Wearable Robots And Exoskeletons Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

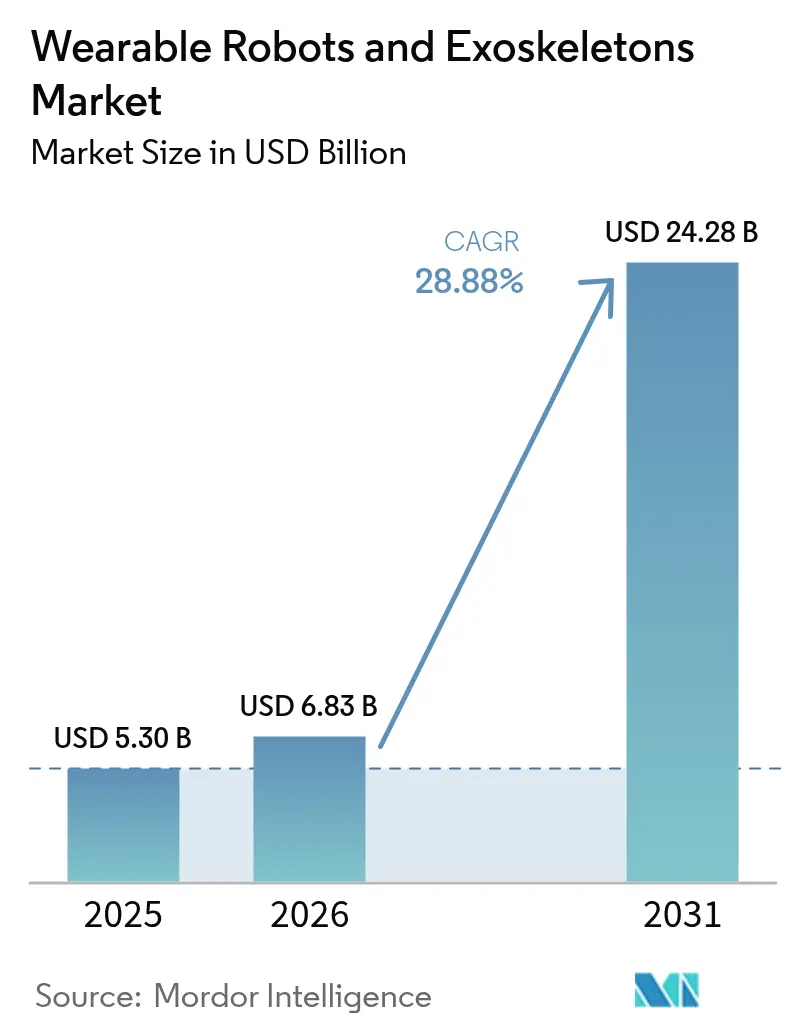

| Market Size (2026) | USD 6.83 Billion |

| Market Size (2031) | USD 24.28 Billion |

| Growth Rate (2026 - 2031) | 28.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wearable Robots And Exoskeletons Market Analysis by Mordor Intelligence

The wearable robots and exoskeletons market size is expected to grow from USD 5.30 billion in 2025 to USD 6.83 billion in 2026 and is forecast to reach USD 24.28 billion by 2031 at 28.88% CAGR over 2026-2031. This growth trajectory underscores a widening gap between rising musculoskeletal-disorder prevalence, surging defense budgets, and employer mandates that prioritize active ergonomics over passive aids. The United States Department of Defense raised fiscal-year 2025 RDT&E funding for soldier-augmentation systems, while the Department of Veterans Affairs removed continuous-supervision requirements that once limited in-home neuro-rehabilitation. Battery-pack prices dipped below USD 140 per kWh in 2024, making full-shift powered designs feasible for logistics fleets. Japanese and European long-term care programs now reimburse assistive robots, expanding the addressable base in super-aged societies. Industrial pilots led by DHL and Hyundai point to rapid corporate adoption once injury-reduction targets become codified in safety KPIs .

Key Report Takeaways

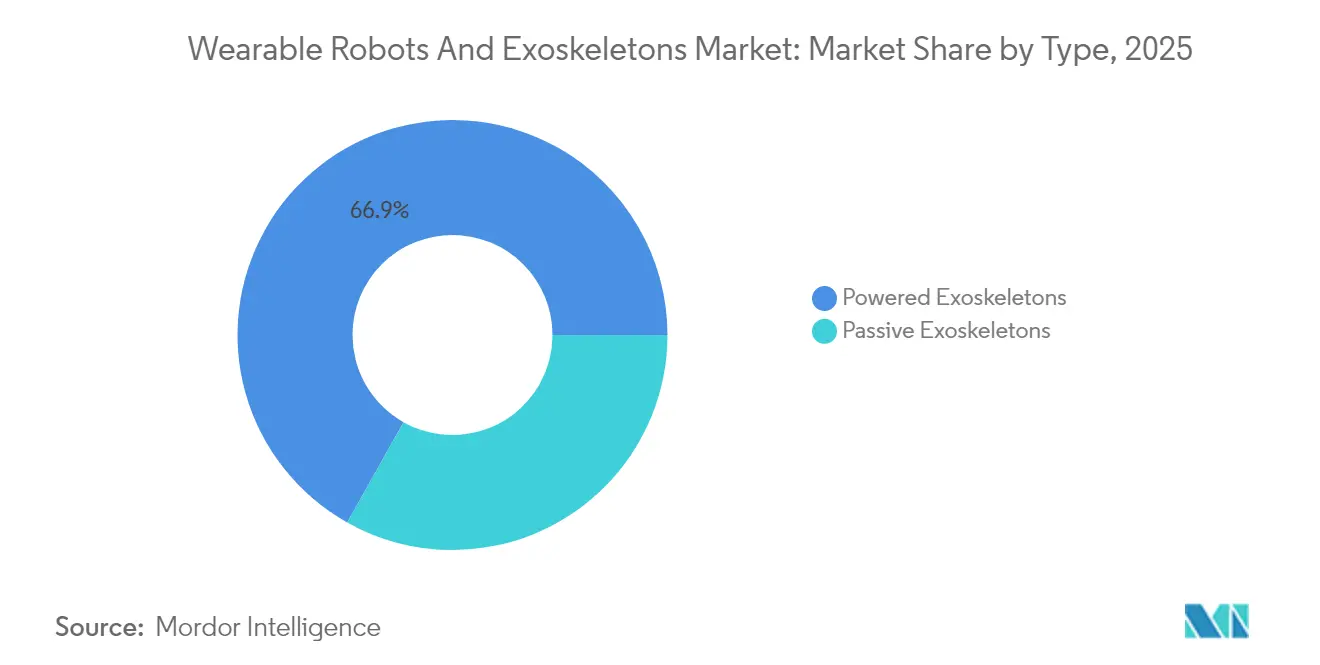

- By type, powered exoskeletons led with 66.85% of the wearable robots and exoskeletons market share in 2025; passive systems are forecast to post a 31.55% CAGR through 2031.

- By component, hardware commanded 73.05% share of the wearable robots and exoskeletons market size in 2025, while software is advancing at 32.05% CAGR through 2031

- By body part assisted, lower-extremity solutions accounted for 59.15% of the wearable robots and exoskeletons market size in 2025; upper-extremity devices are set to grow at 31.05% CAGR. through 2031

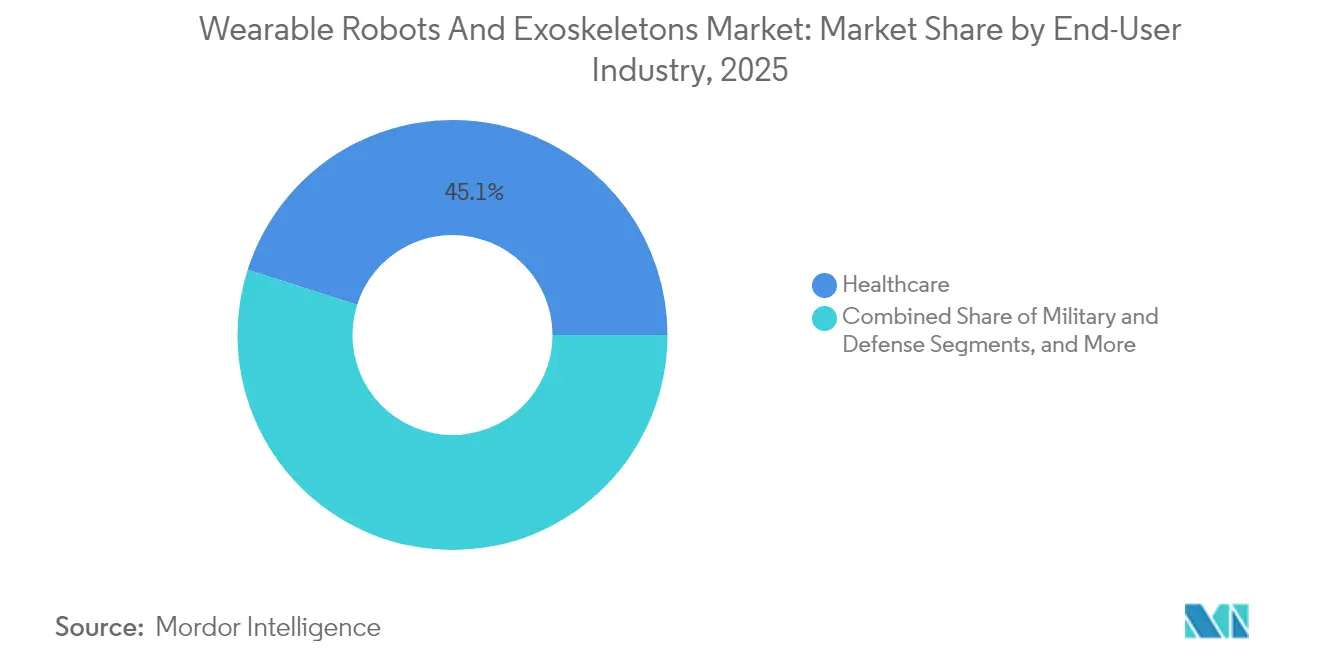

- By end-user industry, healthcare captured 45.10% revenue in 2025; military and defense applications are expanding at 33.2% CAGR through 2031

- By mobility type, mobile configurations made up 71.05% of 2025 deployments and are forecast to grow at 31.4% CAGR through 2031.

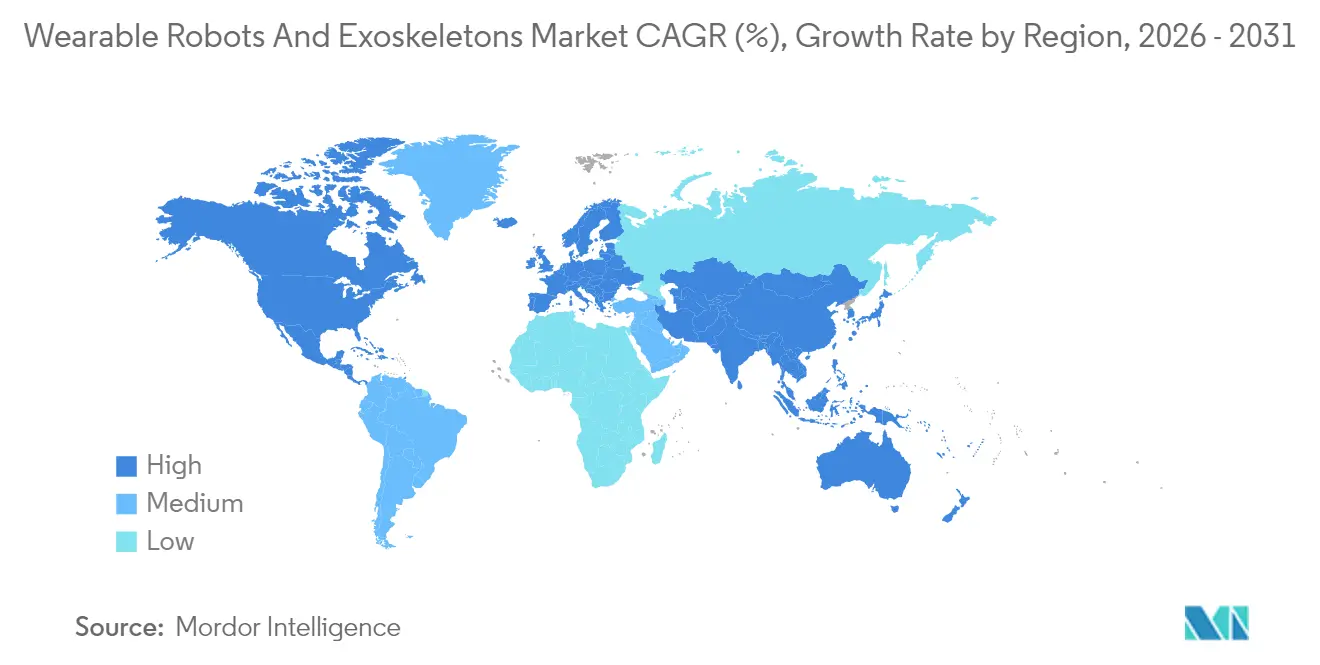

- By geography, North America led with 39.85% revenue in 2025, and Asia Pacific is the fastest climber at 32.1% CAGR through 2031

- Cyberdyne, ReWalk Robotics, Ekso Bionics, Sarcos Technology and Robotics, and Ottobock together controlled nearly 50% of 2024 global revenue, indicating a moderately concentrated field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wearable Robots And Exoskeletons Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-population led surge in musculoskeletal disorders | +6.2% | Global, with concentration in North America, Europe, and Japan | Long term (≥ 4 years) |

| Rapid cost declines in lightweight actuators and battery packs | +7.8% | Global, with supply-chain benefits in Asia Pacific and North America | Medium term (2-4 years) |

| Mandatory workplace-injury reduction targets in heavy industry | +5.4% | North America and Europe, expanding to Asia Pacific manufacturing hubs | Medium term (2-4 years) |

| Record defense budgets earmarked for soldier-augmentation tech | +4.9% | North America, Europe, Middle East | Short term (≤ 2 years) |

| Insurance-reimbursement approvals for in-home neuro-rehab | +3.6% | North America and Europe, limited in emerging markets | Medium term (2-4 years) |

| Emerging lease-as-a-service models for exoskeleton fleets | +2.9% | Global, with early adoption in Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging-Population Surge in Musculoskeletal Disorders

Stroke prevalence climbs sharply after age 55, and older adults already represent 16% of the world population in 2025. The World Health Organization estimates 1.71 billion disability-adjusted life years from musculoskeletal conditions.[1]World Health Organization, “Musculoskeletal Health: Global Burden of Disease Estimates,” who.int Powered gait trainers provide adjustable torque that enables higher-intensity therapy than manual techniques. Japan’s reimbursement for assistive-robot rentals, effective April 2024, accelerated Hybrid Assistive Limb adoption in nursing homes, while the U.S. Centers for Medicare and Medicaid Services opened code E1399 for home-use prescriptions. Clinical trials showed a 23% bump in walking speed after 12-week HAL therapy cycles. These signals demonstrate why healthcare remains the anchor of the wearable robots and exoskeletons market.

Rapid Cost Declines in Actuators and Batteries

Brushless DC motor prices slid 18% between 2022 and 2024 as Chinese plants scaled rare-earth-free rotors, and lithium-ion packs for high-discharge wearables fell to USD 137 per kWh. German Bionic embedded a 1.2 kWh pack in the 4.8 kg Apogee ULTRA, securing 12-hour runtime and 300 rental subscriptions within one quarter. Parker Hannifin’s compact electro-hydraulic actuator now delivers 150 Nm at one-third the weight of pneumatic peers . These shifts lower the bill of materials, propelling the wearable robots and exoskeletons market toward cost-parity with passive braces.

Mandatory Workplace-Injury Reduction Targets

OSHA’s 2024 ergonomic guidance recommends powered exoskeletons for overhead work exceeding 23 kg. Musculoskeletal disorders drove 31% of the 2.8 million U.S. non-fatal injuries in 2024, costing employers USD 15,000 per case. DHL pledged to deploy 500 back-support units by end-2025 to cut lower-back claims 25% . Hyundai’s X-ble Shoulder, rolled out in Alabama and Czech plants, cut shoulder-strain reports 40% in its first quarter. Regulatory backing and quantified ROI illustrate why industrial demand forms a fast-growing wedge within the wearable robots and exoskeletons market.

Record Defense Budgets for Soldier Augmentation

The U.S. FY 2025 budget allocated USD 12.8 million to the Warrior Systems exoskeleton program, a 35% jump year on year. Lockheed Martin’s ONYX trimmed metabolic cost 30% during loaded marches in 10th Mountain Division trials. NATO states collectively raised augmentation R&D outlays 12% in 2024, and Sarcos secured a USD 6.2 million order for 15 Guardian XO suits. Battlefield endurance metrics and logistics use cases reinforce a sizable defense tailwind for the wearable robots and exoskeletons market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront acquisition and lifecycle maintenance costs | -4.7% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Lengthy multi-jurisdictional medical-device certification | -3.2% | Europe, North America, and Asia Pacific | Long term (≥ 4 years) |

| Limited torque-to-weight ratios for full-shift industrial use | -2.1% | Global, particularly in hot-climate regions | Medium term (2-4 years) |

| User-acceptance barriers due to device discomfort and heat | -1.8% | Global, with higher friction in tropical and subtropical zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Acquisition and Lifecycle Maintenance Costs

Industrial units list at USD 40,000–80,000, while healthcare systems face USD 77,000 price tags for home-use devices. Annual maintenance adds up to 20% of initial spend, driven by battery and actuator replacements. German Bionic’s EUR 250 monthly rental still equates to USD 3,396 per year, straining thin-margin firms . Battery swaps every two years cost USD 2,500–4,000; actuator overhauls run USD 5,000–8,000. These economics temper adoption in price-sensitive regions, limiting the near-term upside of the wearable robots and exoskeletons industry.

Lengthy Multi-Jurisdictional Certification

EU Medical Device Regulation stretches approvals to 18–24 months as Notified-Body capacity dwindles to 34 entities. Wandercraft needed 22 months to earn CE marking for its hands-free system. China moved certain powered designs to Class III, layering clinical-trial obligations that add up to 18 months to launch cycles. FDA’s 510(k) can take 180 days but still demands predicate equivalence. Divergent rules compel parallel R&D tracks, lifting cost structures and cooling innovation velocity in the wearable robots and exoskeletons market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Powered Dominance Amid Passive Niche Persistence

Powered designs captured 66.85% of 2025 revenue and are forecast to expand at 31.2% CAGR through 2031, underscoring their pull across healthcare, defense, and heavy-lifting tasks. The wearable robots and exoskeletons market size attributed to powered units is projected to near USD 16.2 billion by 2031, driven by falling actuator prices and subscription models that smooth capital outlays. German Bionic’s rental plan reduces ownership costs 40%, while Lockheed Martin’s ONYX field data signal double-digit endurance gains that military buyers value.

Passive solutions held 33.15% share in 2025, steady demand for rugged, battery-free rigs in construction, agriculture, and maintenance. SuitX’s IX BACK VOLTON blends passive lumbar support with an optional powered mode, illustrating design convergence as buyers seek flexibility without compromising uptime. Passive exoskeletons remain attractive where charging infrastructure is scarce, yet incremental torque benefits mean powered systems will keep widening their reach across the global wearable robots and exoskeletons market.

By Component: Software Gains as Hardware Commoditizes

Hardware delivered 73.05% of 2025 revenue, but commoditization is eroding margins as sensor and motor prices fall. Sensors accounted for 15% of bill-of-materials cost, while actuators still dominate at 45% but are shedding weight and energy draw. Battery innovation looms; solid-state prototypes promise 50% density gains by 2027. Software revenue is pacing at 32.05% CAGR, and fleet dashboards now underpin recurring-revenue bundles.

Fourier Intelligence’s on-device AI tweaks torque in real time, reducing fatigue and differentiating bids in hospital tenders. As a result, software’s slice of the wearable robots and exoskeletons market share will widen as data analytics and remote diagnostics cement themselves in every contract.

By Body Part Assisted: Upper-Extremity Upswing

Lower-extremity systems still led with 59.15% share in 2025, reflecting maturity in stroke and spinal-cord rehabilitation. The wearable robots and exoskeletons market size for lower-limb devices topped USD 3.14 billion in 2025, supported by steady reimbursement wins. However, upper-extremity rigs are sprinting ahead at 31.05% CAGR on the back of automotive and aerospace adoption.

Hyundai’s X-ble Shoulder improved worker-comfort metrics 40% in early deployments, signaling a rising tide for shoulder and elbow devices. Full-body frames remain niche because USD 100,000-plus price tags limit demand to defense and shipyard maintenance, yet Sarcos’ heavy-lift contracts show pockets of growth.

By End-User Industry: Military Momentum

Healthcare remained the anchor at 45.10% revenue in 2025, though its share will ease as defense uptake accelerates. Military programs enjoy earmarked budgets and accelerated procurement; the U.S. Warrior Systems allocation alone jumped 35% year on year.

Industrial and logistics buyers account for roughly 35% of demand and favor subscription models that mesh with OpEx budgets. DHL’s 500-unit roll-out and Airbus’ 12-month pilot validate economic payback for injury reduction and throughput gains. Public safety and consumer niches still trail, yet Tokyo firefighters and ski-assist prototypes point to future adjacency expansion inside the wearable robots and exoskeletons market.

By Mobility Type: Untethered Premium

Mobile exoskeletons owned 71.05% of installations in 2025 and are tracking a 31.4% CAGR as battery density and fleet charging improve. German Bionic’s Apogee ULTRA delivers 12-hour runtime at sub-5 kg weight, giving operators freedom across entire shifts. Tethered rigs remain entrenched in rehabilitation suites where unlimited runtime outweighs mobility.

EksoNR’s cart-based power stage lightens the wearable section, easing fall-risk management during therapy. The dichotomy will persist, yet improved energy density ensures the revenue mix tilts toward mobile designs within the wearable robots and exoskeletons market.

Geography Analysis

North America led with 39.85% revenue in 2025. FDA 510(k) streamlines medical clearances, while USD 12.8 million in FY 2025 Army RDT&E exoskeleton funding signals long-run commitment. VA policy changes removed supervision mandates, boosting veteran access. Canada’s WorkSafeBC offers 50% purchase subsidies, and Mexico’s automotive belt is piloting passive rigs despite training gaps. These factors keep North America atop the wearable robots and exoskeletons market rankings.

Asia Pacific is the fastest climber at 32.1% CAGR. Japan expanded long-term care insurance to cover assistive-robot rentals. Fourier Intelligence installed 120 exoskeletons in Chinese hospitals by late-2024. Hyundai plans 1,000 X-ble Shoulder units by 2026 as South Korea aligns factory automation with labor-safety mandates. India and Australia are early-stage yet promising due to new funding lines and pilot trials. The region’s demographic urgency and reimbursement reforms make it the pivotal growth engine for the wearable robots and exoskeletons market.

Europe held roughly 24.95% of 2025 revenue. MDR lengthens approval cycles to 24 months, benefiting incumbents such as Ottobock and Wandercraft. Germany’s accident-insurance funds reimburse 80% of device costs for high-risk trades. The U.K. National Health Service pilot shows a 30% reduction in therapy hours versus conventional rehab, aiding adoption. Regulatory bottlenecks moderate short-term expansion, yet strong worker-safety cultures sustain demand across the wearable robots and exoskeletons market.

Competitive Landscape

The top five suppliers controlled about 50% of 2024 sales, pointing to moderate concentration. Incumbents leverage regulatory head starts; Cyberdyne and Ekso Bionics both expanded clearances in 2024, widening their reimbursable indications. Hyundai’s vertical integration slashed unit price 30%, spotlighting auto-OEM entry threats. German Bionic’s EUR 250 rental compresses hardware margins yet accelerates fleet scale. Sarcos defends high-capex full-body niches via 47 force-feedback patents, while Wandercraft’s hands-free gait IP addresses daily-mobility segments. IEC 63376 safety certification, expected in late-2025, will raise compliance thresholds, favoring firms with quality-system depth. Regionally, soft-pneumatic forms dominate Japanese elder-care settings, whereas rigid electric frames rule U.S. military and European industrial bids. M&A appetite remains restrained, but joint ventures with battery and AI-software specialists are surfacing to close technology gaps throughout the wearable robots and exoskeletons market.

Wearable Robots And Exoskeletons Industry Leaders

Cyberdyne Inc.

ReWalk Robotics Inc.

Ekso Bionics Holdings Inc.

Honda Motor Co. Ltd

Sarcos Technology and Robotics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: German Bionic launched the Exia exoskeleton, integrating AI-driven load prediction and 14-hour modular batteries. The firm secured agreements with three European logistics firms for 800 units.

- June 2025: Airbus began SuitX shoulder-device pilots in Hamburg and Toulouse lines aiming for 30% injury-claim reductions.

- March 2025: SuitX unveiled IX BACK VOLTON, a 3.2 kg hybrid lumbar brace with 15 Nm powered torque, garnering 400 pre-orders.

- February 2025: Hyundai released the carbon-fiber X-ble Shoulder, deploying 200 units and reporting 40% fewer strain incidents.

Global Wearable Robots And Exoskeletons Market Report Scope

The Wearable Robots and Exoskeletons Market pertains to the worldwide sector engaged in the creation, production, integration, and implementation of powered or passive mechanical devices worn on the body to enhance human strength, endurance, mobility, or rehabilitation results. These systems integrate robotics, sensors, actuators, biomechanics, and AI-based control algorithms to assist or improve human physical abilities in industrial, military, medical, and consumer sectors

The study categorizes the type of exoskeletons as powered exoskeletons and passive exoskeletons. The study also categorizes the use of wearable exoskeletons in various end-user segments, such as healthcare, military and defense, and industrial, among others. The market studied is tracked based on the revenue accrued by vendors operating in the market, received from the sales/rental of the exoskeleton and wearable robots used to enhance the performance of users. Prosthetics are not considered under the scope of the study. Further, the report also covers the analysis of the COVID-19 impact on the market and stakeholders, and the same has been considered for the current market estimation and future projections.

The Wearable Robots and Exoskeletons Market Report is Segmented by Type (Powered, and Passive), Component (Hardware including Sensors, Actuators, Power Sources; Software; and Services), Body Part Assisted (Lower Extremity, Upper Extremity, and Full Body), End-user Industry (Healthcare, Industrial and Logistics, Military and Defense, Other End-user Industry), Mobility Type (Mobile or Wearable, Stationary or Tethered), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Powered Exoskeletons |

| Passive Exoskeletons |

| Hardware | Sensors |

| Actuators | |

| Power Sources | |

| Software | |

| Services |

| Lower Extremity |

| Upper Extremity |

| Full Body |

| Healthcare |

| Industrial and Logistics |

| Military and Defense |

| Other End-user Industrys (Public Safety, Consumer) |

| Mobile / Wearable |

| Stationary / Tethered |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Type | Powered Exoskeletons | ||

| Passive Exoskeletons | |||

| By Component | Hardware | Sensors | |

| Actuators | |||

| Power Sources | |||

| Software | |||

| Services | |||

| By Body Part Assisted | Lower Extremity | ||

| Upper Extremity | |||

| Full Body | |||

| By End-user Industry | Healthcare | ||

| Industrial and Logistics | |||

| Military and Defense | |||

| Other End-user Industrys (Public Safety, Consumer) | |||

| By Mobility Type | Mobile / Wearable | ||

| Stationary / Tethered | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the Wearable Robots and Exoskeletons Market?

The Wearable Robots and Exoskeletons Market size is expected to reach USD 6.83 billion in 2026 and grow at a CAGR of 28.88% to reach USD 24.28 billion by 2031.

What is the current value of the wearable robots and exoskeletons market?

It stands at USD 6.83 billion in 2026 and is forecast to hit USD 24.28 billion by 2031, implying a 28.88% CAGR.

Which segment leads in market share, powered or passive exoskeletons?

Powered models dominate with 66.85% share in 2025, driven by healthcare and heavy-lift use cases.

How quickly are upper-extremity exoskeletons growing?

They are advancing at a 31.05% CAGR through 2031, reflecting automotive and aerospace adoption.

Which region is expanding the fastest?

Asia Pacific shows the highest growth pace at 32.1% CAGR owing to Japanese, Chinese, and South Korean initiatives.

Why are lease-as-a-service models important?

Subscription rentals lower upfront costs, enabling small firms to adopt exoskeletons without major capital outlays while giving manufacturers recurring revenue.

Page last updated on: