Assistive Robotics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

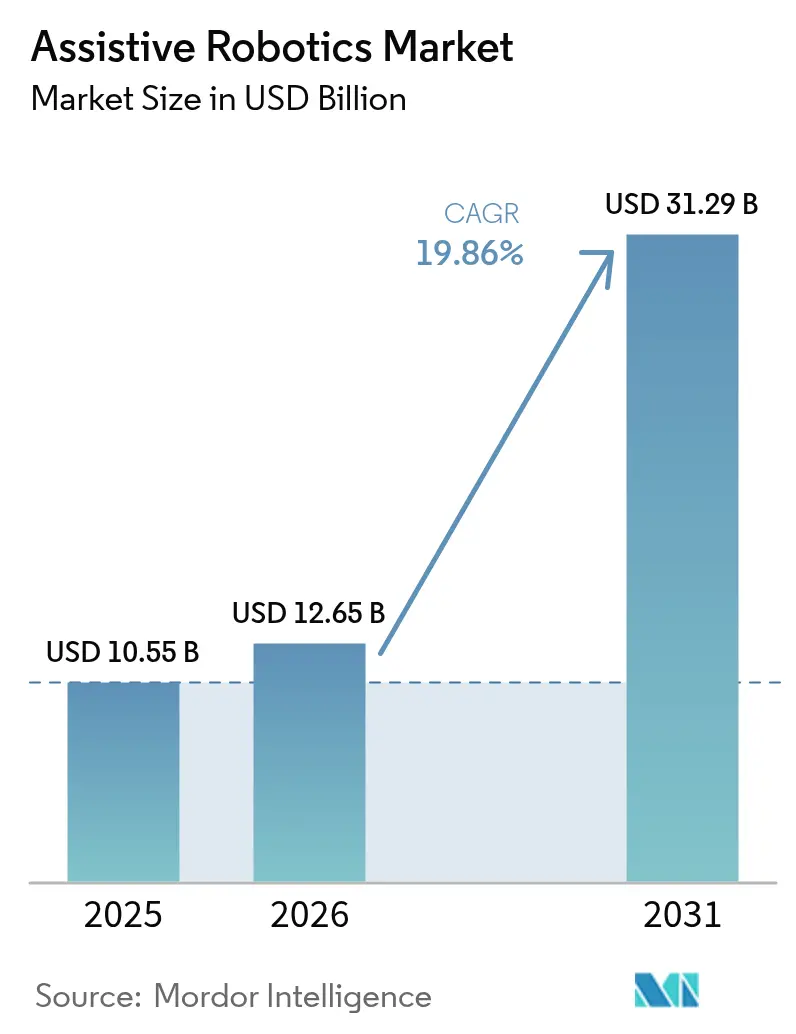

| Market Size (2026) | USD 12.65 Billion |

| Market Size (2031) | USD 31.29 Billion |

| Growth Rate (2026 - 2031) | 19.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Assistive Robotics Market Analysis by Mordor Intelligence

The assistive robotics market size is expected to grow from USD 10.55 billion in 2025 to USD 12.65 billion in 2026 and is forecast to reach USD 31.29 billion by 2031 at 19.86% CAGR over 2026-2031. This rapid expansion coincides with labor shortages in eldercare, growing surgical volumes, and regulators' increasing acceptance of autonomous medical devices, all of which are transforming robots from experimental curiosities into operational necessities. Hospitals are prioritizing multi-modal platforms that combine physical support with cognitive engagement, while home-based rehabilitation is emerging as a mainstream care model. Governments in Japan, South Korea, and China are subsidizing healthcare robots to address demographic pressures, while payers in the United States and Germany are adding reimbursement codes that facilitate capital purchases. Competitive dynamics are driving a shift toward open, AI-enabled systems, and supply-chain volatility in precision sensors is prompting manufacturers to adopt dual-sourcing strategies.

Key Report Takeaways

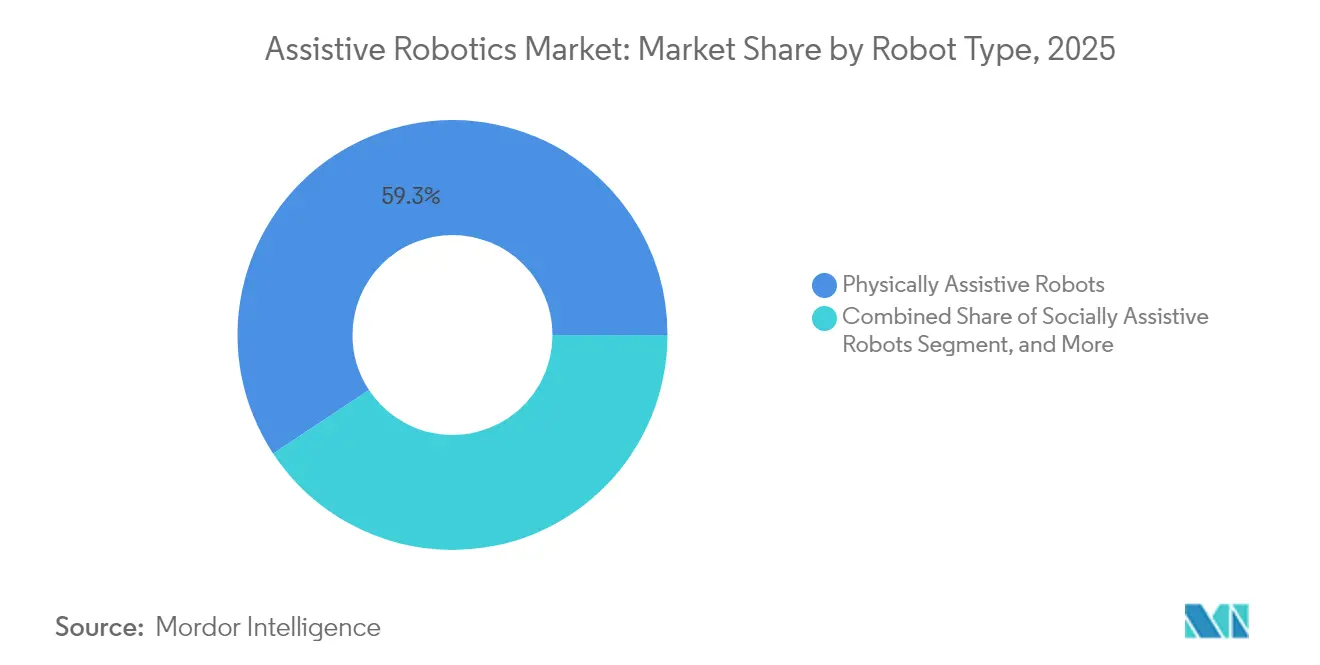

- By robot type, physically assistive platforms led with 59.28% revenue share in 2025; mixed assistive robots are forecast to expand at a 21.65% CAGR through 2031.

- By mobility, mobile systems captured 57.05% of the assistive robotics market share in 2025, while the segment is projected to grow at a 21.05% CAGR through 2031.

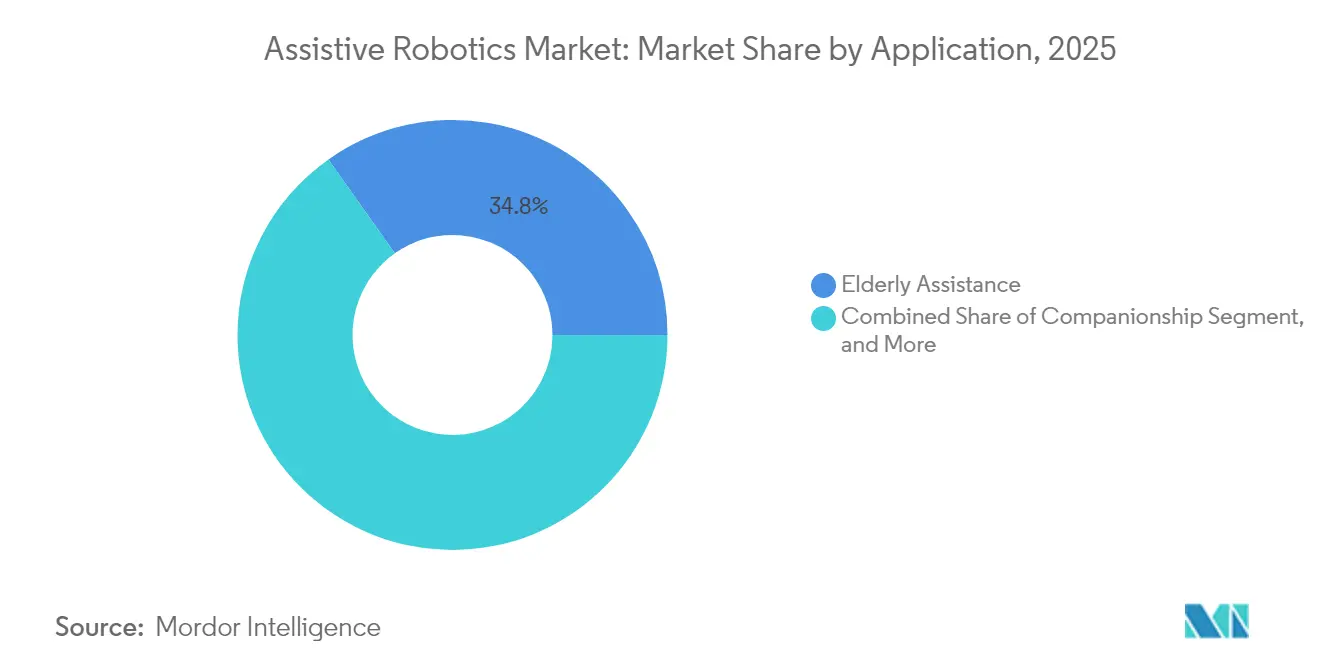

- By application, elderly assistance led with 34.79% revenue share in 2025; surgery assistance accounted for a 21.32% CAGR forecast between 2026 and 2031, outpacing all other use cases.

- By end user, hospitals led with 54.43% revenue share in 2025; homecare settings are projected to advance at a 21.95% CAGR through 2031.

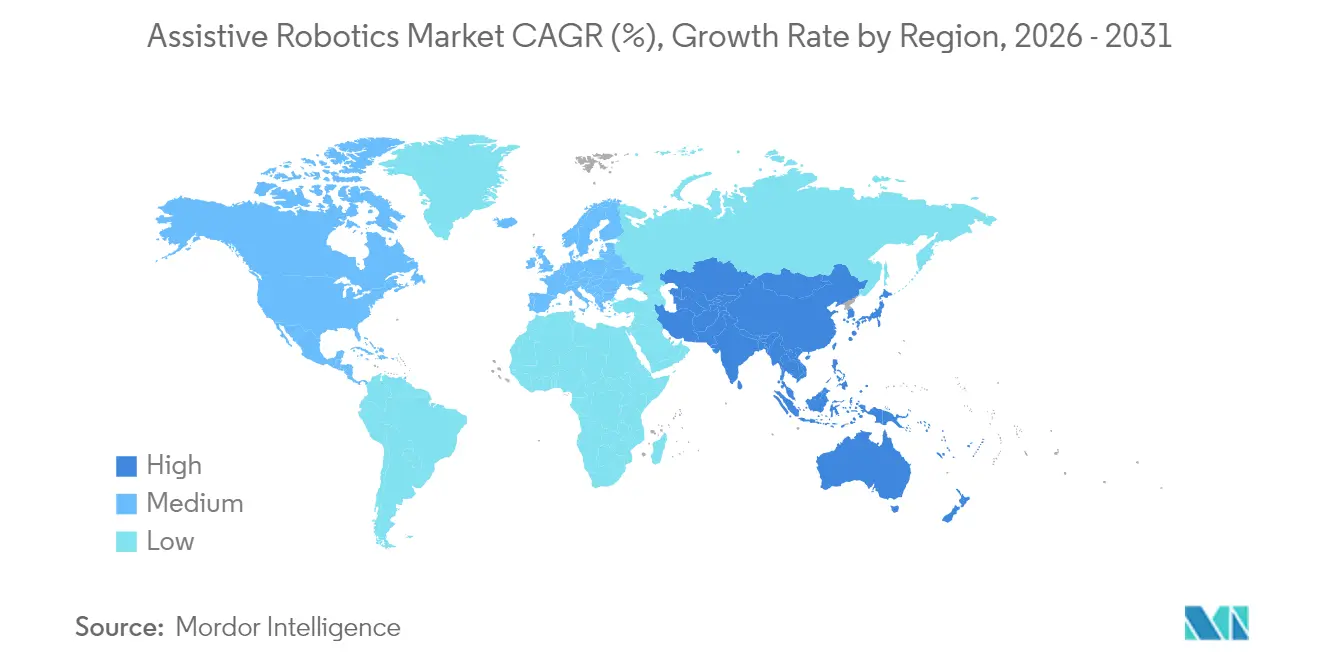

- By geography, North America led with a 39.62% revenue share in 2025; the Asia Pacific is projected to expand at a 22.35% CAGR from 2026 to 2031, surpassing North America’s growth pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Assistive Robotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising geriatric population accelerating care demand | +5.2% | Global, most acute in Japan, South Korea, Italy, Germany | Long term (≥ 4 years) |

| Growing adoption of robot-assisted surgery procedures | +4.8% | North America and Europe, expanding into APAC urban centers | Medium term (2-4 years) |

| Integration of AI with assistive robots enhancing autonomy | +3.9% | Global, led by United States, China, Israel | Medium term (2-4 years) |

| Surge in home-based rehabilitation and tele-rehabilitation models | +3.1% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Emergence of soft robotics improving safety and wearability | +2.4% | Global, with early traction in Japan and United States | Long term (≥ 4 years) |

| Government reimbursement for exoskeletons in select markets | +1.8% | Japan, Germany, United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Geriatric Population Accelerating Care Demand

Global aging is widening the caregiver gap, prompting providers to turn to robotic solutions that help alleviate workforce shortages.[1]United Nations, “World Population Ageing Report 2024,” UN.ORG Japan mandated the installation of robotic lifts in all new nursing facilities starting in 2025, triggering significant orders for transfer-assist platforms. South Korea has allocated USD 120 million to deploy companion robots in 5,000 senior centers by 2027, framing robots as a solution to social isolation. Italy reported that 23% of citizens over 65 live alone, which is accelerating the adoption of social-cognitive robots for medication reminders and emergency alerts. Robots costing USD 30,000 can offset the cost of 0.5 full-time caregivers over five years in high-wage countries, resulting in a sub-three-year payback and validating their economic viability.

Growing Adoption of Robot-Assisted Surgery Procedures

Hospitals in the United States performed more than 1.5 million robotic surgeries in 2024, a 22% increase year-over-year, driven by new reimbursement codes that now cover partial nephrectomy and lobectomy procedures.[2]American College of Surgeons, “Robotic Surgery Statistics 2024,” FACS.ORG Stryker’s Mako orthopedic platform reached 1,500 installed units by late 2024, with revision surgeries decreasing by 30% compared to manual techniques. Europe’s Medical Device Regulation streamlined software update approvals, enabling AI planning tools that reduce operative time by 18 minutes per procedure. The resulting productivity boosts support hospital capital budgets and encourage community facilities to join the adoption curve.

Integration of AI with Assistive Robots Enhancing Autonomy

Kinova’s Gen3 arm utilizes vision and reinforcement learning to adjust grasping according to object weight and shape, eliminating the need for manual reprogramming. The United States Food and Drug Administration cleared three AI-enabled rehabilitation robots in 2024, reflecting regulatory comfort with autonomy in patient-facing systems.[3]U.S. Food and Drug Administration, “510(k) Clearances - Rehabilitation Robotics 2024,” FDA.GOV China published AI safety standards for service robots that require fail-safe protocols, signaling seriousness about export-ready compliance. Large language models integrated into social robots now support 15-minute cognitive assessments, enriching clinical decision-making.

Surge in Home-Based Rehabilitation and Tele-Rehabilitation Models

Hocoma’s Armeo Power gained FDA clearance for home use in 2024, letting stroke survivors complete therapy under remote supervision. Medicare began reimbursing clinicians for up to 40 minutes of remote therapeutic monitoring per month, catalyzing device orders among home-health agencies. ReWalk Robotics shifted 35% of exoskeleton sales to households as coverage expanded and a lighter battery module improved residential usability. Tele-rehabilitation platforms integrating robotics generated USD 1.2 billion in revenue in 2024, with rural regions capturing the most upside.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and maintenance costs for healthcare providers | -3.6% | Global, most acute in emerging markets and rural systems | Short term (≤ 2 years) |

| Limited clinical evidence for long-term outcomes | -2.1% | Global, particularly Europe and North America | Medium term (2-4 years) |

| Fragmented regulatory frameworks slowing approvals | -1.8% | Europe, Latin America, Southeast Asia | Medium term (2-4 years) |

| Supply chain volatility in critical sensors and actuators | -1.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs for Healthcare Providers

Robotic surgery systems cost USD 1.5-3.0 million upfront and require annual service contracts averaging USD 150,000, which restricts their adoption among community hospitals with low case volumes. Exoskeletons priced at USD 80,000-120,000 face similar hurdles outside large academic centers. Exclusive maintenance agreements exacerbate the total cost of ownership, and pay-per-procedure leases often shift risk back onto providers. These financial barriers remain acute in emerging markets where capital budgets are limited.

Limited Clinical Evidence for Long-Term Outcomes

A 2024 systematic review found only 12% of exoskeleton studies extended beyond six months, leaving payers hesitant to fund multi-year deployments. Companion robots face an even thinner evidence base, leading NICE to withhold routine coverage in 2024 due to insufficient data on cost-effectiveness. Manufacturers are launching real-world registries, but actionable results are not expected to arrive before 2027, creating a near-term drag on market acceleration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Robot Type: Multifunctional Platforms Win Budget Approval

Mixed platforms are projected to expand at a 21.65% CAGR, outpacing physically assistive incumbents as healthcare systems seek single investments that tackle mobility and social-cognitive needs. Physically assistive solutions held 59.28% of 2025 revenue, but growth is moderating as saturation builds in core lifting and transfer applications. Socially assistive robots remain the smallest slice, yet increased demand for cognitive engagement in memory care is driving orders for conversational units. Panasonic’s Hospi now bundles a greeting interface that reduced nurse call-button use by 18% in trials.

Providers appreciate the modularity of mixed robots, which can add or remove arms, screens, or conversational software to fit patient requirements, extending lifecycles and smoothing return on investment. Regulators are clarifying the paths for combination devices, simplifying approvals that previously required dual submissions. This framework is expected to shorten commercialization cycles and fuel broader adoption of hybrid designs.

By Mobility: Untethered Designs Capture Homecare Momentum

Mobile robots commanded 57.05% of the revenue in 2025 and are projected to track a 21.05% CAGR, as simultaneous localization and mapping algorithms enable autonomous navigation in cluttered homes. Stationary robots remain critical in operating rooms that need sub-millimeter accuracy, yet their fixed nature limits cross-departmental utility. Hospitals deploy mobile units for logistics, with autonomous carts now handling 30% of internal deliveries at many U.S. medical centers.

The Asia Pacific leads the mobile shift, where urban homes’ tight footprints demand adaptable systems, whereas North America retains a larger stationary base, thanks to spacious residences that can accommodate fixed rehabilitation setups. Supply constraints in precision sensors could hinder mobile deployments, but manufacturers are redesigning boards to accommodate multiple sensor brands, thereby protecting shipment schedules.

By Application: Surgical Robotics Drives the Fastest Revenue Uptick

Elderly assistance accounted for 34.79% of 2025 revenue, while surgery assistance is the fastest-growing application, with a 21.32% CAGR through 2031. The widening reimbursement landscape for orthopedic and minimally invasive procedures is a prime catalyst. Robotic systems reduce the need for open surgery by 40% in complex cases, a metric that CFOs directly translate into shorter lengths of stay and fewer readmissions.

Handicap assistance follows in growth as private insurers broaden coverage beyond workplace accidents. Companion robots are becoming increasingly common in memory-care wings, where they deliver medication reminders and engage residents in cognitive games. Defense customers are adopting medical-grade robots for search and rescue, validating cross-domain use cases that could upscale production volumes and reduce per-unit costs in healthcare.

By End User: Homecare Surges Under Readmission Penalties

Hospitals accounted for 54.43% of revenue in 2025, yet homecare is growing at the fastest rate, with a 21.95% CAGR, as payers penalize avoidable readmissions under programs such as the United States Hospital Readmissions Reduction initiative.

ReWalk’s lighter exoskeletons and Barrett Technology’s WAM arm both recorded double-digit sales to individual consumers, illustrating the direct-to-patient pivot. Rehabilitation centers are differentiating themselves through the use of advanced robotics to justify premium rates, while nursing homes are increasingly leasing exoskeletons to manage staffing gaps.

Geography Analysis

North America remains the largest regional buyer, accounting for USD 4.18 billion of the assistive robotics market size in 2025, and benefiting from cohesive reimbursement frameworks, robust venture funding, and a dense cluster of surgical robot manufacturers. The United States anchors demand as Medicare opens coverage to new orthopedic indications, and the Veterans Health Administration deploys exoskeletons for mobility-impaired veterans. Canada’s provincial pilots signal early momentum, though broad coverage decisions remain pending.

Europe contributed approximately USD 2.16 billion in 2025 sales, led by installations in Germany and the United Kingdom. Germany’s statutory insurance coverage for robotic gait therapy spurred a 35% spike in Lokomat orders, while French caps on annual reimbursement restrain device classes eligible for coverage. Southern and Eastern European markets are price-sensitive, with Italy and Spain emphasizing lower-cost manual therapy despite favorable clinical data.

The Asia Pacific region booked USD 3.58 billion in 2025 revenue and is projected to surpass North America by 2028. Japan’s Ministry of Health, Labour and Welfare is funding offsets for upfront costs of nursing-home robots, and South Korea’s robotics innovation fund is investing USD 200 million in early-stage firms. China’s policy push for one million service robots by 2027 has driven a 48% rise in healthcare installations, with domestic brands capturing a significant share of the hospital market through aggressive pricing. Australia and New Zealand continue to adopt homecare robots under disability and accident schemes.

The Middle East and Africa generated USD 0.27 billion in 2025, with the United Arab Emirates leveraging partnerships to establish itself as a regional hub for robotic rehabilitation.

South America posted USD 0.36 billion, underpinned by Brazil’s private health insurance segment investing in surgical robotics to attract medical tourists. Despite smaller baselines, both regions could accelerate as telemedicine infrastructure reduces barriers to support services.

Competitive Landscape

Assistive robotics presents a moderately fragmented structure. Intuitive Surgical controls 70% of surgical-robot revenue, backed by 8,500 installed da Vinci units and a thriving consumables pipeline that produced USD 6.2 billion in 2024 service and instrument sales. Medtronic’s Hugo obtained FDA clearance for urology in 2024, and Johnson and Johnson’s Ottava platform is slated for 2026, introducing price-competitive pressure. Rehabilitation and mobility assistance remain dispersed, with no firm exceeding a 15% share, leaving room for differentiated user interfaces or EHR integrations.

Strategic movement favors open architectures. Kinova released public APIs in 2024, sparking the development of third-party accessories and deepening customer lock-in through ecosystem effects. Stryker’s USD 240 million acquisition of Serf SAS integrates AI surgical planning onto its Mako platform, reinforcing a data-driven moat. Hyundai Motor Company launched the USD 35,000 H-MEX exoskeleton, leveraging automotive supply chains to undercut medical-device pricing. Patent activity in soft robotics rose 62% year-over-year, with 340 compliant-actuator grants in 2024 alone.

Supply-chain volatility in sensors has doubled lead times, increasing from six months in 2023 to 12 months in 2025, prompting dual sourcing, design revisions, and strategic stockpiling across manufacturers. Evidence gaps remain a headline risk; long-term outcome studies, especially for socially assistive systems, trail commercialization timelines and could temper payer adoption.

Assistive Robotics Industry Leaders

Kinova Inc.

Ekso Bionics Holdings Inc.

Cyberdyne Inc.

Focal Meditech BV

ReWalk Robotics Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Cyberdyne launched its HAL-Hybrid Assistive Limb 2.0 in Europe and North America, featuring modular hip and knee actuators and priced at JPY 4.8 million (USD 32,000) per unit to accelerate adoption in outpatient rehabilitation clinics.

- March 2025: Intuitive Surgical partnered with NVIDIA to integrate real-time AI surgical guidance into the da Vinci 5 platform, aiming to cut operative time by 15% pending expected FDA clearance later in 2025.

- February 2025: Fourier Intelligence secured USD 60 million in Series C funding led by Sequoia Capital China to expand production of its M2 lower-limb exoskeleton and establish a United States manufacturing facility.

- January 2025: Ekso Bionics received FDA clearance for its EksoNR exoskeleton for home use by stroke patients, becoming the first powered exoskeleton approved for unsupervised residential rehabilitation.

Global Assistive Robotics Market Report Scope

The assistive robotics market report is segmented by Robot Type (Physically Assistive Robots, Socially Assistive Robots, Mixed Assistive Robots), Mobility (Mobile Robots, Stationary Robots), Application (Elderly Assistance, Handicap Assistance, Surgery Assistance, Companionship, Public Relation, Industrial Tasks, Defense and Search and Rescue), End User (Hospitals, Rehabilitation Centers, Homecare Settings, Other End User), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Physically Assistive Robots |

| Socially Assistive Robots |

| Mixed Assistive Robots |

| Mobile Robots |

| Stationary Robots |

| Elderly Assistance |

| Handicap Assistance |

| Surgery Assistance |

| Companionship |

| Public Relation |

| Industrial Tasks |

| Defense and Search and Rescue |

| Hospitals |

| Rehabilitation Centers |

| Homecare Settings |

| Other End User |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Robot Type | Physically Assistive Robots | ||

| Socially Assistive Robots | |||

| Mixed Assistive Robots | |||

| By Mobility | Mobile Robots | ||

| Stationary Robots | |||

| By Application | Elderly Assistance | ||

| Handicap Assistance | |||

| Surgery Assistance | |||

| Companionship | |||

| Public Relation | |||

| Industrial Tasks | |||

| Defense and Search and Rescue | |||

| By End User | Hospitals | ||

| Rehabilitation Centers | |||

| Homecare Settings | |||

| Other End User | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of assistive robotics by 2031?

The assistive robotics market is expected to reach USD 31.29 billion by 2031 based on a 19.86% CAGR between 2026 and 2031.

Which application is growing fastest?

Surgery assistance is expanding at a 21.32% CAGR through 2031, driven by widening reimbursement and proven clinical benefits.

Why are mobile assistive robots attracting investment?

Mobile platforms capture 57.05% of 2025 revenue and support home-care growth because untethered navigation enables use in varied residential layouts.

How are governments influencing adoption?

Subsidies in Japan and South Korea and China’s strategic policy support are cutting upfront costs and accelerating hospital deployments.

What challenges slow adoption among smaller hospitals?

Upfront costs of USD 1.5-3.0 million per surgical system and annual maintenance of about USD 150,000 inhibit purchases by community facilities.

Which region will grow the fastest through 2031?

Asia Pacific is expected to post a 22.35% CAGR through 2031 as demographic urgency and policy incentives converge to support large-scale rollouts.

Page last updated on: