Vitrification Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

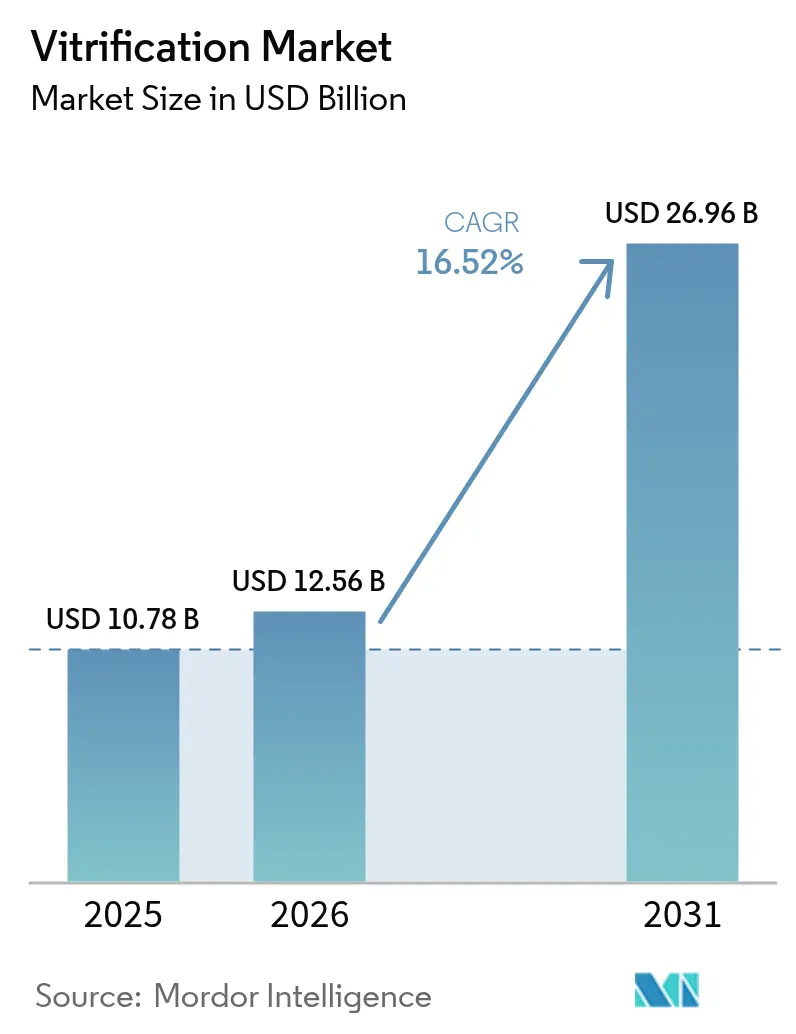

| Market Size (2026) | USD 12.56 Billion |

| Market Size (2031) | USD 26.96 Billion |

| Growth Rate (2026 - 2031) | 16.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

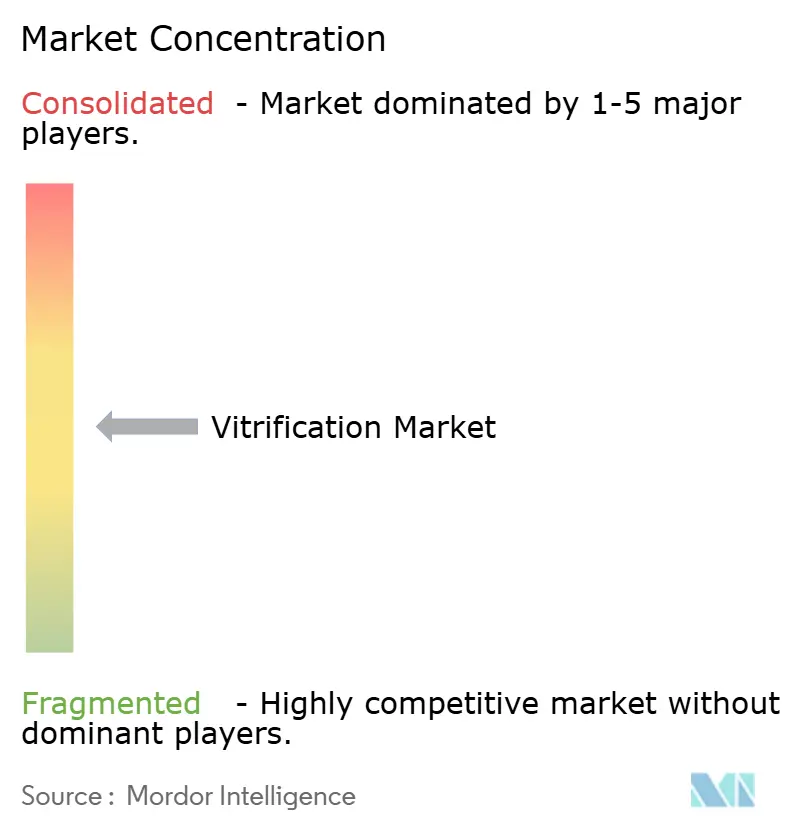

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vitrification Market Analysis by Mordor Intelligence

The vitrification market size was valued at USD 10.78 billion in 2025 and estimated to grow from USD 12.56 billion in 2026 to reach USD 26.96 billion by 2031, at a CAGR of 16.52% during the forecast period (2026-2031). This steep trajectory shows how delayed parenthood, higher infertility prevalence, and rapid laboratory automation have combined to make vitrification the preferred cryopreservation approach over slow-freezing techniques. Expanded insurance coverage, especially in Europe and several Asia-Pacific markets, is widening access, while cloud-connected microfluidic platforms are standardizing outcomes across clinics of varied scale. The shift from “last-chance” oncology fertility care to elective, career-timed egg banking is enlarging the customer base, and falling per-cycle costs are enabling price-sensitive clinics in emerging economies to adopt the technology. Competitive intensity now centers on automation, artificial intelligence, and integrated consumable–device ecosystems that boost survival rates above 90%. These developments confirm the vitrification market as a cornerstone of modern fertility services.

Key Report Takeaways

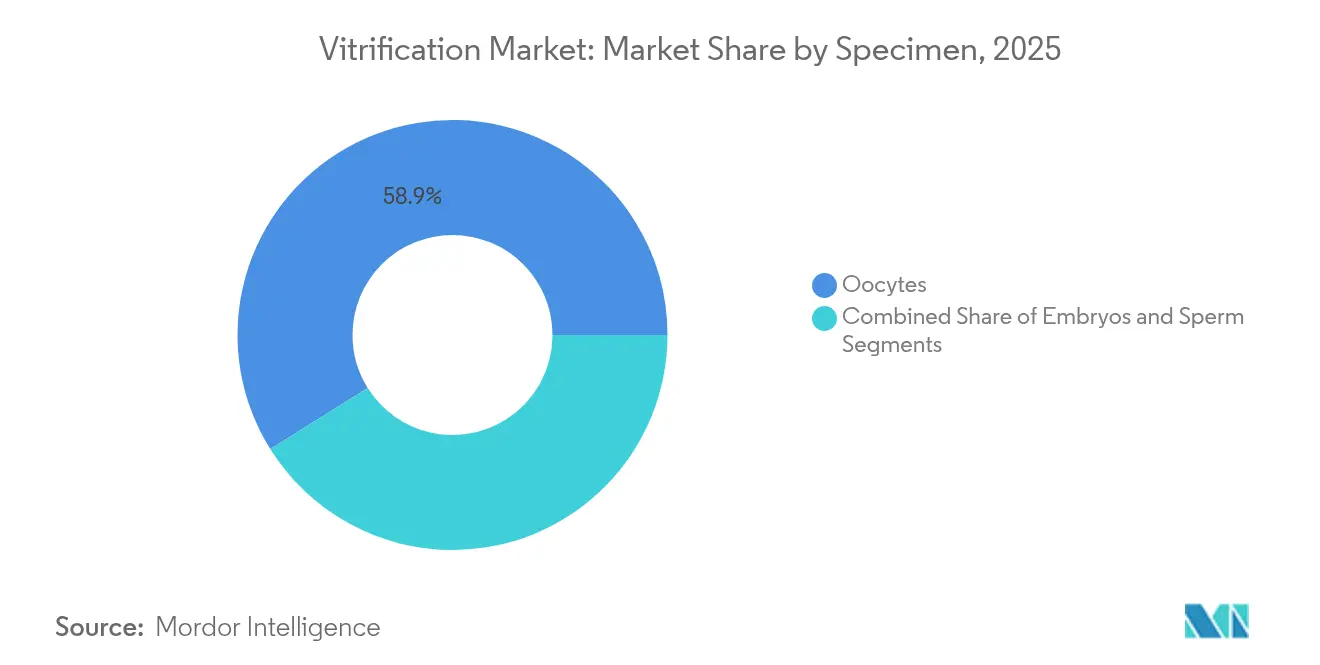

- By specimen, oocytes led with 58.90% vitrification market share in 2025, while embryos are forecast to expand at a 17.65% CAGR through 2031.

- By end user, IVF clinics held 71.80% of the vitrification market share in 2025; biobanks are projected to post the fastest growth at a 17.20% CAGR to 2031.

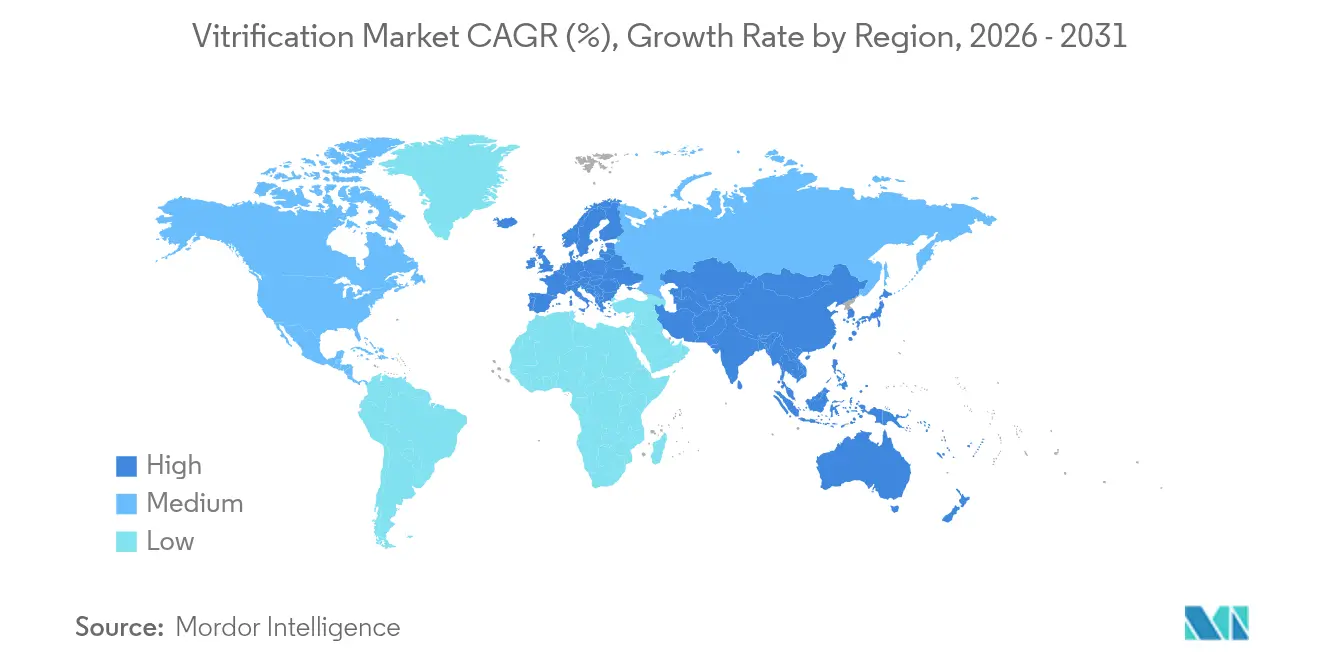

- By geography, Europe commanded 38.20% of the vitrification market size in 2025, whereas Asia-Pacific is anticipated to accelerate at an 18.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vitrification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth In Fertility-Preservation Techniques | +3.2% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Delayed Child-Bearing Due To Sociodemographic Factors | +4.1% | Global, concentrated in developed economies | Long term (≥ 4 years) |

| Rising Global Infertility Prevalence | +2.8% | Global, with highest impact in Asia-Pacific | Medium term (2-4 years) |

| Greater Public Awareness Of Reproductive Health | +1.9% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Automated Micro-Fluidic Vitrification Systems Cut Skill Barriers | +2.6% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Asian Private-Insurance Plans Adding Egg-Freezing Coverage | +1.7% | Asia-Pacific core, spill-over to emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth in Fertility-Preservation Techniques

Improved vitrification protocols have pushed post-thaw embryo survival past 90%, turning what began as a rescue tool for oncology patients into a mainstream option for anyone wanting reproductive flexibility. Live-birth outcomes for vitrified embryos now equal—and in some programs exceed—those of fresh transfers, in part because clinicians can synchronize embryo transfer with an optimally prepared endometrium[1]“Vitrification & Egg Freezing | Learn More with PFC,” Pacific Fertility Center, pacificfertility.com. Artificial-intelligence software is beginning to tailor cryoprotectant dosing and cooling curves to individual oocyte characteristics, making the procedure more predictable and less operator-dependent. This technical leap is expanding indications beyond strict medical necessity and positioning vitrification as a planning resource integrated throughout the fertility journey. Clinics therefore market cryopreservation not as emergency insurance but as a proactive tool that fits varied lifestyle timelines across multiple continents.

Delayed Child-Bearing Due to Sociodemographic Factors

Across high-income economies, the median age at first birth has exceeded 30 years, a shift driven by education gains, career commitments, and evolving partnership norms. Women increasingly regard elective egg freezing as sound life-planning rather than extraordinary medicine, and employer-funded programs are normalizing the practice. Countries such as Sweden, Japan, and South Korea now publish some of the highest per-capita cryopreservation rates, offering an insight into how demand will unfold elsewhere. This demographic momentum is unlikely to reverse, securing a long-run growth engine for the vitrification market. Fertility centers are therefore recalibrating marketing, patient education, and bundled pricing to serve healthy women in their late twenties and early thirties rather than limiting outreach to couples already struggling with conception.

Rising Global Infertility Prevalence

Roughly 17.5% of the adult population now experiences infertility, with Asia-Pacific showing the steepest rise in both primary and secondary forms. Conditions such as polycystic ovary syndrome are lengthening treatment timelines, and embryo banking strategies built on vitrification are becoming essential in multi-cycle IVF plans. Environmental pollutants, sedentary lifestyles, and delayed age at first pregnancy further compound fecundity challenges. As evidence for multi-cycle cumulative live-birth benefits grows, clinics are increasingly recommending embryo or oocyte banking, broadening the vitrification market footprint from an optional add-on to a routine core procedure. These epidemiological realities ensure that demand growth will stay resilient even if economic cycles soften.

Automated Micro-Fluidic Vitrification Systems Cut Skill Barriers

Microfluidic workstations consolidate cryoprotectant loading, equilibration, and plunge into liquid nitrogen into a single sealed device, lifting survival rates to more than 96% in some trials. By shrinking operator variability, they enable medium-volume or resource-constrained clinics to deliver results formerly reserved for top research hospitals. The same platforms stream real-time data to the cloud, allowing quality-assurance teams to spot deviations quickly and adjust parameters across networks of clinics. Over time, the data lake generated will sharpen predictive algorithms and squeeze further variability out of outcomes. Lower training needs, standardized protocols, and declining consumable costs all combine to open new geographic and demographic segments for the vitrification market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ethical Debates On Long-Term Gamete Storage | -1.4% | Global, with strongest impact in conservative regions | Long term (≥ 4 years) |

| High Cost Of Vitrification Media & Devices | -2.3% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Limited Biobank Capacity In Emerging Markets | -1.8% | Asia-Pacific, Middle East, Africa, Latin America | Medium term (2-4 years) |

| Perceived Freeze-All Success-Rate Gap Causing Patient Hesitancy | -1.1% | Global, with regional variations in perception | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Vitrification Media & Devices

Procedure fees in the United States typically range from USD 8,000 to USD 20,000 per cycle, and yearly storage charges often rise faster than general inflation[2]Amber Ferguson, “As the Cost of Storing Frozen Eggs Rises, Some Families Opt to Destroy Them,” Washington Post, washingtonpost.com. In lower-income markets, varying import duties and weakened currencies can make laboratory consumables two to three times more expensive than in origin countries. These economics push clinics to pass costs on to patients, limiting uptake despite high latent demand, especially in populous nations such as India and Indonesia. While automation promises to lower consumable use, the current supply base is concentrated among a handful of device and media suppliers who maintain pricing power through patented formulations. Broader adoption of generic cryoprotectants and local manufacturing could ease the issue, but near-term affordability remains the largest single brake on vitrification market growth.

Limited Biobank Capacity in Emerging Markets

Infrastructure remains patchy across many high-growth geographies. Nations such as the UAE recently expanded cord-blood laboratories from two to eight, illustrating both rising demand and the investment burden linked to safe storage. Temperature excursions and catastrophic sample losses reported in Brazil and parts of Africa highlight the risks when backup generators, telemetry, or maintenance expertise fall short. Building a compliant facility demands concrete vaults, multi-layer monitoring, and accredited personnel—requirements that stretch the budgets of smaller clinics and limit the placements of regional hubs. Partnerships between international device makers and local investors may bridge this gap, but until capacity aligns with demand, storage bottlenecks will dampen full vitrification market potential in several emerging economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Specimen: Oocytes Lead While Embryos Accelerate

Oocytes delivered 58.90% of the vitrification market size in 2025 thanks to social-egg-freezing programs, employer reimbursement, and women’s rising interest in reproductive optionality. Marketing campaigns from large clinic chains now frame egg freezing as a standard life-planning tool, and survival rates above 90% in leading programs have alleviated earlier quality concerns. The segment benefits disproportionately from microfluidic automation because oocyte viability is sensitive to human-induced osmotic shock; precise fluid-exchange control therefore directly boosts clinical outcomes. Embryos, though smaller in revenue today, show an 17.65% CAGR to 2031 as clinics rely on freeze-all protocols to avoid ovarian hyper-stimulation risk and to stagger multiple transfers over time. A 2024 multicenter analysis reported 12.5% live-birth rates for frozen day-6 blastocysts versus 5.5% for fresh controls, fueling clinician comfort with banking multiple embryos ahead of transfer. As payors shift toward outcome-based reimbursement, embryo banking aligns incentives for both providers and patients, supporting the specimen segment’s brisk expansion within the vitrification market.

Technological convergence is narrowing historical outcome gaps between specimen types. AI-driven image analytics can now grade oocyte morphology at a pixel level, flagging sub-optimal samples for tailored cryoprotectant regimes. Meanwhile, embryo monitoring platforms integrate time-lapse photography with metabolic assays, further refining selection and post-thaw implantation odds. These layered innovations increase confidence in deferred transfers, making vitrification an embedded step rather than an optional add-on. Consequently, the share advance of embryos is not expected to erode oocyte revenue; instead both segments will likely grow in parallel, reinforcing the overall momentum of the vitrification market.

By End User: IVF Clinics Dominate as Biobanks Expand

IVF clinics controlled 71.80% of the vitrification market size in 2025 because they own the patient journey from consultation through pregnancy testing. Integration allows a single team to manage stimulation, retrieval, freezing, and eventual transfer, reducing attrition and boosting revenue per patient. Clinics also benefit from in-house lab oversight, which supports continuous protocol refinement. In contrast, independent biobanks captured a smaller share but are growing at 17.20% CAGR as pharma and academic groups require large-scale, GMP-grade sample storage for research pipelines, cell-therapy trials, and long-horizon fertility preservation. Cryo-Cell’s recent 56,000 square-foot Durham site, equipped for 226 liquid-nitrogen dewars, exemplifies the scale needed for next-generation biobank operations.

Automation is reshaping both end-user segments. Clinics are installing tabletop vitrification robots that cut hands-on time per oocyte batch from 12 minutes to under 4, allowing embryologists to oversee more cycles per shift. Biobanks, meanwhile, leverage barcode-to-cloud chain-of-custody and predictive maintenance software to lower risk and satisfy auditors. Regulatory movements toward centralized, accredited storage—especially in the European Union’s updated Tissue and Cells Directive—are likely to accelerate the biobank share lift by encouraging smaller clinics to outsource cryostorage. Over the forecast period, both channels will scale, but their distinct business models mean competition will stay limited, with each set of operators optimizing for different success levers inside a broadening vitrification market.

Geography Analysis

North America remains a mature but steadily expanding pocket of the vitrification market. High disposable incomes, widespread employer coverage for egg freezing, and FDA clearance of several automation systems keep procedure volumes rising despite a plateau in clinic numbers. The United States also hosts the largest installed base of AI-enabled embryo-assessment platforms, which, in turn, drives higher thaw-survival benchmarks. Canada’s single-payer reimbursement for medically indicated fertility preservation further insulates demand from economic cycles, while Mexico’s medical-tourism corridor attracts cost-conscious patients from the broader Americas, giving North America its status as an innovation and volume hub within the global vitrification market.

Europe contributes the largest regional share—38.20% of the overall vitrification market size—thanks to long-standing regulatory clarity and consistent reimbursement policies. National programs in France, Germany, and the Scandinavian bloc limit out-of-pocket costs, cementing vitrification as routine clinical practice. Longitudinal registries also capture outcome data, enabling evidence-based refinements. The region’s early embrace of elective fertility preservation and well-established biobank networks keep utilisation rates high. A 2024 Mayo Clinic review found that ovarian-tissue vitrification protocols developed in Europe now guide practice worldwide. Consequently, European centers export clinical know-how through partnerships in the Middle East and Latin America, reinforcing their leadership role.

Asia-Pacific, forecast to register an 18.20% CAGR, is the most dynamic arena for the vitrification market. Rising infertility prevalence, supportive government policies in Singapore and Japan, and private-insurance coverage extensions in China are driving double-digit cycle growth. Yet the region also faces marked infrastructure gaps: India’s tier-2 cities often lack compliant biobank capacity, and regulatory ambiguity in the Philippines delays clinic license approvals. Nonetheless, device makers are increasingly establishing regional production and training hubs to localize costs. Thailand and Malaysia market themselves as cross-border fertility destinations, offering mid-priced packages that include egg freezing and multi-cycle IVF, broadening access for patients from high-cost home countries. These forces position Asia-Pacific as the primary incremental revenue engine for the vitrification market over the next half-decade.

Competitive Landscape

The vitrification market exhibits moderate fragmentation but rising technological concentration. Legacy device leaders Vitrolife AB, CooperSurgical Inc., and Cook Medical LLC retain broad catalogs that cover cryoware, culture media, and vitrification devices, allowing them to bundle offerings and maintain customer loyalty. Cook’s October 2024 launch of the NestVT series illustrates incumbents’ push to refresh product lines with ergonomic cooktops and pre-measured media cassettes. At the same time, disruptive entrants such as Overture Life, Gameto, and TMRW Life Sciences leverage proprietary microfluidic chips, robotic platforms, and cloud-first tracking to challenge the status quo. Overture’s DaVitri system reported 96.4% oocyte survival in pilot deployments, a figure that outperforms many manual programs and exemplifies the performance pressure new technology brings.

Strategic moves underline a pivot toward integrated hardware-software ecosystems. Gameto’s Phase 3 trial of its investigational in-vitro maturation medium aims to collapse a standard IVF cycle from 12 days to as few as 3, potentially multiplying clinic throughput. Vitrolife, meanwhile, bundles its EmbryoScope time-lapse incubators with analytics licenses, tying consumable use to recurring software subscriptions. In emerging markets, turnkey partnerships between Western device makers and local hospital groups exchange technology transfer for guaranteed consumables contracts, a model that accelerates capacity build-out and locks in future revenue. Competitive intensity therefore revolves less around price and more around total-solution value and data-driven outcome advantages.

M&A activity is expected to intensify as larger players seek niche AI or automation capabilities. Several mid-sized Korean device firms are rumored to be acquisition targets for multinationals needing localized manufacturing to benefit from new Asia-Pacific trade agreements. Likewise, European biobanks exploring IPO exits could attract bids from private-equity funds eager to consolidate storage capacity and scale subscription revenue. Such deals would elevate market concentration and might trigger antitrust scrutiny in jurisdictions where two suppliers already control more than 70% of vitrification media sales. Nevertheless, sustained innovation momentum and regional diversification suggest a healthy competitive ecosystem will prevail, anchoring long-term growth for the vitrification market.

Vitrification Industry Leaders

Kitazato Corporation

IVF Store LLC

Vitrolife AB

Cryotech Co. Ltd.

Cook Medical LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Kitazato Corporation unveiled Ultra-Fast Vitri, a protocol designed to streamline oocyte vitrification and further protect cell viability.

- October 2024: Cook Medical introduced its NestVT vitrification device in the United States.

Global Vitrification Market Report Scope

As per the scope of this report, vitrification is a technique used in the freezing of embryos and eggs so that they can be kept for later use. Vitrification techniques are useful for preserving cells and tissues, and it has a wide range of uses in reproductive biology and regenerative medicine. It is used in human fertility preservation, cell storage for tissue regeneration, cell therapy, and gamete and embryo banking, among other things. The vitrification market is segmented By Specimen (Oocytes (Devices and Kits & Consumables), Embryo (Devices and Kits & Consumables), and Sperm)), By End User (IVF Clinics and Biobanks), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The vitrification market is projected to register a CAGR of 15.9% during the forecast period. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Oocytes | Devices |

| Kits & Consumables | |

| Embryos | Devices |

| Kits & Consumables | |

| Sperm |

| IVF Clinics |

| Biobanks |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Specimen | Oocytes | Devices |

| Kits & Consumables | ||

| Embryos | Devices | |

| Kits & Consumables | ||

| Sperm | ||

| By End User | IVF Clinics | |

| Biobanks | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the vitrification market by 2031?

The vitrification market is expected to reach USD 26.96 billion in 2031, growing at a 16.52% CAGR.

Which specimen type currently generates the highest revenue?

Oocytes account for 58.90% of revenue and maintain leadership due to widespread social egg-freezing programs.

Why is Asia-Pacific the fastest-growing region?

The region’s rising infertility rates, supportive insurance coverage, and infrastructure expansion underpin an 18.20% CAGR through 2031.

How are automated microfluidic systems changing the market?

They lift survival rates above 90%, cut hands-on time, and allow smaller clinics to offer standardized vitrification without extensive embryologist training.

What are the main barriers to broader adoption?

High procedure costs, limited biobank capacity in emerging markets, and ethical debates over long-term gamete storage remain the key restraints.

Page last updated on: