logistics costs, which influenced repair expenses and claim severity management in the India motor insurance market. These operational changes aim to stabilize margins without diminishing service levels in the market.

Growth opportunities center on rural two-wheeler penetration, EV-specific cover for batteries and charging infrastructure, and commercial fleets where uninsured shares remain significant in the India motor insurance market. Regulatory sandbox pilots for telematics and embedded products via mobility platforms offer efficient on-ramps to new cohorts, supported by common digital rails through Bima Sugam in the India motor insurance market. The Bima Trinity plans, including Bima Vistaar, are intended to improve access in remote and semi-urban locations through simplified products and digital processes in the India motor insurance market. Execution will depend on last-mile trust, claim transparency, and sustained cost control that together influence long-term retention in the market.

India Motor Insurance Industry Leaders

-

New India Assurance

-

ICICI Lombard General Insurance

-

Bajaj Allianz General Insurance

-

HDFC ERGO General Insurance

-

IFFCO Tokio General Insurance

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: BMS Group Ltd announced a strategic partnership with Berns Brett India to establish BMS (India) Ltd, subject to regulatory approval, marking its entry into the Indian insurance broking market. The move expands global specialty insurance players’ footprint in India’s risk advisory and broking landscape.

- December 2025: IRDAI approved a shift to a risk-based capital (RBC) regime and updated accounting standards (aligned with global practices), intended to improve solvency transparency and align Indian insurers with international norms from April 2026. These reforms are expected to impact capital adequacy, underwriting discipline, and product pricing across segments, including motor.

- December 2025: Life Insurance Corporation of India (LIC) entered a partnership with Sahaj Insurance Services to expand insurance access in rural and semi-urban areas, enhancing distribution reach. The expanded network may support cross-selling of general insurance products, including motor, helping improve penetration in underserved markets.

- December 2025: The Madras High Court directed police to register 308 FIRs related to motor claim fraud complaints involving Cholamandalam MS General Insurance and New India Assurance, demonstrating judicial enforcement against insurance fraud. The action signals institutional focus on reducing fraudulent claims that inflate cost structures.

- June 2025: ICICI Lombard reported 11.5% FY25 motor-line growth and projected beating industry expansion by 100–200 basis points in FY26 through digital claims and OEM partnerships.

- March 2025: Bajaj Group acquired Allianz SE’s 26% shareholdings in both Bajaj Allianz entities for INR 24,180 crore (USD 2,827.5 million), forming the country’s largest domestic private insurance company.

India Motor Insurance Market Report Scope

Motor insurance is a form of insurance that provides financial protection for the owner of a vehicle, such as a car, truck, motorcycle, or other road vehicle. It is primarily intended to protect against bodily injury or damage caused by traffic accidents and any liability that may arise from incidents occurring within the vehicle. A complete background analysis of the India Motor Insurance Market, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles are covered in the report.

The India Motor Insurance Market is segmented by motor insurance type (own damage, third party), by application (commercial motor insurance (light motor vehicle, heavy motor vehicle, other commercial motors), private motor insurance), by distribution channel (individual agents, brokers, banks, online, others), by state (Maharashtra, Tamil Nadu, Karnataka, Uttar Pradesh, Gujarat, other states).

The report offers market size and forecasts for the Indian motor insurance market in revenue value (USD) for all the above segments.

By Vehicle Type

| Personal |

| Commercial |

By Insurance Type

| Third Party |

| Comprehensive |

By Distribution Channel

| Direct |

| Agents |

| Brokers |

| Banks |

| Other Distribution Channels |

| By Vehicle Type | Personal |

| Commercial | |

| By Insurance Type | Third Party |

| Comprehensive | |

| By Distribution Channel | Direct |

| Agents | |

| Brokers | |

| Banks | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the projected growth profile for the India motor insurance market through 2031?

The India motor insurance market size is expected to reach USD 15.83 billion by 2031 from USD 9.37 billion in 2025, at a 9.14% CAGR, reflecting regulatory mandates, expanding vehicle ownership, and digital distribution gains.

Which policy type is set to expand fastest in the India motor insurance market?

Comprehensive cover is projected to grow at a 12.35% CAGR through 2031 as climate exposure elevates own-damage risk and add-on adoption.

How are distribution channels shifting in the India motor insurance market?

Brokers hold the largest share at 37.26% while direct digital channels are projected to post a 13.76% CAGR through 2031 with support from the Bima Sugam marketplace.

Which vehicle segments define growth dynamics in the India motor insurance market?

Two-wheelers lead policy counts with a 47.34% share, and commercial vehicles are projected to grow fastest at a 11.33% CAGR through 2031 due to logistics expansion and enforcement-led underwriting.

What regulatory changes are most influential for the India motor insurance market in 2026?

IRDAI’s 2024–2025 frameworks include Rural and Motor Third Party Obligations, the Bima Sugam marketplace, Regulatory Sandbox provisions, and fraud monitoring guidelines, which shape distribution, underwriting, and claims.

Page last updated on: