Rehabilitation Robots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

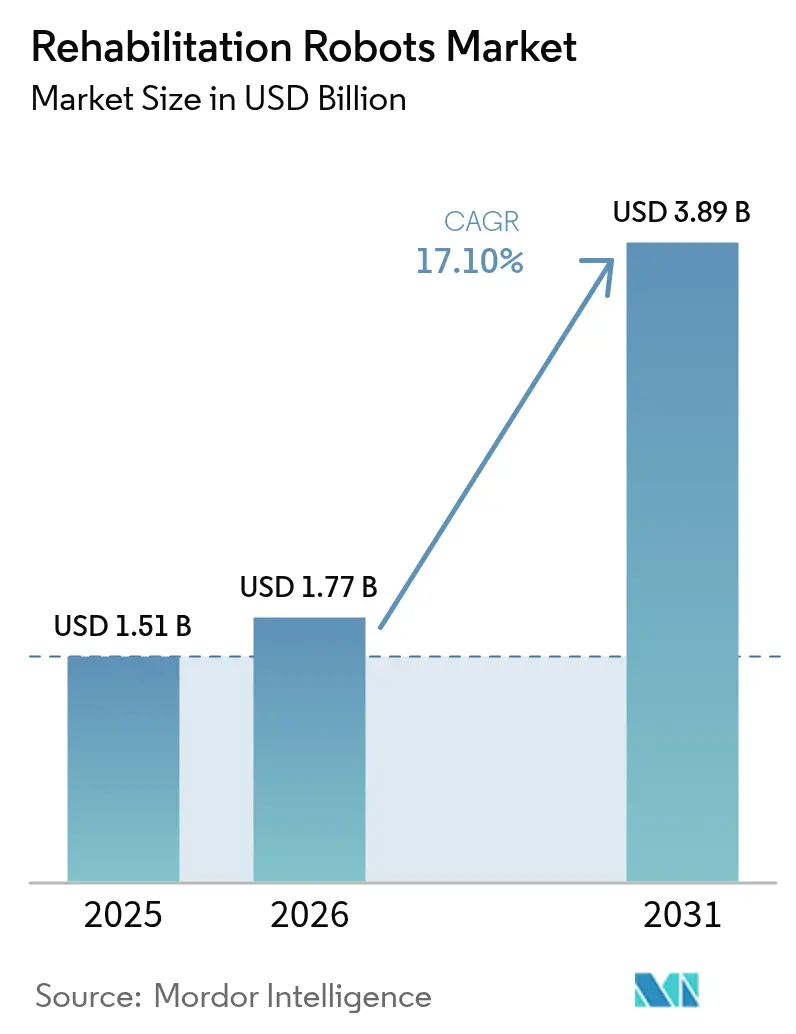

| Market Size (2026) | USD 1.77 Billion |

| Market Size (2031) | USD 3.89 Billion |

| Growth Rate (2026 - 2031) | 17.10% CAGR |

| Fastest Growing Market | Asia |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Rehabilitation Robots Market Analysis by Mordor Intelligence

Rehabilitation robots market size in 2026 is estimated at USD 1.77 billion, growing from 2025 value of USD 1.51 billion with 2031 projections showing USD 3.89 billion, growing at 17.1% CAGR over 2026-2031. The growth reflects demographic aging, favorable reimbursement shifts, and rapid engineering progress that together widen access to advanced neuro-orthopedic therapy. Medicare’s 2024 decision to treat personal exoskeletons as braces—covering roughly 80% of USD 100,000 devices has immediately improved affordability for home users. Exoskeletons dominate institutional settings thanks to mature clinical evidence, while lightweight soft-robot designs accelerate adoption in domestic environments. Capital inflows, exemplified by Wandercraft’s USD 75 million Series D round, continue to lower technology costs and expand product portfolios. Nonetheless, high up-front expenditure and mixed long-term outcome data temper procurement decisions, especially in pediatric and emerging-market use cases.

Key Report Takeaways

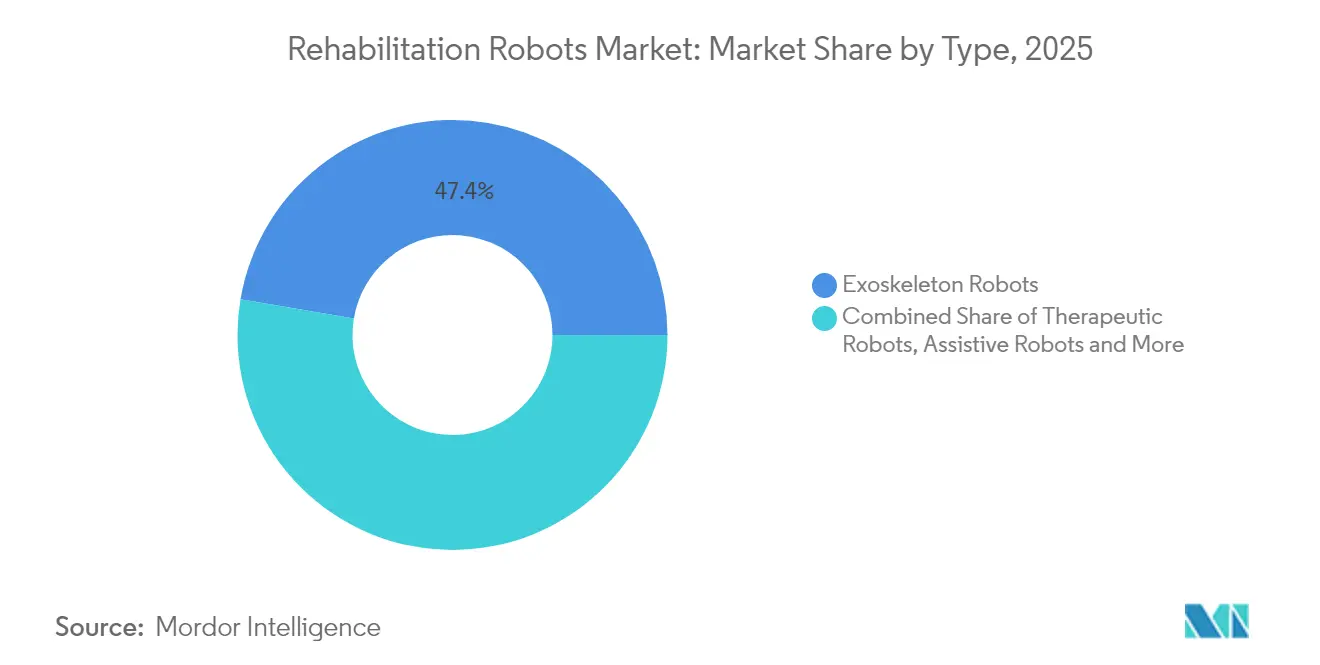

- By type, exoskeleton robots led with 47.35% rehabilitation robots market share in 2025, while wearable soft robots are set to grow at a 29.6% CAGR to 2031.

- By therapy area, upper-limb systems accounted for 54.60% of segment revenue in 2025; full-body gait platforms post the fastest CAGR at 23.4% through 2031.

- By patient group, geriatric users commanded 61.40% share of the rehabilitation robots market size in 2025 and will expand at 18.4% CAGR to 2031.

- By mobility level, stationary platforms retained 65.30% revenue in 2025; mobile over-ground solutions are projected to scale at 27.3% CAGR to 2031.

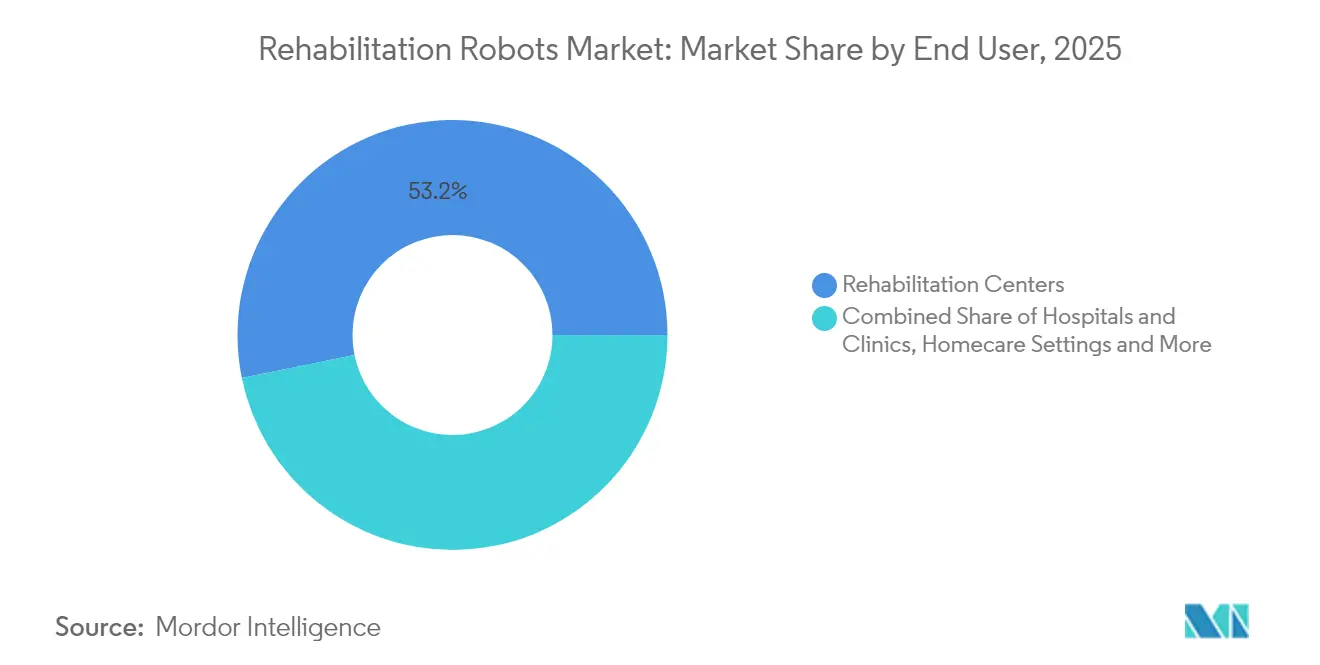

- By end user, rehabilitation centers held 53.20% of the rehabilitation robots market in 2025, whereas homecare adoption is rising at a 27.1% CAGR.

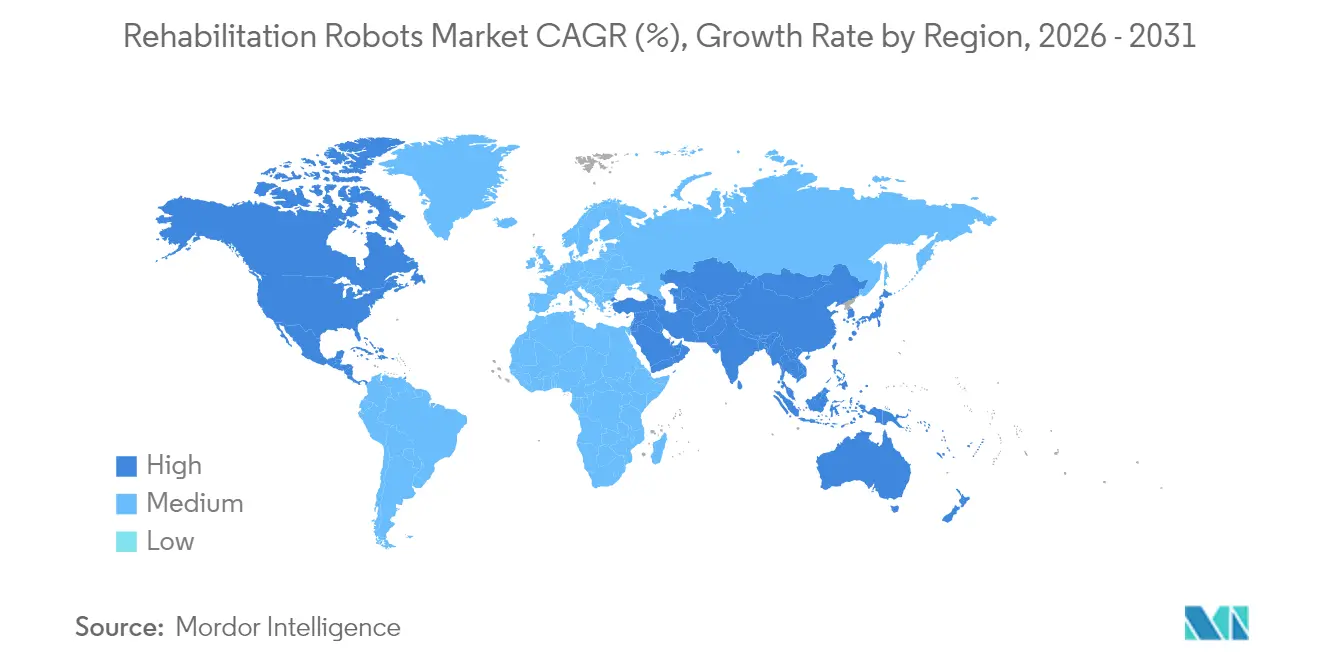

- By geography, North America captured 39.60% revenue in 2025; Asia-Pacific is the fastest-growing region at 21.2% CAGR on rising stroke incidence and aging populations.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rehabilitation Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid post-stroke adoption of upper-limb exoskeletons | +3.20% | Asia-Pacific core; spillover to Japan | Medium term (2-4 years) |

| National neuro-rehabilitation funding programs | +2.80% | Europe, Nordic expansion | Long term (≥ 4 years) |

| Shift toward home-based telerehabilitation robots | +4.10% | North America; early Canada uptake | Short term (≤ 2 years) |

| Lightweight actuator technology (< 10 kg devices) | +2.50% | Global; led by Japan and Germany | Medium term (2-4 years) |

| Insurance reimbursement codes in Japan and Australia | +1.90% | Asia-Pacific; possible OECD roll-out | Medium term (2-4 years) |

| North-American Veterans-Affairs gait programs | +1.80% | US and Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Post-Stroke Adoption of Upper-Limb Exoskeletons in China and South Korea

Government modernisation plans and an aging demographic accelerate procurement of upper-limb robots. Fourier Intelligence’s GR-2 humanoid, equipped with 53 degrees of freedom, highlights Chinese engineering depth. South-Korean researchers’ “Iron Man” robot brings paraplegic gait support, underscoring regional innovation. Clinical data show weekly Fugl-Meyer gains of 1.979 points with robotic therapy versus 1.198 points by conventional means. [1]Valerio Gower, “Cost Analysis of Technological Rehabilitation,” frontiersin.org Closed-loop systems coupling robotics, sensing, and neuronal microfluidics further personalise post-stroke programs.

National Neuro-Rehabilitation Funding Programs in Germany, France and Italy

Germany’s BARMER pact covering 8.5 million lives illustrates Europe’s strategic turn to robotics for cost-efficient therapy. Italian real-world evidence confirms mixed robot-human protocols lower costs without sacrificing outcomes. EU agencies further advocate automation to mitigate caregiver strain and staffing gaps. Coordinated multicentre trials such as STROKEFIT4 aim to standardise evidence-based deployment.

Shift Toward Home-Based Telerehabilitation Robots Under US Medicare Pilot

The Acute Hospital Care at Home program authorised 328 hospitals, reporting 23,000+ discharges by April 2024. Home rehab yields AM-PAC mobility scores 8.2 points above skilled-nursing facilities and trims Medicare spends by USD 17,123 per episode. AI-led virtual therapy shows ≥80% symptom relief. Pilot stroke studies registered 7-point Fugl-Meyer gains during lockdowns, confirming safety and efficacy of domestic robots.

Lightweight Actuator Technology Reducing Device Mass Below 10 kg

Ultra-light manipulators such as SAQIEL (1.5 kg) employ passive wire alignment for precise load handling. [2]Temma Suzuki et al., “SAQIEL Manipulator,” arxiv.org Shape-memory alloy muscles achieve 60% strain and 3.5 Nm assistive torque for energy-efficient wearables. Dielectric-elastomer hands deliver 27 DOF performance under USD 1,000. HASEL-based soft arms from Max Planck suppress tremor, signalling a major shift to comfortable, discreet designs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front Capex and maintenance for multi-DOF platforms | -2.90% | Global; acute in emerging markets | Long term (≥ 4 years) |

| Limited long-term clinical outcome evidence | -2.10% | Global; US and EU focus | Medium term (2-4 years) |

| Safety and liability concerns in pediatrics | -1.40% | Europe; regulatory-sensitive markets | Medium term (2-4 years) |

| Shortage of skilled robot-physiotherapists | -1.80% | LATAM and South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capex and Maintenance for Multi-DOF Platforms

Personal exoskeletons list between USD 75,000 and USD 100,000, while full-scale clinic units cost more, straining budgets. [3]Linda Hersey, “Exoskeleton Walking Suits for Veterans,” stripes.com Beyond purchase, institutions face maintenance, consumables, and specialised training costs that inflate ownership. Investor sentiment remains positive, yet startups confront long R&D cycles and adoption uncertainty. A Veterans Affairs trial showed device use averaging only 86 minutes per week among 161 participants, highlighting utilisation risk. Italian cost analyses underline the need for optimised therapist-to-patient ratios to justify robotic spend.

Limited Long-Term Clinical Outcome Evidence vs. Conventional Therapy

Meta-analysis in spinal cord injury finds no significant walking speed or distance gains over traditional therapy, though balance scores improve. Four-month VA data show similar mental and physical health outcomes between exoskeleton users and wheelchair control groups. Forty percent of therapists report no familiarity with robotic options and cite evidence gaps as a primary barrier. Validation of AI algorithms in live clinics remains essential for broader insurer confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Exoskeletons Maintain Leadership as Soft Robots Surge

Exoskeleton robots generated 47.35% of 2025 revenue, underscoring their entrenched position in hospital-based therapy. Wearable soft robots, aided by pneumatic and shape-memory innovation, are projected to post 29.6% CAGR to 2031, signalling swift consumer-grade penetration. Therapeutic robots target repetitive upper-limb tasks, while assistive robots widen daily-living support. Hybrid care pathways increasingly combine rigid exoskeletons for acute phases with soft devices for home follow-up. Wandercraft’s AI-enabled Atalante X and Eve exemplify exoskeleton evolution toward hands-free mobility. Simultaneously, pneumatically actuated hand exoskeletons enhance comfort in neuromotor therapies. This dual-track development keeps the rehabilitation robots market dynamic and user-centred.

Second-generation systems integrate adaptive algorithms that tailor assistance to muscle-activation data, reinforcing motor-learning principles. Modular designs such as OpenExo let clinics mix-and-match components, reducing inventory costs while broadening use cases. Collectively, these trends sustain the rehabilitation robots market through differentiated performance tiers that address severe impairment, moderate dysfunction, and daily life augmentation.

By Therapy Area: Upper-Limb Dominance Meets Full-Body Innovation

Upper-limb applications control around 54.60% of sector turnover, mirroring stroke prevalence where 80% of patients suffer arm deficits. AGREE trials show comparable clinical improvement to standard care despite reduced treatment time, boosting efficiency. Lower-limb devices such as the ANGEL LEGS M20 deliver similar gait gains while adding muscle-strength benefits. Full-body systems that tie brain-computer interfaces to gait platforms emerge as holistic solutions, uplifting neuroplasticity across multiple joints.

Increasingly, clinicians advocate blended regimens: early full-body gait training to avert compensatory habits, followed by fine-motor upper-limb work in subacute stages. These intertwined protocols underpin the rehabilitation robots market and ensure technology investment aligns with patient-centric outcomes.

By Patient Group: Geriatric Demand Outpaces Adult and Pediatric Uptake

The geriatric cohort captures 61.40% of the rehabilitation robots market size in 2025 thanks to rising stroke, osteoarthritis, and frailty episodes. Japanese nursing-home studies show robotic lifts and monitors lower staff turnover and reduce restraint usage. Adults remain the largest absolute user base but grow slower as penetration approaches maturity in developed economies. Pediatric adoption lags amid liability concerns; however, smaller-scale prototypes tailored for cerebral palsy illustrate future promise. Geriatric focus will therefore dominate revenue yet also shape device ergonomics, usability, and remote-monitoring features for home care.

Regulators are progressively refining paediatric safety norms, and grant-funded trials in Europe aim to clarify benefit-risk profiles. Over time, verified child-safe designs could unlock a sizable untapped slice of the rehabilitation robots market.

By Mobility Level: Stationary Platforms Dominate While Mobile Systems Accelerate

Stationary rigs secured 65.30% of 2025 revenue through high-intensity therapy delivered in controlled clinics. Integration with VR-based gamification platforms such as Max Well-Being lifts engagement and mitigates therapy fatigue. Mobile over-ground systems now expand at 27.3% CAGR, as self-balancing exoskeletons like Atalante X allow hands-free locomotion in corridors and community spaces. Machine-learning navigation guards user safety across uneven terrain, supporting transition from clinic to everyday life.

Emerging modular kits can shift between stationary and mobile modes, letting therapists adjust complexity as patients progress. Such flexibility strengthens adherence and broadens the rehabilitation robots market appeal.

By Body Region: Upper-Extremity Innovation Sets the Pace

Upper-extremity devices dominate due to intricate motor-control needs and daily-living relevance. Dielectric-elastomer hands offering 27 DOF at sub-USD 1,000 price points signal impending democratisation. Lower-extremity products emphasise gait speed and balance, especially in Parkinson’s therapy where 80 N assistive thresholds raise velocity by 58%. Cross-body solutions, integrating EEG-driven intent detection, standardise movement patterns with 84.19% BCI accuracy for stroke rehabilitation.

Continued sensor miniaturisation and AI-powered control loops will sustain superior functional gains, ensuring that the rehabilitation robots market remains at the forefront of human-machine synergy.

By End User: Rehabilitation Centres Lead; Homecare is Most Dynamic

Rehabilitation centres own 53.20% of 2025 turnover owing to concentrated expertise and capital budgets. Hospitals and sports-medicine clinics follow as secondary settings for post-surgical and athlete recovery. Homecare records the highest 27.1% CAGR, catalysed by Medicare reimbursement and maturing telehealth infrastructure. Remote patient-monitoring dashboards let clinicians supervise real-time metrics without in-person visits, slashing transport burdens for mobility-impaired users.

Manufacturers respond with rental and subscription models that bundle maintenance and software updates, enhancing affordability and smoothing cash-flow for households. This economic alignment positions homecare as the long-run growth engine of the rehabilitation robots market.

By Application: Neurological Disorders Command, Orthopaedics Expand

Neurological cases, led by stroke, spinal cord injury, and Parkinson’s disease, underpin the bulk of demand. Hybrid Assistive Limb (HAL) therapy combined with nusinersen shows tangible motor gains in spinal muscular atrophy. Orthopaedic recovery widens as surgical-robot vendors like Stryker extend SmartRobotics to hip revisions and shoulder replacements. Sports-injury rehabilitation exploits motion-capture analytics to speed athlete return-to-play timelines.

AI platforms pairing ChatGPT-4 with wearables for sarcopenia exercise therapy showcase personalised protocols that transcend clinical silos. As such, cross-indication versatility cements the rehabilitation robots market as a core pillar of 2030 healthcare delivery.

Geography Analysis

North America represented 39.60% of 2025 revenue, buoyed by Medicare policy shifts and Veterans Affairs programmes that distribute exoskeletons to spinal-cord-injured veterans. Legislative initiatives such as the STAND Act aim to standardise access criteria, yet VA trials reveal average weekly use below 90 minutes, underscoring utilisation hurdles. Home-based pilots and CMS reimbursement continue to channel growth toward community settings.

Asia-Pacific is the fastest-growing territory with a 21.2% CAGR, led by China, South Korea, and Japan. Fourier’s GR-2 humanoid and Korea’s paraplegic gait robot exemplify regional innovation, while Japan’s nursing-home deployments validate labour-saving benefits. Skill-shortage constraints in India and Brazil could moderate adoption, but rental schemes and international aid projects seek to bridge gaps.

Europe harnesses robust public funding; Germany’s 8.5 million-life reimbursement agreement signifies institutional confidence. Multicentre trials across France and Italy work to validate scalable protocols, while EU agencies emphasise occupational safety and training to mitigate deployment risks. Pediatric liability concerns, particularly under CE-mark regulations, temper near-term uptake but are unlikely to derail the long-range outlook of the rehabilitation robots market.

Competitive Landscape

The field remains moderately fragmented. Market stalwarts such as Cyberdyne, Ekso Bionics, and Lifeward leverage FDA and CE clearances to secure tenders, yet must counter newcomers armed with AI differentiation and venture backing. ReWalk’s USD 19 million AlterG acquisition broadens its product footprint to anti-gravity gait devices, evidencing portfolio expansion momentum. Bioness’ purchase of Harmonic Bionics assets augments upper-limb depth.

Wandercraft’s USD 75 million financing elevates competition in mobile self-balancing exoskeletons and signals investor belief in AI-driven robotics. Surgical-robot majors such as Stryker crossover into postoperative rehab devices, tightening market borders. White-space remains in paediatric indications and emerging economies where skill shortages limit penetration.

Patent filings in soft actuators, dielectric elastomer sensors, and adaptive control ribbons reveal intense R&D rivalry. Companies able to demonstrate cost-effectiveness, clinician usability, and regulatory compliance will consolidate leadership as the rehabilitation robots market matures toward 2030.

Rehabilitation Robots Industry Leaders

-

Bionik Laboratories Corporation

-

Cyberdyne Inc.

-

Ekso Bionics Holdings Inc.

-

ReWalk Robotics Ltd.

-

Hocoma AG (DIH International Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Wandercraft secured USD 75 million Series D funding to fast-track AI exoskeletons and humanoid Calvin 40.

- May 2025: Wandercraft began clinical trials of an AI-powered personal exoskeleton targeting FDA home-use clearance.

- March 2025: Stryker unveiled fourth-generation Mako 4 SmartRobotics with hip-revision capability at AAOS 2025.

- February 2025: Lifeward finalised a reimbursement pact with Germany’s BARMER covering 8.5 million lives.

Global Rehabilitation Robots Market Report Scope

Rehabilitation robot is an automatically operated machine designed to improve movement in persons with impaired physical functioning. These robots can support and enhance clinicians’ productivity and effectiveness as they try to facilitate an individual’s recovery. There are mainly two types of rehabilitation robots. The first one is an assistive robot that substitutes for lost limb movements. The second type is called as therapy robot, that allows patients to perform practice movements aided by robot.

| Exoskeleton Robots |

| Therapeutic Robots |

| Assistive Robots |

| Wearable Soft Robots |

| Upper Limb Rehabilitation |

| Lower Limb Rehabilitation |

| Full-Body / Gait Training |

| Geriatric |

| Adult |

| Pediatric |

| Stationary Platform |

| Mobile / Over-ground |

| Rehabilitation Centers |

| Hospitals and Clinics |

| Homecare Settings |

| Specialty Orthopedic and Sports-Medicine Centers |

| Upper Extremity |

| Lower Extremity |

| Neurological Disorders (Stroke, SCI, CP, Parkinson) |

| Orthopedic Injuries and Post-Surgery |

| Sports Injury Rehabilitation |

| Powered (Motorized / Actuated) |

| Passive / Mechanically Assisted |

| AI-Driven Adaptive Control |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Exoskeleton Robots | |

| Therapeutic Robots | ||

| Assistive Robots | ||

| Wearable Soft Robots | ||

| By Therapy Area | Upper Limb Rehabilitation | |

| Lower Limb Rehabilitation | ||

| Full-Body / Gait Training | ||

| By Patient Group | Geriatric | |

| Adult | ||

| Pediatric | ||

| By Mobility Level | Stationary Platform | |

| Mobile / Over-ground | ||

| By End User | Rehabilitation Centers | |

| Hospitals and Clinics | ||

| Homecare Settings | ||

| Specialty Orthopedic and Sports-Medicine Centers | ||

| By Body Region | Upper Extremity | |

| Lower Extremity | ||

| By Application | Neurological Disorders (Stroke, SCI, CP, Parkinson) | |

| Orthopedic Injuries and Post-Surgery | ||

| Sports Injury Rehabilitation | ||

| By Technology | Powered (Motorized / Actuated) | |

| Passive / Mechanically Assisted | ||

| AI-Driven Adaptive Control | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the rehabilitation robots market?

The rehabilitation robots market size stands at USD 1.77 billion in 2026 and is projected to reach USD 3.89 billion by 2031.

Which product type dominates the rehabilitation robots market?

Exoskeleton robots lead with 47.35% revenue share in 2025, supported by robust clinical validation and hospital uptake.

Why is homecare the fastest-growing end-user segment?

Medicare reimbursement, compact lightweight designs, and remote-monitoring software are pushing a 27.1% CAGR for home-based rehabilitation robots.

Which region shows the highest growth potential?

Asia-Pacific posts the fastest growth at a 21.2% CAGR, fuelled by Chinese and South-Korean innovation and supportive healthcare reforms.

What are the main barriers to wider adoption?

High capital costs, limited long-term efficacy data, paediatric safety concerns, and shortages of trained robot-physiotherapists in emerging markets slow broader diffusion.

How are companies differentiating in this market?

Vendors focus on AI-driven adaptive control, lightweight soft-actuator platforms, reimbursement-friendly pricing models, and strategic acquisitions to build comprehensive rehabilitation portfolios.

Page last updated on: