Virology Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

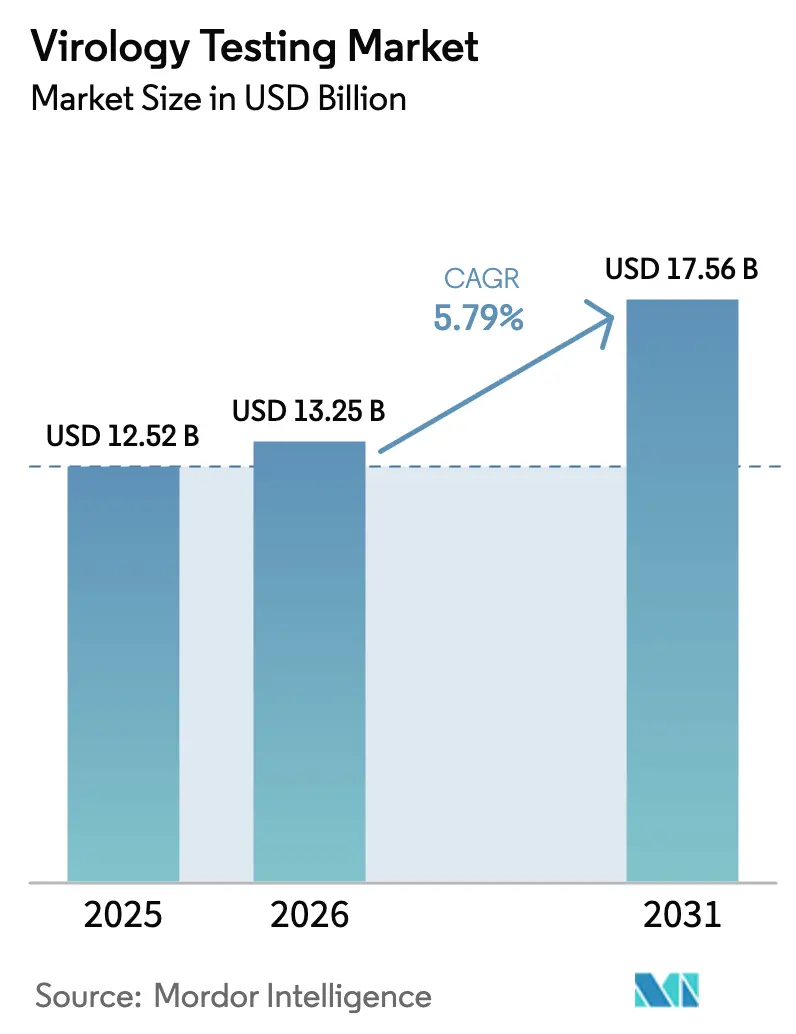

| Market Size (2026) | USD 13.25 Billion |

| Market Size (2031) | USD 17.56 Billion |

| Growth Rate (2026 - 2031) | 5.79% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

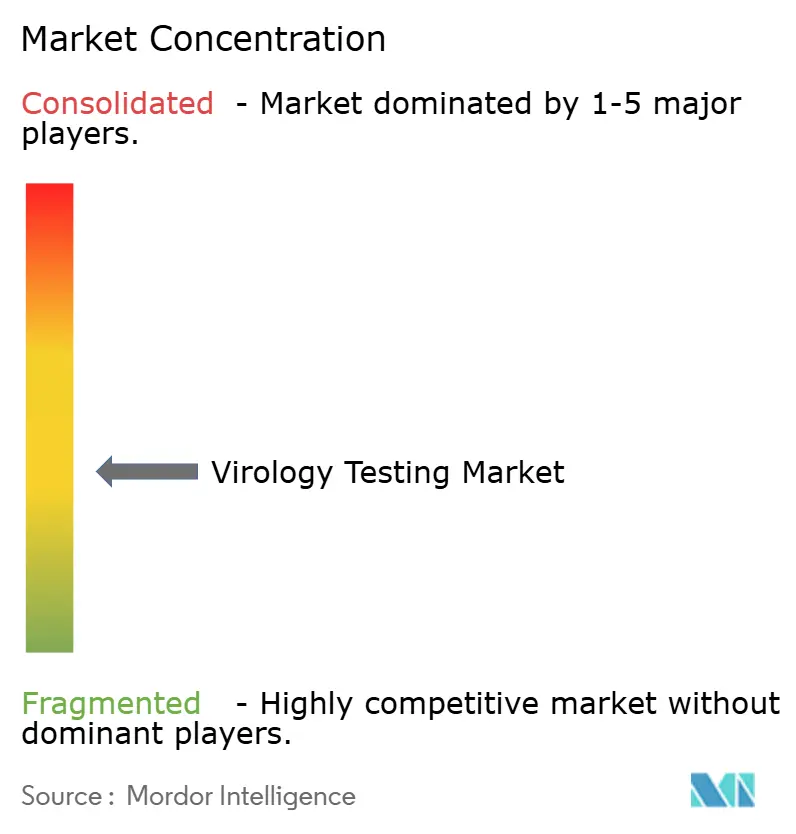

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Virology Testing Market Analysis by Mordor Intelligence

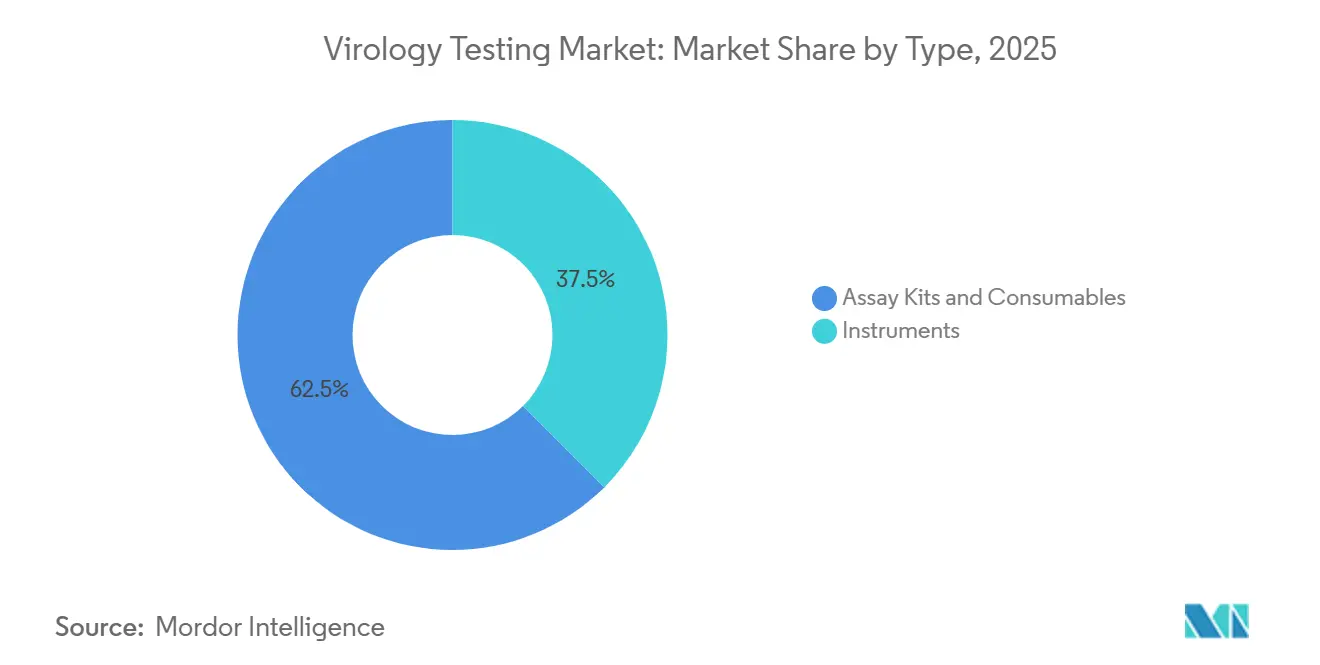

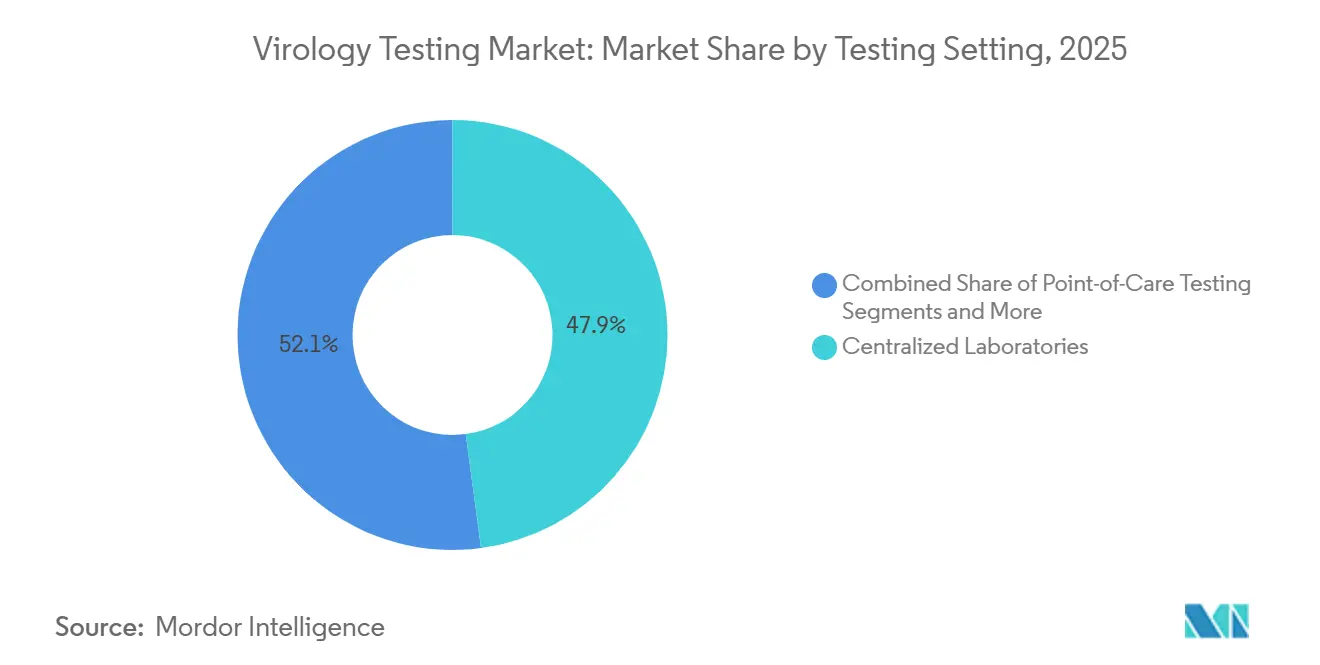

The virology testing market size is expected to increase from USD 12.52 billion in 2025 to USD 13.25 billion in 2026 and reach USD 17.56 billion by 2031, growing at a CAGR of 5.79% over 2026-2031. Laboratories are moving from batch immunoassays to continuous-access molecular systems that trim result times from days to hours, a shift propelled by wastewater-surveillance mandates and strategic stockpiles of multi-pathogen respiratory panels. Consumables commanded 62.46% of 2025 revenue, yet automated instruments will record a 6.76% annual rise through 2031 as hospitals install PCR workcells to handle seasonal testing spikes without adding staff. Molecular diagnostics methods held 49.26% share in 2025 and will grow at 6.67% on the back of FDA-cleared point-of-care platforms such as Cepheid’s CLIA-waived Xpert Bordetella pertussis assay. Centralized laboratories captured 47.89% of 2025 demand, but at-home and self-testing will deliver the quickest 6.81% CAGR as regulatory frameworks mature beyond COVID-19 emergency authorizations.[1]Roche, “Liverpool Clinical Laboratories Case Study,” roche.com

Key Report Takeaways

- By type, consumables captured 62.46% of 2025 revenue, while instruments will post a 6.76% CAGR through 2031.

- By diagnostic technique, molecular methods accounted for a 49.26% virology testing market share in 2025 and are forecast to grow at a 6.67% CAGR through 2031.

- By testing setting, at-home and self-testing are slated to expand at a 6.81% CAGR between 2026 and 2031.

- By end user, hospitals and clinics will grow at a 6.78% pace, overtaking reference-lab growth.

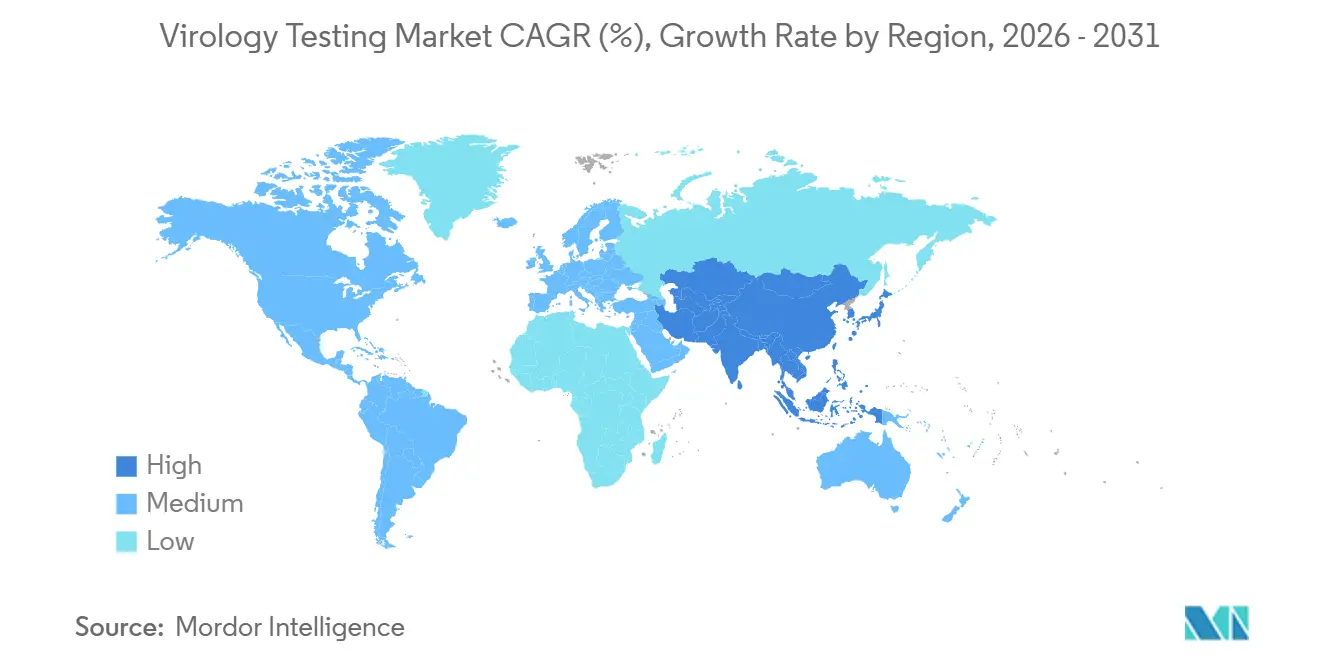

- By geography, Asia-Pacific is positioned for a 6.89% CAGR to 2031, while North America retained 40.23% of 2025 revenue.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Virology Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of viral diseases | +1.2% | Global, with acute pressure in Asia-Pacific and sub-Saharan Africa | Medium term (2-4 years) |

| Growing regulatory clearances for novel assays | +0.9% | North America & EU, spillover to APAC through harmonized submissions | Short term (≤ 2 years) |

| Rapid adoption of molecular POC PCR platforms | +1.4% | North America, Western Europe, urban APAC hubs | Short term (≤ 2 years) |

| Expansion of wastewater-based viral surveillance | +0.7% | North America, Australia, pilot programs in EU and Latin America | Medium term (2-4 years) |

| AI-driven automated laboratory workflows | +0.8% | North America, Western Europe, Japan | Medium term (2-4 years) |

| Government stockpiling of multi-pathogen panels | +0.6% | North America, EU, strategic reserves in Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Viral Diseases

Outbreaks such as 61 U.S. human H5N1 cases in 2024-2025 pressed state labs to expand PCR capacity. Mpox clade Ib detections in Central Africa triggered WHO emergency declarations that accelerated real-time PCR rollouts.[2]Centers for Disease Control and Prevention, “Avian Influenza A(H5N1) Virus,” cdc.gov Chronic programs, for example Egypt’s hepatitis C elimination effort, maintain repeat viral-load testing. These parallel clinical and public-health needs sustain demand for flexible multiplex systems that accept new targets without hardware replacement. Dense populations and expanding access in Asia-Pacific and sub-Saharan Africa amplify volume growth, underpinning the 1.2 percentage-point lift in the global CAGR.

Growing Regulatory Clearances for Novel Assays

The FDA’s breakthrough-device pathway shortened review cycles, exemplified by QIAGEN’s QIAstat-Dx Rise, cleared in September 2025 after an expedited process.[3]QIAGEN, “FDA Clearance for QIAstat-Dx Rise,” qiagen.com Europe’s IVDR, despite deadline extensions, is consolidating suppliers as smaller firms exit rather than absorb high conformity costs. Harmonized guidelines from the International Medical Device Regulators Forum encourage simultaneous submissions, accelerating global launches and adding 0.9 percentage points to the CAGR in developed markets.

Rapid Adoption of Molecular POC PCR Platforms

Cepheid’s GeneXpert network now exceeds 30,000 placements, giving emergency departments rapid triage capability. Abbott’s ID NOW surpasses 100,000 units and returns influenza A/B or SARS-CoV-2 results in 13 minutes. A 2024 Journal of Clinical Microbiology study found point-of-care molecular testing cut hospital stay by 1.2 days, saving USD 2,400 per admission. QIAGEN’s QIAstat-Dx Rise fills the mid-volume gap at 160 continuous samples daily. CLIA waiver extensions broaden the addressable market to roughly 200,000 U.S. physician-office labs, giving the driver a 1.4 percentage-point push.

Expansion of Wastewater-Based Viral Surveillance

The CDC’s National Wastewater Surveillance System spans 1,500 U.S. plants, tracking SARS-CoV-2, influenza A, RSV and mpox. Australia will roll out a nationwide pathogen network in early 2026. The UK evaluated automated liquid-handling and PCR workcells that allow seven-day operation without weekend staff, demonstrating labor savings. Standardized reagent kits tailored to inhibitor-rich wastewater matrices form a new, season-independent consumable stream that lifts CAGR by 0.7 percentage points.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent product-approval regulations | -0.5% | EU (IVDR transition), emerging markets with evolving frameworks | Medium term (2-4 years) |

| Reimbursement & pricing reforms in key markets | -0.7% | North America (CMS CLFS cuts), Europe (national payer negotiations) | Short term (≤ 2 years) |

| Donor-funding cuts disrupting LMIC HIV testing | -0.4% | Sub-Saharan Africa, Southeast Asia | Short term (≤ 2 years) |

| Global shortage of skilled molecular technologists | -0.6% | Global, acute in North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Product-Approval Regulations

IVDR compliance costs can top EUR 500,000 per device family, and notified-body capacity is limited to 30 organizations, creating year-long approval queues. India adopted local-validation rules in 2024, adding further complexity. Smaller assay makers are leaving the EU, narrowing menu variety and shaving 0.5 percentage points off CAGR during the transition.

Reimbursement & Pricing Reforms in Key Markets

CMS cut the Clinical Laboratory Fee Schedule 1.3% in 2025 and Medicare Advantage plans imposed prior authorization for costly molecular tests. Germany’s payer networks negotiated 15%-20% discounts on respiratory panels in 2024. These pricing pressures subtract 0.7 percentage points from CAGR in the short term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Instruments Drive Capital Refresh Cycles

Instruments will climb at a 6.76% pace to 2031, outstripping the overall virology testing market. Hospitals are buying integrated PCR workcells such as Roche’s cobas 5800 to overcome staffing gaps and compress turnaround. Consumables still generated 62.46% of 2025 revenue, anchoring the virology testing market size with recurring sales. Instruments, however, carry 50%-60% gross margins and deliver service-contract annuities, fostering vendor lock-in. Public-sector budget caps in Europe temper adoption, but automation imperatives keep the sub-segment on a faster trajectory.

Consumables will continue to dominate revenue through 2031 as wastewater programs and chronic-disease monitoring lift test volumes. Even so, capital budgets are prioritizing multi-panel PCR systems that accept respiratory, STI and bloodborne targets on a single chassis, keeping instrument growth lively. Validation costs and staff-training hurdles create switching friction that benefits established vendors.

By Diagnostic Technique: Molecular Methods Sustain Dominance

Molecular methods captured 49.26% of 2025 dollars and will advance at a 6.67% clip, steering the virology testing market share toward higher-complexity assays. PCR remains the backbone, bolstered by CLIA-waived cartridges like Xpert Bordetella pertussis.

Falling sequencing costs—USD 200-300 per sample on Illumina’s NextSeq 1000/2000—are making NGS surveillance feasible for routine outbreak response. Immunoassays lose ground as molecular platforms match turnaround speed at declining prices. Mass-spectrometry stays niche for viral work, and culture techniques remain isolated to reference labs.

By Testing Setting: At-Home Testing Rebounds Post-Pandemic

At-home testing will rebound at a 6.81% CAGR, led by FDA-cleared OTC combo tests for flu and SARS-CoV-2. Centralized labs still held 47.89% of 2025 revenue owing to viral-load and genotyping services.

Point-of-care systems like GeneXpert and ID NOW bridge the gap, enabling sub-hour results within clinical workflows. Quality-control warnings from FDA in 2024 spotlight the need for rigorous validation as home tests extend into STI and hepatitis categories.

By End User: Hospitals Gain Share Through Vertical Integration

Hospitals and clinics will edge up at 6.78% through 2031 as health systems internalize testing to curb send-out fees and capture technical revenue. Mid-throughput solutions such as QIAstat-Dx Rise fit hospital daily volumes without batch delays.

Public-health agencies, meanwhile, represent strategic demand anchored in wastewater surveillance, while reference labs grapple with margin compression under CLFS cuts.

Geography Analysis

Asia-Pacific’s rapid infrastructure spend and infectious-disease burden position the region for the fastest ascent, even as North America continues to supply 40.23% of 2025 sales. China’s domestic firms leverage lower pricing to win tenders, while India deploys 1,000 district-level PCR labs by 2027. Australia’s nationwide wastewater network exemplifies policy-driven demand outside clinical cycles.

Europe, holding roughly one-quarter of 2025 revenue, is constrained by IVDR compliance costs that push smaller vendors out, narrowing instrument menus but solidifying demand for big-platform replacements. Bulk-purchase price deals in Germany and France hold down ASPs.

Middle East and Africa expand regional hubs to meet fast-response regulations, yet donor-funding cuts threaten sub-Saharan HIV testing continuity. South America adds capacity via public-private deals, but foreign-exchange swings hamper reagent imports, moderating growth.

Competitive Landscape

The top five suppliers—Roche, Abbott, Danaher, Thermo Fisher and Hologic—collectively command a large share of global revenue. Roche’s cobas 5800 installation in Liverpool cut sexual-health turnaround to one day, underscoring automation value. Danaher’s Cepheid secured CLIA waiver for pertussis cartridges, extending reach to 200,000 U.S. physician-office labs.

Second-tier players, including Seegene and QuidelOrtho, differentiate through broad multiplex menus but face margin pressure from pricing reforms. Oxford Nanopore’s portable sequencers open field-based surveillance opportunities, while QIAGEN’s Rise platform serves mid-volume hospital labs. Agilent embeds AI quality-control in automated workcells to cut manual review by 40%. Regulatory uncertainty over adaptive algorithms may slow high-stakes deployments, but installed-base lock-in keeps competition moderate.

Virology Testing Industry Leaders

F. Hoffmann-La Roche AG

Bio-Rad Laboratories Inc

Hologic Inc.

Thermo Fisher Scientific Inc.

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: QIAGEN secured FDA clearance for QIAstat-Dx Rise, a 160-sample-per-day continuous-access molecular platform.

- October 2024: Healgen obtained FDA authorization for the first OTC combo flu and COVID-19 molecular test.

- September 2024: Roche launched a test using the company’s technology to simultaneously detect up to 12 respiratory viruses. The launch, enables users of Roche’s Cobas 5800, 6800 and 8800 molecular diagnostic analyzers to test for pathogens including influenza A and B, RSV and the COVID-19 virus.

- June 2024: QIAGEN announced the launch of 35 new wet-lab tested digital PCR Microbial DNA Detection Assays for its digital PCR (dPCR) platform QIAcuity, significantly enhancing its offerings in the field of microbial research. The new assays were available on QIAGEN’s comprehensive research platform GeneGlobe and are designed to target a wide range of pathogens responsible for tropical diseases, sexually transmitted infections (STIs) and urinary tract infections (UTIs), further solidifying QIAGEN's position as a leader in microbial detection and analysis.

Global Virology Testing Market Report Scope

As per the scope of the report, virology testing involves different diagnostic techniques used in identifying viruses. Viruses can be diagnosed by different procedures such as cell culture methods, specific antibody detection, antigen detection, virus nucleic acid detection, gene sequencing, and hemagglutination assays. The Virology Testing Market is segmented By Type (Instruments, Assay Kits and Consumables), By Diagnostic Technique (Molecular Diagnostics Method, Immunoassay based Method, Mass Spectroscopy based Method, and Others), By End User (Hospitals and Clinics, Diagnostic Laboratories, and Others) and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The report offers value (in USD million) for the above segments. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally.

| Instruments |

| Assay Kits & Consumables |

| Molecular Diagnostics Method | PCR-based Methods |

| NGS-based Methods | |

| Immunoassay-based Method | |

| Mass-Spectrometry-based Method | |

| Others |

| Centralized Laboratories |

| Point-of-Care Testing |

| At-Home and Self-Testing |

| Hospitals and Clinics |

| Diagnostic Laboratories |

| Public Health and Surveillance Agencies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Instruments | |

| Assay Kits & Consumables | ||

| By Diagnostic Technique | Molecular Diagnostics Method | PCR-based Methods |

| NGS-based Methods | ||

| Immunoassay-based Method | ||

| Mass-Spectrometry-based Method | ||

| Others | ||

| By Testing Setting | Centralized Laboratories | |

| Point-of-Care Testing | ||

| At-Home and Self-Testing | ||

| By End User | Hospitals and Clinics | |

| Diagnostic Laboratories | ||

| Public Health and Surveillance Agencies | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the virology testing market in 2031?

It is forecast to reach USD 17.56 billion by 2031, growing at a 5.79% CAGR.

Which segment will grow fastest by testing setting?

At-home and self-testing are set to expand at a 6.81% CAGR through 2031 as regulatory pathways mature.

Why are instruments outpacing consumables in growth?

Hospitals are refreshing capital with automated PCR workcells that handle rising volumes while offsetting technologist shortages, giving instruments a 6.76% CAGR.

Which region shows the strongest growth outlook?

Asia-Pacific is poised for a 6.89% CAGR, driven by expansive laboratory-network investments and streamlined IVD approvals.

How are reimbursement changes affecting U.S. laboratories?

A 1.3% CLFS cut in 2025 is squeezing reference-lab margins and accelerating hospital in-sourcing of molecular testing.

What role does wastewater surveillance play in market expansion?

National programs in the U.S. and Australia create a steady consumable stream independent of seasonal clinical volume, lifting overall demand.

Page last updated on: