Vocal Biomarkers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.84 Billion |

| Market Size (2031) | USD 7.77 Billion |

| Growth Rate (2026 - 2031) | 15.15% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vocal Biomarkers Market Analysis by Mordor Intelligence

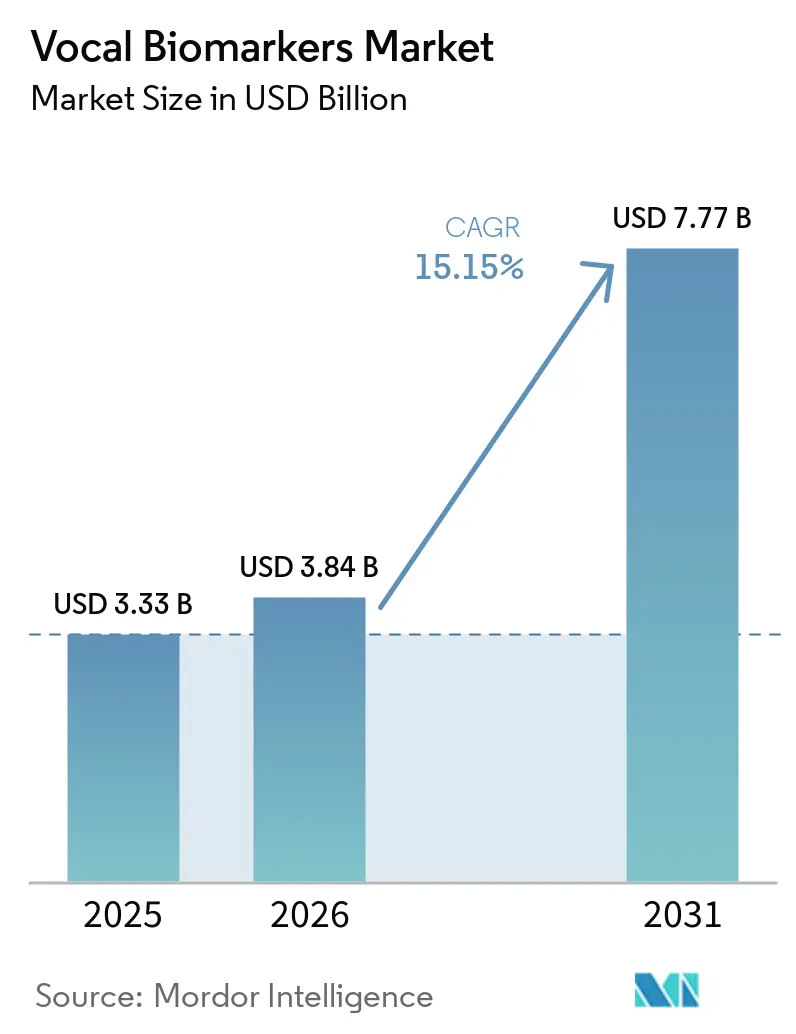

The Vocal Biomarkers Market size is projected to be USD 3.33 billion in 2025, USD 3.84 billion in 2026, and reach USD 7.77 billion by 2031, growing at a CAGR of 15.15% from 2026 to 2031.

The vocal biomarkers market is expanding due to widespread smartphone adoption, advancements in AI-driven acoustic analysis, and growing research linking voice to neurological, psychiatric, respiratory, and cardiovascular conditions. Validation is transitioning from controlled studies to outpatient and home settings, reducing execution risks for healthcare providers and commercial partners. Additionally, the market benefits from low deployment barriers, as voice capture does not rely on invasive methods or specialized hardware. This accessibility and clinical utility are driving competition, partnerships, and new opportunities in the market.

Key Report Takeaways

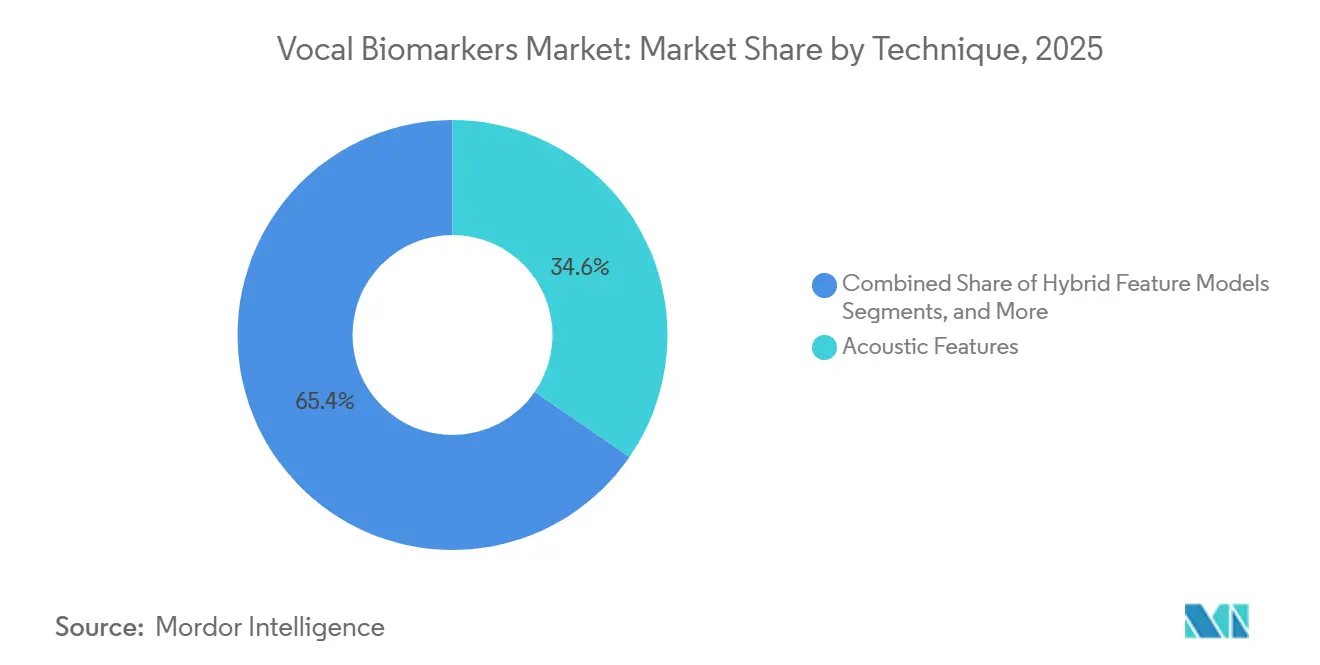

- By technique, acoustic feature extraction led with 34.58% share in 2025, while hybrid feature models are projected to expand at a 16.52% CAGR through 2031.

- By platform type, cloud-based platforms held 67.88% of the segment in 2025, while cloud-based platforms also recorded the highest projected CAGR at 17.30% through 2031.

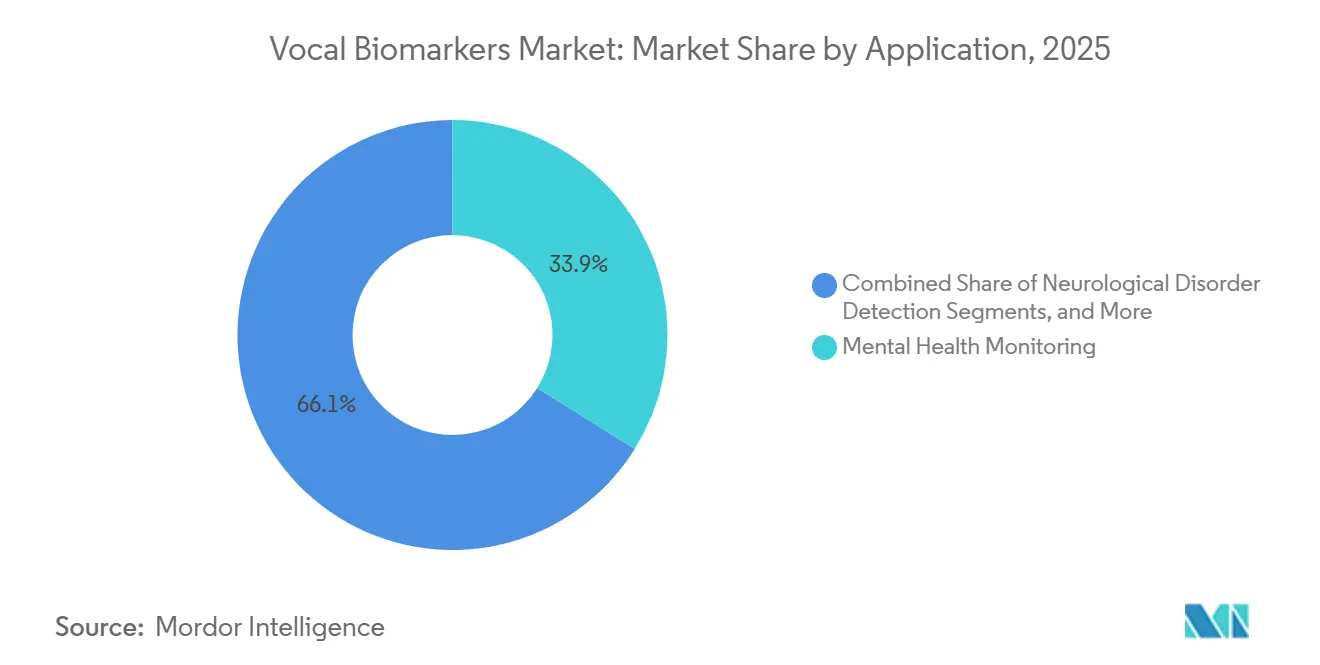

- By application, mental health monitoring accounted for 33.91% of the segment in 2025, while neurological disorder detection is projected at a 15.67% CAGR through 2031.

- By end user, hospitals and clinics held 47.03% of the segment in 2025, while pharmaceutical and biotechnology companies are projected to grow at a 15.95% CAGR through 2031.

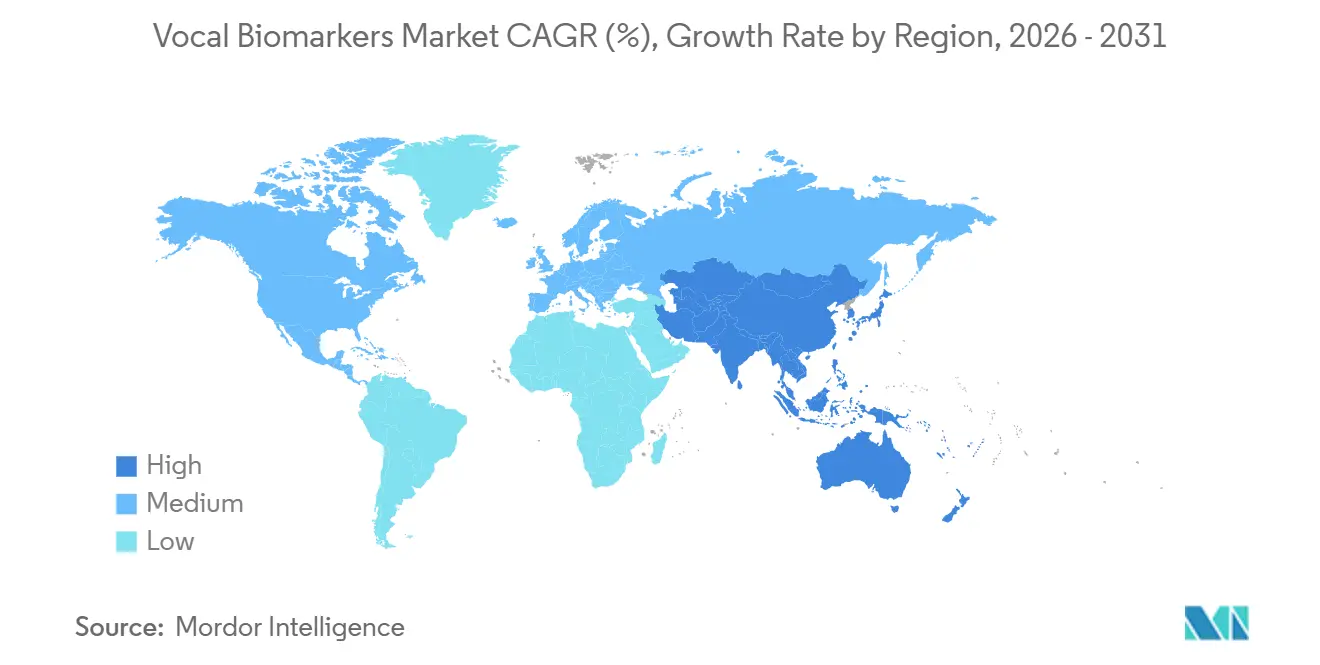

- By geography, North America led with 38.99% of global revenue in 2025, while Asia-Pacific is projected to expand at a 16.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vocal Biomarkers Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising use of voice as a non-invasive digital health tool | +2.8% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| AI and machine learning improve signal extraction accuracy | +3.5% | Global, with high concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| Remote patient monitoring expands clinical utility | +2.3% | Global, with strong early gains in North America and East Asia | Medium term (2-4 years) |

| Broader utility across mental health, neurology, and cardiology | +2.6% | Global, with Western Europe and North America leading clinical adoption | Medium term (2-4 years) |

| Integration into telehealth, call centers, and wellness apps | +1.6% | North America, Europe, and East Asia | Short term (≤ 2 years) |

| Growing research validation and clinical trials | +1.4% | Global, with early gains in North America and European research hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Use of Voice as a Non-Invasive Digital Health Tool

The vocal biomarkers market is thriving, driven by the ability to collect voice data using standard smartphones. This innovation eliminates the need for invasive methods like blood sampling, imaging systems, and wearable sensors. Such ease of deployment is particularly beneficial in rural and underserved areas, where access to healthcare is limited. Research highlighted Sonde Health's vocal biomarker tool, which can assess asthma exacerbation risk using just 6-second vowel recordings. Notably, higher normalized scores indicated a 3.57-fold increased risk of exacerbation in cohorts from both the U.S. and India, spanning five Indian languages. This commercial evidence underscores the vocal biomarkers market's potential to expand into multilingual regions without the need to reconstruct models for each language. Furthermore, there's a noticeable demand in depression screening. The Annals of Family Medicine noted a stark contrast: while routine screening is recommended, only 4% of primary care patients were screened as of 2025. This gap highlights the potential of short-form voice tools in early triage processes.[1]Emily Larsen, Xiang Song, David Joachim, “Respiratory-Responsive Vocal Biomarker for Asthma Exacerbation Monitoring,” Journal of Medical Internet Research, jmir.org

AI and Machine Learning Improve Signal Extraction Accuracy

The vocal biomarkers market is advancing as model designs evolve, shifting from narrowly defined features to broader representations trained on diverse clinical datasets. In May 2026, the Bridge2AI Consortium unveiled VoiceFM, a dual-encoder model trained on their Voice dataset. This model demonstrated impressive capabilities, including cross-site generalization, Parkinson's detection across English, Spanish, and Mandarin, and multi-condition classification. Another study in 2025 highlighted a hybrid CNN-MLP-RNN model achieving 91.11% accuracy and an AUC of 0.9125 for early Parkinson's detection, utilizing MFCC features with explainability.[2]Martin Neumann, Harsh Kothare, Matthew Bartlett, “Speech-Based Digital Endpoints Track ALS Progression and Align With Standard Clinical Outcomes,” Scientific Reports, nature.com Such advancements are pivotal for the vocal biomarkers market as clinicians and regulators favor systems that perform well and provide understandable reasoning at the feature level. Vendors with explainable and versatile models are poised for heightened acceptance in hospitals, regulatory circles, and pharmaceutical endpoints.

Remote Patient Monitoring Expands Clinical Utility

Remote monitoring is paving the way for the vocal biomarkers market. Voice data can now be captured conveniently at home, at varying intervals, and without the need for trained personnel. A 2026 ALS trial found that speech-based digital endpoints correlated well with the ALSFRS-R scale and detected functional declines earlier than traditional benchmarks. Moreover, speech timing measures distinguished between bulbar-affected and non-bulbar participants over 8-week intervals. The AHF-Voice study on heart failure further validated the approach, demonstrating the efficacy of smartphone-based recordings in both hospital and home settings. This underscores the potential of voice as a decentralized endpoint in cardiovascular trials. For sponsors and care teams, this continuity is invaluable. The ability to use the same measurement approach repeatedly, without necessitating additional clinic visits or specialized equipment, broadens the utility of vocal biomarkers. This evolution is steering the market from a primary focus on screening to encompassing comprehensive disease monitoring and follow-up applications.

Broader Utility Across Mental Health, Neurology, and Cardiology

The vocal biomarkers market is evolving beyond just depression screening. The evidence now spans mental health, neurology, and cardiology, showcasing a richer clinical landscape. A 2026 review highlighted the potential of neural network models in screening heart failure via voice and connected vocal biomarkers to hospitalization and mortality risks, referencing established cohort studies. In neurology, a 2025 study demonstrated that AI models trained on unstructured conversational voice data could predict mild cognitive impairment, independent of the speech content, in a study conducted in Japan. Further emphasizing the global relevance, a 2026 cross-cultural study found that acoustic models tailored for the Japanese population achieved an impressive AUC of 0.992 in depression classification.[3]Emily Kiyoshige, Shota Ogata, Nayeon Kwon, “Developing and Testing AI-Based Voice Biomarker Models to Detect Cognitive Impairment Among Community Dwelling Adults,” The Lancet Regional Health Western Pacific, lancet.com

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited clinical standardization across languages and demographics | -1.2% | Global, most acute in multilingual markets such as India, Southeast Asia, and Africa | Long term (≥ 4 years) |

| Regulatory uncertainty for diagnostic and monitoring use cases | -0.9% | North America and Europe, with spillover through export and compliance dynamics | Medium term (2-4 years) |

| Need for larger longitudinal datasets and benchmarks | -0.7% | Global, most severe in low-resource settings | Long term (≥ 4 years) |

| Data privacy, consent, and governance concerns | -0.8% | Europe, North America, and increasingly Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Clinical Standardization Across Languages and Demographics

Standardization remains a critical challenge for the vocal biomarkers market due to variations in language, recording conditions, and sample design, which affect model reliability. A 2025 review highlighted that compressed audio formats like MP3, M4A, and WMA distort jitter and shimmer, based on an analysis of 17,298 uncompressed voice samples. Another review noted that 94% of 67 machine learning studies on major depressive disorder used fewer than 100 participants, with only 13% addressing varying symptom severity. These gaps hinder the reliable application of published accuracy claims in routine care or global deployment, limiting validation and scalability until larger, harmonized datasets become standard.

Regulatory Uncertainty for Diagnostic and Monitoring Use Cases

The vocal biomarkers market faces regulatory challenges as diagnostic and monitoring claims subject software products to stricter compliance pathways. In the U.S., Software as a Medical Device review increases evidence requirements for formal approval. In Europe, GDPR and medical device regulations add complexity to consent design, data management, and clinical evidence, delaying market entry and cross-border data use. Companies often prioritize research applications, decision support systems, or wellness initiatives before pursuing diagnostic roles, resulting in commercial progress outpacing regulatory alignment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technique: Acoustic Features Anchor Current Use While Hybrid Models Gain Ground

In 2025, acoustic feature extraction held a 34.58% share of the vocal biomarkers market by technique, making it the largest segment. This dominance is due to its established use in clinical settings, leveraging parameters like jitter, shimmer, MFCCs, and fundamental frequency. These features remain the foundation for hospitals, research groups, and trial managers, given their integration into earlier algorithms and product development. Prosodic features are significant for affective disorders and Parkinson’s-related speech changes, while spectral features are vital for respiratory and cardiovascular assessments.

Hybrid feature models are expected to grow at a 16.52% CAGR through 2031, making them the fastest-growing technique. This growth reflects the need for models that generalize across diseases, languages, and age groups. The industry is likely to retain acoustic features as the operational base while hybrid systems gain commercial traction, despite their more complex validation requirements.

By Platform Type: Cloud-Based Delivery Leads While Embedded Integration Expands Reach

Cloud-based platforms accounted for 67.88% of the vocal biomarkers market in 2025, maintaining their leadership position. Their dominance is driven by the ability to run large models without hardware constraints, update models post-deployment, and integrate with EHR systems via APIs. This architecture aligns with existing data management practices in healthcare and supports centralized model governance.

Cloud-based platforms are projected to grow at a 17.30% CAGR through 2031, remaining the fastest-growing platform type. Embedded SDK and API solutions are also gaining traction, enabling seamless integration into telehealth platforms, call centers, and documentation tools. This dual approach positions cloud platforms as dominant while embedded solutions expand market reach.

By Application: Mental Health Holds the Largest Base While Neurology Builds Momentum

Mental health monitoring held a 33.91% share of the vocal biomarkers market in 2025, making it the largest application segment. This growth is driven by demand for scalable tools to detect depression and anxiety in primary care and behavioral health settings. Respiratory monitoring is also gaining importance, supported by studies demonstrating clinical relevance and positive patient experiences.

Neurological disorder detection is projected to grow at a 15.67% CAGR through 2031, making it the fastest-growing application. This growth is fueled by aging populations, early detection needs, and evidence linking voice analysis to conditions like Parkinson’s, cognitive impairment, and ALS. Neurology is emerging as a key growth area in the vocal biomarkers market.

By End User: Hospitals and Clinics Hold the Largest Share While Pharma and Biotech Accelerate

Hospitals and clinics held a 47.03% share of the vocal biomarkers market in 2025, making them the largest end-user segment. Their leadership is attributed to access to patient histories, EHR-linked workflows, and established physician-led screening protocols. Academic and research institutions remain critical for providing datasets and validation.

Pharmaceutical and biotechnology companies are projected to grow at a 15.95% CAGR through 2031, making them the fastest-growing end-user group. These companies are leveraging voice endpoints to reduce patient burden in CNS, respiratory, and neuromuscular studies while supporting decentralized trial models. This trend is driving market expansion through both care delivery and trial design channels.

Geography Analysis

In 2025, North America accounted for 38.99% of the global vocal biomarkers market revenue, maintaining its position as the largest regional block. The region benefits from a strong digital health infrastructure, active clinical research networks, and significant pharmaceutical involvement in software-driven endpoint development. The U.S. leads due to clearer regulatory pathways for medical software, despite challenges with uneven reimbursement. Canada contributes through academic and clinical research partnerships, while Mexico, though in early adoption stages, shows potential with telehealth expansion driving wellness and screening-focused voice solutions.

Europe held the second-largest market share in 2025, driven by advancements in hospital digitization and clinical research in Germany, the U.K., and France. The region also influences standards and governance, with initiatives like eVoiceNet promoting unified principles for vocal biomarker development. GDPR regulations, treating voice data as personal information, impose stricter requirements on consent, data usage, and storage, which, while slowing cross-border data exchange, encourage stronger privacy and validation practices.

Asia-Pacific is projected to grow at a 16.64% CAGR through 2031, making it the fastest-growing region. Japan leads with its aging population, high smartphone penetration, and AI-driven elder care initiatives aligning with voice-based monitoring. Studies highlight the value of region-specific models, with Japanese acoustic models achieving an AUC of 0.992 in depression classification. India supports cost-effective multilingual voice data collection, while China progresses with local language standardization, though broader commercialization depends on maturing clinical frameworks. The Middle East, Africa, and South America remain smaller markets, but Brazil is emerging as a hub for Portuguese-language research.

Competitive Landscape

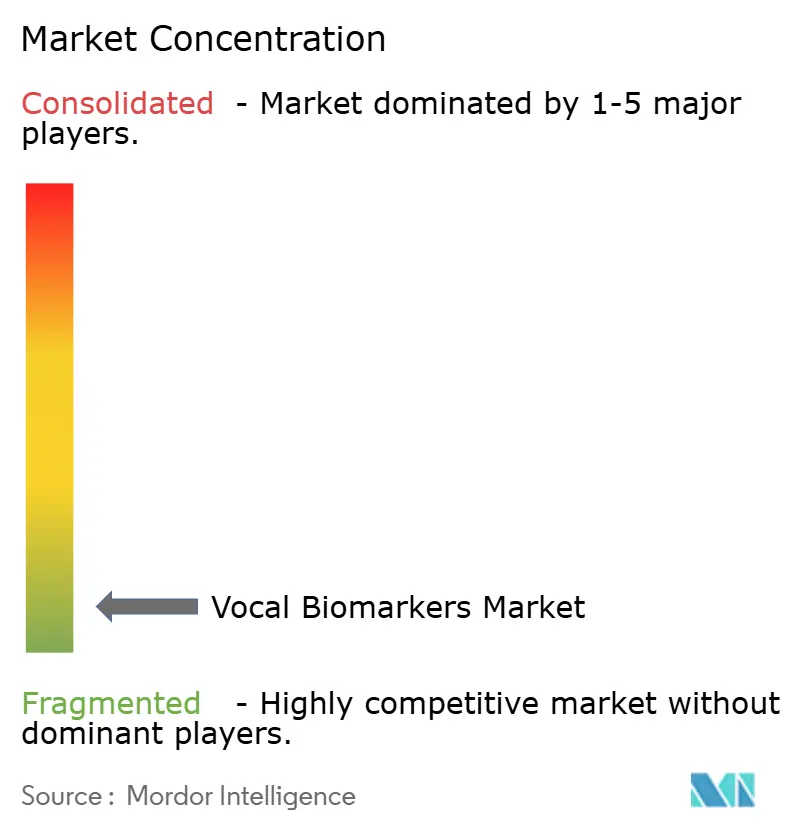

Over 20 entities are actively navigating the fragmented vocal biomarkers market, engaging in areas like clinical screening, monitoring, and wellness tools. No single player has yet claimed dominance across all primary use cases, allowing diverse business models to flourish. While some vendors are crafting platforms for formal medical adoption, others are swiftly tapping into wellness, telehealth, and enterprise integrations. This landscape underscores the importance of evidence quality, regulatory strategies, and distribution partnerships, alongside model performance. The market is vibrant and competitive, yet unmistakably in a pre-consolidation phase.

Partnerships are becoming critical for scaling in the vocal biomarkers market. The March 2026 collaboration between GlobalMed and Canary Speech demonstrated how a voice biomarker platform can integrate into federal healthcare workflows through an authorized reseller model instead of direct consumer channels. PST Inc. adopted a different approach by using its VOISLOG platform and partnering with the insurance sector to expand voice monitoring beyond traditional settings. These strategies highlight that market access increasingly depends on channel alignment rather than solely on algorithm quality.

Data strategy and validation are emerging as key differentiators in the vocal biomarkers market. Companies capable of collecting diverse datasets, supporting multilingual deployment, and meeting medical software standards are better positioned for premium contracts. Canary Speech's June 2024 funding round, which raised USD 13 million with support from health systems and Japanese investors, emphasized the importance of building institutional anchors across multiple geographies. Opportunities remain in cardiovascular applications, pediatric neurological assessments, and sponsor-facing endpoint services for CNS and respiratory trials, leaving room for specialists to gain market share by aligning efficacy with deployment economics.

Vocal Biomarkers Industry Leaders

Cogito Corporation

Sonde Health, Inc.

Canary Speech, Inc.

Kintsugi Mindful Wellness, Inc.

Ellipsis Health, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The Bridge2AI Consortium introduced VoiceFM, a CLIP-style contrastive foundation model designed for clinical voice biomarkers. Trained on the Bridge2AI-Voice dataset, VoiceFM demonstrated capabilities in cross-site generalization, detecting Parkinson's disease across English, Spanish, and Mandarin, and classifying multiple conditions.

- April 2026: Speechmatics and thymia launched a clinical-grade platform capable of identifying over 30 health signals, including stress, depression, type 2 diabetes indicators, and driver impairment, using just 15 seconds of natural speech. The platform combines medical-grade speech-to-text with thymia's voice biomarker intelligence, built on a dataset of 75,000 unique voices.

- March 2026: GlobalMed, a leader in digital health solutions, partnered with Canary Speech as an authorized reseller to deploy vocal biomarker technology across U.S. federal healthcare systems. The partnership integrates Canary Speech's AI-powered platform into clinical workflows for behavioral and neurological screenings.

Global Vocal Biomarkers Market Report Scope

As per the scope of the report, vocal biomarkers are quantifiable characteristics of the human voice that indicate physical, mental, or cognitive health. Using artificial intelligence, software analyzes both the acoustic sound (pitch, tone, pace) and linguistic content (word choice) of speech to detect conditions like depression, respiratory disorders, and cognitive decline.

The vocal biomarkers market is segmented by technique, platform type, application, and end-user. By technique, the market includes acoustic features, prosodic features, spectral features, linguistic features, and hybrid feature models. By platform type, the market is segmented into cloud-based platforms, web-based platforms, mobile applications, and embedded SDK and API solutions. By application, the market is categorized into mental health monitoring, neurological disorder detection, respiratory condition monitoring, cardiovascular condition monitoring, general wellness and preventive screening, and clinical research and trial monitoring. By end-user, the market is segmented into hospitals and clinics, pharmaceutical and biotechnology companies, contract research organizations, academic and research institutes, and others.

| Acoustic Features |

| Prosodic Features |

| Spectral Features |

| Linguistic Features |

| Hybrid Feature Models |

| Cloud-Based Platforms |

| Web-Based Platforms |

| Mobile Applications |

| Embedded SDK and API Solutions |

| Mental Health Monitoring |

| Neurological Disorder Detection |

| Respiratory Condition Monitoring |

| Cardiovascular Condition Monitoring |

| General Wellness and Preventive Screening |

| Clinical Research and Trial Monitoring |

| Hospitals and Clinics |

| Pharmaceutical and Biotechnology Companies |

| Contract Research Organizations |

| Academic and Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technique | Acoustic Features | |

| Prosodic Features | ||

| Spectral Features | ||

| Linguistic Features | ||

| Hybrid Feature Models | ||

| By Platform Type | Cloud-Based Platforms | |

| Web-Based Platforms | ||

| Mobile Applications | ||

| Embedded SDK and API Solutions | ||

| By Application | Mental Health Monitoring | |

| Neurological Disorder Detection | ||

| Respiratory Condition Monitoring | ||

| Cardiovascular Condition Monitoring | ||

| General Wellness and Preventive Screening | ||

| Clinical Research and Trial Monitoring | ||

| By End User | Hospitals and Clinics | |

| Pharmaceutical and Biotechnology Companies | ||

| Contract Research Organizations | ||

| Academic and Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the vocal biomarkers space in 2026?

The vocal biomarkers market size stands at USD 3.84 billion in 2026 and is projected to reach USD 7.77 billion by 2031, with a 15.15% CAGR over 2026-2031.

Which application area currently leads demand for voice-based diagnostics?

Mental health monitoring held the largest application share at 33.91% in 2025, supported by demand for scalable screening in primary care and behavioral health settings.

Which region is expanding the fastest through 2031?

Asia-Pacific is the fastest-growing region, with a forecast CAGR of 16.64% through 2031, supported by Japan's aging population profile and India's multilingual data collection advantage.

Why are hospitals and clinics still the largest buyers?

Hospitals and clinics held 47.03% of end-user demand in 2025 because they already have patient histories, workflow integration paths, and care settings that support physician-led screening and monitoring.

What platform model is winning most deployments?

Cloud-based platforms led with 67.88% share in 2025 and are also the fastest-growing platform type, helped by scalable model delivery and easier EHR and API integration.

What is the main challenge slowing broader adoption?

Clinical standardization and regulatory uncertainty remain the main hurdles because language variation, recording differences, privacy rules, and medical evidence requirements still affect deployment at scale.

Page last updated on: