Vitamin Deficiency Treatment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

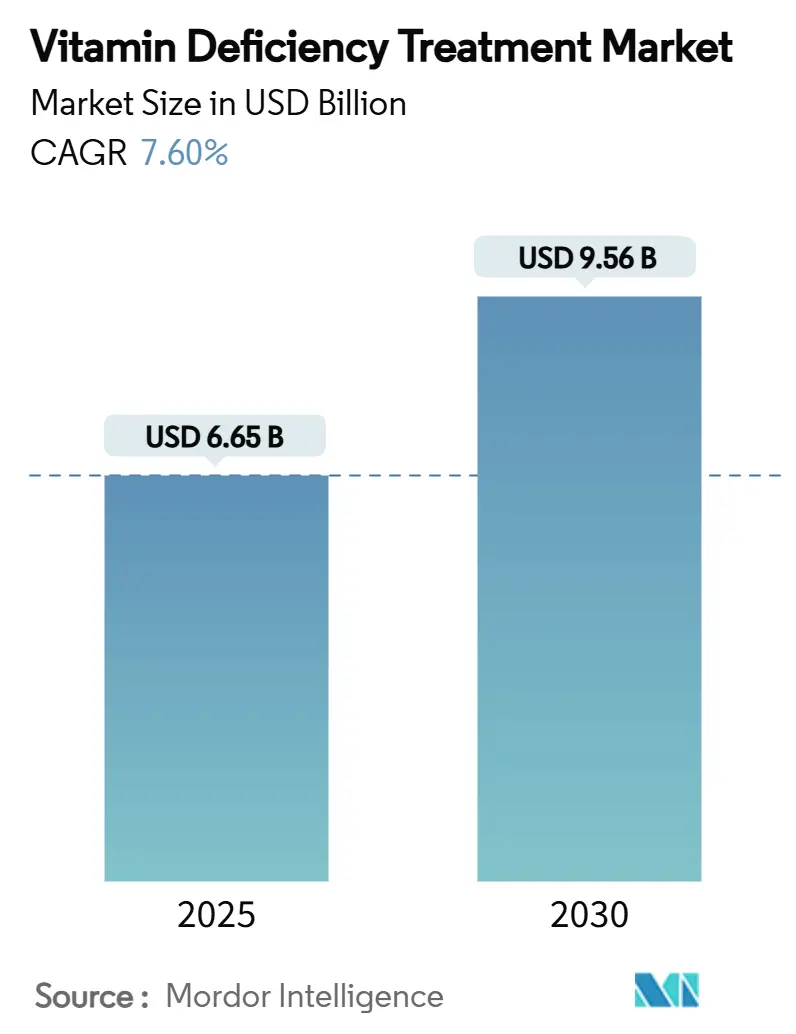

| Market Size (2025) | USD 6.65 Billion |

| Market Size (2030) | USD 9.56 Billion |

| Growth Rate (2025 - 2030) | 7.60% CAGR |

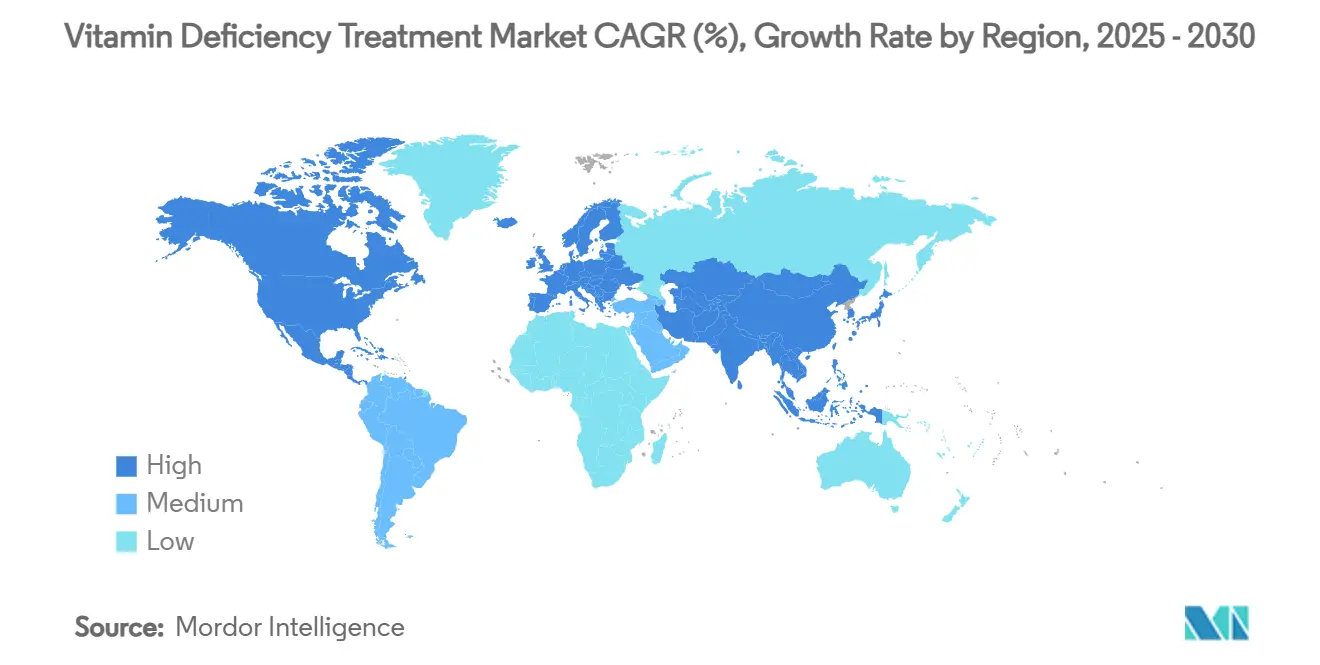

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

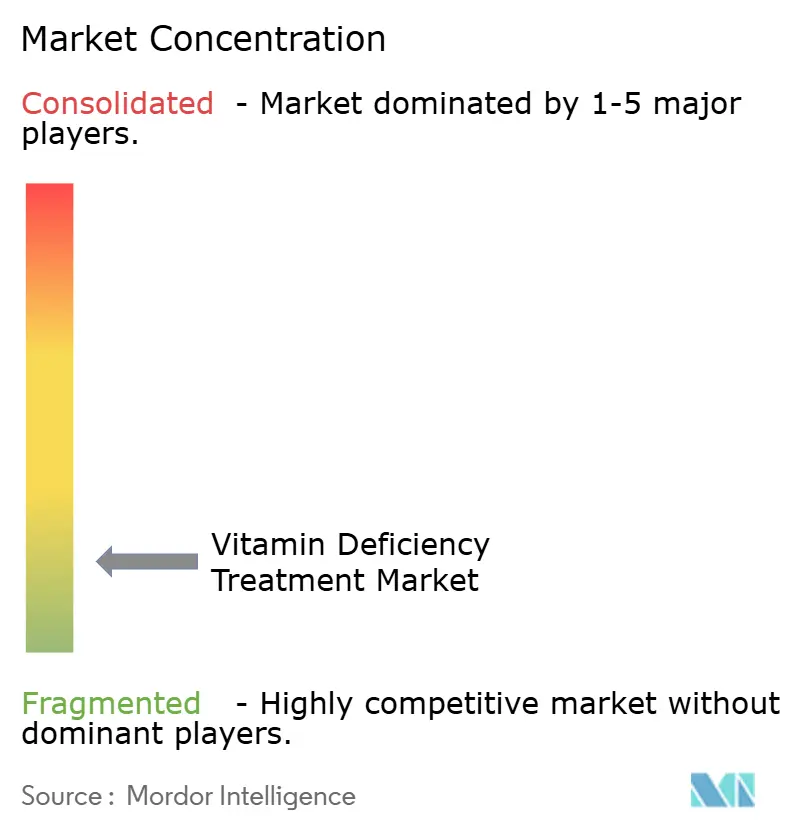

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vitamin Deficiency Treatment Market Analysis by Mordor Intelligence

The current vitamin deficiency treatment market size stands at USD 6.65 billion in 2025 and is forecast to reach USD 9.56 billion by 2030, advancing at a 7.6% CAGR over the period. Rising longevity aspirations, widespread micronutrient deficiencies, and the transition from treatment to prevention are steering the vitamin deficiency treatment market toward double-digit expansion in many sub-segments. An aging consumer base is prioritizing mobility, cognition, and immune resilience, prompting formulators to move beyond generic multivitamins into high-potency, condition-specific offerings. Digital pharmacies, tele-consultations, and AI-driven product matching are removing access frictions, while mandatory food-fortification programs in emerging economies cement baseline demand. Parallel consolidation among ingredient producers and finished-product brands is reshaping competitive dynamics as firms seek end-to-end control of sourcing, formulation, and omnichannel distribution.

Key Report Takeaways

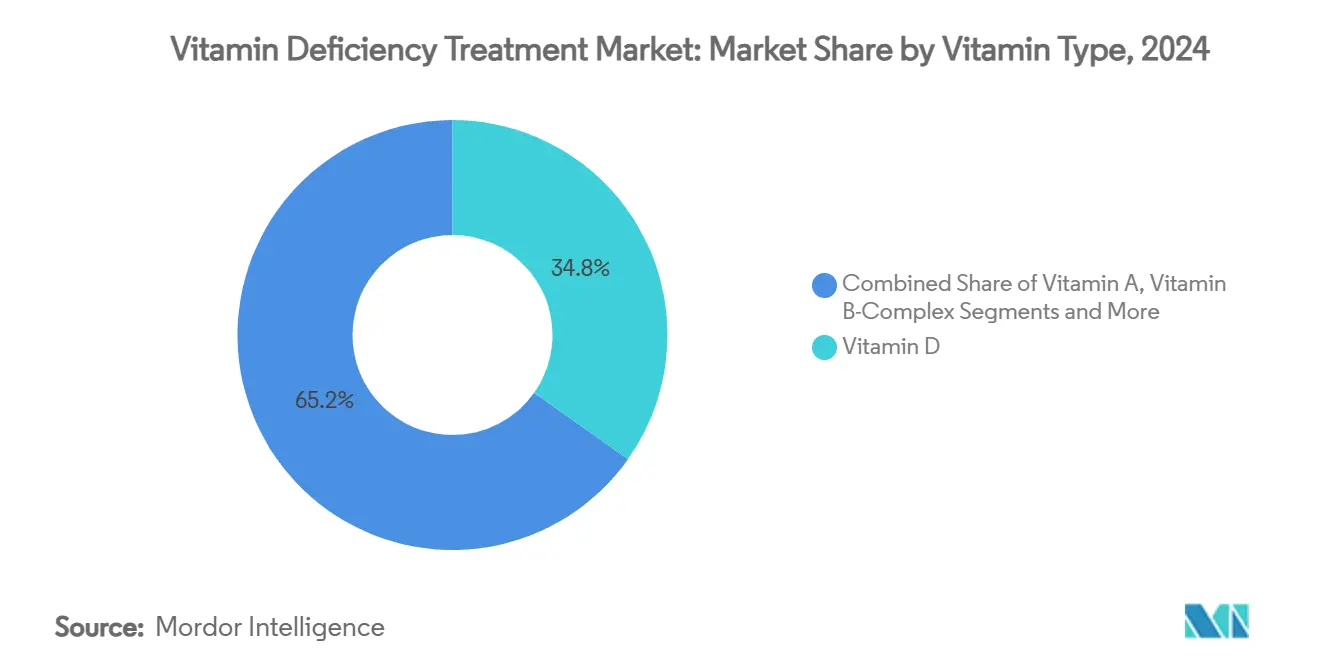

- By vitamin type, Vitamin D captured 34.8% of the vitamin deficiency treatment market share in 2024, whereas Vitamin K2 is projected to post a 10.8% CAGR through 2030.

- By route of administration, oral formats accounted for 72.1% of the vitamin deficiency treatment market size in 2024, while parenteral delivery is forecast to expand at a 12.4% CAGR up to 2030.

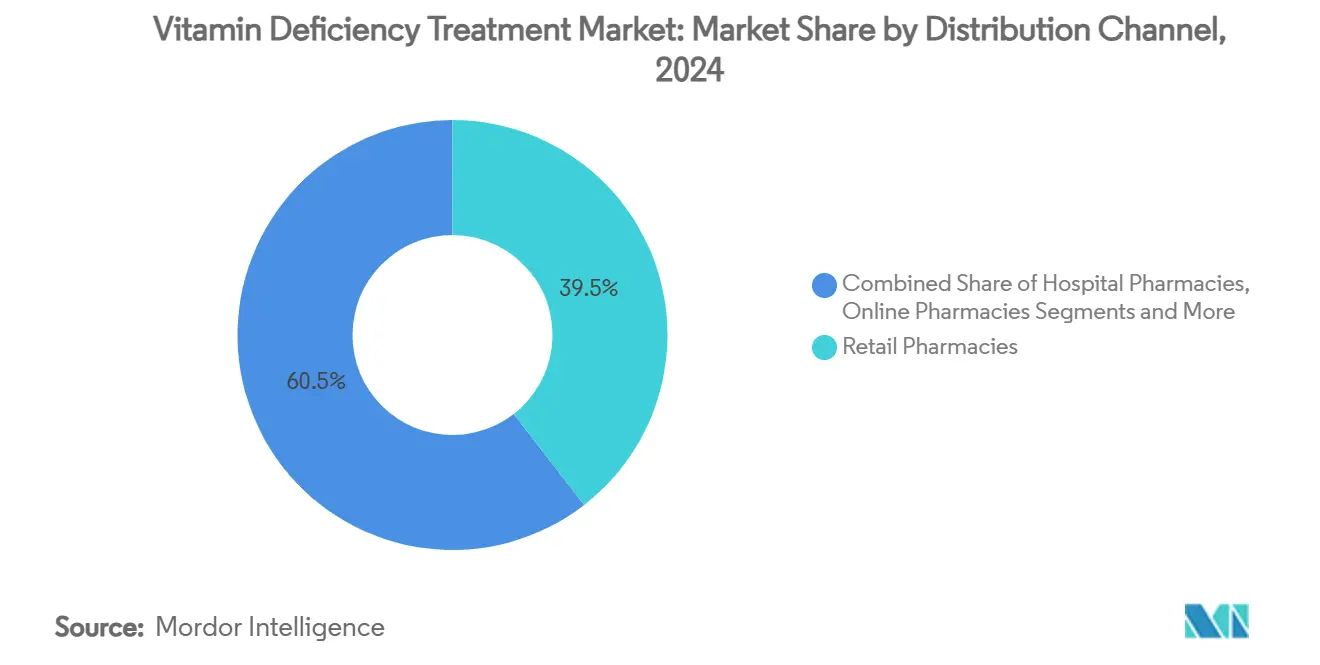

- By distribution channel, retail pharmacies held 39.5% of the vitamin deficiency treatment market share in 2024; online pharmacies are expected to grow at a 14.3% CAGR during the same period.

- By geography, Asia Pacific commanded 35.4% of the vitamin deficiency treatment market size in 2024, and Asia overall is advancing at a 9.0% CAGR through 2030.

Global Vitamin Deficiency Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & chronic disease burden | +2.10% | North America, Europe, Japan | Long term (≥ 4 years) |

| Rising prevalence of vitamin-D & B12 deficits | +1.80% | Asia Pacific, emerging economies | Medium term (2-4 years) |

| Preventive self-care & OTC supplement uptake | +1.40% | North America, EU, urban APAC | Medium term (2-4 years) |

| Expansion of online/tele-pharmacy models | +1.20% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Personalised nutrigenomic algorithms | +0.80% | North America & EU | Long term (≥ 4 years) |

| Mandatory staple-food fortification | +0.90% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Chronic Disease Burden

Longer lifespans in developed and emerging economies are generating sustained demand for nutritional strategies that delay frailty and maintain functional independence. Japan’s anti-aging sector is forecast to exceed USD 3 billion in annual consumer spending by 2028, illustrating how super-aged societies convert demographic pressure into supplemental intake.[1]Produced by, “Sustaining a ‘super-aged’ society,” Nature, nature.comSurveys in 2024 showed 70% of U.S. and U.K. consumers purchasing more healthy-aging formulations, with mobility, immunity, and cognitive clarity cited as top priorities. Generation X—now 44 to 60 years old—reports the highest supplement usage, driven by perceived declines in joint comfort and energy. Clinically backed ingredients position brands to capture premium pricing as shoppers prefer evidence-supported results over generic multivitamins. This demographic engine is expected to propel the vitamin deficiency treatment market well past historical growth norms over the next decade.

Rising Prevalence of Vitamin-D & B12 Deficiencies

One-third of the global population presents sub-optimal serum vitamin D. The deficiency is particularly acute in latitudes where sunlight exposure is limited or cultural dress norms reduce UV contact. Concurrently, vitamin B12 shortfalls affect 47% of Indian adults and a notable share of Chinese hypertensive patients, compromising neurological and cardiovascular health outcomes.[2]Medanta Editorial Team, “Vitamin B12 Deficiency: Symptoms, Causes & Treatment,” medanta.org Large-scale studies from the Czech Republic confirm insufficiency across all age cohorts, emphasizing the need for year-round supplementation irrespective of season. Healthcare systems increasingly frame targeted supplementation as a low-cost prophylactic versus treating rickets, osteoporosis, or neuropathy downstream. Sophisticated machine-learning models now achieve 99.5% accuracy in predicting an individual’s likelihood of deficiency, enabling personalized dosing programs that reinforce demand.

Shift Toward Preventive Self-Care & OTC Supplements

Escalating out-of-pocket medical costs and pandemic-era health awareness have nudged nearly one-third of U.S. adults to maintain multivitamin regimens for day-to-day wellness.[3]Office of Dietary Supplements, “ODS Update: Do Multivitamins Affect Mortality?” National Institutes of Health, nih.gov Retailers are rapidly extending shelf space to emerging condition-specific SKUs, such as GLP-1 support complexes launched in 2025 to offset nutrient losses associated with popular weight-management drugs. Science-driven labeling, clean manufacturing, and transparent sourcing underpin brand differentiation as shoppers scrutinize efficacy claims. The U.S. supplement category still advanced 4.4% in 2024, despite macroeconomic uncertainty, underscoring the resilience of the vitamin deficiency treatment market. With healthy-longevity mindsets entering mainstream culture, preventive self-care stands as a medium-term driver of both volume and average selling price.

Expansion of Online/Tele-Pharmacy Fulfilment Models

Customer willingness to purchase prescriptions and supplements digitally climbed from 34% to 45% within a year on Amazon Pharmacy, indicating a decisive channel shift. Global digital-pharmacy revenue is projected to surpass USD 35 billion by 2026 as AI, blockchain verification, and integrated tele-consultations streamline adherence and personalization. Consumers benefit from algorithmic product matching, same-day delivery, and subscription replenishment, which collectively reduce friction and elevate reorder rates. Regulators have responded by heightening surveillance of e-commerce platforms; the FDA issued multiple warning letters to Amazon to tighten supplement quality oversight, signaling that compliance rigor must keep pace with sales velocity. Overall, the online pivot is contributing the greatest incremental share to the vitamin deficiency treatment market in the short term, while laying infrastructure for longer-term omnichannel ecosystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulatory frameworks & quality-control gaps | -1.30% | Global, pronounced in cross-border trade | Medium term (2-4 years) |

| Risk of hypervitaminosis/toxicity in self-dosing | -0.80% | North America & EU; emerging in urban APAC | Short term (≤ 2 years) |

| Supply-chain volatility for vitamin APIs | -1.10% | North America, Europe | Short term (≤ 2 years) |

| Social-media misinformation eroding consumer trust | -0.60% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Global Regulatory Frameworks & Quality-Control Gaps

Dietary supplement oversight varies widely across jurisdictions, complicating cross-border launches and inflating compliance costs. The U.S. FDA’s inspection resources covered just 5% of registered supplement facilities in FY 2024, raising questions about enforcement consistency. Australia has proposed reclassifying vitamin B6 doses above 50 mg as pharmacist-only medicines by 2027, while France is contemplating stringent upper limits on multiple micronutrients. Within the EU, food-safety heads have listed 117 substances—13 of immediate concern—for harmonized evaluation, further lengthening approval timelines. Such divergence obliges manufacturers to customize formulations and labels market-by-market, deterring smaller entrants and dampening the vitamin deficiency treatment market growth trajectory in the medium term.

Risk of Hypervitaminosis/Toxicity in Unsupervised Self-Dosing

Fat-soluble vitamins accumulate in tissue, and chronic excess can precipitate liver damage, hypercalcemia, or neurological harm. High usage among older adults accentuates the danger; 83% of U.S. residents aged 65 and over use supplements regularly, with overdosing incidents leading to emergency-room admissions. Medical guidance from the Cleveland Clinic warns that megadoses of vitamin A are linked to increased cancer risk, while vitamin D toxicity frequently triggers renal complications. Social-media influencers often recommend unvalidated dosing, amplifying exposure to adverse events. Growing regulatory attention to adverse-event reporting may mandate stricter labeling, potentially constraining near-term category expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vitamin Type: Precision Nutrition Drives Specialization

Vitamin D maintained a commanding 34.8% slice of the vitamin deficiency treatment market in 2024 as clinicians broadened its use beyond bone health to encompass immune modulation and mood balance. Vitamin K2, although comparatively niche, is projected to clock a 10.8% CAGR through 2030—double the overall vitamin deficiency treatment market trajectory, given emerging cardiovascular and bone-metabolism datasets. Balchem’s USD 338 million purchase of Kappa Bioscience underlines surging investor confidence in specialty actives, particularly those backed by clinical validation. Vitamin A continues to attract steady demand from the 4 billion individuals at risk of deficiency worldwide; however, toxicity concerns are pushing formulators toward micro-encapsulated or slow-release formats that minimize overdose potential. Meanwhile, vitamin B complex adoption is buoyed by expanding vegetarian populations and metabolic health discourse across the Asia Pacific.

AI-enabled nutrigenomic testing kits now match genetic polymorphisms to tailored vitamin stacks, nudging consumers away from one-size-fits-all products. Multivitamins still command loyalty among aging cohorts seeking nutritional “insurance,” though market researchers observe trading-up toward condition-specific packs that pair D3 with K2 or B12 with folate for methylation support. Bioavailability has become a premium differentiator; liposomal, nano-emulsified, and cyclodextrin-complexed versions command price premiums of 25-50%, yet deliver absorption scores two to four times higher than conventional tablets. Collectively, evolving science, targeted health goals, and advanced delivery systems ensure that the vitamin deficiency treatment market remains vibrant and increasingly stratified by therapeutic outcome rather than alphabet letter.

By Route of Administration: Innovation Beyond Traditional Oral Delivery

Oral formats, encompassing tablets, capsules, gummies, and powders, retained 72.1% of the vitamin deficiency treatment market share in 2024, thanks to affordability and convenience. Parenteral administration—primarily intramuscular vitamin B12 and intravenous multivitamin cocktails—follows with a 12.4% CAGR up to 2030 as clinicians deploy injectable formulations for malabsorption, bariatric surgery aftercare, and rapid repletion in hospital settings. Although regulatory hurdles remain higher for injectables, growing clinical evidence around improved serum correction rates fuels demand across oncology and geriatrics.

Technologies such as liposomal encapsulation, nano-sphere carriers, and high-pressure micro-fluidization significantly elevate oral bioavailability; recent trials achieved 80% encapsulation efficiency for vitamin C, extending shelf-life and gastric stability. Facilitated Self-Assembling Technology allows solvent-free nano-particle formation for fat-soluble actives like retinoic acid, thereby mitigating reliance on surfactants that often trigger gastrointestinal discomfort. Cyclodextrin complexes have further improved solubility for hydrophobic vitamins, lifting dissolution rates by up to 20-fold and supporting timed release. As scientific refinements narrow efficacy gaps between oral and parenteral modalities, consumer preference for non-invasive intake is expected to keep oral formats dominant within the vitamin deficiency treatment market.

By Distribution Channel: Digital Disruption Reshapes Access

Retail pharmacies accounted for 39.5% of the vitamin deficiency treatment market size in 2024, retaining relevance through pharmacist counseling and insurance-linked traffic. Conversely, online pharmacies are expanding at 14.3% CAGR through 2030, capturing subscription-centric younger demographics and rural populations underserved by brick-and-mortar outlets. Same-day or next-day delivery has become table stakes, with Amazon Pharmacy targeting USD 2 billion in supplement and prescription sales a testament to the channel’s revenue potential.

Hospital outpatient pharmacies are carving a niche for evidence-based, physician-recommended products, particularly injectable vitamin D and B12. Supermarkets and hypermarkets remain volume drivers in Latin America and parts of Asia, yet face margin compression as e-commerce discounts undercut shelf pricing. Specialist wellness stores differentiate by offering in-house nutritional consultations, genomic testing kits, and GLP-1 support stacks not readily available in mass retail. Regulatory scrutiny has intensified for digital platforms; FDA warning letters to Amazon highlight that compliance and transparency must rise in lockstep with sales growth. Looking ahead, omnichannel strategies—combining click-and-collect lockers, virtual chatbots, and brick-and-mortar advisory hubs—are expected to underpin competitive positioning across the vitamin deficiency treatment market.

Geography Analysis

Asia Pacific captured 35.4% of the vitamin deficiency treatment market size in 2024, propelled by widening middle-class disposable income and proactive government fortification policies. India’s health ministry advocates fortifying staples to address a 20% nationwide vitamin D insufficiency rate, potentially lowering barriers for supplement uptake through heightened public awareness. China’s vast but complex regulatory environment, governed by three central agencies, generated about USD 7.5 billion in vitamin sales in 2024, and ongoing rule harmonization aims to bolster consumer confidence.

North America remains the premium epicenter, with legacy brands elevating unit economics via personalization engines and subscription models. The FDA’s new dietary-ingredient master-file pathway promises quicker clearance for innovative formats, yet staffing constraints jeopardize inspection coverage, incentivizing third-party certification to maintain trust. Europe leans toward stricter dosage caps; France’s proposed maximum-level framework could narrow formulation latitude but harmonization may ultimately simplify cross-market launches. Meanwhile, GAIN has channelled USD 300 million into fortification projects across Africa and South Asia, complementing supplement sales by making micronutrients a public-health focus.

Latin America and the Middle East record mid-single-digit growth as economic recovery boosts consumer spending on preventive care. Regulatory convergence through regional trade blocs is gradually easing import procedures, though currency volatility can inflate landed costs for specialty ingredients. In Africa, urbanization and expanding e-commerce infrastructure are opening first-time access to premium vitamins, with Nigeria and Kenya posting double-digit online supplement sales growth in 2024. Collectively, regional disparities in regulation, purchasing power, and health priorities create a diverse tapestry of opportunities that multinational and local players alike must navigate to expand their footprint in the vitamin deficiency treatment market.

Competitive Landscape

The vitamin deficiency treatment market exhibits moderate fragmentation, yet M&A activity is accelerating as conglomerates aim to assemble end-to-end wellness platforms. Nestlé’s USD 1.87 billion integration of The Bountiful Company increases its share of the U.S. VMS aisle while offering data on loyalty-program behaviour to refine cross-selling. Sanofi’s USD 1 billion acquisition of Qunol delivers a high-equity CoQ10 brand, enabling entry into healthy-aging adjacency products. These moves signal a pivot from single-product scale toward ecosystem control spanning research, formulation, digital engagement, and last-mile delivery.

Ingredient manufacturers are following suit: DSM-Firmenich has consolidated upstream vitamin-A and -E capacity, though 2025 outages and geopolitical rifts exposed supply vulnerability, pushing prices upward in Q2. Balchem’s takeover of Kappa Bioscience secures proprietary K2 synthesis pathways and de-risks raw-material sourcing for higher-margin finished products. Start-ups wielding direct-to-consumer genetic tests and telehealth scripts are nibbling share at the fringes, compelling incumbents to accelerate digital investment or pursue bolt-on buys.

Strategic partnerships with telemedicine providers and fitness-tracking apps are becoming commonplace to harness real-time biomarker data for dosage refinement. Blockchain batch-tracking systems now offer ingredient provenance to mitigate counterfeits—a rising issue in global e-commerce. Liposomal and nano-liposome delivery IP has turned into a licensing battleground as firms vie for superior bioavailability claims. Heightened regulator focus on influencer marketing compliance is expected to favour companies with robust scientific communication and transparent testing regimes, potentially squeezing fringe operators out of the vitamin deficiency treatment market.

Vitamin Deficiency Treatment Industry Leaders

Pfizer Inc.

Bayer AG

Koninklijke DSM N.V.

BASF SE

The Bountiful Company (Nature’s Bounty)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Nestlé signalled plans to restructure its vitamins division after sluggish sales despite above-forecast organic growth.

- April 2025: The Vitamin Shoppe introduced a GLP-1 Support range addressing nutrient gaps linked to weight-loss injections.

- February 2025: L Catterton agreed to acquire Thorne HealthTech for USD 680 million, reviving nutraceutical M&A momentum.

Global Vitamin Deficiency Treatment Market Report Scope

| Vitamin A |

| Vitamin B-Complex |

| Vitamin C |

| Vitamin D |

| Multivitamins |

| Oral |

| Parenteral |

| Retail Pharmacies |

| Hospital Pharmacies |

| Online Pharmacies |

| Supermarkets/Hypermarkets |

| Specialty & Wellness Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Vitamin Type | Vitamin A | |

| Vitamin B-Complex | ||

| Vitamin C | ||

| Vitamin D | ||

| Multivitamins | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| By Distribution Channel | Retail Pharmacies | |

| Hospital Pharmacies | ||

| Online Pharmacies | ||

| Supermarkets/Hypermarkets | ||

| Specialty & Wellness Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the vitamin deficiency treatment market in 2025?

The vitamin deficiency treatment market size is USD 6.65 billion in 2025 and is projected to grow to USD 9.56 billion by 2030.

Which vitamin type leads sales?

Vitamin D holds the largest slice at 34.8% of 2024 revenue, driven by widespread deficiency screening and expanded therapeutic uses.

What is driving the fastest channel growth?

Online pharmacies are growing at a 14.3% CAGR thanks to AI-driven product matching, fast delivery, and broader assortment.

Which region is expanding most rapidly?

Asia is set to post a 9.0% CAGR through 2030 on the back of rising incomes and government-backed fortification initiatives.

Are injections gaining ground over pills?

Yes, parenteral formats are forecast to grow at 12.4% CAGR as clinicians turn to injectables for malabsorption and rapid repletion cases.

What regulatory issues should brands watch?

Divergent dosage caps across markets and heightened scrutiny of influencer marketing are key compliance challenges in the next two to four years.

Page last updated on: