Audiological Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.81 Billion |

| Market Size (2031) | USD 19.71 Billion |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Audiological Devices Market Analysis by Mordor Intelligence

The Audiological Devices market size is expected to grow from USD 13.99 billion in 2025 to USD 14.81 billion in 2026 and is forecast to reach USD 19.71 billion by 2031 at 5.86% CAGR over 2026-2031. Rising life expectancy, rapid digitalisation of hearing aids, and favourable regulatory updates such as the United States over-the-counter (OTC) rule are expanding both clinical and retail channels for hearing care.[1]Source: U.S. Food and Drug Administration, “FDA Finalizes Historic Rule Enabling Access to Over-the-Counter Hearing Aids for Millions of Americans,” fda.gov A growing base of older adults is intensifying device demand, while artificial intelligence (AI) integration is lifting premium product performance and pricing power. Broader newborn and elderly screening initiatives foster early diagnosis, which in turn stimulates sales of diagnostic instruments and software. Connectivity features built on Bluetooth LE Audio and Auracast are blurring the line between medical and consumer devices, opening fresh partnership opportunities with electronics brands. However, high out-of-pocket costs and variable insurance cover remain barriers in several regions.

Key Report Takeaways

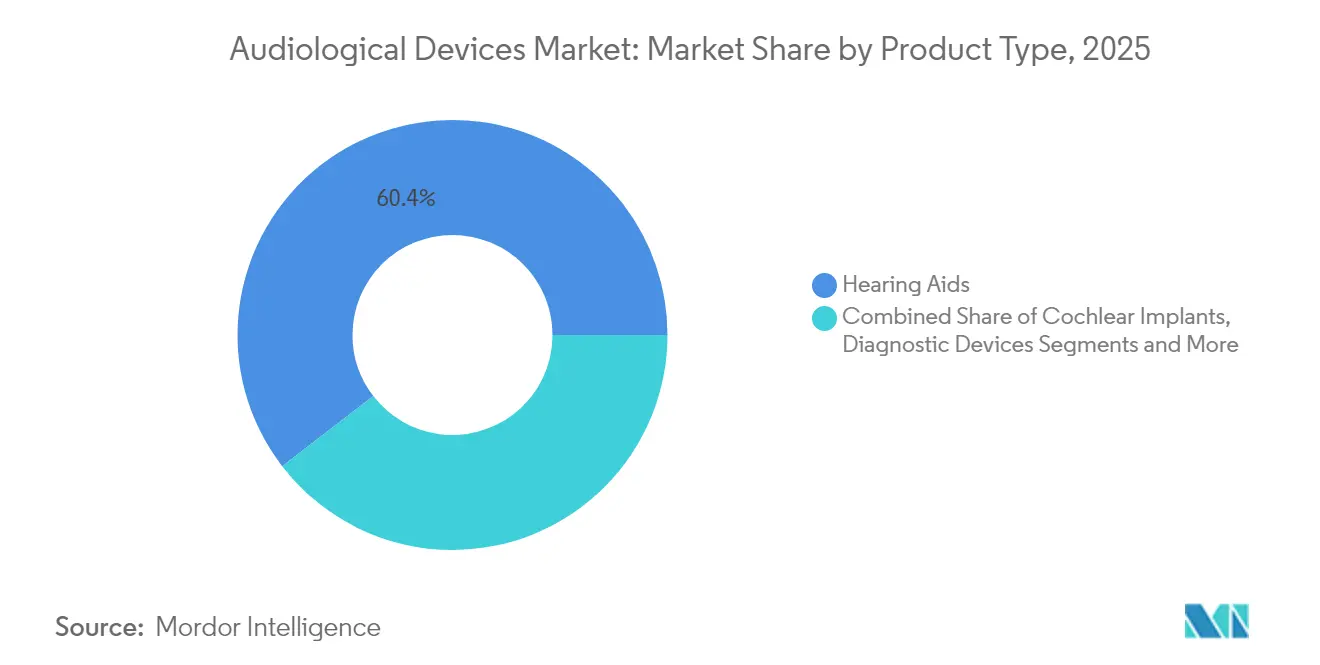

- By product type, hearing aids held 60.44% of audiological devices market share in 2025; diagnostic devices are projected to expand at 6.93% CAGR through 2031.

- By disease type, Meniere’s disease led with 29.21% revenue share in 2025, whereas otosclerosis is forecast to grow at 6.59% CAGR to 2031.

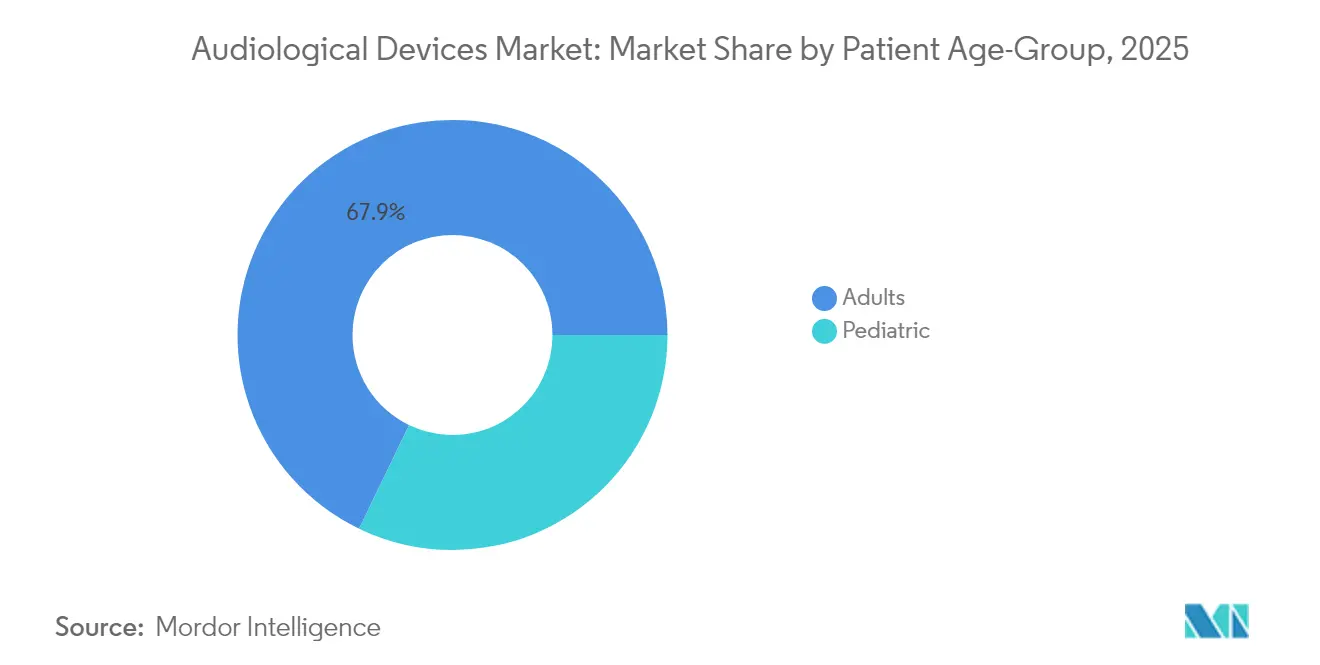

- By patient age group, adults commanded 67.85% of the audiological devices market size in 2025, while paediatrics is advancing at 6.3% CAGR during 2026-2031.

- By end user, hospitals led with 45.30% share of the audiological devices market size in 2025; ear-nose-throat (ENT) clinics are growing fastest at 7.28% CAGR to 2031.

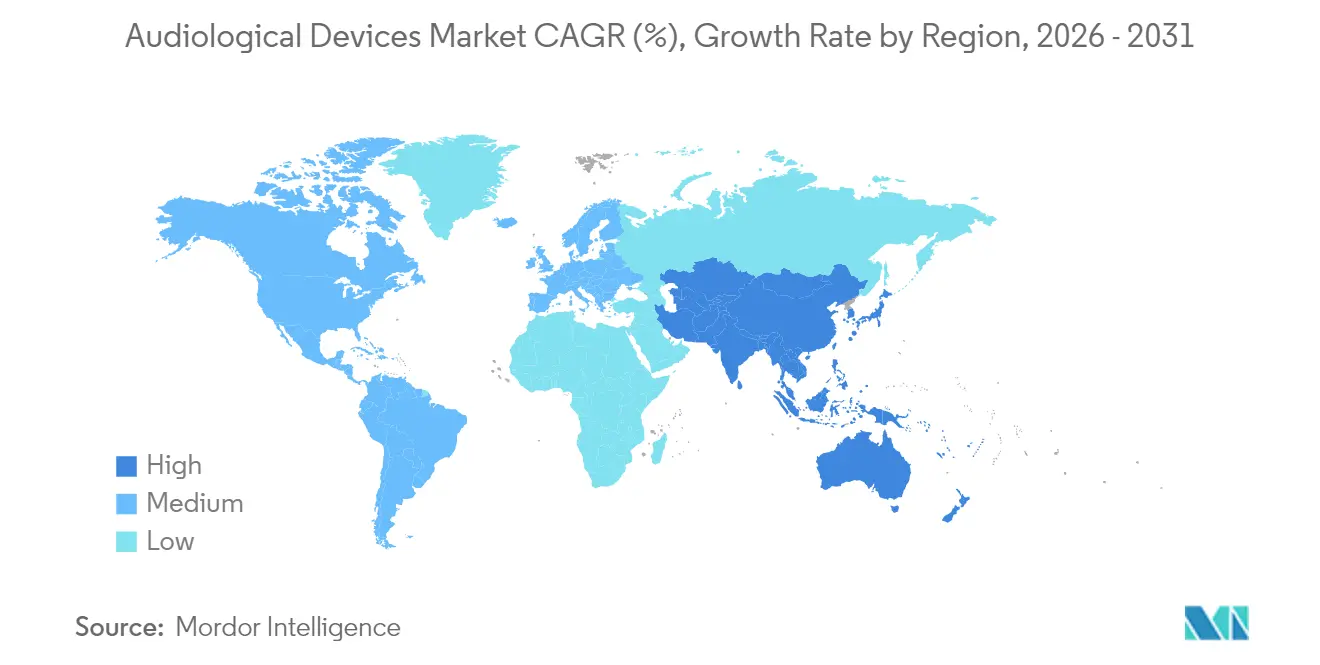

- By geography, North America held 34.12% of audiological devices market share in 2025, while Asia-Pacific shows the highest regional CAGR at 7.71% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Audiological Devices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population and Rising Prevalence of Hearing Loss | +2.1% | Global, with highest impact in North America, Europe, and Japan | Long term (≥ 4 years) |

| Rapid Adoption of Digital and Bluetooth-Enabled Hearing Aids | +1.8% | Global, led by developed markets in North America and Europe | Medium term (2-4 years) |

| Government-Led Newborn and Elderly Hearing-Screening Programs | +0.9% | Global, with early gains in developed countries and expanding to emerging markets | Medium term (2-4 years) |

| High Noise-Exposure Levels in Urban and Industrial Settings | +0.7% | Global, particularly in manufacturing-heavy regions like Asia-Pacific and industrial centers | Long term (≥ 4 years) |

| OTC Hearing-Aid Legislation Unlocking Untapped Consumer Base | +1.2% | North America initially, expanding to Europe and other developed markets | Short term (≤ 2 years) |

| Tele-Audiology Platforms Accelerating Rural Market Penetration | +0.6% | Global, with highest impact in rural areas of developing countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Rising Prevalence of Hearing Loss

Worldwide demographic ageing is lifting baseline demand as bilateral loss affects 37.9 million Americans and 90.7% of adults above 80 years. This demographic shift creates sustained demand pressure, as age-related hearing loss typically begins with high-frequency deficits that progressively impact speech comprehension in noisy environments. Age-related deficits diminish speech comprehension, increase cognitive decline risk, and reduce workforce productivity, prompting public and private stakeholders to invest in early intervention and rehabilitation.

Rapid Adoption of Digital and Bluetooth-Enabled Hearing Aids

Bluetooth LE Audio and Auracast broadcast functions are now baseline in premium lines, enabling direct links to public address systems and smartphones. Brands such as ReSound, Beltone, and Phonak integrate these features to deliver 10 dB signal-to-noise gains and 45% listening-effort reduction. This connectivity revolution extends beyond entertainment to healthcare integration, with devices now capable of real-time health monitoring and telehealth consultations, positioning hearing aids as comprehensive wellness platforms rather than single-purpose medical devices.

Government-Led Newborn and Elderly Screening Programmes

Systematic hearing screening initiatives demonstrate measurable impact on early detection rates and intervention outcomes, particularly in underserved populations where traditional healthcare access remains limited. Tele-enabled screening pilots like the North STAR trial in rural Alaska improved follow-up to 68.5% versus 32.1% for standard referrals, underscoring technology’s role in early detection. Digital ENT assessments show 85% sensitivity compared with 20% for traditional methods, boosting efficiency without compromising safety. The integration of tympanometry with mobile health screening significantly improves detection sensitivity, particularly in environments with high infection-related hearing loss prevalence, establishing new protocols for global hearing health initiatives.[2]Source: Ear and Hearing, “Demographic and Audiological Characteristics of OTC Candidates,” earandhearing.com

High Noise Exposure in Urban and Industrial Settings

Occupational studies report 34.69% loss prevalence among Iranian factory workers, while complex impulse noise requires kurtosis-adjusted measures to predict injury risk. Urban traffic noise raises tinnitus incidence, highlighting a need for both prevention and advanced rehabilitation devices. These multifaceted exposure patterns drive demand for sophisticated hearing protection and rehabilitation technologies, including specialized devices for specific occupational sectors such as dental professionals, who show 15-25% prevalence of hearing thresholds exceeding ISO standards.

Restraints Impact Analysis of Audiological Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Device and Fitting Costs | -1.4% | Global, with highest impact in emerging markets and underinsured populations | Long term (≥ 4 years) |

| Persistent Social Stigma Among Younger Demographics | -0.8% | Global, particularly in image-conscious markets like Asia-Pacific and urban centers | Medium term (2-4 years) |

| Patchy Reimbursement in Many Emerging and Developed Markets | -1.1% | Global, with varying impact by healthcare system structure | Long term (≥ 4 years) |

| Semiconductor Supply-Chain Disruptions Impacting Production | -0.9% | Global, with highest impact on manufacturers with Asian supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Device and Fitting Costs

High upfront costs for devices and fittings pose a significant barrier to the growth of the audiological devices market. Many potential users, especially in emerging economies, find these expenses prohibitive. This financial hurdle limits the accessibility of audiological solutions, curbing market expansion. Average premium hearing aid bundles exceed USD 4,000 per pair, deterring adoption where insurance coverage is limited. Cost-sensitive buyers may postpone purchase or switch to basic amplification products, tempering revenue growth. As a result, manufacturers and providers are exploring innovative financing options and subsidies to mitigate this challenge and broaden their market reach.

Persistent Social Stigma Among Younger Users

Style concerns delay help-seeking, particularly in image-conscious urban markets. Fashion-centric solutions such as smart earbuds and eyewear-based amplifiers aim to normalise device use. Highlighting the impact of social perceptions, younger individuals often shy away from using audiological devices due to prevailing societal judgments. This reluctance not only curtails the potential user base but also stifles the overall growth of the audiological devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Audiological Devices Market Segment Analysis

By Product Type:

AI Integration Drives Premium Hearing Aid EvolutionHearing aids held 60.44% of audiological devices market share in 2025, underpinned by sustained demand from older adults and expanding OTC access. The segment benefits from real-time AI chips that deliver up to 10 dB noise-reduction gains, as seen in Phonak Audéo Sphere Infinio. Receiver-in-the-ear and behind-the-ear styles dominate thanks to space for high-capacity batteries and antennas.

Diagnostic devices are growing fastest at 6.93% CAGR, lifted by broader screening mandates and portable imaging advances such as optical coherence tomography otoscopes. Cochlear implants, bone-anchored aids, and software each target niche needs; fully implantable prototypes from MED-EL and Envoy Medical indicate a future of discreet rehabilitation options.

By Disease Type:

Meniere’s Disease Dominance Reflects Diagnostic ComplexityMeniere’s disease accounted for 29.21% of 2025 revenue owing to its multifaceted symptoms that require both vestibular diagnostics and tinnitus-friendly amplification, sustaining demand for premium solutions. The audiological devices market size for this indication will remain robust as awareness campaigns improve early referral patterns.

Otosclerosis is set to record a 6.59% CAGR, supported by refined stapedectomy techniques and conductive-loss-specific hearing aid algorithms. Acoustic neuroma care integrates surgical navigation with post-operative cochlear implantation, while otitis media continues to drive paediatric diagnostic equipment sales such as tympanometers and ultrasound otoscopes.

By Patient Age-Group:

Adult Segment Stability Contrasts with Paediatric InnovationAdults represented 67.85% of 2025 revenue, reflecting demographic weight and rising appreciation of untreated hearing loss consequences. The audiological devices market size for adults is reinforced by value-added functions like fall detection and cognitive health tracking in premium lines.

Paediatrics advances faster at 6.3% CAGR on the back of universal newborn screening and lower implant age approvals, such as FDA clearance for the Osia System at 5 years. Remote monitoring tools let parents track device performance, while classroom audio integration supports inclusive education.

By End User:

ENT Clinics Emerge as Growth LeadersHospitals held 45.30% revenue share in 2025 due to capacity for surgery and complex diagnostics. ENT clinics are growing quickest at 7.28% CAGR by leveraging portable equipment and cloud data solutions to offer one-stop testing and fitting with lower overheads.

Home healthcare is a nascent but rising channel, as remote fitting and smartphone testing enable aging users to receive professional support without clinic visits. Ambulatory surgery centres gain from minimally invasive cochlear implant techniques that permit same-day discharge.

Geography Analysis

North America Audiological Devices Market

North America captured 34.12% of global revenue in 2025 on the back of advanced infrastructure, strong research pipelines, and the landmark OTC rule that expands retail access. Widespread private insurance and Medicare Advantage plans support premium product uptake, yet patchy traditional Medicare coverage creates affordability gaps.

APAC Audiological Devices Market

Asia-Pacific is the fastest-growing region at 7.71% CAGR through 2031, driven by ageing populations in Japan and South Korea and rising disposable incomes in China and India. Government cochlear implant programmes and expanding private clinics accelerate penetration. Urban industrial zones deepen the need for occupational hearing protection, while growing middle-class awareness boosts adoption of advanced hearing aids.

EMEA and South America Audiological Devices Market

Europe shows steady momentum, supported by universal care models that ensure basic access and stringent regulations that maintain quality. Reimbursement frameworks vary, prompting manufacturers to tailor pricing tiers. Middle East and Africa and South America remain nascent but improving: investments in tertiary hospitals and mobile outreach programmes widen access, while urbanisation lifts noise-related demand.

Competitive Landscape

The audiological devices market displays moderate consolidation as leading groups pursue scale to fund R&D while new entrants leverage consumer-electronics know-how. Cochlear’s USD 30 million acquisition of Oticon Medical’s implant unit expanded its portfolio and client base. WS Audiology secured EUR 590 million from ATHOS KG to accelerate growth and possible public listing.

Technology differentiation hinges on AI and connectivity. Phonak’s dedicated AI processor supports speech enhancement, while GN Hearing’s Vivia platform uses Bluetooth LE Audio for multi-stream media access. Consumer players such as Apple integrate hearing assistance into earbuds, intensifying competition and pushing incumbents toward ecosystem partnerships.

Vertical integration and flexible sourcing respond to semiconductor volatility. Manufacturers diversify suppliers and design modular boards to accommodate multiple chipsets, mitigating production risk. Marketing focuses on retail experience: multi-brand clinics, remote service portals, and subscription models aim to lower upfront costs and raise lifetime value.

Audiological Devices Industry Leaders

Audina Hearing Instruments, Inc.

Cochlear Ltd.

GN Hearing A/S

Amplifon SpA

Horentek Hearing Diagnostic

- *Disclaimer: Major Players sorted in no particular order

Audiological Devices Market Companies Covered in this Report

- Sonova

- Demant

- GN Hearing

- WS Audiology

- Cochlear

- Starkey Laboratories

- Amplifon

- Audina Hearing Instruments

- MED-EL

- Natus Medical

- INVENTIS

- Horentek Hearing Diagnostic

- Beltone (GN subsidiary)

- Rion Co. Ltd.

- Eargo

- Elkon Pvt. Ltd.

- Oticon Medical

- Sivantos (Signia)

- Resound

- Interacoustics

Recent Industry Developments in Audiological Devices Market

- March 2025: Envoy Medical enrolled first participants in pivotal study of Acclaim fully implanted cochlear implant.

- March 2025: Medical University of South Carolina launched national trial for fully internal cochlear implants.

- February 2025: Beltone introduced Envision hearing aids with AI-based noise management and Auracast support.

- November 2024: MicroPort unveiled prototype of totally implantable cochlear implant with body-noise cancellation.

Global Audiological Devices Market Report Scope

As per the scope of the report, audiological devices are used for diagnosis and treatment of hearing impairment. The Audiological Devices Market is segmented By Product (Hearing Aids, Cochlear Implants, Bone Anchored Hearing Aids, Diagnostic Devices), By Diseases type (Otosclerosis, Meniere's Disease, Acoustic Tumors, Otitis Media, Others), By End user (Hospitals, Clinics, Ambulatory Centers) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD million) for the above segments. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally.

Segmentation Overview

| Hearing Aids | Behind-the-Ear (BTE) |

| Receiver-in-the-Ear (RITE) | |

| In-the-Ear (ITE) | |

| Canal Hearing Aids (CHA) | |

| Bone-Anchored Hearing Aids | |

| Cochlear Implants | |

| Diagnostic Devices | Audiometers |

| Tympanometers | |

| Otoscopes | |

| Software & Accessories |

| Otosclerosis |

| Meniere’s Disease |

| Acoustic Neuroma |

| Otitis Media |

| Others |

| Pediatric |

| Adults |

| Hospitals |

| ENT Clinics |

| Home Healthcare |

| Ambulatory Surgery Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Hearing Aids | Behind-the-Ear (BTE) |

| Receiver-in-the-Ear (RITE) | ||

| In-the-Ear (ITE) | ||

| Canal Hearing Aids (CHA) | ||

| Bone-Anchored Hearing Aids | ||

| Cochlear Implants | ||

| Diagnostic Devices | Audiometers | |

| Tympanometers | ||

| Otoscopes | ||

| Software & Accessories | ||

| By Disease Type | Otosclerosis | |

| Meniere’s Disease | ||

| Acoustic Neuroma | ||

| Otitis Media | ||

| Others | ||

| By Patient Age-Group | Pediatric | |

| Adults | ||

| By End User | Hospitals | |

| ENT Clinics | ||

| Home Healthcare | ||

| Ambulatory Surgery Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the audiological devices market?

The market stood at USD 14.81 billion in 2026 and is projected to reach USD 19.71 billion by 2031.

Which product category leads the audiological devices market?

Hearing aids dominate with 60.44% 2025 market share, supported by AI and connectivity upgrades.

Why is Asia-Pacific the fastest-growing region?

Rapid ageing, expanding middle-class income, and government implant programmes drive a 7.71% CAGR in Asia-Pacific.

How will OTC regulation influence demand?

The United States OTC rule opens a new retail channel for 49.5 million potential users who previously lacked access to prescription devices.

Which end-user segment is growing quickest?

ENT clinics show the highest CAGR at 7.28%, benefitting from specialised services and efficient workflows.

What technology trends shape future product design?

Real-time AI processing, Bluetooth LE Audio, and fully implantable cochlear implants are setting new performance and cosmetic benchmarks.

Page last updated on: